📌 Today’s Highlights

Today we cover 80 IR announcements. Notable among them: 橋本総業HD (7570), G-note (5243), ヨドコウ (5451). Use the table of contents below to navigate to each company.

- 7570|橋本総業HD

- 5243|G-note

- 5451|ヨドコウ

- 3401|帝人

- 4203|住友ベーク

- 9739|NSW

- 4404|ミヨシ油脂

- 9101|郵船

- 2790|ナフコ

- 5035|G-HOUSEI

- 3777|G-環境フレンドリー

- 7443|横浜魚類

- 1807|佐藤渡辺

- 3447|信和

- 4624|イサム塗料

- 5660|神鋼鋼線

- 6364|AIRMAN

- 6928|エノモト

- 7636|ハンズマン

- 9273|コーア商事HD

- 3577|東海染工

- 7199|プレミアグループ

- 2903|シノブフーズ

- 4186|東応化

- 4189|KHネオケム

- 5867|G-エスネット

- 7994|オカムラ

- 8850|スターツ

- 9304|渋沢倉

- 1813|不動テトラ

- 1783|fantasista

- 5713|住友鉱

- 1447|G-SAAFHD

- 1826|佐田建

- 204A|P-タイヨーパッケー

- 2763|エフティグループ

- 2816|ダイショー

- 4091|日本酸素HD

- 4202|ダイセル

- 4491|Cマネージメント

- 4633|サカタインクス

- 7931|未来工業

- 9342|G-スマサポ

- 130A|G-VIS

- 1375|ユキグニファクトリー

- 1414|ショーボンド

- 189A|G-D&Mカンパニー

- 1992|神田通機

- 265A|G-エイチエムコム

- 3070|G-ジェリービーンズ

- 3288|オープンハウスG

- 3294|イーグランド

- 3317|フライングG

- 3970|G-イノベーション

- 4385|メルカリ

- 438A|G-インフキュリオン

- 4553|東和薬品

- 4568|第一三共

- 4627|ナトコ

- 6632|JVCKW

- 2811|カゴメ

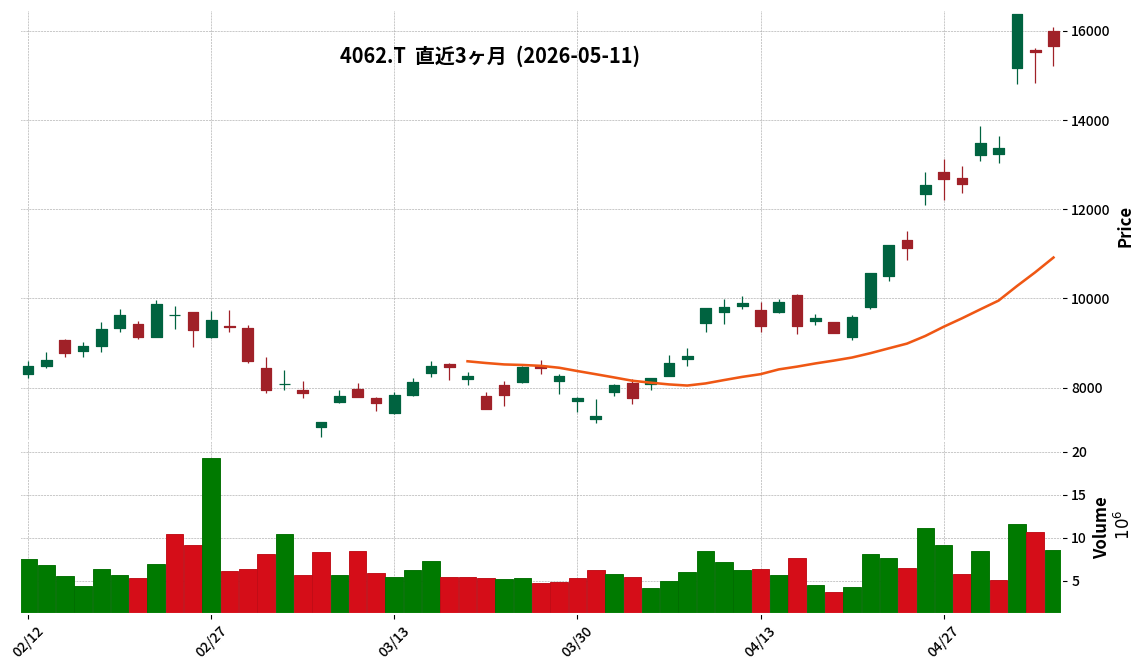

- 4062|イビデン

- 4884|G-クリングル

- 4960|ケミプロ化成

- 9664|御園座

- 208A|構造計画HD

- 2902|太陽化

- 3276|JPMC

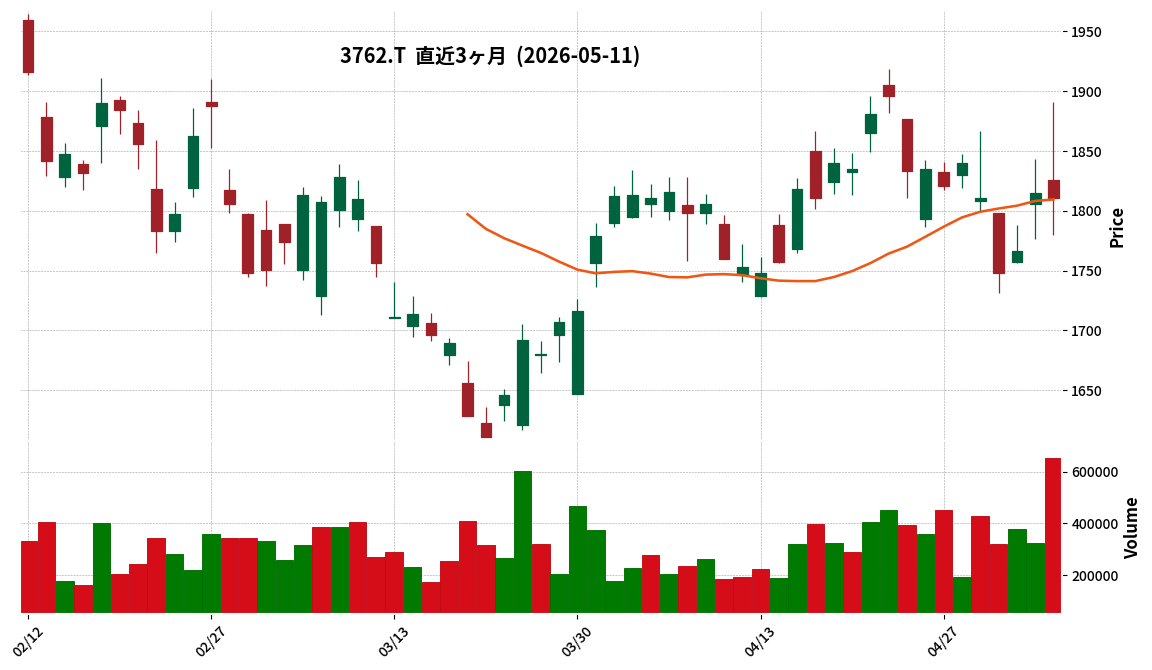

- 3762|テクマト

- 4366|ダイトーケミックス

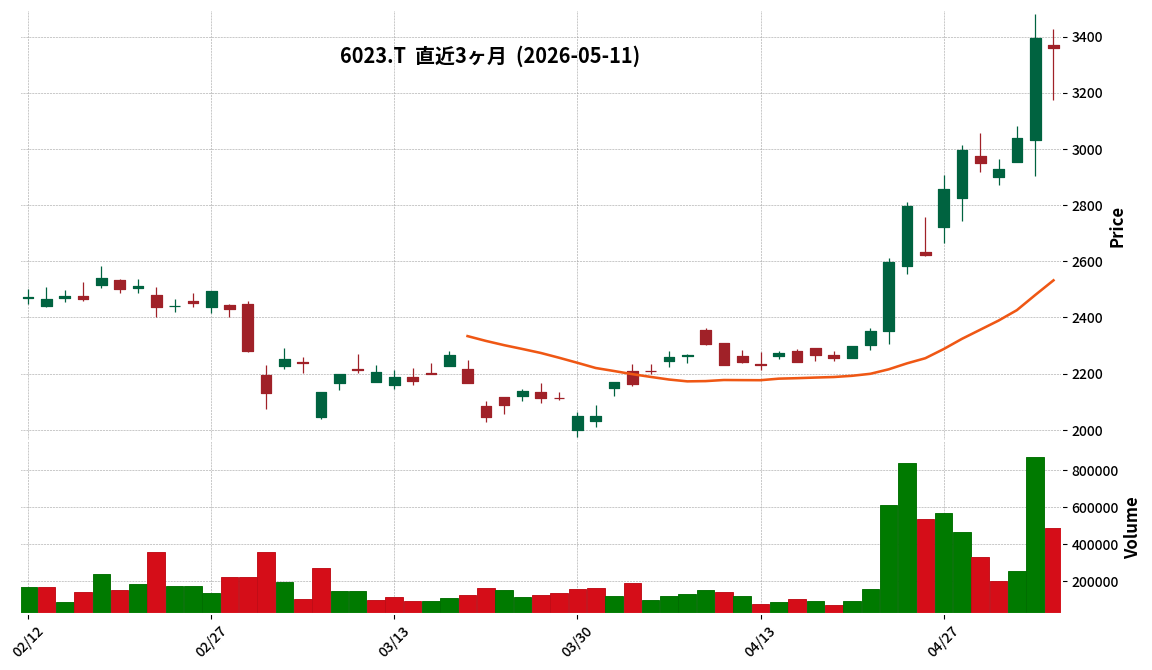

- 6023|ダイハツインフィ

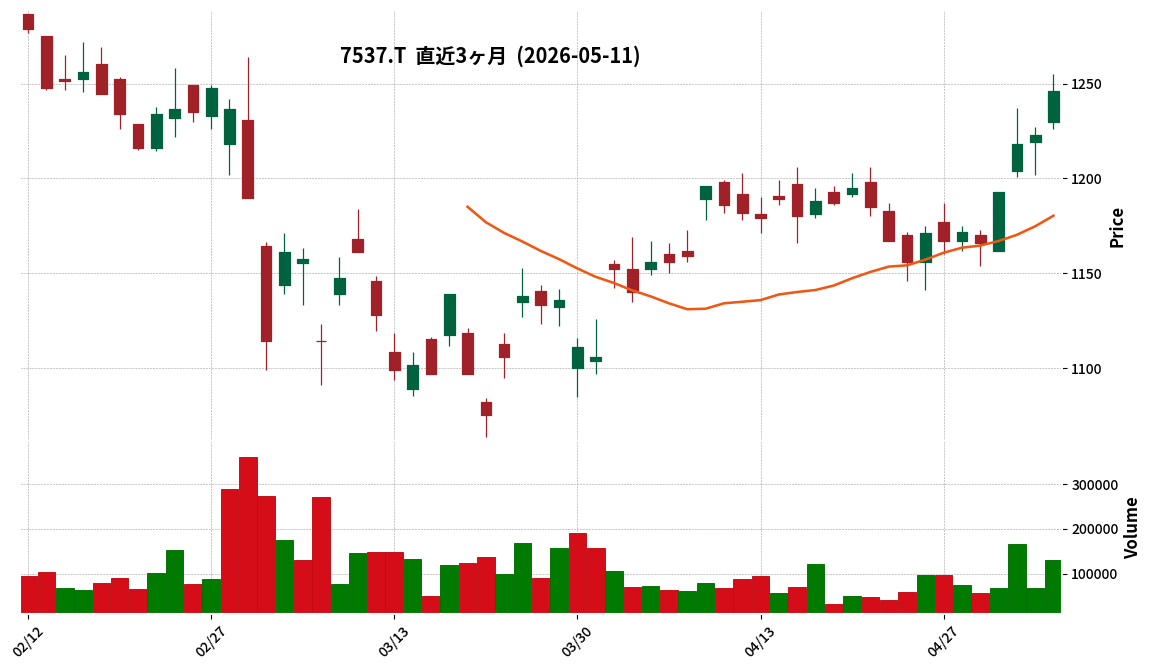

- 7537|丸文

- 7846|パイロット

- 8518|アジア投資

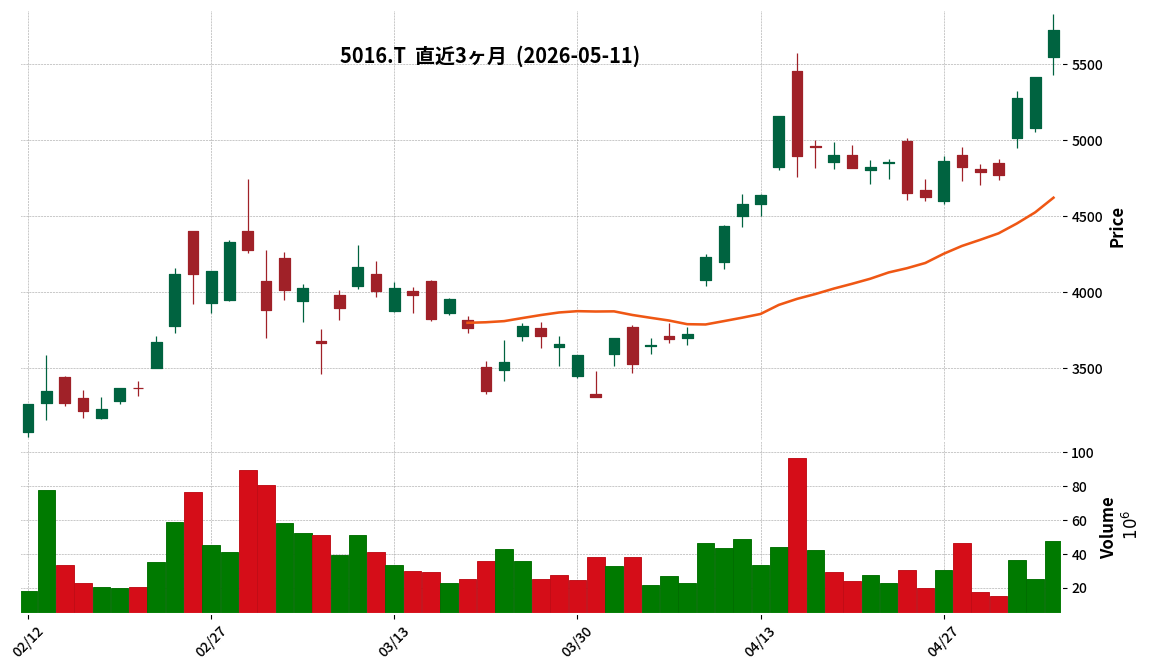

- 5016|JX金属

- 1787|ナカボーテック

- 2162|nms HD

- 6466|TVE

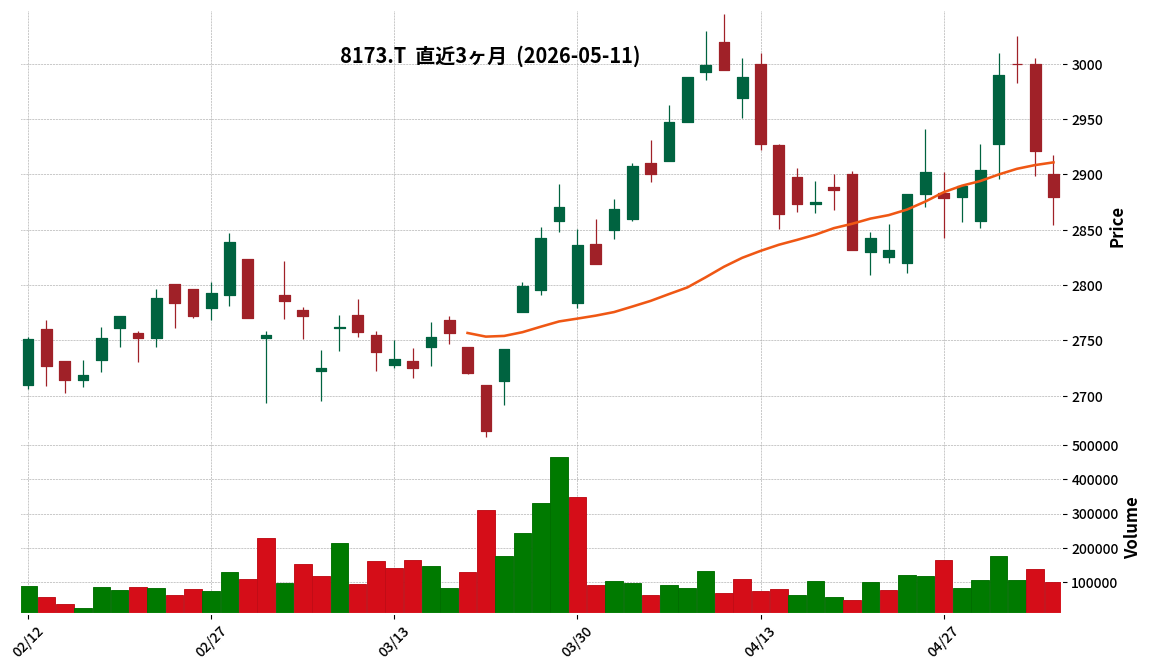

- 8173|Joshin

- 9942|ジョイフル

7570|橋本総業HD

1308.0

▲ +2.19%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- On May 11, 2026, Hashimoto Sogyo Holdings Co., Ltd. (TSE Standard, Code: 7570) announced its dividend forecast for the fiscal year ending March 2027.

- The company plans to pay an annual dividend of JPY 52.00 per share for the fiscal year ending March 2027, consisting of JPY 26.00 for the interim and JPY 26.00 for the year-end dividend.

- This represents a JPY 2.00 increase from the previous fiscal year (March 2026), which had an annual dividend of JPY 50.00 (JPY 25.00 interim, JPY 25.00 year-end).

- With this increase, the company is set to achieve its 11th consecutive year of dividend increases, including commemorative dividends.

- The company’s basic policy for profit distribution includes stable dividends through improved profitability, performance-linked shareholder returns, and maintaining a strong management foundation through internal reserves.

🤖 AI Perspective

- The announcement of an 11th consecutive year of dividend increases may signal a consistent commitment to shareholder returns and robust financial health.

- This long-term trend of increasing dividends could be viewed by investors as an indication of stable business performance and a positive management outlook.

- The stated aim for continued revenue growth and further shareholder returns might suggest a proactive stance towards enhancing corporate value in the medium term.

- Disclaimer: This article is for informational purposes only and does not constitute investment advice.

5243|G-note

2128.0

▼ -1.02%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of the fiscal year ending November 2026, G-note reported Net Sales of 1,218 million yen (up 27.3% year-on-year), Adjusted EBITDA of 255 million yen (up 1,273.5% year-on-year), and Operating Income of 235 million yen (up 4,167.1% year-on-year).

- Despite strong Q1 progress rates against full-year forecasts (Net Sales 21.8%, Adjusted EBITDA 31.6%), the full-year earnings forecast remains unchanged. This is attributed to anticipated increases in personnel costs from hiring in Q2 and beyond, and the concentration of the GENIAC project’s 500 million yen full-year sales in Q2 onwards.

- The company is enhancing operational efficiency through AI utilization, leading to a decrease in headcount at the end of Q1 compared to the previous quarter. However, a net increase of 10-20 personnel is projected from Q2, primarily in new business areas.

- The note business’s Q1 GMV reached 6,203 million yen (up 25% year-on-year), with the company expressing confidence in maintaining a high GMV growth rate of approximately 20-30% going forward.

- Transitioning to the Prime Market is positioned as a key mid-to-long-term management objective. While certain requirements such as tradable share ratio are met, profit criteria are not yet achieved. The company aims for Net Sales of 10 billion yen and an EBITDA margin of 30-40% around 2028-2030 to support this transition.

🤖 AI Perspective

The first quarter results demonstrate significant growth, particularly in profitability, suggesting that the company’s AI-driven productivity initiatives are effectively containing costs while business expands. The decision to maintain the full-year forecast, despite strong initial profit performance, appears to be a prudent approach, considering planned future personnel investments and specific project revenue recognition timelines. The sustained high growth in note’s GMV, coupled with the clear mid-to-long-term goal of a Prime Market transition and specified financial targets, could indicate a strategic focus on both current operational efficiency and future market positioning.

5451|ヨドコウ

1333.0

▲ +0.30%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- YODOKO Co., Ltd. announced its consolidated financial results for the fiscal year ended March 2026. Sales reached ¥195,373 million (down 6.3% year-on-year), operating profit was ¥11,868 million (down 14.5%), and ordinary profit was ¥17,517 million (down 18.7%).

- Net profit attributable to owners of parent increased by 28.9% to ¥17,404 million for the period.

- The annual dividend for the fiscal year ended March 2026 is ¥91.00 per share, with the year-end dividend changed from the initially announced ¥69 to ¥71.

- For the fiscal year ending March 2027, the company forecasts consolidated sales of ¥196,000 million (up 0.3% year-on-year), operating profit of ¥10,300 million (down 13.2%), ordinary profit of ¥11,900 million (down 32.1%), and net profit attributable to owners of parent of ¥10,000 million (down 42.5%).

- The company implemented a 1-for-5 stock split of its common shares effective July 1, 2025. Per-share indicators and dividend figures are calculated and stated considering this stock split.

🤖 AI Perspective

For the fiscal year ended March 2026, while sales, operating profit, and ordinary profit decreased, the significant increase in net profit attributable to owners of parent stands out, and the factors contributing to this divergence may be a key point for investors. Looking ahead, the consolidated earnings forecast for the fiscal year ending March 2027 projects declines in key profit figures, suggesting that investors may want to monitor the company’s future business environment and strategies. The dividend trend, with ¥91 for the current period and a forecast of ¥53 for the next, could also attract interest, particularly in conjunction with the impact of the stock split.

3401|帝人

1639.5

▲ +4.63%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Teijin reported consolidated revenue of JPY 873,190 million for the fiscal year ended March 31, 2026, marking a 13.2% decrease from the previous fiscal year.

- The net loss attributable to owners of parent amounted to JPY 88,003 million, a significant shift from the JPY 28,347 million profit recorded in the prior year.

- Business profit decreased by 6.6% to JPY 25,781 million, and the company posted an operating loss of JPY 70,714 million.

- Impairment losses were recorded in the Aramid and Healthcare business segments during the fiscal year.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated revenue of JPY 850,000 million (a 2.7% decrease) and anticipates a return to net profit attributable to owners of parent of JPY 45,000 million.

- The annual dividend per share is projected to remain at JPY 50.00 for both FY2026/3 (actual) and FY2027/3 (forecast), comprising an interim dividend of JPY 25.00 and a year-end dividend of JPY 25.00.

🤖 AI Perspective

Teijin’s FY2026/3 results show a significant net loss primarily due to impairment charges, despite an increase in cash flow from operating activities. The company’s FY2027/3 forecast anticipates a return to profitability across business, operating, and net profit levels, which may suggest expected improvements from ongoing cost structure reforms and segment-specific strategies. The consistent dividend policy could indicate management’s confidence in future recovery.

4203|住友ベーク

5489.0

▼ -1.03%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sumitomo Bakelite Co., Ltd. announced its consolidated financial results (IFRS) for the fiscal year ended March 31, 2026, on May 11, 2026.

- For FY2026/3, consolidated revenue was ¥319,867 million (+5.0% year-on-year), business profit was ¥34,490 million (+11.8%), operating profit was ¥35,478 million (+43.1%), and profit attributable to owners of parent was ¥28,014 million (+45.3%).

- The annual dividend for FY2026/3 was ¥110.00 per share (¥50.00 interim, ¥60.00 year-end).

- The consolidated earnings forecast for FY2027/3 projects revenue of ¥337,000 million (+5.4% year-on-year), business profit of ¥38,000 million (+10.2%), operating profit of ¥37,500 million (+5.7%), and profit attributable to owners of parent of ¥28,500 million (+1.7%).

- The annual dividend forecast for FY2027/3 is ¥120.00 per share (¥60.00 interim, ¥60.00 year-end).

🤖 AI Perspective

The strong performance in FY2026/3, particularly the significant increases in profits, may be attributed to robust demand for semiconductor-related materials and successful efforts in shifting to high-value-added products and improving profit structures, as well as a rebound from impairment losses in the previous period. The positive outlook for FY2027/3, including projected increases in revenue, profits, and dividends, could indicate management’s confidence in continued favorable market conditions and strategic execution. These trends are worth monitoring for insights into the company’s sustained growth potential.

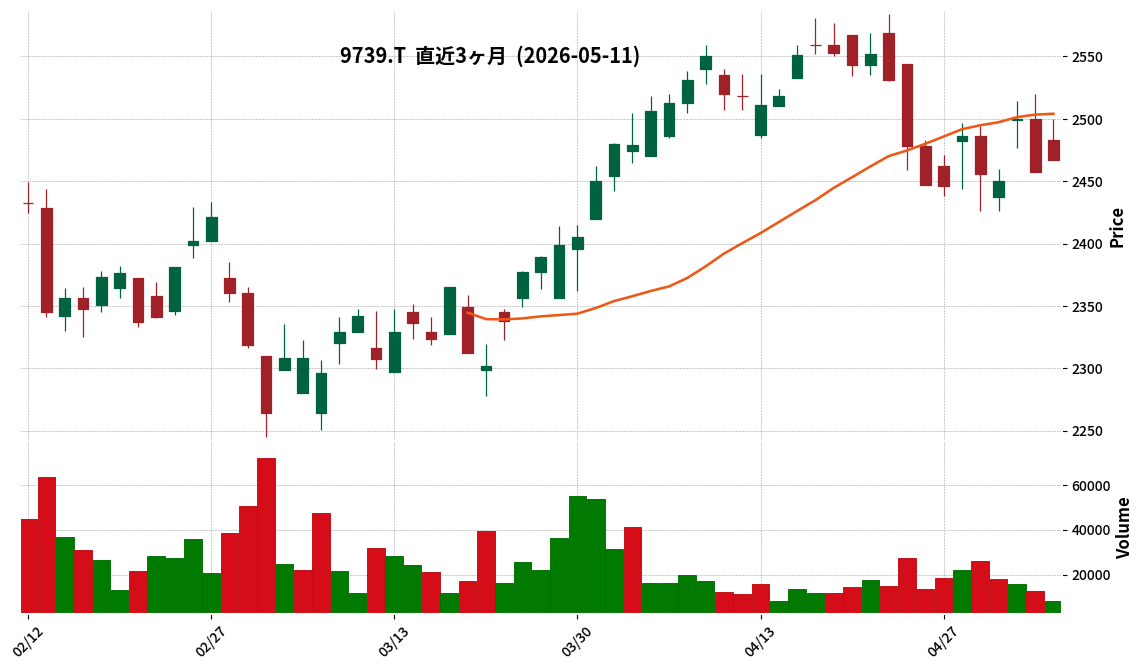

9739|NSW

2467.0

▲ +0.41%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- NSW announced on May 11, 2026, that its Board of Directors resolved to increase the year-end dividend for the fiscal year ended March 31, 2026.

- The year-end dividend per share is set at JPY 85.00, which is an increase of JPY 40.00 from the previous forecast of JPY 45.00.

- This decision results in a total annual dividend of JPY 125.00 per share for the fiscal year ended March 31, 2026, including the JPY 40.00 interim dividend.

- The company cited its established business foundation, including consolidated net sales exceeding JPY 50 billion for three consecutive years in FY2026/3, as a primary reason for the dividend change.

- NSW stated its policy to clarify its commitment to shareholder returns by setting a dividend payout ratio of 50% as a near-term guideline.

🤖 AI Perspective

This dividend increase suggests that NSW is strengthening its commitment to shareholder returns, supported by a solid performance foundation. The establishment of a 50% dividend payout ratio as a guideline could offer investors clearer expectations regarding future capital distribution policies. This move, combined with the stated policy of continuous stable dividends, might be viewed as a positive indicator of the company’s financial health and shareholder-centric approach.

4404|ミヨシ油脂

2172.0

▲ +1.83%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of the fiscal year ending December 2026 (January 1, 2026 – March 31, 2026), consolidated net sales reached ¥15,154 million, marking a 5.9% increase compared to the prior-year period.

- Consolidated operating profit was ¥543 million (up 54.1% year-over-year), and consolidated ordinary profit was ¥481 million (up 89.3% year-over-year).

- Net income attributable to owners of parent soared by 145.0% year-over-year to ¥279 million.

- By segment, the Food Business reported sales of ¥10,589 million (up 5.0% year-over-year) and operating profit of ¥486 million (up 264.0% year-over-year).

- The Oil & Fat Chemicals Business segment recorded sales of ¥4,457 million (up 6.6% year-over-year), but its operating profit decreased by 73.9% to ¥36 million.

- The consolidated earnings forecast for the full fiscal year ending December 2026 remains unchanged from the announcement made on February 13, 2026.

🤖 AI Perspective

The company’s first-quarter consolidated results demonstrate significant growth across sales and all profit metrics, with net income attributable to owners of parent showing a substantial increase of 145.0% year-over-year.

The strong performance of the Food Business segment, which saw significant growth in both sales and operating profit, appears to be a primary driver for the overall positive results. Conversely, the Oil & Fat Chemicals Business experienced a notable decline in profit despite increased sales, suggesting varying performance dynamics between segments.

The decision to maintain the full-year earnings forecast might indicate that the company had already incorporated the robust Q1 performance into its initial projections or is adopting a cautious outlook for the remainder of the fiscal year.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

9101|郵船

5703.0

▲ +2.37%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nippon Yusen Kabushiki Kaisha (NYK Line) announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- Consolidated operating results show net sales of ¥2,423,689 million (down 6.4% year-on-year), operating profit of ¥138,601 million (down 34.3% year-on-year), ordinary profit of ¥211,135 million (down 57.0% year-on-year), and profit attributable to owners of parent of ¥211,750 million (down 55.7% year-on-year).

- Basic earnings per share was ¥504.85.

- The annual dividend for the fiscal year ended March 31, 2026, was ¥230.00 per share (interim: ¥115.00, year-end: ¥115.00). The year-end dividend includes an ordinary dividend of ¥90.00 and a commemorative dividend of ¥25.00.

- For the fiscal year ending March 31, 2027 (April 1, 2026 – March 31, 2027), the company forecasts consolidated net sales of ¥2,605,000 million (up 7.5% year-on-year), operating profit of ¥145,000 million (up 4.6% year-on-year), ordinary profit of ¥185,000 million (down 12.4% year-on-year), and profit attributable to owners of parent of ¥195,000 million (down 7.9% year-on-year).

- The forecast for the annual dividend for the fiscal year ending March 31, 2027, is ¥200.00 per share (interim: ¥100.00, year-end: ¥100.00).

🤖 AI Perspective

The consolidated results for the fiscal year ended March 31, 2026, indicate a significant decline across all profit categories, with ordinary profit and profit attributable to owners of parent seeing reductions exceeding 50% from the previous fiscal year. This performance may be influenced by factors such as a substantial decrease in equity method investment income compared to the prior period. For the fiscal year ending March 31, 2027, while net sales and operating profit are projected to increase, ordinary profit and profit attributable to owners of parent are expected to continue their decline, suggesting that trends in equity method investment income will be a key area for monitoring.

2790|ナフコ

2192.0

▲ +0.87%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- NAFCO Co.,Ltd. reported its FY2026/3 financial results (April 1, 2025 – March 31, 2026), with operating revenue of JPY 175,272 million (96.4% year-on-year). Operating profit increased to JPY 1,636 million (129.2% year-on-year), ordinary profit to JPY 1,488 million (111.9% year-on-year), and net profit to JPY 223 million (121.6% year-on-year).

- The increase in operating profit was primarily attributed to “cost review and suppression” and “review of sales promotion resulting in gross profit retention.”

- On the balance sheet, total assets stood at JPY 215,957 million and net assets at JPY 152,842 million. The equity ratio improved by 2.4 percentage points from the previous fiscal year-end, reaching 70.8%.

- In the cash flow statement, cash flow from operating activities turned positive at JPY 3,064 million, compared to a negative JPY 709 million in the previous fiscal year.

- The Private Brand (PB) ratio was 45.5% (down 0.1 percentage points from the previous period).

🤖 AI Perspective

- The significant profit increase despite a revenue decline may suggest the effectiveness of NAFCO’s strategies in cost management and profit margin optimization amid challenging market conditions.

- The improvement in the equity ratio and positive operating cash flow could indicate a strengthening of the company’s financial stability.

- Investors might monitor how the company sustains these efficiency gains while navigating external factors such as inflation and seasonal demand in the upcoming periods.

5035|G-HOUSEI

422.0

▲ +2.43%

📎 Source:G-HOUSEI Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of the fiscal year ending December 2026 (January 1 to March 31, 2026), consolidated net sales were ¥1,214 million, representing a 6.5% decrease year-over-year.

- Despite the decrease in sales, operating profit increased by 50.3% to ¥46 million, ordinary profit by 95.0% to ¥50 million, and net profit attributable to parent company shareholders surged by 151.4% to ¥36 million.

- The Domestic IT segment reported sales of ¥1,120,598 thousand (down 6.1% YoY) and operating profit of ¥76,350 thousand (up 184.4% YoY). The Overseas IT segment had sales of ¥94,106 thousand (down 11.0% YoY) and an operating loss of ¥36,238 thousand.

- During the quarter, the company reported initiating technology research with Juntendo University utilizing its generative low-code development platform “imprai” and commencing sales of the WMS solution “LOGIFLUX WMS.”

- The consolidated full-year earnings forecast for the fiscal year ending December 2026 remains unchanged, projecting net sales of ¥5,200 million (up 8.8% YoY), operating profit of ¥240 million (up 556.6% YoY), and net profit attributable to parent company shareholders of ¥170 million.

🤖 AI Perspective

- Although sales decreased year-over-year, the significant increase in profit figures suggests improved gross profit margins and reduced selling, general, and administrative expenses.

- The improved profitability of the Domestic IT segment appears to have contributed to the overall results, while the Overseas IT segment continues to record losses, which may warrant further monitoring of the company’s business portfolio strategy.

- The company is advancing business investments aimed at medium-to-long-term growth, including AI-driven technology research in the medical field and the deployment of new WMS solutions.

3777|G-環境フレンドリー

59.0

▲ +0.00%

📎 Source:G-環境フレンドリー Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Kankyo Friendly Holdings Co., Ltd. resolved on May 11, 2026, for its consolidated subsidiary, EF Investment, to acquire shares of three special purpose companies (EFI Solar 1 Co., Ltd., EFI Solar 2 Co., Ltd., and EFI Solar 3 Co., Ltd.) in South Korea, making them consolidated subsidiaries.

- This acquisition is the first project under the strategic business alliance memorandum with Econetwork Co., Ltd., previously disclosed on March 17, 2026.

- It represents EF Investment’s first direct investment in the South Korean solar power business and is positioned as the initial step in its strategy to expand into the Asian market.

- The three acquired SPCs will operate solar power plants with a total planned capacity of approximately 2.6MW, located in Wonju City, Gangwon Province, and Chungju City, Chungcheongbuk Province, South Korea.

- These power plants are currently in the pre-construction phase, with completion scheduled for July 2026. The total acquisition cost for the shares is 201,000,000 KRW.

🤖 AI Perspective

This development marks G-Kankyo Friendly Group’s concrete entry into the South Korean renewable energy market. The strategy of leveraging EF Investment’s expertise cultivated in Japan for the development and operation of solar power plants in South Korea may suggest potential synergies for future business expansion. Positioning this as the first step in its Asian market expansion strategy indicates that the company’s future international business growth could be worth monitoring.

7443|横浜魚類

631.0

▲ +0.32%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Yokohama Gyorui Co., Ltd. (Code: 7443) announced its non-consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- For the period, net sales increased by 3.8% year-on-year to ¥20,978 million, operating income surged by 34.7% to ¥211 million, ordinary income rose by 30.2% to ¥236 million, and net income increased by 2.5% to ¥185 million.

- Earnings per share (EPS) for the period was ¥29.67, and net assets per share was ¥430.63.

- The year-end dividend for FY2026 was raised to ¥8.00 from ¥6.00 in the previous fiscal year, resulting in a total annual dividend of ¥8.00 (total dividend payment of ¥50 million).

- For the fiscal year ending March 31, 2027, the company forecasts net sales of ¥21,200 million (up 1.1% year-on-year), but expects a decline in profits with operating income at ¥180 million (down 14.9%), ordinary income at ¥200 million (down 15.6%), and net income at ¥150 million (down 19.2%).

🤖 AI Perspective

Yokohama Gyorui demonstrated strong performance in FY2026 with increases across all key profit metrics, notably a 34.7% surge in operating income, potentially supported by reduced bad debt write-off expenses. However, the company’s forecast for FY2027 projects a decline in operating and net income despite a modest increase in sales, which may suggest that rising costs could impact future profitability. The increase in the annual dividend could be interpreted as a positive signal regarding the company’s commitment to shareholder returns.

1807|佐藤渡辺

2050.0

▲ +4.06%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sato Watana Co., Ltd. reported consolidated financial results for the fiscal year ended March 2026, with net sales of ¥33,704 million (down 16.6% year-on-year), operating profit of ¥1,070 million (down 9.1%), ordinary profit of ¥1,369 million (up 3.1%), and profit attributable to owners of parent of ¥883 million (down 0.9%).

- The decline in net sales for the current fiscal year was primarily due to a 120-day business suspension order from the Kanto Regional Development Bureau of the Ministry of Land, Infrastructure, Transport and Tourism (effective from April 9 to August 6, 2025), which impacted order intake and sales in the construction division.

- Regarding the financial position, total assets at the end of March 2026 were ¥32,672 million, and net assets were ¥22,920 million, with the equity ratio improving to 69.8% from 60.2% at the end of the previous fiscal year.

- Cash flow from operating activities significantly improved to ¥5,095 million (compared to △¥3,964 million in the previous year), with cash and cash equivalents at the end of the period totaling ¥6,394 million.

- The consolidated earnings forecast for the fiscal year ending March 2027 projects net sales of ¥38,000 million (up 12.7% year-on-year), operating profit of ¥1,100 million (up 2.8%), ordinary profit of ¥1,300 million (down 5.1%), and profit attributable to owners of parent of ¥900 million (up 1.9%). An annual dividend of ¥80.00 per share is also forecast.

🤖 AI Perspective

In FY2026, while net sales significantly decreased year-on-year due to the business suspension, it is notable that ordinary profit saw a slight increase, and the decline in net profit was limited compared to the sales decrease. The substantial improvement in operating cash flow and the higher equity ratio suggest a potential strengthening of the company’s financial foundation. The FY2027 forecast, projecting increases in both sales and profit, indicates an anticipated recovery in business activities, possibly reflecting a rebound from the previous period’s challenges.

3447|信和

959.0

▼ -1.34%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Shinwa reported consolidated revenue of ¥20,138 million (+15.1% YoY), operating profit of ¥2,488 million (+53.4% YoY), and profit attributable to owners of parent of ¥1,718 million (+76.2% YoY) for the fiscal year ended March 31, 2026.

- Both revenue and all stages of profit reached record highs since listing.

- The annual dividend for FY2026/3 was ¥34.00 (year-end dividend of ¥18.00), an increase of ¥2.00 from the previous fiscal year’s ¥32.00.

- For FY2027/3, Shinwa forecasts consolidated revenue of ¥22,000 million (+9.2% YoY) but anticipates profit attributable to owners of parent to be ¥1,600 million (-6.9% YoY).

- During the current consolidated fiscal year, Kaizu Construction Co., Ltd. was newly added to the scope of consolidation.

🤖 AI Perspective

The achievement of record-high revenue and profits, along with an increased annual dividend for the fiscal year ended March 2026, could be viewed favorably by investors. However, the forecast for a decrease in profit attributable to owners of parent for the fiscal year ending March 2027 may raise questions regarding future profitability and business strategies. The addition of a new consolidated subsidiary suggests business expansion, and its integration effects on future performance will be worth monitoring.

4624|イサム塗料

3725.0

▼ -0.67%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, consolidated net sales were ¥8,403 million, an increase of 3.0% year-on-year.

- Consolidated operating profit increased by 45.9% to ¥915 million, ordinary profit by 40.5% to ¥1,077 million, and profit attributable to owners of parent by 37.6% to ¥755 million.

- Diluted earnings per share for the period was ¥396.34, up from ¥288.00 in the previous fiscal year.

- The consolidated equity ratio remained high at 82.5%.

- The annual dividend for the fiscal year ended March 31, 2026, was ¥50.00 (interim ¥25.00, year-end ¥25.00), maintaining the same level as the previous year.

- The consolidated earnings forecast for the fiscal year ending March 31, 2027, has been announced as undecided due to the difficulty in making a reasonable estimate amid the impact of the Middle East situation.

🤖 AI Perspective

The FY2026 results show a notable increase in sales, driven by price revisions and speculative demand for certain products, leading to significant growth across all profit metrics compared to the previous year. The company also maintains a strong financial position, as indicated by a high consolidated equity ratio of 82.5%. However, the decision to leave the FY2027 earnings forecast undecided, citing the Middle East situation, suggests potential uncertainties regarding future business conditions that warrant monitoring.

5660|神鋼鋼線

1650.0

▲ +7.77%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Shinko Wire Co., Ltd. reported consolidated results for the fiscal year ended March 31, 2026, with net sales of ¥33,074 million (down 3.6% year-on-year), operating profit of ¥653 million (down 44.0% year-on-year), and ordinary profit of ¥660 million (down 46.6% year-on-year).

- Profit attributable to owners of parent increased by 8.3% year-on-year to ¥1,120 million, primarily due to special gains from the sale of policy-held shares and insurance proceeds related to hailstorm damage at a rope manufacturing plant.

- The annual dividend for the fiscal year ended March 31, 2026, was ¥65.00 per share (interim ¥25.00, year-end ¥40.00), representing an increase of ¥5.00 from the previous year’s ¥60.00.

- Consolidated earnings forecasts and dividend forecasts for the fiscal year ending March 31, 2027, have been withheld due to the planned delisting on August 28, 2026, following a share exchange with Kobe Steel, Ltd.

- In terms of consolidated financial position, total assets stood at ¥44,582 million, net assets at ¥25,386 million, and the equity ratio improved to 56.9% from 54.5% at the end of the previous fiscal year.

🤖 AI Perspective

The reported decrease in net sales, operating, and ordinary profits, offset by an increase in net profit attributable to owners of parent due to special gains, highlights a mixed financial performance for the period. The decision to withhold forecasts for the next fiscal year and dividends, stemming from the impending delisting due to a share exchange with Kobe Steel, suggests a significant transition period for the company. Investors may consider monitoring the implications of this corporate restructuring.

6364|AIRMAN

2257.0

▲ +6.71%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- AIRMAN Co., Ltd. reported consolidated results for the fiscal year ended March 31, 2026, with net sales of ¥55,604 million (up 2.3% year-on-year), operating profit of ¥7,184 million (up 11.2%), ordinary profit of ¥8,014 million (up 17.4%), and profit attributable to owners of parent of ¥5,596 million (up 17.4%).

- The annual dividend for the fiscal year ended March 31, 2026, was ¥72.00, including a year-end dividend of ¥52.00, an increase from ¥57.00 in the previous fiscal year.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥58,500 million (up 5.2% year-on-year), but expects operating profit of ¥5,630 million (down 21.6%), ordinary profit of ¥5,760 million (down 28.1%), and profit attributable to owners of parent of ¥3,960 million (down 29.2%).

- The annual dividend forecast for the fiscal year ending March 31, 2027, is ¥72.00 (including a year-end dividend of ¥52.00), which is the same amount as the previous fiscal year.

- The consolidated equity ratio as of March 31, 2026, stood at 68.5%.

🤖 AI Perspective

While AIRMAN achieved increased revenue and profit in the fiscal year ended March 2026 and raised its annual dividend, the company’s forecast for the fiscal year ending March 2027 projects a decrease in profit, which may draw investor attention. The shift to negative operating cash flow in the current period could also be a factor to consider when evaluating future financial health. The robust equity ratio suggests a stable financial foundation.

6928|エノモト

3505.0

▼ -3.18%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Enomoto Co., Ltd. reported consolidated results for the fiscal year ended March 31, 2026, with net sales of ¥30,415 million (up 13.2% year-on-year), operating profit of ¥1,650 million (up 166.8% year-on-year), ordinary profit of ¥1,766 million (up 164.0% year-on-year), and net profit attributable to owners of parent of ¥1,231 million (up 174.9% year-on-year).

- Diluted earnings per share (EPS) for the period were ¥191.21, compared to ¥68.51 in the previous fiscal year.

- The annual dividend for the fiscal year ended March 31, 2026, was ¥75.00 per share (interim ¥35.00, year-end ¥40.00), an increase from ¥71.00 in the prior fiscal year.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥32,000 million (up 5.2% year-on-year), operating profit of ¥2,000 million (up 21.2% year-on-year), and net profit attributable to owners of parent of ¥1,400 million (up 13.7% year-on-year).

- The forecast for the annual dividend for the fiscal year ending March 31, 2027, is ¥77.00 per share (interim ¥37.00, year-end ¥40.00).

🤖 AI Perspective

The significant year-on-year increases in revenue and all profit metrics for FY2026, particularly the over 160% growth in operating, ordinary, and net profits, suggest a strong turnaround in business performance. This strong performance may be attributed to strategic initiatives such as the expansion of LED lead frame production and the pursuit of high-value micro-connector components, as outlined in the company’s overview. Furthermore, the positive outlook for FY2027, including projected growth in revenue, profits, and an increased dividend, could indicate management’s confidence in sustained future performance.

7636|ハンズマン

799.0

▼ -0.25%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Handsman Co., Ltd. announced its financial results for the third quarter of the fiscal year ending June 2026 (July 1, 2025, to March 31, 2026).

- During this period, net sales were 25,516 million yen (down 0.0% year-on-year), while operating profit was 727 million yen (down 10.2% year-on-year), ordinary profit was 943 million yen (down 4.8% year-on-year), and net income attributable to owners of the parent was 637 million yen (down 4.6% year-on-year).

- The gross profit margin decreased by 0.5 percentage points year-on-year to 31.1%, with the company stating that rising purchase prices due to higher raw material costs and yen depreciation were key factors.

- Total store customer traffic was reported as 100.2% of the prior year, and the average customer spend was 99.8% of the prior year.

- The full-year forecast for the fiscal year ending June 2026 remains unchanged from the most recently announced figures, projecting net sales of 35,050 million yen, operating profit of 1,080 million yen, ordinary profit of 1,350 million yen, and net income of 910 million yen.

🤖 AI Perspective

Handsman’s Q3 results indicate largely flat sales year-on-year, but a decline in profits, primarily attributed to a lower gross profit margin influenced by rising raw material costs and yen depreciation. Efforts to manage selling, general, and administrative expenses, which saw a decrease, may have partially offset these pressures. Investors might observe how the company continues to address cost challenges and adapt its product mix, given the contrasting performance among its DIY, household, and car/leisure product categories.

9273|コーア商事HD

871.0

▼ -1.36%

📎 Source:コーア商事HD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the third quarter of the fiscal year ending June 2026 (July 1, 2025 – March 31, 2026), consolidated net sales reached JPY 18,334 million (up 4.0% year-on-year), operating income was JPY 4,580 million (up 4.5%), ordinary income was JPY 4,551 million (up 3.0%), and net income attributable to owners of the parent was JPY 3,052 million (up 3.1%).

- Diluted earnings per share for the quarter were JPY 72.47.

- The consolidated financial position showed total assets of JPY 38,039 million, net assets of JPY 30,494 million, and an equity ratio of 80.2%.

- The forecast for the annual dividend for the fiscal year ending June 2026 remains JPY 18.00 per share (JPY 18.00 at year-end), with no revisions from the latest forecast.

- The consolidated full-year earnings forecast for the fiscal year ending June 2026 includes net sales of JPY 25,700 million (up 10.4% year-on-year) and net income attributable to owners of the parent of JPY 3,640 million (up 0.1%), with no revisions from the latest forecast.

🤖 AI Perspective

KOA Shoji HD demonstrated a steady performance, achieving increased revenue and profit for the cumulative third quarter. This growth appears to be supported by robust sales in its raw material sales business, particularly for “allergy medications” and “central nervous system medications.” The high equity ratio could indicate the company’s strong financial stability, which may be a key point for investors to monitor.

3577|東海染工

966.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tokai Senko Co., Ltd. has released its consolidated financial results for the fiscal year ending March 2026.

🤖 AI Perspective

This announcement is expected to disclose key financial figures reflecting the company’s profitability and financial health. Investors will likely analyze metrics such as net sales, various levels of profit, dividend forecasts, and future outlook to assess the company’s operational strength and growth prospects.

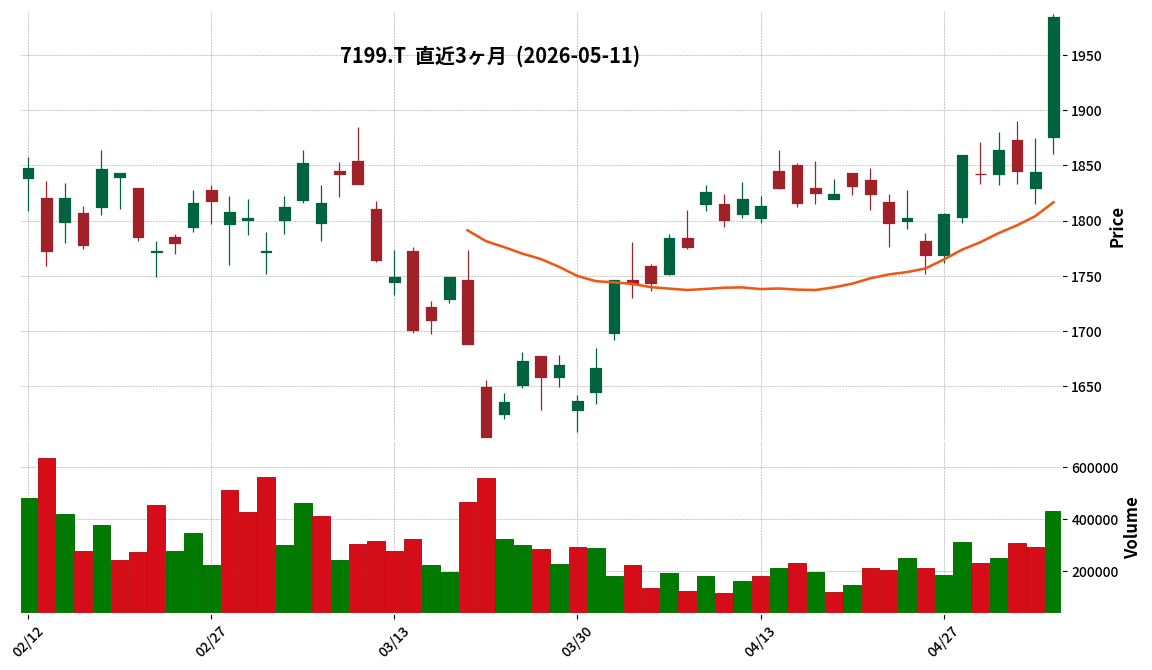

7199|プレミアグループ

1984.0

▲ +7.59%

📎 Source:プレミアグループ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Premier Group’s consolidated operating revenue for the fiscal year ended March 31, 2026, increased by 21.0% year-on-year to ¥44,042 million.

- Profit attributable to owners of the parent grew by 30.5% year-on-year, reaching ¥6,069 million.

- Basic earnings per share stood at ¥157.22.

- The annual dividend per share was set at ¥54.00, an increase from ¥40.00 in the previous fiscal year.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated operating revenue of ¥51,000 million (up 15.8% year-on-year) and profit attributable to owners of the parent of ¥6,900 million (up 13.7% year-on-year).

🤖 AI Perspective

The strong performance in the current fiscal year appears to be supported by increased transaction volumes in the finance business and growth in high-profit products within the warranty business. The positive outlook for the next fiscal year, projecting continued revenue and profit growth, could indicate ongoing expansion of the business foundation and improvements in the revenue structure. Investors may wish to monitor how the company’s future business strategies and evolving market conditions impact its financial results.

2903|シノブフーズ

1547.0

▲ +5.31%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Shinobu Foods reported consolidated net sales of ¥61,974 million for the fiscal year ended March 31, 2026, marking a 7.5% increase year-on-year.

- Net income attributable to owners of parent significantly rose by 70.4% year-on-year, reaching ¥1,698 million.

- The annual dividend for FY2026 was increased to ¥32.00 per share, up from ¥27.00 in the previous fiscal year.

- For FY2027, the company forecasts consolidated net sales of ¥63,800 million (+2.9% YoY) and net income attributable to owners of parent of ¥1,700 million (+0.1% YoY).

- The equity ratio improved to 52.9% at the end of FY2026, compared to 50.5% at the end of FY2025.

🤖 AI Perspective

Shinobu Foods’ significant 70.4% increase in net income attributable to owners of parent for FY2026, alongside a 7.5% rise in net sales, suggests robust operational performance. The increase in annual dividend and the projected stable growth for FY2027 could indicate a positive outlook for shareholder returns and business stability. The improvement in the equity ratio to 52.9% may also reflect a strengthened financial position.

4186|東応化

10270.0

▲ +6.01%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tokyo Ohka Kogyo Co., Ltd. (TOK) announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026 – March 31, 2026).

- Consolidated net sales reached ¥67,077 million (up 23.6% year-on-year), operating profit was ¥15,074 million (up 53.8%), ordinary profit ¥15,374 million (up 56.2%), and profit attributable to owners of parent was ¥11,725 million (up 55.8%).

- Segment sales showed Electronics Functional Materials at ¥35,795 million (up 29.0% year-on-year) and High Purity Chemicals at ¥29,986 million (up 17.2% year-on-year).

- The equity ratio as of the end of the first consolidated accounting period was 68.9%, an increase of 1.0 percentage point from the end of the previous fiscal year.

- The consolidated earnings forecast for the fiscal year ending December 2026, including the annual dividend forecast of ¥80.00, remains unchanged from the figures announced on February 9, 2026.

🤖 AI Perspective

The strong performance in the first quarter appears to be primarily driven by robust demand for generative AI-related products and a favorable yen depreciation trend. The significant increase in sales for the Electronics Functional Materials segment, in particular, may suggest a recovery in the semiconductor market. Despite the substantial profit growth, keeping the full-year earnings forecast unchanged could indicate a cautious stance in monitoring future market conditions and business developments.

4189|KHネオケム

2751.0

▲ +0.29%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- KH Neochem Co., Ltd. announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026 – March 31, 2026).

- For the cumulative first quarter, net sales were ¥25,581 million (down 11.2% year-on-year), operating income was ¥2,094 million (down 22.6% year-on-year), and profit attributable to owners of parent was ¥1,348 million (down 23.8% year-on-year), indicating a decrease in both revenue and profit.

- By business segment, Electronic Materials recorded sales of ¥3,365 million (up 22.5% year-on-year) and operating income of ¥754 million (up 33.0% year-on-year), showing growth in both revenue and profit.

- Conversely, Functional Materials saw sales of ¥12,109 million (down 17.6% year-on-year) and operating income of ¥2,156 million (down 16.1% year-on-year), while Basic Chemicals recorded sales of ¥9,942 million (down 11.0% year-on-year) and operating income of ¥191 million (down 58.2% year-on-year).

- The consolidated full-year earnings forecast for the fiscal year ending December 2026 and the annual dividend forecast (¥110.00 per share) remained unchanged from the most recently announced figures.

🤖 AI Perspective

The first quarter results show a mixed performance across business segments, with an overall decline in revenue and profit. The Electronic Materials segment’s strong growth, driven by AI-related investments, stands out as a key highlight and its continued performance will be worth monitoring. Conversely, the challenges faced by Functional Materials and Basic Chemicals, including inventory adjustments and increased manufacturing costs, may warrant closer attention from investors for their potential impact on future earnings. The unchanged full-year forecast could suggest management anticipates a recovery in the latter half of the fiscal year.

5867|G-エスネット

1254.0

▲ +1.95%

📎 Source:G-エスネット Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of the fiscal year ending December 2026 (January 1, 2026 to March 31, 2026), G-Esnet reported consolidated net sales of ¥978 million (up 19.5% year-on-year), operating income of ¥160 million (up 22.9%), ordinary income of ¥159 million (up 20.8%), and net income attributable to owners of parent of ¥100 million (up 25.7%).

- Diluted earnings per share for the quarter were ¥32.09.

- As of the end of the first quarter, consolidated total assets stood at ¥2,547 million, net assets at ¥1,779 million, and the equity ratio was 66.6%.

- The consolidated full-year forecast for the fiscal year ending December 2026 remains unchanged, projecting net sales of ¥3,936 million, operating income of ¥400 million, ordinary income of ¥376 million, and net income attributable to owners of parent of ¥245 million.

- The full-year forecast for basic earnings per share, ¥77.90, incorporates the impact of the disposal of treasury shares and issuance of new shares as restricted stock, resolved by the Board of Directors on May 11, 2026.

🤖 AI Perspective

G-Esnet’s first-quarter performance for the fiscal year ending December 2026, showing double-digit growth across net sales and all profit categories, may suggest a strong start to the fiscal year. The maintained full-year forecast could indicate the company’s confidence in its current performance trajectory towards achieving its annual goals. Furthermore, an equity ratio of 66.6% points to a solid financial foundation, which investors might consider a positive aspect of the company’s balance sheet.

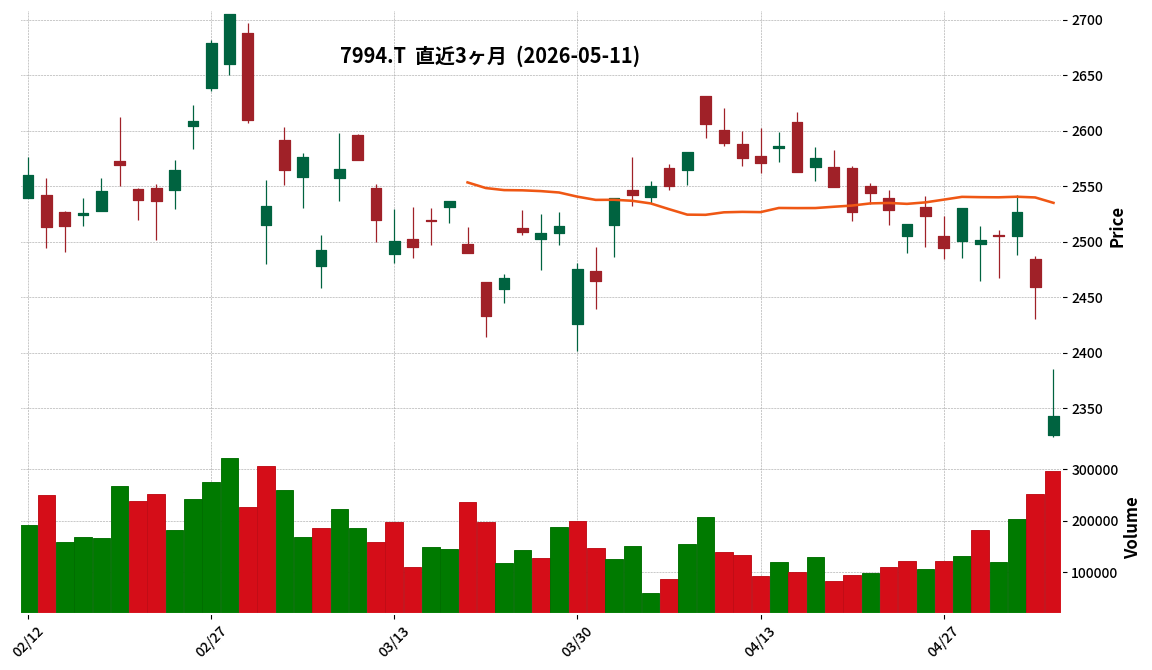

7994|オカムラ

2343.0

▼ -4.72%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Okamura Corporation announced a partial correction to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 (Japanese GAAP)” on May 11, 2026, which was originally published on May 8, 2026.

- The correction addresses an error in the numerical reference for the second quarter (cumulative) within “Summary Information 3. Consolidated Earnings Forecast for the Fiscal Year Ending March 31, 2027.”

- The revised consolidated earnings forecast for the second quarter (cumulative) of FY2027 now projects profit attributable to owners of parent at ¥7,000 million (previously ¥9,800 million) and basic earnings per share at ¥73.94 (previously ¥103.51).

- The year-on-year percentage changes for net sales, operating profit, and ordinary profit for the second quarter (cumulative) were also corrected.

- The consolidated full-year earnings forecast for the fiscal year ending March 31, 2027, remains unchanged by this correction.

🤖 AI Perspective

This revision primarily concerns the downward adjustment of the net income forecast for the cumulative second quarter of FY2027, while the consolidated full-year earnings forecast remains unchanged. This could suggest an effort to improve the accuracy of interim reporting without altering the company’s overall annual outlook. Investors may monitor the company’s performance against the unchanged full-year targets.

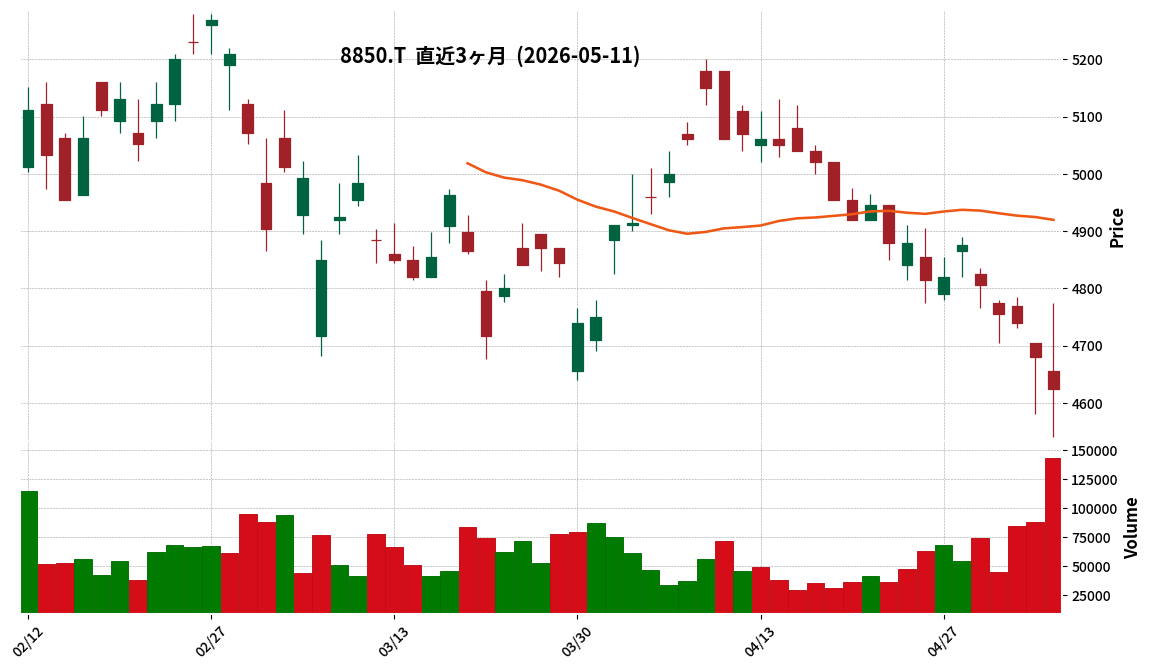

8850|スターツ

4625.0

▼ -1.18%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, Starts Corporation reported consolidated net sales of ¥251.911 billion (up 8.1% year-on-year), operating profit of ¥36.272 billion (up 11.2%), ordinary profit of ¥38.244 billion (up 14.5%), and net profit attributable to parent company shareholders of ¥25.311 billion (up 4.3%).

- The annual dividend for FY2026 was ¥140 per share, an increase of ¥20 from the previous year’s ¥120.

- The company’s stable revenue base strengthened with increased property management numbers, including 158,562 apartment/condominium units, 103,894 monthly parking spaces, and 60,112 “Navi Park” hourly parking spaces.

- The “Pitat House” real estate brokerage network expanded to 632 stores nationwide (116 group stores, 516 network stores), and 131 facilities for elderly support and childcare are in operation.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥290.0 billion (up 15.1% year-on-year), operating profit of ¥40.0 billion (up 10.3%), ordinary profit of ¥39.0 billion (up 2.0%), and net profit attributable to parent company shareholders of ¥26.0 billion (up 2.7%), with an anticipated annual dividend of ¥150 per share.

🤖 AI Perspective

Starts Corporation achieved strong financial performance in FY2026, reporting increases across net sales and all profit metrics, signaling robust business momentum. The growth in managed property units and the expansion of the “Pitat House” network appear to be key factors contributing to the strengthening of its stable revenue foundation. The announced increase in the annual dividend may suggest a commitment to shareholder returns. Furthermore, the positive consolidated earnings forecast for FY2027, projecting continued growth, could indicate management’s confidence in sustained business expansion.

9304|渋沢倉

1271.0

▼ -0.39%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Shibusawa Warehouse Co., Ltd. resolved at its Board of Directors meeting on May 11, 2026, to distribute a surplus dividend for the fiscal year ended March 31, 2026.

- This dividend was set at JPY 32 per share, an increase of JPY 2 from the most recent forecast. The effective date is June 5, 2026.

- The company forecasts a dividend of JPY 70 per share for the next fiscal year (ending March 31, 2027).

- Shibusawa Warehouse adheres to a shareholder return policy of a dividend payout ratio of 50% or more, coupled with progressive dividends.

- It is noted that the company implemented a 4-for-1 stock split for its common shares, effective October 1, 2025.

🤖 AI Perspective

The decision to increase the dividend for the fiscal year 2026, coupled with a higher forecast for FY2027, may suggest a continued commitment to shareholder returns. The progressive dividend policy, targeting a payout ratio of 50% or more, could be viewed by investors as a factor supporting long-term dividend stability. The consistent dividend increases, even after a stock split, indicate the company’s focus on returning profits to shareholders.

1813|不動テトラ

3050.0

▼ -0.97%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Fudo Tetra Co., Ltd. reported consolidated net sales of ¥81,700 million (up 17.5% year-on-year), operating profit of ¥5,919 million (up 86.3%), and ordinary profit of ¥6,124 million (up 81.9%) for the fiscal year ended March 31, 2026.

- Net income attributable to owners of parent increased by 102.6% to ¥4,461 million, resulting in earnings per share of ¥294.62.

- The year-end dividend for the fiscal year ended March 31, 2026, was ¥115.00 per share (an increase of ¥55.00 from the previous year), bringing the annual dividend to ¥115.00 per share.

- In the Civil Engineering segment, net sales rose by 18.9% to ¥33,739 million, while segment profit declined by 49.9% to ¥280 million.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥81,000 million (down 0.9%), operating profit of ¥4,800 million (down 18.9%), and net income attributable to owners of parent of ¥3,200 million (down 28.3%).

🤖 AI Perspective

The fiscal year ended March 31, 2026, saw substantial profit growth across all income categories, alongside increased net sales. However, the Civil Engineering segment experienced a decrease in profit despite higher sales, which may indicate varying profitability trends across business segments. The forecast for the fiscal year ending March 2027 projects a decline in revenue and profit, yet the company plans to maintain an annual dividend of ¥115, including a commemorative dividend, which could be interpreted as a commitment to shareholder returns.

1783|fantasista

66.0

▲ +3.12%

📎 Source:fantasista Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Fantasista Inc. announced that the payment and share transfer procedures for the acquisition of Amoty Co., Ltd. shares were completed on May 11, 2026.

- A total of 8,000 shares were acquired, consisting of 3,332 shares through transfer and 4,668 shares through a third-party allotment.

- The total acquisition price was 120 million yen, with a price of 15,000 yen per share.

- Following the acquisition, Fantasista Inc. holds 8,000 shares, representing a 54.98% voting interest, making Amoty Co., Ltd. a consolidated subsidiary.

- Amoty Co., Ltd. is scheduled to be included in Fantasista Inc.’s consolidated results starting from the September 2026 fiscal year.

🤖 AI Perspective

- Fantasista Inc.’s full acquisition of Amoty Co., Ltd. may suggest an acceleration of business expansion and leveraging of group management resources for the entire group.

- This completion marks the finalization of a process initiated by the basic agreement for a capital and business alliance signed on February 25, 2026, indicating a strategic move for mid-to-long-term growth.

- Fantasista Inc. is currently evaluating the impact on its consolidated performance for the current fiscal year, and further disclosures regarding this impact may be worth monitoring.

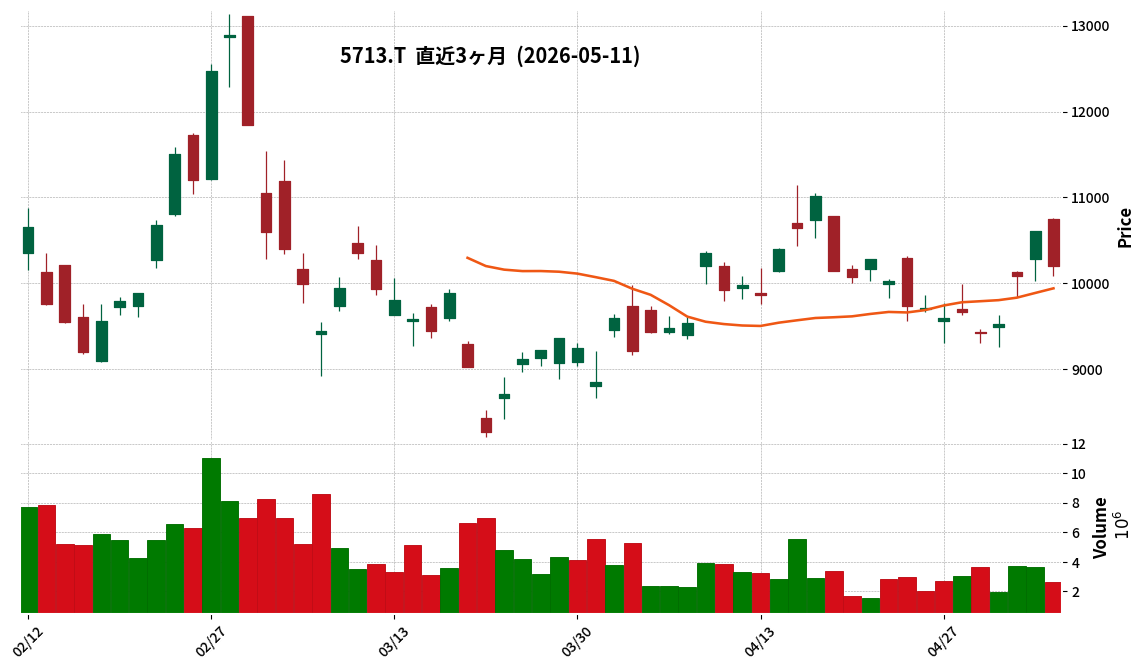

5713|住友鉱

10205.0

▼ -3.86%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sumitomo Metal Mining Co., Ltd. announced on May 11, 2026, a revision to its dividend forecast for the fiscal year ending March 2026 (101st fiscal period).

- The annual dividend per share has been revised upward from the previously announced forecast (February 9, 2026) of JPY 183.00 to JPY 228.00.

- The year-end dividend forecast is now JPY 163.00 per share, an increase of JPY 45.00 from the previous forecast of JPY 118.00 per share.

- This revision is based on the changes to the basic policy for financial strategy and shareholder return policy, which were announced on February 9, 2026.

- The revised shareholder return policy stipulates a consolidated payout ratio of 35% or more in principle, with a lower limit of DOE 3.5% when the consolidated equity ratio exceeds the appropriate level of 55%.

🤖 AI Perspective

This dividend increase appears to be a direct result of Sumitomo Metal Mining’s updated shareholder return policy, revised on February 9, 2026. The policy, which includes a minimum consolidated payout ratio of 35% or a DOE of 3.5% under certain conditions, may suggest a commitment to enhanced and stable shareholder distributions. This adjustment could indicate that the company’s financial performance and capital structure meet the criteria outlined in its new distribution guidelines.

1447|G-SAAFHD

298.0

▼ -0.67%

📎 Source:G-SAAFHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 2026, G-SAAF HD reported consolidated net sales of ¥29,580 million (up 102.5% year-on-year), operating profit of ¥1,093 million (up 327.5% year-on-year), and net profit attributable to parent company shareholders of ¥460 million, achieving a turnaround from a loss in the previous fiscal year.

- Operating profit, ordinary profit, and net profit attributable to parent company shareholders reached record highs since the company’s establishment in 2018.

- All core segments, including the Consulting business, achieved revenue growth, with the Consulting business recording sales of ¥2,276 million (up 114.1% year-on-year).

- The company implemented profit structure reforms, including the downsizing and liquidation of unprofitable businesses and a reduction in head office expenses, which contributed ¥566 million to the improvement of operating profit.

- In the fourth quarter of FY2026/3, the company executed growth investments, including the acquisition of shares (approximately ¥1.57 billion) associated with a capital and business alliance with Schoo Co., Ltd.

🤖 AI Perspective

The significant turnaround from a loss in the previous fiscal year to record-high profits in key indicators for FY2026/3 appears to be a notable point for investors. Revenue growth across all segments, particularly the strong performance of the Consulting business, alongside the effects of profit structure reforms, likely contributed to this improvement. The strategic investment in a capital and business alliance with Schoo Co., Ltd. could also signal future business expansion directions.

1826|佐田建

1047.0

▲ +0.77%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sata Kensetsu Co., Ltd. announced its consolidated financial results for the fiscal year ended March 31, 2026, on May 11, 2026.

- For the period, net sales were ¥36,769 million (up 14.0% year-on-year), operating profit was ¥1,772 million (up 84.4% year-on-year), and net profit attributable to owners of parent was ¥964 million (up 57.7% year-on-year).

- Basic earnings per share for FY2026 were ¥71.57.

- The company announced an annual dividend of ¥60.00 per share for FY2026, consistent with the previous fiscal year, and forecasts the same for FY2027.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥37,600 million (up 2.3% year-on-year), but expects operating profit of ¥1,500 million (down 15.3% year-on-year) and net profit attributable to owners of parent of ¥910 million (down 5.6% year-on-year).

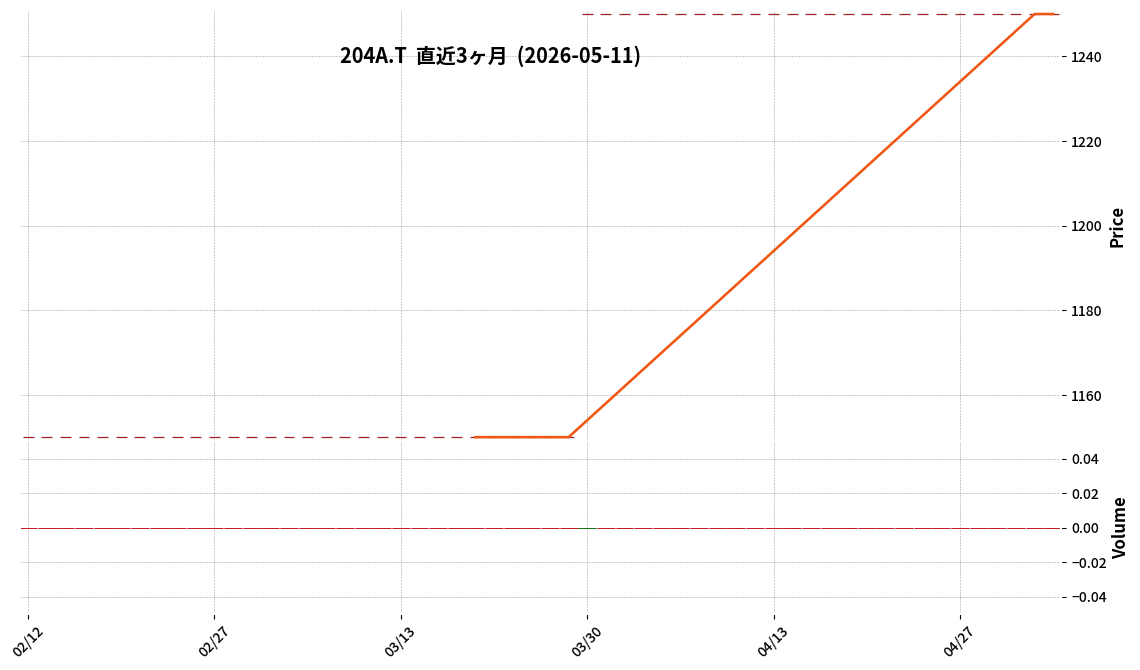

204A|P-タイヨーパッケー

1250.0

▲ +0.00%

📎 Source:P-タイヨーパッケー Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Taiyo Package Co., Ltd. (Code: 204A) announced its non-consolidated interim financial results for the fiscal year ending September 2026 (October 1, 2025 – March 31, 2026).

- For the interim period, net sales were ¥2,149 million (down 0.1% year-on-year), operating profit ¥158 million (down 15.7%), ordinary profit ¥169 million (down 14.9%), and interim net profit ¥123 million (down 9.6%).

- As of the end of the interim period, total assets stood at ¥4,547 million, net assets at ¥1,463 million, and the equity ratio at 32.2%.

- The full-year performance forecast for FY2026 remains unchanged, projecting net sales of ¥4,440 million (up 2.5% year-on-year), operating profit of ¥225 million (down 29.9%), and net profit of ¥167 million (down 35.0%).

- The projected annual dividend for FY2026 is ¥200.00 per share (interim ¥100.00, year-end ¥100.00), with no revisions from the latest forecast.

🤖 AI Perspective

The interim period shows net sales largely flat year-on-year, yet all profit categories experienced double-digit declines, which may indicate ongoing challenges in profitability. With the full-year forecast remaining unchanged, examining the interim performance in relation to the full-year targets could offer insights into future business operations and management strategies. The impact of changes in cost structure and the competitive landscape on performance will be worth monitoring.

2763|エフティグループ

1120.0

▼ -1.06%

📎 Source:エフティグループ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 2026, consolidated revenue was JPY 31,579 million (down 8.8% year-on-year), and net profit attributable to owners of parent was JPY 6,461 million (down 2.3% year-on-year).

- The annual dividend for FY2026 was JPY 55.00 (interim JPY 20.00, year-end JPY 35.00), with a consolidated payout ratio of 25.3%.

- The consolidated earnings forecast for FY2027 projects revenue of JPY 29,400 million (down 6.9% year-on-year) and net profit attributable to owners of parent of JPY 3,800 million (down 41.2% year-on-year).

- FT Group shares are scheduled to be delisted on July 30, 2026, due to a share exchange with Hikari Tsushin Inc., and consequently, the dividend forecast for FY2027 has not been disclosed.

- As of March 2026, the consolidated financial position showed an increase in equity attributable to owners of parent to JPY 35,287 million (up 18.2% year-on-year), with the ratio of equity attributable to owners of parent rising to 77.8% (up 4.3 percentage points).

🤖 AI Perspective

While FT Group’s revenue and profits decreased in FY2026, the company maintained high-profit margins, which may be a point of interest for investors. However, the substantial projected decline in profits for FY2027 could indicate shifts in the business environment. The upcoming share exchange with Hikari Tsushin Inc. and subsequent delisting represent a significant strategic turning point, and investors might monitor the implications for the company’s business continuity and governance structure.

2816|ダイショー

1407.0

▲ +0.43%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Daisho Co., Ltd. announced its non-consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- For the current fiscal year, net sales increased by 4.8% to 27,489 million yen, and operating profit rose by 3.7% to 680 million yen, marking increases in both revenue and profit.

- However, ordinary profit decreased by 1.0% to 666 million yen, and net profit declined by 0.7% to 455 million yen.

- The annual dividend for the fiscal year ended March 31, 2026, was set at 21.00 yen per share (including a year-end dividend of 12.00 yen and a commemorative dividend of 3.00 yen), an increase from 18.00 yen in the previous fiscal year.

- For the fiscal year ending March 31, 2027 (April 1, 2026 – March 31, 2027), the company forecasts net sales of 28,500 million yen (up 3.7% YoY) and operating profit of 700 million yen (up 2.9% YoY), while anticipating a decrease in net profit to 420 million yen (down 7.7% YoY).

🤖 AI Perspective

The financial results for FY2026 indicate that while net sales and operating profit saw growth, an increase in non-operating expenses likely impacted the decline in ordinary and net profits. The increased annual dividend, including a commemorative dividend, may suggest a focus on shareholder returns. For the FY2027 forecast, the projected increase in sales and operating profit alongside a decrease in net profit could draw attention to the company’s future cost structure and business strategies.

4091|日本酸素HD

5876.0

▲ +4.26%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nippon Sanso Holdings reported consolidated revenue of ¥1,359,611 million for the fiscal year ended March 31, 2026, marking a 3.9% increase year-on-year, with profit attributable to owners of parent rising 25.4% to ¥123,891 million.

- Core operating profit reached ¥203,084 million (up 7.4% year-on-year), and operating profit was ¥197,882 million (up 19.3% year-on-year).

- The annual dividend for the fiscal year ended March 31, 2026, was ¥62.00 per share, an increase of ¥11.00 from the previous fiscal year.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated revenue of ¥1,380,000 million (up 1.5% year-on-year) and profit attributable to owners of parent of ¥131,000 million (up 5.7% year-on-year).

- At the end of the fiscal year, total assets were ¥2,767,679 million, and the ratio of equity attributable to owners of parent improved to 44.0%, a 3.5 percentage point increase from the previous fiscal year-end.

🤖 AI Perspective

The significant increase in profits for FY2026, despite a decrease in shipment volumes in key markets, appears to be primarily driven by effective price management and continuous productivity improvement initiatives. The improved ratio of equity attributable to owners of parent may also suggest a strengthening of the company’s financial foundation. The forecast for continued revenue and profit growth in FY2027 indicates management’s confidence in navigating dynamic business environments and maintaining a stable growth trajectory. The increase in the annual dividend for FY2026 and the projected further increase for FY2027 could be seen as a commitment to enhancing shareholder returns.

4202|ダイセル

1229.5

▲ +0.65%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Daicel Corporation received a dividend of ¥10,950 million on February 10, 2026, from its consolidated subsidiary, Daicel (China) Investment Co., Ltd.

- On April 27, 2026, the company resolved to record a provision for contingent liabilities from debt guarantees amounting to ¥24,322 million for its consolidated subsidiary, TOPAS Advanced Polymers GmbH, to prepare for potential losses related to debt guarantees.

- The received dividend will be recorded as non-operating income, and the provision for contingent liabilities as an extraordinary loss, in the individual financial statements for the fiscal year ended March 2026.

- These entries solely affect the individual financial statements and have no impact on the consolidated financial performance.

🤖 AI Perspective

This announcement highlights two significant items impacting Daicel’s individual financial statements: a dividend receipt from one consolidated subsidiary and the recording of a provision for contingent liabilities related to another. While the dividend receipt positively affects individual earnings and the provision negatively impacts individual earnings, the key takeaway for investors may be that these items will not affect the company’s consolidated results. The provision for TOPAS Advanced Polymers GmbH could suggest a need to monitor the financial health of this specific subsidiary.

4491|Cマネージメント

3005.0

▲ +0.30%

📎 Source:Cマネージメント Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2024 (FY2024), C Management’s consolidated net sales increased by 4.2% year-on-year to ¥8,235 million, operating profit grew by 22.3% to ¥628 million, and profit attributable to owners of parent increased by 28.6% to ¥511 million.

- Diluted earnings per share for FY2024 was ¥251.21.

- The consolidated financial position for FY2024 showed total assets of ¥5,727 million, net assets of ¥4,150 million, and an equity ratio of 72.5%.

- The annual dividend for FY2024 was announced at ¥60.00 per share, including a year-end dividend of ¥60.00.

- For the fiscal year ending March 31, 2025 (FY2025), the company forecasts consolidated net sales of ¥9,020 million (up 9.5% year-on-year), operating profit of ¥675 million (up 7.3% year-on-year), and profit attributable to owners of parent of ¥512 million (up 0.0% year-on-year).

🤖 AI Perspective

C Management delivered a strong performance in FY2024, with year-on-year increases in net sales, operating profit, ordinary profit, and net profit attributable to owners of parent, driven by robust IT investment demand in the information services industry. The significant growth in profit metrics, all exceeding 20%, suggests effective business strategies. Furthermore, an equity ratio of 72.5% indicates a stable financial foundation, which could be a positive factor for investors.

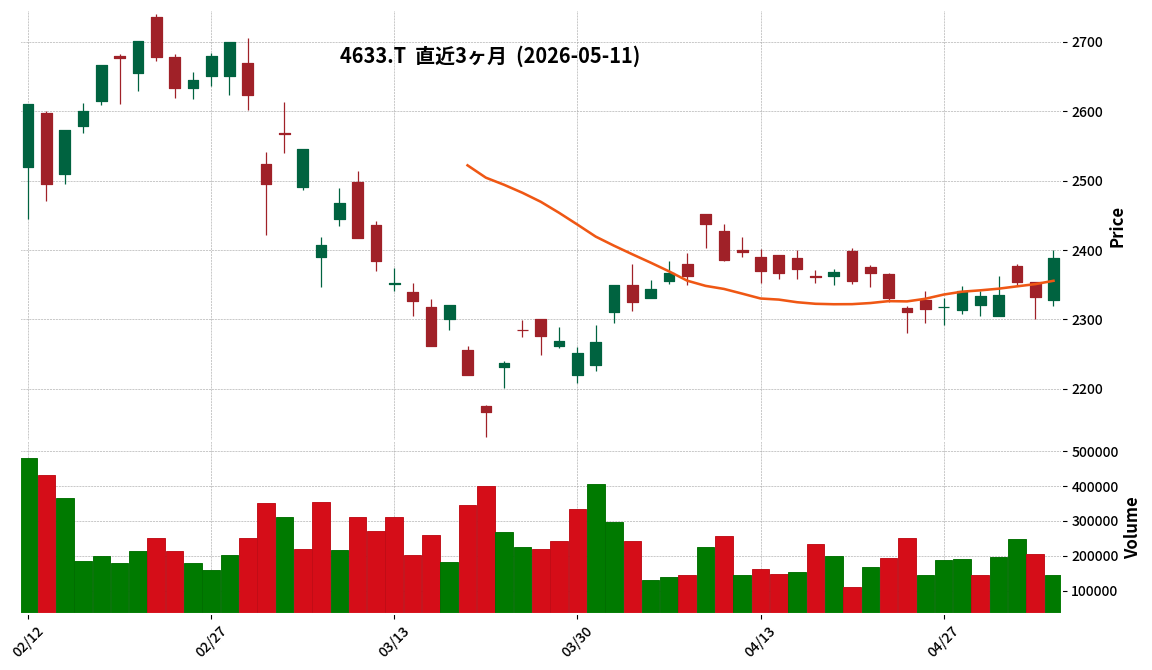

4633|サカタインクス

2388.0

▲ +2.40%

📎 Source:サカタインクス Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sakata INX announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1 to March 31, 2026).

- During this period, net sales reached JPY 68,121 million, marking a 6.3% increase year-on-year. Operating income grew by 8.2% to JPY 4,173 million, ordinary income by 13.3% to JPY 4,796 million, and net income attributable to owners of parent by 7.7% to JPY 3,314 million.

- Key factors contributing to the sales growth included strong sales performance, particularly in the Americas, robust sales of functional materials, and the positive impact of yen depreciation on currency translation.

- The company’s consolidated full-year earnings forecast for the fiscal year ending December 2026 (Net Sales: JPY 276,000 million, Operating Income: JPY 17,000 million, Ordinary Income: JPY 17,800 million, Net Income Attributable to Owners of Parent: JPY 11,800 million) remains unchanged from the most recently announced figures.

- The annual dividend forecast for the fiscal year ending December 2026 is JPY 100.00 (JPY 50.00 interim, JPY 50.00 year-end), with no revisions from the latest public announcement.

🤖 AI Perspective

Sakata INX’s first-quarter consolidated results for the fiscal year ending December 2026 indicate a solid start, with increases across all key revenue and profit metrics compared to the previous year. Strong sales in the Americas and functional materials, coupled with favorable foreign exchange effects, appear to have been significant contributors. The decision to maintain the full-year forecast may suggest a prudent outlook, and investors might monitor how the company’s strategic initiatives evolve to meet these targets amidst ongoing global economic conditions.

7931|未来工業

3130.0

▲ +2.12%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Mirai Industry Co., Ltd. announced on May 11, 2026, a partial correction to its “Consolidated Financial Results for the Fiscal Year Ended March 2026 (Japanese GAAP),” originally disclosed on April 23, 2026.

- The reason for the correction was the discovery of an error in the cost of sales ratio used for intercompany transaction eliminations.

- The corrections primarily affected figures within the “Consolidated Statements of Income,” where the cost of sales for FY2026 March was revised from ¥28,020 million to ¥28,012 million, and gross profit from ¥17,653 million to ¥17,661 million.

- For selling, general and administrative expenses, “Freight” for FY2026 March was revised from ¥2,356 million to ¥2,136 million, and “Other” from ¥4,214 million to ¥4,442 million, changing the total from ¥10,929 million to ¥10,937 million.

- Despite these revisions, the operating profit, ordinary profit, profit before income taxes, net profit, and net profit attributable to owners of the parent for the fiscal year ended March 2026 remained unchanged.

🤖 AI Perspective

This correction is attributed to an accounting error in intercompany transactions. The fact that the revisions to the cost of sales and selling, general and administrative expenses offset each other, resulting in no change to key profitability metrics such as operating income and net income, suggests that the overall impact on the company’s reported performance may be limited. However, the accuracy of financial reporting is a critical factor for investors evaluating a company, and any future disclosures regarding internal control improvements could be worth monitoring.

9342|G-スマサポ

911.0

▼ -0.11%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Sumasapo announced its Q2 FY2026 (interim) financial results for the period from October 1, 2025, to March 31, 2026.

- For the interim period, net sales were ¥1,368 million (down 3.9% year-on-year), operating profit was ¥60 million (down 47.1% year-on-year), ordinary profit was ¥60 million (down 46.9% year-on-year), and interim net profit was ¥37 million (down 60.5% year-on-year).

- User numbers for the key tenant app “totono” increased by 18.0% quarter-on-quarter, and ARPU (average revenue per user) reached ¥122, showing steady progress.

- The overall sales decreased year-on-year due to a transitional period from “totono 1.0” to “totono 2.0.”

- The full-year FY2026 earnings forecast remains unchanged from the most recently announced figures, projecting net sales of ¥3,150 million (up 11.8% year-on-year) and net profit of ¥155 million (up 19.0% year-on-year).

🤖 AI Perspective

While G-Sumasapo reported a decrease in revenue and profits for the interim period, the company highlighted steady progress in its key “totono” app, with increased user numbers and ARPU. The decline in performance is attributed to a transitional period as services migrate from “totono 1.0” to “totono 2.0,” with full-year forecasts remaining unchanged. This suggests the company views the current dip as a short-term effect of strategic upgrades, and investors may monitor the progress of this transition and the impact of ongoing investments in human capital and AI R&D for long-term growth.

130A|G-VIS

466.0

▲ +0.43%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of fiscal year 2026 (January 1 to March 31, 2026), business revenue amounted to ¥17 million, representing a 26.2% decrease compared to the same period of the previous year.

- The net loss for the quarter expanded to ¥256 million, compared to a net loss of ¥79 million in the prior fiscal year’s first quarter.

- An impairment loss of ¥135,520 thousand was recorded as an extraordinary loss, stemming from the impairment of tangible fixed assets acquired during the first quarter.

- As of March 31, 2026, total assets stood at ¥1,785 million and net assets at ¥1,527 million, with the equity ratio decreasing from 94.6% at the end of the previous fiscal year to 85.6%.

- G-VIS reported advancements in its proprietary AI drug discovery platform, aibVIS, through version upgrades, and progressed joint drug discovery research with pharmaceutical companies including Toray Corporation, Shionogi & Co., Ltd., RaQualia Pharma Inc., and Takeda Pharmaceutical Company Limited. The ASO project for acute kidney injury also moved forward with preparations for animal experiments.

🤖 AI Perspective

- The decline in business revenue, coupled with R&D expenses and the recognition of an impairment loss on tangible fixed assets, appears to be key factors in the expanded net loss for the quarter.

- The company’s updates on its AI drug discovery platform and collaborative research efforts may be significant indicators for future revenue generation.

- With the full-year performance forecast remaining unchanged, ongoing progress in business development and monetization efforts will likely be crucial for investors to monitor.

1375|ユキグニファクトリー

1052.0

▲ +0.00%

📎 Source:ユキグニファクトリー Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Yukiguni Factory announced that its consolidated operating results for the fiscal year ended March 31, 2026, exceeded the full-year forecast published on May 9, 2025. Profit attributable to owners of parent increased by 47.2% from ¥2,010 million to ¥2,958 million, and operating profit increased by 32.1% from ¥3,270 million to ¥4,319 million.

- While consolidated revenue fell short of the forecast at ¥37,845 million, higher selling prices for key mushroom products, efficient business operations, and strict control over selling, general and administrative expenses led to the upward revision in profits.

- For individual performance, net profit for the fiscal year ended March 31, 2026, significantly improved to ¥1,568 million from a loss of ¥3 million in the previous fiscal year (ended March 31, 2025). This was primarily due to the resolution of the one-time impact of impairment losses recognized in the mushroom business in the prior period.

- The company decided to increase the year-end dividend for the fiscal year ended March 31, 2026, by ¥7 from the most recent forecast (announced February 9, 2026) of ¥12 per share, to ¥19 per share.

🤖 AI Perspective

- The significant outperformance in profits despite slightly lower revenue suggests the company’s effective cost management and strategic product mix have been successful.

- The substantial improvement in individual net profit, driven by the resolution of prior period’s one-time factors and stabilization of production, may indicate strengthening business fundamentals.

- The increased dividend, consistent with the company’s policy of maintaining a payout ratio of around 30%, reflects a commitment to shareholder returns and confidence in future business growth.

1414|ショーボンド

1305.0

▼ -1.81%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Showa Bond Holdings Co., Ltd. announced its consolidated financial results for the third quarter of the fiscal year ending June 2026 (July 1, 2025, to March 31, 2026).