📌 Today’s Highlights

Today we cover 92 IR announcements. Notable among them: JR東海 (9022), 田谷 (4679), 東海東京 (8616). Use the table of contents below to navigate to each company.

- 9022|JR東海

- 4679|田谷

- 8616|東海東京

- 1878|大東建

- 5893|P-RAVIPA

- 7172|JIA

- 9533|東邦瓦斯

- 2060|フィード・ワン

- 4626|太陽HD

- 7157|ライフネット生命

- 7981|タカラスタン

- 9104|商船三井

- 9201|JAL

- 2892|日食化

- 2972|R-サンケイRE

- 3776|BBタワー

- 4221|大倉工

- 2692|伊藤忠食

- 4410|ハリマ化成G

- 5257|ノバシステム

- 5440|共英製鋼

- 5938|LIXIL

- 6325|タカキタ

- 7539|アイナボHD

- 8133|エネクス

- 8218|コメリ

- 9362|兵機海運

- 9830|トラスコ中山

- 7896|セブン工

- 2216|カンロ

- 3992|ニーズウェル

- 1950|日本電設

- 6888|アクモス

- 7441|Misumi

- 9534|北海瓦斯

- 4098|チタン工

- 4463|日華化学

- 6557|G-AIAI

- 7063|G-Birdman

- 7779|G-サイバダイン-議

- 7947|エフピコ

- 8015|豊田通商

- 9914|植松商会

- 9235|G-売れるネットG

- 7177|GMOFHD

- 1381|アクシーズ

- 2127|日本M&A

- 2204|中村屋

- 2329|東北新社

- 2579|コカ・コーラBJH

- 2926|篠崎屋

- 3197|すかいらーくHD

- 3496|アズーム

- 3681|ブイキューブ

- 3807|G-フィスコ

- 3836|アバントグループ

- 3934|ベネフィットジャパン

- 4318|クイック

- 4667|アイサンテクノロ

- 4768|大塚商会

- 5214|日電硝

- 5280|ヨシコン

- 6027|弁護士ドットコム

- 6080|M&Aキャピタル

- 6920|レーザーテック

- 2811|カゴメ

- 3839|ODK

- 8704|トレイダーズHD

- 2410|キャリアDC

- 2428|ウェルネット

- 244A|G-グロースエクスパ

- 3657|ポールHD

- 372A|レント

- 3760|ケイブ

- 4417|G-グローバルセキュ

- 4762|XNET

- 5208|有沢製

- 5386|鶴弥

- 5892|G-yutori

- 5901|洋缶HD

- 6268|ナブテスコ

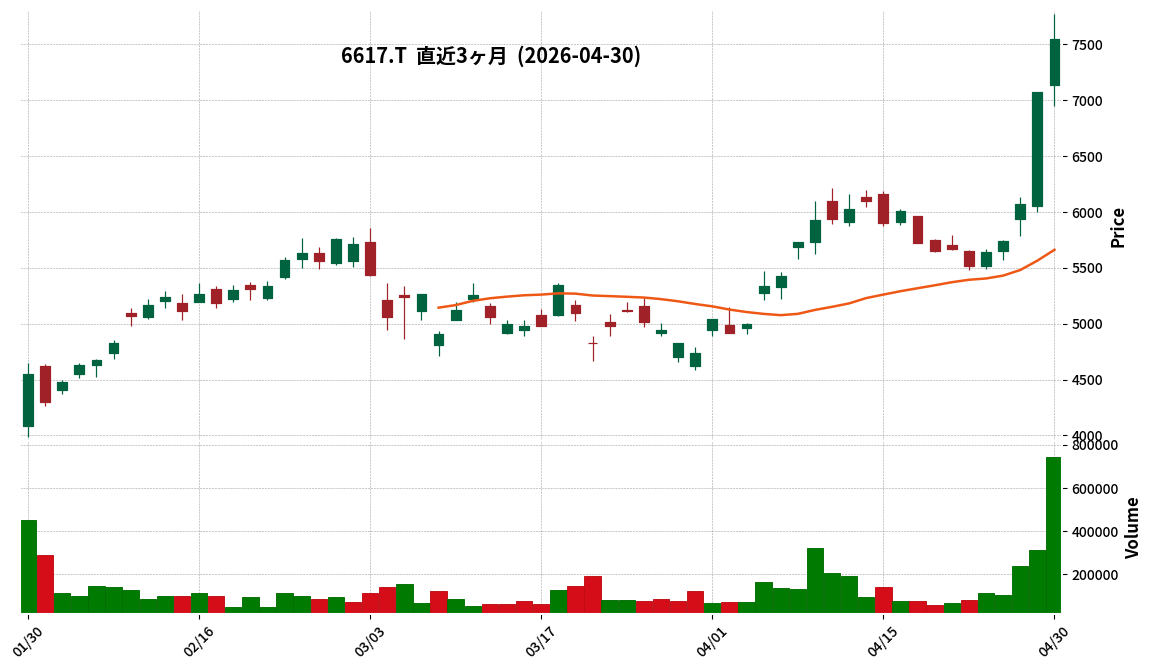

- 6617|東光高岳

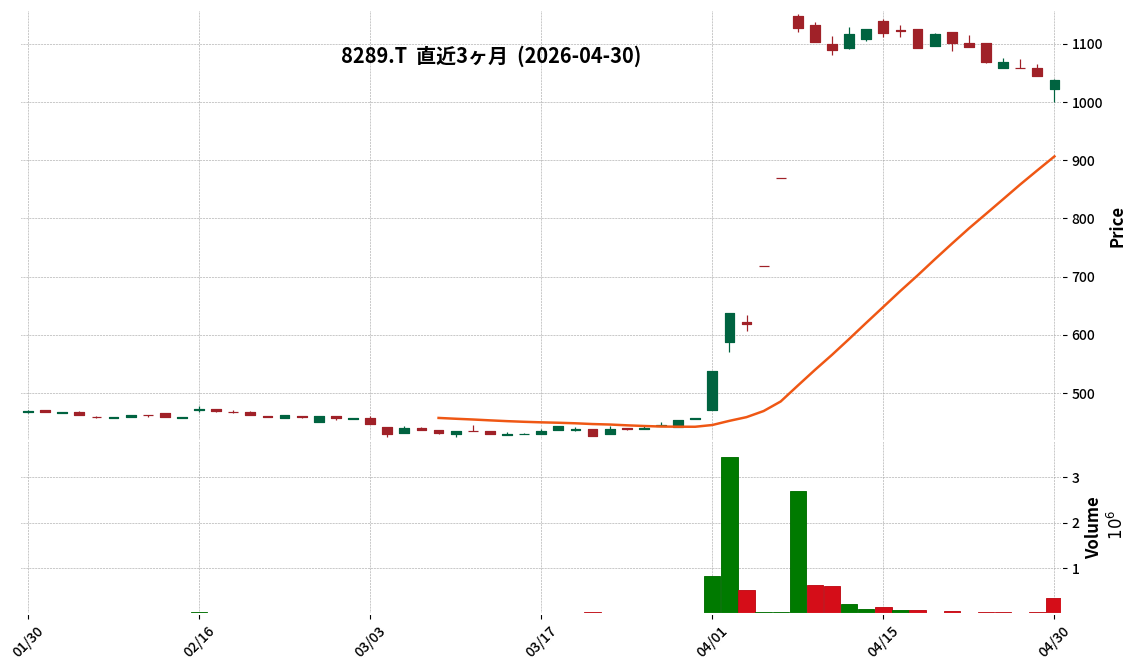

- 8289|OlympicG

- 8898|センチュリー21

- 9979|大庄

- 6391|加地テック

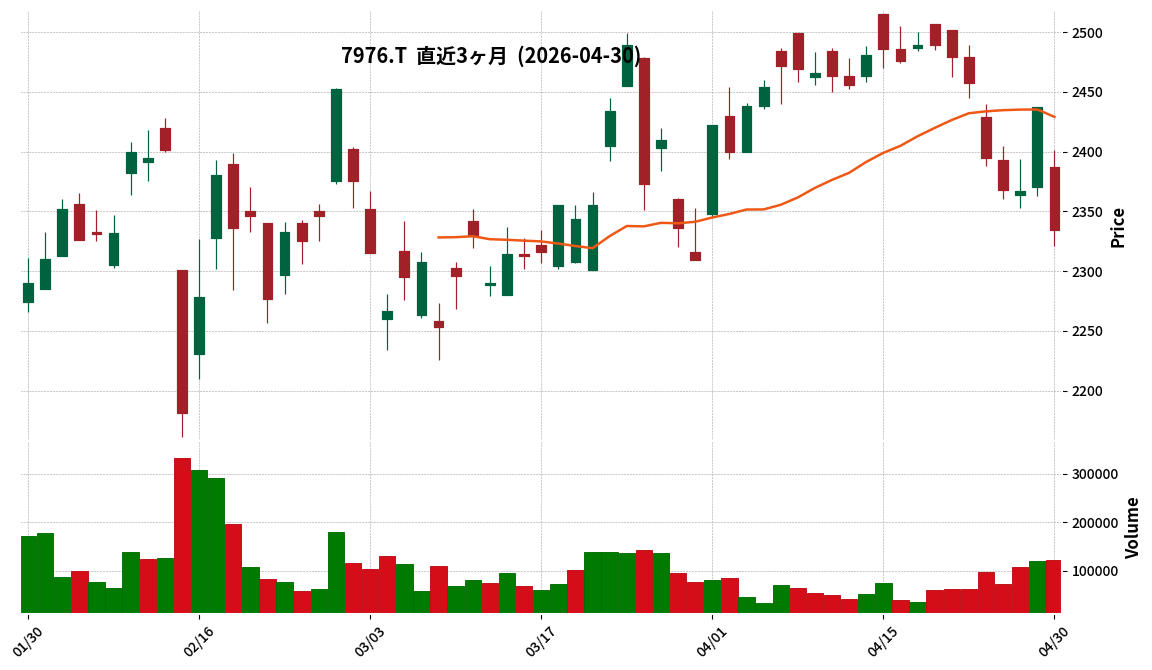

- 7976|三菱鉛筆

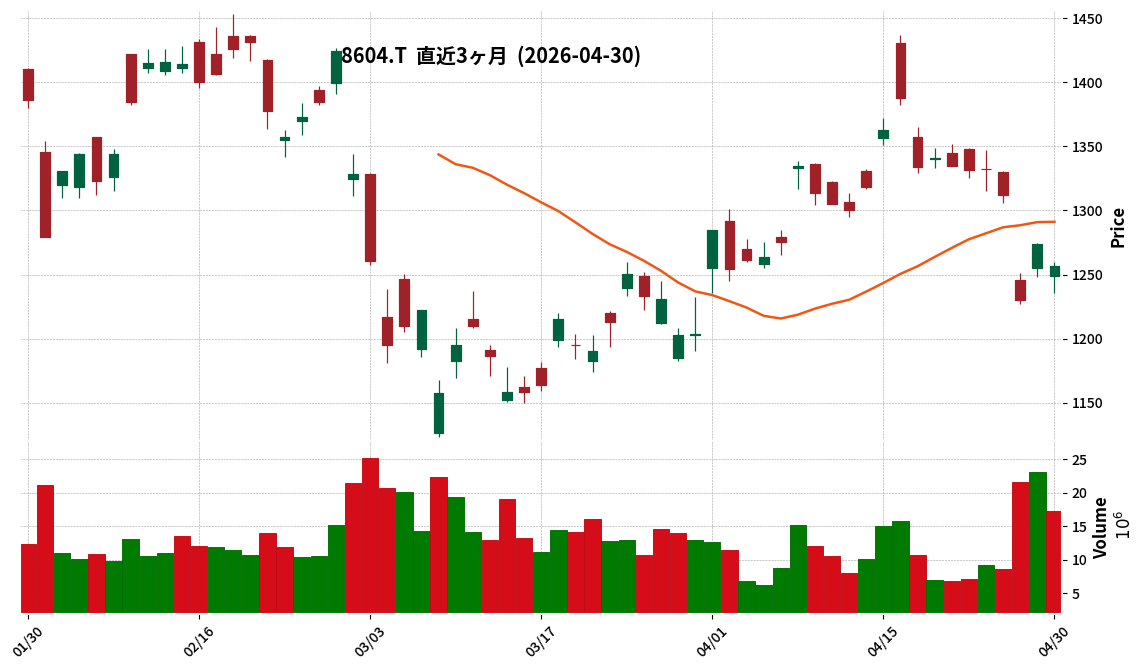

- 8604|野村

- 7812|クレステック

- 278A|G-テラドローン

- 509A|I-Gライト・再エネ

- 9501|東電力HD

9022|JR東海

4069.0

▲ +0.42%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For fiscal year 2025, consolidated operating revenue increased by 9.5% to ¥2,006.2 billion, and net profit attributable to owners of the parent rose by 20.6% to ¥552.8 billion, marking an increase in both revenue and profit.

- The company forecasts a decrease in both revenue and profit for consolidated and non-consolidated results in fiscal year 2026.

- Regarding shareholder returns, the year-end dividend for FY2025 is set at ¥16 per share (annual dividend of ¥32), with an annual dividend of ¥32 also projected for FY2026. Additionally, a share buyback of up to ¥20 billion will be executed.

- As part of its growth strategy, Tokaido Shinkansen operations saw an increase to a maximum of 13 “Nozomi” trains per hour during certain times from March 2026, with the introduction of premium private compartments planned for October 1, 2026.

- For fiscal year 2026, the company anticipates an increase in costs of approximately ¥40 billion (non-consolidated) due to rising prices and labor costs, and is addressing this through new demand creation, business reforms, and advocacy for fundamental changes to the fare system.

🤖 AI Perspective

The strong FY2025 results are juxtaposed with a forecast of decreased revenue and profit for FY2026, which may suggest the impact of inflation on costs and the leveling off of recovery from past service disruptions. The company’s focus on enhancing Shinkansen services, implementing business reforms for cost reduction, and advocating for fare system adjustments appears crucial for sustaining and improving profitability. The commitment to stable dividends and share buybacks could indicate a balanced approach to shareholder returns amidst a challenging operational environment.

4679|田谷

305.0

▲ +22.49%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, sales were JPY 5,075 million, a 6.8% decrease year-on-year.

- Operating profit for the same period was JPY 37 million (compared to JPY 3 million in the previous year), and ordinary profit was JPY 34 million (compared to JPY 4 million in the previous year).

- The company recorded a net loss of JPY 160 million, primarily due to JPY 169 million in special losses related to store closures and impairment losses.

- The equity ratio improved to 36.0% as of March 31, 2026 (from 20.9% at the end of the previous fiscal year), with net assets increasing by JPY 382 million to JPY 798 million, driven by the exercise of stock acquisition rights and third-party allotments.

- For the fiscal year ending March 31, 2027, the company forecasts sales of JPY 5,200 million (up 2.5% year-on-year), operating profit of JPY 40 million (up 5.6%), ordinary profit of JPY 40 million (up 17.2%), and a net profit of JPY 10 million.

🤖 AI Perspective

- Despite a decline in sales, the significant improvement in operating and ordinary profits may suggest an enhancement in operational efficiency.

- The continued net loss is largely attributable to special losses, which could indicate ongoing structural reforms such as store closures and impairment write-downs.

- The substantial improvement in the equity ratio and the forecast for a return to net profitability in the next fiscal year could be viewed as positive indicators for strengthening financial health and future earnings recovery.

8616|東海東京

719.0

▼ -1.78%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, Tokai Tokyo FH reported consolidated operating revenue of ¥97,716 million (up 13.2% year-on-year) and net operating revenue of ¥91,920 million (up 10.5% year-on-year).

- Net income attributable to owners of parent significantly increased by 50.0% year-on-year to ¥16,569 million. Basic earnings per share stood at ¥65.82.

- The annual dividend for the fiscal year ended March 31, 2026, totaled ¥50.00 per share, comprising an interim dividend of ¥22 (ordinary ¥14, commemorative ¥8) and a year-end dividend of ¥28 (ordinary ¥20, commemorative ¥8).

- Consolidated earnings and dividend forecasts for the fiscal year ending March 31, 2027, have not been disclosed due to the difficulty in forecasting performance in the financial instruments business, which is highly susceptible to market fluctuations.

- During the period, two companies, TT Digital Platform Co., Ltd. and ETERNAL Co., Ltd., were removed from the scope of consolidation.

🤖 AI Perspective

Tokai Tokyo Financial Holdings’ FY2026 results highlight a substantial 50.0% increase in net income attributable to owners of parent, which may suggest effective management of market conditions leading to revenue growth. The significant rise in the annual dividend from ¥28.00 to ¥50.00 per share could indicate a strengthened commitment to shareholder returns. The non-disclosure of FY2027 forecasts reflects the inherent volatility of the financial instruments business, where market fluctuations can heavily impact performance, making forward-looking statements challenging.

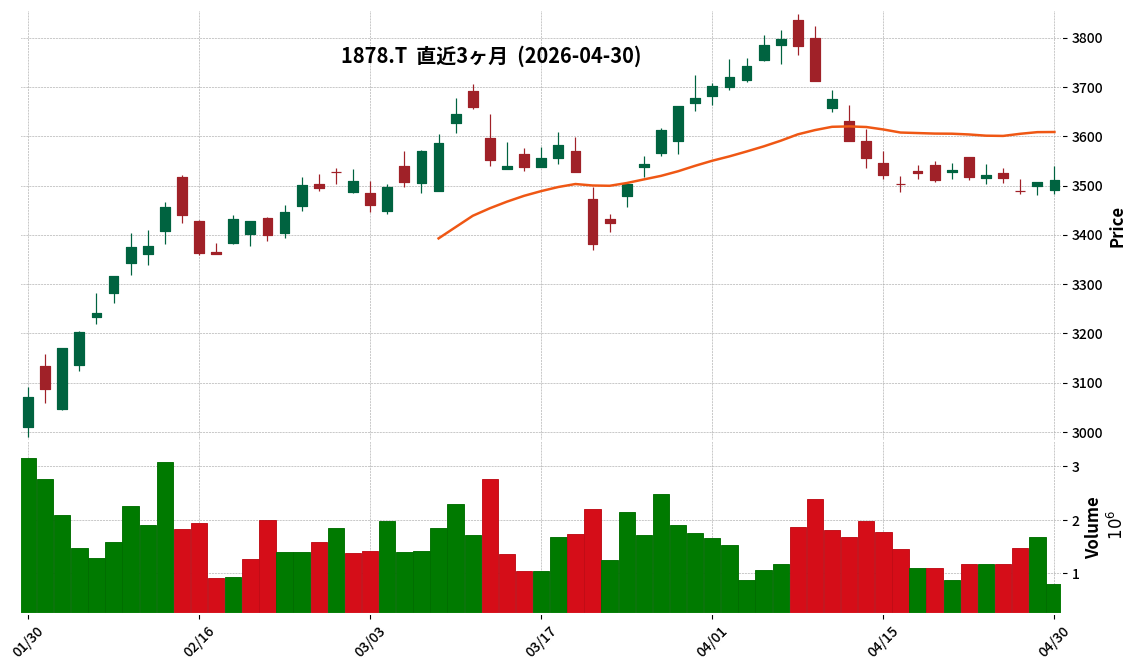

1878|大東建

3511.0

▲ +0.09%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Daito Trust Construction Co., Ltd. announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- Consolidated results show net sales of ¥1,984,743 million (up 7.7% year-on-year), operating profit of ¥135,256 million (up 13.8%), ordinary profit of ¥139,169 million (up 7.5%), and profit attributable to owners of parent of ¥99,030 million (up 5.5%).

- The year-end dividend for the fiscal year ended March 31, 2026, is ¥82.00 per share, adjusted for the stock split effective October 1, 2025.

- For the fiscal year ending March 31, 2027 (April 1, 2026 – March 31, 2027), the company forecasts consolidated net sales of ¥2,050,000 million (up 3.3% year-on-year), operating profit of ¥142,000 million (up 5.0%), and profit attributable to owners of parent of ¥108,000 million (up 9.1%).

- The company implemented a 5-for-1 stock split of its common shares effective October 1, 2025.

🤖 AI Perspective

- The FY2026 consolidated financial results indicate growth across all key profit metrics, which may suggest a robust performance trend for the company.

- The forecast for FY2027 also projects increases in both sales and profits, potentially reflecting confidence in sustained business expansion.

- Investors should be mindful of the 5-for-1 stock split implemented on October 1, 2025, when comparing per-share metrics and historical data.

5893|P-RAVIPA

510.0

▲ +0.00%

📎 Source:P-RAVIPA Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- RAVIPA Co., Ltd. (Code: 5893, TOKYO PRO Market) announced on April 30, 2026, a partial correction to its “Notice Regarding Financial Results of Non-Listed Parent Company, etc.”

- This correction addresses an error in the content of the IR document originally published on April 28, 2026.

- The specific section corrected is “2. Shareholder Status by Owner, Major Shareholders, and Officer Status of the Parent Company, etc.,” under “(2) Major Shareholders.”

- The correction involves the address of major shareholder Mr. Osamu Nishiyama, changing from “Before Correction: Kamagawa Ken Yokohama City Minami-ku” to “After Correction: Kanagawa Prefecture Yokohama City Minami-ku.”

- There are no changes to Mr. Osamu Nishiyama’s shareholding (116 shares) or the percentage of total outstanding shares held (58.0%).

🤖 AI Perspective

This correction addresses a typographical error in the address of a major shareholder of the non-listed parent company, aiming to ensure the accuracy of disclosed information. It is considered a procedural update to reflect correct details. This specific amendment is not expected to have a direct impact on RAVIPA’s financial performance, operational strategy, or fundamental business outlook.

7172|JIA

1975.0

▼ -1.64%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Japan Investment Adviser Co., Ltd. (JIA) announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1 to March 31, 2026).

- Consolidated net sales reached ¥13,755 million (up 24.8% year-on-year), operating profit was ¥9,270 million (up 32.9% year-on-year), and ordinary profit was ¥8,688 million (up 46.5% year-on-year).

- Net income attributable to owners of the parent increased to ¥6,167 million (up 53.0% year-on-year), with basic earnings per share at ¥101.86.

- By segment, operating lease business sales were ¥12,878 million (up 27.5% year-on-year). Investment product sales amounted to ¥63,947 million (up 66.4% year-on-year), and deal origination volume was ¥102,334 million (up 29.1% year-on-year).

- The capital adequacy ratio at the end of the first quarter improved to 30.8%, up from 25.0% at the end of the previous consolidated fiscal year.

🤖 AI Perspective

- JIA’s Q1 FY2026 results demonstrate significant year-on-year growth across all key earnings indicators.

- The robust performance of the operating lease business appears to be a major contributor to the overall sales and profit increases.

- The improvement in the capital adequacy ratio could indicate enhanced financial stability for the company.

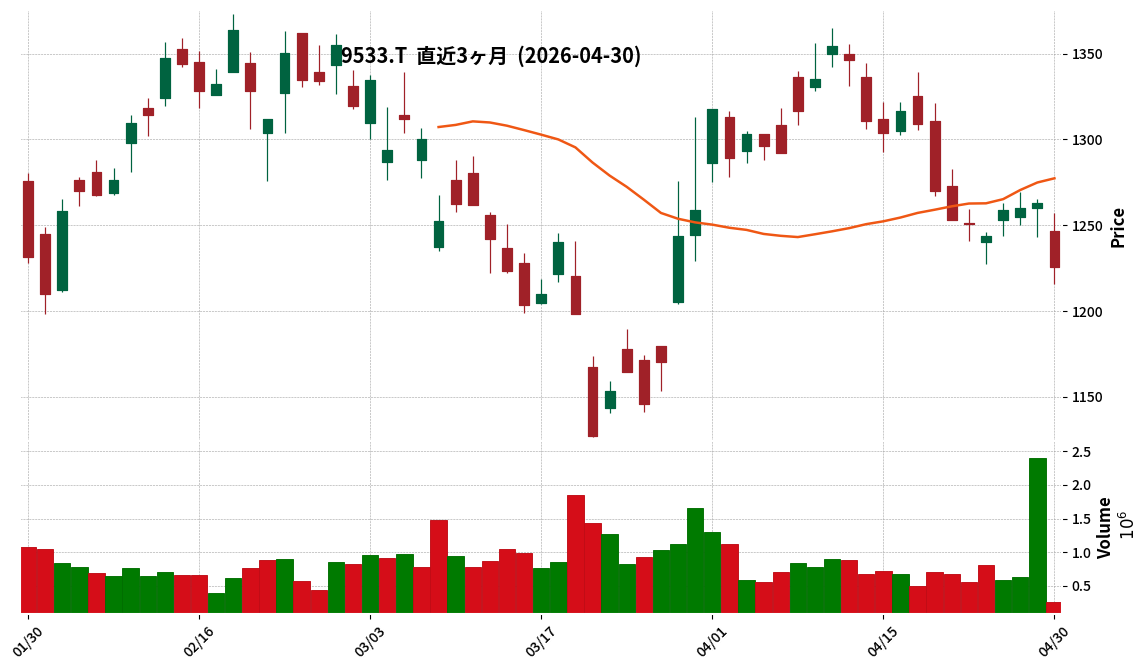

9533|東邦瓦斯

1225.5

▼ -2.97%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the consolidated fiscal year ended March 31, 2026, Toho Gas reported net sales of JPY 651,085 million (down 0.8% year-on-year). Operating profit was JPY 31,784 million (up 2.9%), ordinary profit was JPY 37,879 million (up 16.9%), and profit attributable to owners of parent was JPY 31,449 million (up 23.6%).

- Diluted earnings per share (EPS) for the period was JPY 83.76, adjusted for the 1-for-4 stock split effective April 1, 2026.

- The annual dividend for the fiscal year ended March 31, 2026, was JPY 90.00 (compared to JPY 80.00 in the previous year). The forecast for the fiscal year ending March 31, 2027, is JPY 22.50 per share, reflecting the stock split.

- The consolidated earnings forecast for the fiscal year ending March 31, 2027, includes net sales of JPY 670,000 million (up 2.9% year-on-year), but anticipates operating profit of JPY 19,000 million (down 40.2%), ordinary profit of JPY 25,000 million (down 34.0%), and profit attributable to owners of parent of JPY 23,000 million (down 26.9%).

- A key factor contributing to the increase in profit for the current fiscal year was the expansion of time-lag profit between raw material costs and sales revenue due to the raw material cost adjustment system.

🤖 AI Perspective

While net sales showed a slight decline, Toho Gas recorded a significant increase in various profit metrics for FY2026/3, with profit attributable to owners of parent rising over 20%. This performance appears to be primarily driven by an expansion of time-lag profit from the raw material cost adjustment system. However, the company’s forecast for FY2027/3 projects a substantial decrease in profits despite an expected increase in sales, which may warrant close monitoring of the underlying factors influencing this outlook.

2060|フィード・ワン

1080.0

▼ -1.01%

📎 Source:フィード・ワン Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Feed One has announced an upward revision to its consolidated financial forecasts for the fiscal year ending March 2026.

- The revised forecasts are: Revenue JPY 290,000 million (up 0.7% from previous), Operating Profit JPY 8,000 million (up 5.3%), Ordinary Profit JPY 8,600 million (up 6.2%), and Net Profit Attributable to Parent Company Shareholders JPY 6,300 million (up 5.0%).

- The reason for the performance revision is attributed to an improved profitability environment in the livestock and aquaculture feed business, followed by continued strong performance.

- The year-end dividend forecast for the fiscal year ending March 2026 has been revised upward by JPY 3.5 per share, from JPY 21.00 to JPY 24.50.

- This revision is expected to result in a total annual dividend of JPY 45.50 per share for FY2026/3, with a projected consolidated Dividend on Equity (DOE) of 3.1%.

🤖 AI Perspective

Feed One’s “second” upward revision of its consolidated financial forecasts for the fiscal year ending March 2026 could suggest a sustained favorable business environment in its livestock and aquaculture feed segment. Furthermore, the announced dividend increase, aligning with the company’s progressive dividend policy and 3% DOE target, and resulting in a projected DOE of 3.1%, may be viewed as a strong commitment to shareholder returns. These announcements could draw investor attention as indicators of the company’s financial stability and robust operational performance.

4626|太陽HD

4825.0

▲ +0.52%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Taiyo Holdings Co., Ltd. announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 to March 31, 2026).

- For the consolidated operating results, net sales increased by 15.8% year-on-year to ¥137,851 million, operating profit increased by 47.4% to ¥32,529 million, ordinary profit increased by 49.4% to ¥32,244 million, and profit attributable to owners of parent increased by 122.7% to ¥24,011 million.

- The annual dividend for the fiscal year ended March 31, 2026, was ¥165.00 (interim dividend: ¥165.00, year-end dividend: ¥0.00), compared to a total of ¥190.00 in the previous fiscal year.

- The company resolved not to pay a year-end dividend for the fiscal year ended March 31, 2026, and announced plans not to pay interim or year-end dividends for the fiscal year ending March 31, 2027.

- For the fiscal year ending March 31, 2027, the consolidated earnings forecast projects net sales of ¥146,300 million (up 6.1% year-on-year), operating profit of ¥34,300 million (up 5.4%), ordinary profit of ¥33,400 million (up 3.6%), and profit attributable to owners of parent of ¥24,100 million (up 0.4%).

🤖 AI Perspective

The strong revenue and profit growth reported for FY2026/3 is a notable development. However, the decision to suspend both the FY2026/3 year-end dividend and all dividends for FY2027/3 may suggest a strategic shift in capital allocation or a focus on future investments. Investors may monitor how this change in dividend policy aligns with the company’s projected continued growth in revenue and profit for FY2027/3.

7157|ライフネット生命

2151.0

▲ +0.05%

📎 Source:ライフネット生命 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Lifenet Insurance Company announced on April 30, 2026, the signing of a new capital and business alliance agreement with Japan Airlines Co., Ltd. (JAL).

- The capital alliance with au Financial Holdings Corporation (auFH) will be dissolved, and the business alliance with auFH and KDDI Corporation will be modified.

- auFH has agreed to transfer all of its 14,726,100 common shares of Lifenet Insurance (18.32% of total outstanding shares) to JAL.

- Consequently, JAL is expected to become a major insurance shareholder of Lifenet Insurance, and a secondary offering of the company’s common shares has also been decided.

- The business alliance with JAL aims to jointly develop and sell insurance products utilizing JAL’s brand power, customer base (including approximately 41 million JAL Mileage Bank members), and mileage assets, as well as to establish a sales system for Lifenet Insurance products by the JAL Group.

🤖 AI Perspective

This alliance is expected to accelerate Lifenet Insurance’s “Embedded” strategy, a key focus in its mid-term plan. Access to JAL’s extensive customer base could generate new customer touchpoints and business opportunities. The change in major shareholders from KDDI Group to JAL Group may also influence the future strategic direction of the company.

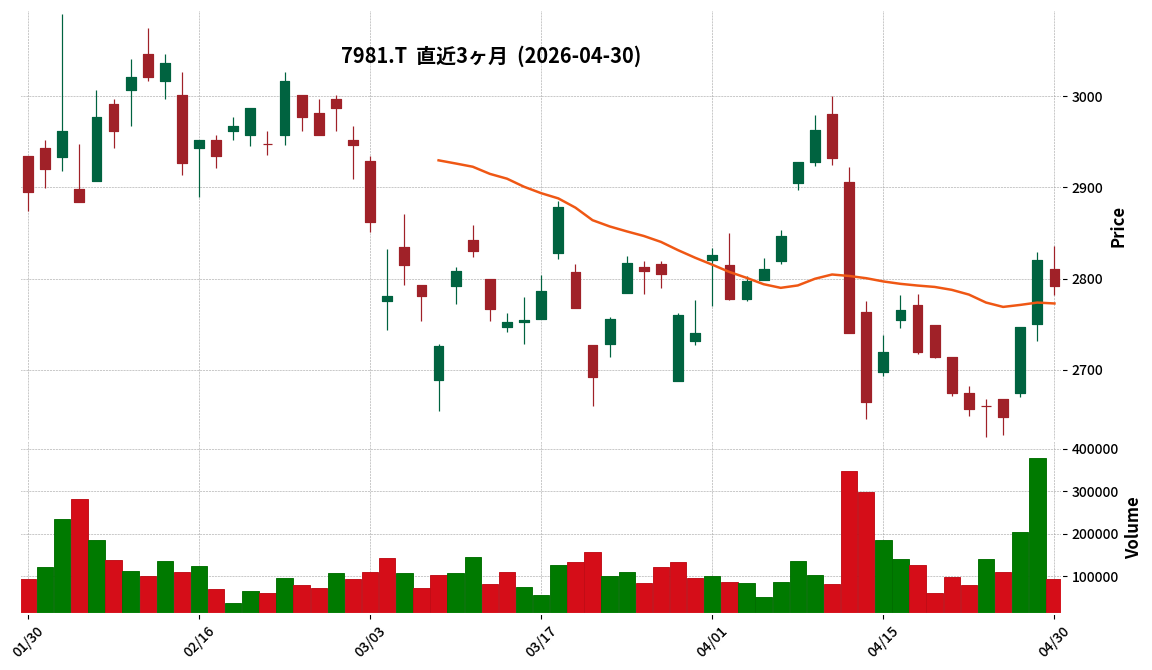

7981|タカラスタン

2792.0

▼ -0.99%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Takara Standard Co., Ltd. announced on April 30, 2026, an increase in year-end dividends for the fiscal year ended March 31, 2026.

- The year-end dividend per share for March 2026 has been set at ¥66.00, an increase of ¥16.00 from the previous forecast of ¥50.00 per share (announced on May 8, 2025).

- Consequently, the projected annual dividend per share will be ¥116.00, representing a ¥38.00 increase compared to the previous fiscal year’s (March 2025) actual dividend of ¥78.00.

- The consolidated dividend payout ratio is expected to be 50.0%. The total dividend amount is ¥4,173 million, with an effective date of June 25, 2026.

- This decision is subject to approval at the 152nd Ordinary General Meeting of Shareholders scheduled for June 2026.

🤖 AI Perspective

This dividend increase aligns with Takara Standard’s stated shareholder return policy within its “Medium-Term Management Plan 2026,” which prioritizes growth investments, strengthening management foundations, and enhancing shareholder returns while maintaining financial soundness. Specifically, it reflects the “New Shareholder Return Policy and Initiatives for Profit Growth towards Achieving ROE 8%” announced on May 8, 2025. The move may indicate the company’s commitment to returning profits to shareholders and could be viewed as a positive signal regarding its capital allocation strategy.

9104|商船三井

6049.0

▲ +1.41%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, Mitsui O.S.K. Lines reported consolidated net sales of JPY 1,825,098 million (up 2.8% year-on-year). Operating profit was JPY 127,002 million (down 15.8%), ordinary profit was JPY 175,839 million (down 58.1%), and profit attributable to owners of parent was JPY 213,260 million (down 49.9%).

- Equity in earnings of affiliates amounted to JPY 41,665 million in FY2026, a significant decrease from JPY 262,368 million in the prior fiscal year.

- The annual dividend for FY2026 was JPY 200.00 per share, comprising an interim dividend of JPY 85.00 and a year-end dividend of JPY 115.00 (down from JPY 360.00 in the prior year).

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of JPY 2,040,000 million (up 11.8% year-on-year), operating profit of JPY 105,000 million (down 17.3%), ordinary profit of JPY 145,000 million (down 17.5%), and profit attributable to owners of parent of JPY 170,000 million (down 20.3%).

- The consolidated equity ratio at the end of the fiscal year was 48.2%.

🤖 AI Perspective

The financial results for FY2026 show a significant decline in profits, particularly ordinary profit and net profit, despite an increase in net sales. This decline appears to be influenced by a substantial reduction in equity in earnings of affiliates compared to the previous year’s high level. The FY2027 forecast indicates a projected increase in sales but further decreases in profits, which may suggest a cautious outlook on the business environment. The reduction in the annual dividend for FY2026 and a modest increase projected for FY2027 could also reflect the company’s adjusted profit expectations.

9201|JAL

2413.0

▼ -2.13%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Japan Airlines Co., Ltd. (JAL, Code 9201) reported consolidated revenue of ¥2,012,515 million for the fiscal year ended March 31, 2026, marking a 9.1% increase year-on-year.

- Profit attributable to owners of the parent for the same period was ¥144,452 million, an increase of 28.2% compared to the previous fiscal year.

- Basic earnings per share stood at ¥306.96.

- The annual dividend for the fiscal year ended March 31, 2026, was announced as ¥96.00, comprising an interim dividend of ¥46.00 and a year-end dividend of ¥50.00.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated revenue of ¥2,095,000 million (up 4.1% year-on-year), while anticipating profit attributable to owners of the parent to decrease by 20.1% to ¥110,000 million.

🤖 AI Perspective

The financial results for the fiscal year ended March 31, 2026, demonstrate robust performance with significant increases in both revenue and profit attributable to owners of the parent. However, the forecast for the fiscal year ending March 31, 2027, projects revenue growth alongside a notable decrease in profit attributable to owners of the parent, which may suggest potential headwinds or increased costs. The unchanged dividend forecast of ¥96.00 for the next fiscal year indicates a consistent approach to shareholder returns.

2892|日食化

3900.0

▼ -1.64%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nisshoku Kako Co., Ltd. (Code: 2892) announced its consolidated financial results for the fiscal year ended March 2026, reporting net sales of JPY 62,993 million, a 0.5% increase year-on-year, and operating income of JPY 1,251 million, up 4.2% from the previous year.

- However, ordinary income decreased by 18.1% to JPY 1,568 million, and profit attributable to owners of parent declined by 23.5% to JPY 1,168 million.

- The company declared an annual dividend of JPY 145.00 per share, an increase from JPY 95.00 in the prior fiscal year. The forecast for FY2027 is an annual dividend of JPY 150.00.

- For the fiscal year ending March 2027, the consolidated earnings forecast projects net sales of JPY 65,500 million (up 4.0%), operating income of JPY 1,900 million (up 51.8%), and profit attributable to owners of parent of JPY 1,500 million (up 28.3%).

- As of the end of March 2026, the equity ratio improved to 59.6% (from 56.7% at the end of the previous fiscal year), and net assets per share reached JPY 6,235.72 (compared to JPY 5,779.32 previously).

🤖 AI Perspective

For the reported fiscal year, the company saw an increase in net sales and operating income, yet a decline in both ordinary and net income, which may present a mixed performance picture. The announced dividend increase and the achievement of the DOE target of 2.5% or more could indicate a focus on shareholder returns. The company’s robust outlook for the next fiscal year, particularly the significant projected growth in operating income, will be a key area for investors to monitor.

2972|R-サンケイRE

124400.0

▲ +0.48%

📎 Source:R-サンケイRE Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- R-Sankei RE reported an impairment loss of JPY 4,933 million related to the “Fukuoka Green Building” in its Q14 (FY2026/2) financial results.

- Due to the impairment loss, the investment corporation recorded a net loss of JPY 4,009 million and decided on zero distribution per investment unit, compared to an initial forecast of JPY 2,773/unit.

- A gratuitous capital reduction of JPY 4,009 million, equal to the current period’s unappropriated loss, has been resolved to enable future distributions from Q15 (FY2026/8) onwards. This will not involve refunds or changes in the total number of investment units outstanding.

- Operating revenue for the period was JPY 2,882 million (up 10.3% year-on-year), while operating loss amounted to JPY 3,323 million (down JPY 4,670 million year-on-year).

- A tender offer for R-Sankei RE’s investment units by Tiger Investment Limited Partnership and Lion Investment Limited Partnership has been ongoing since January 7, 2026, with the investment corporation expressing its support and recommendation for application.

🤖 AI Perspective

The significant impairment loss on a specific property was a primary driver of the reported net loss and zero distribution for the period. The announced capital reduction appears to be a strategic move to reset the financial foundation and facilitate future distributions. Investors may want to consider these developments in light of the ongoing tender offer.

3776|BBタワー

229.0

▼ -3.38%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of the fiscal year ending December 2026 (January 1, 2026, to March 31, 2026), consolidated results show net sales of ¥3,193 million (up 2.9% year-on-year), operating profit of ¥224 million (up 41.0% year-on-year), ordinary profit of ¥226 million (up 46.0% year-on-year), and net income attributable to owners of parent of ¥130 million (up 30.7% year-on-year).

- Diluted earnings per share for the quarter were ¥2.12.

- As of the end of the first quarter, the consolidated financial position indicates total assets of ¥19,394 million, net assets of ¥12,296 million, and an equity ratio of 45.4%.

- The consolidated full-year earnings forecast and the annual dividend forecast for the fiscal year ending December 2026 (totaling ¥2.00) remain unchanged from the most recently announced figures.

- Effective from the current consolidated first quarter, there has been a change in accounting policy regarding the presentation of “cost of sales” in the consolidated statement of income, with prior period figures retrospectively adjusted accordingly.

🤖 AI Perspective

The company achieved significant year-on-year growth across key profit metrics in the first quarter, with increases exceeding 40%. The IR information indicates that this was contributed by an increase in high-margin storage design and construction-related sales within the Data Solution segment of the Computer Platform business. As the company’s cumulative second-quarter and full-year earnings forecasts remain unrevised, monitoring future progress against these targets could be a key point of interest for investors.

4221|大倉工

4875.0

▲ +3.17%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of the fiscal year ending December 2026, Okura Industrial reported consolidated net sales of ¥24,026 million (up 10.8% year-on-year), operating profit of ¥2,245 million (up 33.8%), ordinary profit of ¥2,215 million (up 31.7%), and net income attributable to owners of parent of ¥1,474 million (up 17.8%).

- During this consolidated cumulative quarter, two companies, Fujiko Co., Ltd. and OKURA VIETNAM CO., LTD., were included in the scope of consolidation.

- The Synthetic Resins business saw net sales increase by 16.9% and operating profit by 24.3%, partly due to the consolidation of Fujiko Co., Ltd. The New Materials business recorded a 4.0% increase in net sales and a 63.2% increase in operating profit, driven by strong performance in optical films for large LCD TVs.

- The Building Materials business experienced a 4.2% decrease in net sales due to customer inventory adjustments and a 36.4% decrease in operating profit due to factors including increased expenses for the launch of the Takase Plant.

- The full-year consolidated earnings forecast and annual dividend forecast for the fiscal year ending December 2026 remain unchanged from the most recently published figures.

🤖 AI Perspective

The robust year-on-year growth in consolidated net sales and various profit metrics suggests positive impacts from new consolidations and efforts in productivity improvement. The company’s decision to maintain its full-year earnings forecast indicates management’s confidence in achieving its initial targets. While the Synthetic Resins and New Materials segments showed strong performance, the Building Materials segment faced challenges, which may warrant monitoring in future reports.

2692|伊藤忠食

12920.0

▲ +0.08%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Consolidated net sales for the fiscal year ended March 31, 2026, increased by 3.0% year-on-year to ¥720,217 million.

- Operating profit notably rose by 24.2% year-on-year to ¥10,562 million, and ordinary profit increased by 11.6% to ¥12,591 million.

- Net profit attributable to parent company shareholders grew by 0.8% year-on-year to ¥8,273 million.

- Earnings per share reached ¥652.06, and the equity ratio at the end of the period was 43.9%.

- The consolidated earnings forecast and dividend forecast for the fiscal year ending March 31, 2027, have not been disclosed, as the company is scheduled to be delisted following a share demand by Itochu Corporation, as announced on April 28, 2026.

🤖 AI Perspective

In the current period’s consolidated financial results, the significant double-digit growth in operating profit, alongside a steady increase in net sales, stands out. This could suggest advancements in operational efficiency or profitability improvement initiatives. However, the absence of an earnings and dividend forecast for FY2027, attributed to Itochu Corporation’s share demand and the subsequent planned delisting, indicates a potential shift in the company’s future public information disclosure practices.

4410|ハリマ化成G

899.0

▼ -1.86%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Harima Chemicals Group, Inc. announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- Consolidated net sales for the period reached ¥103,763 million, marking a 2.7% increase compared to the previous fiscal year.

- Consolidated operating profit was ¥3,283 million (up 57.6% year-on-year), and consolidated ordinary profit was ¥2,996 million (up 125.2% year-on-year).

- Profit attributable to owners of parent amounted to ¥2,345 million (up 207.5% year-on-year), with basic earnings per share at ¥96.56.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥110,000 million (up 6.0% year-on-year) and profit attributable to owners of parent of ¥2,650 million (up 13.0% year-on-year).

🤖 AI Perspective

Harima Chemicals Group’s FY2026 results demonstrate a significant increase in profitability across all profit metrics, despite a more moderate rise in net sales, which may suggest enhanced operational efficiency. The substantial surge in profit attributable to owners of parent, exceeding 200% year-on-year, is particularly noteworthy for investors. The positive outlook for FY2027, projecting continued sales and profit growth, could indicate confidence in their business strategies and market position.

5257|ノバシステム

2520.0

▼ -2.14%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of the fiscal year ending December 2026, NOVA SYSTEM reported net sales of ¥1,718 million, representing a 2.4% increase year-on-year, and operating profit of ¥121 million, an increase of 26.6% year-on-year.

- Net profit for the period was ¥69 million, a 4.2% decrease year-on-year, primarily due to the recording of ¥22.5 million in extraordinary losses for retirement benefits to officers.

- Progress against the first half plan was strong, with net sales at 50.5% and operating profit at 73.9%, indicating that both revenue and profit are progressing favorably above plan.

- The company made investments in human capital, including the hiring of 26 new graduates (effective April 1) and 15 mid-career professionals (January-April), and opened a new Yodoyabashi office.

- Under its AI growth strategy, sales for AI-themed projects for banks increased by 21.3% quarter-on-quarter. Additionally, the company established a new Management Strategy Department to promote company-wide AI utilization, advancing phases such as infrastructure development, rule formulation, talent development, and operational initiation.

🤖 AI Perspective

NOVA SYSTEM’s Q1 FY2026 results show solid revenue growth and a significant increase in operating profit, which could suggest effective cost management and project execution. The high operating profit progress against the first-half plan indicates a strong start to the fiscal year.

The concrete progress in AI growth strategies, including increased AI-themed project sales and internal AI utilization initiatives, may suggest the company’s commitment to leveraging AI for future growth and efficiency.

While the reported extraordinary loss impacted net profit, this appears to be a one-off item, and the underlying operational performance remains a key aspect for investors to monitor.

5440|共英製鋼

2023.0

▼ -7.41%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kyoei Steel reported consolidated net sales of ¥315,106 million for the fiscal year ended March 31, 2026, marking a 2.4% decrease year-on-year.

- Consolidated operating profit increased by 10.7% to ¥16,967 million, and ordinary profit rose by 3.0% to ¥16,211 million.

- Net profit attributable to owners of parent decreased by 8.6% to ¥9,864 million.

- In the domestic steel business segment, sales were ¥125,527 million (down 12.0% YoY) and operating profit was ¥11,258 million (down 35.2% YoY). The overseas steel business saw improved performance due to strong steel demand and cost reduction efforts in Vietnam, along with robust demand in North America.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥360,000 million (up 14.2% YoY), operating profit of ¥16,000 million (down 5.7% YoY), ordinary profit of ¥14,000 million (down 13.6% YoY), and net profit attributable to owners of parent of ¥9,000 million (down 8.8% YoY). The annual dividend is projected to decrease from ¥90.00 to ¥70.00 per share.

🤖 AI Perspective

For the fiscal year ended March 2026, Kyoei Steel reported a decrease in revenue, but an increase in consolidated operating and ordinary profits, which appears to be supported by the improved performance of its overseas steel business. While net profit attributable to owners of parent declined, the overseas segment seems to have mitigated the impact of a sluggish domestic steel market. However, the forecast for the fiscal year ending March 2027 indicates an increase in revenue but a decline across all profit metrics, along with a projected reduction in the annual dividend, which investors may find noteworthy.

5938|LIXIL

1595.0

▼ -2.03%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 2026, consolidated revenue was JPY 1,510,704 million, an increase of 0.4% compared to the previous fiscal year.

- Profit attributable to owners of the parent significantly increased by 306.9% year-on-year to JPY 8,143 million.

- Business profit rose by 22.9% to JPY 38,500 million, while operating profit decreased by 4.3% to JPY 28,403 million, and profit before tax decreased by 22.0% to JPY 15,708 million.

- Basic earnings per share were JPY 28.33, up from JPY 6.97 in the prior fiscal year.

- For the fiscal year ending March 2027, the company forecasts consolidated revenue of JPY 1,600,000 million (up 5.9% YoY) and profit attributable to owners of the parent of JPY 12,000 million (up 47.4% YoY).

- The annual dividend for both FY2026/3 and the FY2027/3 forecast is JPY 90.00 per share, with a year-end dividend of JPY 45.00.

🤖 AI Perspective

LIXIL’s FY2026/3 consolidated results show a substantial increase in profit attributable to owners of the parent, despite a modest rise in revenue. The divergence between business profit growth and declines in operating profit and profit before tax suggests specific expense factors between these levels warranting attention. The company’s forecast for FY2027/3 projects growth in both revenue and profit, indicating a positive outlook for the upcoming period.

6325|タカキタ

408.0

▲ +0.99%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 2026 (non-consolidated), Takakita Co., Ltd. reported net sales of JPY 6,548 million, marking a 6.6% decrease year-on-year.

- Operating income for the same period was JPY 326 million (down 5.3% year-on-year), and ordinary income was JPY 376 million (down 5.9% year-on-year).

- Net income for the period stood at JPY 205 million, a significant decrease of 63.7% compared to the previous fiscal year.

- The annual dividend for FY2026 March was JPY 10.00 per share, consisting of an interim dividend of JPY 5.00 and a year-end dividend of JPY 5.00.

- For the fiscal year ending March 2027, the company forecasts an increase in net sales to JPY 7,000 million (up 6.9% year-on-year), operating income to JPY 346 million (up 6.0%), ordinary income to JPY 378 million (up 0.5%), and net income to JPY 248 million (up 20.6%).

🤖 AI Perspective

The fiscal year ended March 2026 saw a decline in both sales and profits, attributed to factors such as reduced demand in the agricultural machinery business and a reaction to gain on sale of investment securities in the previous period.

However, the forecast for FY2027 March indicates an expectation of increased sales and profits across all stages, which could suggest an anticipation of an improving business environment and advancements in in-house production.

The projected maintenance of an annual dividend of JPY 10 per share for two consecutive periods may signal a continued commitment to shareholder returns.

7539|アイナボHD

784.0

▼ -1.38%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Ainavo Holdings Co., Ltd. (Code: 7539) announced its consolidated results for the second quarter (interim period) of the fiscal year ending September 2026, reporting net sales of JPY 48,258 million (up 1.7% year-on-year), operating profit of JPY 1,744 million (up 9.5%), ordinary profit of JPY 1,935 million (up 9.3%), and net profit attributable to parent company shareholders of JPY 1,202 million (up 10.9%).

- Interim basic earnings per share stood at JPY 51.75.

- The consolidated earnings forecast for the full fiscal year ending September 2026 remains unchanged, with projected net sales of JPY 98,500 million, operating profit of JPY 2,100 million, ordinary profit of JPY 2,600 million, and net profit attributable to parent company shareholders of JPY 1,600 million, resulting in basic earnings per share of JPY 68.97.

- The annual dividend forecast also remains unrevised at JPY 26.00 per share (JPY 13.00 for the interim period and JPY 13.00 for the year-end).

- Notably, Ueno Tile Co., Ltd. was newly included within the scope of consolidation from this interim period.

🤖 AI Perspective

The interim consolidated results demonstrate solid performance with year-on-year increases across all key profit metrics. However, the unchanged full-year consolidated earnings forecast, which anticipates a year-on-year decrease in operating profit, ordinary profit, and net profit attributable to parent company shareholders, may warrant investor attention on the company’s performance in the second half. The company has highlighted ongoing challenging market conditions, including a decline in new housing starts and potential impacts from the Middle East situation, making the progress of its growth strategies, such as improving gross profit margins and leveraging M&A, key areas for investors to monitor.

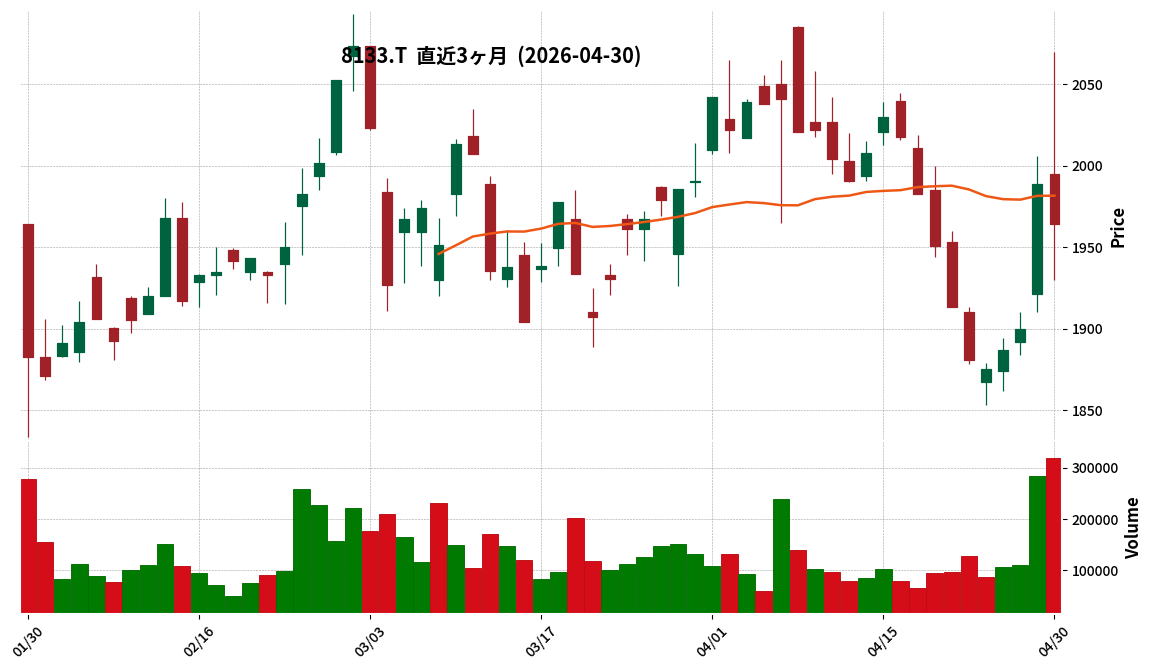

8133|エネクス

1964.0

▼ -1.26%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Itochu Enex announced its consolidated financial results for the fiscal year ended March 31, 2026, reporting revenue of ¥851.235 billion (down 7.9% year-on-year).

- Profit attributable to owners of the parent was ¥16.058 billion, a decrease of 6.1% compared to the previous fiscal year.

- The annual dividend per share for the fiscal year 2026 was set at ¥66, an increase of ¥4 from the previous year, following a change in the year-end dividend to ¥35 per share.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated profit attributable to owners of the parent to be ¥16.500 billion, representing a 2.8% increase from the prior year.

- Cash and cash equivalents at the end of the period increased to ¥21.924 billion from ¥13.931 billion at the end of the previous fiscal year.

🤖 AI Perspective

While the fiscal year 2026 saw a year-on-year decline in revenue and various profit metrics, the company noted that the profit attributable to owners of the parent met its plan. The declared dividend increase and the projected profit growth for the upcoming fiscal year may suggest the company’s confidence in future performance. Improvements in cash and cash equivalents could also indicate strengthening financial liquidity.

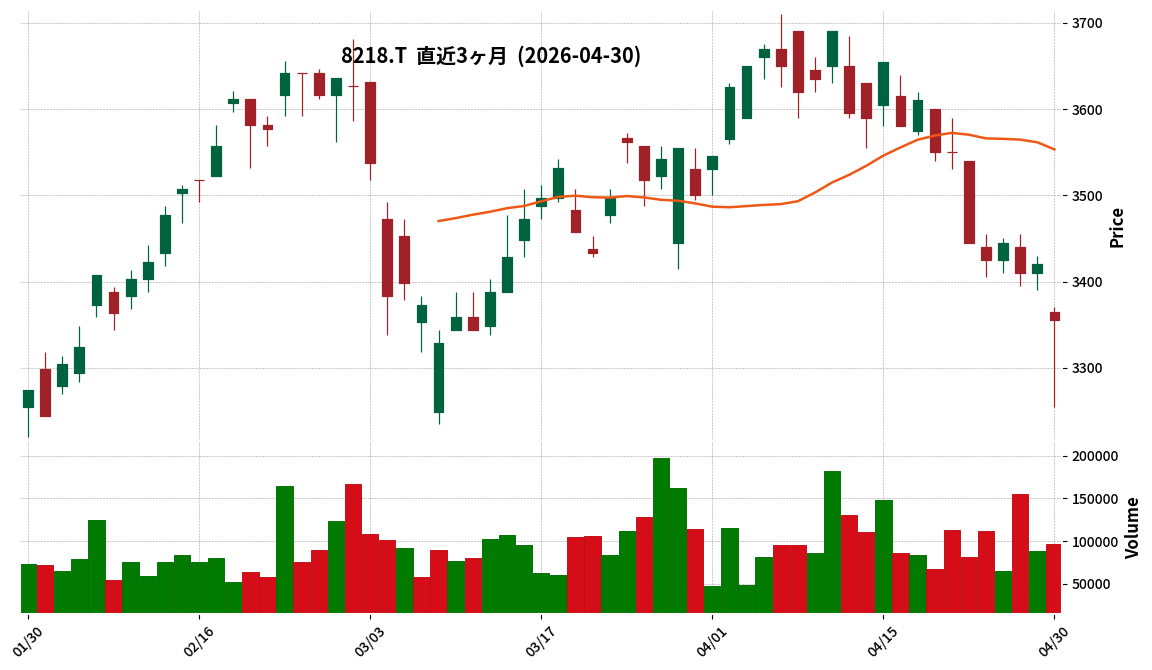

8218|コメリ

3355.0

▼ -1.90%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- KOMERI reported consolidated results for the fiscal year ended March 2026, with operating revenue of ¥385,384 million (up 1.6% year-on-year), operating profit of ¥23,055 million (up 2.9% year-on-year), and net profit attributable to owners of parent of ¥14,645 million (up 6.7% year-on-year).

- By product category, “Gardening, Agriculture, & Pet Supplies” contributed the most with sales of ¥116,313 million (up 3.3% year-on-year), followed by “Tools, Hardware, & Work Supplies” with ¥69,840 million (up 1.8% year-on-year).

- During FY2026, the company opened 22 new stores, renovated 142 existing stores, and commenced operations at the new Kansai Distribution Center, investing a total of ¥25,000 million in capital expenditure.

- For the fiscal year ending March 2027, KOMERI projects consolidated operating revenue of ¥400,800 million (up 4.0% year-on-year), operating profit of ¥24,000 million (up 4.1% year-on-year), and net profit attributable to owners of parent of ¥15,000 million (up 2.4% year-on-year).

- The company’s shareholder return policy is based on progressive dividends, with a planned annual dividend of ¥58 (¥29 interim, ¥29 year-end) for FY2027, marking the 11th consecutive year of dividend increases.

🤖 AI Perspective

KOMERI achieved revenue and profit growth in FY2026, driven by strong performance in its “PRO” format for professionals and agricultural supplies. Continued aggressive investment in new store openings, existing store renovations, and logistics infrastructure may suggest a strategic focus on future business expansion. The plan for an 11th consecutive dividend increase could indicate a strong commitment to shareholder returns.

9362|兵機海運

3850.0

▲ +1.32%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, Hyoki Kaiun reported net sales of ¥13,389 million (down 2.5% year-on-year), operating profit of ¥436 million (down 20.3%), ordinary profit of ¥499 million (down 19.2%), and net profit of ¥397 million (down 8.8%), marking a decrease in both revenue and profit.

- By segment, the shipping business, including domestic and international shipping, saw reduced revenue and profit. In contrast, the port and warehouse business experienced revenue growth due to increased handling of imported food and robust export customs clearance.

- The annual dividend for the fiscal year ended March 31, 2026, was announced at ¥110.00 per share (down ¥5.00 from the previous year).

- The company’s financial position showed total assets of ¥13,042 million and net assets of ¥5,653 million, with the equity ratio improving to 43.3% (from 38.7% in the prior year).

- For the fiscal year ending March 31, 2027, the company forecasts net sales of ¥14,500 million (up 8.3% year-on-year), operating profit of ¥510 million (up 16.8%), ordinary profit of ¥540 million (up 8.0%), and net profit of ¥400 million (up 0.7%), with an annual dividend planned to remain at ¥110.00 per share.

🤖 AI Perspective

The fiscal year 2026 results show a divergence in performance, with the shipping business facing headwinds like steel demand decline and fuel costs, while the port and warehouse segment performed strongly. Despite the profit decrease, the improvement in the equity ratio suggests a potential strengthening of the company’s financial foundation. The forecast for increased revenue and profit in the upcoming fiscal year, coupled with the plan to maintain the annual dividend, may indicate the company’s confidence in its future business outlook.

9830|トラスコ中山

2194.0

▼ -5.10%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of the fiscal year ending December 2026 (January 1 to March 31, 2026), TRUSCO Nakayama recorded consolidated net sales of ¥86,961 million (up 9.8% year-on-year), operating income of ¥6,000 million (up 2.7%), ordinary income of ¥5,908 million (up 1.6%), and net income attributable to owners of parent of ¥4,105 million (up 2.6%).

- The equity ratio as of the end of the first quarter of FY2026 was 56.2%.

- The forecasted annual dividend for FY2026 is ¥58.50 per share, comprising an interim dividend of ¥30.00 and a year-end dividend of ¥28.50. There are no revisions from the latest announced dividend forecast.

- The consolidated full-year earnings forecast for FY2026 remains unchanged, projecting net sales of ¥341,000 million (up 6.5% year-on-year), operating income of ¥21,720 million (down 4.8%), ordinary income of ¥21,220 million (down 5.9%), and net income attributable to owners of parent of ¥14,540 million (down 8.4%).

🤖 AI Perspective

While the first quarter saw increased sales and profits, the full-year consolidated earnings forecast projects a decrease in profits. This may be attributed to a rise in the cost of sales ratio and increases in selling, general, and administrative expenses such as freight, packing costs, salaries, and bonuses. Strategic initiatives like “Niawase + U-Choku” (consolidated shipment + direct user delivery) and “MRO Stocker” appear to contribute to sales growth, but the company’s cost management efforts toward achieving its full-year profit targets could be a point of focus for investors.

7896|セブン工

501.0

▼ -0.20%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Seven Kogyo Co., Ltd. announced its non-consolidated financial results for the fiscal year ended March 31, 2026.

- Net sales for the period were ¥15,589 million, representing a 1.1% increase year-on-year.

- The company reported an operating loss of ¥56 million, an ordinary loss of ¥60 million, and a net loss of ¥127 million, marking a shift from profit to loss compared to the previous fiscal year.

- For the fiscal year ending March 31, 2027, the company forecasts net sales of ¥16,765 million (up 7.5% year-on-year), an operating profit of ¥135 million, an ordinary profit of ¥110 million, and a net profit of ¥45 million, projecting a return to profitability.

- The annual dividend was ¥20.00 (¥10.00 year-end) for both FY2025/3 and FY2026/3, with a forecast to maintain ¥20.00 for FY2027/3.

🤖 AI Perspective

While net sales increased in the fiscal year ended March 2026, the company recorded losses across operating, ordinary, and net income metrics. This performance may be attributed to factors such as sluggish demand in the core detached housing market, rising material costs, intensified price competition, and upfront investments in facilities. However, the forecast for a return to profitability with increased sales and earnings in the fiscal year ending March 2027 could suggest a positive outlook for future business improvements.

2216|カンロ

1124.0

▼ -3.68%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kanro Co., Ltd. announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026 to March 31, 2026).

- Consolidated results for the first quarter showed net sales of ¥8,710 million, operating profit of ¥1,399 million, ordinary profit of ¥1,407 million, and net income attributable to owners of parent of ¥993 million. Year-on-year growth rates are not provided as consolidated financial statements for the same period in the previous fiscal year were not prepared.

- As of the end of the first quarter, total assets stood at ¥30,573 million, net assets at ¥19,249 million, and the equity ratio was 63.0%.

- The forecast for the annual dividend for the fiscal year ending December 2026 remains unchanged from the most recently announced forecast, set at ¥33.00 per share (interim ¥15.00, year-end ¥18.00). This forecast is adjusted for the 3-for-1 stock split effective July 1, 2025.

- The consolidated earnings forecast for the full fiscal year ending December 2026 remains unchanged from the announcement made on February 13, 2026, projecting net sales of ¥36.5 billion (+5.0% year-on-year), operating profit of ¥4.9 billion (+4.4% year-on-year), ordinary profit of ¥4.9 billion (+3.2% year-on-year), and net income attributable to owners of parent of ¥3.45 billion (+2.1% year-on-year).

🤖 AI Perspective

- The absence of year-on-year comparison data for the first quarter of the fiscal year ending December 2026, due to this being the first time consolidated financial statements for the period were prepared, may make direct historical performance assessment challenging for investors.

- Despite a decline in demand for throat candies, the company reported increased sales, driven by strong performance in other candy categories, the gummy segment, high-value products like “GummyTzel,” and growing sales from its U.S. subsidiary.

- While fixed costs, including personnel expenses and depreciation from a new core system, increased, these were absorbed by higher sales, suggesting that the company is managing to balance its operational investments with revenue growth.

3992|ニーズウェル

459.0

▲ +0.22%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- NeedsWell Co., Ltd. announced an upward revision to its consolidated earnings forecast for the second quarter (interim period) of the fiscal year ending September 2026, effective April 30, 2026.

- The revised forecast includes revenue of ¥5,206 million (up 0.1% from previous), operating profit of ¥608 million (up 1.5%), ordinary profit of ¥621 million (up 3.6%), and net profit attributable to owners of the parent of ¥406 million (up 1.7%).

- Reasons for the revision include robust performance in solutions and system development, which is expected to result in record-high first-half sales, along with improved project profitability and enhanced productivity.

- While profit items show a decrease compared to the prior year, this is attributed to a change in the timing of recording expenses related to the shareholder benefit program, with a minor impact on full-year performance.

- The full-year consolidated earnings forecast for the fiscal year ending September 2026 remains unchanged at this time, considering potential strategic investments in human resources, R&D, and new businesses to accelerate growth.

🤖 AI Perspective

NeedsWell’s upward revision for its Q2 FY2026 consolidated earnings forecast suggests a strong performance in its solutions and system development segments. The expectation of record-high first-half sales could be interpreted as an indication of the company’s strengthening core earnings power. However, the decision to keep the full-year forecast unchanged may lead investors to monitor the timing and impact of planned growth investments on future results.

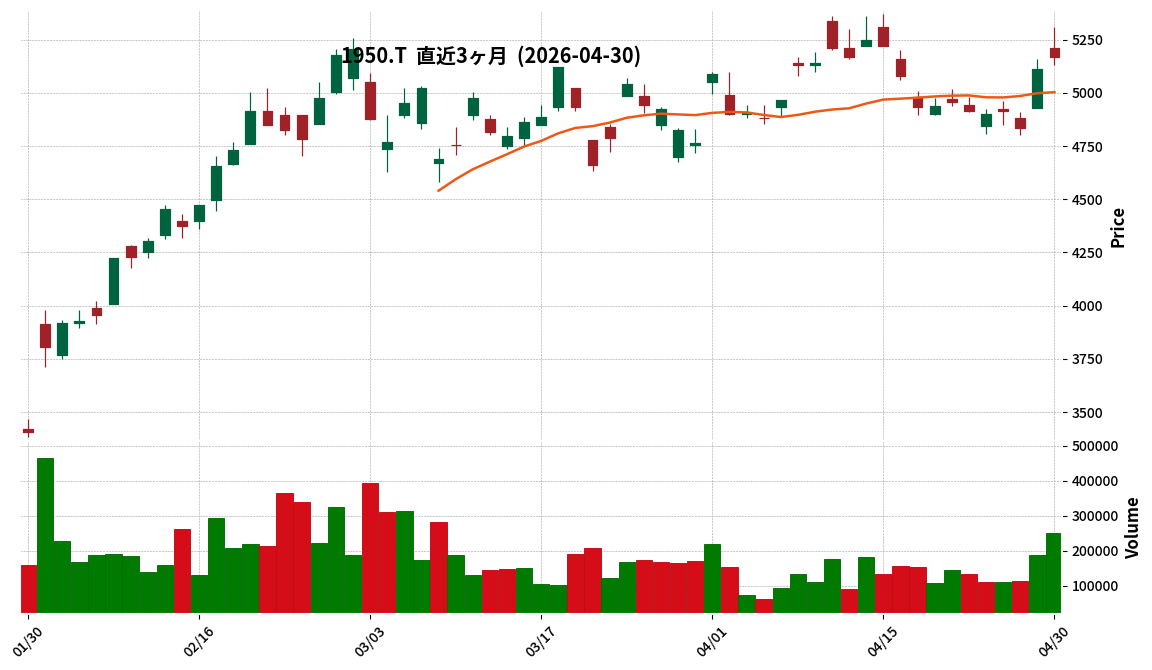

1950|日本電設

5170.0

▲ +1.17%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nippon Densetsu Kogyo Co., Ltd. resolved at its Board of Directors meeting held on April 30, 2026, to increase the year-end dividend for the fiscal year ended March 31, 2026.

- The per-share dividend for the fiscal year ended March 2026 is planned to be ¥124.00, an increase of ¥9 from the most recent forecast (¥115.00, announced on January 30, 2026). The previous fiscal year’s (March 2025) dividend was ¥90.00.

- The total dividend amount is ¥7,429 million, with the dividend source being retained earnings. The effective date is scheduled for June 29, 2026.

- The company also announced a per-share dividend forecast of ¥127.00 for the next fiscal year ending March 2027, which represents an increase of ¥3 from the planned dividend of ¥124.00 for the current fiscal year.

- This dividend proposal is scheduled to be submitted for approval at the 84th Ordinary General Meeting of Shareholders on June 26, 2026.

🤖 AI Perspective

Nippon Densetsu Kogyo’s announcement reveals an increase in the year-end dividend for the fiscal year ending March 2026 from the initial forecast, coupled with a further dividend increase projected for the subsequent fiscal year ending March 2027. The company’s policy to consistently provide stable dividends in line with growth, with a target payout ratio of 40%, appears to underpin these decisions. This multi-period upward trend in dividends could be seen as a notable point for investors to consider.

6888|アクモス

560.0

▼ -0.18%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Acmos Co., Ltd. reported consolidated net sales of JPY 5,698 million for the third quarter of fiscal year 2026 (cumulative period), representing a 17.6% increase year-on-year.

- For the same period, operating profit was JPY 409 million (down 17.2% year-on-year), ordinary profit was JPY 412 million (down 17.3% year-on-year), and net profit attributable to owners of parent was JPY 250 million (down 22.3% year-on-year).

- The primary cause for the decrease in profit was the increase in selling, general and administrative expenses, including personnel costs.

- Acmos acquired 100% of the shares of Systems Service Co., Ltd. (SYS) on January 29, 2026, making it a wholly-owned subsidiary, with an absorption-type merger scheduled for October 1, 2026.

- The consolidated full-year earnings forecast for fiscal year 2026 has been revised, as announced in the “Notice of Revision of Earnings Forecast” published today (April 30, 2026).

🤖 AI Perspective

While sales increased in this quarter, the rise in operating expenses, particularly personnel costs, appears to have pressured profits. Strategic moves such as the acquisition and planned merger of SYS, alongside an increase in employee numbers, could indicate investments aimed at medium-term business growth. The revision of the full-year earnings forecast suggests adjustments to the company’s outlook, which may be a key point for investors to monitor.

7441|Misumi

—

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Misumi Co., Ltd. announced the finalization of the financial results for its parent company, Sankaku Kaihatsu Co., Ltd., for the fiscal year ended January 2026.

- Sankaku Kaihatsu Co., Ltd. operates golf courses and holds 26.2% of Misumi Co., Ltd.’s voting rights as of January 31, 2026.

- For the fiscal year ended January 2026 (February 1, 2025, to January 31, 2026), sales were ¥505,893 thousand, and operating income was an operating loss of △¥29,930 thousand.

- Despite the operating loss, the company recorded ordinary income of ¥70,264 thousand and net income of ¥56,085 thousand, primarily due to non-operating income, including ¥74,686 thousand in dividends received.

- Sankaku Kaihatsu Co., Ltd.’s Representative Director and President, Kosaburo Misumi, also serves as Honorary Chairman of Misumi Co., Ltd., and Director Tsunenori Oka also serves as Representative Director Group CEO of Misumi Co., Ltd.

🤖 AI Perspective

The financial results of a parent company can offer insights into the broader operational and strategic context for Misumi Co., Ltd. It appears that Sankaku Kaihatsu Co., Ltd. offset an operating loss with substantial non-operating income, particularly dividends received from investment securities, which could suggest a specific financial strategy or asset allocation within the group. The cross-appointment of directors between Misumi and its parent company also implies a close management relationship, which investors might consider when evaluating the overall governance and strategic alignment.

9534|北海瓦斯

885.0

▼ -3.49%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hokkaido Gas Co., Ltd. has announced an upward revision to its year-end dividend forecast for the record date of March 31, 2026.

- The year-end dividend forecast has been revised to JPY 13.00 per share, an increase of JPY 1.50 from the previous forecast of JPY 11.50 per share.

- This revision results in an anticipated annual dividend of JPY 24.50 per share for the fiscal year ending March 2026 (comprising the H1 actual dividend of JPY 11.50 and the revised year-end forecast of JPY 13.00).

- The company states the reason for the revision is solid business performance, including expanded sales volumes, aligning with its dividend policy of progressive dividends and a target DOE (Dividend on Equity) of 2.5%.

- This matter is scheduled to be decided at the Board of Directors meeting expected to be held on May 25, 2026, following audits by the company’s accounting auditors and Audit & Supervisory Board.

🤖 AI Perspective

This upward revision of the year-end dividend forecast may suggest Hokkaido Gas’s commitment to shareholder returns, supported by its strong operational performance and clear dividend policy targeting a 2.5% DOE. The company’s adherence to a progressive dividend approach, alongside robust business trends, could be a key factor for investors to consider. It is worth monitoring how this revised dividend aligns with the company’s future financial outlook and capital allocation strategies.

4098|チタン工

1009.0

▼ -1.66%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Titan Kogyo Co., Ltd. announced the expected recognition of deferred tax assets for the fiscal year ending March 2026, projecting an adjustment of △JPY 34 million in income taxes.

- The company revised its consolidated full-year financial forecast for the fiscal year ending March 31, 2026, raising the net profit attributable to owners of parent from JPY 100 million to JPY 200 million, representing a 100.0% increase.

- Operating profit for the same period was revised upwards from JPY 240 million to JPY 290 million, and ordinary profit from JPY 170 million to JPY 240 million.

- Net sales were revised downwards from JPY 8,700 million to JPY 8,100 million (a △6.9% decrease) due to sluggish shipments in titanium oxide-related and iron oxide-related businesses.

- The year-end dividend forecast for the fiscal year ending March 31, 2026, was revised upwards from JPY 10.00 to JPY 12.00 per share, with the annual dividend expected to be the same amount.

🤖 AI Perspective

The recognition of deferred tax assets and thorough cost reductions appear to be key factors contributing to the significant upward revision of net profit and increased dividend, despite a downward revision in net sales. This may suggest that the company has improved its profitability through internal efforts separate from sales volume. The revised dividend forecast could indicate management’s confidence in the company’s financial standing and future business developments, balanced with its stable dividend policy.

4463|日華化学

1638.0

▼ -0.06%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nicca Chemical Co., Ltd. reported consolidated results for the first quarter of the fiscal year ending December 2026, with net sales of ¥15,017 million (up 13.8% year-on-year), operating income of ¥1,159 million (up 35.4%), and ordinary income of ¥1,176 million (up 46.2%).

- Net income attributable to owners of parent significantly increased by 214.0% year-on-year to ¥919 million, with basic earnings per share at ¥57.78.

- In the Chemicals segment, sales rose by 18.5% to ¥11,530 million, and segment profit increased by 39.0% to ¥1,499 million, marking record-high sales, segment profit, and segment profit margin for a first quarter.

- The Cosmetics segment recorded a slight decrease in sales by 0.4% to ¥3,287 million and a decrease in segment profit by 28.5% to ¥187 million.

- The full-year consolidated earnings forecast for the fiscal year ending December 2026 remains unchanged, projecting net sales of ¥58,500 million, operating income of ¥4,200 million, ordinary income of ¥4,050 million, and net income attributable to owners of parent of ¥2,800 million. The annual dividend forecast is also unchanged at ¥70.00 per share.

🤖 AI Perspective

The significant year-on-year increases in net sales and various profit metrics for Q1 FY2026, especially the substantial surge in net income attributable to owners of parent, appear to be primarily driven by the robust performance of the Chemicals segment. While the full-year forecast remains consistent with previous announcements, investors may closely monitor if the company can sustain this strong momentum throughout the subsequent quarters. The diverging performance between the Chemicals and Cosmetics segments could also be a point of interest for market participants.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

6557|G-AIAI

1154.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- AIAI Group Corporation announced on April 30, 2026, an upward revision to its consolidated earnings forecast for the full fiscal year ending March 31, 2026 (April 1, 2025, to March 31, 2026).

- The newly announced forecast projects net sales of JPY 14.6 billion, EBITDA of JPY 1.78 billion, operating profit of JPY 1.1 billion, ordinary profit of JPY 930 million, and profit attributable to owners of parent of JPY 620 million.

- Compared to the previous forecast (announced on January 30, 2026), net sales are up 1.4%, EBITDA up 22.8%, operating profit up 46.7%, ordinary profit up 55.0%, and profit attributable to owners of parent up 24.0%.

- The reasons for the upward revision include an improved acquisition rate of local government subsidies, the impact of year-end adjustments for operational consignment subsidies, and increased child enrollment due to new facilities and business acquisitions.

- The increased net sales from these factors are expected to absorb rising costs, such as those for promoting improved childcare worker benefits and M&A expenses for expanding the “AIAI Sanku-ken” initiative, leading to higher profit figures.

🤖 AI Perspective

The significant increase in profit figures, particularly a 46.7% rise in operating profit and a 55.0% rise in ordinary profit, despite a more modest 1.4% increase in net sales, may suggest an improvement in profitability or effective cost management. This performance could indicate that the company’s growth strategies, including new facility openings and business acquisitions, are translating into enhanced financial results. Investors might find it worthwhile to monitor the sustainability of these factors in future reports.

7063|G-Birdman

102.0

▲ +2.00%

📎 Source:G-Birdman Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Birdman Co., Ltd. resolved on April 30, 2026, at its Board of Directors meeting, to enter into a business alliance with Pylon Technologies Japan Inc., including a distributorship agreement, and to commence a new business.

- Through this alliance, G-Birdman will become a domestic distributor for Pylon Technologies Japan Inc., acquiring reselling rights for their battery storage products (industrial and residential) in Japan.

- Pylon Technologies Japan Inc. is the Japanese subsidiary of Pylon Technologies Co., Ltd., which ranked #1 globally in household battery energy storage system (BESS) shipments in 2022 (S&P Global Commodity Insights survey).

- G-Birdman states that this partnership will establish a “vertically integrated model for energy solutions business,” covering “energy creation,” “provision of storage devices,” and “optimization of operations,” aiming to secure a robust revenue structure.

- The new business is scheduled to commence on May 1, 2026. While the impact on consolidated performance for the fiscal year ending June 2026 is expected to be minor, it is projected to contribute significantly to mid-to-long term performance growth from the fiscal year ending June 2027 onwards.

🤖 AI Perspective

- For G-Birdman, which has positioned renewable energy as a core growth strategy, this alliance with a globally leading battery storage system supplier like Pylontech Japan could significantly enhance its business competitiveness.

- The establishment of a “vertically integrated model for energy solutions business” may be a strategic initiative to secure a robust revenue structure amidst market shifts, such as the transition to the FIP scheme and the expansion of the electricity supply-demand adjustment market.

- As the alliance is expected to contribute significantly to performance from the fiscal year ending June 2027, the long-term impact on the company’s growth and earnings will be worth monitoring.

7779|G-サイバダイン-議

295.0

▼ -1.99%

📎 Source:G-サイバダイン-議 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- CYBERDYNE Inc. announced its shareholder benefit program for fiscal year 2026 on April 30, 2026.

- The updated program introduces a new “First-time Benefit,” offering shareholders holding 10 or more units one free trial of the HAL Lumbar Type Short-term Program. This can be combined with either the “A Course” or “B Course.”

- The “A Course” provides discounts on the Neuro HALFIT Personal Rental Program (3 months or more), while the “B Course” offers percentage discounts on the Neuro HALFIT One-on-One Program (10 sessions), varying by shareholding.

- The benefits are applicable to shareholders registered as of March 31, 2026, and will be valid from June 2026 through the end of May 2027.

🤖 AI Perspective

This revision to the shareholder benefit program may suggest CYBERDYNE’s commitment to both shareholder returns and its corporate philosophy of contributing to “Good Health and Well-Being,” one of the UN SDGs. The introduction of the “First-time Benefit” could also serve to broaden awareness and encourage wider adoption of the Neuro HALFIT program, potentially expanding its user base. Investors may view this as an initiative that aligns corporate social responsibility with business strategy.

7947|エフピコ

2296.0

▼ -3.29%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- F-pico Co., Ltd. (Code: 7947) announced on April 30, 2026, that its Board of Directors resolved to revise the year-end dividend forecast for the fiscal year ending March 2026.

- The year-end dividend forecast for the fiscal year ending March 31, 2026, has been revised upwards by JPY 1.50 per share, from JPY 40.00 to JPY 41.50.

- This revision results in an adjusted total annual dividend forecast of JPY 73.00 per share, up from the previous JPY 71.50.

- The revision is attributed to net profit attributable to parent company exceeding initial business forecasts, in line with the company’s progressive dividend policy targeting a consolidated payout ratio of 40%. The revised estimated consolidated payout ratio is 39.7%.

🤖 AI Perspective

This dividend increase aligns with the company’s stated progressive dividend policy, which targets a consolidated payout ratio of 40%. The fact that net profit attributable to the parent company exceeded forecasts may suggest a stronger-than-expected financial performance for the period.

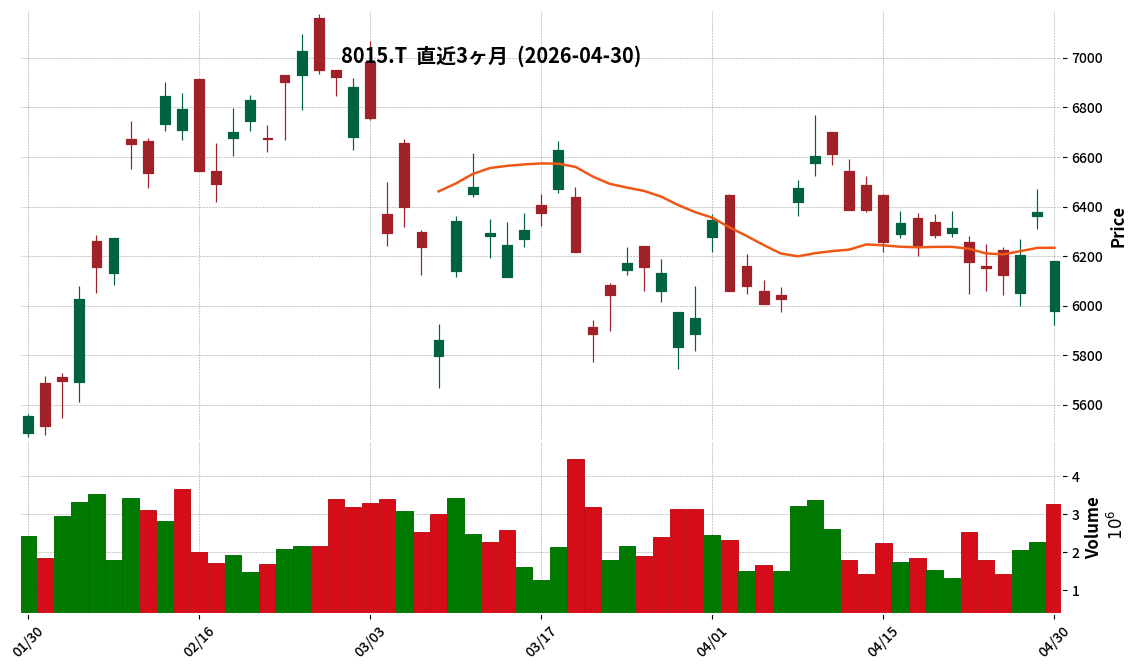

8015|豊田通商

6163.0

▼ -3.39%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Consolidated revenue for the fiscal year ended March 31, 2026, totaled 11,561,935 million yen, marking a 12.1% increase year-on-year.

- Profit attributable to owners of the parent reached 370,516 million yen, up 2.2% from the previous fiscal year.

- The annual dividend for FY2026 was set at 120.00 yen per share (58.00 yen interim, 62.00 yen year-end), an increase from 105.00 yen in the prior year.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated profit attributable to owners of the parent to be 400,000 million yen (an 8.0% increase year-on-year) and an annual dividend of 125.00 yen per share (62.00 yen interim, 63.00 yen year-end).

- Non-consolidated net profit for FY2026 was 463,767 million yen, a 69.7% increase year-on-year, primarily due to a 263,777 million yen increase in gain on sale of investment securities and equity interests, resulting from the sale of all ordinary shares of Toyota Industries Corporation owned by the company.

🤖 AI Perspective

Toyota Tsusho’s FY2026 consolidated financial results indicate growth in both revenue and profit attributable to owners of the parent, suggesting a general expansion in business activities. The increase in the annual dividend and the forecast for further growth in both profit and dividend for FY2027 may reflect the company’s commitment to shareholder returns and its outlook on future earnings. The substantial rise in non-consolidated net profit can be attributed to the contribution of a specific asset sale during the period.

9914|植松商会

954.0

▲ +2.47%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Uematsu Shohkai announced its non-consolidated financial results for the fiscal year ended March 2026, reporting net sales of JPY 6,631 million, a 5.2% increase year-on-year.

- Operating profit surged by 93.5% to JPY 85 million, ordinary profit increased by 29.1% to JPY 182 million, and net income rose by 44.0% to JPY 124 million, indicating substantial profit growth.

- The self-capital ratio improved from 61.8% at the end of the previous fiscal year to 67.7%, with earnings per share reaching JPY 55.35.

- By product category, sales of “Industrial Machinery” increased by 8.4% and “Tools” by 4.6%, while “Machines” saw an 11.7% decrease.

- For the fiscal year ending March 2027, the company forecasts net sales of JPY 6,800 million (up 2.5% year-on-year) and net income of JPY 113 million (down 8.9% year-on-year). An annual dividend of JPY 32.50 per share is planned.

🤖 AI Perspective

The significant increase in profits for FY2026 appears to be driven by higher net sales, effective cost control, and the recording of gains from the sale of investment securities. The notable improvement in the self-capital ratio suggests a strengthening of the company’s financial health. However, while the forecast for FY2027 anticipates continued revenue growth, the projected decline in net income may be a point of interest for investors to monitor for further details regarding its underlying factors.

9235|G-売れるネットG

549.0

▼ -0.90%

📎 Source:G-売れるネットG Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Ureru Net Advertising Group Co.,Ltd. has completed the acquisition of “ADWAYS CHINA” and “ADWAYS ASIA” from Adways Inc. (TYO: 2489).

- The acquired businesses reported an annual transaction volume of ¥3.3 billion and a net profit of ¥7 million for the fiscal year ending December 2025.

- This M&A provides the company with a strategic foothold for full-scale entry into the world’s largest EC and SNS market in China, immediately gaining a business foundation with an annual transaction volume of approximately ¥3.3 billion.

- The acquired businesses offer solutions in app marketing, brand advertising support, and live commerce/EC.

- The company aims to achieve consolidated sales of ¥10 billion and a market capitalization of over ¥25 billion by 2028, with a plan to execute continuous strategic M&As of comparable scale.

🤖 AI Perspective

This acquisition positions G-Ureru Net Advertising Group for significant global expansion beyond the domestic market, particularly into China’s vast digital advertising and e-commerce landscape. The immediate acquisition of a profitable business unit suggests a strategy to secure instant revenue contribution and diversify its service portfolio. Investors may view this as a concrete step towards achieving the company’s ambitious mid-term financial targets, including the ¥10 billion sales and ¥25 billion market capitalization goals by 2028.

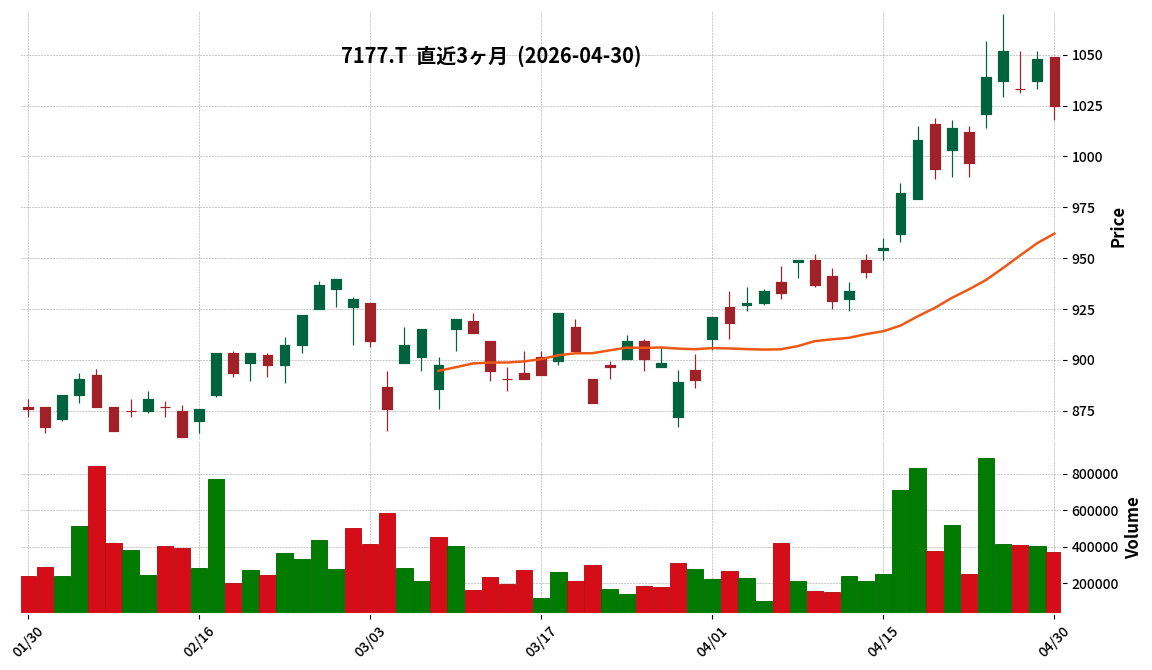

7177|GMOFHD

1025.0

▼ -2.19%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- GMO Financial Holdings reported record quarterly performance for Q1 FY2026 (January 1 – March 31, 2026), with operating revenue reaching ¥16.23 billion and operating profit ¥6.46 billion.

- Operating profit increased by 53.1% year-on-year, and the operating profit margin improved to 39.8% (+7.3 percentage points YoY).

- CFD (Contracts For Difference) revenue expanded 3.5 times year-on-year to ¥6.40 billion, becoming the primary driver of overall performance, particularly due to increased trading volume in high-profit commodity CFDs like gold, silver, and crude oil.

- The company completed the acquisition of LASHIC Small Amount Short Term Insurance Co., Ltd. on March 27, 2026, marking a full-scale entry into the small amount short term insurance business.

- Shareholder return policy was strengthened with the introduction of a dividend payout ratio of 65% or more and a minimum DOE (Dividend on Equity) indicator of 10%. Consequently, the full-year dividend forecast for FY2026 was raised from ¥42.08 to ¥54.76, resulting in a Q1 dividend per share of ¥13.69.

🤖 AI Perspective