📌 Today’s Highlights

Today we cover 27 IR announcements. Notable among them: G-バトンズ (554A), G-メディア (3815), 不動テトラ (1813). Use the table of contents below to navigate to each company.

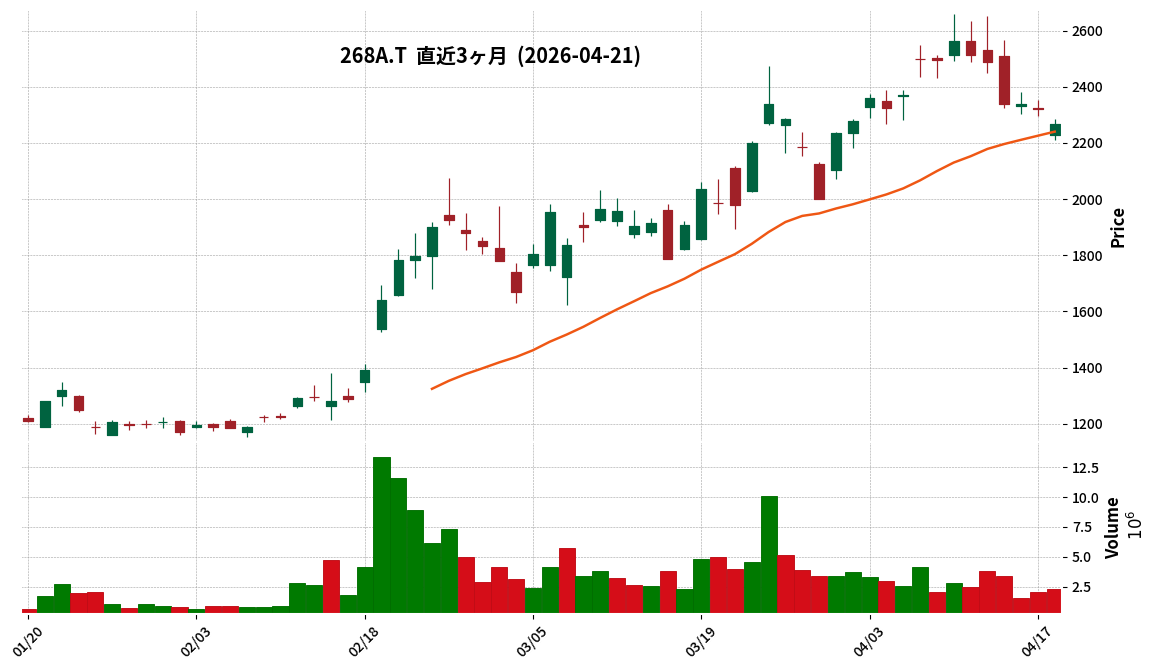

268A|リガク

2266.0

▼ -2.37%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Rigaku Holdings Corporation resolved to conclude a capital and business alliance agreement with Onto Innovation Inc. on April 20, 2026.

- As part of the alliance, Atom Investment, L.P. will transfer 61,123,436 shares of Rigaku stock, representing 27.0% of Rigaku’s total outstanding shares (excluding treasury stock), to Onto Innovation Inc. This transfer is scheduled for the second half of 2026.

- The business alliance will expand collaboration from existing hybrid measurement solution co-development to include R&D, market deployment, manufacturing, and supply chain domains, accelerating solutions for next-generation semiconductors (AI, advanced logic, advanced memory, advanced packaging).

- Onto Innovation Inc. has agreed to respect Rigaku’s management autonomy and independence, and to implement restrictions on the transfer and additional acquisition of Rigaku shares for a certain period post-transfer.

- Onto Innovation Inc. holds the right to nominate one non-executive director candidate to Rigaku, provided its shareholding does not fall below 50% of the acquired shares, with Michael Plisinski (Onto Innovation CEO) expected to be nominated.

🤖 AI Perspective

This alliance appears to strengthen the complementary relationship between Rigaku’s X-ray analysis technology and Onto Innovation’s measurement and analysis technologies in the semiconductor process control sector, aiming to enhance competitiveness in the next-generation semiconductor market. The capital tie-up involving a change in the major shareholder could solidify the collaboration between the two companies, potentially fostering significant business synergies. The agreement for Onto Innovation to respect Rigaku’s management autonomy while having the right to nominate a director suggests a balanced approach to strategic alignment and independence.

554A|G-バトンズ

—

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-BATONZ, Inc. listed on the Tokyo Stock Exchange Growth market today, April 21, 2026.

- For the fiscal year ending March 2026 (forecast), the company anticipates net sales of ¥2,010 million (up 45.8% year-on-year), operating profit of ¥344 million (up 574.5% YoY), ordinary profit of ¥346 million (up 507.0% YoY), and net income of ¥242 million (up 490.2% YoY).

- Segment-wise sales forecasts for FY2026/3 include M&A Platform business at ¥1,516 million (up 53.1% YoY) and M&A SaaS business at ¥437 million (up 20.5% YoY).

- For the nine months ended December 31, 2025 (third quarter), actual results were net sales of ¥1,371 million, operating profit of ¥187 million, and net income of ¥122 million.

- The company does not prepare consolidated financial statements or quarterly consolidated financial statements. Per-share net income is calculated assuming a stock split (100 shares for 1 share effective January 8, 2026) was conducted at the beginning of the fiscal year.

🤖 AI Perspective

The FY2026/3 performance forecast, released concurrently with the listing, highlights significant expected growth across key profit metrics. Given that sales in the M&A Platform business and “Other” segments tend to be concentrated towards the fiscal year-end, evaluating full-year targets based solely on Q3 progress may warrant consideration of these business characteristics. Furthermore, the fact that the performance forecast is based on actual results up to December 2025 could be perceived as providing a degree of objectivity to the information.

3815|G-メディア

447.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-MEDIA (Media Kobo, Inc.) announced its consolidated financial results for the first half of the fiscal year ending August 2026 (September 1, 2025 – February 29, 2026). Net sales were ¥828 million (down 13.5% year-on-year), and the operating loss expanded to ¥309 million (a deterioration of ¥236 million from ¥72 million loss in the prior year period). Net loss attributable to owners of parent was ¥268 million (a deterioration of ¥198 million from ¥69 million loss in the prior year period).

- The primary reason for the sales decline was the sluggish performance of core digital content and LINE chat fortune-telling services. Factors cited include delays in the operational launch of a new content production platform and the emergence of AI fortune-telling by individual app developers as an alternative service, leading to a decrease in consultation requests.

- The expansion of operating loss is attributed to the impact of declining revenue from existing businesses, increased personnel and outsourcing costs for new business promotion, ¥62 million in shareholder benefit expenses, and office relocation costs.

- By segment, the fortune-telling business reported sales of ¥769 million (down 14.6% YoY) and operating profit of ¥118 million (down 39.2% YoY), showing both decreased revenue and profit. In contrast, the data & technology business saw sales increase to ¥53 million (up 12.0% YoY) but its operating loss expanded to ¥115 million.

- The company recognizes the necessity for structural reform and plans to invest management resources into physical domains and human values (e.g., phone calls, face-to-face interactions, real events, emotional connections) that are less susceptible to AI replacement, while integrating AI technology. New business initiatives include BtoC physical services, BtoB cross-industry collaborations, IP businesses, and data marketing.

🤖 AI Perspective

G-MEDIA’s Q2 FY2026 interim results indicate a challenging period, with core business declines and new investments contributing to reduced revenue and expanded losses. This situation may suggest the significant impact of shifts in the digital content market and the rapid adoption of AI technology on established business models. The company’s announced structural reforms, focusing on AI integration and physical services, could be interpreted as a strategic response to evolving market conditions, making their future execution and effectiveness key areas for investors to monitor.

1813|不動テトラ

2989.0

▲ +0.81%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- FUDO TETRA announced on April 21, 2026, revisions to its consolidated earnings forecast and dividend forecast for the fiscal year ending March 31, 2026.

- For the full fiscal year 2026, consolidated net sales are revised upwards from JPY 80.0 billion to JPY 81.5 billion, operating income from JPY 4.9 billion to JPY 5.8 billion, ordinary income from JPY 5.0 billion to JPY 6.0 billion, and net income attributable to owners of parent from JPY 3.45 billion to JPY 4.3 billion.

- The primary reasons for the earnings revision are cited as smooth progress in civil engineering and ground improvement projects, along with improved profit margins from additional change orders in the ground improvement business.

- The year-end dividend forecast has been revised upwards by JPY 25 from the previous forecast of JPY 90 per share, to JPY 115 per share.

- This dividend revision aligns with the company’s profit distribution policy, which targets a dividend payout ratio of approximately 40%, and reflects the updated earnings forecast.

🤖 AI Perspective

The upward revision of earnings suggests robust performance driven by both revenue growth and significant improvements in profit margins, particularly within the ground improvement business. The increased dividend forecast aligns with the company’s stated goal of a 40% payout ratio, indicating a commitment to shareholder returns in line with stronger financial results. Continued strong project progress and improved profitability in core businesses could be a key focus for investors monitoring the company’s future outlook.

4750|ダイサン

576.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Daisan Co., Ltd. resolved on April 21, 2026, to acquire all 200,000 shares (100.0% voting rights) of Penguin Engineering & Construction Pte. Ltd. (Penguin Co.) in Singapore, making it a wholly-owned subsidiary.

- The acquisition price for the shares is 2,000 thousand Singapore Dollars (approximately 249 million Japanese Yen, with estimated total costs including incidental expenses at 255 million Japanese Yen).

- This acquisition is part of Daisan’s “Deepening Core Business Areas” strategy outlined in its “Reborn” mid-term management plan, aiming to enhance the value-added engineering business in overseas markets, specifically Singapore.

- Penguin Co. is a specialized engineering contractor in Singapore, focusing on services such as piping installation for petrochemical plants.

- There will be no impact on Daisan’s consolidated financial results for the fiscal year ending April 2026 from this acquisition. The forecast for the fiscal year ending April 2027 will be disclosed in the financial report scheduled for June 2026.

🤖 AI Perspective

This acquisition appears to be a concrete step by Daisan to execute its mid-term management plan, particularly regarding the enhancement of its overseas business and value-added services. By incorporating a specialized engineering firm in Singapore, the company may aim to strengthen its competitive position through synergies with existing subsidiaries. Investors may find it worthwhile to monitor the detailed impact on consolidated performance, which is expected to be disclosed in the fiscal year 2027 earnings forecast in June 2026.

8622|水戸証

702.0

▼ -0.57%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Mito Securities Co., Ltd. announced on April 21, 2026, its preliminary financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026). The official announcement is scheduled for April 28, 2026.

- For the fiscal year ended March 2026, operating revenue reached ¥16,074 million, representing a 15.0% increase compared to the previous fiscal year’s ¥13,983 million.

- Operating profit stood at ¥3,146 million (up 69.3% YoY), ordinary profit at ¥3,598 million (up 54.5% YoY), and net profit attributable to owners of parent at ¥3,095 million (up 27.9% YoY).

- The primary factors contributing to the revenue increase were attributed to higher stock-related revenue and stock revenue (investment trust agency fees and fund wrap fees).

🤖 AI Perspective

- Mito Securities’ preliminary financial results for the fiscal year ended March 2026 indicate significant year-on-year growth across key profit metrics, with the substantial increase in operating profit being particularly noteworthy.

- The reported rise in stock-related revenue and stock revenue, cited as primary drivers for the overall revenue increase, could reflect specific market conditions or evolving client asset management demands.

- These preliminary figures serve as an initial indicator of the company’s performance trajectory and may be considered by investors when evaluating the full financial results upon their official release.

5845|全保連

983.0

▼ -0.61%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Zempo Hoshou Co., Ltd. announced an upward revision to its full-year earnings forecast for the fiscal year ending March 2026 on April 21, 2026.

- The revised forecast projects net sales of 26,150 million yen (an increase of 0.2% from the previous forecast), operating income of 3,150 million yen (+5.0%), ordinary income of 3,150 million yen (+5.0%), and net profit of 1,680 million yen (+2.4%).

- Net sales, operating income, ordinary income, and net profit are all expected to reach record highs. The net profit forecast includes a 600 million yen special loss for retirement benefits for directors.

- Reasons for the revision include becoming a consolidated subsidiary of Mitsubishi UFJ Financial Group, launching the “Mitsubishi UFJ Card Plan” in collaboration with Mitsubishi UFJ NICOS Co., Ltd., and reducing credit costs through a proprietary AI screening system.

- The company also stated that digitalization and efficiency improvements through IT utilization led to cost reductions exceeding expectations.

🤖 AI Perspective

- This upward revision to the earnings forecast may suggest that the enhanced collaboration with the MUFG Group and the implementation of AI-driven operational efficiencies are strengthening the company’s business foundation and profitability.

- The successful reduction in credit costs and expense control appear to be significant drivers behind the improved profit outlook.

- The company’s consistent revenue and profit growth, alongside initiatives like the introduction of progressive dividends, could be seen as indicators of a strong growth strategy and commitment to shareholder returns.

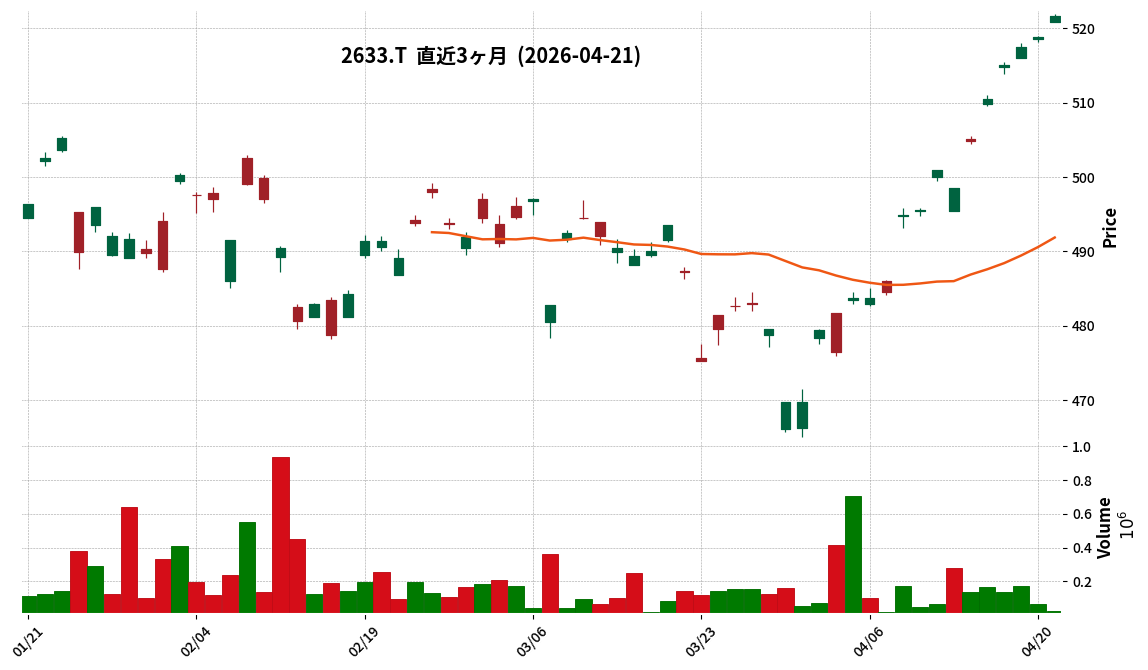

2633|S&P500ヘッジ無

521.7

▲ +0.56%

📎 Source:S&P500ヘッジ無 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- NEXT FUNDS S&P 500 (Unhedged) Exchange Traded Fund (Code: 2633) announced its earnings report for the fiscal year ended March 2026 (September 11, 2025 – March 10, 2026) on April 21, 2026.

- Total net assets as of the end of the current fiscal period (March 10, 2026) amounted to JPY 22,591 million, an increase from JPY 19,992 million at the end of the previous fiscal period (September 10, 2025).

- The Net Asset Value per 100 units for the fiscal year ended March 2026 was JPY 49,334, an increase from JPY 44,239 in the previous period.

- The dividend per 100 units for the fiscal year ended March 2026 was announced as JPY 240, an increase from JPY 220 in the previous period.

- During the current fiscal period, the number of units created was 8,200 thousand units, and units redeemed were 7,600 thousand units, resulting in 45,793 thousand issued units at the period end.

🤖 AI Perspective

The increase in the fund’s total net assets, net asset value per unit, and dividend per unit compared to the previous fiscal period may suggest favorable operational performance. Additionally, the fact that units created exceeded units redeemed could indicate new capital inflows from investors, reflecting growing interest in the fund. These figures serve as objective information for evaluating the fund’s operational status.

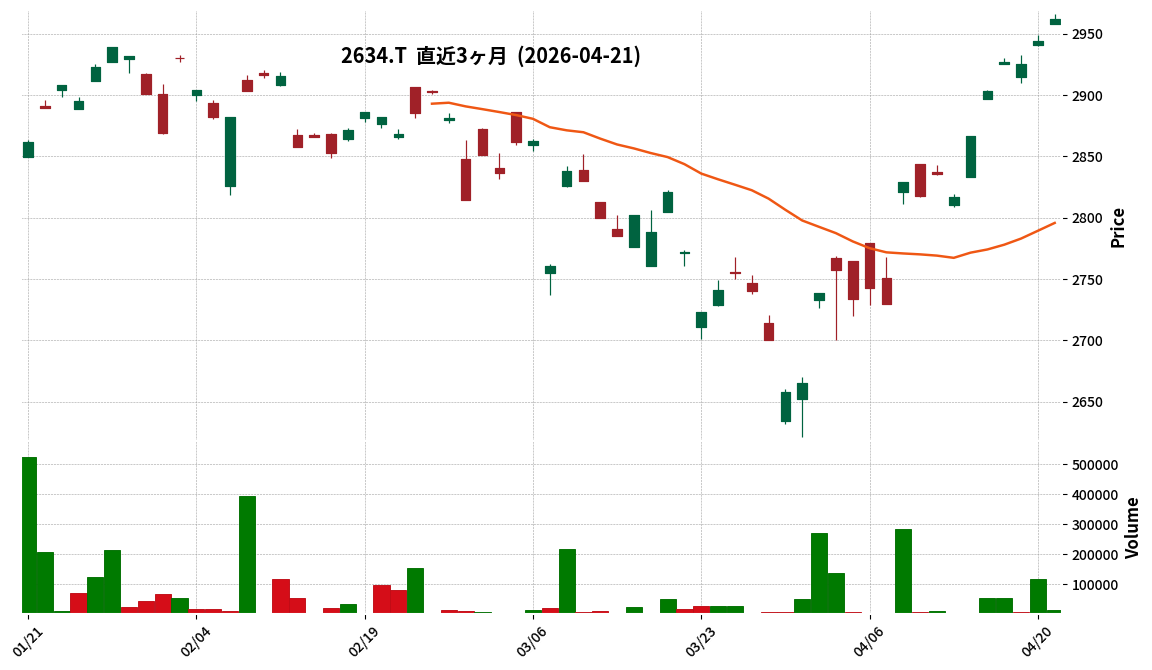

2634|S&P500ヘッジ有

2962.0

▲ +0.61%

📎 Source:S&P500ヘッジ有 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- NEXT FUNDS S&P 500 (Yen-Hedged) Exchange Traded Fund (Code: 2634) released its earnings report for the fiscal year ended March 2026 (September 11, 2025 – March 10, 2026) on April 21, 2026.

- Total net assets as of the end of March 2026 were JPY 32,615 million, representing a decrease from JPY 36,014 million at the end of the previous fiscal period (September 2025).

- The Net Asset Value (NAV) per 100 units at the end of the period was JPY 284,216, an increase compared to JPY 277,129 at the end of the previous fiscal period.

- The dividend per 100 units for the fiscal year ended March 2026 was JPY 1,500, which is a decrease from JPY 1,520 in the previous period.

- During the reporting period, 5,080 thousand units were created, while 6,600 thousand units were redeemed, resulting in 11,475 thousand units issued at the end of the period.

🤖 AI Perspective

While total net assets saw a decrease, the rise in NAV per 100 units suggests a degree of positive performance for the fund during the period. Conversely, the decline in dividends per 100 units and the fact that redemptions exceeded creations in terms of unit volume could be a point of interest for investors monitoring fund flows. These trends may reflect shifts in market conditions or investor sentiment towards the fund.

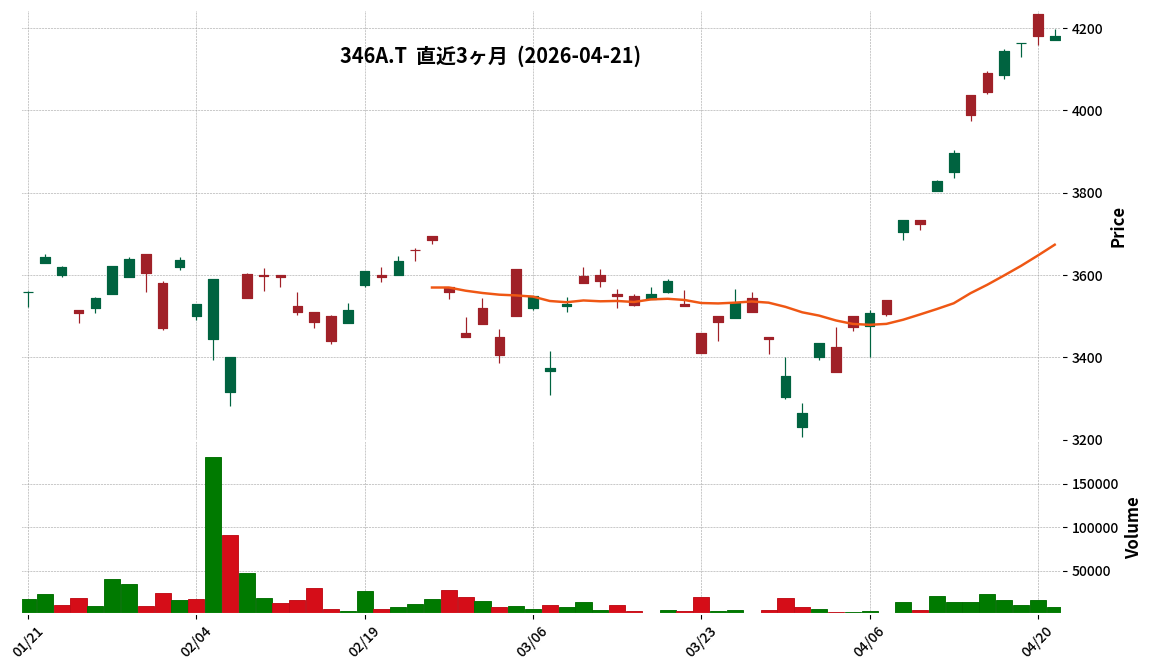

346A|S&P500半導体

4182.0

▲ +0.05%

📎 Source:S&P500半導体 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- NEXT FUNDS S&P 500 Semiconductors & Semiconductor Equipment 35% Capped Index Exchange Traded Fund (346A) announced its semi-annual earnings report for the fiscal year ending September 2026 on April 21, 2026.

- For the half-year ended March 2026 (September 11, 2025 – March 10, 2026), Net Assets amounted to JPY 2,238 million, an increase from JPY 1,077 million at the end of the previous fiscal period (FY ended September 2025).

- The Net Asset Value per 100 units at the end of the period was JPY 355,361, up from JPY 276,340 at the end of the previous fiscal period.

- The number of issued units at the end of the semi-annual period was 630 thousand units, an increase from 390 thousand units at the end of the previous fiscal period.

- Primary invested assets totaled JPY 2,195 million, accounting for 98.1% of Net Assets.

🤖 AI Perspective

This report indicates significant increases in net assets, net asset value per unit, and issued units compared to the previous fiscal period. This trend may reflect strong performance in the underlying S&P 500 Semiconductors & Semiconductor Equipment sector, potentially combined with increased investor interest and capital inflows into the fund. Such developments could suggest growing market confidence in the semiconductor industry and the appeal of this ETF as an investment vehicle.

6888|アクモス

561.0

▼ -0.18%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Ackmos Co., Ltd. has decided to merge with its wholly-owned subsidiary, Systems Service Co., Ltd., through an absorption-type merger, effective October 1, 2026.

- Under this merger, Ackmos will be the surviving company, and Systems Service Co., Ltd. will be dissolved.

- The merger aims to strengthen the revenue base of Systems Service Co., Ltd.’s System Engineering Service (SES) business, expand its customer base, and secure human resources, aligning with Ackmos’s Mid-Term Management Plan 2028 goal of achieving 10 billion yen in group sales by June 2028.

- The merger will not impact the consolidated or non-consolidated financial results for the fiscal year ending June 2026. However, a special loss (loss on cancellation of treasury stock held by a subsidiary) may be recorded in non-consolidated results for the fiscal year ending June 2027, though it will be eliminated in consolidated financial statements and thus have no impact on consolidated earnings forecasts.

- Systems Service Co., Ltd. primarily provides System Engineering Services (SES) focusing on system development for financial institutions, reporting net sales of 716 million yen and net income of 14 million yen for its single fiscal year ended December 2025.

🤖 AI Perspective

This merger appears to be a strategic move to consolidate resources and enhance operational efficiency within the Ackmos Group, aligning with its mid-term growth objectives. Integrating the wholly-owned subsidiary could potentially lead to synergies and a stronger market position in the SES sector. While the possibility of a special loss on non-consolidated results is mentioned, the confirmation that it will not affect consolidated earnings forecasts may be a key point for investors focusing on the group’s overall financial health.

4733|OBC

6607.0

▼ -2.42%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, OBC (Obic Business Consultants Co., Ltd.) reported non-consolidated net sales of ¥51,400 million (up 9.4% year-on-year), operating profit of ¥23,580 million (up 8.4%), ordinary profit of ¥25,218 million (up 9.4%), and net income of ¥18,132 million (up 12.0%), achieving increased revenues and profits.

- Diluted earnings per share for FY2026 stood at ¥241.20.

- The annual dividend for FY2026 was ¥111.00 per share, an increase of ¥11.00 from the previous year, with a payout ratio of 46.0%.

- For the fiscal year ending March 31, 2027, the company forecasts net sales of ¥57,500 million (up 11.9% year-on-year), operating profit of ¥26,500 million (up 12.4%), and net income of ¥19,350 million (up 6.7%).

- The projected annual dividend for FY2027 is ¥130.00 per share, with an expected payout ratio of 50.5%.

🤖 AI Perspective

OBC demonstrated solid growth across revenue and profit metrics in its FY2026 results, indicating robust business performance. The projected continued growth in FY2027, coupled with a significant increase in the forecasted annual dividend, could be viewed positively by investors. These factors suggest a company with ongoing operational strength and a commitment to shareholder returns.

7419|ノジマ

1259.0

▲ +12.31%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nojima Co., Ltd. resolved on April 21, 2026, at its Board of Directors meeting, to acquire an equity stake in a new company (name undecided) to be established by Hitachi Global Life Solutions, Inc. (Hitachi GLS), making it a subsidiary, and executed related agreements.

- Nojima’s special purpose company will acquire 80.1% of the issued shares of the new company, which will take over Hitachi GLS’s home appliance business.

- The acquisition price is approximately JPY 110.1 billion, comprising JPY 110 billion for the new company’s common shares and approximately JPY 100 million for related expenses.

- The execution of this share acquisition is scheduled for the fiscal year ending March 2027.

- The new company will integrate Hitachi GLS’s domestic operations with its overseas home appliance business by acquiring all shares of Arçelik Hitachi Home Appliances B.V. (AHHA), including the 60% stake to be acquired from Arçelik A.S., thus consolidating Hitachi GLS’s home appliance business resources and operational base globally.

🤖 AI Perspective

This acquisition by Nojima appears to target the creation of a new business model that integrates retail customer touchpoints with manufacturing expertise. The consolidation of Hitachi’s domestic and international home appliance businesses under the new entity suggests an ambition to accelerate global expansion and deepen a customer-centric strategy from product development to after-sales service. Investors may find it worthwhile to monitor how this move could reshape Nojima’s future business portfolio and revenue structure.

3091|ブロンコB

4410.0

▼ -0.90%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Bronco Billy Co., Ltd. announced its consolidated financial results reference materials for the first quarter of the fiscal year ending December 2026 (January 1, 2026, to March 31, 2026) on April 21, 2026.

- During this period, net sales were JPY 8,241 million, an increase of 13.1% compared to the same period of the previous year.

- Operating profit stood at JPY 1,031 million, marking a 93.5% increase year-on-year.

- Ordinary profit reached JPY 1,037 million (up 87.6% year-on-year), and net profit was JPY 693 million (up 85.9% year-on-year).

- Existing store sales increased by 6.7% year-on-year, with customer traffic up 0.5% and average customer spending up 6.2%.

- The consolidated full-year forecast for the fiscal year ending December 2026 projects net sales of JPY 33,000 million (up 9.2% year-on-year), operating profit of JPY 3,000 million (up 2.4%), ordinary profit of JPY 3,050 million (up 0.8%), and net profit of JPY 2,000 million (up 1.5%).

🤖 AI Perspective

The first quarter of the fiscal year ending December 2026 saw significant profit growth alongside double-digit sales increase. The operating profit margin improved from 7.3% in the prior-year quarter to 12.5%, which may be attributed to a rise in gross profit margin and a decrease in selling, general and administrative expenses ratio. The strong performance in existing store sales could indicate positive momentum, making the progress towards the full-year forecast a point of interest for investors.

3440|日創グループ

957.0

▼ -0.31%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nisso Group announced a correction to a portion of the numerical data (XBRL) in its “Summary of Consolidated Financial Results for the First Quarter of the Fiscal Year Ending August 2026 (Japanese GAAP)” as of April 21, 2026.

- The correction specifically pertains to the XBRL summary information data from the earnings report initially disclosed on January 14, 2026.

- The company had mistakenly submitted XBRL data for the first quarter of the fiscal year ending August 2025, instead of the correct data for the first quarter of the fiscal year ending August 2026.

- To rectify this error, the company has resubmitted the correct XBRL data for the first quarter of the fiscal year ending August 2026.

- No corrections were made to the disclosure documents (PDF files) or the XBRL data for the consolidated financial statements themselves.

🤖 AI Perspective

This announcement from Nisso Group addresses an error in the XBRL data submitted for a past earnings report. The correction is limited to an informational processing mistake within the machine-readable XBRL format and does not impact the financial figures presented in the PDF disclosure documents or the consolidated financial statements. For investors, this may suggest that the issue is an administrative data submission error rather than a revision to the underlying financial performance of the company.

4293|セプテーニHD

431.0

▼ -1.15%

📎 Source:セプテーニHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Septeni Holdings Co., Ltd. resolved to introduce a shareholder benefit program at a Board of Directors meeting held on April 21, 2026.

- The program targets shareholders recorded on the company’s shareholder register as of December 31st each year, who hold 1,000 shares or more.

- The benefit entails presenting 5,500 yen equivalent points to eligible shareholders, which are exchangeable for various e-money.

- Information regarding the shareholder benefits is scheduled to be enclosed with the notice of convocation for the ordinary general meeting of shareholders, dispatched in early March each year.

- The program will commence for shareholders recorded on the shareholder register as of December 31, 2026.

🤖 AI Perspective

The introduction of a shareholder benefit program by Septeni Holdings appears to be part of its management strategy to enhance shareholder returns, increase investment appeal, and encourage long-term shareholding. The choice of points exchangeable for e-money suggests an emphasis on shareholder convenience. As the initial implementation is set for December 2026, it may be worth monitoring in conjunction with the company’s future business strategies.

4684|オービック

4194.0

▼ -1.71%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the consolidated fiscal year ended March 31, 2026, sales increased by 11.5% year-on-year to JPY 135,209 million, operating profit rose by 13.3% to JPY 88,823 million, and profit attributable to owners of parent increased by 16.4% to JPY 75,191 million, resulting in both higher revenue and profit.

- The annual dividend for the fiscal year ended March 31, 2026, was JPY 84.00 per share.

- The consolidated business forecast for the fiscal year ending March 31, 2027, projects sales of JPY 148,700 million (up 10.0% year-on-year), operating profit of JPY 98,000 million (up 10.3%), and profit attributable to owners of parent of JPY 82,000 million (up 9.1%).

- The forecasted annual dividend for the fiscal year ending March 31, 2027, is JPY 94.00 per share.

- The consolidated equity ratio as of March 31, 2026, was 83.4%, and net assets per share were JPY 1,190.80.

🤖 AI Perspective

The results for the fiscal year ended March 31, 2026, showed an increase in sales and various profits, indicating robust growth. Furthermore, the business forecast for the fiscal year ending March 31, 2027, projects continued sales and profit growth, which may suggest ongoing stability and expansion in the company’s operations. The high equity ratio also remains maintained, which could be viewed as a positive indicator of financial health.

5026|G-トリプルアイズ

616.0

▲ +2.67%

📎 Source:G-トリプルアイズ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- In the second quarter of the fiscal year ending August 2026, AI products positively contributed to the profit improvement in the first half. Key factors include increased demand for attendance management driven by labor law revisions, growing demand for security solutions in renewable energy, and expanded customized development utilizing the company’s facial recognition API/SDK.

- The service combining “alcohol detection x facial recognition” recorded a growth rate of approximately 157% in customer adoption and approximately 112% in Monthly Recurring Revenue (MRR) compared to the beginning of the period over the past six months.

- The high-profit level in the second quarter was primarily due to stronger-than-expected sales and operating income in the AI Solution business, not from underspending on selling, general, and administrative expenses.

- The GPU server business is accelerating its business model shift from conventional mining machine sales to GPU server sales for AI development purposes. While the crypto asset market downturn impacted the first half, an impairment loss of approximately 23 million yen on crypto assets was recorded in Q2, and the gross profit margin improved by approximately 10% year-over-year.

- Regarding measures to address the stock price decline, the company outlined a four-pillar strategy: early improvement of profitability, launching new products in growth domains such as manufacturing, considering strategic M&A, and strengthening IR communications.

🤖 AI Perspective

This Q&A provides insights into how AI products specifically contributed to the first-half profit improvement and discloses key business KPIs such as the adoption rate and MRR growth for the “alcohol detection x facial recognition” service. The stated transition of the GPU server business model and efforts to improve its profitability structure are noteworthy, suggesting potential shifts in future business composition. Additionally, the company’s direct address of stock price concerns and outlined countermeasures may be viewed as an indication of its commitment to investor engagement.

6058|ベクトル

1189.0

▼ -0.34%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Vector Inc., at its Board of Directors meeting held on April 21, 2026, resolved to acquire all shares of AILES Inc., making it a consolidated subsidiary, and signed the share transfer agreement on the same date.

- The acquisition aims to integrate AILES’s expertise in influencer/creator training and its talent resources, establishing a flexible system for supplying high-quality personnel for the rapidly expanding PR x short-video projects.

- AILES operates an online school for influencer/creator training, a membership community offering direct instruction from renowned influencers, and an SNS operation agency business.

- The total acquisition price is an estimated JPY 1,310 million, comprising JPY 1,250 million for AILES’s common shares and an estimated JPY 60 million for advisory fees.

- The share transfer is scheduled to be executed on April 30, 2026, with the impact on Vector’s consolidated financial results for the fiscal year ending February 2027 expected to be minor.

🤖 AI Perspective

- Vector Inc. appears to be pursuing M&A to strengthen its SNS services, responding to the expansion of the internet advertising market, particularly the growing demand for vertical video ads on SNS and connected TV.

- The integration of AILES’s influencer training know-how and human resources could potentially enhance Vector’s capabilities in providing PR services related to short-form videos.

- AILES has demonstrated growth in sales and profits over the past three fiscal years (September 2023 to September 2025), which may suggest its potential contribution to Vector’s group strategy moving forward.

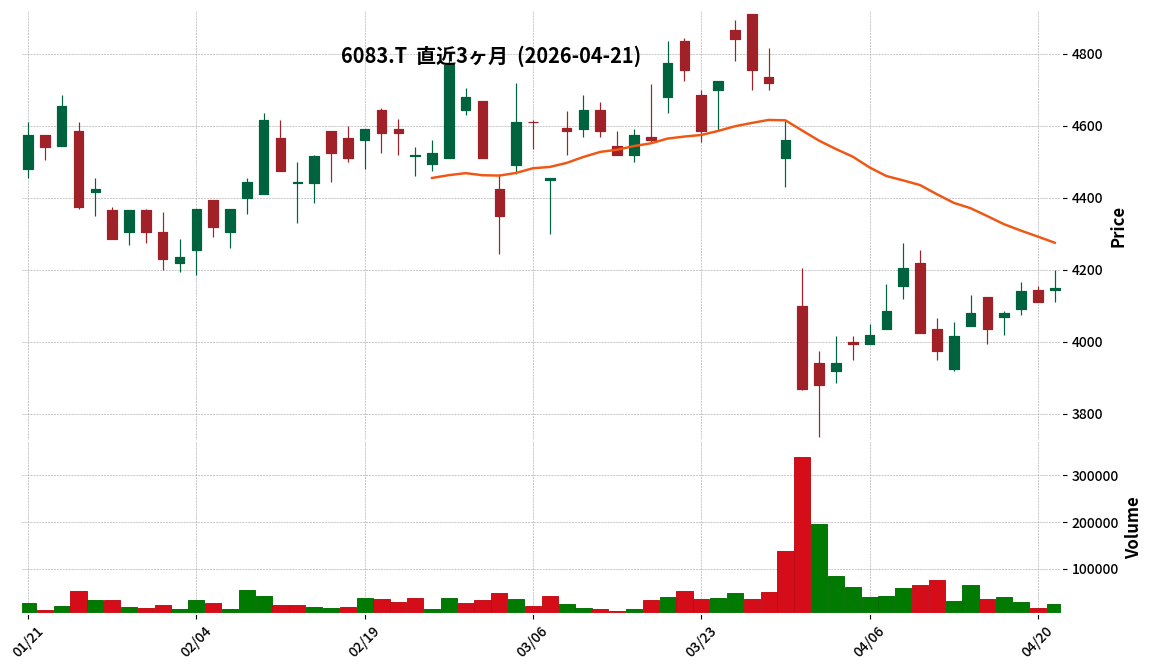

6083|ERI HD

4150.0

▲ +0.97%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- ERI HD resolved to implement a stock split and amend its Articles of Incorporation at a Board of Directors meeting held on April 21, 2026.

- The company will split its common shares at a ratio of three shares for every one share held, with May 31, 2026 (Sunday), set as the record date.

- The stock split will become effective on June 1, 2026 (Monday), increasing the total number of issued shares from 7,832,400 to 23,497,200.

- Concurrently, in accordance with Article 184, Paragraph 2 of the Companies Act, the total number of authorized shares stipulated in Article 6 of the Articles of Incorporation will be revised from 28,500,000 shares to 85,500,000 shares.

- There will be no change to the capital amount as a result of this stock split, and the fiscal year-end dividend for May 2026, based on the record date of May 31, 2026, will be distributed according to the number of shares prior to the split.

🤖 AI Perspective

A stock split is generally considered a strategy to reduce the per-share investment unit, which may make the company’s shares more accessible to a wider range of investors. This action could lead to enhanced stock liquidity and potentially attract new shareholder participation. Furthermore, the increase in the total number of authorized shares might provide the company with greater flexibility for future financing activities.

8225|タカチホ

3340.0

▼ -1.76%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- On April 21, 2026, Takachiho Co., Ltd. resolved to invest JPY 400 million in the “Omiyage Fund No. 1 Investment Limited Partnership,” which is managed and operated by Omiyage Company HD Co., Ltd., a wholly-owned subsidiary of Japan Asia Investment Co., Ltd.

- This investment stems from “collaboration on forming a fund specializing in the roll-up of the souvenir industry,” one of the key elements of the business alliance with Japan Asia Investment announced on March 4, 2025.

- The capital for this investment will come from JPY 133.7 million, derived from funds raised through a third-party allotment after deducting issuance expenses, combined with borrowed funds.

- The “Omiyage Fund No. 1 Investment Limited Partnership” was established on March 24, 2026, with an expected total fund amount of JPY 813 million upon completion of investment, and Takachiho’s projected investment ratio is 49.2%.

- The fund’s objective is to target small and medium-sized regional souvenir-related companies facing challenges in business succession or growth, aiming to strengthen product development and sales utilizing regional specialties and expand into overseas markets through collaboration with portfolio companies.

🤖 AI Perspective

Takachiho’s investment in the fund suggests a tangible advancement in its business alliance with Japan Asia Investment. This move appears to align with Takachiho’s 10-year vision as a “regional charm creation producer,” potentially strengthening product development and sales of regional specialties and building a foundation for overseas business expansion. Participation in a fund focused on the souvenir industry’s roll-up could be a strategic investment for the company, seeking synergistic effects for business growth through potential M&A within the sector.

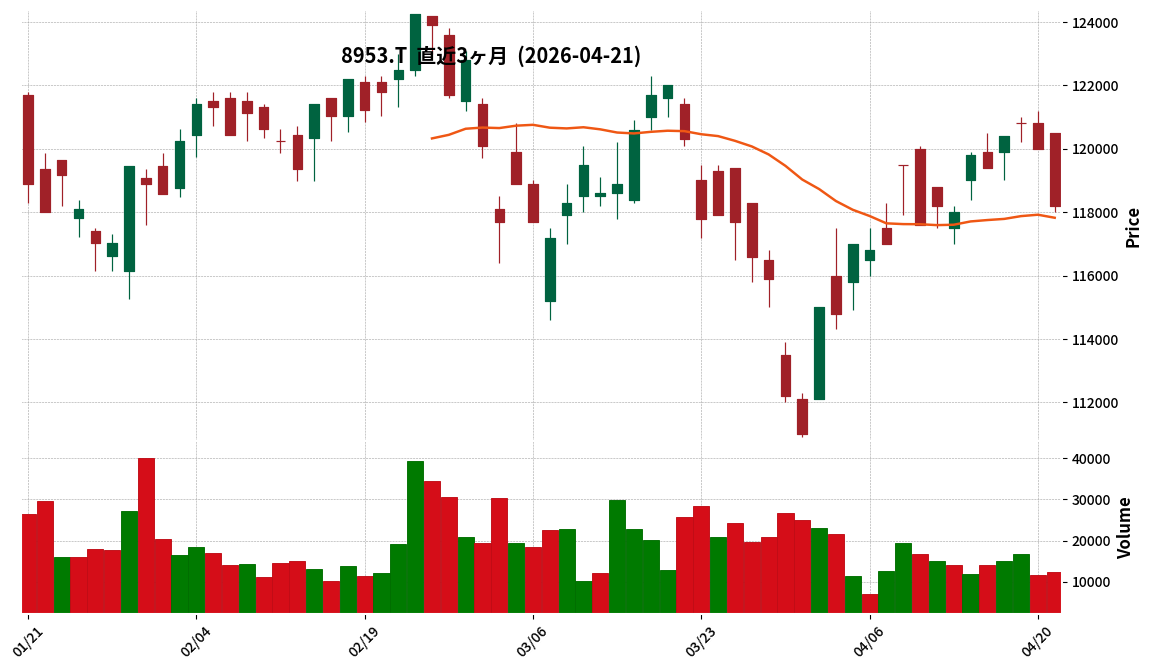

8953|R-都市ファンド

118200.0

▼ -1.50%

📎 Source:R-都市ファンド Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Japan Urban Fund, Inc. announced its financial results for the February 2026 fiscal period (September 1, 2025, to February 28, 2026), reporting an increase in revenue and profit with operating revenue of ¥52,075 million (up 5.6% from August 2025 period), operating income of ¥26,650 million (up 9.7%), and net income of ¥23,695 million (up 9.2%).

- Distribution per unit (excluding excess distribution of profits) for the period was ¥3,006 (an increase of ¥186 from August 2025 period).

- As of February 28, 2026, total assets stood at ¥1,363,436 million, net assets at ¥653,100 million, and the equity ratio at 47.9%.

- During the period, the fund acquired 17 properties and transferred 3 properties (including partial acquisitions and transfers). It completed the acquisition of 14 office properties owned by the Fujisoft Group, a CRE carve-out project in collaboration with KKR. Additionally, it made further investments in two privately placed REITs primarily targeting residential properties.

- For the next period, August 2026, the fund forecasts operating revenue of ¥51,028 million (down 2.0% from February 2026 period), net income of ¥22,453 million (down 5.2%), and DPU of ¥2,981. A decrease in revenue and profit is also projected for the subsequent February 2027 period, with operating revenue of ¥46,168 million (down 9.5% from August 2026 period) and DPU of ¥2,900.

🤖 AI Perspective

The February 2026 fiscal period showed robust performance with increases in operating revenue, operating income, net income, and DPU compared to the previous period. This suggests that the active management strategies, including the acquisition of multiple properties and additional investments in private REITs, contributed positively to earnings.

However, the fund has projected a decline in both revenue and profit for the upcoming August 2026 and February 2027 periods, which investors may wish to monitor closely for underlying reasons. Amidst continued strong investor appetite in the real estate transaction market and a robust leasing market, the fund’s future asset replacement strategies and initiatives to stabilize earnings could be key areas of focus.

8954|R-オリックスF

100800.0

▼ -0.20%

📎 Source:R-オリックスF Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal period ended February 2026, operating revenue was ¥31,181 million (up 9.7% from the previous period), operating income was ¥16,250 million (up 14.9%), ordinary income was ¥14,417 million (up 15.2%), and net income was ¥14,404 million (up 15.3%).

- Distribution per unit (excluding excess distributions) was ¥2,414, with total distributions amounting to ¥13,325 million. The distribution payout ratio was 92.4%.

- As of the end of the period, total assets stood at ¥743,354 million, net assets at ¥353,645 million, the unitholders’ equity ratio at 47.6%, and net assets per unit at ¥64,066.

- During the period, the REIT acquired “Holiday Inn Express Osaka City Centre Midosuji” (acquisition price ¥22,516 million), “Prime Shin-Yokohama Building” (acquisition price ¥9,250 million), and a 16% co-ownership interest in “Tenjin North Front Building” (acquisition price equivalent to ¥1,016 million), while selling a 40% co-ownership interest in “Aoyama Suncrest Building” (sale price ¥6,796 million).

- The occupancy rate of its real estate assets remained high at 99.1% as of February 28, 2026.

- A 2-for-1 investment unit split was implemented with a record date of August 31, 2025, and an effective date of September 1, 2025. Per-unit metrics are calculated based on the number of units after the split.

🤖 AI Perspective

R-Orix F’s strong performance in the February 2026 fiscal period, characterized by solid growth in operating revenue and profits, may suggest effective asset management and a robust market presence. The REIT’s strategy of optimizing its portfolio through both acquisitions and disposals, coupled with a high occupancy rate of 99.1%, could indicate a resilient income base. Looking forward, the projected distribution per unit of ¥2,450 for both the August 2026 and February 2027 fiscal periods highlights the REIT’s commitment to consistent unitholder returns, which will be a key factor for investors to monitor.

9763|丸建リース

1356.0

▲ +0.22%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Maruken Lease Co., Ltd. announced on April 21, 2026, the completion of its acquisition of all shares of Daichi Lease Co., Ltd., making it a subsidiary.

- This acquisition serves as a progress report on the “Notice Regarding the Acquisition of Shares of Daichi Lease Co., Ltd. (Making it a Subsidiary)” previously disclosed on March 17, 2026.

- The company stated that this transaction will have no impact on its full-year consolidated performance for the fiscal year ending March 2026.

🤖 AI Perspective

This announcement confirms the successful execution of a previously disclosed M&A strategy by Maruken Lease. The statement regarding no impact on the fiscal year ending March 2026 consolidated results may indicate that the financial effects were either already accounted for or are not material within the current fiscal period. Investors might now look for future updates on potential synergies and integration progress.

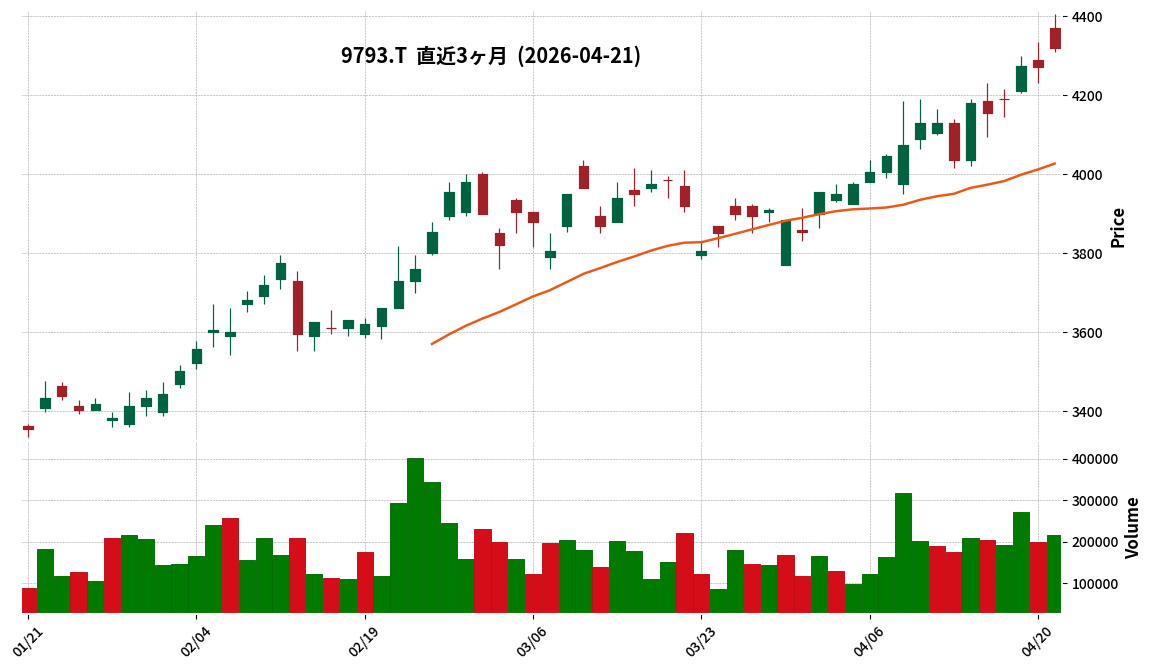

9793|ダイセキ

4320.0

▲ +1.17%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Daiseki Co., Ltd. announced on April 21, 2026, an amendment to its “Consolidated Financial Results for the Fiscal Year Ended February 28, 2026 (Japanese GAAP),” originally released on April 7, 2026.

- The reason for the amendment is stated as the discovery of errors in certain descriptions due to an administrative mistake after the initial publication.

- The corrections primarily affect the “Summary Information (1) Consolidated Business Results” and the “Consolidated Statement of Comprehensive Income” within “3. Consolidated Financial Statements and Primary Notes (2) Consolidated Statements of Income and Comprehensive Income.”

- The consolidated comprehensive income for the fiscal year ended February 2026 has been revised from ¥10,233 million (△0.4%) to ¥10,221 million (△0.5%).

- Specifically, in the Consolidated Statement of Comprehensive Income for the fiscal year (March 1, 2025, to February 28, 2026), “Adjustments relating to retirement benefits” changed from △83 to △94, “Total other comprehensive income” from 340 to 328, “Comprehensive income” from 10,233 to 10,221, and “Comprehensive income attributable to owners of the parent” from 9,504 to 9,492 (all figures in millions of yen).

🤖 AI Perspective

This amendment primarily concerns the consolidated comprehensive income for the fiscal year ended February 2026 and is attributed to an administrative error. It is noted that the net income for the period itself remains unchanged, with only specific figures within comprehensive income being revised. Investors may find it important to monitor such correction notices to ensure the accuracy of reported financial data.

375A|P-YAKHD

2125.0

▲ +0.00%

📎 Source:P-YAKHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- P-YAKHD announced that its wholly-owned subsidiary, YAK Development Co., Ltd., will acquire 100% of RISE ON Co., Ltd.’s shares, making it a wholly-owned subsidiary, as resolved by the Board of Directors on April 21, 2026.

- The purpose of this share acquisition is to expand YAK Development’s real estate trading business, strengthen new operational bases, and achieve synergies with existing businesses.

- RISE ON Co., Ltd. operates in real estate brokerage, rental brokerage, and property management. For the fiscal year ending August 2025, it reported net sales of 102,246 thousand yen and a net loss of 7,430 thousand yen.

- The acquisition involves 200 shares, representing 100% of the voting rights, with the share transfer scheduled for April 30, 2026.

- P-YAKHD expects the impact of this acquisition on its consolidated financial results for the current fiscal year to be minor.

🤖 AI Perspective

This acquisition suggests P-YAKHD Group’s strategic intent to strengthen and expand its real estate business through a wholly-owned subsidiary. RISE ON Co., Ltd.’s business in real estate brokerage and property management could potentially generate synergies and broaden the service offerings when integrated with existing real estate trading operations. Investors might monitor the post-acquisition integration progress and the implementation of profitability improvement measures, especially given the target company’s recent net loss.

7444|ハリマ共和物産

1967.0

▼ -2.48%

📎 Source:ハリマ共和物産 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- On April 21, 2026, Harima Kyowa Bussan announced the financial results for the fiscal year ended January 2026 of its non-listed parent company (other affiliated company), Tsuda Bussan Co., Ltd.

- Tsuda Bussan’s business activities consist of real estate leasing and management, with its location in Himeji City, Hyogo Prefecture.

- According to Tsuda Bussan’s income statement for the fiscal year ended January 2026, net sales were ¥53,393 thousand, operating income was ¥4,023 thousand, ordinary income was ¥107,942 thousand, and net income for the period was ¥109,729 thousand.

- As of January 31, 2026, Tsuda Bussan’s balance sheet reported total assets of ¥2,462,091 thousand, total liabilities of ¥1,324,990 thousand, and total net assets of ¥1,137,101 thousand.

- Major shareholders as of January 31, 2026, include Shinya Tsuda (16.48%), Takao Tsuda (14.16%), Noriko Tsuda (9.10%), with individuals owning 100% of the total issued shares.

🤖 AI Perspective

The disclosure of a parent company’s financial results may enhance transparency in the corporate governance of its listed subsidiary, Harima Kyowa Bussan. Investors might consider the financial status of a non-listed parent company as a reference point for evaluating the overall financial health and business strategy of the entire group. Furthermore, given that the parent company is engaged in real estate leasing and management, this information could contribute to understanding the group’s diversified business portfolio.

💡 Start investing with IR insights

※ 本ページには広告が含まれます(PR)

Disclaimer: This article is for informational purposes only and does not constitute investment advice. All investment decisions are at your own risk.

コメント