📌 Today’s Highlights

Today we cover 62 IR announcements. Notable among them: G-エフ・コード (9211), G-技術承継機構 (319A), G-ヒューマンT (5621). Use the table of contents below to navigate to each company.

- 9211|G-エフ・コード

- 319A|G-技術承継機構

- 5621|G-ヒューマンT

- 4387|G-ZUU

- 1397|SMDAM 225

- 2674|ハードオフ

- 2652|まんだらけ

- 3954|PAXXS

- 1499|MXS高配当70MN

- 1660|MXS高利Jリート

- 3176|三洋貿易

- 9008|京王

- 4579|G-ラクオリア創薬

- 4051|GMO-FG

- 4884|G-クリングル

- 9170|成友興業

- 6104|芝浦機械

- 7616|コロワイド

- 9048|名鉄

- 1847|イチケン

- 267A|P-トワライズ

- 2751|テンポスHD

- 3489|フェイスネットワーク

- 353A|エレコミ

- 4373|シンプレクスHD

- 4464|ソフト99

- 4825|WNIウェザー

- 4882|G-ペルセウス

- 5938|LIXIL

- 6155|高松機械

- 6890|フェローテック

- 7064|ハウテレビジョン

- 7084|G-SmileHD

- 7134|アップガレージG

- 7214|GMB

- 7383|ネットプロHD

- 7729|東精密

- 8153|モスフード

- 8938|G-グロームHD

- 9619|イチネンHD

- 6676|BUFFALO

- 146A|コロンビア・ワークス

- 206A|G-PRISMBio

- 3635|コーエーテクモ

- 399A|上場日経高配当50

- 9381|エーアイテイー

- 3097|物語コーポ

- 3694|オプティム

- 6360|東自機

- 2769|ヴィレッジV

- 398A|P-リアルクオリティ

- 4893|G-ノイルイミューン

- 4896|G-ケイファーマ

- 5572|G-リッジアイ

- 6943|NKK

- 262A|インターメスティック

- 6993|大黒屋

- 6349|小森

- 9913|日邦産業

- 3633|GMOペパボ

- 4019|G-スタメン

- 4591|G-リボミック

9211|G-エフ・コード

1425.0

▼ -1.86%

📎 Source:G-エフ・コード Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-F CODE announced its financial results for the first quarter of the fiscal year ending December 2026.

- For Q1 FY2026, revenue was ¥3.90 billion, an increase of 161.6% year-over-year (YoY).

- Operating profit for the quarter reached ¥785 million, a 138.6% increase YoY.

- Profit attributable to owners of parent was ¥460 million, up 143.7% YoY.

- The company completed 3 M&A transactions in Q1 FY2026 with a total investment of approximately ¥1.4 billion, projected to add approximately ¥600 million to annual operating profit.

- Against the full-year FY2026 forecasts, Q1 progress rates were 26.9% for revenue and 23.8% for operating profit.

🤖 AI Perspective

G-F CODE’s Q1 FY2026 results show substantial growth in both revenue and operating profit compared to the prior year, suggesting a positive impact from its M&A strategy. While revenue progress against full-year targets appears solid, the operating profit progress may be influenced by front-loaded investments in the AI and Technology sectors. The company’s continued focus on M&A, business development, and talent acquisition as part of its growth model could be worth monitoring for future performance.

319A|G-技術承継機構

13280.0

▲ +2.08%

📎 Source:G-技術承継機構 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of the fiscal year ending December 2026, adjusted EBITDA increased by 216.7% year-on-year, and adjusted net income rose by 335.7% year-on-year.

- Key drivers for this strong performance include the robust performance of acquired companies, fueled by demand in areas such as superconductivity for nuclear fusion, semiconductors, and AI data centers, as well as the full-year contribution from seven companies acquired since Q2 FY2025.

- The company expects to achieve its full-year 2026 guidance of 23.0 billion yen in sales, 4.0 billion yen in adjusted EBITDA, and 2.0 billion yen in adjusted net income. This guidance does not include the impact of new acquisitions made in 2026, such as Horikoshi Seiki (acquired in January) and Osaki Dengyosha (acquired in March).

- Regarding the impact of the Bank of Japan’s interest rate hikes and rising raw material costs due to the Middle East situation, the company stated that it continues to secure favorable financing terms from financial institutions and that current issues have not materialized due to the ability to pass on costs to sales prices.

- One year post-listing, the company reports enhanced credibility and brand recognition, leading to an increase in high-profit and high-margin acquisition opportunities, and strengthened recruitment capabilities for its acquired companies.

🤖 AI Perspective

G-Gijutsu Shokei Kiko’s announcement suggests that both organic growth and its M&A strategy are contributing significantly to its financial performance. The substantial year-on-year increases in adjusted EBITDA and adjusted net income are likely key points of interest for investors. The fact that the full-year guidance excludes the impact of new acquisitions made in 2026 could indicate potential for upward revisions in the future.

5621|G-ヒューマンT

1353.0

▼ -13.55%

📎 Source:G-ヒューマンT Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- HumanTechnologies, Inc. (Securities Code: 5621) has released its financial results presentation material for the fiscal year ended March 2026.

- For the fiscal year ended March 2026, consolidated results show net sales of ¥7,496 million (up 23.8% year-on-year), operating profit of ¥1,370 million (up 47.2% year-on-year), ordinary profit of ¥1,383 million (up 48.0% year-on-year), and net profit of ¥1,016 million (up 55.1% year-on-year).

- Both net sales and operating profit exceeded full-year forecasts, with achievement rates of 103.2% and 106.6% respectively.

- KOT SaaS sales reached ¥6,709 million (up 25.1% year-on-year), partly due to a change in the billing system (transition to per-registered-user billing).

- The number of billed IDs increased by 22.8% year-on-year, and the churn rate remained stable at a low level.

- The ratio of personnel expenses to net sales decreased from 37.7% to 34.4%, while the ratio of outsourcing expenses to net sales increased from 15.3% to 17.4%.

4387|G-ZUU

525.0

▼ -2.05%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 2026, G-ZUU Co. reported net sales of ¥2,622 million (down 12.4% year-on-year), an operating loss of ¥345 million, an ordinary loss of ¥67 million, and a net loss attributable to parent company shareholders of ¥398 million.

- The full-year performance deviated significantly from initial guidance, with net sales ¥778 million (22.9%) lower and operating profit ¥445 million below target. Key factors include the loss of a large project in Q1, reduced revenue in the Real Estate/Financial DX and Management Consulting businesses, decreased revenue and profit from ZUU Wealth Management (ZWM), additional large earnout payments for ZWM, and special losses (fund outflow incident, impairment/sale losses on investment securities).

- A ¥96 million fund outflow incident on March 19, 2026, was concluded to be caused by a malicious third party, with no intentional misconduct by company officers or employees. Identified causes include insufficient internal controls for payment approval and disbursement, resource shortages in the accounting department, inadequate internal audit resources, and cyber security vulnerabilities.

- Preventive measures against the fund outflow incident include strengthening internal control systems for payment procedures, improving accounting department resources, enhancing the sharing and timely response to internal audit results, bolstering cybersecurity measures, and reinforcing governance and internal management systems.

- As a management responsibility, Representative Director Kazunari Tomita and Director (Head of Administration) Takuro Higuchi will voluntarily return 30% of their monthly compensation for three months. Furthermore, the Representative Director will directly oversee the accounting and finance domains for the time being, and the company plans to recruit an executive officer or director with expertise in governance, internal control, and financial management.

🤖 AI Perspective

G-ZUU’s fiscal year 2026 results show a significant loss driven by multiple factors, including reduced revenue, a fund outflow incident, and additional earnout payments. The management’s response to the fund outflow and the implementation of preventive measures will be crucial for restoring corporate trust and achieving future performance recovery. Investors may also want to monitor whether the earnout payment is a one-off event or if it signals broader implications for the company’s strategic direction.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

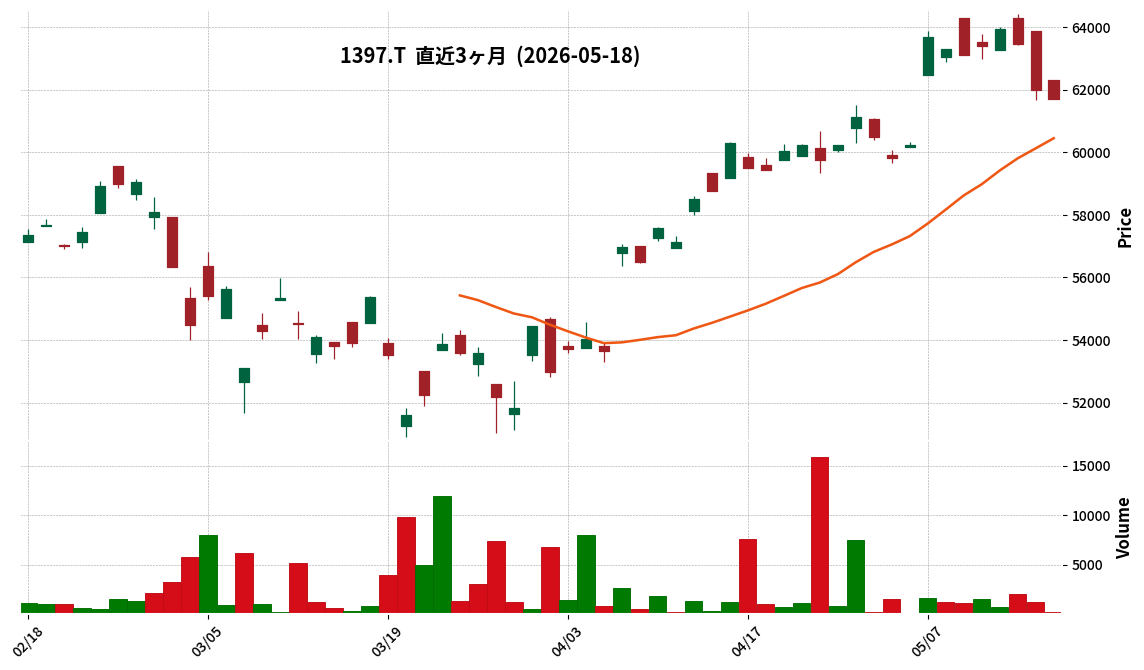

1397|SMDAM 225

61700.0

▼ -0.48%

📎 Source:SMDAM 225 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SMDAM Nikkei 225 ETF (Code: 1397) announced its financial results for the fiscal period ended April 2026 (October 9, 2025, to April 8, 2026).

- As of the end of April 2026, net assets totaled ¥192,041 million (100.0% of total assets), with primary investment assets (equities) accounting for ¥188,131 million (98.0%). This marks an increase compared to the previous period’s (October 2025) net assets of ¥177,897 million.

- The total number of units outstanding at the end of the period was 3,372 thousand units, with the net asset value per unit reported at ¥56,948. This is an increase from ¥48,239 at the end of the previous period.

- The distribution per unit for the April 2026 fiscal period was announced as ¥410. This represents an increase from the ¥360 distribution per unit in the previous period.

- The scheduled submission date for the securities report is July 2, 2026, and the distribution payment commencement date is May 15, 2026.

🤖 AI Perspective

The financial results for SMDAM Nikkei 225 ETF for the April 2026 fiscal period show an increase in net assets and net asset value per unit compared to the previous period, along with a higher distribution per unit. Given that equities constitute the majority of the fund’s primary investment assets, the movements of the Nikkei 225 stock average, its linked index, likely influenced the fund’s performance. These reported figures provide crucial data points for investors evaluating the performance of this ETF.

2674|ハードオフ

2387.0

▼ -0.62%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hard Off Corporation reported consolidated results for the fiscal year ended March 2026, with net sales of 39,276 million JPY (+17.1% year-on-year), operating profit of 3,387 million JPY (+5.3% year-on-year), ordinary profit of 3,489 million JPY (+2.5% year-on-year), and net profit attributable to parent company shareholders of 2,519 million JPY (+8.9% year-on-year).

- Net sales and all profit categories marked record highs for the fourth consecutive fiscal year.

- Domestic existing store sales increased by a robust 4.3%.

- During the fiscal year, 30 new directly managed stores were opened, and the acquisition of ECONOS Co., Ltd. as a consolidated subsidiary resulted in 53 of its stores being transferred from franchised to directly managed, with an additional 16 Book Off stores.

- For the fiscal year ending March 2027, the company forecasts consolidated net sales of 45,700 million JPY (+16.4% year-on-year), operating profit of 4,050 million JPY (+19.6% year-on-year), ordinary profit of 4,100 million JPY (+17.5% year-on-year), and net profit attributable to parent company shareholders of 3,300 million JPY (+31.0% year-on-year).

🤖 AI Perspective

Hard Off’s FY2026 results are notable for the fourth consecutive year of record-high net sales and profits, driven by new store openings and the acquisition of ECONOS. This expansion of the store network appears to have significantly contributed to top-line growth. The FY2027 forecast projects continued revenue and profit increases, with a substantial rise in net profit, partly due to the planned recognition of a gain on the sale of investment securities, which could be seen as an indication of active asset management.

2652|まんだらけ

356.0

▲ +2.89%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Mandarake Inc. announced a partial correction to its “Consolidated Financial Results Briefing for the Second Quarter of the Fiscal Year Ending September 2026 (Non-consolidated).”

- The corrections pertain to the descriptions in “1. Information regarding future forecasts such as consolidated business performance” and “2. Basic policy on selection of accounting standards.”

- Specifically, the statement regarding “Significant changes in parent companies, etc.” was removed from “Qualitative information regarding consolidated business performance forecasts.”

- Additionally, the description concerning the transition to IFRS was removed from “Basic policy on selection of accounting standards.”

- This correction relates to the financial results briefing originally disclosed on May 10, 2024.

🤖 AI Perspective

This correction involves revisions to certain statements regarding future performance forecasts and accounting standards, which ensures the accuracy of information for investors. The removal of statements concerning changes in parent companies within consolidated performance forecasts and the removal of IFRS transition plans could be worth monitoring as they may indicate shifts in future management policy or financial reporting strategy.

3954|PAXXS

3080.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- PAXXS Inc. announced on May 18, 2026, a partial correction to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026,” originally released on May 13, 2026.

- The reason for the correction is stated as an error in the description within the financial results.

- The specific correction is located on page 2 of the attached document, within “1. Overview of Business Results (1) Overview of Business Results for the Current Period,” concerning the performance of consolidated subsidiaries.

- Specifically, the description for the consolidated subsidiary “Nesco Co., Ltd.” was amended from “Transactions with key customers were strong, resulting in increased revenue and profit.” to “Transactions with key customers slightly decreased, resulting in decreased revenue but increased profit.”

- No corrections were made to the numerical data (XBRL data).

🤖 AI Perspective

This correction primarily addresses a textual description regarding the business performance of a specific consolidated subsidiary, Nesco Co., Ltd., without altering any numerical data. Investors may view this as an indication of the company’s commitment to transparency and accuracy in its disclosures. While it does not appear to significantly impact the overall financial performance, the rationale behind the nuanced change in phrasing for Nesco’s performance might be worth monitoring for any future clarifications from the company.

1499|MXS高配当70MN

9077.0

▼ -0.03%

📎 Source:MXS高配当70MN Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- MAXIS Japan High Dividend 70 Market Neutral ETF (Code: 1499) has announced its financial results for the fiscal year ended April 2026 (October 11, 2025 – April 10, 2026).

- Net assets at the end of the current period totaled ¥6,414 million, a decrease from ¥8,144 million at the end of the previous period (October 2025).

- The net asset value per unit at the end of the current period was ¥9,297, showing an increase compared to ¥8,852 at the end of the previous period.

- The distribution per unit for the current period (April 2026) was announced as ¥134, which is a decrease from ¥144 in the previous period (October 2025).

- The number of outstanding units at the end of the current period was 690 thousand units, a decrease from 920 thousand units at the end of the previous period.

🤖 AI Perspective

For the MAXIS Japan High Dividend 70 Market Neutral ETF, the April 2026 fiscal year results show a decrease in total net assets and outstanding units, while the net asset value per unit increased. This could suggest a combined impact of unit reductions and changes in the valuation of investment assets. The decrease in distribution per unit from the previous period may be a point for investors to monitor regarding future distribution policies and operational performance.

1660|MXS高利Jリート

10675.0

▼ -1.16%

📎 Source:MXS高利Jリート Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- MAXIS High-Yield J-REIT (Fund Name: MAXIS高利回りJリート上場投信, Code: 1660) announced its Q4 FY2026 financial results on May 18, 2026.

- Net assets for the period ended April 10, 2026, totaled ¥62,383 million, up from ¥55,367 million in the previous period.

- The primary investment asset accounted for ¥60,968 million (97.7% of total assets), while cash, deposits, and other assets (net of liabilities) amounted to ¥1,414 million (2.3%).

- The number of outstanding units at the end of the current period increased to 5,594 thousand from 4,962 thousand at the end of the previous period.

- The net asset value per unit was reported as ¥11,151 (down from ¥11,158), and the distribution per unit was ¥269 (up from ¥221).

🤖 AI Perspective

This earnings report indicates an expansion in the fund’s size, with increases in both net assets and outstanding units for MAXIS High-Yield J-REIT. While the net asset value per unit experienced a slight decrease, the increase in distribution per unit could be a key factor for investors. The asset allocation remains heavily concentrated in primary investment assets, reflecting a continued focus on J-REITs.

3176|三洋貿易

1564.0

▼ -1.39%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sanyo Trading Co., Ltd. announced its consolidated financial results for the second quarter of the fiscal year ending September 2026.

- For the first half, net sales reached 70,258 million yen (up 3.1% year-on-year), and operating income was 4,466 million yen (up 8.8% year-on-year).

- Net income attributable to owners of parent was 3,657 million yen (up 5.9% year-on-year).

- The achievement rate against the initial full-year forecast for the first half was 72.0% for operating income and 89.2% for net income.

- Based on these first-half results, the company revised its full-year earnings forecast for the fiscal year ending September 2026 upwards.

- By segment, Fine Chemicals, Industrial Products, and Life Science each accounted for approximately 30% of total sales.

- The Life Science segment recorded net sales of 21,008 million yen (up 4.9% year-on-year) and operating income of 1,186 million yen (up 17.7% year-on-year), showing increases in both revenue and profit.

🤖 AI Perspective

Sanyo Trading’s first-half results show positive growth in both revenue and profit, which may be attributed to an increase in gross profit and controlled selling, general, and administrative expenses. The upward revision of the full-year forecast could indicate the company’s confidence in its business momentum and future prospects. Strong overseas sales, particularly in North America and ASEAN regions, suggest the effectiveness of its global expansion strategy.

9008|京王

765.1

▼ -1.34%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Keio’s FY2025 financial results show operating revenue of ¥496.9 billion (+¥44.0 billion year-on-year), setting a new record high.

- Net income attributable to owners of the parent for FY2025 reached a record high of ¥42.9 billion, partly due to the sale of policy-held shares.

- The annual dividend for FY2025 is projected at ¥110.0 per share, an increase of ¥10.0 year-on-year.

- For FY2026, the company forecasts record operating revenue of ¥504.0 billion (+¥7.0 billion year-on-year).

- The annual dividend for FY2026 is projected at ¥22.0 per share (¥110.0 equivalent pre-stock split).

🤖 AI Perspective

Keio’s FY2025 results indicate broad-based revenue growth across all segments, with real estate sales and high-value hotel offerings appearing to be key drivers of the record operating revenue. While operating profit decreased due to increased railway safety investments, the sale of strategic shareholdings significantly boosted net income. The FY2026 outlook suggests continued revenue growth, though increased depreciation from hotel renovations and the recording of asset retirement obligations related to Shinjuku redevelopment could impact operating profit.

4579|G-ラクオリア創薬

620.0

▼ -13.17%

📎 Source:G-ラクオリア創薬 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-RaQualia Pharma announced a correction to its “Q1 FY2026 Earnings Presentation” released on May 15, 2026, changing the fiscal period on the cover from “18th Fiscal Year” to “19th Fiscal Year.”

- For the first quarter of FY2026, consolidated business revenue decreased by 16.9% year-on-year to 801 million yen, with an operating loss of 160 million yen, an ordinary loss of 158 million yen, and a net loss attributable to parent company shareholders of 225 million yen.

- The Q1 business revenue of 801 million yen represents a 20.2% progress rate against the full-year plan of 3,980 million yen.

- The company stated that the primary reason for the year-on-year decline in Q1 performance was the absence of milestone and upfront payments, which is in line with the initial plan.

- The consolidated balance sheet shows an improved equity ratio of 70.5%, a 5.4 percentage point increase from the end of the previous fiscal year, and cash and cash equivalents increased by 1,250 million yen (38.5%) to 4,494 million yen.

🤖 AI Perspective

This IR addresses a minor correction in the earnings presentation while providing a comprehensive overview of the financial performance and business activities for the first quarter of FY2026. Although business revenue saw a year-on-year decrease, the progress against the full-year plan remains at over 20%, suggesting that the variability in “other income” impacts overall performance. The improvement in the equity ratio and the increase in cash and cash equivalents could indicate a strengthening of the company’s financial foundation.

4051|GMO-FG

5460.0

▼ -1.97%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- GMO Financial Gate (GMO-FG) held its Q2 FY2026 earnings presentation.

- For the first half (1H) of FY2026, total revenue reached JPY 10.515 billion (+16.2% YoY) and operating profit was JPY 1.559 billion (+12.8% YoY), representing 53.3% and 55.7% of the full-year plan, respectively.

- Recurring revenue increased to JPY 5.228 billion (+29.9% YoY), raising its share of total revenue to 49.7%.

- The number of payment processing transactions grew to 630 million (+33.3% YoY), and active IDs increased to 456,000 (+45,000 IDs YoY).

- Multiple projects for major commercial facilities have successfully commenced operations, with full-scale deployment continuing towards Q3.

🤖 AI Perspective

GMO-FG’s Q2 earnings presentation highlights strong financial performance, with both revenue and operating profit advancing ahead of their full-year targets. The significant growth in recurring revenue suggests a strengthening of the company’s stable revenue base. The successful launch of projects for major commercial facilities could further accelerate the expansion of its ecosystem and revenue growth in the coming quarters.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

4884|G-クリングル

429.0

▼ -2.50%

📎 Source:G-クリングル Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For acute spinal cord injury (domestic), face-to-face consultation with PMDA has concluded, agreeing on the protocol outline for additional clinical trials.

- The clinical trial notification for the additional trial is expected to be submitted within several months, with the aim to commence trials by the end of the current fiscal year.

- In the US, preparations are underway for an IND application targeting acute spinal cord injury, with efforts to secure subsidies from US government/public institutions and strengthen partnering activities for funding.

- Phase III clinical trials for vocal fold scarring completed patient enrollment in January 2024, with results expected in 2027. Partnering negotiations are ongoing with multiple pharmaceutical companies, aiming for results announcement within the year.

- A joint patent with Keio University for a chronic spinal cord injury treatment has been secured, but development for this indication will be pursued as a mid-to-long-term growth opportunity, accumulating basic and non-clinical research data.

🤖 AI Perspective

G-Cringle provided updates on the progress of domestic additional clinical trials for its acute spinal cord injury treatment and preparations for US development. The indication of potential partnering progress for vocal fold scarring within the year could be a significant development for the company’s future business. The overall financial situation and ongoing collaborations are worth monitoring for their impact on the company’s long-term value.

9170|成友興業

—

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Seiyu Kogyo resolved a stock split, amendment to its Articles of Incorporation, and a revised dividend forecast (increase) at a Board of Directors meeting on May 18, 2026.

- The stock split will be conducted at a ratio of 3 shares for every 1 common share, with a record date of June 30, 2026, and an effective date of July 1, 2026.

- Post-split, the total number of issued shares will be 8,463,759, and the total number of authorized shares will be 30,146,400.

- The per-share dividend forecast for the September 2026 fiscal year has been revised to ¥14.00 (equivalent to ¥42.00 on a pre-split basis), representing an effective increase of ¥2.00 from the previous forecast of ¥40.00.

- The Articles of Incorporation will be amended to change the total number of authorized shares from the current 10,048,800 to 30,146,400, in conjunction with the stock split.

🤖 AI Perspective

The stock split aims to reduce the investment unit, potentially making the company’s shares more accessible to a broader range of investors and enhancing market liquidity. The simultaneous announcement of an effective dividend increase may be seen as a positive signal regarding the company’s commitment to shareholder returns. These actions could potentially contribute to increased investor interest in Seiyu Kogyo’s shares.

6104|芝浦機械

4920.0

▲ +0.10%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Shibaura Machine announced on May 18, 2026, a further postponement of its financial results announcement for the fiscal year ending March 2026.

- The announcement was initially scheduled for May 12, 2026, then postponed to May 18, 2026, and is now re-postponed.

- The reason for the re-postponement is that the valuation of goodwill and assets related to SHIBAURA MACHINE LWB GmbH, acquired on November 28, 2025, is taking longer than anticipated.

- The new scheduled date for the financial results announcement is May 25, 2026.

🤖 AI Perspective

The extended time required for the valuation of SHIBAURA MACHINE LWB GmbH’s assets and goodwill appears to be the primary cause for this second postponement. Repeated delays in financial reporting can impact investor sentiment and the timely dissemination of financial information. Investors may monitor the eventual announcement for details regarding the acquisition’s financial impact.

7616|コロワイド

1857.5

▼ -0.43%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kolowide Co., Ltd. announced a partial correction to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 [IFRS]” initially released on May 8, 2026.

- The reason for the correction is stated as an error in the calculation process of EBITDA, necessitating revisions to EBITDA and related indicators.

- The revised consolidated EBITDA for the fiscal year ended March 31, 2026, is ¥22,538 million, an increase of 21.9% from the previous year, corrected from the prior ¥20,988 million.

- The consolidated EBITDA forecast for the fiscal year ending March 31, 2027, remains at ¥27,748 million, but its year-on-year growth rate was corrected from “32.2% increase” to “23.1% increase.”

- In the “Trend of Major Management Indicators,” the EBITDA ratio for the fiscal year ended March 31, 2026, was corrected from 7.0% to 7.5%, and the Net Debt/EBITDA ratio was corrected from 3.9 times to 3.7 times.

🤖 AI Perspective

This correction stems from an error in EBITDA calculation, impacting previously announced figures and future earnings forecasts for EBITDA-related metrics. As EBITDA is a key indicator of a company’s cash flow generation, investors may find it important to review these revised figures. Changes to financial health indicators like the EBITDA ratio and Net Debt/EBITDA ratio could also be worth monitoring, as these adjustments might influence how the company’s financial standing is perceived.

9048|名鉄

1889.0

▲ +3.93%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nagoya Railroad Co.,Ltd. (Meitetsu) has released its Investor Presentation for the fiscal year ended March 2026.

- The company plans to announce the direction for the review and revision of the Nagoya Station Area Redevelopment Plan by FY2026. This review will consider feasibility and financial soundness, aiming to reduce investment scale, and will also explore the introduction of new external partners.

- To improve capital efficiency, Meitetsu plans to monetize assets (including real estate sales) totaling ¥130 billion and sell strategic shareholdings amounting to ¥60 billion (based on market value as of March 31, 2026) between FY2024 and FY2030.

- The business portfolio will be reorganized by establishing a new “Aviation, Information & Technology Service Business” segment, reducing the total segments from seven to five. The company has also decided to withdraw from the low-profit forwarding business (external sale of Meitetsu World Transport Co., Ltd.).

- Meitetsu has enhanced its shareholder return policy, introducing a minimum annual dividend per share of ¥60, while maintaining a consolidated dividend payout ratio of 30% or more, effective from FY2026.

🤖 AI Perspective

The revision of the Nagoya Station area redevelopment plan, with a focus on reducing investment scale, may suggest a strategic shift towards financial prudence. The acceleration of asset monetization and business portfolio restructuring indicates a proactive approach to enhancing capital efficiency and improving profitability. Furthermore, the introduction of a minimum dividend per share could signal increased commitment to stable shareholder returns, which might be viewed favorably by investors seeking consistency.

1847|イチケン

2538.0

▼ -0.55%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Ichiken’s consolidated financial results for the fiscal year ended March 2026 show net sales of ¥106,176 million, a 7.2% increase compared to the previous year.

- Operating profit reached ¥9,033 million, a 32.2% increase year-on-year, and ordinary profit was ¥8,954 million, up 32.3% year-on-year.

- Net income attributable to owners of parent was ¥6,408 million, marking a 36.9% increase from the previous fiscal year.

- Earnings per share (EPS) for the period were ¥441.40, an increase from ¥322.34 in the prior fiscal year.

- For the fiscal year ending March 2027, the consolidated earnings forecast projects net sales of ¥108,000 million (up 1.7% YoY), operating profit of ¥8,500 million (down 5.9% YoY), ordinary profit of ¥8,400 million (down 6.2% YoY), and net income attributable to owners of parent of ¥5,600 million (down 12.6% YoY).

🤖 AI Perspective

The fiscal year March 2026 results demonstrated strong growth across sales and all profit metrics, with operating and ordinary profits increasing by over 30%. This may suggest improved operational efficiency or favorable market conditions during the period. However, the forecast for fiscal year March 2027 anticipates a decline in profits, which could indicate the company’s cautious outlook on future business conditions or potential cost pressures.

267A|P-トワライズ

1989.0

▲ +0.00%

📎 Source:P-トワライズ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- P-Towalize Co., Ltd. resolved at its Board of Directors meeting on May 18, 2026, to absorb and merge its consolidated subsidiary, FC Partners Co., Ltd., with an effective date of August 1, 2026.

- The merger will be an absorption-type merger, with P-Towalize Co., Ltd. as the surviving company and FC Partners Co., Ltd. as the absorbed company, which will be dissolved.

- Since FC Partners Co., Ltd. is a wholly-owned subsidiary of P-Towalize Co., Ltd., no shares or other consideration will be allotted or delivered in connection with this merger.

- This merger qualifies as a simplified merger for P-Towalize under Article 796, Paragraph 2 of the Companies Act, and a short-form merger for FC Partners under Article 784, Paragraph 1 of the Companies Act, thus requiring no shareholder approval from either company.

- The purpose of this merger is to consolidate management resources with FC Partners, which primarily engages in payment consulting and collection agency services, and to enhance overall group management efficiency.

🤖 AI Perspective

This merger indicates P-Towalize’s intention to consolidate management resources and enhance efficiency within the group by absorbing FC Partners, a wholly-owned subsidiary acquired in 2020. The simplified and short-form merger process, applicable to wholly-owned subsidiaries, suggests a streamlined execution of the integration. While the impact on consolidated performance is stated to be minor, the long-term synergistic effects resulting from this business reorganization could be a focal point for investors to monitor.

2751|テンポスHD

3515.0

▼ -0.57%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- TENPOS Holdings Co., Ltd. decided on May 18, 2026, to subscribe to a third-party allotment of shares by Marche Corporation.

- Following this subscription, TENPOS Holdings is expected to acquire 50.59% of Marche’s outstanding shares, making Marche a consolidated subsidiary.

- Prior to this acquisition, TENPOS Holdings held 21.02% of Marche’s voting rights (2,106,300 shares).

- The number of shares acquired through this third-party allotment is 6,000,000 shares, with an acquisition price of 986,000,000 JPY. The total estimated cost, including issuance expenses, is 996,000,000 JPY.

- After the transaction, TENPOS Holdings’ ownership will be 8,106,300 shares, representing 50.59% of voting rights.

- The payment due date is scheduled for June 29, 2026.

🤖 AI Perspective

TENPOS Holdings has been strengthening its relationship with Marche, an izakaya-focused restaurant operator, as part of its strategy to be a comprehensive producer in the restaurant industry. This consolidation is stated to accelerate support for Marche’s franchise business restructuring and growth strategies, with an aim to achieve TENPOS Holdings’ ¥50 billion F&B group sales target sooner. The increased capital tie-up suggests potential for enhanced synergies and operational integration between the two entities, which could be worth monitoring for future financial performance.

3489|フェイスネットワーク

752.0

▲ +8.51%

📎 Source:フェイスネットワーク Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- FaithNetwork Co., Ltd. announced that its consolidated financial results for the fiscal year ended March 2026 set new records for net sales, operating income, ordinary income, and net income attributable to owners of the parent.

- Consolidated net sales amounted to ¥32,916 million, marking a 10.0% increase year-on-year, while consolidated ordinary income reached ¥5,165 million, a 25.8% increase year-on-year.

- The gross profit margin improved to 26.9%, with a total gross profit of ¥8,854 million.

- The company forecasts a dividend per share of ¥42.5 for FY2026, representing an increase of ¥9.7 from the previous year, projecting a sixth consecutive year of dividend increases.

- The primary factor contributing to the increase in profit was the rise in gross profit from the real estate investment support business, while increased personnel expenses and advertising costs contributed to higher selling, general, and administrative expenses.

🤖 AI Perspective

FaithNetwork’s strong FY2026 results, with record-high sales and profits, coupled with a projected sixth consecutive dividend increase, indicate robust operational performance. The significant improvement in the gross profit margin may suggest the effectiveness of the company’s strategies to enhance property value and its integrated business model. Investors might view these results as a positive sign of sustained profitability and shareholder return, making the company’s future growth trajectory worth monitoring.

353A|エレコミ

—

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Elevator Communications Co., Ltd. announced “Change in Timing of Commemorative Shareholder Benefit Gift” on May 18, 2026.

- The previous gift timing was “enclosed with the resolution notice after the close of the Company’s Ordinary General Meeting of Shareholders.”

- The revised gift timing will be “enclosed with the convocation notice for the Company’s Ordinary General Meeting of Shareholders.”

- This change aims to allow shareholders to utilize the “digital gift” shareholder benefit earlier.

- There are no changes to the eligible shareholders, benefit items, gift amount, record date, receipt method, or other contents of the benefit.

🤖 AI Perspective

This announcement suggests Elevator Communications is prioritizing shareholder convenience by accelerating the delivery of its commemorative shareholder benefits. The earlier access to digital gifts, now included with the convocation notice, could be viewed as a positive step in enhancing shareholder relations and engagement. Investors might consider this a minor but favorable adjustment to the company’s shareholder return policy.

4373|シンプレクスHD

950.0

▼ -0.11%

📎 Source:シンプレクスHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Simplex Holdings Inc. resolved to introduce a shareholder benefit program at its Board of Directors meeting held today, May 18, 2026.

- The initial eligible shareholders are those registered in the company’s shareholder registry as of September 30, 2026, holding 600 or more shares. This eligibility criteria is expected to apply annually thereafter.

- The shareholder benefit will consist of points for the “Premium Shareholder Benefits Club” platform provided by Wills Co., Ltd. One point is equivalent to approximately one yen, redeemable for various products such as food, electronics, and experience gifts.

- The number of points awarded varies by shareholding: 3,000 points for 600-899 shares, 4,000 points for 900-1,299 shares, 5,000 points for 1,300-1,499 shares, and 25,000 points for 1,500 or more shares.

- Shareholder benefit points will be granted annually around mid-November, with an exchange period from mid-November to the end of February of the following year. Exchange for Amazon Gift Cards is also available, with the company bearing the conversion fees.

🤖 AI Perspective

Simplex Holdings’ introduction of a shareholder benefit program appears to be aimed at increasing recognition of its shares in the capital market and expanding its investor base to enhance liquidity. The use of the “Premium Shareholder Benefits Club” platform specifically suggests an intention to create new points of contact and strengthen ongoing communication with individual investors. The minimum holding requirement of 600 shares may be a notable factor for some investors.

4464|ソフト99

3845.0

▼ -1.91%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Soft99 Corporation announced a “Correction (Correction of Numerical Data) to a Part of the ‘Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 [Japanese GAAP]'” on May 18, 2026.

- This correction pertains to the content of the “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 [Japanese GAAP]” disclosed on May 14, 2026.

- The reason for the correction was the discovery of an error in the stated dividend payment commencement date after the initial disclosure.

- The corrected section is “【Dividend Payment Commencement Date】” on page 1 of the summary information.

- The dividend payment commencement date was corrected from “June 30, 2026” to “June 29, 2026.”

🤖 AI Perspective

This correction is limited to a change in the dividend payment commencement date and is not considered to directly impact the company’s performance or financial condition. For investors, the primary point of attention would be the slight acceleration of the dividend receipt timeline by one day. Such corrections are generally viewed as part of a company’s efforts to ensure the accuracy of its information disclosure.

4825|WNIウェザー

2056.0

▼ -1.63%

📎 Source:WNIウェザー Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Weathernews Inc. resolved to revise its year-end dividend forecast for the 40th fiscal year at a Board of Directors meeting held on May 18, 2026.

- The previous year-end dividend forecast per share was ¥57.50 (¥22.50 ordinary dividend, ¥35.00 commemorative dividend).

- The revised forecast increases the year-end dividend per share to ¥62.50 (¥22.50 ordinary dividend, ¥40.00 commemorative dividend).

- The revision is attributed to the company’s policy of implementing a 40th-anniversary commemorative dividend, alongside an upward revision in the consolidated earnings forecast for the current 40th fiscal year.

- The company maintains a policy to pay out dividends, including ordinary and commemorative dividends, targeting a consolidated dividend payout ratio of 100%.

🤖 AI Perspective

This upward revision of the dividend forecast appears to stem from an improved consolidated earnings outlook, signaling a commitment to shareholder returns. The stated policy of targeting a 100% consolidated dividend payout ratio, inclusive of ordinary and commemorative dividends for its 40th anniversary, may be a significant factor for investors. The continued alignment of the company’s performance with this dividend policy will likely be a key area for investors to monitor.

4882|G-ペルセウス

174.0

▼ -3.33%

📎 Source:G-ペルセウス Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Revenue for the fiscal year ended March 2026 was ¥135 million, representing approximately a 12.6% increase year-over-year.

- Operating loss was ¥744 million, and net loss was ¥718 million.

- The investigator-initiated trial period for the lead pipeline PPMX-T003 in aggressive NK-cell leukemia has been extended until March 31, 2027, with Osaka University Hospital newly participating as a clinical trial site.

- The PPMX-T003 investigator-initiated trial was selected for AMED’s Program for Promoting Research and Development of Innovative Drugs for Rare Diseases, securing a ¥100 million grant for trial expenses in FY2026.

- Non-GLP toxicity studies for PPMX-T004 are progressing as planned and are expected to conclude in September 2026.

- G-Perseus issued the 29th series of share options to Macquarie Bank Limited, with a potential maximum fundraising of ¥930,380,800.

🤖 AI Perspective

G-Perseus’s financial results for FY2026/3 indicate continued investment in research and development, despite an increase in revenue. The extension of the PPMX-T003 clinical trial period and the significant grant from AMED could be seen as positive developments, providing both financial support and external validation for its key pipeline. Furthermore, the issuance of new share options is expected to provide essential capital for future R&D initiatives.

5938|LIXIL

1634.0

▼ -2.30%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- LIXIL Corporation announced a partial correction to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 [IFRS]” on May 18, 2026.

- The corrections relate to the non-consolidated financial results and do not affect the consolidated financial statements.

- The reasons for the corrections include a review of the valuation of receivables from some consolidated subsidiaries and a revision of the application of deferred tax accounting under Japanese standards.

- For individual operating results, ordinary profit for the fiscal year ended March 31, 2026, was revised from ¥20,163 million to ¥19,567 million, and net profit was revised from ¥19,492 million to ¥17,584 million.

- For individual financial position, total assets were revised from ¥1,150,038 million to ¥1,148,130 million, net assets from ¥395,644 million to ¥393,736 million, equity ratio from 34.4% to 34.3%, and basic earnings per share from ¥1,376.42 to ¥1,369.79 for the fiscal year ended March 31, 2026.

🤖 AI Perspective

While the corrections do not impact the consolidated financial statements, the revisions to LIXIL’s non-consolidated profit figures and financial position are noteworthy for evaluating the company’s standalone financial health. Specifically, the adjustments to ordinary profit, net profit, and earnings per share could influence perceptions of the company’s individual earning power. Investors may wish to monitor how these corrections are perceived in relation to overall company valuation and future disclosures.

6155|高松機械

483.0

▲ +0.62%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Takamaz Machine Tools Corp. announced a partial correction to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 [Japanese GAAP]” initially released on May 8, 2026.

- The correction was necessitated by an error in the individual financial statements where “prepaid pension expense” should have been recorded for a defined benefit pension plan with assets exceeding liabilities, but was incorrectly accounted for as “provision for retirement benefits.”

- This error led to inaccuracies in “deferred tax liabilities,” “income taxes — adjustments,” and “accumulated adjustments for retirement benefits” due to tax effect accounting.

- Importantly, the consolidated financial statements were not affected by this error, with no changes to the amounts of “retirement benefit assets” and “retirement benefit liabilities.”

- The corrections involve multiple items, including the summary information, and a fully revised document has been re-submitted.

🤖 AI Perspective

This correction primarily concerns an accounting error in the individual financial statements, with no impact on the consolidated financial figures, which may be a key point for investors to consider. While such amendments highlight a commitment to accurate financial reporting, they could also draw attention to the effectiveness of internal control processes. Investors may want to monitor future disclosures for consistency and accuracy.

6890|フェローテック

9200.0

▼ -2.75%

📎 Source:フェローテック Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Ferrotec Corporation announced on May 18, 2026, a correction to certain errors in its “Financial Results Briefing Material and Mid-Term Management Plan (Rolling Plan) Material,” originally disclosed on May 15, 2026.

- The reason for the correction was identified as a transcription error in accounting figures.

- The primary target value corrected was the Net Profit for the fiscal year ending December 2027, which was revised from ¥30,000 million (pre-correction) to ¥29,000 million (post-correction).

- Other key target values, including sales revenue, operating profit, operating profit margin, and capital expenditure, remained unchanged.

- The corrected materials include highlights of the changes using yellow markers.

🤖 AI Perspective

This correction to the net profit target in Ferrotec’s mid-term management plan is attributed to a transcription error, suggesting it does not reflect changes in business strategy or market conditions. Investors may consider this an administrative adjustment rather than a fundamental shift in company outlook. It could be worth monitoring the company’s progress against other unchanged key performance indicators, such as sales and operating profit targets, as well as the broader strategic initiatives outlined in the mid-term plan.

7064|ハウテレビジョン

791.0

▼ -6.72%

📎 Source:ハウテレビジョン Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Howtelevision Co., Ltd. resolved at its Board of Directors meeting on May 18, 2026, to absorb its consolidated subsidiary, Loglio Co., Ltd.

- The effective date of the merger is scheduled for July 1, 2026.

- The purpose of the merger is to accelerate integrated business development with Loglio (which became a subsidiary on April 1, 2024), achieve further business growth, and streamline group management.

- The merger method will be an absorption-type merger with Howtelevision as the surviving company and Loglio dissolving.

- As Loglio is a wholly-owned subsidiary of Howtelevision, the merger will be conducted without consideration.

- There will be no changes to Howtelevision’s name, location, representative, business content, capital, or fiscal year due to this merger.

- Howtelevision announced that the impact of this merger on its consolidated financial results is minor.

🤖 AI Perspective

This merger represents an internal reorganization targeting an existing consolidated subsidiary, aiming to strengthen business collaboration within the group and enhance management efficiency. It could be seen as a move towards more integrated business operations approximately two years after Loglio became a subsidiary. While the announced impact on consolidated performance is expected to be minor, the future progression of business synergies warrants monitoring.

7084|G-SmileHD

2698.0

▼ -5.40%

📎 Source:G-SmileHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-SmileHD announced its consolidated financial results for the fiscal year ended March 2026.

- Net sales reached ¥14,517 million (+6.3% year-on-year), EBITDA was ¥1,108 million (-5.4%), operating income ¥370 million (-9.9%), ordinary income ¥350 million (-15.1%), and net income attributable to owners of parent ¥220 million (+45.6%).

- Excluding one-time expenses of ¥352 million related to the acquisition of WITH Holdings Co., Ltd. shares, operating income would have been ¥664 million (+61.8%), ordinary income ¥703 million (+70.1%), and net income attributable to owners of parent ¥464 million (+206.3%).

- The annual dividend for the fiscal year ended March 2026 is ¥95.00 per share (¥47.50 for the year-end dividend). The forecast for the fiscal year ending March 2027 is also ¥95.00 per share.

- The consolidated earnings forecast for the fiscal year ending March 2027 is currently undecided due to the integration of WITH Holdings Co., Ltd.

🤖 AI Perspective

G-SmileHD’s FY2026/3 consolidated results show a sales increase, but one-time M&A related expenses impacted operating and ordinary income. Excluding these expenses, a significant profit increase was achieved, suggesting underlying business strength. The impact of business expansion under the new medium-term management plan, especially after the consolidation of WITH Holdings, will be a key point of interest once the FY2027/3 earnings forecast is announced.

7134|アップガレージG

1151.0

▼ -0.95%

📎 Source:アップガレージG Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ending March 2026, results exceeded revised plans due to increased winter tire demand and subsequent shift to summer tires in Q4 (Jan-Mar), and expanded sales of supplies to business partners in the wholesale segment.

- FC royalty rates were raised from 3% to 3.8% of sales from the second half of the previous fiscal year, intended to fund new chain-wide initiatives and maintain/improve store quality, not solely for head office profit expansion.

- The company reports no direct and significant impact from the Middle East situation at present, expecting increased demand for reuse products amid rising prices, while monitoring potential impacts on new product procurement for the wholesale business.

- Human capital investment expansion led to a 9.2% increase in personnel costs for FY2026/3, largely as expected. For the current fiscal year, the company plans to maintain the selling, general, and administrative (SG&A) expense ratio to sales in the low 30% range through overall cost control.

- Both US stores are performing well in sales and procurement, with the second store in Ontario achieving monthly profitability since February, and plans to open one more store in California during FY2026.

🤖 AI Perspective

This IR update suggests UP GARAGE GROUP is actively adapting to market conditions while pursuing its growth strategies. The proactive domestic store expansion and successful trajectory in the US market could serve as key drivers for future business expansion. Furthermore, the increase in FC royalty and the planned control of the SG&A ratio may indicate management’s focus on maintaining and enhancing profitability.

7214|GMB

985.0

▲ +4.23%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- GMB Corporation announced its consolidated financial results for the fiscal year ended March 31, 2026. Revenue was ¥105,280 million, representing a 1.5% increase from the previous year.

- Operating profit reached ¥3,320 million (up 70.9% year-on-year), and ordinary profit was ¥2,948 million (up 66.8% year-on-year).

- Net income attributable to owners of parent resulted in a loss of ¥1,035 million (compared to a profit of ¥592 million in the previous year).

- Diluted earnings per share for the fiscal year ended March 31, 2026, was △194.60 yen.

- The consolidated earnings forecast for the fiscal year ending March 31, 2027, projects revenue of ¥115,300 million (up 9.5% year-on-year), operating profit of ¥3,600 million (up 8.4% year-on-year), and net income of ¥1,000 million.

🤖 AI Perspective

GMB’s FY2026/3 results show a modest increase in revenue, while operating and ordinary profits significantly improved, partly due to reduced retirement benefit expenses in Korea and foreign exchange gains on foreign currency-denominated assets. However, the recognition of an impairment loss on fixed assets of ¥1,947 million at a subsidiary as an extraordinary loss led to a net loss for the period. The company’s forecast for FY2027/3, anticipating increased revenue and operating profit, along with a return to net profit, may be a key point for investors to monitor.

7383|ネットプロHD

408.0

▼ -6.64%

📎 Source:ネットプロHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- The Q&A transcript from Net Protections Holdings’ FY2026 full-year earnings briefing held on May 15, 2026, was released on May 18, 2026.

- The company stated that the financial impact of the litigation has not yet been incorporated into the current forecasts.

- Regarding atone’s merchant acquisition strategy, the company prioritizes acquiring clients through partnerships with PSPs and carts over opening atone to existing NP Atobarai merchants.

- The 3-year business plan includes the effects of partnerships with credit card companies as a factor accelerating GMV growth.

- The acceleration in B2C (NP Atobarai) GMV growth is attributed to the accelerated growth of NP Atobarai air and AFTEE, in addition to the strong performance of NP Atobarai itself.

- CEO Shibata expressed increased confidence in achieving the 3-year business plan due to current strong project acquisition and robust sales systems across all businesses.

🤖 AI Perspective

This Q&A session highlights Net Protections HD’s confidence in its current business environment and strategic direction. Key points for investors include the current non-inclusion of litigation financial impacts in forecasts, the strategic shift in atone’s growth approach, and the robust outlook for the NP Atobarai business, all of which could influence future performance. The incorporation of partnership effects with credit card companies into the 3-year plan also suggests potential future growth drivers worth monitoring.

7729|東精密

16395.0

▼ -0.73%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- TOKYO SEIMITSU announced on May 18, 2026, a partial correction to its “FY2025 (March 2026) Financial Results Presentation” and “FY2025 (March 2026) Financial Results Presentation (with notes).”

- The reason for the correction is the discovery of errors in certain parts of the materials disclosed on May 13, 2026.

- The corrections relate to the “Balance Sheet” sections found on “page 7” and “page 31” of both presentation documents.

- The corrected portions are indicated with underlines in the updated documents, showing a comparison between the original and revised figures.

🤖 AI Perspective

Corrections to disclosed financial documents, such as those for financial results presentations, are important for investors to ensure they are basing decisions on accurate information. Financial presentation materials are key resources for understanding a company’s financial health and outlook, so any corrections warrant careful review. Investors should specifically examine the changes made to the balance sheet items to understand their potential implications, as detailed accuracy is crucial for financial analysis.

8153|モスフード

3675.0

▼ -5.53%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- MOS FOOD SERVICES, Inc. absorbed its wholly-owned subsidiary, MOS CREDIT Co., Ltd., with an effective date of April 1, 2026.

- Following this merger, a gain on extinguishment of treasury stock totaling ¥1,820 million will be recognized as an extraordinary gain in the non-consolidated financial statements for the fiscal year ending March 2027.

- This gain arises from the difference between the net assets received from the merged company (MOS CREDIT) and the book value of the shares held by MOS FOOD SERVICES on the effective date of the merger.

- This gain on extinguishment of treasury stock will be eliminated in the consolidated accounts and therefore will have no impact on the consolidated financial statements.

🤖 AI Perspective

This announcement indicates an extraordinary gain recorded at the non-consolidated level for MOS FOOD SERVICES. As this gain results from an internal transaction involving a wholly-owned subsidiary’s absorption merger, it is stated to have no impact on the consolidated financial results. Investors may find it important to distinguish between the non-consolidated gain and its non-effect on consolidated performance when evaluating the company’s financials.

8938|G-グロームHD

326.0

▲ +3.16%

📎 Source:G-グロームHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Gloom Holdings Co., Ltd. has announced a partial correction to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 [Japanese GAAP]”, initially disclosed on May 15, 2026.

- The correction addresses an error in the text description of the consolidated earnings forecast for the fiscal year ending March 2027; there are no changes to the numerical data itself.

- The revised information is located in “Attachment,” “1. Overview of Business Results,” and “(4) Future Outlook.”

- The original forecast for FY2027 projected consolidated net sales of 3,058 million yen, operating profit of 156 million yen, ordinary profit of 157 million yen, and net profit attributable to owners of parent of 205 million yen.

- Following the correction, the revised forecast for FY2027 is consolidated net sales of 3,166 million yen, operating profit of 197 million yen, ordinary profit of 198 million yen, and net profit attributable to owners of parent of 186 million yen.

🤖 AI Perspective

This correction primarily rectifies a textual error in the FY2027 earnings forecast, aligning the narrative with the figures originally presented on page one of the financial results. The change in the forecast for the new grid-scale battery storage business’s sales to 107 million yen appears to be a key driver behind the adjustments in the consolidated figures. While sales, operating profit, and ordinary profit forecasts were revised upwards, the net profit attributable to owners of parent saw a downward adjustment, which may suggest re-evaluation of tax effects or minority interests.

9619|イチネンHD

2115.0

▼ -0.89%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Ichinen Holdings has finalized executive appointments for its newly acquired subsidiaries, Mitsubishi Corporation Agri-Service Co., Ltd. and MC Ferticom Co., Ltd., resolving previously undisclosed details from the April 3, 2026 announcement.

- At Ainoh Co., Ltd., Naotoshi Oinuma is slated to become Representative Director and President, effective June 1, 2026. Tetsuya Kuroda, Heihachi Kimura, and Mitsuo Wada are appointed as Directors, with Hiroshi Adachi as Audit & Supervisory Board Member.

- For Seki Hishi Chemical Co., Ltd., Koji Sasaki is scheduled to become Representative Director and President, effective June 1, 2026. Tetsuya Kuroda, Heihachi Kimura, and Mitsuo Wada are appointed as Directors, with Hiroshi Adachi as Audit & Supervisory Board Member.

- Tokiwa Kaken Co., Ltd. will see Ken Iimura assume the role of Representative Director and President, effective June 1, 2026. Tetsuya Kuroda, Heihachi Kimura, Mitsuo Wada, Yukihiro Harada, and Yasuji Ota are appointed as Directors, with Kunihito Nagata as Audit & Supervisory Board Member.

- At Hokkaido Yuki Co., Ltd., Tetsuya Kuroda is set to become Representative Director and President, effective June 1, 2026. Heihachi Kimura, Mitsuo Wada, and Yoshinori Yamasaki are appointed as Directors, with Kunihito Nagata as Audit & Supervisory Board Member.

🤖 AI Perspective

This announcement provides concrete details regarding the management structures of the newly acquired subsidiaries under Ichinen HD. The appointment of executives from Ichinen HD and its existing subsidiaries to key positions within the new group companies suggests a strategic move to strengthen overall group cohesion and realize synergies. Investors may find these personnel changes significant as they could influence the future business strategies and performance of each new subsidiary, offering a basis for evaluating the integrated management approach and future business developments.

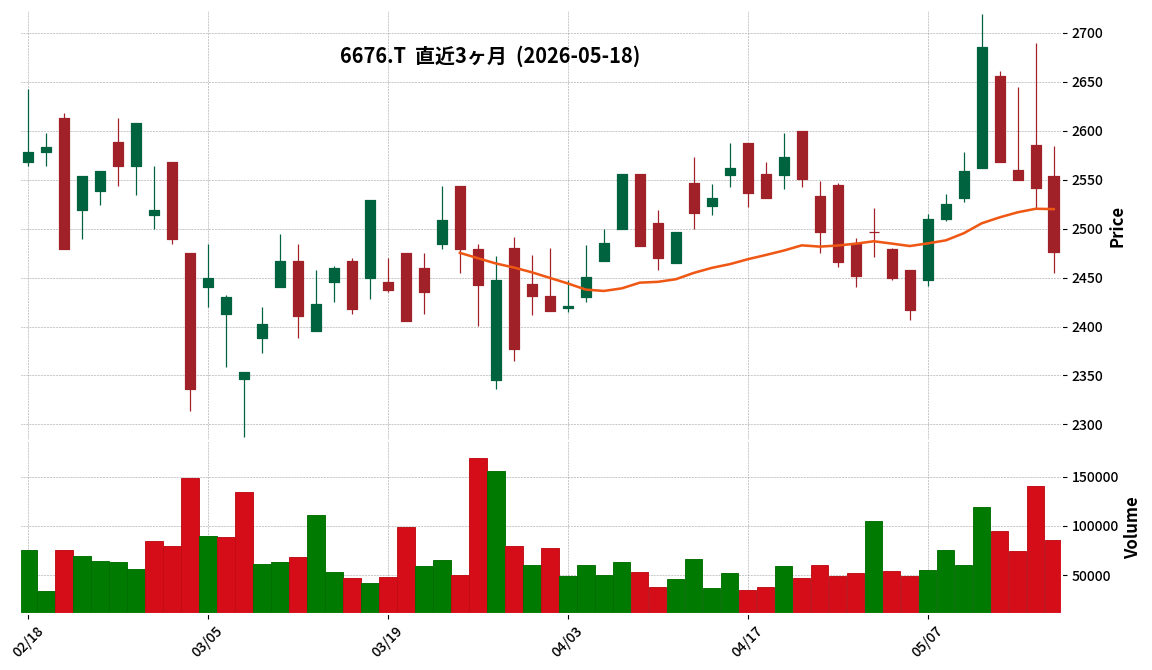

6676|BUFFALO

2476.0

▼ -2.56%

📎 Source:BUFFALO Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- BUFFALO Inc. announced corrections to a portion of its “FY2026/3 Financial Results Presentation Material,” initially published on May 14, 2026.

- The corrections pertain to page 6, “FY2026/3 Consolidated Performance Fluctuation Factors (Overall),” and page 11, “FY2027/3 Consolidated Performance Forecast, Plan based on actual values excluding temporary factors from previous period,” of the presentation material.

- For the FY2026/3 consolidated net sales graph, Airdog’s contribution changed from △12.2 billion yen to △12.7 billion yen, with “Other subsidiaries” added at +0.6 billion yen and “Other” added at △0.1 billion yen.

- For the FY2026/3 consolidated operating income graph, “Other subsidiaries” changed from +0.4 billion yen to +0.1 billion yen, and Airdog changed from △3.0 billion yen to △2.7 billion yen.

- For the FY2207/3 consolidated net sales forecast graph, Airdog’s forecast changed from △10.0 billion yen to △10.8 billion yen, with “Other subsidiaries” added at +1.1 billion yen.

- No corrections were made to the figures in previously disclosed financial statements.

🤖 AI Perspective

These corrections provide a more precise breakdown of the contributing factors to consolidated performance, particularly concerning the Airdog business and other subsidiaries. The adjustments to Airdog’s impact on both net sales and operating income, and subsequent effects on the FY2027/3 sales forecast, may help investors gain a clearer understanding of the company’s business segments. Investors might consider these detailed revisions when evaluating the company’s performance and outlook.

146A|コロンビア・ワークス

3125.0

▼ -3.10%

📎 Source:コロンビア・ワークス Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Columbia Works announced its Q1 FY2026 financial results summary.

- Operating profit for Q1 FY2026 was ¥1,288 million, marking a significant increase of +51.2% compared to the prior year period.

- Net sales reached ¥10,140 million, representing a substantial increase of +87.0% YoY.

- Revenue from the real estate development business increased by +89.7% YoY, while the real estate operation business saw revenue grow by +56.8% YoY.

- The company stated that its FY2026 EPS forecast of ¥544.28 is expected to exceed the mid-term management plan’s FY2026 EPS forecast of ¥460.61 (based on shares outstanding before capital increase), indicating an anticipated achievement of the mid-term plan one year ahead of schedule.

🤖 AI Perspective

Columbia Works’ strong Q1 performance appears to be driven by successful sales of self-developed properties in its real estate development segment and an increase in managed properties within its real estate operation business. The company’s view that inflation and rising rents are positively impacting performance, despite a rising interest rate environment, suggests a strategic positioning within the current real estate market. The announcement of achieving its mid-term management plan objectives ahead of schedule may potentially boost investor confidence in its future business trajectory.

206A|G-PRISMBio

154.0

▼ -9.94%

📎 Source:G-PRISMBio Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-PRISM Bio released its earnings presentation for the interim accounting period ending September 2026.

- The company achieved its first milestone in the joint research project with Ono Pharmaceutical in November 2025, receiving an upfront payment and joint research fees.

- A new program with an undisclosed partner company was initiated in January 2026, progressing to the “hit compound identification” stage.

- Intellectual property expanded with Japanese patents for new bicyclic PepMetics® compounds obtained in September and November 2025, and a U.S. patent allowance for the PepMetics® technology library compound group in May 2026.

- In its in-house development, G-PRISM Bio successfully identified two hit compounds by April 2026 and initiated four new “hit compound identification” programs.

- Collaboration agreements were signed with Talus Bioscience (December 2025) for joint research and with Receptor.AI (March 2026) for drug discovery partnership.

- Joint research agreements with LES LABORATOIRES SERVIER (October 2025) and Boehringer Ingelheim International GmbH (May 2026) were terminated.

- For the interim accounting period ending September 2026, net sales were 253 million JPY, operating loss was △584 million JPY, and net loss was △603 million JPY.

🤖 AI Perspective

G-PRISM Bio’s interim earnings presentation highlights progress in multiple collaborative research projects and expansion of its intellectual property. The achievement of a milestone with Ono Pharmaceutical indicates external validation of the company’s technology. However, the termination of certain joint research agreements and the ongoing net loss are factors that may warrant continued observation regarding the company’s operational trajectory.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

3635|コーエーテクモ

1492.5

▼ -1.68%

📎 Source:コーエーテクモ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Koei Tecmo Holdings announced the confirmed financial results of its parent company, KOYU Holdings, for the fiscal year ending February 2026.

- KOYU Holdings reported a net profit of JPY 16,622,267,472 for the period.

- KOYU Holdings’ business activities include real estate leasing and management, as well as the holding and management of marketable securities.

- Koei Tecmo Holdings’ ownership stake in KOYU Holdings is 51.92% of voting rights as of March 31, 2026.

- The executive lineup of KOYU Holdings includes Keiko Erikawa (Director Honorary Chairman), Yoichi Erikawa (Representative Director Chairman), Mei Erikawa (Representative Director President), and Ai Erikawa (Auditor), all of whom also hold positions within Koei Tecmo Holdings.

🤖 AI Perspective

The disclosure of KOYU Holdings’ financial results provides investors with key insights into the financial health and stability of Koei Tecmo Holdings’ major shareholder. The reported net profit exceeding JPY 16.6 billion may suggest robust asset management and business activities by the parent company, which could indicate a strong financial foundation for the entire group. Furthermore, the significant overlap in key executive positions between both companies suggests a deep level of operational synergy and strategic alignment within the group.

399A|上場日経高配当50

2120.0

▼ -1.49%

📎 Source:上場日経高配当50 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- The Listed Index Fund Nikkei 225 High Dividend Yield Stock 50 (Code: 399A) announced its financial results for the fiscal year ended April 2026 (October 5, 2025 – April 4, 2026).

- Total net assets for the period amounted to JPY 55,327 million, compared to JPY 4,439 million in the fiscal year ended October 2025.

- Primary invested assets, consisting of stocks, totaled JPY 54,439 million, representing 98.4% of the portfolio.

- The Net Asset Value per 1 unit was JPY 2,091.14, an increase from JPY 1,651.87 in the fiscal year ended October 2025.

- The dividend per 1 unit was declared as JPY 29 (compared to JPY 26 in the fiscal year ended October 2025), with the dividend payment commencement date set for May 13, 2026.

- The number of issued units at the end of the fiscal period was 26,458 thousand units, up from 2,687 thousand units in the fiscal year ended October 2025.

🤖 AI Perspective

The fiscal year ended April 2026 results for the Listed Index Fund Nikkei 225 High Dividend Yield Stock 50 indicate a substantial increase in total net assets, outstanding units, and net asset value per unit compared to the previous period. This growth may reflect both capital inflows into the fund and an appreciation in the value of its underlying assets. The rise in dividend per unit is also a notable point for a fund structured around a high-dividend yield strategy.

9381|エーアイテイー

2233.0

▼ -1.19%

📎 Source:エーアイテイー Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- AIT Co., Ltd. announced information regarding the financial results of a non-listed parent company, Logisteed Co., Ltd., on May 18, 2026.

- The non-listed parent company (other affiliated company) subject to the disclosure is Logisteed Co., Ltd.

- The disclosed financial period for Logisteed Co., Ltd. is the fiscal year ended March 2026.

- Logisteed Co., Ltd.’s corporate profile includes its head office in Chuo-ku, Tokyo, Representative Director, Chairman & CEO Yasuo Nakatani, primary business of comprehensive logistics services, and capital of 100 million yen.

- The consolidated financial statements, non-consolidated financial statements, shareholder status, major shareholders, and executive officer information for Logisteed Co., Ltd. were referenced as separate attachments in the announcement.

🤖 AI Perspective

The disclosure by AIT, a listed company, regarding the financial results of its non-listed “other affiliated company,” Logisteed Co., Ltd., can be significant for investors to understand the business collaboration and potential impact on AIT’s consolidated performance. The performance of Logisteed Co., Ltd., which provides comprehensive logistics services, could be a noteworthy factor in assessing AIT’s overall business environment.

3097|物語コーポ

4725.0

▼ -1.36%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Monogatari Corporation announced on May 18, 2026, a capital increase for Storytellers USA, Inc., a holding company for the “SHOGUN Group” operating restaurants in the U.S.

- The capital injection amounts to 6.5 million USD, with payment scheduled for June 30, 2026.

- Post-capital increase, Storytellers USA, Inc.’s capital will be 10 million USD.

- This capital increase will result in Storytellers USA, Inc. becoming a specified subsidiary of Monogatari Corporation.

- The company stated that this transaction will have a minor impact on its consolidated financial results for the fiscal year ending June 2026.

🤖 AI Perspective

This capital increase aligns with Monogatari Corporation’s “Monogatari Vision 2030” strategy, aiming to strengthen its management foundation, operational structure, and expand store presence in the growing U.S. restaurant market. The move to make Storytellers USA, Inc. a specified subsidiary may suggest a deepening commitment to its international expansion efforts. Investors may wish to monitor future developments in the company’s U.S. business strategy.

3694|オプティム

394.0

▼ -11.06%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- OPTiM Corporation announced on May 18, 2026, corrections to a part of its “FY2026 March Earnings Supplemental Materials” initially released on May 15, 2026, at 3:50 PM.

- On page 21, in the “FY2027 March Earnings Forecast, By Segment: AX Business,” the Year-on-Year (YoY) change was corrected from “YoY+0.3%” to “YoY▲0.3%.”

- On page 23, in the “FY2027 March Earnings Forecast, By Segment: AgriTech Business,” the full-year figure for “26/3” within the graph was corrected from “26.2” to “26.3.”

- On page 26, in “3. Growth Strategy, By Segment: AgriTech Business, Agri Buddy,” the description “バーチャネルな土地集約による大規模化” was corrected to “バーチャルな土地集約による大規模化” (virtual land aggregation for large scale).

- On page 28, in “3. Growth Strategy, By Segment: AgriTech Business, Smart Agriculture Service (Core Technology),” the term “シュミレーション” was corrected to “シミュレーション” (simulation).

6360|東自機

4030.0

▼ -1.35%