📌 Today’s Highlights

Today we cover 87 IR announcements. Notable among them: トクヤマ (4043), 楽天225ダブルブル (1458), レシップHD (7213). Use the table of contents below to navigate to each company.

- 4043|トクヤマ

- 1458|楽天225ダブルブル

- 7213|レシップHD

- 9040|大宝運

- 6902|デンソー

- 5834|G-SBIリーシング

- 8609|岡三

- 6201|豊田織

- 6029|アトラG

- 8613|丸三証

- 8697|JPX

- 8914|エリアリンク

- 1934|ユアテック

- 6592|マブチモーター

- 8624|いちよし

- 1777|川崎設備

- 2502|アサヒ

- 4345|シーティーエス

- 7259|アイシン

- 7646|PLANT

- 8362|福井銀

- 135A|G-VRAIN

- 4578|大塚HD

- 1964|中外炉

- 3116|トヨタ紡織

- 4045|東亜合

- 4620|藤倉化

- 4826|CIJ

- 6302|住友重

- 8014|蝶理

- 8053|住友商

- 8524|北洋銀行

- 8708|アイザワ証G

- 9412|スカパーJSAT

- 5482|愛知鋼

- 4728|トーセ

- 6301|コマツ

- 8334|群馬銀

- 1941|中電工

- 284A|P-フクヤ建設

- 6473|ジェイテクト

- 7919|野崎印

- 9539|京葉瓦斯

- 162A|AIセレクトETN

- 2130|メンバーズ

- 2175|SMS

- 2212|山崎パン

- 2305|スタジオアリス

- 2359|コア

- 2469|ヒビノ

- 265A|G-エイチエムコム

- 2664|カワチ薬品

- 2972|R-サンケイRE

- 3070|G-ジェリービーンズ

- 3358|Trailhead

- 3426|アトムリビン

- 3439|三ツ知

- 3622|ネットイヤー

- 3911|G-Aiming

- 3964|オークネット

- 3969|エイトレッド

- 4063|信越化

- 4479|G-マクアケ

- 4812|電通総研

- 5532|G-リアルゲイト

- 6360|東自機

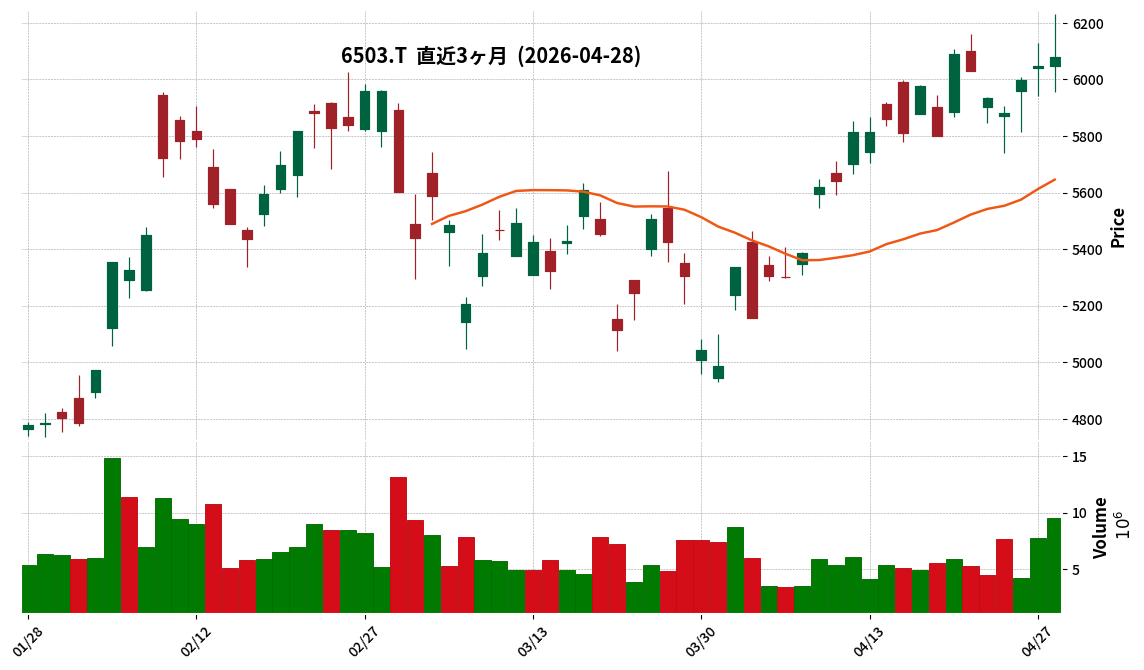

- 6503|三菱電

- 6702|富士通

- 6586|マキタ

- 1418|インターライフ

- 2491|Vコマース

- 432A|P-クリニファー

- 4661|OLC

- 4722|フューチャー

- 4755|楽天グループ

- 5819|カナレ電気

- 5279|日本興業

- 7148|FPG

- 9560|G-プログリット

- 5903|SHINPO

- 2162|nms HD

- 274A|ガーデン

- 3547|ユニシアHD

- 3835|eBASE

- 5893|P-RAVIPA

- 7236|ティラド

- 4375|G-セーフィー

4043|トクヤマ

3897.0

▲ +3.01%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tokuyama Corporation announced its consolidated financial results for the fiscal year ended March 31, 2026.

- For the fiscal year 2026, consolidated net sales were ¥349,476 million (up 1.9% year-on-year), operating income was ¥37,017 million (up 23.5% year-on-year), and ordinary income was ¥38,203 million (up 29.1% year-on-year).

- Net profit attributable to owners of parent for the same period was ¥22,205 million (down 5.1% year-on-year).

- The annual dividend for the fiscal year ended March 31, 2026, was increased to ¥120.00, compared to ¥100.00 in the previous fiscal year.

- The consolidated earnings forecast and annual dividend forecast for the fiscal year ending March 31, 2027, have been announced as undetermined due to the difficulty of making reasonable calculations at this time.

🤖 AI Perspective

The financial results show a robust increase in operating and ordinary income despite a modest rise in net sales for FY2026, while net profit attributable to owners of parent declined. This divergence may suggest significant impacts from non-operating items, extraordinary gains/losses, or tax expenses during the period. The undetermined outlook for FY2027 earnings and dividends could indicate the company’s cautious stance amid current market uncertainties, making future announcements worth monitoring.

1458|楽天225ダブルブル

71980.0

▼ -0.68%

📎 Source:楽天225ダブルブル Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Rakuten ETF-Nikkei Leveraged Index (Code 1458) announced its financial results for the fiscal year ended March 2026 (March 16, 2025, to March 15, 2026).

- Total net assets for the period amounted to JPY 45,447 million, a decrease from JPY 61,140 million at the end of the previous fiscal year.

- The net asset value per 100 units reached JPY 5,688,033, marking a significant increase from JPY 2,859,185 at the end of the prior period.

- Net income for the period was JPY 15,652 million (JPY 15,652,755,063), a substantial increase from JPY 1,360 million (JPY 1,360,107,302) in the previous period.

- No distribution was paid for the current period, consistent with the previous period.

🤖 AI Perspective

- While total net assets decreased, the substantial rise in net asset value per 100 units is a key highlight. This could suggest that a significant increase in net income, primarily driven by gains from derivatives transactions, outweighed the decrease in outstanding units, contributing to the uplift in per-unit value.

- The fund’s performance appears to be strongly influenced by the movements of its benchmark, the Nikkei Average Leveraged Index, and the outcomes of its related derivative transactions.

7213|レシップHD

471.0

▼ -0.42%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Lecip Holdings has revised its consolidated earnings forecast for the full fiscal year ending March 2026 (April 1, 2025, to March 31, 2026). While net sales are expected to decrease by ¥200 million to ¥23,800 million (△0.8%) from the previous forecast, operating income is projected to increase by ¥100 million to ¥1,200 million (+9.1%), ordinary income by ¥400 million to ¥1,500 million (+36.4%), and net income attributable to owners of parent by ¥300 million to ¥1,100 million (+37.5%), all representing upward revisions.

- The primary reasons for the earnings revision include stronger-than-expected demand in the domestic bus and railway market within the main transport equipment business, improved profitability due to continuous cost reductions, and foreign exchange gains (non-operating income) resulting from a weaker yen than anticipated.

- The annual dividend forecast for the fiscal year ending March 2026 has also been revised, with the year-end dividend increased by ¥4 from the previously announced ¥20.00 per share to ¥24.00 per share, making the total annual dividend ¥24.00.

- This dividend forecast revision is based on the expectation that net income attributable to owners of parent will exceed the initial public forecast.

- The company’s dividend policy has also been modified, with the target level for the Dividend on Equity (DOE) ratio, a key shareholder return indicator, raised from the previous “2% or more” to “3% or more.” This change will apply from the year-end dividend for the fiscal year ending March 2026.

🤖 AI Perspective

Lecip Holdings’ revised consolidated earnings forecast highlights a significant increase in profit, despite a slight decrease in net sales, driven by robust domestic business performance, cost reductions, and foreign exchange gains. The 37.5% increase in net income attributable to owners of parent compared to the previous forecast may suggest an improvement in profitability. Furthermore, the upward revision of the dividend forecast and the increase in the target DOE ratio could be interpreted as a strengthening of the company’s proactive stance on shareholder returns.

9040|大宝運

—

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 2026 (March 21, 2025 to March 20, 2026), net sales increased by 4.2% to JPY 8,084 million, operating profit increased by 31.0% to JPY 321 million, and ordinary profit increased by 28.2% to JPY 332 million.

- Net income for the same period decreased by 33.0% to JPY 204 million.

- For the fiscal year ending March 2027, the company forecasts net sales of JPY 8,300 million (up 2.7% year-on-year), while expecting operating profit of JPY 280 million (down 12.9%), ordinary profit of JPY 300 million (down 9.9%), and net income of JPY 190 million (down 7.0%).

- The annual dividend is planned to be maintained at JPY 100.00 (JPY 50.00 interim, JPY 50.00 year-end) for both FY2026 (actual) and FY2027 (forecast).

- As of the end of March 2026, total assets stood at JPY 9,854 million, net assets at JPY 6,832 million, and the equity ratio at 69.3%. Cash and cash equivalents at period-end amounted to JPY 2,560 million.

🤖 AI Perspective

For the fiscal year ended March 2026, improved revenue and profits, excluding net income, appear to have been driven by pricing negotiations, new business development, and operational improvements. The decline in net income, despite increases in operating and ordinary profits, may warrant closer examination by investors. While the company projects increased revenue but decreased profits for FY2027, its commitment to maintaining the annual dividend could suggest a stable approach to shareholder returns.

6902|デンソー

1917.0

▲ +1.78%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- DENSO Corporation announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- For the fiscal year, revenue was ¥7,539,975 million (up 5.3% year-on-year), operating profit was ¥552,538 million (up 6.5%), and profit attributable to owners of the parent was ¥443,755 million (up 5.9%).

- The annual dividend for the fiscal year ended March 31, 2026, including a year-end dividend of ¥35.00, totaled ¥67.00 per share (compared to ¥64.00 for the prior fiscal year).

- For the fiscal year ending March 31, 2027 (April 1, 2026 – March 31, 2027), DENSO forecasts revenue of ¥7,670,000 million (up 1.7% year-on-year), but expects operating profit to decrease to ¥500,000 million (down 9.5%) and profit attributable to owners of the parent to ¥382,000 million (down 13.9%).

- By segment, revenue in Japan increased to ¥4,404.1 billion (up 4.5%), North America to ¥2,025.1 billion (up 8.7%), and Europe to ¥767.9 billion (up 6.8%).

🤖 AI Perspective

The fiscal year ended March 31, 2026, saw an increase in both revenue and profit across key financial metrics, alongside a higher annual dividend. However, the forecast for the fiscal year ending March 31, 2027, projects a decrease in operating profit and profit attributable to owners of the parent, despite an anticipated increase in revenue. This outlook suggests that investors may closely monitor the company’s strategies to address future business conditions and cost fluctuations, particularly given the reported decline in operating profit for the Japan segment.

5834|G-SBIリーシング

2743.0

▲ +3.90%

📎 Source:G-SBIリーシング Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-SBI Leasing Service Co., Ltd. has resolved to pay a year-end dividend of JPY 180.00 per share for the fiscal year ended March 31, 2026.

- This dividend amount represents an increase of JPY 15.00 per share from the company’s most recent dividend forecast of JPY 165.00, published on January 29, 2026.

- The total dividend amount is JPY 1,433 million, with an effective date of June 26, 2026.

- Consequently, the total annual dividend for the fiscal year ending March 2026 will be JPY 230.00 per share, combining the JPY 50.00 second-quarter dividend (compared to JPY 170.00 for the previous year).

- The stated per-share dividend amount is prior to the 2-for-1 stock split implemented on April 1, 2026.

🤖 AI Perspective

G-SBI Leasing’s decision to increase its year-end dividend beyond the most recent forecast may suggest a strong commitment to shareholder returns. This move aligns with the company’s stated policy of aiming for a consolidated dividend payout ratio of 30% or more, potentially reflecting confidence in its earnings growth and financial stability. Investors might view this as a positive sign regarding the company’s future performance and dividend policy consistency.

8609|岡三

920.0

▲ +3.25%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, consolidated net income attributable to owners of the parent increased by 83.3% year-on-year to ¥21,360 million.

- Consolidated operating revenue was ¥95,595 million (up 16.7% year-on-year), consolidated operating income was ¥18,730 million (up 45.9% year-on-year), and consolidated ordinary income was ¥22,867 million (up 46.8% year-on-year).

- The annual dividend for the fiscal year ended March 31, 2026, was set at ¥50.00, an increase from ¥30.00 in the previous fiscal year. This includes an ordinary dividend of ¥40.00 and a special dividend of ¥10.00.

- As of March 31, 2026, consolidated total assets stood at ¥1,401,090 million, consolidated net assets at ¥230,972 million, and the equity ratio at 16.5%.

- The consolidated earnings forecast for the fiscal year ending March 31, 2027, has not been disclosed due to the difficulty in forecasting performance, as the financial instruments business is susceptible to market fluctuations.

🤖 AI Perspective

Okasan’s financial results for the fiscal year ended March 31, 2026, highlight significant growth across key revenue and profit metrics. The substantial 83.3% increase in net income attributable to owners of the parent may suggest a notable improvement in the company’s profitability. Furthermore, the increase in the annual dividend to ¥50 from the previous year’s ¥30 could be viewed as a positive indicator of shareholder returns. However, the non-disclosure of the FY2027 earnings forecast, attributed to market volatility inherent in the financial instruments business, means future market conditions will be a key factor for investors to monitor.

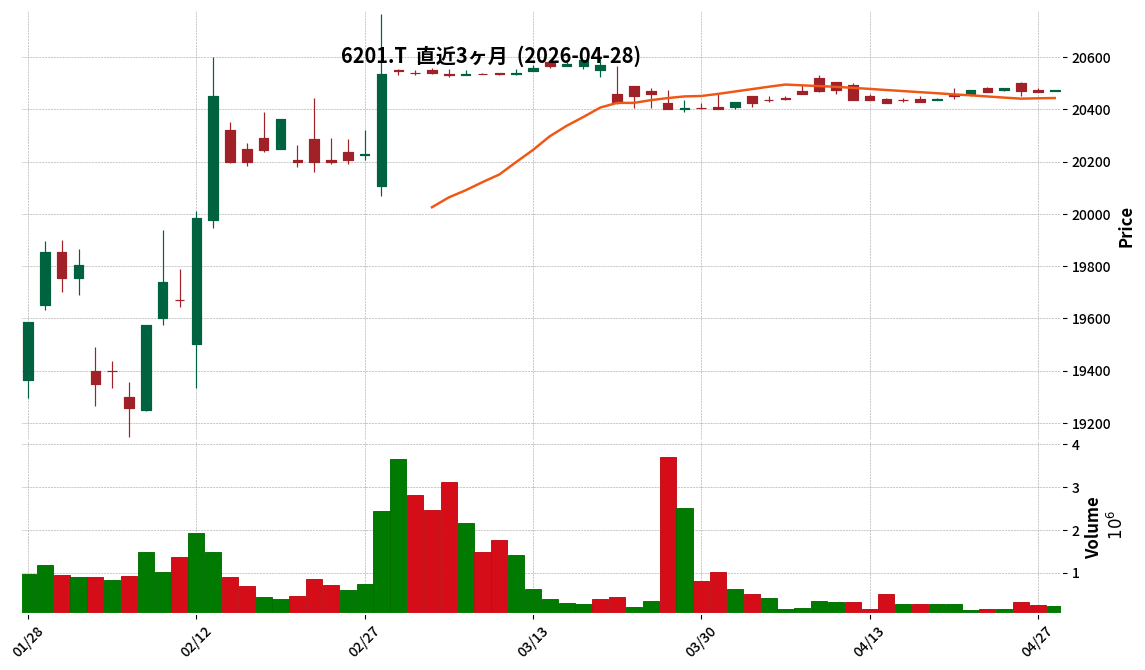

6201|豊田織

20475.0

▲ +0.05%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, consolidated net sales were ¥4,369,512 million, representing a 7.0% increase year-on-year.

- Consolidated operating profit for the same period was ¥137,023 million (a 38.2% decrease year-on-year), and profit attributable to owners of the parent was ¥223,785 million (a 14.7% decrease year-on-year).

- The annual dividend per share was ¥0.00, down from ¥280.00 in the previous fiscal year, attributed to the company’s shares being scheduled for delisting on June 1, 2026.

- Consolidated financial forecasts and dividend forecasts for the fiscal year ending March 31, 2027, were not provided due to the planned delisting.

- During the fiscal year, Aichi Corporation was excluded from the scope of consolidation.

🤖 AI Perspective

While net sales increased, factors such as increased engine certification-related expenses, personnel costs, U.S. tariffs, and research and development expenses are indicated as contributing to the decrease in operating profit. However, compared to the initial forecasts, the company exceeded its projections for net sales and various profit metrics, driven by a weaker yen than anticipated and robust production and sales in the industrial vehicles and automotive segments. The upcoming delisting means a change in information disclosure practices for investors, which is a noteworthy development for market transparency.

6029|アトラG

203.0

▲ +14.69%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Artra Group Inc. signed a Memorandum of Understanding (MOU) for a business alliance with Remed Co., Ltd. (REMED), a KOSDAQ-listed Korean medical device manufacturer, on April 21, 2026, with formal approval on April 28, 2026.

- The alliance aims to establish a foundation for mutual cooperation between REMED and Artra Group across all business sectors, including medical, rehabilitation, and beauty device fields.

- REMED specializes in the development, manufacturing, and sales of non-invasive magnetic field therapy devices, such as Transcranial Magnetic Stimulation (TMS), Neuromuscular Magnetic Stimulation (NMS), and Extracorporeal Shock Wave Therapy (ESWT).

- Artra Group plans to integrate REMED’s advanced technologies with its A-COMS platform, which supports 3,053 acupuncture and osteopathic clinics nationwide (as of December 2025), to offer new value in brain rehabilitation, chronic pain, and aesthetic fields.

- The MOU is valid for one year from the signing date (April 21, 2026) and is not legally binding; specific cooperation details will be defined in separate written agreements.

🤖 AI Perspective

This announcement by Artra Group appears to be a strategic move to enhance its value-added services in the non-insured (private pay) sector, driven by Japan’s aging population and healthcare cost containment trends. The combination of REMED’s advanced non-invasive magnetic therapy device technology with Artra Group’s extensive customer network could lead to new service offerings and expanded business domains. Investors may wish to monitor the progress of future detailed discussions and the signing of definitive agreements, as the current understanding is an MOU without legal enforceability.

8613|丸三証

1030.0

▲ +0.49%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026), Marusan Securities reported operating revenue of ¥21,725 million (up 15.3% year-on-year), operating income of ¥5,375 million (up 51.0%), ordinary income of ¥5,923 million (up 44.0%), and net income of ¥5,010 million (up 10.8%).

- Earnings per share increased to ¥75.66 from ¥68.40 in the previous fiscal year.

- The annual dividend per share was raised by ¥10 to ¥70.00 (interim ¥32, year-end ¥38). The payout ratio stood at 92.5%, and the dividend on equity ratio was 9.4%.

- Regarding the financial position, total assets at the end of the period were ¥88,476 million, and net assets were ¥51,444 million. The equity ratio was 58.0%, and the capital adequacy ratio was 576.9%.

- Stock brokerage fees increased by 36.3% to ¥7,298 million, and the net increase in Japanese stocks (recommended individual stocks) under the medium-term management plan reached ¥52.3 billion over 24 months, achieving 130.8% of its target.

🤖 AI Perspective

The substantial increase in profits for the period appears to be primarily driven by a rise in stock brokerage fees and investment trust commissions. Strategic initiatives, such as focusing on AI-related stocks and underwriting new IPOs, likely contributed significantly to this revenue growth. The high dividend payout ratio suggests a strong commitment to shareholder returns, while the healthy capital adequacy ratio indicates a stable financial foundation.

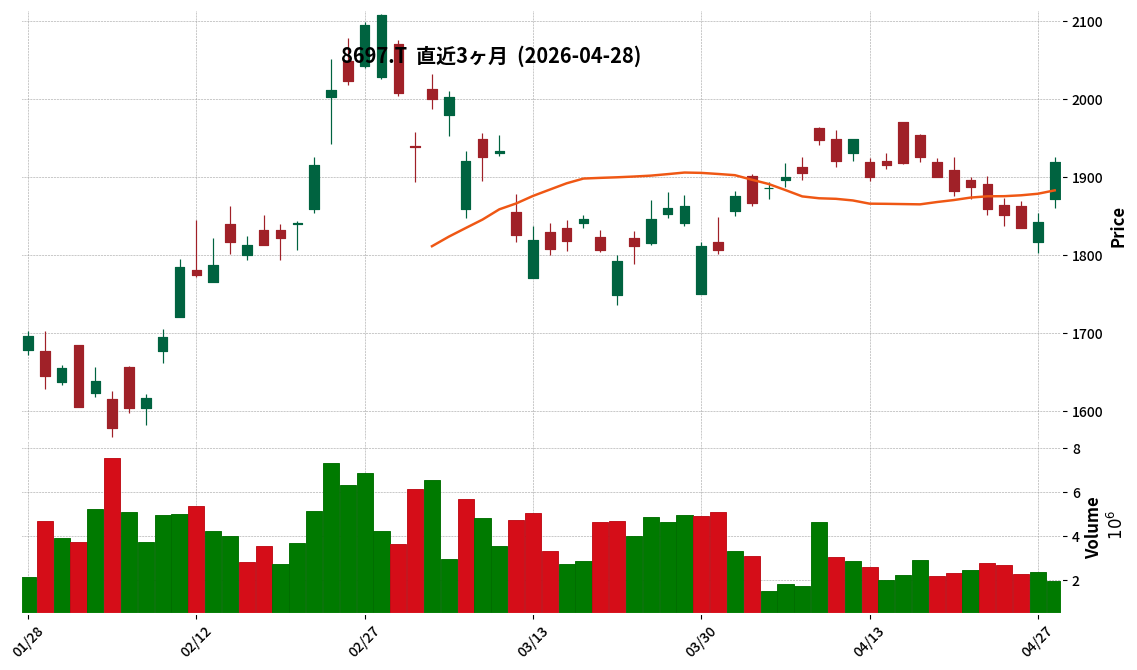

8697|JPX

1920.0

▲ +4.21%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, Japan Exchange Group, Inc. (JPX) reported consolidated operating revenue of ¥198,735 million, an increase of 22.5% year-on-year. Profit attributable to owners of parent rose by 29.5% to ¥79,139 million.

- Basic earnings per share (EPS) for FY2026 was ¥76.81.

- The annual dividend for FY2026 was set at ¥61.00 per share (¥25.00 interim, ¥36.00 year-end), with a total dividend payment of ¥62,938 million.

- For the fiscal year ending March 31, 2027, JPX forecasts consolidated operating revenue of ¥205.0 billion (up 3.2% year-on-year) but anticipates profit attributable to owners of parent to be ¥77.5 billion (down 2.1% year-on-year). Basic EPS is projected to be ¥75.39.

- A 2-for-1 stock split was implemented effective October 1, 2024. Per-share figures, including basic EPS, are calculated assuming the split occurred at the beginning of the previous consolidated fiscal year.

🤖 AI Perspective

- The significant increase in operating revenue and profits for FY2026 appears to be driven by factors such as higher transaction-related revenues.

- The forecast for FY2027 suggests continued growth in operating revenue, yet a slight decline in profit attributable to owners of parent is projected, which may warrant monitoring by investors regarding the future profit structure.

- The company’s commitment to shareholder returns is indicated by the proposed annual dividend of ¥61.00 for FY2027, maintaining the same level as the FY2026 actual dividend.

8914|エリアリンク

1121.0

▲ +2.56%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Arealink Co., Ltd. announced its non-consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1 to March 31, 2026).

- For the quarter, net sales were ¥7,144 million (down 5.0% year-on-year), operating income was ¥1,571 million (up 0.5%), ordinary income was ¥1,415 million (down 5.3%), and net income attributable to owners of parent was ¥1,006 million (down 9.6%).

- By business segment, the Storage Business reported net sales of ¥6,079 million (down 4.4%) but operating income of ¥1,683 million (up 0.1%), and the Land Rights Adjustment Business recorded net sales of ¥681 million (down 12.3%) with operating income of ¥134 million (up 36.4%).

- As of the end of the first quarter, total assets stood at ¥65,441 million, net assets at ¥29,574 million, and the equity ratio was 45.2%.

- The full-year and second-quarter consolidated earnings forecasts for the fiscal year ending December 2026, as well as the annual dividend forecast (¥26.50), remain unchanged from the most recently announced figures.

🤖 AI Perspective

- While net sales decreased in the first quarter, the core Storage Business and Land Rights Adjustment Business achieved reduced revenue but increased profits, leading to an overall increase in operating income compared to the prior year.

- This performance may suggest that improved precision in store openings and efficient advertising in the Storage Business, along with a focus on acquiring quality properties in the Land Rights Adjustment Business, contributed to enhanced profitability.

- The unchanged full-year earnings forecast could indicate that the company views its progress against initial plans as generally on track.

1934|ユアテック

2744.0

▲ +5.54%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026 (consolidated), net sales were ¥252,262 million, a decrease of 1.9% year-on-year.

- Operating profit for the same period increased by 11.4% to ¥18,038 million, and ordinary profit rose by 9.2% to ¥18,901 million.

- Net income attributable to owners of parent amounted to ¥10,325 million, a decrease of 13.8% from the previous fiscal year.

- The equity ratio stood at 67.8% at the end of the period, an increase from 63.2% at the end of the previous fiscal year.

- The annual dividend for FY2026 was ¥72.00 (interim ¥36.00, year-end ¥36.00), an increase from ¥68.00 in the previous fiscal year.

- For the fiscal year ending March 31, 2027 (consolidated), the company forecasts net sales of ¥273,000 million (up 8.2% year-on-year), operating profit of ¥18,900 million (up 4.8% year-on-year), and net income attributable to owners of parent of ¥13,200 million (up 27.8% year-on-year).

🤖 AI Perspective

Despite a slight decrease in net sales for FY2026, Yurtec reported an increase in operating and ordinary profits, which may suggest improvements in operational efficiency. While net income attributable to owners of parent declined, the rise in the equity ratio could indicate a strengthened financial position. The increased annual dividend and the forecast for growth in both sales and profits for FY2027 are aspects that investors might find noteworthy.

6592|マブチモーター

1618.5

▲ +1.51%

📎 Source:マブチモーター Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Mabuchi Motor Co., Ltd. reported consolidated net sales of JPY 50,373 million for the first quarter of the fiscal year ending December 2026 (January 1 to March 31, 2026), marking a 7.3% increase year-on-year.

- During the same period, consolidated operating profit decreased by 15.4% year-on-year to JPY 5,395 million. However, ordinary profit surged by 66.8% to JPY 7,918 million, and net income attributable to owners of parent significantly increased by 74.4% to JPY 5,801 million.

- Basic earnings per share for the quarter stood at JPY 23.62, calculated after accounting for a 2-for-1 stock split of common shares effective January 1, 2026.

- In this consolidated cumulative quarter, 13 new companies, including Mabuchi Motor NPM Corporation (formerly Nippon Pulse Motor Co., Ltd.), were added to the scope of consolidation.

- The consolidated full-year earnings forecast for the fiscal year ending December 2026 and the annual dividend forecast of JPY 56.00 remain unchanged from the most recently announced figures.

🤖 AI Perspective

The observation that net sales increased while operating profit declined, yet ordinary profit and net income attributable to owners of parent rose significantly, presents a notable point. This could indicate that factors such as improved foreign exchange gains or the contributions from newly consolidated subsidiaries played a substantial role in the overall profitability. The unchanged full-year earnings forecast suggests that management’s existing outlook may already factor in these recent performance dynamics.

8624|いちよし

1379.0

▲ +0.88%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Ichiyoshi Securities announced on April 28, 2026, a revision to its year-end ordinary dividend forecast for the fiscal year ending March 2026.

- The revised year-end ordinary dividend forecast is ¥49 per share, an increase of ¥1 from the previously announced ¥48 (announced on March 18, 2026).

- The reason for the dividend increase is an upward revision in the earnings forecast, which serves as the basis for the consolidated payout ratio (approximately 50%), in line with the company’s dividend policy.

- The total annual dividend for the fiscal year ending March 2026 is projected to be ¥89 per share, comprising an interim dividend of ¥30 (¥20 ordinary, ¥10 commemorative) and a year-end dividend of ¥59 (¥49 ordinary, ¥10 commemorative).

- The final decision on the year-end dividend is scheduled to be made at the Board of Directors meeting concerning the year-end financial results, expected in mid-May 2026.

🤖 AI Perspective

This announcement indicates that Ichiyoshi Securities is adjusting its year-end dividend forecast upward in response to an improved earnings outlook, consistent with its dividend policy of targeting a consolidated payout ratio of approximately 50%. This action may suggest the company’s commitment to shareholder returns aligned with its performance. Investors might monitor the company’s continued adherence to this policy and future earnings trends as key points.

1777|川崎設備

—

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 2026, Kawasaki Setsubi reported non-consolidated net sales of ¥37,652 million (up 29.1% year-on-year), operating profit of ¥4,904 million (up 80.8%), ordinary profit of ¥4,986 million (up 82.4%), and net profit of ¥3,684 million (up 88.1%).

- Operating profit, ordinary profit, and net profit all reached record highs.

- The annual dividend per share increased from ¥50 in the previous fiscal year to ¥95 (¥50 ordinary dividend, ¥45 special dividend).

- For the fiscal year ending March 2027, the company forecasts net sales of ¥39,000 million (up 3.6% year-on-year), operating profit of ¥5,000 million (up 1.9%), and ordinary profit of ¥5,060 million (up 1.5%).

- The equity ratio at the end of the period stood at 62.1%, an increase from 54.9% at the end of the previous fiscal year.

🤖 AI Perspective

Kawasaki Setsubi achieved significant profit growth across all key metrics in FY2026, with operating, ordinary, and net profits reaching record highs. This performance can be attributed to increased orders and completed construction in all project types and segments. The substantial increase in the annual dividend payment may suggest a strong commitment to shareholder returns. The company’s forecast for continued revenue and profit growth in the next fiscal year indicates an expectation of ongoing business expansion.

2502|アサヒ

1555.5

▲ +1.53%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Asahi Group Holdings announced that its consolidated subsidiary, Asahi Holdings (Australia) Pty Ltd, disclosed its financial results for the fiscal year ended December 2025 on April 28, 2026.

- The parent company, Asahi Group Holdings, has postponed the announcement of its FY2025 results due to the impact of a cyberattack that occurred on September 29, 2025.

- Asahi Holdings (Australia) Pty Ltd reported sales of AUD 5,335 million (JPY 514,816 million), operating profit of AUD 739 million (JPY 71,283 million), and net profit of AUD 508 million (JPY 48,948 million for the fiscal year from January 1, 2025, to December 31, 2025).

- Compared to the reference FY2024, sales in AUD increased from AUD 5,210 million, while operating profit decreased from AUD 778 million and net profit decreased from AUD 552 million.

- This disclosure was made in accordance with local regulations, specifically the Australian Accounting Law (simplified disclosure standards) and the Corporations Act 2001, and is available for viewing at the Australian Securities and Investments Commission.

🤖 AI Perspective

- The disclosure of specific financial results for the Australian consolidated subsidiary provides some insight for investors, especially as the parent company’s overall FY2025 results remain delayed due to the cyberattack.

- While the Australian subsidiary’s sales increased, the decline in operating and net profits could indicate various factors such as currency fluctuations, changes in the business environment, or increased costs, warranting further analysis once comprehensive results are available.

- The announcement that the parent company’s full financial disclosure date will be promptly released suggests that investors will continue to monitor for the complete picture of Asahi Group Holdings’ performance.

4345|シーティーエス

898.0

▲ +1.13%

📎 Source:シーティーエス Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- CTS Corporation reported consolidated financial results for the fiscal year ended March 31, 2026, with net sales of ¥12,747 million (up 7.8% year-on-year), operating income of ¥3,369 million (up 9.5%), ordinary income of ¥3,734 million (up 18.1%), and profit attributable to owners of parent of ¥2,686 million (up 22.7%).

- Profitability ratios improved, with an operating profit margin of 26.4% (vs. 26.0% prior year), ordinary income to total assets of 19.8% (vs. 18.7%), and profit attributable to owners of parent to equity of 18.8% (vs. 17.5%).

- The annual dividend for the fiscal year ended March 31, 2026, was ¥29 (interim ¥14, year-end ¥15), an increase of ¥4 from the previous fiscal year, with a payout ratio of 44.6%.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥13,500 million (up 5.9% year-on-year), operating income of ¥3,530 million (up 4.8%), ordinary income of ¥3,890 million (up 4.2%), and profit attributable to owners of parent of ¥2,720 million (up 1.2%).

- The forecast for the fiscal year ending March 31, 2027, includes an annual dividend of ¥30 (interim ¥15, year-end ¥15).

🤖 AI Perspective

The strong performance for the fiscal year ended March 31, 2026, with increased sales and all profit metrics, suggests robust operational execution. The more than 20% growth in profit attributable to owners of parent indicates a notable enhancement in earnings power. Furthermore, the improvement in key profitability ratios, such as the operating profit margin, is noteworthy.

The increase in the annual dividend for the current fiscal year and the forecast for a further increase in the next fiscal year could reflect the company’s commitment to shareholder returns, supported by its profit growth. This performance may also be linked to the company’s strategic shift outlined in its mid-term management plan, transitioning from a “hardware rental IT infrastructure company” to a “construction ICT specialist providing integrated data and information services.”

7259|アイシン

2351.0

▲ +6.52%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- AISIN Corporation reported consolidated revenue of 5,117,764 million JPY for the fiscal year ended March 31, 2026, marking a 4.5% increase year-on-year.

- Operating profit for the same period stood at 228,796 million JPY, up 12.7% from the previous fiscal year, with profit attributable to owners of the parent significantly rising by 59.6% to 171,697 million JPY.

- The annual dividend per share for FY2026 was 70 JPY (30 JPY interim, 40 JPY year-end), and the forecast for FY2027 annual dividend per share is 75 JPY (35 JPY interim, 40 JPY year-end).

- For the fiscal year ending March 31, 2027, the company forecasts consolidated revenue of 5,250,000 million JPY (a 2.6% increase) and operating profit of 235,000 million JPY (a 2.7% increase).

- AISIN executed a 3-for-1 stock split of its common shares effective October 1, 2024, and resolved on April 28, 2026, to acquire treasury shares, conduct a tender offer for treasury shares, and cancel treasury shares.

🤖 AI Perspective

The strong growth in both revenue and profit for FY2026, especially the substantial increase in profit attributable to owners of the parent, may draw investor attention. While the company forecasts continued revenue and operating profit growth for FY2027, the projected decrease in profit attributable to owners of the parent could indicate the impact of share buybacks and cancellations, among other factors. The dividend payout ratio of 30.1% suggests a commitment to shareholder returns, which investors might consider as part of the company’s financial strategy.

7646|PLANT

1807.0

▼ -0.17%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first half of the fiscal year ending September 2026, PLANT reported net sales of ¥47,555 million (down 1.5% year-on-year), operating profit of ¥891 million (down 9.0%), and interim net profit of ¥657 million (down 12.5%).

- The interim dividend forecast for FY2026 is ¥40 per share, with an annual dividend forecast of ¥95 (¥55 at year-end), representing an increase from the previous year’s actual annual dividend of ¥75.

- The full-year forecast was revised to net sales of ¥95,500 million (down 2.3% from the previous period), operating profit of ¥1,500 million (down 25.2%), and net profit of ¥1,100 million (down 18.3%).

- As of the end of the interim period, total assets were ¥35,804 million, net assets ¥15,690 million, and the equity ratio was 43.8%.

- The full-year performance forecast has been revised from the most recently published forecast.

🤖 AI Perspective

The interim financial results show a decrease in net sales and various profit indicators compared to the previous year. The downward revision of the full-year sales and profit forecasts may suggest a recalibration of expectations regarding the business environment or operational performance. Conversely, the annual dividend forecast remains higher than the prior year’s actual dividend, which could indicate a continued commitment to shareholder returns.

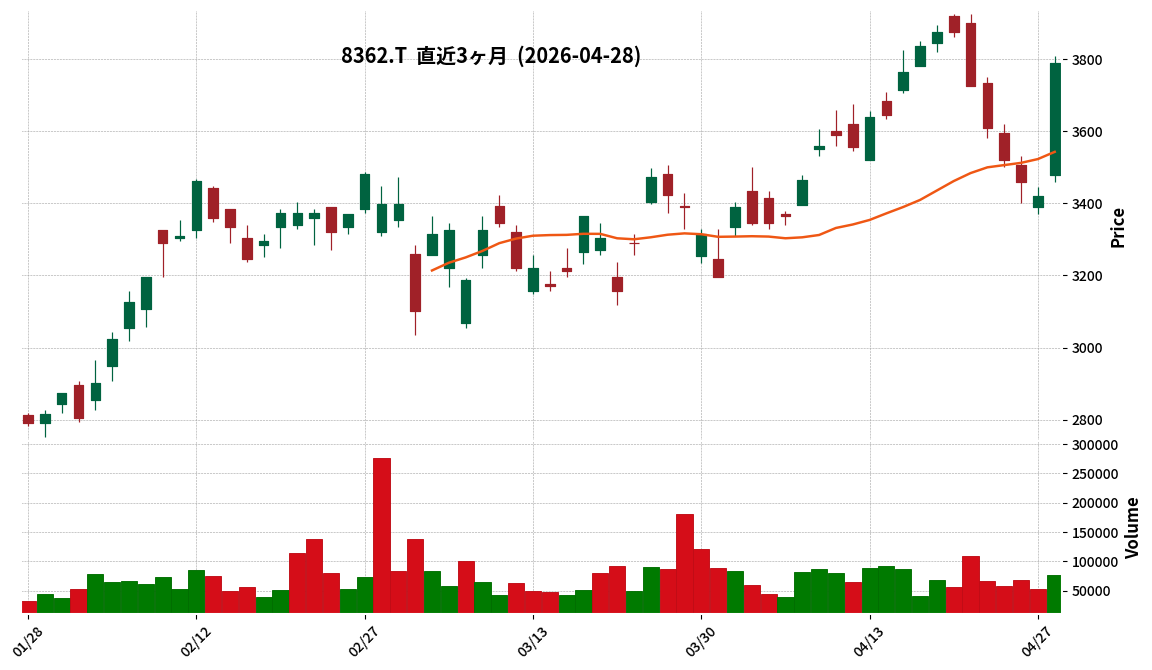

8362|福井銀

3790.0

▲ +10.82%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Fukuibank Co., Ltd. announced on April 28, 2026, a revision to its consolidated earnings forecast and dividend forecast for the fiscal year ending March 2026 (April 1, 2025 – March 31, 2026).

- The consolidated ordinary profit forecast was revised upwards by 27.6% from the previously announced JPY 10,500 million to JPY 13,400 million.

- The consolidated net profit attributable to owners of parent forecast was revised upwards by 43.3% from the previously announced JPY 6,000 million to JPY 8,600 million. This adjusts the earnings per share from JPY 253.49 to JPY 363.57.

- Key reasons for the earnings revision include solid performance in lending interest due to improved lending rates, increased interest and dividends from investment securities through portfolio restructuring, and recording of gains on sales of shares, including strategic shareholdings.

- The annual dividend per share forecast for the fiscal year ending March 2026 was revised from JPY 75.00 to JPY 108.00 (the year-end dividend was revised from JPY 46.00 to JPY 79.00). This revision is based on the upward revision of net profit and the bank’s shareholder return policy (payout ratio of approximately 30%).

🤖 AI Perspective

- Fukuibank’s upward revision of its consolidated earnings forecast for the fiscal year ending March 2026 appears to be driven by improved lending interest income, increased returns from securities, and gains from share sales.

- The simultaneous announcement of an increased annual dividend forecast is likely a direct result of the improved earnings outlook, aligned with the company’s shareholder return policy.

- These revisions could be seen as reflecting positive developments in the bank’s revenue streams and a commitment to shareholder returns.

135A|G-VRAIN

3295.0

▼ -2.08%

📎 Source:G-VRAIN Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-VRAIN Solutions Inc. (Code: 135A) announced the release of its full-year FY2026 earnings presentation video and a summary of the Q&A session on April 28, 2026.

- The company stated that it anticipates recurring customer sales to constitute approximately 50% of total sales in FY2027, even while accelerating new customer acquisition.

- Implementation of AI external inspection systems is significantly expanding beyond the food industry, with an increasing trend observed across diverse sectors such as automotive (particularly in the Nagoya region), pharmaceutical, steel, and paper.

- For international expansion, the strategy is to first advance into Asia (e.g., Thailand, Vietnam), building on numerous existing installation successes at overseas factories of Japanese clients. International sales have not been conservatively included in the current fiscal year’s performance forecast.

- Regarding shareholder returns, the company indicated that funds are currently prioritized for growth investments to capture the large manufacturing market, and retained earnings will be prioritized for the time being.

🤖 AI Perspective

The projected recurring customer sales ratio of approximately 50% for FY2027 could suggest increasing stability in the company’s business model. The expanding adoption of AI visual inspection systems beyond the food industry into diverse sectors like automotive and pharmaceutical indicates a broader market opportunity for the company’s solutions. Furthermore, the strategic focus on international expansion, particularly in the Asian market, is positioned as a future growth engine, potentially offering new avenues for business development.

4578|大塚HD

10660.0

▲ +0.14%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of fiscal year 2026 (January 1, 2026 – March 31, 2026), consolidated net sales increased by 8.2% year-on-year to JPY 630,342 million.

- Profit attributable to owners of the parent for the quarter rose by 15.7% year-on-year, reaching JPY 98,348 million.

- Sales growth in the pharmaceutical segment was notably driven by core products such as the antipsychotic “Rexulti,” the anticancer agent “Lonsurf,” and the anti-APRIL antibody “Voizact” (launched in 2025).

- The nutraceuticals segment also experienced increased sales across all three social challenge categories designated as growth drivers.

- The consolidated full-year earnings forecast for fiscal year 2026 and the annual dividend forecast of JPY 140.00 remain unchanged from the figures most recently announced.

🤖 AI Perspective

The significant growth in Q1 net sales and profit attributable to owners of the parent may suggest robust performance in core business segments, particularly in pharmaceuticals with key products and consistent growth in nutraceuticals. While the full-year forecast remains unchanged, the sustained investment in research and development could indicate a strategic focus on future pipeline expansion. Investors may continue to monitor how these factors contribute to future quarterly results against the maintained full-year guidance.

1964|中外炉

4180.0

▲ +2.58%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the consolidated fiscal year ended March 31, 2026, Chugai Ro reported net sales of ¥37,332 million (up 3.0% year-on-year), operating profit of ¥2,879 million (up 5.3%), and ordinary profit of ¥3,110 million (up 3.6%).

- Profit attributable to owners of parent increased by 55.7% year-on-year to ¥4,668 million.

- Diluted earnings per share were ¥643.70, and the equity ratio stood at 60.8%.

- The annual dividend for the fiscal year ended March 31, 2026, is ¥166.00 per share, an increase from ¥150.00 in the previous fiscal year.

- The consolidated forecast for the fiscal year ending March 31, 2027, projects net sales of ¥40,300 million (up 7.9%) and operating profit of ¥3,620 million (up 25.7%), while profit attributable to owners of parent is expected to decrease by 46.1% to ¥2,516 million. An annual dividend of ¥180.00 per share is planned for the next fiscal year.

🤖 AI Perspective

The significant increase in net profit for the fiscal year ended March 31, 2026, appears to be primarily driven by gains from the sale of strategic shareholdings, a factor that may not recur in future periods. The company’s improved equity ratio to 60.8% could indicate a strengthening of its financial position. While the forecast for the upcoming fiscal year shows continued growth in sales and operating profit, the projected decline in net profit attributable to owners of parent suggests a normalization of earnings after the one-off gains. The planned increase in the dividend for FY2027/3 may be viewed as a continued commitment to shareholder returns.

3116|トヨタ紡織

2393.5

▲ +1.96%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Toyota Boshoku Corporation announced consolidated revenue of ¥2,037,063 million for the fiscal year ended March 31, 2026, an increase of 4.2% year-over-year.

- Consolidated operating profit for the period was ¥53,948 million, up 27.2% from the previous fiscal year, while profit attributable to owners of the parent reached ¥23,271 million, an increase of 39.2%.

- Basic earnings per share for the fiscal year ended March 31, 2026, was ¥130.30.

- The annual dividend for FY2026 was ¥86.00 per share, consisting of an interim dividend of ¥43.00 and a year-end dividend of ¥43.00.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated revenue of ¥2,120,000 million (up 4.1% YoY) and operating profit of ¥80,000 million (up 48.3% YoY).

🤖 AI Perspective

The fiscal year 2026 results indicate a recovery and growth in revenue and all profit categories from the previous period, with notable increases in operating profit and profit attributable to owners of the parent. The company’s forecast for FY2027 projects continued growth in both revenue and profit, with a significant increase anticipated in operating profit, which may be a key area for investor observation.

4045|東亜合

1688.5

▼ -1.14%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Toagosei Co., Ltd. announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026 to March 31, 2026).

- Consolidated net sales amounted to ¥38,634 million (down 3.0% year-on-year), and operating profit was ¥3,206 million (down 4.7% year-on-year).

- Net profit attributable to owners of parent increased significantly to ¥2,774 million (up 38.7% year-on-year), partly due to the sale of idle real estate.

- The full-year consolidated earnings forecast (net sales ¥167,000 million, net profit attributable to owners of parent ¥11,500 million) and the annual dividend forecast (¥70) remain unchanged from the most recently announced figures.

- By segment, the High-Performance Materials business achieved a 14.8% increase in net sales and a 200.7% increase in operating profit, driven by demand for AI-related semiconductors and memory.

🤖 AI Perspective

The significant increase in net profit attributable to owners of parent, despite a decline in net sales and operating profit, appears to be influenced by non-recurring factors such as the sale of idle real estate. However, the strong performance in the High-Performance Materials segment, supported by demand from AI-related semiconductors and memory, could indicate a potential growth driver. The reaffirmation of the full-year earnings forecast may suggest the company maintains confidence in its overall business plan despite the mixed Q1 results.

4620|藤倉化

1200.0

▲ +3.99%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

1. Fujikura Kasei Co., Ltd. revised its consolidated financial forecast for the full fiscal year ending March 31, 2026. Net sales are revised from JPY 55,000 million to JPY 55,600 million, operating profit from JPY 2,000 million to JPY 2,300 million, ordinary profit from JPY 3,300 million to JPY 4,200 million, and profit attributable to owners of parent from JPY 3,000 million to JPY 4,200 million.

2. The upward revision in net sales is primarily attributed to strong sales of paints for renovation in the coatings segment. The increase in profits is due to the effect of higher sales and improved profit margins from the sale of value-added products. Additionally, ordinary profit benefited from higher-than-expected gains from the sale of cross-shareholdings.

3. The year-end dividend forecast for the fiscal year ending March 2026 has been revised upwards from JPY 9.00 per share to JPY 11.00 per share. This revision will result in an expected annual dividend of JPY 20.00 per share, including the interim dividend of JPY 9.00.

4. The dividend forecast revision is based on the updated profit forecast and the company’s 11th Medium-Term Management Plan, which aims for a total shareholder return ratio of 70% or more.

5. This matter regarding the year-end dividend will be submitted for approval at the 115th Ordinary General Meeting of Shareholders, scheduled to be held in June 2026.

🤖 AI Perspective

The upward revision of the earnings forecast suggests that Fujikura Kasei’s core coatings business is performing robustly, with higher-margin products contributing to improved profitability. The unexpected gain from cross-shareholdings also played a role in boosting ordinary profit, potentially reflecting strategic financial management. The announced dividend increase, linked to the improved profit outlook and the company’s total shareholder return target, could be viewed by investors as a positive sign regarding shareholder value commitment.

4826|CIJ

505.0

▼ -2.88%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the third quarter of fiscal year 2026 (July 1, 2025 – March 31, 2026), consolidated net sales reached ¥21,935 million, representing a 9.0% increase year-on-year.

- Operating profit for the same period increased by 27.5% to ¥2,162 million, ordinary profit rose by 27.8% to ¥2,186 million, and net profit attributable to parent company shareholders grew by 28.6% to ¥1,420 million.

- Infotech Solution Co., Ltd. was made a consolidated subsidiary on December 1, 2025, with the aim of expanding business in the public sector.

- Strong order performance in the public and energy sectors contributed to the increase in sales.

- The consolidated earnings forecast and annual dividend forecast for the full fiscal year 2026 remain unchanged from the most recently announced figures.

🤖 AI Perspective

CIJ Co., Ltd. reported significant double-digit growth in sales and all profit categories for the third quarter of fiscal year 2026. This performance may suggest that the company’s strategies to secure strong orders in key sectors, such as public and energy, along with improved cost management, are yielding positive results. The consolidation of Infotech Solution Co., Ltd. also indicates an active move towards strategic business expansion, which could contribute to future growth.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

6302|住友重

5617.0

▲ +7.38%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sumitomo Heavy Industries, Ltd. announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026, to March 31, 2026).

- For the period, consolidated net sales were ¥255,566 million (up 5.8% year-on-year), operating profit was ¥13,377 million (up 19.6% year-on-year), and net profit attributable to owners of parent was ¥7,913 million (up 21.8% year-on-year).

- By segment, the Mechatronics business recorded net sales of ¥72.4 billion (up 12% year-on-year) and operating profit of ¥6.8 billion (up 43% year-on-year). Additionally, the Energy & Lifeline segment’s orders received increased to ¥80.5 billion (up 94% year-on-year).

- The consolidated full-year forecast for FY2026 remains unchanged from the most recently published figures, with net sales projected at ¥1,090,000 million (up 2.2% year-on-year), operating profit at ¥60,000 million (up 16.5% year-on-year), and net profit attributable to owners of parent at ¥34,000 million (up 9.9% year-on-year).

- The annual dividend forecast is also unchanged at ¥145 per share (interim ¥70, year-end ¥75).

🤖 AI Perspective

Sumitomo Heavy Industries’ first-quarter results indicate a positive trend with increases in net sales and all profit stages compared to the previous year. The robust performance in the Mechatronics segment and substantial order intake in the Energy & Lifeline segment appear to be key drivers of the overall business performance. The unchanged full-year outlook and dividend forecast might suggest that the company is progressing largely as planned towards its annual targets.

8014|蝶理

4370.0

▼ -0.91%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Chori has decided to set the year-end dividend for the fiscal year ending March 2026 (record date: March 31, 2026) at ¥75.00 per share. This represents an increase of ¥3.00 from the most recent dividend forecast of ¥72.00.

- As a result, the total annual dividend for the fiscal year ending March 2026 will be ¥147.00 per share, including the interim dividend of ¥72.00, marking a ¥5.00 increase compared to the previous fiscal year’s ¥142.00.

- Based on the annual dividend of ¥147.00 for the fiscal year ending March 2026, the consolidated dividend payout ratio is 30.2%, and the dividend on equity (DOE) is 4.1%.

- Effective from the dividends related to the fiscal year ending March 2027 (including interim dividends), the company will revise its dividend policy. Under the new policy, the consolidated dividend payout ratio will be raised from the previous “30% or more (annual)” to “40% or more (annual).”

- Additionally, the DOE criterion will be changed from the previous “DOE of 3.5% or more based on shareholders’ equity” to “DOE of 3.5% or more based on net assets.” This revision was made as part of the “Chori Innovation Plan 2028” medium-term management plan, with the aim of further enhancing shareholder returns.

🤖 AI Perspective

Chori’s recent IR announcement highlights both an increased year-end dividend for the fiscal year ending March 2026 and a new dividend policy to be implemented from the fiscal year ending March 2027. The upward revision of the consolidated dividend payout ratio may suggest the company’s commitment to enhancing shareholder returns relative to net income attributable to parent company shareholders in the future. The alignment of this policy change with the medium-term management plan could indicate the company’s strategic focus on balancing sustainable corporate value enhancement with robust shareholder distribution.

8053|住友商

5790.0

▲ +1.70%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sumitomo Corporation announced on April 28, 2026, the recording of a gain on the sale of shares in an affiliated company in its non-consolidated financial results for the fiscal year ending March 2027.

- The company decided to transfer its entire stake in consolidated subsidiary SCSK Corporation to SC Investments Management Corporation, a 100% consolidated subsidiary, with July 1, 2026, as the effective date of transfer.

- This transfer is expected to result in the recording of an “extraordinary gain on sale of investment securities” of approximately JPY 850 billion as non-operating revenue in Sumitomo Corporation’s non-consolidated financial results for the fiscal year ending March 2027.

- The purpose of this share transfer is to streamline stockholding management within the company’s operating group.

- As this transaction is between wholly-owned subsidiaries, the impact on Sumitomo Corporation’s consolidated financial results is stated to be minor.

🤖 AI Perspective

While the impact on Sumitomo Corporation’s consolidated financial results is stated to be minor due to this being an intra-group share transfer, the non-consolidated results are expected to record a substantial extraordinary gain of approximately JPY 850 billion. This could significantly affect Sumitomo Corporation’s standalone financial statements. The move also appears to reflect an ongoing effort to optimize the group’s internal shareholding structure for improved management efficiency.

8524|北洋銀行

994.0

▲ +6.65%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- The Hokuyo Bank, Ltd. announced on April 28, 2026, an upward revision to its consolidated and non-consolidated earnings forecasts for the full fiscal year ending March 2026.

- For the consolidated forecast, ordinary revenue was revised from the previous forecast of ¥212,800 million to ¥235,900 million (an increase of 10.8%), and net profit attributable to parent company from ¥24,300 million to ¥25,600 million (an increase of 5.3%).

- The non-consolidated forecast also saw revisions, with ordinary revenue moving from ¥184,200 million to ¥206,800 million (an increase of 12.2%), and net profit from ¥24,200 million to ¥25,100 million (an increase of 3.7%).

- The reason cited for the earnings revision is that ordinary revenue is expected to exceed the previous forecast due to agile securities trading based on market trends by the bank on a non-consolidated basis.

- The dividend forecast for the fiscal year ending March 2026 was also revised, increasing the year-end dividend per share from the previously forecasted ¥6.50 to ¥8.50. This results in an annual dividend forecast of ¥28.00, up from ¥26.00.

🤖 AI Perspective

The simultaneous announcement of an upward revision to the full-year earnings forecast and an increase in the annual dividend suggests a positive performance trend and a commitment to shareholder returns. The agile trading of securities is highlighted as a key contributor to the improved earnings, indicating the bank’s responsiveness to market conditions.

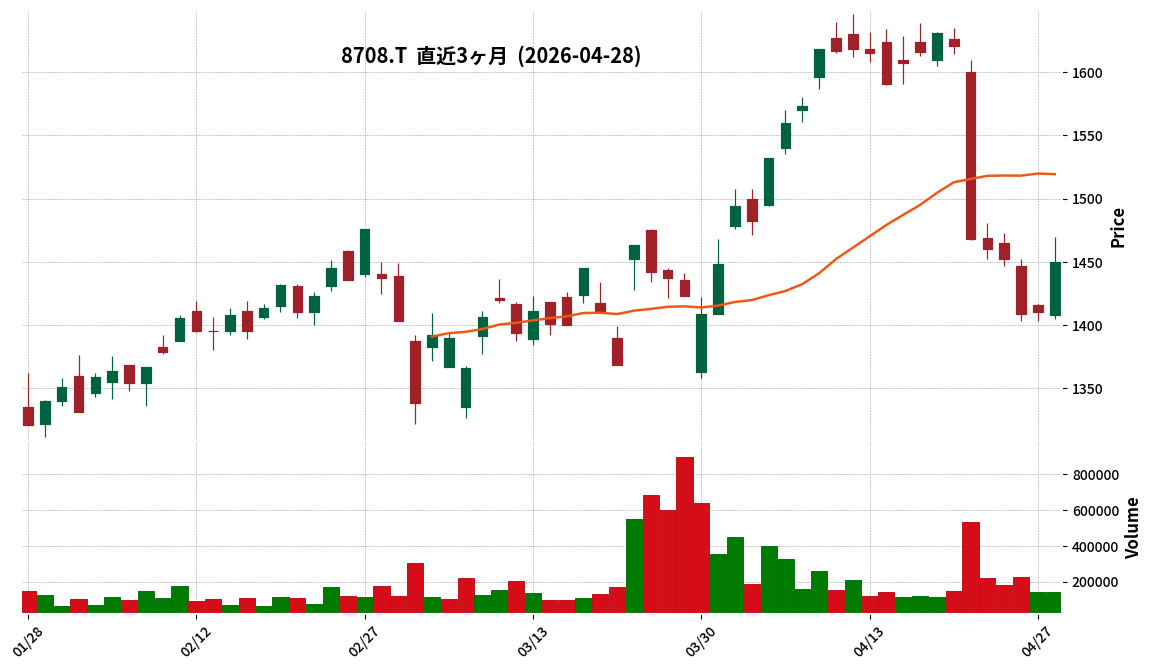

8708|アイザワ証G

1450.0

▲ +2.84%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, consolidated operating revenue increased by 1.9% year-on-year to ¥20,973 million.

- Consolidated operating profit was ¥26 million (a 98.6% decrease YoY), consolidated ordinary profit was ¥666 million (a 74.1% decrease YoY), and profit attributable to owners of parent was ¥2,752 million (a 13.2% decrease YoY).

- Earnings per share for the period stood at ¥88.44.

- The annual dividend per share increased by ¥21 from the previous year to ¥117.00 (interim ¥48.00, year-end ¥69.00), resulting in a consolidated payout ratio of 132.3%.

- As of March 31, 2026, consolidated total assets were ¥124,324 million, and consolidated net assets were ¥50,486 million.

🤖 AI Perspective

While consolidated operating and ordinary profits saw significant declines, the decrease in profit attributable to owners of parent was comparatively smaller, which could suggest the impact of extraordinary items or tax effects. Simultaneously, the increase in the annual dividend and a payout ratio exceeding 100% may indicate a strong commitment to shareholder returns. Furthermore, the positive shift in cash flow from operating activities, from a negative in the previous period to a positive, could suggest an improvement in financial stability.

9412|スカパーJSAT

3330.0

▲ +7.77%

📎 Source:スカパーJSAT Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SKY Perfect JSAT Corporation resolved its year-end dividend for the fiscal year ending March 2026 and the dividend forecast for the fiscal year ending March 2027 at its Board of Directors meeting held on April 28, 2026.

- The year-end dividend for FY March 2026 was set at JPY 23.00 per share, which is consistent with the latest dividend forecast and an increase from the JPY 16.00 per share paid in FY March 2025.

- The total dividend amount for this period is JPY 6,519 million, with an effective date of June 4, 2026.

- The dividend forecast for FY March 2027 is JPY 48.00 per share annually, an increase of JPY 6.00 from the JPY 42.00 per share of FY March 2026, based on the company’s dividend policy (payout ratio of 50% or more, with a minimum annual dividend of JPY 38 per share).

🤖 AI Perspective

This announcement highlights a confirmed year-end dividend increase for FY March 2026 compared to the previous period, along with a projected dividend increase for FY March 2027. The company’s explicit dividend policy, which includes a payout ratio of 50% or more and a minimum annual dividend of JPY 38 per share, suggests a consistent commitment to shareholder returns. Investors might view such a sustained increase, guided by a clear policy, as an indication of management’s confidence in the company’s future financial performance and stability.

5482|愛知鋼

2699.0

▲ +1.35%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Aichi Steel announced its consolidated financial results for the fiscal year ended March 2026, reporting revenue of ¥304,341 million, a 1.7% increase from the previous fiscal year.

- Consolidated operating profit reached ¥17,371 million, up 44.6% year-on-year, while profit attributable to owners of the parent increased by 43.8% to ¥11,248 million.

- An annual dividend of ¥145.00 per share was declared for the fiscal year ended March 2026.

- For the fiscal year ending March 2027, the company forecasts consolidated revenue of ¥310,000 million (up 1.9% year-on-year) and profit attributable to owners of the parent of ¥11,300 million (up 0.5% year-on-year).

- Aichi Steel conducted a 4-for-1 stock split for common shares on July 1, 2025, and per-share information and dividends from the fiscal year ended March 2026 onward are stated considering this split.

🤖 AI Perspective

The significant increase in operating profit for FY2026/3, despite a more modest revenue growth, is notably attributed to an increase in sales volume, which offset a decrease in selling prices, as indicated in the company’s report. While the forecast for FY2027/3 suggests continued revenue and profit growth, the projected slowdown in the rate of profit increase may indicate a more cautious outlook on future market conditions or cost management. Investors might consider these factors when evaluating the company’s future performance.

4728|トーセ

639.0

▼ -0.31%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- TOSE’s interim performance for the fiscal year ending August 2026 was strong, attributed to high operating rates in key game development projects, maintained stable profitability, and additional orders resulting from client satisfaction.

- The Project Management Support Office, established in September 2024, objectively reviews and provides guidance on quality, progress, and costs from outside project teams, and is recognized as contributing to the strengthening and stabilization of the business foundation.

- An overseas client’s home console game software development project was temporarily suspended due to the client’s management decision to curb investment. This project, which started in FY2025, had received generally good evaluations in interim inspections, but the client communicated a policy change in February 2026.

- To address the sudden availability of development resources from the suspended project, TOSE is focusing on early order acceptance and swift launch of new projects. Multiple negotiations are underway, with some projects already starting ahead of schedule or having development provisionally decided with budget negotiations in progress, indicating a certain level of success. The company currently believes a downward revision to the full-year earnings forecast (announced October 9, 2025) is not necessary.

- Regarding AI utilization, it is already being used for mini-game prototyping in the planning phase and for operational efficiency improvements like asset management and automated test play. TOSE is strengthening AI-related investments and improving organizational proficiency; while concrete results are emerging, the quantitative assessment of these effects has not yet been achieved.

🤖 AI Perspective

TOSE’s strong interim performance for FY2026, driven by stable game development and additional orders, is noteworthy. However, the temporary suspension of an overseas project introduces a new variable for future operations. The company’s proactive approach to securing new projects to optimize resource utilization will be crucial for meeting its full-year earnings forecast. Furthermore, the ongoing investment in AI integration could enhance long-term development efficiency and competitiveness, suggesting a strategic focus on future operational improvements.

6301|コマツ

6914.0

▼ -1.97%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the consolidated fiscal year ended March 31, 2026, Komatsu reported net sales of 4,132,751 million yen (up 0.7% year-over-year). Operating profit decreased by 13.7% to 567,323 million yen, and net profit attributable to owners of parent fell by 14.4% to 376,391 million yen. Basic earnings per share was 413.90 yen.

- The annual dividend for FY2026 was 190.00 yen, with a consolidated payout ratio of 45.9%.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of 4,118,000 million yen (down 0.4%), operating profit of 508,000 million yen (down 10.5%), and net profit attributable to owners of parent of 318,000 million yen (down 15.5%), with basic EPS of 352.90 yen.

- A resolution for share repurchase and cancellation was approved at the Board of Directors meeting on April 28, 2026, but its impact is not included in the FY2027 forecast for basic earnings per share.

🤖 AI Perspective

- Komatsu’s FY2026 results show a slight increase in net sales, but a double-digit decline in both operating and net profits, which may suggest the impact of market conditions or cost pressures.

- The company’s forecast for FY2027 projects further decreases in revenue and profit, indicating an anticipated challenging operating environment.

- However, the decision to maintain the annual dividend at 190 yen and proceed with share repurchase and cancellation could be seen as a continued commitment to shareholder returns.

8334|群馬銀

2182.5

▲ +7.70%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- The Gunma Bank, Ltd. has revised its consolidated earnings forecast for the fiscal year ending March 2026 upward. Operating profit is raised by 8.7% from the previous forecast of ¥78.0 billion to ¥84.8 billion, and profit attributable to owners of parent is increased by 6.9% from ¥55.0 billion to ¥58.8 billion.

- The non-consolidated earnings forecast has also been revised upward, with operating profit increasing by 9.3% from ¥72.0 billion to ¥78.7 billion, and net income by 7.3% from ¥51.0 billion to ¥54.7 billion.

- The primary reasons for the earnings revision are the favorable progression of core business net profit, mainly driven by an increase in loan interest income and interest/dividend income from securities at the bank alone. Both consolidated and non-consolidated figures are revised upward to record highs.

- The year-end dividend forecast for the fiscal year ending March 2026 has been revised, increasing by ¥2.00 per share from the previous forecast of ¥30.00 to ¥32.00. Consequently, the annual dividend per share, combined with an interim dividend of ¥30.00, will be ¥62.00, representing an increase of ¥17.00 compared to the previous fiscal year (ending March 2025) of ¥45.00.

- The reason for the dividend revision is based on the bank’s progressive dividend policy, aiming for a dividend payout ratio of approximately 40% of profit attributable to owners of parent, in light of the upward revision to said profit.

🤖 AI Perspective

Gunma Bank’s upward revision to its earnings forecast suggests a robust performance in its core business, including loan interest income and securities-related income. The projection of new record-high profits for both consolidated and non-consolidated results indicates positive operational momentum. Furthermore, the dividend increase, aligned with the company’s progressive dividend policy and improved profit outlook, may be seen as a notable commitment to shareholder returns.

1941|中電工

4860.0

▲ +5.65%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Chudenko Co., Ltd. has decided to increase its year-end dividend for the fiscal year ended March 2026 to ¥70.00 per share, an increase from the previously forecast ¥65.00 (announced on April 28, 2025).

- This decision results in an annual dividend of ¥135.00 per share for the fiscal year ended March 2026, marking a ¥5.00 increase from the prior forecast of ¥130.00.

- The total dividend amount for FY2026 is projected to be ¥3,705 million.

- For the fiscal year ending March 2027, the company forecasts an annual dividend of ¥140.00 per share (¥70.00 for interim and ¥70.00 for year-end).

- The company’s dividend policy emphasizes sustainable and stable dividends, aiming for a DOE (Dividend on Equity ratio) of approximately 3.0%.

🤖 AI Perspective

- Chudenko’s announcement of an increased year-end dividend for FY2026 and a further increase in the dividend forecast for FY2027 suggests a strong commitment to continuous shareholder returns.

- The company’s dividend policy, which targets a DOE (Dividend on Equity ratio) of approximately 3.0%, may indicate an emphasis on stable dividends that are less susceptible to short-term earnings fluctuations.

- The simultaneous disclosure of the dividend forecast for the next fiscal year provides investors with forward-looking clarity regarding the company’s capital allocation strategy.

284A|P-フクヤ建設

2335.0

▲ +0.00%

📎 Source:P-フクヤ建設 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- On April 28, 2026, P-Fukuya Kensetsu’s Board of Directors resolved to acquire all shares of M’s Associates, making it a wholly-owned subsidiary.

- The acquisition aims to foster collaboration with P-Fukuya Kensetsu’s construction business, anticipating significant synergies to drive mid-to-long-term growth and enhance corporate value.

- M’s Associates specializes in new construction, expansion, renovation of residential and commercial properties, and architectural and interior design/planning services.

- For its most recent fiscal year ended March 2025, M’s Associates reported net sales of 1,030 million yen and net income of 14 million yen.

- The acquisition price was not disclosed at the seller’s request but was determined based on fair net asset value after third-party valuation. The share transfer execution date is undetermined, and funding for the acquisition is planned through borrowings from financial institutions.

🤖 AI Perspective

This acquisition appears to be a strategic move by P-Fukuya Kensetsu to reinforce its core construction business, aligning with its corporate philosophy of “creating excitement in this town.” The integration of M’s Associates’ expertise in residential and commercial renovation, design, and planning services could expand P-Fukuya Kensetsu’s service offerings and potentially enhance its value proposition to customers. Further disclosures regarding the share transfer execution date, financing details, and the specific impact on consolidated earnings could be worth monitoring.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

6473|ジェイテクト

1759.5

▲ +5.11%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, JTEKT reported consolidated revenue of JPY 1,924.95 billion (up 2.2% year-on-year) and business profit of JPY 75.679 billion (up 16.5% year-on-year).

- Consolidated operating profit for the same period was JPY 24.847 billion (down 35.4% year-on-year), and profit attributable to owners of the parent was JPY 11.974 billion (down 12.7% year-on-year).

- The annual dividend for the fiscal year ended March 31, 2026, was JPY 60.00 per share (interim JPY 30.00, year-end JPY 30.00), an increase from JPY 50.00 in the previous fiscal year.

- For the fiscal year ending March 31, 2027, JTEKT forecasts consolidated revenue of JPY 1,880.0 billion (down 2.3% year-on-year), business profit of JPY 90.0 billion (up 18.9% year-on-year), operating profit of JPY 75.0 billion (up 201.8% year-on-year), and profit attributable to owners of the parent of JPY 50.0 billion (up 317.6% year-on-year).

7919|野崎印

202.0

▼ -0.49%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, Nozaki Printing Co., Ltd. reported consolidated net sales of ¥14,016 million (down 3.8% year-on-year) and operating profit of ¥516 million (down 25.2% year-on-year).

- Profit attributable to owners of parent for the same period amounted to ¥359 million (down 31.2% year-on-year).

- As of March 31, 2026, the consolidated financial position showed net assets of ¥4,865 million (up ¥238 million from the previous fiscal year-end), with the equity ratio improving to 43.5% (from 41.3% at the previous fiscal year-end).

- The annual dividend for the fiscal year ended March 31, 2026, remained unchanged at ¥7.50 per share (interim dividend ¥2.50, year-end dividend ¥5.00).

- The consolidated earnings forecast for the fiscal year ending March 31, 2027, is currently undetermined due to numerous uncertain factors impacting performance, such as soaring raw material prices and procurement uncertainty stemming from the Middle East situation.

🤖 AI Perspective

Nozaki Printing’s FY2026 results indicate a year-on-year decline in both revenue and various profit metrics, which may suggest the impact of factors such as the reversal of special demand for logistics, heightened price competition, persistently high raw material costs, and rising personnel expenses.

Conversely, the improvement in the equity ratio could point to a strengthening of the company’s financial foundation.

The decision to leave the FY2027 earnings forecast undetermined highlights the significant uncertainty in the business environment, particularly concerning geopolitical risks affecting raw material prices and supply chain stability, making future disclosures a key focus for investors.

9539|京葉瓦斯

1380.0

▲ +0.44%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Keiyo Gas Co., Ltd. announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1 to March 31, 2026).

- Revenue was ¥37,742 million (up 0.1% year-on-year), operating profit was ¥3,679 million (up 46.1%), ordinary profit was ¥3,770 million (up 44.1%), and profit attributable to owners of parent was ¥2,750 million (up 50.5%).

- Total gas sales volume for the first quarter decreased by 0.7% year-on-year to 220 million cubic meters. While residential use increased by 0.1% due to a rise in customer accounts, commercial and industrial use decreased by 1.7%.

- Cost of sales decreased by 3.9% year-on-year to ¥24,757 million, primarily due to a reduction in gas raw material costs driven by lower raw material prices.

- For the full fiscal year ending December 2026, the consolidated earnings forecast for revenue was revised upward by ¥3,200 million to ¥120,000 million. However, operating profit, ordinary profit, and profit attributable to owners of parent were all revised downwards by ¥600 million, ¥600 million, and ¥400 million, respectively, compared to the previous forecast.

- The annual dividend forecast for the full fiscal year remains unchanged from the most recently announced forecast, with ¥13.00 for the interim dividend and ¥13.00 for the year-end dividend, totaling ¥26.00.

🤖 AI Perspective

* The significant profit growth in the first quarter, despite only a slight increase in revenue, appears to be primarily driven by a decrease in the cost of sales, likely due to lower raw material prices.

* However, the downward revision of the full-year profit forecast, despite an upward revision in revenue, suggests that factors such as the future trend of gas raw material prices or changes in the sales environment may impact the full fiscal year’s performance.

* Investors may find it valuable to examine the detailed explanations provided by the company to understand the discrepancy between the strong Q1 results and the adjusted full-year outlook, especially considering the seasonal nature of the gas business.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

162A|AIセレクトETN

15755.0

▼ -0.91%

📎 Source:AIセレクトETN Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Mitsubishi UFJ Securities Holdings Co., Ltd., the issuer of AI Select ETN, announced its consolidated financial results for the fiscal year ended March 31, 2026.

- Consolidated operating revenue for FY2026/3 was ¥860,667 million, a decrease of 26.7% compared to the previous fiscal year.

- Profit attributable to owners of parent increased by 27.5% year-on-year, reaching ¥64,325 million.

- As of March 31, 2026, consolidated total assets stood at ¥36,871,647 million, and consolidated net assets were ¥757,824 million.

- The total amount of ETNs issued by the company was ¥44,707 million as of April 24, 2026, representing 5.9% of net assets. During the fiscal year (April 1, 2025 – March 31, 2026), additional units were issued for four ETN series, including the High Dividend Growth Japan Stock (Net Return) ETN.

🤖 AI Perspective

The issuer’s financial results show a decrease in operating revenue but an increase in profit attributable to owners of parent, which may suggest shifts in revenue streams or effective cost management. The fact that the total ETN issuance accounts for 5.9% of net assets, along with additional units issued for several ETN series during the period, could indicate consistent market interest in ETN products and the issuer’s active product offering strategy.

2130|メンバーズ

1090.0

▲ +0.55%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)