📌 Today’s Highlights

Today we cover 158 IR announcements. Notable among them: 日触媒 (4114), G-ユニネク (3566), レノバ (9519). Use the table of contents below to navigate to each company.

- 4114|日触媒

- 3566|G-ユニネク

- 9519|レノバ

- 3241|ウィル

- 480A|G-リブコンサル

- 5301|東海カーボン

- 5533|エリッツHD

- 5576|オービーシステム

- 8772|アサックス

- 2613|Jオイル

- 2270|雪印メグ

- 3103|ユニチカ

- 5702|大紀アルミ

- 7953|菊水化学工業

- 6563|G-みらいワークス

- 3109|シキボウ

- 3561|力の源HD

- 3787|テクノマセマ

- 4058|G-トヨクモ

- 5929|三和HD

- 6330|洋エンジ

- 6947|図研

- 7409|G-AeroEdge

- 7944|ローランド

- 9336|大栄環境

- 1332|ニッスイ

- 2170|LINK&M

- 2750|石光商事

- 2764|ひらまつ

- 343A|IACEトラベル

- 3774|IIJ

- 3853|アステリア

- 4838|SSSK HD

- 4896|G-ケイファーマ

- 5139|G-オープンワーク

- 519A|G-ベーシック

- 7075|G-QLS

- 7805|プリントネット

- 8089|ナイス

- 9564|FCE

- 1921|巴

- 2117|ウェルネオシュガー

- 2974|大英産業

- 4337|ぴあ

- 4401|ADEKA

- 5268|旭コンクリ

- 5975|東プレ

- 7726|黒田精工

- 8358|スルガ銀

- 8007|高島

- 2976|A-Nグランデ

- 4005|住友化

- 5542|新報国マテリアル

- 9501|東電力HD

- 9502|中部電力

- 7267|ホンダ

- 7988|ニフコ

- 1815|鉄建建設

- 2325|NJS

- 2938|オカムラ食品工業

- 4109|ステラケミファ

- 4224|ロンシール工

- 4620|藤倉化

- 5741|UACJ

- 8117|中央自動車工業

- 1914|日基礎

- 3446|JTECCORP

- 3940|ノムラシステム

- 5108|ブリヂス

- 7003|三井E&S

- 7567|栄電子

- 7821|前田工繊

- 8600|トモニHD

- 6846|中央製

- 7380|十六FG

- 1853|森組

- 2501|サッポロHD

- 266A|P-グローカルマーケ

- 2982|ADワークスグループ

- 3020|アプライド

- 342A|F-光貴

- 3477|G-フォーライフ

- 4437|G-GDH

- 4482|G-ウィルズ

- 4486|G-ユナイト&グロウ

- 4491|Cマネージメント

- 5843|ニッポンインシュア

- 6194|アトラエ

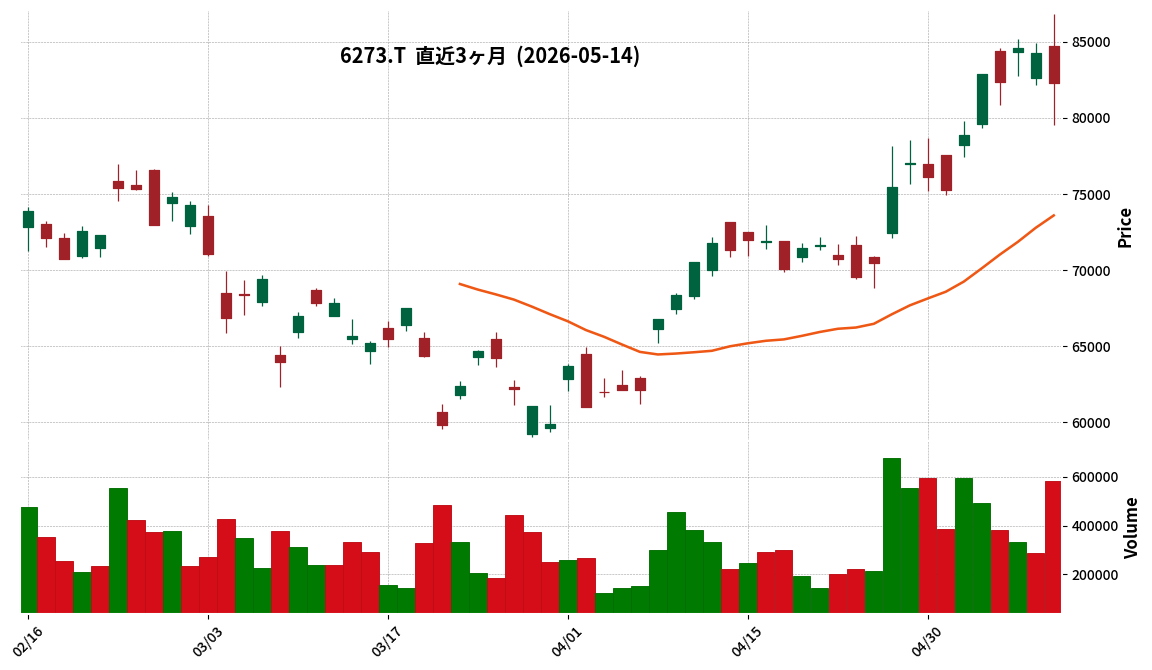

- 6273|SMC

- 6480|日トムソン

- 7791|ドリームベッド

- 8119|三栄コーポ

- 8559|豊和銀

- 2986|G-LAHD

- 3135|マーケットエンター

- 336A|G-ダイナミクマップ

- 3895|ハビックス

- 4406|新日本理化

- 4575|G-CANBAS

- 7076|名南M&A

- 3633|GMOペパボ

- 410A|G-GMOコマース

- 479A|G-PRONI

- 7048|G-ベルトラ

- 141A|G-トライアル

- 148A|G-ハッチ・ワーク

- 166A|G-タスキHD

- 9346|G-ココルポート

- 334A|G-VPJ

- 8891|AMGHD

- 1449|FUJIジャパン

- 1888|若築建

- 206A|G-PRISMBio

- 217A|P-サポート

- 2425|ケアサービス

- 2475|WDB

- 2573|北海コカ

- 2667|イメージワン

- 269A|G-Sapeet

- 2904|一正蒲鉾

- 2961|日本調理機

- 300A|MIC

- 3156|レスター

- 321A|P-ヒューマンSHD

- 3306|日製麻

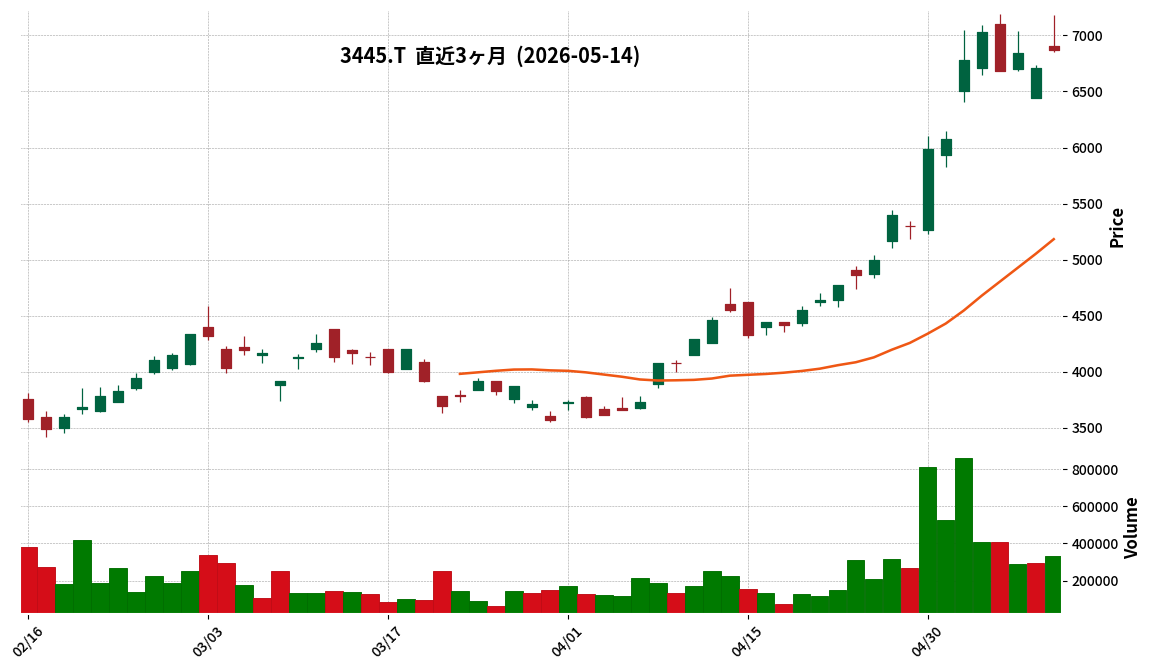

- 3445|RSTECH

- 3559|ピーバンドットコム

- 3591|ワコールHD

- 3710|ジョルダン

- 3842|ネクストジェン

- 2485|ティア

- 4619|日特塗料

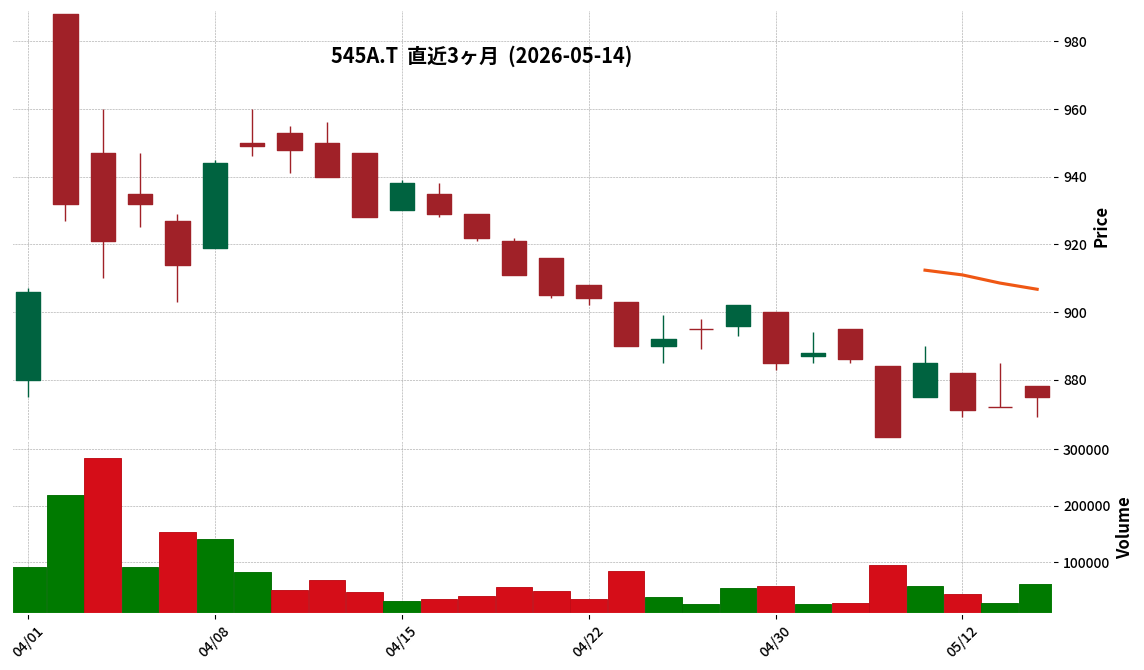

- 545A|トランヴィア

- 2207|meito

- 199A|P-メディエア

- 3687|フィックスターズ

- 4884|G-クリングル

- 6078|バリューHR

- 6659|メディアリンクス

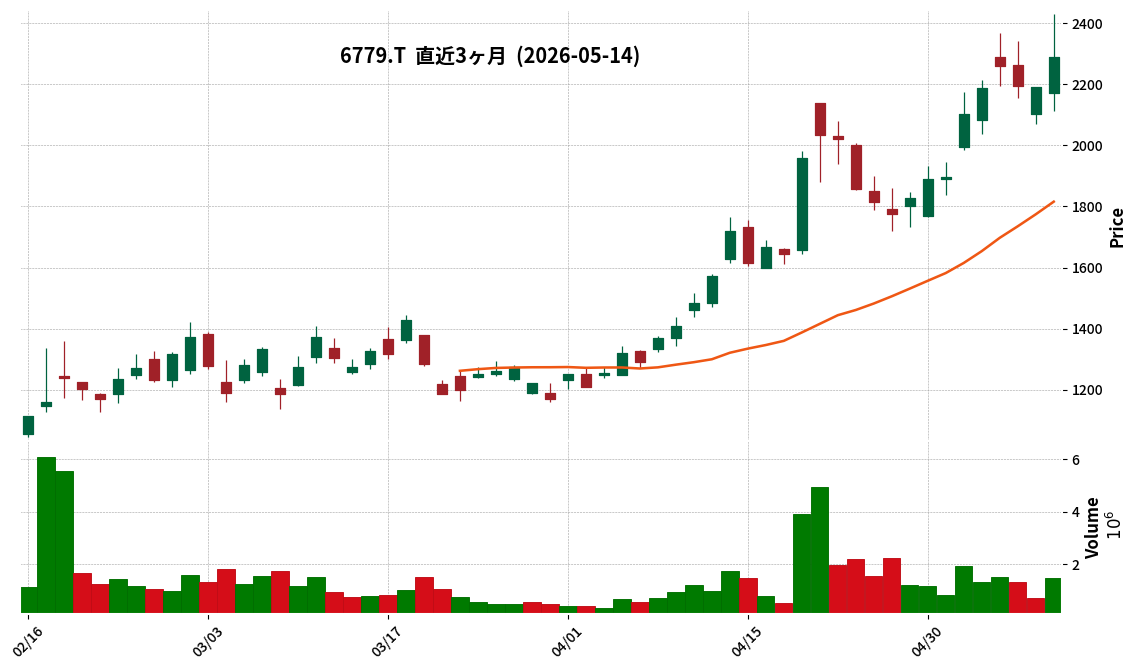

- 6779|日電波

- 7362|G-T.S.I

- 9404|日テレHD

- 9713|ロイヤルホテル

- 4013|G-勤次郎

- 330A|G-TalentX

- 243A|P-トップス

- 4068|G-ベイシス

- 5133|テリロジーHD

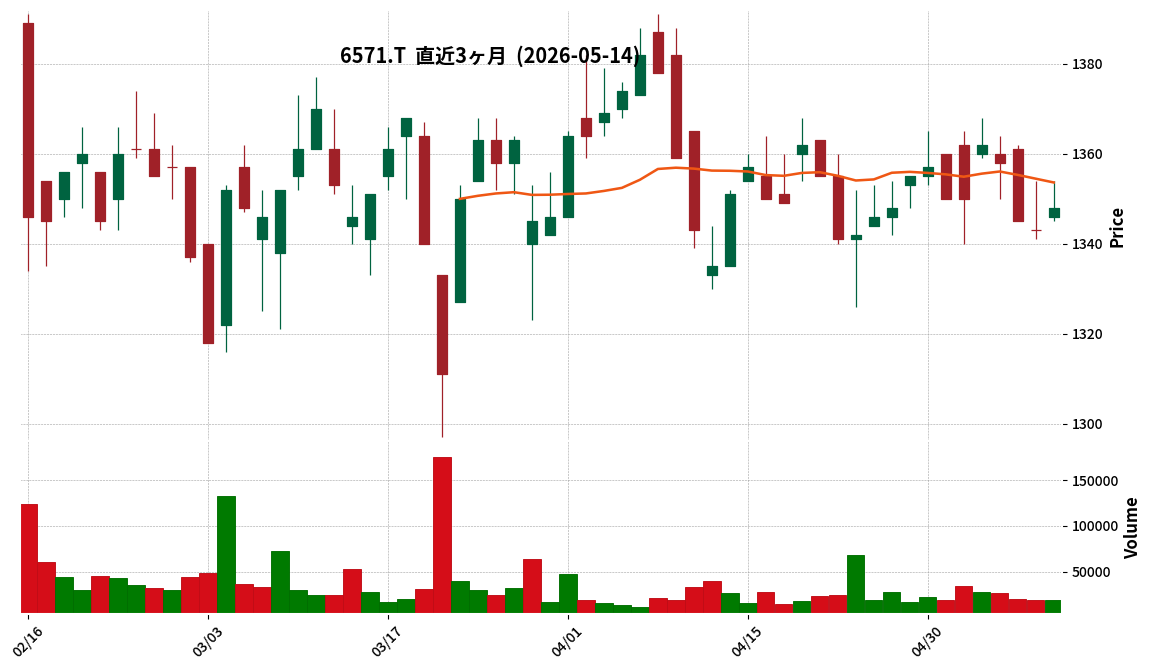

- 6571|キュービーネットHD

- 9028|ゼロ

- 9409|テレビ朝日HD

- 2334|G-イオレ

- 4480|メドレー

- 7363|G-ベビーカレンダー

- 4937|G-Waqoo

- 5033|G-ヌーラボ

- 2436|共同PR

- 3034|クオールHD

4114|日触媒

2142.5

▼ -2.06%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nippon Shokubai reported full-year results for the fiscal year ended March 2026, with net sales of ¥399.9 billion (down 2.3% year-on-year), operating profit of ¥17.5 billion (down 8.0% year-on-year), and profit attributable to owners of parent of ¥16.8 billion (down 3.6% year-on-year).

- By segment, the Materials business recorded segment profit of ¥11.9 billion (down 24.8% year-on-year), while the Solutions business recorded segment profit of ¥6.0 billion (down 2.4% year-on-year, but up in revenue and profit excluding equity-method investment gain/loss).

- Key factors contributing to the profit decrease included increased selling, general and administrative expenses, higher manufacturing fixed costs, a decrease in inventory valuation gains, and impairment losses at equity-method affiliates.

- The company has stated that the earnings forecast for the fiscal year ending March 2027 is currently undecided due to the difficulty in reasonably calculating the impact of escalating tensions in the Middle East.

- Regarding shareholder returns, the company announced a policy to distribute dividends at 100% payout ratio or DOE of 2.0%, whichever is higher, and to acquire treasury shares with funds obtained from reducing strategic shareholdings.

🤖 AI Perspective

Nippon Shokubai’s FY2026/3 results indicate that while spread expansion due to lower raw material prices provided a positive factor, increased SG&A expenses and impairment losses at equity-method affiliates weighed down overall profits, particularly from the Materials business. The decision to leave the FY2027/3 earnings forecast undecided highlights the significant uncertainty surrounding geopolitical risks in the Middle East and their potential impact on the company’s operations and supply chain. Investors may find it worth monitoring how the company addresses these external factors and when a more definitive outlook becomes available.

3566|G-ユニネク

909.0

▲ +1.45%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of the fiscal year ending December 2026 (January 1, 2026 to March 31, 2026), sales revenue totaled ¥2,056 million, representing a 19.8% increase compared to the same period in the previous year.

- Operating income for the quarter was ¥16 million, ordinary income was ¥19 million, and net income for the quarter was ¥12 million, marking a return to profitability or significant profit growth from losses in the prior-year period.

- As of the end of the first quarter, total assets stood at ¥6,079 million, an increase of ¥723 million from the end of the previous fiscal year. Current assets increased by ¥657 million, primarily due to increases in merchandise, notes, and accounts receivable.

- Total liabilities amounted to ¥2,259 million, an increase of ¥758 million from the end of the previous fiscal year, mainly driven by an ¥807 million increase in notes and accounts payable.

- The full-year performance forecast for the fiscal year ending December 2026 and the annual dividend forecast of ¥6.00 per share remain unchanged from the most recently published figures.

🤖 AI Perspective

G-ユニネク’s Q1 FY2026 results indicate robust sales growth and a significant turnaround in profitability across all income levels compared to the prior year. Achieving profitability in the first quarter, typically an off-season for uniform sales, suggests effective strategies. The reported increases in merchandise inventory and the advancement of their hybrid sales model may have contributed to these results. Investors may want to continue monitoring the company’s progress against its full-year earnings forecast.

9519|レノバ

1220.0

▼ -2.01%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Renova Inc. reported consolidated results for the fiscal year ended March 2026: net sales of JPY 87,622 million (up 24.7% year-on-year), EBITDA of JPY 30,526 million (up 31%), and operating income of JPY 8,283 million (up 104%).

- For the fiscal year ending March 2027, the company forecasts consolidated net sales of JPY 95,700 million (up 9% year-on-year), EBITDA of JPY 33,800 million (up 11%), and operating income of JPY 11,300 million (up 36%).

- In March 2026, the investment decision and construction start for the Kikukawa Nishimura Battery Storage Project (90MW/270MWh) were announced, with project finance secured as one of Japan’s largest market-sale battery storage projects. Operations are scheduled to commence in FY2028.

- The Power Purchase Agreement (PPA) for the Reihoku-Amakusa Onshore Wind Project is stated to be nearing finalization.

- Planned annual maintenance days for biomass power generation projects in FY2027/3 are projected to decrease by 57 days year-on-year to 194 days, with maintenance primarily concentrated in the first quarter.

🤖 AI Perspective

Renova’s strong performance in the fiscal year ended March 2026, driven by full-year contributions from biomass power plants and project development fees, indicates successful execution of its growth strategy. The significant increase in operating income suggests improved operational efficiency and profitability. The successful project financing for the Kikukawa Nishimura Battery Storage Project, a large-scale market-sale initiative, highlights the company’s commitment to expanding its battery storage portfolio. Investors may also note the projected reduction in maintenance days for biomass operations in FY2027/3, which could contribute to sustained earnings growth.

3241|ウィル

586.0

▼ -1.18%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Will Co., Ltd. announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026 to March 31, 2026).

- Consolidated net sales amounted to ¥4,143 million, a 33.6% increase compared to the same period of the previous year.

- Consolidated operating profit reached ¥434 million (up 122.2% year-on-year), and ordinary profit was ¥394 million (up 135.0% year-on-year).

- Profit attributable to owners of parent was ¥236 million, marking a 137.7% increase year-on-year.

- By segment, the Real Estate Development and Sales business reported net sales of ¥2,602 million (up 47.9% year-on-year) and operating profit of ¥193 million (up 127.5% year-on-year), driving overall sales. The Real Estate Brokerage business also performed strongly with net sales of ¥1,044 million (up 30.3% year-on-year) and operating profit of ¥355 million (up 113.9% year-on-year).

🤖 AI Perspective

Will’s Q1 FY2026 results show substantial year-on-year growth across net sales and all profit metrics. This performance appears to be primarily driven by strong sales progress in the Real Estate Development and Sales business, coupled with an increase in contract volumes and commission fees within the Real Estate Brokerage business. The robust start to the fiscal year suggests that investors may wish to monitor the company’s progress against its full-year earnings forecast.

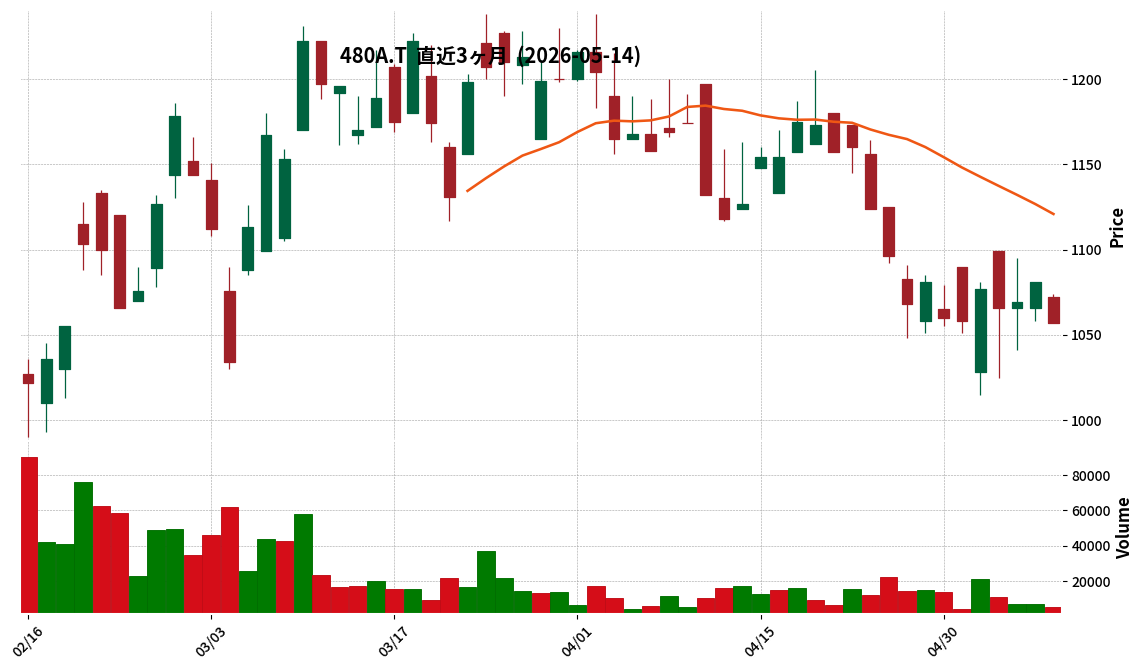

480A|G-リブコンサル

1057.0

▼ -2.22%

📎 Source:G-リブコンサル Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Libcon (Code: 480A) announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026 to March 31, 2026).

- For the first quarter, consolidated net sales were ¥1,805 million, EBITDA ¥324 million, operating income ¥295 million, ordinary income ¥303 million, and net income attributable to owners of parent ¥201 million.

- Year-on-year growth rates are not provided as the company did not prepare consolidated financial statements for the first quarter of the fiscal year ended December 2025.

- The full-year consolidated earnings forecast for the fiscal year ending December 2026 remains unchanged, with net sales projected at ¥7,086 million (16.0% increase year-on-year) and net income attributable to owners of parent at ¥721 million (41.2% increase year-on-year).

- As of the end of the first quarter, total assets stood at ¥4,535 million, net assets at ¥3,770 million, and the equity ratio at 82.9%.

🤖 AI Perspective

G-Libcon has disclosed its first consolidated Q1 financial results. While direct year-on-year comparisons are unavailable, these figures provide a baseline for evaluating progress against the full-year forecast. The high equity ratio of 82.9% may suggest a strong financial position, which could be a point of interest for investors monitoring the company’s stability.

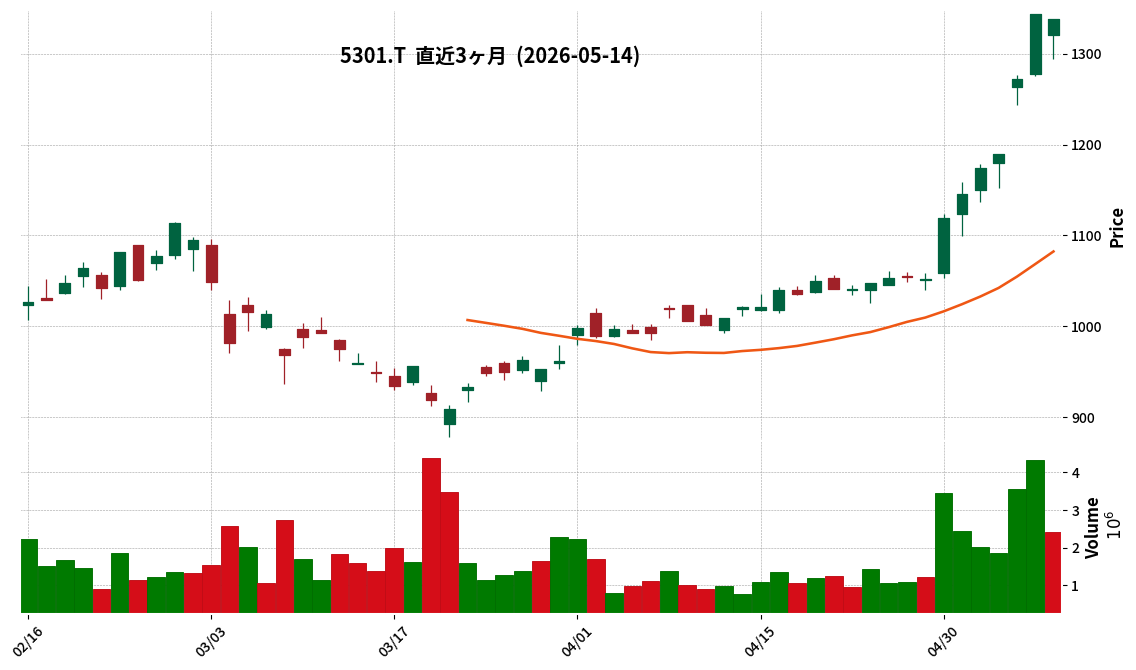

5301|東海カーボン

1338.0

▼ -0.41%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tokai Carbon has released its presentation materials for the first quarter of the fiscal year ending December 2026.

- The document summarizes information regarding the company’s financial performance and business activities during the first quarter.

- The fiscal year in question is FY2026, and the disclosed information specifically covers the first quarter.

🤖 AI Perspective

The released earnings presentation materials provide fundamental information for understanding Tokai Carbon’s current business status and financial health. Investors may be looking for detailed numerical data on revenue, profit margins, and segment performance to gain insights into the company’s present condition and future outlook. Comparisons to the prior year’s same quarter and against broader market trends could be crucial for evaluating the company’s competitiveness and growth strategies.

5533|エリッツHD

1949.0

▼ -0.05%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- ERITZ HOLDINGS announced its consolidated financial results for the second quarter (cumulative) of the fiscal year ending September 2026.

- Net sales reached ¥3.526 billion, an increase of 8.2% compared to the same period of the previous year.

- Operating profit amounted to ¥0.590 billion, marking a 16.1% increase year-on-year.

- Net income attributable to owners of the parent was ¥0.389 billion, up 18.4% from the prior year’s period.

- Key Performance Indicators (KPIs) include a 1.7% increase (209 units) in rental brokerage contracts and a 1.5% increase (430 units) in rental property management units compared to the end of the previous fiscal year.

- Growth was observed across the real estate brokerage, real estate management, and resident support businesses, with spot transactions also contributing to profit.

- The full-year consolidated earnings forecast remains unchanged as of this earnings announcement.

🤖 AI Perspective

ERITZ HOLDINGS’ Q2 results demonstrate solid revenue and profit growth across all segments, indicating a stable expansion of its core businesses. The increase in both rental brokerage contracts and managed property units suggests a strengthening foundation for the company’s business model. The contribution from spot transactions also highlights an additional revenue stream that helped boost profitability.

5576|オービーシステム

2781.0

▲ +0.04%

📎 Source:オービーシステム Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- O.B.System reported record-high financial results for the fiscal year ended March 2026, with net sales of ¥8,655 million (up 12.6% YoY), gross profit of ¥1,675 million (up 15.7% YoY), operating income of ¥672 million (up 19.5% YoY), ordinary income of ¥727 million (up 18.9% YoY), and net income attributable to owners of the parent of ¥599 million (up 23.6% YoY).

- Despite a decrease in orders due to the completion of large projects in the banking sector, the expansion of the insurance sector and M&A (consolidation of Green Cat Co., Ltd.) contributed to the increase in net sales.

- Selling, general, and administrative expenses increased to ¥1,003 million (up 13.3% YoY) due to higher personnel costs and training expenses for staffing reinforcement, but the increase in gross profit absorbed these costs, leading to higher profits.

- The equity ratio stood at 74.8% (down 4.2 percentage points from the previous fiscal year-end), and net assets increased to ¥5,698 million.

- Operating cash flow was ¥329 million, and free cash flow significantly increased.

🤖 AI Perspective

O.B.System’s achievement of record-high sales and profits, despite the completion of a major project in its core banking sector, suggests successful strategic diversification through M&A and growth in the insurance domain. The ability to absorb increased SG&A expenses from proactive investments while still expanding profitability could indicate effective business management and a resilient operational model. The continued strong equity ratio further highlights the company’s solid financial foundation, which may be a point of interest for investors.

8772|アサックス

872.0

▲ +0.35%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Asax Co., Ltd. announced on May 14, 2026, an “Amendment to the ‘Notice of Revision to Dividend Forecast (Increase in Dividend)'”.

- The amendment addresses the incorrect attachment of past disclosure materials in the original “Notice of Revision to Dividend Forecast (Increase in Dividend)” released on May 13, 2026.

- According to the May 13, 2026, announcement, the year-end dividend forecast for the fiscal year ending March 2026 has been revised.

- The revised year-end dividend per share is ¥22.00 (annual total ¥22.00), an increase of ¥2.00 from the previous forecast of ¥20.00 (announced on May 1, 2025).

- The reason for the dividend forecast revision is stated as the company’s strong performance and its policy of actively returning profits to shareholders.

🤖 AI Perspective

This IR correction clarifies that the original dividend forecast revision (an increase) remains unchanged, and the correction pertains only to an erroneously attached document. Investors may view this as a reaffirmation of the increased dividend and an indication of the company’s commitment to accurate information disclosure. The increased dividend itself reflects the company’s efforts to enhance profitability and its intent to actively return profits to shareholders.

2613|Jオイル

1967.0

▲ +0.05%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- JOYL’s consolidated financial results for the fiscal year ended March 2026 show net sales of ¥226.57 billion, operating income of ¥4.40 billion, ordinary income of ¥5.78 billion, and net income attributable to owners of the parent of ¥4.75 billion.

- Compared to the previous fiscal year, net sales decreased by ¥4.21 billion (98.2%), and operating income decreased by ¥4.17 billion (51.4%), resulting in decreased revenue and profit.

- Operating income for the Oils & Fats Business was ¥3.38 billion (40.9% year-on-year), while the Specialty Food Business reported operating income of ¥0.83 billion (613.1% year-on-year).

- The consolidated forecast for the fiscal year ending March 2027 projects net sales of ¥243.00 billion, operating income of ¥5.50 billion, ordinary income of ¥6.20 billion, and net income attributable to owners of the parent of ¥5.00 billion.

- The company plans an annual dividend of ¥80 for the fiscal year ending March 2027, an increase of ¥10 from the previous year.

🤖 AI Perspective

JOYL’s FY2026/3 results show a revenue and profit decline, primarily attributed to cost increases that price revisions could not fully offset, particularly impacting the Oils & Fats business. In contrast, the Specialty Food business demonstrated significant profit growth, highlighting diverging performance across segments. The company’s FY2027/3 forecast projects a recovery with increased revenue and profit, suggesting that the completion of price revisions and expansion into high-value-added areas may be key drivers. The planned dividend increase could also indicate confidence in future profitability improvements.

2270|雪印メグ

3145.0

▲ +1.29%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Snow Brand Megmilk Co., Ltd. announced its consolidated financial results for the fiscal year ended March 2026.

- Consolidated net sales amounted to ¥615,761 million, representing a slight decrease of 0.0% year-on-year.

- Consolidated operating profit was ¥18,266 million, a decrease of 4.5% compared to the previous fiscal year.

- Net profit attributable to owners of parent significantly increased by 136.6% year-on-year, reaching ¥32,897 million.

- This substantial increase in net profit was primarily driven by the recording of gains from the sale of policy-held shares.

- Earnings per share (EPS) for the fiscal year ended March 2026 was ¥524.82.

- A resolution for share buybacks has been announced, and its impact has been considered in the projected EPS for the fiscal year ending March 2027.

🤖 AI Perspective

The significant increase in net profit attributable to owners of parent was primarily a result of gains from the sale of policy-held shares, which suggests a strategic portfolio adjustment. While sales remained largely flat, the decrease in operating profit could indicate pressures from rising costs or increased promotional spending. For the upcoming fiscal year, the company forecasts both revenue and operating profit growth, and the impact of the announced share buyback on EPS will be a key point for investors to monitor.

3103|ユニチカ

2287.0

▼ -1.21%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Unitika Ltd. has announced its consolidated financial results for the fiscal year ended March 31, 2026.

- Consolidated net sales amounted to ¥118,563 million, marking a 6.2% decrease compared to the previous fiscal year.

- Operating profit was ¥10,549 million, representing an 80.3% increase year-on-year.

- Ordinary profit reached ¥10,392 million, an increase of 121.4% from the prior fiscal year.

- Net profit attributable to parent company shareholders turned profitable at ¥18,153 million, a significant improvement from a loss of △¥24,283 million in the previous period.

- Earnings per share (EPS) for the period stood at ¥310.33.

- The equity ratio improved to 35.7%.

- The consolidated earnings forecast for the fiscal year ending March 31, 2027, projects net sales of ¥84,000 million (a 29.2% decrease year-on-year), operating profit of ¥8,000 million (a 24.2% decrease), and net profit attributable to parent company shareholders of ¥5,000 million (a 72.5% decrease).

🤖 AI Perspective

Unitika’s FY2026 results show a notable improvement in profitability, with operating profit, ordinary profit, and net profit attributable to parent company shareholders all increasing significantly, despite a decrease in net sales. This turnaround could suggest that the company’s structural reforms, including business divestitures and cost reduction initiatives, are yielding positive results. Investors may want to monitor the company’s progress on these reforms and how they will impact the forecasted decline in sales and profits for FY2027.

5702|大紀アルミ

1566.0

▼ -2.31%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Daiki Aluminium Industry Co., Ltd. announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- Consolidated net sales reached ¥331,109 million, an increase of 10.4% year-on-year.

- Operating profit was ¥7,268 million (up 50.4% YoY), and ordinary profit was ¥5,620 million (up 49.9% YoY).

- Profit attributable to owners of parent significantly increased to ¥3,680 million, a 426.4% rise from the previous fiscal year.

- For the fiscal year ending March 31, 2027 (April 1, 2026 – March 31, 2027), the company forecasts consolidated net sales of ¥386,700 million (up 16.8% YoY) and profit attributable to owners of parent of ¥8,840 million (up 140.2% YoY).

- The annual dividend for FY2026 was finalized at ¥55.00 (interim ¥25.00, year-end ¥30.00), and the forecast for FY2027 is ¥70.00 (interim ¥35.00, year-end ¥35.00).

🤖 AI Perspective

Daiki Aluminium’s FY2026 results show substantial growth across all key profit metrics, with a notable 426.4% increase in profit attributable to owners of parent. This performance may suggest the positive impact of rising LME prices, robust demand, pricing adjustments, and material shifts on the company’s profitability. The strong FY2027 outlook, anticipating continued revenue and profit growth alongside an increased dividend forecast, could indicate the company’s confidence in its future operational trajectory and strategic initiatives.

7953|菊水化学工業

390.0

▲ +1.30%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kikusui Chemical Industry announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- Consolidated net sales amounted to ¥21,602 million, representing a 1.0% increase from the previous fiscal year.

- Consolidated operating profit was ¥403 million (up 52.3% year-on-year), and consolidated ordinary profit was ¥495 million (up 44.9% year-on-year).

- Profit attributable to owners of parent reached ¥270 million, marking a 63.1% increase from the prior year.

- The consolidated performance forecast for the fiscal year ending March 31, 2027, is currently undetermined due to the difficulty in making reasonable estimates impacted by the situation in the Middle East.

- The year-end dividend is set at ¥10.00 per share, making the annual dividend ¥17.00 (same as the previous year).

🤖 AI Perspective

Kikusui Chemical Industry’s FY2026/3 results show significant profit growth despite a modest increase in net sales, which may suggest improved profitability and operational efficiency. The substantial rise in operating profit, exceeding 50%, could indicate effective cost management or higher-margin product sales. However, the decision to leave the FY2027/3 forecast undetermined due to geopolitical factors introduces an element of uncertainty, which investors might consider when evaluating future prospects.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

6563|G-みらいワークス

580.0

▲ +0.17%

📎 Source:G-みらいワークス Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-mirai works reported consolidated net sales of ¥5,846 million for the second quarter of the fiscal year ending September 2026, marking a 2.2% increase year-on-year.

- Operating profit stood at ¥253 million, a 2.0% increase from the same period last year, and ordinary profit was ¥256 million, also up 2.0% year-on-year.

- Net income attributable to owners of parent increased by 13.6% year-on-year to ¥175 million.

- Basic earnings per share for the interim period were ¥33.81.

- The full-year consolidated earnings forecast for the fiscal year ending September 2026 (Net sales ¥13,000 million, Operating profit ¥600 million, Ordinary profit ¥600 million, Net income attributable to owners of parent ¥360 million) remains unchanged.

🤖 AI Perspective

G-mirai works’ Q2 results demonstrate growth in both revenue and various profit metrics. The higher growth rate in net income attributable to owners of parent, compared to other profit figures, may suggest improved profitability or efficiency within the company. The decision to keep the full-year forecast unchanged indicates management’s current view on future performance, which will likely be a point of continued observation for investors.

3109|シキボウ

1038.0

▼ -0.29%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Consolidated net sales for the fiscal year ended March 31, 2026, increased by 14.0% year-on-year to ¥44,554 million.

- Consolidated operating profit for the same period was ¥974 million (down 27.6% year-on-year), and ordinary profit was ¥658 million (down 37.1% year-on-year).

- Net income attributable to parent company shareholders increased by 4.0% year-on-year to ¥950 million.

- For the fiscal year ending March 31, 2027 (forecast), the company projects consolidated net sales of ¥55,700 million (up 25.0% year-on-year) and operating profit of ¥1,500 million (up 53.9% year-on-year).

- The annual dividend per share is projected to remain at ¥50.00 (¥25.00 interim, ¥25.00 year-end) for both FY2026/3 and FY2027/3 (forecast).

- Effective from the current consolidated fiscal year, the company has changed its reporting segments, establishing a new Functional Materials segment for its functional materials business.

- A significant change in the scope of consolidation occurred during the period, with PT. SHIKIBO MERMAID INDONESIA newly consolidated.

🤖 AI Perspective

Shikibo’s FY2026/3 results show a significant increase in net sales, which may be largely attributed to the business acquisition from Unitika Group. However, the decline in operating and ordinary profits could indicate the impact of acquisition-related expenses and increased depreciation costs from new factory operations. The rise in net income attributable to parent shareholders might be influenced by one-time factors such as the recognition of negative goodwill from the business acquisition. The robust FY2027/3 forecast for sales and operating profit suggests that the full benefit of the acquisition and potential changes in cost structure could be key factors for investors to monitor.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

3561|力の源HD

1474.0

▲ +0.61%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Chikaranomoto Holdings Co., Ltd. announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- Net sales for the period were ¥36,261 million, an increase of 6.1% compared to the previous fiscal year.

- Operating income was ¥2,325 million (down 17.3% year-on-year), and ordinary income was ¥2,582 million (down 9.1% year-on-year).

- Profit attributable to owners of parent was ¥1,829 million, an increase of 4.0% compared to the previous fiscal year.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥40,125 million (up 10.7% year-on-year), operating income of ¥2,595 million (up 11.6% year-on-year), and profit attributable to owners of parent of ¥1,807 million (down 1.2% year-on-year).

- The annual dividend for FY2026/3 was ¥20 (¥10 interim, ¥10 year-end), and the forecast for FY2027/3 is ¥24 (¥12 interim, ¥12 year-end).

🤖 AI Perspective

Chikaranomoto HD’s FY2026/3 results show a revenue increase, but a decrease in operating and ordinary income, while net profit attributable to owners of parent saw an increase. This could suggest a shift in the company’s profit structure despite top-line growth. Investors may focus on the quality of earnings and the underlying reasons for the projected slight decrease in net profit attributable to owners of parent for FY2027/3, even with forecasted increases in sales and operating income.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

3787|テクノマセマ

411.0

▼ -1.91%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- TechmoMathematica Inc. has announced its non-consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- Net sales for FY2026 reached ¥685 million, marking a 64.6% increase compared to the previous fiscal year.

- The company reported an operating income of ¥44 million (vs. an operating loss of ¥286 million in FY2025), ordinary income of ¥106 million (vs. an ordinary loss of ¥282 million in FY2025), and net income of ¥85 million (vs. a net loss of ¥285 million in FY2025), indicating a return to profitability.

- Basic earnings per share stood at ¥33.16 for FY2026, compared to a loss per share of ¥109.91 in FY2025.

- For the fiscal year ending March 31, 2027, the company forecasts full-year net sales of ¥705 million (a 2.8% increase YoY) and a net income of ¥31 million (a 64.0% decrease YoY).

🤖 AI Perspective

The significant increase in net sales and the return to profitability across all key income metrics for FY2026 are notable for investors, suggesting successful business expansion and project acquisitions in both the software license and solution divisions. However, the forecast for FY2027, while projecting continued revenue growth, anticipates a substantial decrease in net income, which may warrant further analysis into the company’s future cost structure and profitability drivers. This divergence between revenue and profit growth in the outlook could indicate shifting operational dynamics.

4058|G-トヨクモ

1856.0

▼ -1.01%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Toyokumo announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026 – March 31, 2026).

- Sales revenue reached 1,389 million yen, marking a 29.0% increase compared to the same period last year.

- EBITDA was 665 million yen (+70.0% YoY), operating profit was 600 million yen (+80.5% YoY), and ordinary profit was 604 million yen (+81.2% YoY).

- Net profit attributable to owners of the parent company increased by 82.9% year-on-year to 401 million yen.

- Earnings per share for the quarter were 36.72 yen.

- There were no revisions to the consolidated full-year earnings forecast or the dividend forecast for the fiscal year ending December 2026 from the most recently published figures.

🤖 AI Perspective

G-Toyokumo’s Q1 FY2026 results show significant year-over-year growth across sales and all profit metrics. The higher growth rates in operating and net profit compared to sales growth may suggest an improvement in profitability. The sustained performance of its cloud service business will be a key area to monitor in future earnings reports.

5929|三和HD

3521.0

▼ -0.42%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sanwa Holdings Corporation has announced its consolidated financial results for the fiscal year ended March 31, 2026.

- Net sales were ¥660,712 million (down 0.3% from the previous year), operating profit was ¥79,095 million (down 1.8%), and ordinary profit was ¥80,647 million (down 4.0%).

- Profit attributable to owners of parent increased by 3.9% to ¥59,776 million.

- The annual dividend per share increased from ¥106 in the prior year to ¥130.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥677,000 million (up 2.5% year-on-year), operating profit of ¥81,000 million (up 2.4%), and profit attributable to owners of parent of ¥60,000 million (up 0.4%).

🤖 AI Perspective

Sanwa Holdings’ FY2026 results show a slight decline in net sales, operating, and ordinary profit, but an increase in net profit attributable to owners of parent, which may suggest improved efficiency or contributions from non-operating income. The significant increase in the annual dividend could indicate a strong commitment to shareholder returns. The company’s forecast for FY2027 projects growth in both revenue and profit, which is worth monitoring for investors.

6330|洋エンジ

2125.0

▼ -0.38%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Toyo Engineering reported consolidated net sales of ¥182,941 million for the fiscal year ended March 31, 2026, marking a 34.2% decrease compared to the previous fiscal year.

- The company recorded an operating loss of ¥19,003 million, an ordinary loss of ¥11,398 million, and a net loss attributable to owners of parent of ¥14,944 million for the same period.

- Basic earnings per share for the fiscal year ended March 31, 2026, was ¥-255.03.

- The annual dividend for the fiscal year ended March 31, 2026, was ¥0.00.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥190,000 million (a 3.9% increase year-on-year), operating profit of ¥3,000 million, ordinary profit of ¥7,500 million, and net profit attributable to owners of parent of ¥6,000 million, with a planned year-end dividend of ¥25.00.

🤖 AI Perspective

The fiscal year 2026 consolidated results indicate a significant decline in revenue and a shift to losses across all key profitability metrics, suggesting a challenging period possibly influenced by specific project impacts or broader market conditions. However, the company’s forecast for fiscal year 2027 projects a return to revenue growth and profitability, along with the resumption of dividends. This outlook may suggest management’s confidence in an operational recovery. Investors could find it valuable to monitor the company’s progress against these forward-looking statements.

6947|図研

4455.0

▲ +0.22%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, Zuken reported consolidated net sales of ¥43,101 million (up 5.8% year-on-year), operating profit of ¥5,865 million (up 8.8%), ordinary profit of ¥7,133 million (up 20.2%), and profit attributable to owners of parent of ¥5,400 million (up 3.3%).

- The annual dividend per share is projected to be ¥200, an increase of ¥100 from the previous fiscal year, comprising a regular dividend of ¥100 and a commemorative dividend of ¥100.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥46,000 million (up 6.7% year-on-year), operating profit of ¥6,700 million (up 14.2%), ordinary profit of ¥7,800 million (up 9.3%), and profit attributable to owners of parent of ¥5,700 million (up 5.6%).

- The annual dividend per share for the fiscal year ending March 31, 2027, is expected to be ¥150, reflecting a ¥50 increase in the regular dividend from ¥100.

- Total assets reached ¥67,625 million, net assets were ¥41,277 million, and the equity ratio stood at 61.0%.

🤖 AI Perspective

Zuken’s FY2026/3 results demonstrate robust performance with increases across all key profit metrics, notably a significant 20.2% rise in ordinary profit, which may suggest improved operational efficiency. The substantial increase in the annual dividend, including a commemorative payout, along with a projected further increase for FY2027/3, could indicate a strong commitment to shareholder returns. The positive outlook for FY2027/3, forecasting continued sales and profit growth, suggests sustained business momentum and may be a point of interest for investors.

7409|G-AeroEdge

4325.0

▼ -0.69%

📎 Source:G-AeroEdge Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-AeroEdge announced its Q3 FY2026 financial results for the period from July 1, 2025, to March 31, 2026.

- Cumulative net sales reached ¥3.775 billion, marking a 36.0% increase year-on-year, while operating profit grew by 67.9% to ¥1.007 billion.

- Ordinary profit was ¥969 million (+81.4% YoY), and quarterly net profit was ¥660 million (+44.2% YoY).

- The equity ratio as of the end of Q3 FY2026 stood at 39.4%.

- The full-year FY2026 forecast remains unchanged, projecting net sales of ¥5.050 billion (+40.2% YoY) and operating profit of ¥1.070 billion (+63.3% YoY).

🤖 AI Perspective

G-AeroEdge achieved significant revenue and profit growth this quarter, largely attributed to the recovery and expansion of aircraft demand, which boosted sales of its core titanium-aluminum low-pressure turbine blades. The company is actively pursuing mass production of new materials and the launch of new aircraft engine components, suggesting ongoing efforts to build a foundation for future business expansion. While increased upfront investments have been reported, their contribution to future earnings will be worth monitoring.

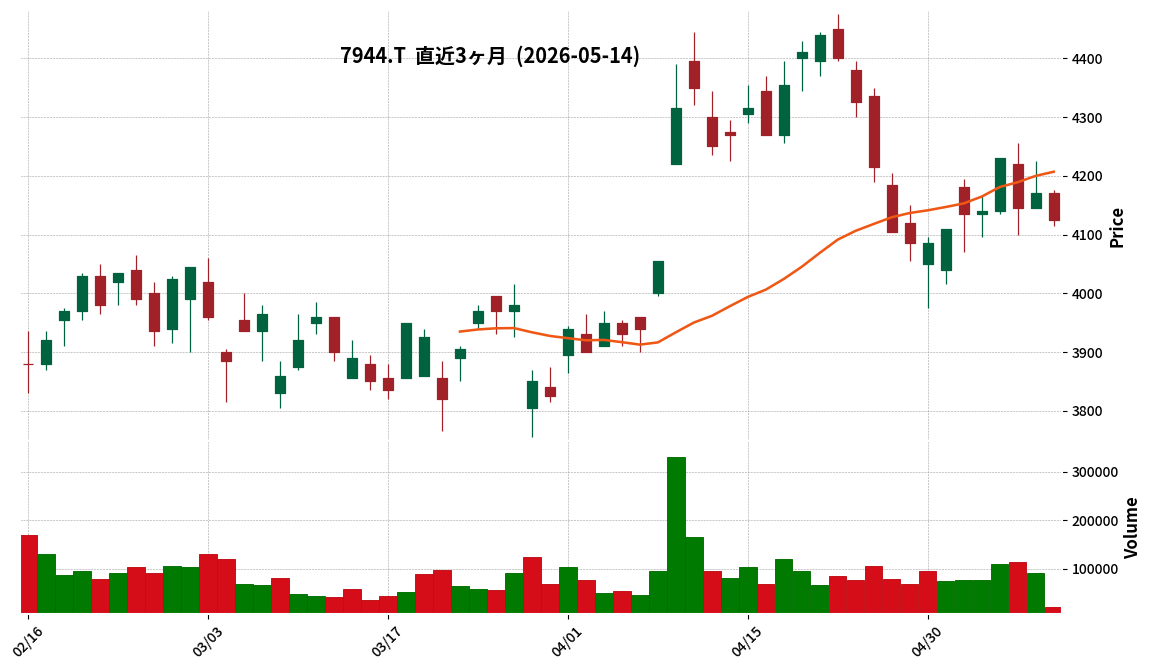

7944|ローランド

4125.0

▼ -1.08%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Roland’s consolidated net sales for the first quarter of fiscal year 2026 (January 1 to March 31, 2026) were ¥25,633 million, representing a 13.7% increase year-on-year.

- Consolidated operating profit amounted to ¥1,947 million, a 35.0% increase compared to the same period last year.

- Consolidated ordinary profit was ¥1,731 million, an increase of 28.9% year-on-year.

- Net profit attributable to owners of parent decreased by 22.1% year-on-year to ¥1,429 million.

- By product category, keyboard instruments saw a 19.2% increase, wind & percussion instruments a 16.3% increase, and guitar-related equipment a 20.9% increase. However, creation-related equipment & services decreased by 6.6%, and video & audio equipment by 21.0%.

- The full-year consolidated earnings forecast for FY2026 remains unchanged, projecting net sales of ¥106,400 million (up 5.4% year-on-year), operating profit of ¥10,000 million (up 6.2% year-on-year), and net profit attributable to owners of parent of ¥7,200 million (up 232.1% year-on-year).

🤖 AI Perspective

Roland’s Q1 results show strong year-over-year growth in both net sales and operating profit, which may suggest effective product strategies and market recovery in key segments. However, the decline in net profit attributable to owners of parent warrants investor attention to understand underlying factors. With the full-year forecast maintained, the company’s ability to sustain growth and manage profitability throughout the year will be a key focus for stakeholders.

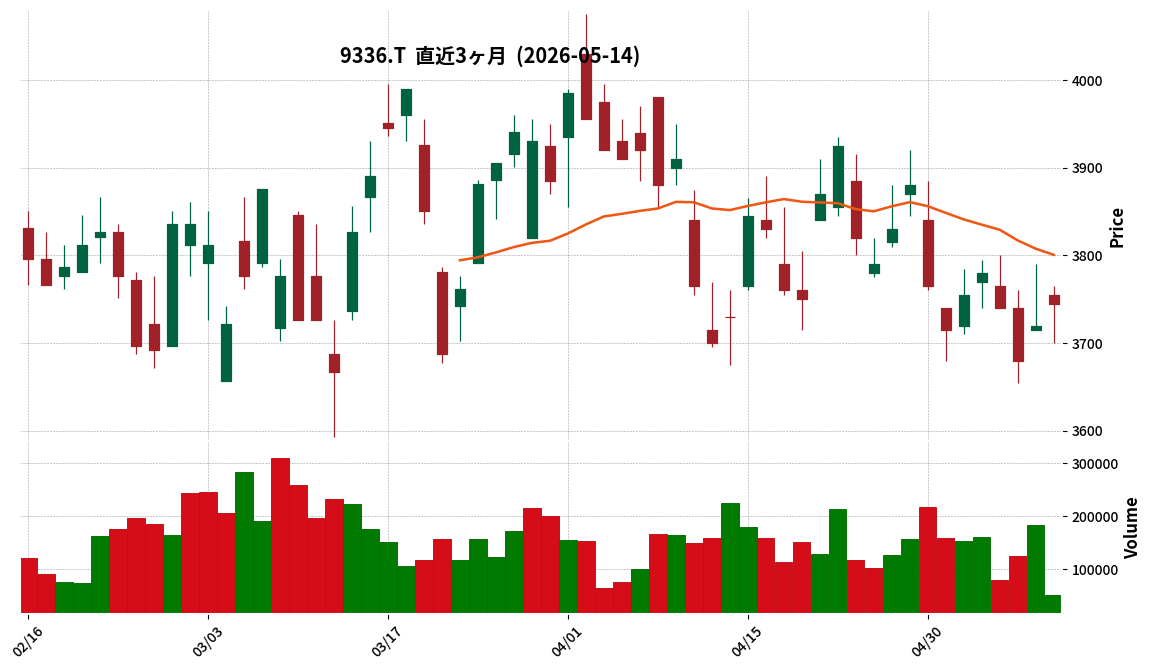

9336|大栄環境

3745.0

▲ +0.67%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Daiei Kankyo reported net sales of ¥87,855 million (up 9.6% year-on-year) and operating profit of ¥22,189 million (up 3.0% year-on-year) for the fiscal year ended March 2026.

- For the fiscal year ending March 2027, the company projects net sales of ¥93,900 million (up 6.9% year-on-year) and operating profit of ¥24,300 million (up 9.5% year-on-year).

- As part of key initiatives, Daiei Kankyo acquired Scarabe Sacre Co., Ltd. and four other companies as consolidated subsidiaries in October 2025, expanding its business area by securing final disposal sites in the Kyushu and Okinawa regions.

- According to the consolidated statement of income for the fiscal year ended March 2026, EBITDA was ¥31,908 million (up 14.7% year-on-year) and profit attributable to owners of parent was ¥15,845 million (up 10.3% year-on-year).

- By business segment, environmental-related business recorded net sales of ¥85,248 million (up 10.0% year-on-year), with the soil remediation business notably growing to ¥7,159 million (up 47.3% year-on-year).

1332|ニッスイ

1207.5

▲ +1.86%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026), Nissui reported consolidated net sales of ¥931,265 million (up 5.1% year-over-year), operating profit of ¥40,430 million (up 27.2%), ordinary profit of ¥43,187 million (up 22.3%), and profit attributable to owners of parent of ¥27,517 million (up 8.4%).

- Net sales, operating profit, ordinary profit, and profit attributable to owners of parent all achieved record highs.

- The annual dividend per share increased from ¥28.00 in FY2025/3 to ¥32.00 in FY2026/3. The forecast for the FY2027/3 annual dividend is ¥32.00.

- Significant changes occurred in the scope of consolidation, with two new companies, PESQUERA YADRAN S.A. and CULTIVOS YADRAN S.A., being added, and one company, Seinan Suisan Co., Ltd., being excluded.

- The consolidated earnings forecast for FY2027/3 projects net sales of ¥980,000 million (up 5.2% year-over-year), operating profit of ¥42,500 million (up 5.1%), ordinary profit of ¥43,000 million (down 0.4%), and profit attributable to owners of parent of ¥29,000 million (up 5.4%).

🤖 AI Perspective

Nissui’s achievement of record-high performance in FY2026/3, coupled with an increased annual dividend, may suggest a strong commitment to shareholder returns. The additions to and removals from the scope of consolidation, along with the forecasted increase in sales and most profit metrics for FY2027/3, could indicate continued strategic growth in its business operations. Further analysis of segment-specific performance would be worthwhile for investors to evaluate the company’s future direction.

2170|LINK&M

529.0

▼ -3.29%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- LINK & M (2170) announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026, to March 31, 2026).

- Consolidated revenue reached ¥10,688 million, marking a 14.1% increase compared to the same period of the previous year.

- Consolidated operating profit was ¥1,489 million, an increase of 21.9% year-on-year.

- Profit attributable to owners of the parent for the quarter amounted to ¥867 million, up 16.2% from the prior year.

- In the Organization Development Division, revenue was ¥4,287 million (up 118.7% YoY) and segment profit was ¥2,954 million (up 120.2% YoY). The Consulting and Cloud Services business specifically reported revenue of ¥3,411 million (up 111.2% YoY) and gross profit of ¥2,491 million (up 111.5% YoY), with a significant year-on-year increase in monthly subscription revenue for “Motivation Cloud.”

🤖 AI Perspective

LINK & M’s Q1 FY2026 results demonstrate significant year-on-year growth across revenue and all profit stages, aligning with expectations. The strong performance appears to be driven by its focus on consulting and cloud services, with “Motivation Cloud” serving as a key growth driver. This trend could indicate increasing demand for the company’s services amidst a growing emphasis on human capital management, making future business developments worth monitoring.

2750|石光商事

1237.0

▲ +1.81%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Ishimitsu Shoji Co., Ltd. announced its consolidated financial results for the fiscal year ended March 31, 2026.

- Net sales for the period amounted to ¥76,527 million, marking a 17.8% increase compared to the previous fiscal year.

- Operating profit reached ¥2,707 million (up 73.8% year-on-year), and ordinary profit was ¥2,161 million (up 61.7% year-on-year).

- Net profit attributable to parent company increased by 42.8% to ¥1,267 million.

- Earnings per share were ¥163.18.

- The company plans to implement annual dividends twice a year (interim and year-end) starting from the fiscal year ending March 31, 2027. The forecast for the FY2027/3 annual dividend is ¥55 (interim ¥20, year-end ¥35, including a ¥5 commemorative dividend).

🤖 AI Perspective

Ishimitsu Shoji’s FY2026/3 results show significant growth across all key financial metrics, with operating profit increasing by over 70%. This strong performance may suggest positive initial outcomes from their new mid-term management plan, “SHINE2027,” which focuses on growth investments and internal system strengthening. The initiation of an interim dividend and an increased annual dividend forecast for FY2027/3 could indicate a more robust shareholder return policy, which may be worth monitoring for investors.

2764|ひらまつ

150.0

▼ -0.66%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 2026, consolidated net sales were ¥9.881 billion, a 7.3% decrease from the previous fiscal year.

- Operating profit was ¥200 million (down 19.7% YoY), ordinary profit was ¥204 million (up 17.3% YoY), and profit attributable to owners of parent was ¥219 million (down 85.6% YoY).

- Total assets stood at ¥11.914 billion, net assets at ¥6.116 billion, and the equity ratio increased to 51.2% from 48.4% in the prior period.

- For the fiscal year ending March 2027 (forecast), the company projects consolidated net sales of ¥10.591 billion (up 7.2% YoY) and profit attributable to owners of parent of ¥288 million (up 31.1% YoY).

- A year-end dividend of ¥1.22 per share is planned for FY2027/3 (forecast), which would be the total annual dividend.

🤖 AI Perspective

Hiramatsu’s FY2026/3 results show a decline in revenue and net profit, which the company attributes to accounting treatment following the transfer of hotel assets. However, an improved equity ratio suggests enhanced financial stability, which may be a point of interest for investors. The positive forecast for FY2027/3 indicates anticipated recovery in business activities and profit improvement efforts, which could be worth monitoring.

343A|IACEトラベル

1185.0

▼ -1.25%

📎 Source:IACEトラベル Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- IACE Travel reported consolidated results for the fiscal year ended March 2026: Revenue of ¥3,015 million (up 11.9% YoY), Operating Profit of ¥754 million (up 24.2% YoY), Ordinary Profit of ¥755 million (up 28.6% YoY), and Net Profit attributable to owners of parent of ¥529 million (up 34.2% YoY).

- Diluted EPS for FY2026 was ¥111.39, with adjusted diluted EPS at ¥111.09.

- Total assets reached ¥5,774 million (up ¥884 million from previous fiscal year-end), net assets ¥4,290 million (up ¥1,436 million), and the equity ratio stood at 74.3%.

- A year-end dividend of ¥30.00 per share (total annual dividend also ¥30.00) is planned for FY2026.

- The consolidated forecast for the full fiscal year ending March 2027 projects Revenue of ¥3,375 million (up 11.9% YoY), Operating Profit of ¥900 million (up 19.3% YoY), Ordinary Profit of ¥900 million (up 19.2% YoY), Net Profit attributable to owners of parent of ¥600 million (up 13.3% YoY), and EPS of ¥125.85.

🤖 AI Perspective

IACE Travel’s FY2026 results indicate a strong performance, with double-digit growth across revenue and all profit metrics, notably a more than 30% increase in net profit. The company’s forecast for continued revenue and profit growth in FY2027 suggests an anticipation of sustained favorable business conditions. These figures may suggest a positive trend in the company’s operational efficiency and market demand for its services.

3774|IIJ

2891.5

▼ -3.87%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Internet Initiative Japan Inc. (IIJ) announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- Revenue totaled ¥345,395 million (up 9.0% year-on-year), operating profit was ¥34,835 million (up 15.7% year-on-year), and profit attributable to owners of the parent was ¥24,188 million (up 21.3% year-on-year).

- Basic earnings per share were ¥136.51, compared to ¥112.68 in the previous fiscal year.

- The annual dividend for the fiscal year ended March 31, 2026, was ¥39.00 per share (¥19.50 interim, ¥19.50 year-end), an increase from ¥35.00 in the previous fiscal year.

- For the fiscal year ending March 31, 2027 (April 1, 2026 – March 31, 2027), the company forecasts consolidated revenue of ¥385,000 million (up 11.5% year-on-year), operating profit of ¥38,500 million (up 10.5% year-on-year), and profit attributable to owners of the parent of ¥25,000 million (up 3.4% year-on-year). The projected annual dividend is ¥43.00 per share (¥21.50 interim, ¥21.50 year-end).

3853|アステリア

1434.0

▼ -0.97%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Asteria Corporation announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- Revenue reached ¥3,389 million, marking a 6.9% increase compared to the previous fiscal year.

- Profit attributable to owners of the parent company stood at ¥799 million, a 35.7% increase year-on-year.

- Operating profit was ¥1,025 million (up 31.2% year-on-year), and profit before tax was ¥974 million (up 27.2% year-on-year).

- The Investment Business segment recorded valuation gains, primarily from SpaceX.

- For the fiscal year ending March 31, 2027, consolidated performance forecasts include revenue of ¥3,700 million (up 9.2% year-on-year) and operating profit of ¥1,100 million (up 7.3% year-on-year).

- The year-end dividend for the fiscal year ended March 31, 2026, is ¥9.00, and for the fiscal year ending March 31, 2027 (forecast), it is ¥10.00.

🤖 AI Perspective

Asteria’s FY2026/3 results highlight stable revenue growth, significantly boosted by valuation gains from SpaceX in the Investment Business segment. The software business’s subscription sales drove revenue expansion, suggesting a solid recurring revenue base. The company forecasts continued growth in both revenue and profit for the next fiscal year, which may indicate management’s confidence in its ongoing strategies and market position.

4838|SSSK HD

715.0

▲ +0.14%

📎 Source:SSSK HD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SSSK HD resolved to revise its year-end dividend forecast (increase) for the fiscal year ending March 2026 at a board meeting held on May 14, 2026.

- The revised year-end dividend forecast per share is ¥25.00.

- The previous year-end dividend forecast per share, announced on February 13, 2026, was ¥24.00.

- The reason for the revision is attributed to achieving better-than-expected performance for the fiscal year ending March 2026 and a comprehensive consideration of financial conditions.

- This dividend forecast is conditional upon approval at the 32nd Ordinary General Meeting of Shareholders scheduled for June 25, 2026.

🤖 AI Perspective

This dividend increase suggests that SSSK HD has experienced stronger financial performance than initially anticipated for the fiscal year ending March 2026. For investors, this could indicate a positive trend in the company’s operational results and a commitment to shareholder returns. The company’s future performance and dividend policy may warrant continued monitoring.

4896|G-ケイファーマ

752.0

▲ +2.45%

📎 Source:G-ケイファーマ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-ケイファーマ announced its Q1 FY2026 financial results (January 1, 2026 – March 31, 2026).

- For the first quarter, the company reported no net sales. Operating loss was ¥237 million, ordinary loss ¥242 million, and net loss attributable to owners of parent was ¥250 million.

- Compared to the previous year’s corresponding quarter, operating loss, ordinary loss, and net loss all widened.

- In terms of financial position, total assets stood at ¥2,821 million (down ¥117 million from end of previous fiscal year), net assets at ¥1,015 million (down ¥249 million), and the equity ratio was 36.0% (down from 43.1% at previous fiscal year-end).

- Development pipelines include preparations for a confirmatory clinical trial (Phase III) for ALS in Japan and the receipt of a patent allowance notice from the U.S. Patent and Trademark Office. In regenerative medicine, a basic agreement for manufacturing consignment for subacute spinal cord injury and an extension of a joint research agreement for chronic cerebral infarction were reported.

5139|G-オープンワーク

925.0

▲ +2.55%

📎 Source:G-オープンワーク Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-OpenWork announced its financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026, to March 31, 2026).

- Operating revenue reached ¥1,376.55 million, representing a 31.5% increase compared to the same period in the previous year.

- Operating profit was ¥504.90 million (up 55.4% year-on-year), ordinary profit was ¥511.70 million (up 56.6% year-on-year), and quarterly net profit was ¥352.06 million (up 57.8% year-on-year).

- The “OpenWork Recruiting” service contributed ¥995.52 million in operating revenue, marking a 43.5% increase year-on-year, and was the primary driver of overall revenue growth.

- The full-year earnings forecast for the fiscal year ending December 2026 and the dividend forecast (interim ¥4.50, year-end ¥4.50, total ¥9.00) remain unchanged.

- Following the resolution of the Board of Directors on March 17, 2026, the company plans to transition to consolidated financial statements from the second quarter of FY2026 due to the complete acquisition of BNG Partners Inc.

🤖 AI Perspective

G-OpenWork’s Q1 performance demonstrates robust growth, largely driven by its “OpenWork Recruiting” service, which significantly contributed to both increased revenue and profit. The strong increase in registered web resumes appears to have fueled recruitment activities by companies and applications from job seekers. The upcoming transition to consolidated financial statements from Q2, incorporating the acquired BNG Partners, will be a key area for investors to monitor regarding potential shifts in business structure and future performance.

519A|G-ベーシック

511.0

▼ -7.09%

📎 Source:G-ベーシック Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Basic released a summary of Q&A regarding its Q1 FY2026 financial results on May 14, 2026.

- The company addressed the slowdown in ARR growth, stating it is due to an ongoing review of target customers, which has led to allowing some customer cancellations.

- G-Basic announced a strategic shift to focus management resources on customers who prioritize safety, security, and reliable operations, aiming to drive upsells and cross-sells.

- Regarding new products, the company reported multiple inquiries for ferret SFA/CRM, over 100 business negotiations at the pre-sales stage for workrun, and greater-than-expected interest for the beta version of askrun.

- The decline in the run business’s churn rate was attributed to an increasing number of customers subscribing to higher-tier plans, which exhibit a churn rate in the low 1% range.

🤖 AI Perspective

G-Basic’s candid explanation for the ARR growth deceleration, coupled with a defined strategic pivot towards large enterprises and enhanced upsell/cross-sell initiatives, may be a focal point for investors. The company’s emphasis on leveraging AI-driven development for cost competitiveness and targeting replacement demand from foreign SaaS products could indicate a shift in its future revenue streams. Additionally, the positive initial feedback on new products suggests potential future growth drivers for the business.

7075|G-QLS

793.0

▲ +0.63%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 2026, consolidated net sales were ¥12,024 million, a 14.0% increase year-over-year.

- Operating profit reached ¥880 million, marking a 44.1% increase compared to the previous year.

- Ordinary profit was ¥904 million, up 51.4% year-over-year.

- Net income attributable to owners of parent increased by 37.1% year-over-year, totaling ¥510 million.

- By segment, childcare business sales were ¥6,671 million (+12.4%), nursing care and welfare business sales were ¥3,020 million (+16.0%), and temporary staffing business sales were ¥1,948 million (+19.1%), all achieving increased sales and profits.

- The year-end dividend for the fiscal year ended March 2026 is ¥10 per share, and the forecast for the full fiscal year ending March 2027 is ¥11 per share.

🤖 AI Perspective

G-QLS’s FY2026 results demonstrate robust growth across all segments, with significant increases in sales and all profit metrics. This performance appears to be driven by new childcare facility openings, M&A in the nursing care and welfare sector, and sustained demand in the temporary staffing business coupled with successful coordinator recruitment. The projected dividend increase for the next fiscal year may suggest the company’s confidence in its continued business trajectory.

7805|プリントネット

754.0

▼ -0.26%

📎 Source:プリントネット Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Printnet Co., Ltd. announced a correction to a portion of its “Q1 FY2026 Financial Results (Japanese GAAP) (Non-consolidated)” on May 14, 2026.

- The correction pertains to the content disclosed on January 14, 2026, within the same financial results report.

- The reason for the correction is an error in the wording in the “Independent Auditor’s Interim Review Report on Quarterly Financial Statements.”

- Specifically, the phrase “the first quarter accounting period and the first quarter cumulative period of the previous fiscal year ended November 30, 2024” was corrected to “the first quarter accounting period and the first quarter cumulative period of the previous fiscal year ended August 31, 2025.”

- The corrected statement maintains that the financial statements for the previous fiscal year ended August 31, 2025, were audited by the previous auditor, who issued an unqualified opinion on November 26, 2025.

🤖 AI Perspective

This correction addresses a clerical error in the independent auditor’s report regarding the description of a past accounting period, rather than a change in the financial figures themselves. For investors, this may indicate the company’s commitment to ensuring the accuracy of its disclosed information. Such administrative corrections are generally not expected to have a direct impact on the company’s performance or financial health.

8089|ナイス

1944.0

▲ +0.67%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- NICE Co., Ltd. announced its consolidated financial results for the fiscal year ended March 31, 2026.

- Consolidated net sales were ¥259,154 million (up 6.6% year-on-year), operating profit was ¥5,322 million (up 15.0%), and ordinary profit was ¥5,162 million (up 19.9%).

- Net profit attributable to owners of the parent decreased by 9.9% to ¥2,586 million.

- Earnings per share (EPS) were ¥218.21, compared to ¥242.53 in the previous fiscal year.

- The annual dividend per share was ¥72.00 (interim ¥28.00, year-end ¥44.00), an increase from ¥65.00 in the previous fiscal year.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥270,000 million (up 4.2%), operating profit of ¥5,700 million (up 7.1%), and net profit attributable to owners of the parent of ¥3,200 million (up 23.7%).

- One company, Arai Shoji Building Management Co., Ltd., was newly consolidated, and Smart Power Co., Ltd. was excluded from consolidation during the period.

🤖 AI Perspective

The reported results indicate growth in consolidated net sales and operating profit, contrasting with a decline in net profit attributable to owners of the parent. The increase in the annual dividend may suggest a commitment to shareholder returns. The company’s forecast for the next fiscal year projects increases across sales, operating profit, and net profit, potentially indicating an optimistic outlook for future business performance.

9564|FCE

461.0

▼ -4.55%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- FCE’s consolidated results for the second quarter of the fiscal year ending September 2026 show net sales of ¥3,434 million (up 14.0% year-on-year), operating profit of ¥742 million (up 14.4%), ordinary profit of ¥763 million (up 14.5%), and net income attributable to owners of the parent of ¥539 million (up 18.3%).

- By segment, the DX Promotion Business recorded net sales of ¥2,027 million (up 25.3% year-on-year) and segment profit of ¥505 million (up 12.8%). The flagship “Robo-Pat AI” saw its number of client companies reach 2,055 as of March 31, 2026 (up 26.2% year-on-year).

- The Education and Training Business reported net sales of ¥1,407 million (down 0.9% year-on-year) and segment profit of ¥238 million (up 24.7%).

- The full-year consolidated earnings forecast remains unchanged from the most recently announced figures: net sales of ¥6,800 million (up 11.5% from previous year), operating profit of ¥1,130 million (up 23.9%), ordinary profit of ¥1,160 million (up 25.4%), and net income attributable to owners of the parent of ¥865 million (up 30.5%).

- The forecast for annual dividends is ¥10.00 per share for the fiscal year-end, totaling ¥10.00. There are no revisions to the most recently announced dividend forecast.

🤖 AI Perspective

FCE’s Q2 FY2026 results indicate solid growth in both revenue and profit, primarily driven by its DX Promotion Business. The increase in client companies for “Robo-Pat AI” suggests a successful capture of market demand for digital transformation. While selling, general, and administrative expenses in the DX Promotion Business have risen due to new business investments, this may reflect strategic forward-looking investments for future growth that could be worth monitoring.

1921|巴

1882.0

▼ -1.83%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tomoe Corporation announced its consolidated financial results for the fiscal year ended March 31, 2025.

- Consolidated net sales increased by 0.8% year-on-year to ¥34,951 million, and consolidated operating profit increased by 21.0% year-on-year to ¥4,759 million.

- Consolidated ordinary profit increased by 16.2% year-on-year to ¥5,481 million, but profit attributable to owners of parent decreased by 58.1% year-on-year to ¥6,227 million.

- Earnings per share (EPS) for the period were ¥170.06.

- A year-end dividend of ¥36.00 per share (ordinary dividend ¥24.00, special dividend ¥12.00) was paid for FY2025, with total dividends amounting to ¥1,208 million.

- For the fiscal year ending March 31, 2026, the company forecasts consolidated net sales of ¥32,000 million (down 8.4% year-on-year), operating profit of ¥2,800 million (down 41.2% year-on-year), and profit attributable to owners of parent of ¥2,600 million (down 58.2% year-on-year).

🤖 AI Perspective

Tomoe Corporation’s FY2025 results show an increase in net sales and operating profit, but a significant decline in profit attributable to owners of parent. This substantial decrease in net profit compared to the previous year may suggest the presence of extraordinary income in the prior period. The forecast for FY2026 indicates a projected decrease in both revenue and profit, which could signal a challenging business environment or a strategic re-evaluation.

2117|ウェルネオシュガー

2653.0

▼ -0.04%

📎 Source:ウェルネオシュガー Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Wellneo Sugar Co., Ltd. reported consolidated revenue of ¥112,904 million for the fiscal year ended March 31, 2026, marking a 16.3% increase from the previous fiscal year.

- Consolidated operating profit for the same period was ¥10,324 million (up 25.8% year-on-year), and profit attributable to owners of the parent was ¥6,472 million (up 12.6% year-on-year).

- The annual dividend for the fiscal year ended March 31, 2026, was announced at ¥119 per share (interim dividend of ¥54, year-end dividend of ¥65), an increase from ¥102 in the previous fiscal year.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated revenue of ¥110,000 million (down 2.6% year-on-year), operating profit of ¥9,200 million (down 10.9% year-on-year), and profit attributable to owners of the parent of ¥6,500 million (up 0.4% year-on-year).

- During the fiscal year ended March 31, 2026, Daiichi Sugar Co., Ltd. was excluded from the scope of consolidation due to its absorption merger with the company, effective October 1, 2025.

🤖 AI Perspective

Wellneo Sugar’s FY2026 results indicate a robust performance with significant double-digit growth in revenue, operating profit, and profit attributable to owners of the parent. The increase in the annual dividend may suggest a positive outlook on shareholder returns. However, the forecast for FY2027 projecting a decline in revenue and operating profit, along with the impact of changes in the scope of consolidation due to the corporate merger, are factors worth monitoring for future performance evaluation.

2974|大英産業

—

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Daiei Sangyo announced its consolidated financial results for the second quarter (interim period) of the fiscal year ending September 2026.

- Consolidated results show net sales of ¥13,087 million (down 7.6% year-on-year), an operating loss of ¥291 million (compared to a loss of ¥146 million in the prior interim period), an ordinary loss of ¥504 million (compared to a loss of ¥335 million), and a net loss attributable to parent company shareholders of ¥426 million (compared to a loss of ¥230 million).

- By segment, the condominium business reported net sales of ¥5,288 million (down 13.9% year-on-year) and segment profit of ¥8 million (down 95.6% year-on-year). The housing business reported net sales of ¥7,718 million (down 3.3% year-on-year) and segment profit of ¥206 million (up 10.0% year-on-year).

- In the condominium business, the number of delivered condominium units increased year-on-year, but net sales decreased due to the absence of large-scale corporate property sales recorded in the prior year and a higher proportion of deliveries for the “Sunrelius” compact condominium series.

- In the housing business, while deliveries of business properties and contracted construction for specific buildings increased, deliveries of detached houses, redeveloped pre-owned homes, and investment-purpose detached rental homes decreased. However, segment profit increased due to intensified sales promotion for long-term inventory properties, strengthened product competitiveness, and rigorous selection of highly profitable acquisition properties.

🤖 AI Perspective

Daiei Sangyo’s Q2 FY2026 results show a decline in net sales and a widening of losses across all profit stages compared to the previous year. This appears to be primarily driven by the timing of sales recognition for large-scale properties and changes in the product mix within the condominium business. Conversely, despite a decrease in sales, the housing business achieved an increase in segment profit, suggesting that profitability improvement initiatives are taking effect in this area. With the full-year forecast unchanged, the progress of sales for properties scheduled for delivery in the latter half of the year will be a key factor for investors to monitor.

4337|ぴあ

3420.0

▼ -2.29%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Pia Corporation announced discrepancies between its full-year consolidated performance forecast and actual results for the fiscal year ending March 2026, along with a revision to its dividend forecast (increase).

- For the fiscal year ended March 2026, consolidated net sales were JPY 55,330 million, exceeding the previous forecast of JPY 50,000 million (an increase of 10.7%).

- Operating profit was JPY 4,311 million (up 2.6%), ordinary profit was JPY 4,345 million (up 3.5%), and profit attributable to owners of parent was JPY 3,317 million (up 22.9%) compared to previous forecasts of JPY 4,200 million, JPY 4,200 million, and JPY 2,700 million, respectively.

- Basic earnings per share were JPY 216.37, up from the previous forecast of JPY 176.20.

- The year-end dividend forecast was revised from JPY 20 per share to JPY 35 per share, making the total annual dividend JPY 35. This amount represents the highest dividend per share since the company’s listing.

- The company attributed the higher-than-expected performance to strong ticket sales, which progressed smoothly above the previous forecast, driven by the buoyant domestic leisure and entertainment market.

🤖 AI Perspective

The announcement reveals that Pia Corporation’s performance for the fiscal year ended March 2026 surpassed previous forecasts across all metrics, with a notable increase of over 20% in profit attributable to owners of parent. This outcome suggests that the recovery in the domestic leisure and entertainment market has directly benefited Pia’s ticket sales business. Furthermore, the upward revision of the year-end dividend to an all-time high, concurrent with the improved performance, may be viewed as a positive indication of the company’s commitment to shareholder returns.

4401|ADEKA

4228.0

▲ +2.30%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- ADEKA Co. has decided to increase its year-end dividend for the fiscal year ending March 2026.

- The year-end dividend per share will be ¥60, an increase of ¥8 from the initial forecast of ¥52 (announced on May 14, 2025).

- This revision brings the total annual dividend for the fiscal year ending March 2026 to ¥112 per share, including the interim dividend of ¥52 (compared to ¥100 for the prior year).

- The consolidated dividend payout ratio is projected to be 40.3%.

- This dividend proposal is subject to approval at the 164th Ordinary General Meeting of Shareholders scheduled for June 19, 2026.

🤖 AI Perspective

ADEKA has stated its commitment to a dividend payout ratio of 40% or more as a key objective in its mid-term management plan, “ADX 2026,” launched in April 2024. This dividend increase aligns with that shareholder return policy. The upward revision from the initial forecast may suggest the company’s confidence in its current fiscal year performance and financial position. Consistent execution of dividend policies could be a notable point for long-term investors.

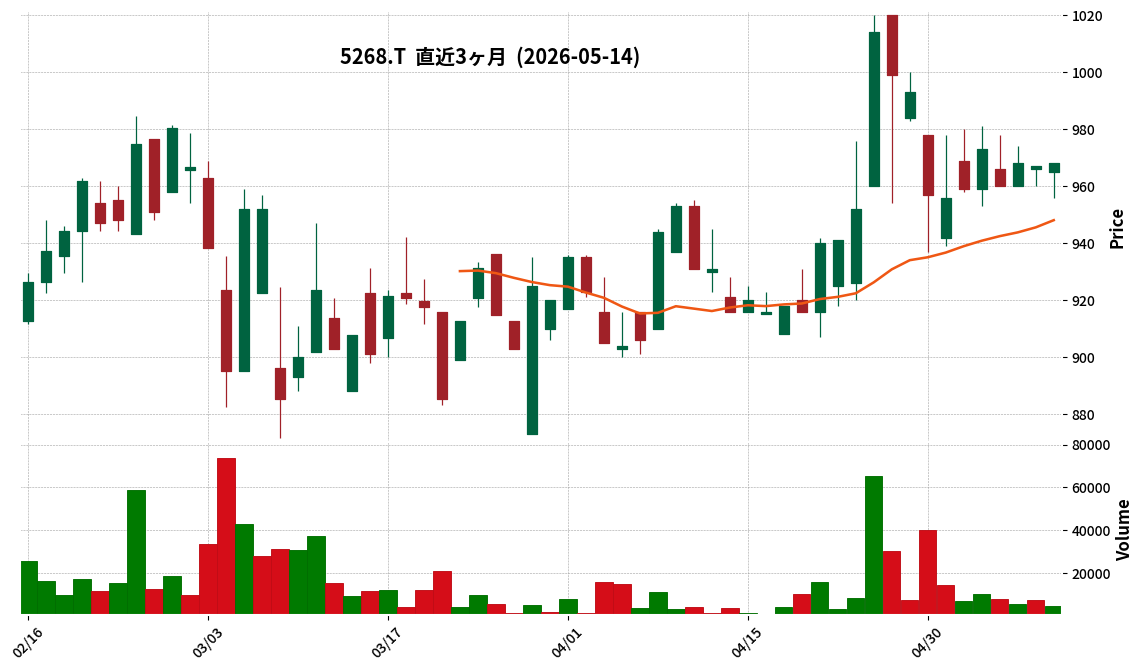

5268|旭コンクリ

968.0

▲ +0.10%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Asahi Concrete Co., Ltd. announced its non-consolidated financial results for the fiscal year ended March 2026 (April 1, 2025 – March 31, 2026).

- Net sales for the period amounted to ¥7.63 billion, representing a 5.7% increase compared to the previous fiscal year.

- Operating profit reached ¥609 million, marking a 9.8% increase year-on-year.

- Ordinary profit was ¥676 million (up 10.7% YoY), and net profit was ¥455 million (up 10.6% YoY).

- Earnings per share were ¥34.57, and net assets per share were ¥965.17.

- The company plans a year-end dividend of ¥17 per share for FY2026 (¥14 ordinary dividend, ¥3 special dividend).

- For the fiscal year ending March 2027 (forecast), the company projects full-year net sales of ¥7.80 billion (up 2.1% YoY), operating profit of ¥620 million (up 1.8% YoY), and net profit of ¥470 million (up 3.3% YoY).

🤖 AI Perspective

Asahi Concrete’s FY2026 results indicate stable performance with increases across sales and all profit metrics. A notable point is the significant 18.3% increase in sales within the “Other departments” of the Concrete-related business, which may suggest a shift in sales composition or strong growth in specific areas. The company’s commitment to maintaining a dividend of ¥17 per share, including a special dividend, could be viewed positively by investors seeking consistent shareholder returns.

5975|東プレ

2475.0

▲ +1.73%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Topre Corporation has resolved to pay a year-end dividend of ¥60.00 per share for the fiscal year ending March 31, 2026.

- This represents an increase of ¥20.00 per share from the most recent dividend forecast of ¥40.00 per share announced on February 13, 2026.

- The previous fiscal year’s (March 2025) year-end dividend was ¥50.00 per share (including ¥40.00 ordinary dividend and ¥10.00 commemorative dividend).

- The total annual dividend for the current fiscal year will be ¥100.00 per share, combining the interim dividend of ¥40.00 per share already paid.

- The annual dividend for the previous fiscal year was ¥85.00 per share.

- The source of the dividend is retained earnings, and the effective date is June 25, 2026.

🤖 AI Perspective