📌 Today’s Highlights

Today we cover 26 IR announcements. Notable among them: P-北王GROUP (555A), G-SQUEEZE (558A), R-都市ファンド (8953). Use the table of contents below to navigate to each company.

- 555A|P-北王GROUP

- 558A|G-SQUEEZE

- 8953|R-都市ファンド

- 189A|G-D&Mカンパニー

- 296A|G-令和AH

- 3070|G-ジェリービーンズ

- 5592|G-くすりの窓口

- 2798|Y’s

- 9644|タナベコンサルG

- 7177|GMOFHD

- 1434|JESCO HD

- 3232|三重交通GHD

- 3249|R-産業ファ

- 3466|R-ラサールロジ

- 6186|一蔵

- 6653|正興電機製作所

- 7372|G-デコルテHD

- 8060|キヤノンMJ

- 8961|R-森トラスト

- 1783|fantasista

- 4548|生化学

- 5576|オービーシステム

- 6146|ディスコ

- 7462|CAPITA

- 3234|R-森ヒルズ

- 4413|ボードルア

555A|P-北王GROUP

—

▲ +0.00%

📎 Source:P-北王GROUP Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- P-HOKUO GROUP Co., Ltd. (Code: 555A) was listed on the TOKYO PRO Market of the Tokyo Stock Exchange on April 22, 2026.

- For the consolidated fiscal year ending October 2026 (November 1, 2025 – October 31, 2026), the company forecasts net sales of 6,832 million yen (+4.2% YoY), operating income of 100 million yen (+93.6% YoY), ordinary income of 96 million yen (+260.7% YoY), and net income attributable to owners of parent of 67 million yen (+448.4% YoY).

- The forecast includes basic earnings per share of 343.16 yen and a dividend per share of 0.00 yen.

- The consolidated results for the fiscal year ended October 2025 (November 1, 2024 – October 31, 2025) were net sales of 6,559 million yen (+19.2% YoY), operating income of 51 million yen, ordinary income of 26 million yen, and net income attributable to owners of parent of 12 million yen.

- The earnings forecast for October 2026 is based on expectations of increased transaction volume from existing customers, acquisition of new business, a review of project composition emphasizing profitability, and optimization of personnel allocation to improve productivity.

🤖 AI Perspective

The listing on TOKYO PRO Market could serve as a platform for the company’s growth strategy and may enhance its visibility in the market. The robust earnings forecast for the October 2026 fiscal year, projecting significant improvements across all profit metrics in addition to solid sales growth, could indicate the potential success of efforts to strengthen existing businesses and improve efficiency. Investors may closely monitor the company’s future business developments and ongoing disclosure as a newly listed entity.

558A|G-SQUEEZE

—

▲ +0.00%

📎 Source:G-SQUEEZE Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-SQUEEZE (Securities Code: 558A) was listed on the Tokyo Stock Exchange Growth Market today, April 22, 2026.

- For the consolidated fiscal year ending December 2026, the company forecasts net sales of ¥7,034 million (+31.0% YoY), operating profit of ¥705 million (+37.9% YoY), and ordinary profit of ¥700 million (+32.9% YoY).

- Consolidated net profit attributable to owners of parent for FY2026 is projected to be ¥513 million, a 16.7% decrease from the previous fiscal year, attributed to an increase in corporate taxes due to the reversal of deferred tax assets recorded in the prior period.

- For the consolidated fiscal year ended December 2025, G-SQUEEZE reported net sales of ¥5,367 million (+74.9% YoY), operating profit of ¥511 million (+112.6% YoY), ordinary profit of ¥526 million (+147.4% YoY), and net profit attributable to owners of parent of ¥617 million (+111.7% YoY).

- The FY2026 forecast is based on the premise of continued growth in global tourism demand, particularly inbound demand, and the expansion of managed facilities, including existing facilities contributing for the full year and new facilities commencing operations.

🤖 AI Perspective

G-SQUEEZE’s listing on the TSE Growth Market coincides with the announcement of its FY2026 earnings forecast, which indicates substantial growth in sales and operating profit. The projected decline in net profit for FY2026, attributed to a tax-related item from the prior period, suggests a one-time accounting adjustment rather than a fundamental shift in operational performance. Investors may find the company’s strategic focus on expanding its managed facilities amidst a robust inbound tourism market to be a key area for monitoring future growth.

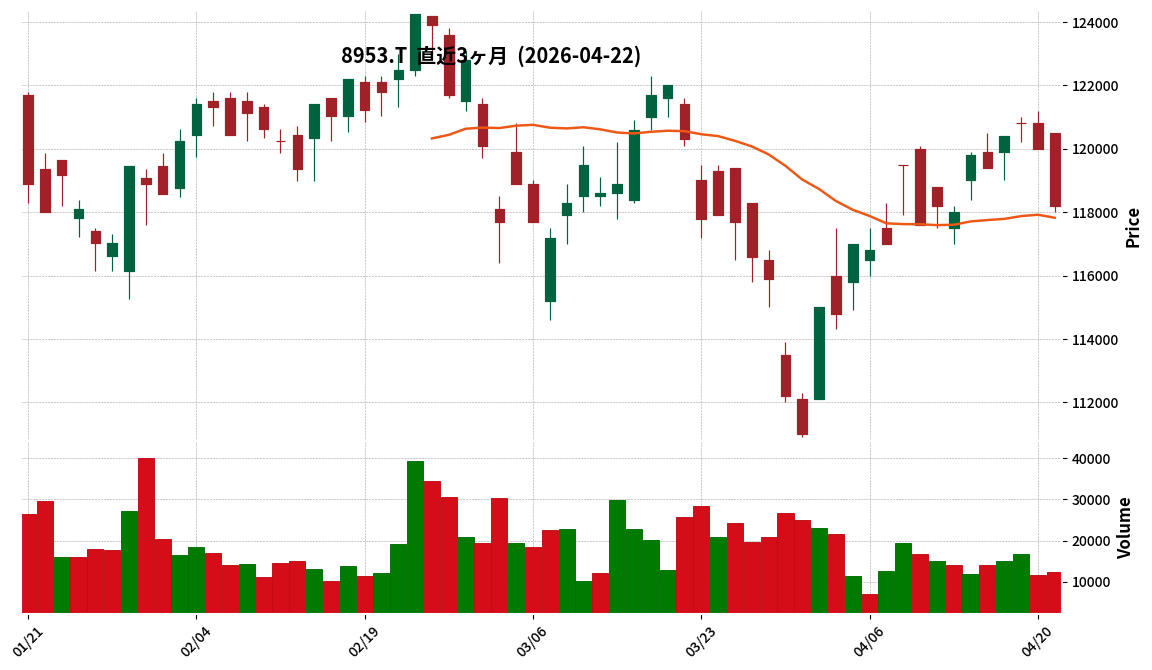

8953|R-都市ファンド

118200.0

▼ -1.50%

📎 Source:R-都市ファンド Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Japan Urban Fund Investment Corporation (R-CITY FUND) announced a partial correction to its “FY2026/2 Financial Results (REIT)” initially disclosed on April 21, 2026. The correction was made on April 22, 2026.

- The reason for the correction was an error in a part of the description, with no significant changes to the numerical data.

- For the August 2026 period operating forecast, ordinary income was revised upwards from 22,454 million yen to 22,457 million yen, and net income from 22,453 million yen to 22,456 million yen. The estimated distribution per unit of net income was also adjusted from 3,121 yen to 3,122 yen.

- For the February 2027 period operating forecast, ordinary income was revised downwards from 17,667 million yen to 17,664 million yen, and net income from 17,667 million yen to 17,664 million yen. The estimated distribution per unit of net income was also adjusted from 2,456 yen to 2,455 yen.

- The projected distribution per unit (excluding excess distribution) for both periods remains unchanged: 2,981 yen for the August 2026 period and 2,900 yen for the February 2027 period.

🤖 AI Perspective

This correction appears to be a minor adjustment to certain numerical figures in the future earnings forecasts, aimed at ensuring the accuracy of the disclosed information. While there are slight revisions to ordinary income and net income, the stability of the projected distribution per unit, a key metric for investors, may be a point of interest. This revision could be seen as an indication of the company’s commitment to accuracy in its financial reporting.

189A|G-D&Mカンパニー

962.0

▲ +1.26%

📎 Source:G-D&Mカンパニー Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-D&M Company announced on April 22, 2026, a capital and business alliance with MedTech Group Inc.

- G-D&M Company will subscribe to 436 common shares through a third-party allotment, with a total payment of JPY 30 million.

- The payment date is April 30, 2026, resulting in G-D&M Company holding approximately 12.5% (based on 3,486 shares) of MedTech Group after the acquisition.

- This alliance aims to combine G-D&M Company’s financial, human resources, and management support in the medical and nursing care sectors with MedTech Group’s “AI Hippo Medical Loop,” an AI platform for medical data utilization.

- MedTech Group Inc., established on February 20, 2019, specializes in system development and consulting for healthcare and nursing care.

🤖 AI Perspective

This alliance suggests G-D&M Company’s strategic move to accelerate digital transformation in the healthcare and nursing care sectors by integrating MedTech Group’s advanced AI technology with its existing client base. The introduction of a private AI platform focused on secure medical data utilization could potentially contribute to improving efficiency and quality of medical services, which may lead to expanded mid-to-long term revenue opportunities.

296A|G-令和AH

853.0

▲ +0.24%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Reiwa AH announced on April 22, 2026, a revision (increase) to its year-end dividend forecast for the fiscal year ending March 31, 2026, following a board meeting.

- The revised year-end dividend per share is ¥20.00, an increase from the previous forecast of ¥19.50. The total annual dividend per share is revised from ¥32.00 to ¥32.50.

- This revision to the year-end dividend forecast for the current fiscal year was made based on a target consolidated payout ratio of 85% and the finalized net income for the fourth quarter exceeding the previous forecast.

- The company’s basic dividend policy aims for a consolidated payout ratio of 81% to 90% annually, based on a fundamental ratio of 80% with an additional 1% to 10% considering the company’s financial condition.

- The estimated DOE (Dividend on Equity) for the fiscal year ending March 2026 is 42.6%, an increase of 8.7 percentage points from the 33.9% recorded in the fiscal year ended March 2025.

🤖 AI Perspective

The company maintains a clear dividend policy and a commitment to stable ordinary dividends, supported by its business performance, which is largely unaffected by external environmental fluctuations. This dividend increase, prompted by fourth-quarter net income surpassing expectations, may suggest the company’s strong commitment to shareholder returns. The significant rise in DOE could indicate an enhanced focus on distributing profits back to shareholders.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

3070|G-ジェリービーンズ

112.0

▼ -2.61%

📎 Source:G-ジェリービーンズ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Jellybeans Group’s subsidiary, JB Sustainable Co., Ltd., entered into a business alliance agreement with Bioseller Co., Ltd. on April 22, 2026, for a food waste processing solution business.

- Under this alliance, JB Sustainable obtained non-exclusive sales rights for Bioseller’s commercial food waste processing machine “BIOPOWER,” targeting key sectors such as food factories, accommodations, commercial facilities, and municipal facilities.

- JB Sustainable aims to establish a subscription-based service (monthly fee) that combines product sales with leasing/rental options, consumables supply, and regular maintenance.

- JB Sustainable secured an order for one “BIO POWER 500R” commercial food waste processing machine from an undisclosed client, a local food supermarket chain, for JPY 28,050,000. Delivery is scheduled for the end of May 2026.

- Sales and profit from this order are expected to be recorded in the fiscal year ending January 2027. The impact of the business alliance on the January 2027 fiscal year performance is currently under review, with prompt disclosure planned if necessary.

🤖 AI Perspective

This announcement suggests G-Jellybeans Group’s strategic move to expand its environmental solution business domain, contributing to a sustainable society while securing new revenue streams. The planned introduction of a subscription model is noteworthy, as it aims to establish a continuous and stable recurring revenue base. The simultaneous announcement of a business alliance and a specific order contract could indicate an acceleration of their business development.

5592|G-くすりの窓口

2764.0

▲ +0.36%

📎 Source:G-くすりの窓口 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-KUSURI NO MADOGUCHI Co., Ltd. resolved at its Board of Directors meeting on April 22, 2026, to acquire all shares of Technonetwork Co., Ltd., making it a wholly-owned subsidiary.

- Concurrently, Technonetwork’s wholly-owned subsidiary, King Co., Ltd., will also become a group company of G-KUSURI NO MADOGUCHI.

- Technonetwork operates a medical IT business, focusing on the sale and implementation support of the Japan Medical Association’s standard receipt software “ORCA,” with over 1,200 medical institution clients primarily in the Kyushu region.

- The acquisition price for Technonetwork shares is undisclosed but is stated to be less than 15% of the consolidated net assets at the end of the previous consolidated fiscal year.

- The share transfer is scheduled for May 1, 2026, and the acquired companies are expected to be included in G-KUSURI NO MADOGUCHI’s consolidated financial statements from the first quarter of the fiscal year ending March 2027, with the impact on the consolidated earnings forecast for that period deemed minor.

🤖 AI Perspective

This acquisition by G-KUSURI NO MADOGUCHI appears to strategically strengthen its healthcare IT solutions for medical institutions, aligning with Japan’s government-led medical DX and electronic medical record standardization initiatives. It could signify an acceleration of the company’s full-scale entry into the medical institution market, complementing its existing pharmacy-focused business. Investors may monitor the potential for synergies through combined customer bases and shared operational know-how.

2798|Y’s

2984.0

▼ -0.03%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Y’s reported consolidated sales of ¥13,046 million for the fiscal year ended February 2026 (up 7.6% year-on-year), operating profit of ¥249 million (up 109.5% year-on-year), and ordinary profit of ¥345 million (up 39.1% year-on-year).

- Net profit attributable to owners of parent was ¥205 million (down 21.3% year-on-year), falling short of the plan. This was attributed to increased selling, general and administrative expenses, the non-execution of a planned store sale in the second half, an impairment loss of ¥80 million, and a negative impact from deferred tax adjustments of ¥55 million.

- Existing store sales (monthly basis) increased by 6.9% year-on-year, driven by inbound demand in the first half and enhanced promotional site utilization and delivery services in the second half.

- For the fiscal year ending February 2027, the company forecasts consolidated sales of ¥15,446 million (up 18.4% year-on-year), operating profit of ¥424 million (up 70.4% year-on-year), ordinary profit of ¥483 million (up 39.9% year-on-year), and net profit attributable to owners of parent of ¥422 million (up 105.7% year-on-year).

- The FY2027/2 outlook incorporates the opening of five new stores (4 directly managed, 1 FC store) and the planned addition of Hotel Yamanoue Co., Ltd. as a consolidated subsidiary.

🤖 AI Perspective

- While Y’s achieved increased revenue and profit in FY2026/2 compared to the previous year, the company fell short of its internal profit targets, which may be attributed to higher operating costs and the recognition of special losses.

- The robust forecasts for FY2027/2, projecting significant growth in sales and profits, could indicate a strong focus on expansion through new store openings, the consolidation of Hotel Yamanoue, and initiatives to strengthen existing operations.

- Strategic efforts such as targeting affluent inbound tourists and enhancing its Japanese cuisine business may reshape the company’s future revenue streams, making these developments worth monitoring for investors.

9644|タナベコンサルG

711.0

▲ +0.71%

📎 Source:タナベコンサルG Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- On April 22, 2026, Tanabe Consulting Group resolved to partially revise its shareholder benefit program during a board meeting.

- The change will take effect from the shareholder benefits with the record date of September 30, 2026.

- The existing shareholder benefit, QUO cards (ranging from 500 yen to 10,000 yen depending on shareholding), will be replaced with an equivalent value of Digital Gift®.

- Digital Gift® is planned to be exchangeable for various electronic money and points, including PayPay Money Light, Amazon Gift Cards, Rakuten Point Gifts, and d Point.

- Shareholders will select their preferred gift via a dedicated website after receiving a “Shareholder Benefit Guide” mailed within approximately three months from the record date.

🤖 AI Perspective

The shift to Digital Gift® may enhance convenience and broaden options for shareholders. Offering a variety of exchange partners such as electronic money and points could potentially maintain existing shareholder satisfaction and attract new individual investors.

7177|GMOFHD

996.0

▼ -1.78%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of the fiscal year ending December 2026 (preliminary), GMOFH reported consolidated operating revenue of JPY 16,234 million (up 25.1% year-on-year), operating profit of JPY 6,462 million (up 53.1%), ordinary profit of JPY 6,435 million (up 80.3%), and quarterly net income attributable to parent company shareholders of JPY 4,205 million (up 67.9%).

- The first quarter results marked a new record high on a quarterly basis.

- The company stated that CFD (Contract for Difference) revenue, which more than tripled year-on-year due to strong commodity markets for gold and crude oil and stock index movements, was a primary driver of overall performance.

- The full-year dividend forecast for the fiscal year ending December 2026 has been revised upward from the previous JPY 42.08 per share to JPY 54.76 per share (quarterly dividend revised from JPY 10.52 to JPY 13.69).

- The revision in dividend forecast is attributed to the estimated dividend amount, calculated based on a 65% payout ratio from the preliminary Q1 net income attributable to parent company shareholders, exceeding the previous forecast, with the surplus distributed equally across each quarter.

🤖 AI Perspective

The strong Q1 performance, with significant increases across key revenue and profit metrics and achieving a record quarterly high, warrants attention. The substantial growth in CFD revenue, driven by commodity and stock index market volatility, appears to be a key factor contributing to these results. The upward revision of the annual dividend forecast, consistent with the company’s dividend policy (payout ratio of 65% or more and a DOE of 10% as a lower limit), may suggest a commitment to stable shareholder returns aligned with profit growth.

1434|JESCO HD

2269.0

▼ -2.74%

📎 Source:JESCO HD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- JESCO Holdings, Inc. reported consolidated results for the second quarter of the fiscal year ending August 2026, with net sales of ¥10,934 million (up 25.9% year-on-year), operating profit of ¥1,315 million (up 119.8%), ordinary profit of ¥1,340 million (up 117.9%), and profit attributable to owners of parent of ¥831 million (up 118.0%).

- By segment, the Domestic EPC business recorded net sales of ¥6,084 million (up 7.0% year-on-year) and operating profit of ¥764 million (up 78.7%), driven by strong performance in communication system and electrical equipment construction, improved operating rates, and progress on high-profit projects.

- The Real Estate business saw net sales of ¥4,091 million (up 102.9% year-on-year) and operating profit of ¥779 million (up 145.4%), attributed to the sale of two properties for sale and full occupancy of owned buildings.

- The ASEAN EPC business reported net sales of ¥758 million (down 22.8% year-on-year), but its operating loss decreased to ¥29 million from ¥80 million in the previous year. While design and estimation orders expanded, the company focused on collecting outstanding receivables and restrained from accepting orders from local companies for construction.

- The full-year consolidated earnings forecast for the fiscal year ending August 2026 remains unchanged, projecting net sales of ¥20,000 million (up 4.9% from the previous year), operating profit of ¥1,800 million (up 4.5%), ordinary profit of ¥1,750 million (up 3.4%), and profit attributable to owners of parent of ¥1,100 million (up 2.2%).

🤖 AI Perspective

JESCO Holdings’ second-quarter results for the fiscal year ending August 2026 demonstrate substantial revenue and profit growth, primarily driven by strong performances in its Domestic EPC and Real Estate segments. The significant contribution from real estate sales and robust domestic infrastructure demand appear to be key factors. While the ASEAN EPC business experienced a decline in sales, the reduction in operating loss may suggest improving operational efficiencies or strategic adjustments within that segment.

3232|三重交通GHD

532.0

▼ -1.66%

📎 Source:三重交通GHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Mie Kotsu Group Holdings, Inc. announced on April 22, 2026, the recording of an extraordinary loss in its standalone financial statements.

- The company will record an extraordinary loss in its standalone financial results for the fiscal year ending March 31, 2026 (April 1, 2025, to March 31, 2026).

- The extraordinary loss amounts to JPY 808 million, recorded as a provision for losses on business of affiliated companies.

- This loss arises from the dissolution of a consolidated subsidiary, San-Kotsu Creative Life Co., Ltd., which led to a deterioration in its financial condition.

- This provision will only be recorded in the company’s standalone financial statements and will be eliminated in the consolidated financial statements, resulting in no impact on consolidated earnings.

🤖 AI Perspective

While the recording of an extraordinary loss in standalone financial statements affects the parent company’s individual net profit, the fact that it will not impact consolidated earnings is a key point for investors. This suggests that the financial restructuring through the subsidiary’s dissolution is being managed in a way that limits direct negative effects on the overall group’s performance. Such an action may indicate a strategic decision to streamline the group’s business portfolio.

3249|R-産業ファ

147300.0

▼ -1.01%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- R-Industrial Fund Investment Corporation announced on April 22, 2026, a correction to a part of its “Financial Results for the Fiscal Period Ended January 2026 (REIT),” originally disclosed on March 17, 2026.

- The correction applies to “Unexpired lease payments” under “Operating Lease Transactions (Lessor side)” within “2. Financial Statements (8) Notes to Financial Statements” on page 22 of the financial results.

- The reason for the correction is that errors in the description were identified during the preparation of the Securities Report for the 37th fiscal period (from August 1, 2025, to January 31, 2026).

- The “Unexpired lease payments” for the “Current Period (January 31, 2026)” were corrected as follows: within 1 year from 24,867,094 thousand yen to 23,483,110 thousand yen, over 1 year from 214,077,027 thousand yen to 215,357,212 thousand yen, and the total from 238,944,121 thousand yen to 238,840,323 thousand yen.

🤖 AI Perspective

This correction demonstrates the company’s process of reviewing financial disclosures during the preparation of formal reports like the Securities Report, leading to the identification and amendment of errors. Investors may view this as an indication of the company’s commitment to financial reporting accuracy and may want to understand the nature of the error to assess any potential implications for the overall financial picture. Monitoring whether these corrected figures impact any key financial ratios or future projections could be worthwhile.

3466|R-ラサールロジ

155100.0

▼ -0.83%

📎 Source:R-ラサールロジ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal period ended February 2026, operating revenue was JPY 12,471 million (down 5.8% from the previous period), operating income was JPY 6,914 million (down 6.9%), ordinary income was JPY 6,021 million (down 8.3%), and net income was JPY 6,020 million (down 8.3%).

- Distribution per unit (DPU), including excess distributions, was JPY 3,725, with total distributions amounting to JPY 6,469 million.

- As of the end of the period, total assets stood at JPY 385,306 million, net assets at JPY 203,698 million, and the equity ratio was 52.9%.

- The portfolio maintained a high occupancy rate of 98.6% and comprised 172 tenants.

- Interest-bearing debt amounted to JPY 171,020 million, and the loan-to-value (LTV) ratio was 44.4%.

- The REIT completed refinancing totaling JPY 17,580 million on February 17, 2026.

🤖 AI Perspective

- While operating revenue and profits decreased compared to the previous period, the DPU including excess distributions reached JPY 3,725.

- The portfolio’s high occupancy rate of 98.6% and diversified tenant base could be seen as indicators of operational stability.

- The status of interest-bearing debt, LTV, and the recent refinancing activity may provide insights into the REIT’s financial management and future funding strategies.

6186|一蔵

374.0

▼ -0.80%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Ichikura Co., Ltd. (Code: 6186, Tokyo Stock Exchange Standard) resolved to partially enhance its shareholder benefit program at a board meeting on April 22, 2026.

- The enhancement introduces “Restaurants (company-owned and partner)” as a new benefit option, supplementing existing kimono, wedding, and flower gift services.

- At designated restaurants, a discount of 3,000 yen per person will be applied for up to two people per shareholder benefit ticket.

- The specified partner restaurants include “Restaurant Perfume,” “Il Ghiottone,” “Il Ghiottone di Piu,” and eight locations of “Dynamic Kitchen & Bar Hibiki.”

- This revised program will be effective from the record date of March 31, 2026, and will apply to shareholder benefit tickets scheduled for dispatch in late June 2026 (valid until June 30, 2027).

🤖 AI Perspective

This expansion of Ichikura’s shareholder benefit program appears to be aimed at increasing shareholder engagement and enhancing the investment appeal of the company. The addition of new partner restaurants may broaden the utilization opportunities for shareholders, potentially increasing the perceived value of the benefits. The inclusion of several well-known restaurants, particularly in urban centers, could serve to attract more attention from the investor community.

6653|正興電機製作所

2718.0

▼ -4.43%

📎 Source:正興電機製作所 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Seiko Denki Co., Ltd. announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026 – March 31, 2026).

- Consolidated net sales reached ¥9,574 million (+12.6% year-on-year), operating profit ¥1,280 million (+16.3% YoY), ordinary profit ¥1,456 million (+25.4% YoY), and net profit attributable to owners of parent ¥1,057 million (+41.6% YoY).

- New orders received amounted to ¥12,288 million (+6.7% YoY).

- The Service segment experienced a significant increase in large-scale projects for data centers and power storage facilities, with sales growing to ¥2,138 million (+53.4% YoY). The Environment & Energy segment also performed strongly, with sales of ¥3,929 million (+10.5% YoY) and segment profit of ¥652 million (+110.8% YoY) due to robust public sector demand and improved profit margins.

- The full-year consolidated earnings forecast and annual dividend forecast for the fiscal year ending December 2026 remain unchanged as of April 22, 2026.

🤖 AI Perspective

Seiko Denki’s first quarter results for FY2026 demonstrate substantial year-on-year growth across key profit metrics. This performance appears to be driven by increased demand for large-scale projects in the Service segment, particularly for data centers and power storage facilities, coupled with improved profitability in the public sector within the Environment & Energy segment. The sale of investment securities also contributed positively to ordinary profit. As the full-year forecast remains unrevised, monitoring the company’s progress in subsequent quarters could be insightful.

7372|G-デコルテHD

380.0

▼ -1.55%

📎 Source:G-デコルテHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- DECOLLTE HOLDINGS CO., LTD. resolved and signed an agreement on April 22, 2026, to acquire all shares of Emu Co., Ltd. and Emu Lab Co., Ltd., making them wholly-owned subsidiaries.

- The acquisition aims to significantly strengthen the anniversary photo service, a key part of the company’s mid-term management plan, with the service’s contribution to consolidated net sales projected to increase from 5.1% in Sept. 2025 to over 10% by Sept. 2027.

- Emu Co., Ltd., founded in 1998, operates six “Studio Emu” locations in Hyogo Prefecture, specializing in children’s photography. Emu Lab Co., Ltd., established in 2015, handles image data retouching and production design.

- The total acquisition cost is approximately JPY 1,090 million, consisting of JPY 740 million for Emu shares, JPY 260 million for Emu Lab shares, and an estimated JPY 90 million for advisory fees.

- The share transfer is scheduled for April 30, 2026, and the impact on the company’s consolidated financial results for the fiscal year ending September 2026 is currently undetermined.

🤖 AI Perspective

This acquisition appears to be a strategic move for G-DECOLLTE HD to diversify its business portfolio by strengthening its anniversary photo services, leveraging Emu’s expertise in children’s photography. The integration of Emu’s regional brand strength and operational know-how into existing studios, coupled with cross-selling opportunities between wedding and anniversary photo services, could lead to enhanced customer lifetime value. Furthermore, the centralization of internal administrative operations may contribute to overall group efficiency.

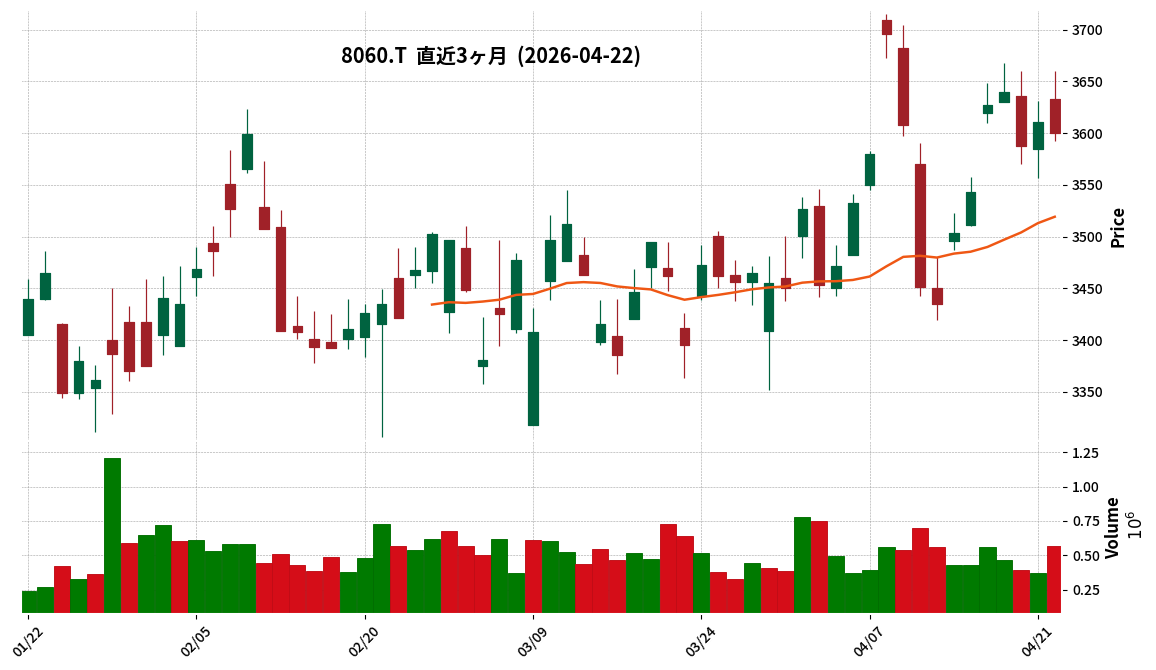

8060|キヤノンMJ

3600.0

▼ -0.30%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Canon Marketing Japan (Canon MJ) announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026 – March 31, 2026).

- Consolidated net sales amounted to ¥171,666 million (up 2.6% year-on-year), operating profit was ¥18,526 million (up 40.7% year-on-year), and ordinary profit reached ¥18,565 million (up 40.6% year-on-year).

- Net income attributable to owners of the parent was ¥12,800 million (up 45.3% year-on-year), with basic earnings per share at ¥60.09.

- The company implemented a 2-for-1 stock split of common shares, effective April 1, 2026, with March 31, 2026, as the record date. The aforementioned per-share figures are calculated assuming this stock split took place at the beginning of the previous fiscal year.

- The full-year consolidated earnings forecast (Net sales ¥685,000 million, Operating profit ¥60,000 million, Ordinary profit ¥60,700 million, Net income attributable to owners of the parent ¥42,000 million) and the year-end dividend forecast (¥90.00 per share, after considering the stock split) remain unchanged from the latest publicly announced figures.

🤖 AI Perspective

The first quarter saw Canon MJ achieve over 40% year-on-year growth in key profit metrics. This performance appears to be driven by robust activity in the IT Solutions segment and an increased proportion of high-value-added products and services, which likely contributed to an improved gross profit margin. The unchanged full-year outlook suggests that the company anticipates performance to align with its initial plans.

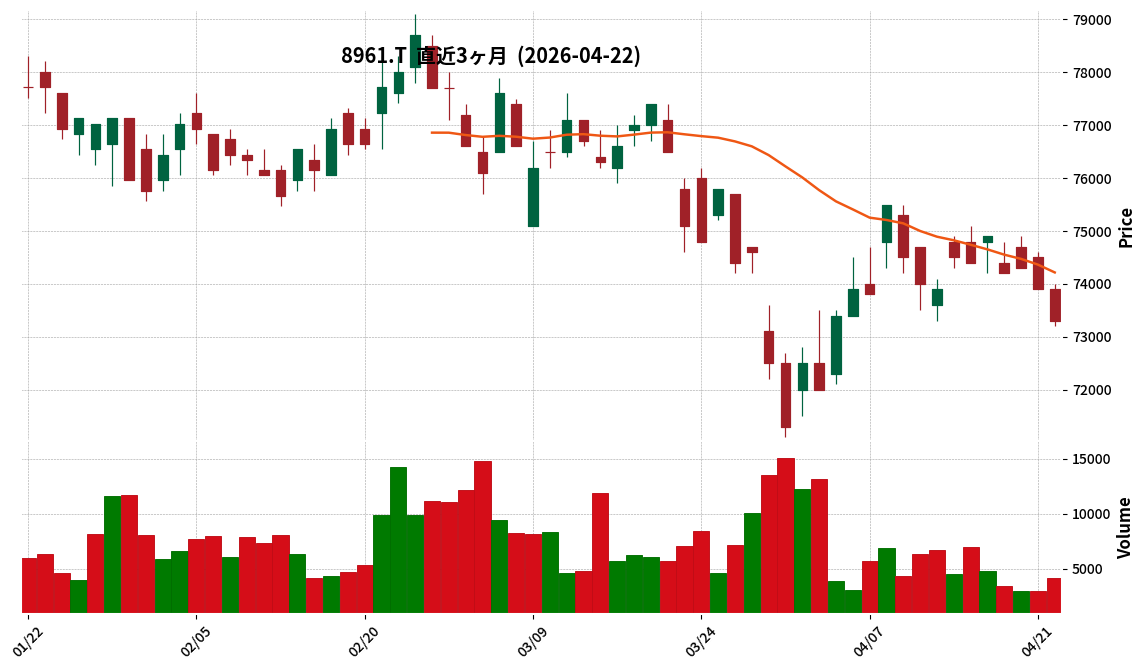

8961|R-森トラスト

73300.0

▼ -0.81%

📎 Source:R-森トラスト Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- R-Mori Trust announced its financial results for the fiscal period ending February 2026 (September 1, 2025 – February 28, 2026).

- For the period, operating revenue was JPY 11,584 million (down 0.7% from the previous period), operating income was JPY 7,421 million (down 0.3%), and net income was JPY 6,537 million (down 0.9%).

- Distribution per unit (DPU) was JPY 1,837 (excluding excess distributions), maintaining a payout ratio of 100.0%.

- As of the end of the period (February 28, 2026), total assets stood at JPY 471,002 million, net assets at JPY 234,483 million, and the equity ratio at 49.8%.

- The portfolio consisted of 20 properties, with an occupancy rate of 99.6% (99.2% based on sublease agreements) at period-end.

🤖 AI Perspective

- While operating revenue and net income saw a slight decrease compared to the previous period for FY2026 Feb., the DPU was nearly equivalent to net income, maintaining a 100.0% payout ratio.

- The portfolio’s occupancy rate remained high at 99.6% at period-end, which suggests stable operational performance of the managed assets.

- For the forecast periods of August 2026 and February 2027, DPU is projected at JPY 1,814 and JPY 1,795 respectively, with distributions anticipated to include the reversal of compression reserves.

1783|fantasista

66.0

▲ +3.12%

📎 Source:fantasista Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Fantasista Co., Ltd. resolved to acquire shares of Amoti Co., Ltd. to make it a subsidiary at its Board of Directors meeting held on April 22, 2026.

- The company had been discussing a capital and business alliance as announced on February 25, 2026, but decided to proceed with the stock acquisition for consolidation instead.

- Amoti Co., Ltd. operates 20 precious metals and other goods purchasing stores primarily in Tokyo, engaging in the reuse business of such items.

- Fantasista will acquire 8,000 shares (voting rights ratio: 54.98%) of Amoti’s total issued shares of 14,550 shares (after capital increase) for a total of JPY 120 million.

- Following this acquisition, Amoti Co., Ltd. is expected to become a consolidated subsidiary of Fantasista from the third quarter of the fiscal year ending September 2026.

🤖 AI Perspective

- Fantasista’s shift from a capital and business alliance to full subsidiary acquisition suggests an intent for more integrated and agile management of Amoti Co., Ltd.

- The inclusion of Amoti, which operates in the precious metals reuse business, could indicate Fantasista’s strategy to diversify its business portfolio and secure new revenue streams.

- The acquisition price calculation, based on a third-party valuation using the DCF method, suggests an emphasis on transparency in the transaction.

4548|生化学

713.0

▼ -2.19%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Seikagaku Corporation announced that it obtained manufacturing and marketing approval for its adhesion barrier SI-449 (Product name: “CS Barrier”) in Japan as of April 20, 2026.

- Covidien Japan Corporation, the Japanese subsidiary of global medical device manufacturer Medtronic, has been determined as the sales partner for “CS Barrier” in Japan. Covidien Japan has a strong presence in areas such as gastrointestinal surgery and gynecology.

- Seikagaku will support the sales partner’s activities, including providing academic information, as the marketing authorization holder, aiming to reduce the risk of complications associated with post-surgical adhesions.

- The domestic launch timing for “CS Barrier” will be announced after discussions with Covidien Japan and the acquisition of the reimbursement price.

- The impact of this matter on consolidated financial forecasts will be incorporated into the consolidated earnings forecast for the fiscal year ending March 2027, which is to be disclosed in the financial results for the fiscal year ending March 2026, scheduled for announcement on May 13, 2026.

🤖 AI Perspective

- The acquisition of manufacturing and marketing approval in Japan is a significant milestone for bringing a new product to market.

- The partnership with Covidien Japan, a subsidiary of a global medical device manufacturer, could accelerate the market penetration of “CS Barrier” due to its established presence and portfolio in relevant surgical fields.

- Investors may focus on upcoming announcements regarding the launch timing, reimbursement pricing, and the specific integration into the consolidated earnings forecasts.

5576|オービーシステム

3065.0

▲ +10.45%

📎 Source:オービーシステム Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- OB System Co., Ltd. resolved to increase its year-end dividend for the fiscal year ended March 31, 2026, at a Board of Directors meeting held on April 22, 2026.

- The year-end dividend per share for the period with a record date of March 31, 2026, will be JPY 55.00.

- This represents an increase of JPY 5.00 from the previously announced dividend forecast of JPY 50.00, published on April 23, 2025.

- The total annual dividend per share for the fiscal year ending March 2026 is expected to be JPY 105.00, combining the JPY 50.00 interim dividend and the JPY 55.00 year-end dividend.

- The total dividend amount for the current fiscal year (ending March 2026) is JPY 127 million, an increase from JPY 92 million in the previous fiscal year (ended March 2025).

- This dividend proposal is scheduled to be submitted to the 54th Ordinary General Meeting of Shareholders on June 19, 2026.

🤖 AI Perspective

OB System’s decision to increase its dividend appears to align with its mid-term management plan, which emphasizes strengthening shareholder returns and identifies shareholder profit distribution as a key management priority. The company has also articulated a goal to raise its dividend payout ratio to over 40% in the near future, suggesting a potential ongoing commitment to enhanced shareholder distributions.

6146|ディスコ

74830.0

▲ +0.79%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- DISCO announced its consolidated financial results for the fiscal year ended March 2026, with net sales increasing by 11.1% year-on-year to ¥436,889 million and net income attributable to owners of parent rising by 9.4% year-on-year to ¥135,521 million.

- Both full-year net sales and shipments achieved record highs for the sixth consecutive year.

- The annual dividend per share was increased to ¥505.00 from ¥413.00 in the previous fiscal year.

- Total assets grew by ¥89,323 million from the previous fiscal year-end to ¥743,410 million, while net assets increased by ¥95,422 million to ¥588,125 million.

- For the first quarter of the fiscal year ending March 2027, the company forecasts consolidated net sales of ¥106,100 million (+18.0% YoY) and net income attributable to owners of parent of ¥29,500 million (+24.1% YoY).

🤖 AI Perspective

DISCO’s FY2026/3 results show a continuation of strong performance, with both net sales and shipments achieving record highs for the sixth consecutive year, driven by increased demand for high-value-added products for high-performance semiconductors, potentially linked to the expanding generative AI market. The increase in the annual dividend per share may suggest a robust financial position and a commitment to shareholder returns.

7462|CAPITA

595.0

▼ -1.65%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- CAPITA Co., Ltd. resolved at its Board of Directors meeting held today, April 22, 2026, to make its consolidated subsidiary, Bio-Site Capital Co., Ltd., a wholly-owned subsidiary.

- The purpose of acquiring additional shares is to enable agile management decisions as a unified group and minimize considerations for minority shareholders and adjustment costs.

- Through the additional acquisition of shares from existing shareholders, CAPITA’s voting rights ownership in Bio-Site Capital will increase from the current 63.76% to 100%.

- Bio-Site Capital operates laboratory business, fund business, and other related services.

- The company announced that the impact of this transaction on its consolidated performance for the fiscal year ending March 2027 is expected to be minor.

🤖 AI Perspective

The full acquisition of its consolidated subsidiary suggests that the CAPITA Group aims to strengthen its framework for accelerating decision-making processes and optimizing the allocation of management resources more flexibly. This move may particularly enable the group to swiftly implement business portfolio restructuring based on optimal solutions for the entire group, especially in a rapidly changing market environment. As the short-term impact on financial performance is stated as minor, this initiative appears to be intended for the promotion of the group’s mid- to long-term strategies.

3234|R-森ヒルズ

134100.0

▼ -0.96%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Mori Building Investment Management Co., Ltd. (MIM), the asset management company for Mori Hills REIT (MHR), has signed an absorption-type merger agreement with Mori Building Real Estate Advisory Co., Ltd. (MIA).

- The merger will take effect on June 30, 2026, with MIM as the surviving company and MIA as the absorbed company.

- The purpose of the merger is to consolidate human resources and expertise in asset management within the Mori Building Group, aiming to improve operational productivity and further stabilize the operating base.

- This merger does not involve MHR, and there are no planned changes to the asset management agreement between MHR and MIM.

- MIM also decided to amend its Articles of Incorporation, adding investment advisory and agency services as well as Type II Financial Instruments Business to its business objectives.

🤖 AI Perspective

This merger suggests an effort by the Mori Building Group to streamline its asset management operations by integrating MIA’s real estate trust beneficiary rights advisory services into MIM. The establishment of separate REIT Management and Advisory divisions within the post-merger MIM, along with measures to prevent conflicts of interest, indicates a focus on strengthening the organizational structure and governance. These strategic steps could potentially contribute to enhanced long-term asset management service quality.

4413|ボードルア

2230.0

▲ +0.72%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended February 2026, Boardlux Inc. reported a 49% year-over-year increase in revenue and a 37.8% increase in profit.

- The mid-term management plan has been revised upwards and rolled forward by one year, with a projected revenue of ¥23.5 billion for FY2027/2 and an annual growth rate of +30% thereafter.

- Regarding AI-driven task replacement, the company stated that its business operations are not directly substitutable by AI, and AI’s auxiliary use (e.g., document creation support, config generation) accounts for approximately 10% of total man-hours.

- The M&A strategy aims to improve consolidated operating profit margins by enhancing the profitability of acquired subsidiaries through Post Merger Integration (PMI).

- The company has maintained a record of never experiencing a quarter-over-quarter decline in revenue since its listing.

🤖 AI Perspective

- Boardlux’s strong financial performance for FY2026/2, coupled with the upward revision of its mid-term plan, may suggest a continued trajectory of robust business expansion.

- The company’s specialization in “IT Infrastructure,” a domain perceived as less susceptible to direct AI replacement, along with its unique growth strategy focused on nurturing inexperienced talent and strategic M&A, could be key areas for investor attention.

- The consistent quarter-over-quarter revenue growth since listing might indicate the stability of its demand environment and the reproducibility of its business model.

💡 Start investing with IR insights

※ 本ページには広告が含まれます(PR)

Disclaimer: This article is for informational purposes only and does not constitute investment advice. All investment decisions are at your own risk.

コメント