📌 Today’s Highlights

Today we cover 58 IR announcements. Notable among them: 梅乃宿酒造 (559A), P-寶結 (562A), 第一三共 (4568). Use the table of contents below to navigate to each company.

- 559A|梅乃宿酒造

- 562A|P-寶結

- 4568|第一三共

- 5592|G-くすりの窓口

- 6723|ルネサス

- 2865|GXNDXカバコ

- 424A|GXゴールドH

- 8706|極東証券

- 3927|フーバーブレイン

- 4956|コニシ

- 8595|ジャフコ グループ

- 8393|宮崎銀

- 8358|スルガ銀

- 1407|ウエストHD

- 1803|清水建

- 2737|トーメンデバ

- 3739|コムシード

- 3912|モバファク

- 8541|愛媛銀

- 4765|SBIGアセットM

- 1870|矢作建

- 3891|高度紙

- 4973|高純度化

- 5423|東製鉄

- 3181|買取王国

- 1814|大末建

- 1972|三晃金

- 2804|ブルドックソース

- 8059|第一実業

- 8395|佐賀銀

- 8707|岩井コスモ

- 5990|スーパーツール

- 6345|アイチ

- 7102|日車輌

- 7422|東邦レマック

- 1436|G-グリーンエナジー

- 3932|アカツキ

- 2134|キタハマキャピタル

- 2481|タウンニュース

- 2801|キッコマン

- 3236|プロパスト

- 3762|テクマト

- 4056|G-ニューラル

- 4307|NRI

- 4571|G-NANO

- 5609|日鋳造

- 1720|東急建設

- 217A|P-サポート

- 4069|G-BlueMeme

- 6861|キーエンス

- 7962|キングジム

- 9788|ナック

- 6023|ダイハツインフィ

- 4519|中外薬

- 5288|アジアパイルHD

- 3260|エスポア

- 9941|太洋物産

- 4832|JFE-SI

559A|梅乃宿酒造

—

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Umenoyado Shuzo announced its listing on the Tokyo Stock Exchange Standard Market.

- In conjunction with this listing, the company disclosed its financial results and other relevant information.

- The announcement was officially made through the Tokyo Stock Exchange.

🤖 AI Perspective

- Listing on the TSE Standard Market can enhance corporate credibility and broaden access to capital for Umenoyado Shuzo.

- The disclosure of financial information concurrent with the listing provides crucial data for investors to assess the company’s financial health and performance.

- This development is likely to draw attention from market participants interested in the company’s future business strategies and growth potential.

562A|P-寶結

—

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- HOYU Co., Ltd. (Code: 562A) listed its shares on the Tokyo Stock Exchange TOKYO PRO Market and the Fukuoka Stock Exchange Fukuoka PRO Market on April 24, 2026.

- For the fiscal year ending August 2026 (September 1, 2025 – August 31, 2026), the company forecasts net sales of JPY 1,250 million (up 52.5% YoY), operating income of JPY 125 million (up 141.3% YoY), ordinary income of JPY 125 million (up 141.1% YoY), and net income of JPY 80 million (up 111.1% YoY).

- Actual results for the interim period of FY2026 (September 1, 2025 – February 28, 2026) were net sales of JPY 662 million, operating income of JPY 8 million, ordinary income of JPY 7 million, and net income of JPY 4 million.

- The company announced a per-share dividend of JPY 0.00 for both the interim actual and full-year forecast for FY2026.

- HOYU conducted a 1-for-3 stock split of its common shares effective November 28, 2025.

🤖 AI Perspective

HOYU Co., Ltd. announced its full-year earnings forecast for FY2026 concurrently with its listing on the TOKYO PRO Market and Fukuoka PRO Market. The company’s projections indicate substantial growth in both revenue and profit, driven by its assessment of a robust business environment characterized by sustained DX-related investments, cloud migration, expanded use of generative AI, and increasing IT service demand due to labor shortages. This PRO Market listing may enhance the company’s credibility and provide a platform for broader information dissemination to support business expansion.

4568|第一三共

2790.0

▼ -1.88%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Daiichi Sankyo announced a change in the release date for its financial results for the fiscal year ending March 2026 from April 27, 2026, to May 11, 2026.

- The announcement date for the 6th Mid-Term Business Plan has also been changed from May 19, 2026, to May 11, 2026, to be released concurrently with the financial results.

- The reason for the schedule change is that it requires more time to finalize the financial figures.

- Specifically, the company stated that due to rapid changes in the business environment, it is re-evaluating the supply plans for its oncology product portfolio and development candidates, which necessitates additional consideration for a reasonable estimate of provisions for loss compensation related to contracts with manufacturing contractors.

- The impact of this matter on the company’s financial performance for the fiscal year ending March 2026 is currently under scrutiny, and any discloseable matters will be announced promptly.

🤖 AI Perspective

The postponement of financial results may introduce a degree of uncertainty for investors regarding the company’s performance. The specific mention of re-evaluating supply plans for oncology products and the need for additional review regarding loss compensation provisions could indicate potential impacts on future earnings, making the detailed explanation particularly noteworthy. Combining the mid-term business plan announcement with the results may provide investors with a comprehensive view of the company’s strategy and outlook.

5592|G-くすりの窓口

2805.0

▲ +1.15%

📎 Source:G-くすりの窓口 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-KUSURI NO MADOGUCHI announced an upward revision of its consolidated earnings forecast for the fiscal year ending March 2026. Consolidated net sales are revised from JPY 12,300 million to JPY 12,330 million, operating profit from JPY 2,450 million to JPY 2,681 million, ordinary profit from JPY 2,400 million to JPY 2,666 million, and profit attributable to owners of parent from JPY 2,690 million to JPY 2,900 million.

- The revised forecast indicates a 9.4% increase in consolidated operating profit, an 11.1% increase in consolidated ordinary profit, and a 7.8% increase in profit attributable to owners of parent, compared to the previous forecast.

- Reasons for the revision include a greater-than-planned increase in new users for the prescription online reception service in the media business, the addition of two consolidated subsidiaries following the complete acquisition of Medi-web, Inc. (effective December 5, 2025), and ongoing cost optimization across group companies.

- The company also revised its year-end dividend forecast for the fiscal year ending March 2026 upward, from JPY 36.00 per share to JPY 38.00 per share, making the annual dividend JPY 38.00 per share.

- The dividend revision is based on the company’s basic policy of maintaining stable dividends with a target consolidated payout ratio of approximately 15%, in conjunction with the upward revision of the consolidated earnings forecast.

🤖 AI Perspective

The upward revision of the consolidated earnings forecast suggests that growth in the core media business, coupled with strategic M&A and cost efficiency measures, has contributed positively to the company’s financial performance. The subsequent increase in the dividend forecast, aligned with the target payout ratio, indicates a return of profits to shareholders. These developments may suggest a strengthening operational foundation and could be worth monitoring for future performance trends.

6723|ルネサス

3300.0

▲ +6.69%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Renesas Electronics Corporation announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026, to March 31, 2026).

- Sales Revenue for the quarter amounted to ¥380,293 million, representing a 23.2% increase compared to the same period of the previous year.

- Operating Profit reached ¥90,564 million, marking a substantial 320.7% year-on-year increase.

- Profit attributable to owners of the parent increased by 162.1% year-on-year to ¥68,149 million.

- On a Non-GAAP basis, sales revenue for Q1 FY2026 was ¥372.3 billion (+20.6% YoY), and operating profit was ¥125.4 billion (+49.6% YoY).

- The company forecasts Non-GAAP sales revenue for the cumulative second quarter of FY2026 (January 1 – June 30, 2026) to range between ¥752,842 million and ¥767,842 million, an anticipated increase of 18.9% to 21.2% year-on-year.

🤖 AI Perspective

The Q1 FY2026 results indicate significant year-on-year growth in both sales revenue and various profit metrics, measured by both IFRS and Non-GAAP standards. The notable increase in operating profit may suggest improvements in the company’s profitability. Segment-wise, Non-GAAP sales in the Industrial, Infrastructure, and IoT business grew by 32.0% year-on-year, surpassing the 10.6% growth in the Automotive business, which could suggest diversified demand drivers supporting Renesas’ performance.

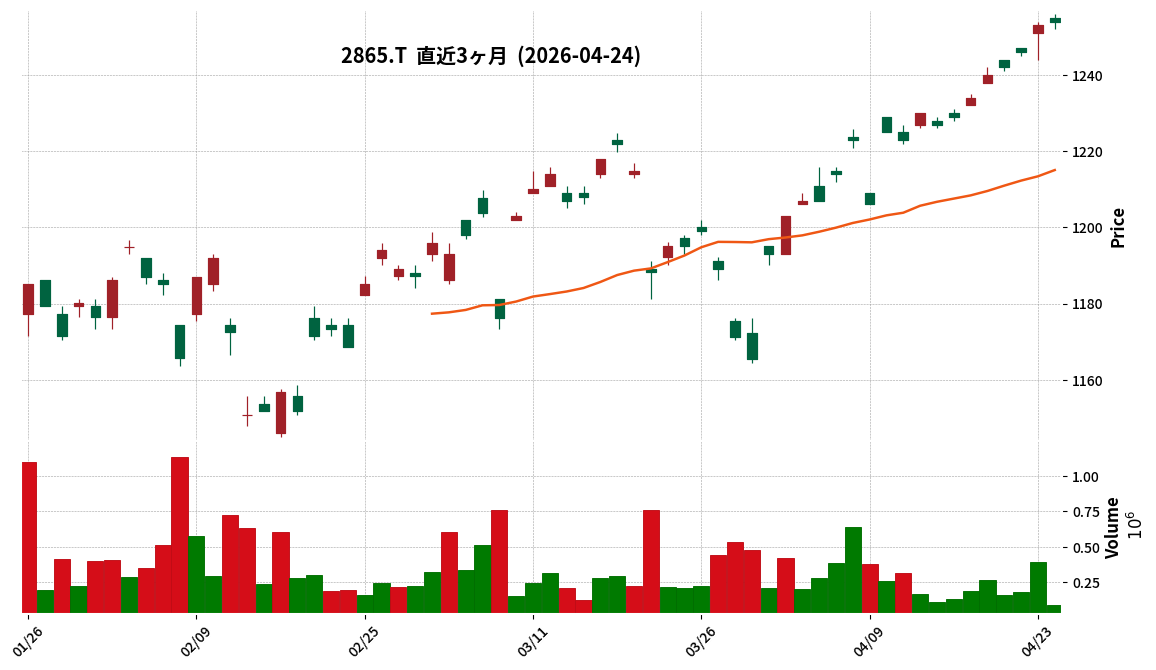

2865|GXNDXカバコ

1255.0

▲ +0.32%

📎 Source:GXNDXカバコ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Global X NASDAQ-100 Covered Call ETF (2865) announced its financial results for the fiscal period ended March 2026 (September 11, 2025 – March 10, 2026) on April 24, 2026.

- Total net assets at the end of the current period were JPY 42,619 million, an increase from JPY 33,117 million at the end of the previous period (September 2025).

- The Net Asset Value (NAV) per 100 units at the end of the current period was JPY 121,769, up from JPY 108,902 at the end of the previous period (September 2025).

- The number of outstanding units for the current period increased to 35,000 thousand units, from 30,410 thousand units at the end of the previous period. Units set were 7,810 thousand units, and units cancelled were 3,220 thousand units.

- Net income for the specified period (September 11, 2025 – March 10, 2026) amounted to JPY 6,040,918,103.

- The distribution per 100 units for the March 2026 period was JPY 1,100, with total distributions within this period reaching JPY 2,055,580,000.

🤖 AI Perspective

The results for the current period show increases in total net assets, outstanding units, and NAV per 100 units compared to the previous period, which may suggest an expansion in fund size and an improvement in operational performance. The rise in NAV, in particular, could indicate an increase in the asset value of the investment trust. Furthermore, a track record of consistent distributions may be a factor that contributes to the fund’s appeal for investors.

424A|GXゴールドH

363.2

▼ -0.38%

📎 Source:GXゴールドH Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Global X Gold ETF (Hedged, Code: 424A) announced its financial results for the period ended March 2026 (September 24, 2025 to March 10, 2026).

- Net assets at the end of the calculation period amounted to ¥3,781 million, with the 100-unit net asset value (NAV) at ¥40,268.

- New subscriptions totaled 12,210 thousand units, while redemptions were 2,820 thousand units, resulting in 9,390 thousand units outstanding at the end of the period.

- Total operating revenue was ¥532,715,836, with operating profit and net profit for the period both recorded at ¥531,770,632.

- No distribution was paid per 100 units.

🤖 AI Perspective

This fund, “Global X Gold ETF (Hedged),” tracks a gold price index while implementing currency hedging, a key characteristic for investors. The breakdown of operating revenue indicates that profits from securities trading and foreign exchange gains were primary contributors, suggesting that market movements and the fund’s hedging strategy played a significant role in its performance. The absence of a dividend is noted as due to a lack of distributable amount, which could be an important detail for investors understanding the fund’s operational specifics.

8706|極東証券

1596.0

▼ -0.75%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kyokuto Securities announced its consolidated financial results for the fiscal year ended March 31, 2026, reporting operating revenue of ¥8.317 billion, a 4.1% increase year-on-year.

- Net income attributable to owners of the parent company amounted to ¥4.790 billion, representing a 7.7% increase from the previous fiscal year.

- Operating income grew by 12.9% to ¥3.039 billion, and ordinary income increased by 16.0% to ¥4.006 billion.

- Basic earnings per share for FY2026/3 was ¥150.37, up from ¥139.38 in the prior year.

- The annual dividend for FY2026/3 is ¥110.00 per share, consisting of an interim dividend of ¥50.00 and a year-end dividend of ¥60.00, unchanged from the previous fiscal year.

🤖 AI Perspective

Kyokuto Securities’ FY2026/3 results show increases across key revenue and profit metrics, suggesting a solid performance for the period. The double-digit growth in operating and ordinary income, alongside a significant rise in net income, may indicate a favorable operating environment or effective business strategies. The unchanged annual dividend payout could be seen as a sign of consistent shareholder returns, which might be a point of interest for investors.

3927|フーバーブレイン

1031.0

▲ +0.49%

📎 Source:フーバーブレイン Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hooverbrain Co., Ltd. resolved at its Board of Directors meeting on April 24, 2026, to acquire a portion of FieldTech Corporation’s shares (51.0% voting rights) and make it a consolidated subsidiary.

- As part of the consideration for this acquisition, a third-party allocation of treasury shares was also announced. The disposition is for 19,493 common shares to Mr. Kazuo Chiba of FieldTech, with a total disposal value of JPY 19,999,818.

- The estimated total acquisition cost for this share acquisition is JPY 231 million, comprising JPY 203 million for common shares and JPY 27 million for advisory fees.

- FieldTech Corporation operates in mobile communication, fixed-line network, and IT solution businesses, with 30 years of transaction history with major telecommunication carriers.

- FieldTech Corporation is expected to become a consolidated subsidiary of Hooverbrain from Q2 of the fiscal year ending March 2027.

🤖 AI Perspective

- This consolidation appears to be part of Hooverbrain’s ongoing M&A strategy outlined in its mid-term management plan, aimed at strengthening its business domain in response to the growing demand for communication infrastructure in the AI era.

- By integrating FieldTech’s technical capabilities and project management expertise in communication infrastructure construction into the group, Hooverbrain may anticipate synergies such as internalizing security product installation services and expanding its client base.

- The third-party allotment of treasury shares could be seen as an effort to align interests with FieldTech’s existing shareholder, thereby enhancing commitment to long-term corporate value improvement.

4956|コニシ

1345.0

▼ -1.10%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the consolidated fiscal year ended March 2026, Konishi reported net sales of JPY 136,569 million (up 0.6% year-on-year), operating profit of JPY 10,464 million (down 0.9%), ordinary profit of JPY 11,098 million (down 0.9%), and net income attributable to owners of parent of JPY 8,033 million (down 0.6%).

- The annual dividend for the fiscal year ended March 2026 was set at JPY 38.00 per share, comprising an interim dividend of JPY 19.00 and a year-end dividend of JPY 19.00, maintaining the same amount as the previous fiscal year.

- The consolidated earnings forecast for the fiscal year ending March 2027 projects net sales of JPY 150,000 million (up 9.8% year-on-year), operating profit of JPY 11,500 million (up 9.9%), ordinary profit of JPY 11,900 million (up 7.2%), and net income attributable to owners of parent of JPY 8,190 million (up 2.0%).

- Effective from the beginning of the fiscal year ended March 2026, the company changed its accounting treatment for real estate leasing income and expenses, reclassifying them from net sales and cost of sales to non-operating income and expenses. Comparative figures for the fiscal year ended March 2025 have been restated to reflect this change.

- Cash flows from operating activities for the fiscal year ended March 2026 increased to JPY 13,733 million, up from JPY 7,174 million in the previous fiscal year.

🤖 AI Perspective

While Konishi achieved increased net sales for FY2026, profit figures across all categories saw a slight decrease. However, the company’s consolidated earnings forecast for FY2027 anticipates growth in both sales and all profit metrics, which may suggest expectations for improved market conditions or the realization of benefits from ongoing capital expenditures. The substantial increase in cash flows from operating activities in FY2026 compared to the prior year could indicate enhanced operational cash generation.

8595|ジャフコ グループ

2309.5

▲ +0.52%

📎 Source:ジャフコ グループ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026 (non-consolidated), JAFCO Group reported net sales of JPY 21,619 million (down 23.3% year-on-year), operating income of JPY 5,607 million (down 53.5%), ordinary income of JPY 5,905 million (down 55.1%), and net income of JPY 6,576 million (down 31.7%).

- The annual dividend per share is JPY 133.00 (interim dividend JPY 66.50, year-end dividend JPY 66.50), resulting in a dividend payout ratio of 107.6%. The company forecasts a minimum annual dividend of JPY 133.00 for the fiscal year ending March 31, 2027.

- From the third quarter of the fiscal year ending March 31, 2026, the company shifted from consolidated financial reporting to non-consolidated (individual) reporting. This change followed the completion of share transfers for consolidated subsidiaries and the removal of JAFCO Consulting Co., Ltd. from the scope of consolidation.

- As of March 31, 2026, total assets stood at JPY 157,856 million, net assets at JPY 134,113 million, and the equity ratio was 85.0%.

- The dividend policy was revised to set the annual dividend per share from FY2026/3 onwards as the greater of a dividend on equity (DOE) of 6% against shareholders’ equity at the end of the previous fiscal year, or a dividend payout ratio of 50%.

🤖 AI Perspective

The year-on-year changes in financial performance may be influenced by the shift to non-consolidated financial reporting from Q3 FY2026/3, as the comparison figures for the prior year are based on individual results. The annual dividend of JPY 133 per share and a payout ratio exceeding 100% reflect the company’s revised dividend policy, which prioritizes a minimum Dividend on Equity (DOE) of 6%, potentially indicating a strong commitment to shareholder returns. Due to the nature of its business, the company deems it difficult to reasonably forecast future performance and has not provided earnings guidance for FY2027/3.

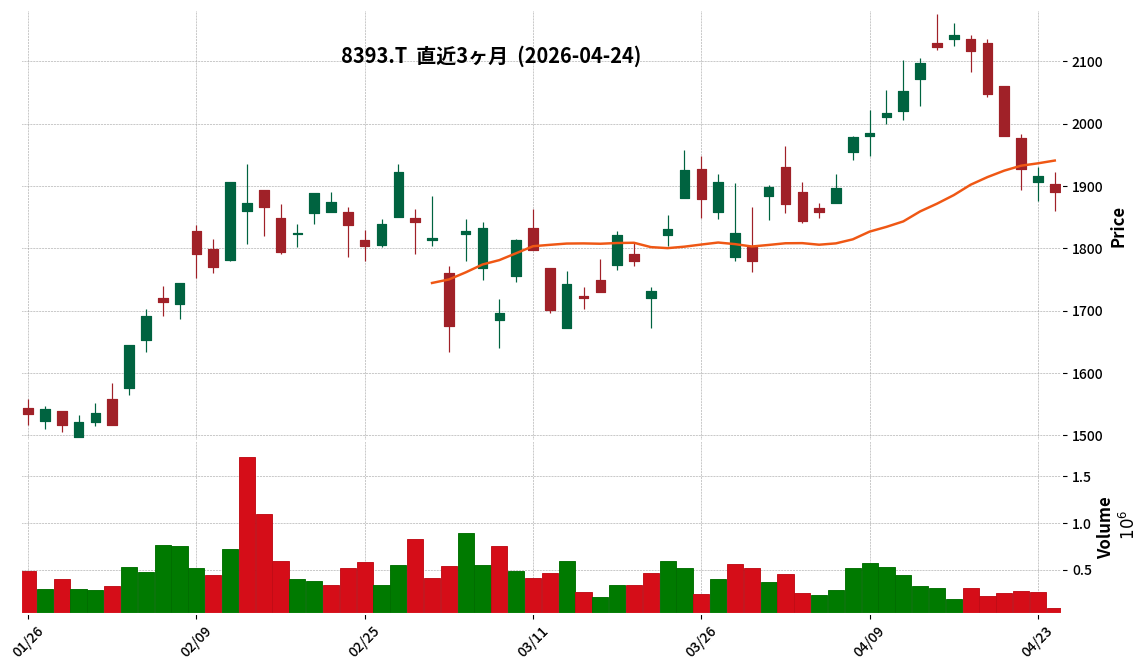

8393|宮崎銀

1891.0

▼ -1.30%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Miyazaki Bank resolved to introduce a shareholder benefit program at its Board of Directors meeting held on April 24, 2026.

- The program will commence from fiscal year 2027, with the objectives of showing gratitude to shareholders, enhancing investment appeal, and contributing to the local region.

- Eligible shareholders are those recorded in the shareholder register on March 31 each year who continuously hold 500 or more shares for over one year. For the first time only, eligibility will extend to shareholders recorded with 500 or more shares consecutively on September 30, 2026, and March 31, 2027.

- Shareholder benefits include QUO cards or regional specialty products, valued at JPY 2,000, JPY 4,000, or JPY 8,000, depending on the number of shares held. Selections are made via a dedicated website, and shipments are limited to addresses within Japan. The option to donate to social contribution organizations is also under consideration.

🤖 AI Perspective

The introduction of a shareholder benefit program by a regional financial institution could be seen as a strategic move to attract and retain long-term individual investors. The requirement for continuous holding over one year, alongside the relaxed initial eligibility, may suggest an aim to build a stable shareholder base while generating immediate interest. Furthermore, offering regional specialty products as benefits might indicate a dual focus on shareholder value and local economic contribution.

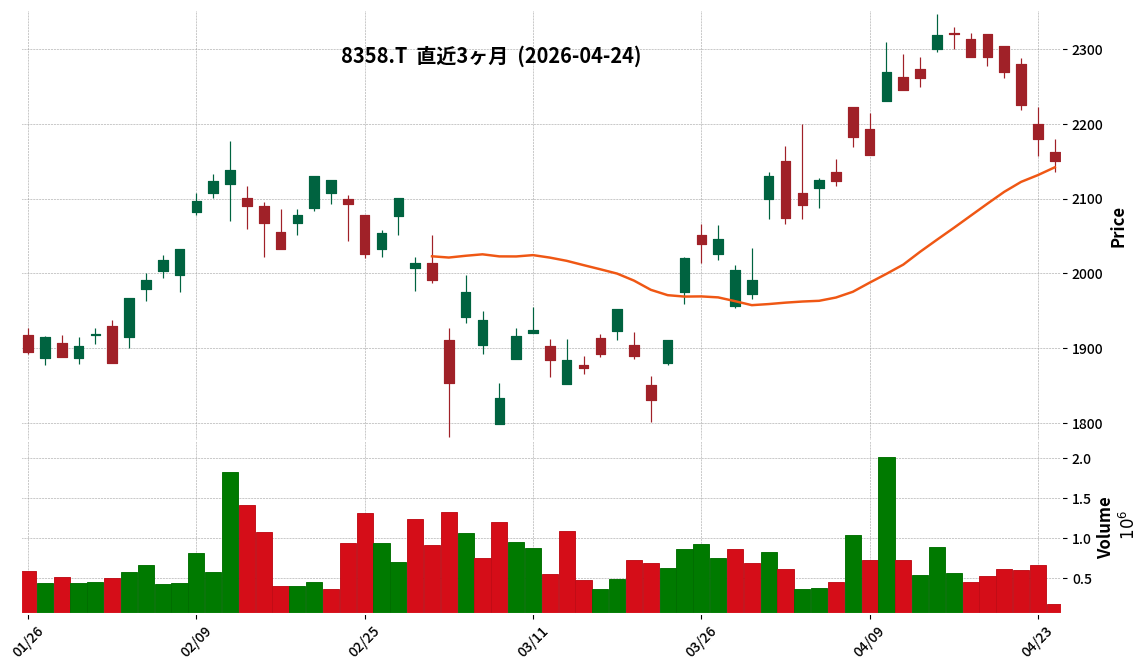

8358|スルガ銀

2150.0

▼ -1.38%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Suruga Bank announced an upward revision to its consolidated full-year earnings forecast for the fiscal year ending March 2026, with ordinary profit revised from JPY 31.0 billion to JPY 35.0 billion, and net profit attributable to owners of the parent revised from JPY 25.0 billion to JPY 34.0 billion.

- The annual dividend forecast for the fiscal year ending March 2026 has been revised upward by JPY 16 to JPY 60 per share, from the previously announced JPY 44.

- Consolidated ordinary revenue for the fiscal year ending March 2026 is projected to be JPY 109.5 billion, compared to the previous fiscal year’s JPY 91.092 billion.

- Key reasons for the earnings revision include the favorable performance of the loan business, steady progress in cost reductions primarily in property expenses, and real credit costs expected to be lower than previous estimates due to improved asset quality.

- The increase in net profit is also attributed to additional recording of deferred tax assets and tax-exempt treatment of some provisions from prior fiscal years, which led to a decrease in tax expenses.

🤖 AI Perspective

This upward revision to earnings and the significant dividend increase may suggest a strengthening of Suruga Bank’s core business operations and effective cost management. The substantial increase in the annual dividend could be interpreted as a positive signal regarding the company’s commitment to shareholder returns and confidence in its future financial stability. Investors might view these developments as indicators of improved financial health and a potentially more stable earnings outlook for the bank.

1407|ウエストHD

2555.0

▲ +8.45%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- West Holdings Co., Ltd. resolved to merge its wholly-owned subsidiaries during a Board of Directors meeting held on April 24, 2026.

- The merger will be an absorption-type merger, with West Energy Solution Co., Ltd. as the surviving company and West Begin Co., Ltd. as the absorbed company.

- The effective date of the merger is scheduled for June 1, 2026.

- The stated purpose of the merger is to optimize the effective utilization of group management resources, enhance efficiency, expedite decision-making, and strengthen customer support systems.

- As this merger involves wholly-owned subsidiaries, there will be no issuance of new shares or allotment of cash, and the impact on the company’s consolidated earnings is projected to be minor.

🤖 AI Perspective

This merger between wholly-owned subsidiaries may suggest West Holdings’ strategic initiative to streamline operations and enhance management efficiency within its group. By integrating two entities with distinct business activities, “construction work” and “wholesale of renewable energy-related products,” the company could aim for synergies and a unified management structure. While the immediate impact on consolidated earnings is indicated to be minor, investors might observe how this reorganization contributes to long-term operational efficiency and market responsiveness.

1803|清水建

2786.0

▼ -0.50%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Shimizu Corporation announced on April 24, 2026, revisions to its full-year consolidated earnings forecast and year-end dividend forecast for the fiscal year ending March 31, 2026.

- The consolidated earnings forecast was revised upwards for all key metrics: Net Sales to 2,057,800 million JPY (up 2.4% from previous forecast), Operating Profit to 118,600 million JPY (up 7.8%), Ordinary Profit to 122,300 million JPY (up 10.2%), and Profit attributable to owners of parent to 126,600 million JPY (up 15.1%).

- Reasons for the upward revision include smooth progress in domestic building and civil engineering works and improved profitability in individual performance, as well as enhanced project profitability at domestic and overseas construction subsidiaries.

- Additionally, a gain on bargain purchase of 5,900 million JPY, resulting from the acquisition of Aomi Construction Co., Ltd. as a subsidiary, was recorded as extraordinary income.

- The year-end dividend forecast was revised up by 7 JPY to 50 JPY per share, leading to a total annual dividend forecast of 72 JPY per share (an increase of 34 JPY from the previous fiscal year).

🤖 AI Perspective

- Shimizu Corporation’s upward revision across all key consolidated earnings metrics, particularly the significant increase in profit attributable to owners of parent, suggests a broad improvement in operational performance.

- The company’s announcement indicates that both core business progress in domestic construction and enhanced profitability in subsidiaries, alongside a one-time gain from a bargain purchase, contribute to the improved outlook.

- The revised dividend forecast, aligned with a target consolidated payout ratio of 40%, could be seen as a reflection of the improved earnings being returned to shareholders.

2737|トーメンデバ

11820.0

▼ -3.75%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tomen Devices Corporation announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- For the reported fiscal year, consolidated net sales were ¥633,668 million (up 50.3% year-on-year), operating profit was ¥18,784 million (up 84.7%), ordinary profit was ¥13,322 million (up 80.6%), and profit attributable to owners of parent was ¥10,015 million (up 79.2%).

- The annual dividend for the fiscal year ended March 2026 is ¥540 per share (total of ¥540 including year-end dividend), compared to ¥300 for the previous fiscal year.

- For the fiscal year ending March 2027, the company forecasts consolidated net sales of ¥750,000 million (up 18.4% year-on-year), operating profit of ¥18,200 million (down 3.1%), ordinary profit of ¥14,500 million (up 8.8%), and profit attributable to owners of parent of ¥11,000 million (up 9.8%).

- Total consolidated assets amounted to ¥344,957 million (up 202.7% from the previous fiscal year-end), and net assets were ¥59,237 million (up 19.4%).

🤖 AI Perspective

The significant growth in net sales and profits for FY2026 suggests strong operational performance, potentially driven by increased demand in server, storage, and automotive segments, alongside rising memory product prices. While the FY2027 forecast projects continued sales growth, the slight anticipated decrease in operating profit could be an area for investors to monitor.

3739|コムシード

—

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- CommSeed Corporation’s Board of Directors resolved on April 24, 2026, to form a capital and business alliance with BAMBOO NETWORK Co., Ltd., a short drama studio based in South Korea.

- The business alliance stipulates joint planning and production of new IPs, which will be used to create “FMV games” (interactive games utilizing live-action footage) and short dramas. CommSeed will hold all operating rights for distribution, game adaptation, and secondary use of BAMBOO NETWORK’s content within Japan.

- For the capital alliance, CommSeed will acquire 8,685 shares of BAMBOO NETWORK’s Redeemable Convertible Preferred Stock for 999,973,530 Korean Won, resulting in a 2.1% stake post-acquisition.

- BAMBOO NETWORK is a leading short drama studio in South Korea, having recently received a post-money valuation of 47 billion Korean Won (approximately 5.1 billion Japanese Yen) in its latest investment round.

- The stock acquisition is scheduled for April 30, 2026, and includes investor protection clauses such as prior consent rights for key management matters and a put option in case of contract violation.

🤖 AI Perspective

This alliance positions CommSeed to enter the rapidly expanding global short drama market, potentially leveraging its existing game development and publishing capabilities to establish new revenue streams. The joint creation of IP with BAMBOO NETWORK, a prominent Korean studio, and the development of FMV games could diversify content offerings and enhance CommSeed’s strategic role as BAMBOO NETWORK’s partner in the Japanese market. The capital investment, aimed at strengthening the partnership and realizing future capital gains, may suggest a strategic move for long-term corporate value enhancement.

3912|モバファク

1223.0

▲ +0.25%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Mobile Factory, Inc. announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026 – March 31, 2026) on April 24, 2026.

- For the quarter, consolidated net sales were ¥749 million (up 7.7% year-on-year), EBITDA was ¥209 million (up 16.9% year-on-year), operating profit was ¥209 million (up 17.0% year-on-year), and profit attributable to owners of parent was ¥141 million (up 10.0% year-on-year).

- In the mobile game business segment, net sales reached ¥690,288 thousand (up 9.6% year-on-year) and segment profit was ¥166,171 thousand (up 26.2% year-on-year), attributed to battle events, accessory gacha implementation, and increased promotional activities for its main service “Ekime mo!”.

- The company’s financial position saw total assets decrease by ¥1,098 million from the previous fiscal year-end to ¥2,880 million, and net assets decrease by ¥827 million to ¥2,256 million. This was primarily due to a decrease in cash and deposits from dividend payments, treasury stock acquisition, tax payments, and bonus payments, as well as the cancellation of treasury stock effective March 31, 2026.

- The consolidated full-year earnings forecast for the fiscal year ending December 2026 remains unchanged from the forecast announced on January 29, 2026, with the annual dividend forecast also maintained at ¥51.00 per share.

🤖 AI Perspective

- The consolidated performance indicates strong growth driven by the robust mobile game business.

- While the full-year forecast remains unchanged, the first quarter’s progress appears favorable, suggesting that future business developments will be worth monitoring.

- Actions like treasury stock acquisition, cancellation, and dividend payments reflect a focus on shareholder returns, while a high equity ratio may suggest a sound financial foundation.

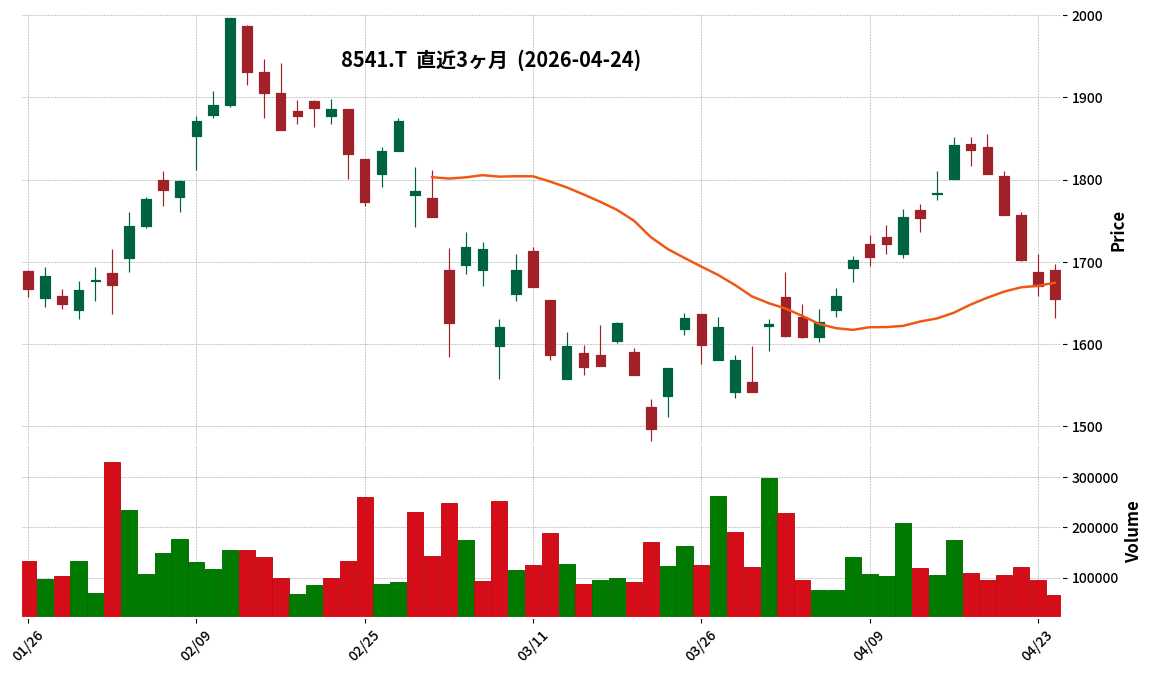

8541|愛媛銀

1655.0

▼ -0.96%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Ehime Bank announced a revision to its consolidated earnings forecast for the fiscal year ending March 31, 2024.

- Concurrently, the forecast for profit attributable to owners of parent was also revised.

- The company announced a revision to its year-end dividend forecast, indicating an increase in the dividend payout.

- As a result, the annual dividend forecast will also be revised.

🤖 AI Perspective

The revision of the earnings forecast may suggest shifts in the bank’s operational performance or financial outlook. Furthermore, the announced dividend increase could be interpreted as a positive signal regarding the company’s commitment to shareholder returns. These developments are likely to be key points for investors evaluating the company’s financial health and shareholder distribution policies.

4765|SBIGアセットM

601.0

▼ -0.17%

📎 Source:SBIGアセットM Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SBI Global Asset Management Co., Ltd. has decided on a year-end dividend of JPY 13.75 per share for the record date of March 31, 2026.

- Combined with the interim dividend of JPY 9.00 per share for the record date of September 30, 2025, the total annual dividend will be JPY 22.75 per share.

- This represents an increase of JPY 0.75 (3.4%) from the JPY 22.00 per share paid in the previous fiscal year, marking 17 consecutive years of dividend increases.

- The effective date for the year-end dividend is June 1, 2026, with the source of funds being retained earnings.

- This dividend level remains unchanged from the forecast announced by the company on February 20, 2026.

🤖 AI Perspective

- The announcement of 17 consecutive years of dividend increases may suggest the company’s consistent commitment to shareholder returns as a key management priority.

- Robust consolidated results for the fiscal year ended March 2026, including 14 consecutive years of revenue growth and 17 consecutive years of operating income growth, appear to underpin this dividend decision.

- Strategic organizational restructuring and the strong performance of key subsidiaries could be seen as factors contributing to the company’s strengthened management foundation and potential for continued earnings stability.

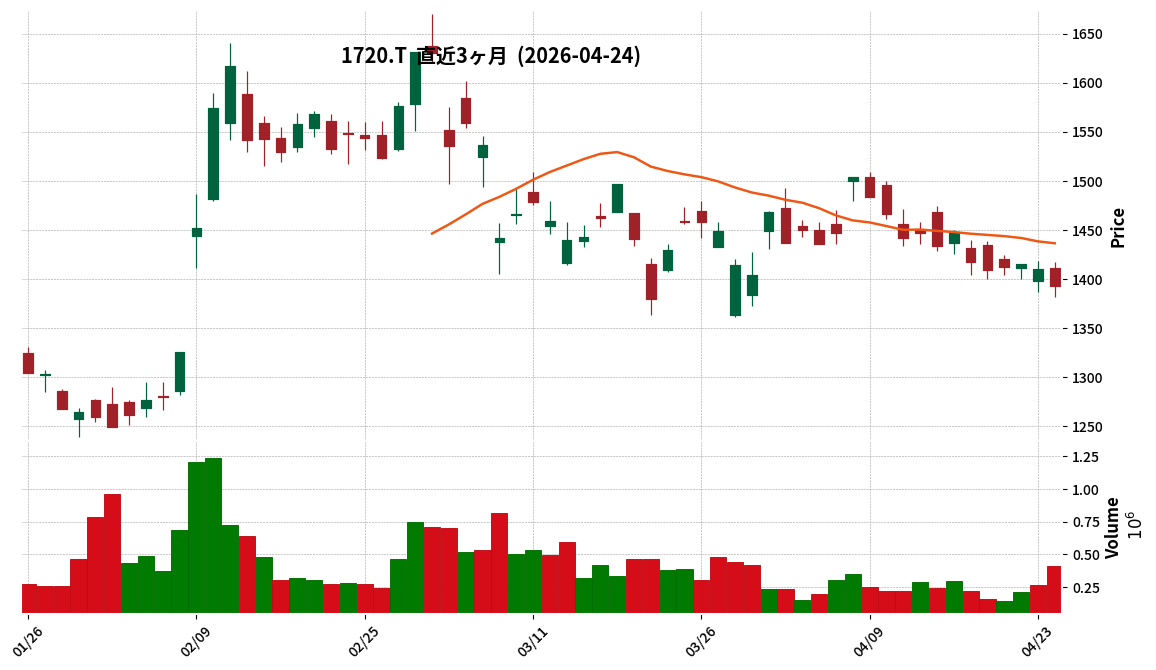

1870|矢作建

2006.0

▼ -1.81%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Yahagi Construction Co., Ltd. announced on April 24, 2026, a revision of its full-year consolidated earnings forecast and dividend forecast for the fiscal year ending March 2026.

- For the full-year consolidated earnings forecast for FY2026/3, the company revised its operating profit upward from ¥11,500 million to ¥13,700 million (a 19.1% increase) and profit attributable to owners of parent from ¥7,000 million to ¥8,400 million (a 20.0% increase). Net sales remained unchanged at ¥168,000 million.

- The reasons for the earnings forecast revision include progress in signing additional/amended contracts due to rising material costs in the late stages of construction projects and increased contract amounts from design change negotiations and cost reductions through budget reviews in the civil engineering business.

- The annual dividend forecast for FY2026/3 was revised, with the year-end dividend increased from ¥45.00 to ¥55.00 per share, resulting in a total annual dividend of ¥100.00 per share, including the interim dividend of ¥45.00.

- The dividend forecast revision is based on the company’s fundamental policy of continuous and stable shareholder returns, targeting a “DOE (Dividend on Equity) of 5% or more and progressive dividends,” and reflects the revised full-year consolidated earnings forecast.

🤖 AI Perspective

Yahagi Construction’s upward revision of its earnings forecast may suggest that the company effectively managed rising material costs in its construction segment and achieved improved profitability in its civil engineering projects. The increased dividend, aligned with the company’s policy of “DOE of 5% or more and progressive dividends,” could indicate a strong commitment to shareholder returns supported by robust performance. This consistent approach to profit distribution may be a point of interest for investors.

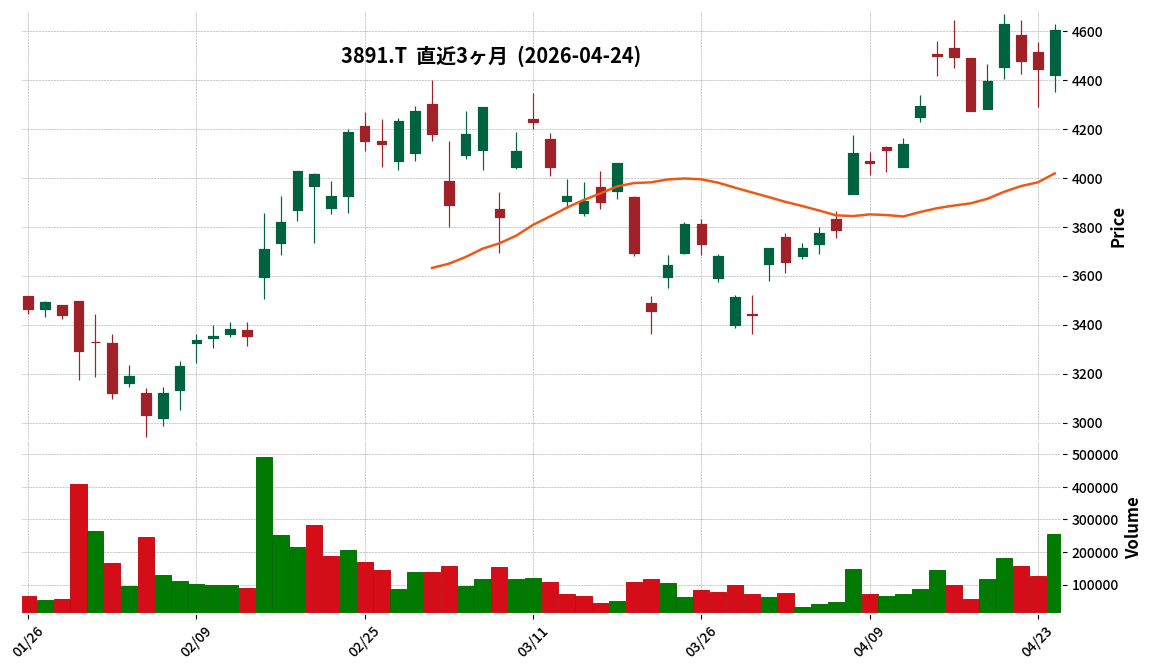

3891|高度紙

4605.0

▲ +3.60%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nippon Kodoshi Corporation’s Board of Directors resolved on April 24, 2026, to revise its dividend forecast (upward revision) for the fiscal year ending March 31, 2026.

- The year-end dividend forecast for the fiscal year ending March 2026 has been revised to JPY 50 per share, an increase of JPY 10 from the previous forecast of JPY 40 per share.

- Consequently, the annual dividend forecast for the fiscal year ending March 2026, including the interim dividend of JPY 40, is revised to JPY 90 per share, an increase of JPY 10 from the previous forecast of JPY 80 per share.

- The company stated that this revision is a result of comprehensively considering its shareholder return policy, which targets a consolidated payout ratio of 40% and a minimum consolidated Dividend on Equity (DOE) of 3%, along with its current financial situation.

- The formal decision on the year-end dividend for the fiscal year ending March 2026 is scheduled to be made at the Board of Directors meeting concerning financial results in May and approved at the Ordinary General Meeting of Shareholders planned for June of this year.

🤖 AI Perspective

This revised dividend forecast indicates Nippon Kodoshi Corporation’s commitment to its established shareholder return policy, which aims for a consolidated payout ratio of 40% and a minimum consolidated DOE of 3%. The increase of JPY 30 in the annual dividend compared to the previous fiscal year’s actual result may suggest a consistent focus on providing stable returns to shareholders. While the final decision awaits approval at the upcoming general shareholders’ meeting, this announcement could be a key factor for investors assessing the company’s capital allocation strategy.

4973|高純度化

4970.0

▲ +0.81%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 2026, Net Sales amounted to ¥18,073 million (up 43.3% year-on-year), Operating Profit was ¥576 million (up 14.7%), Ordinary Profit ¥776 million (up 18.0%), and Net Profit was ¥1,803 million (up 14.2%).

- The annual dividend for the same period was ¥200.00 (compared to ¥126.00 in the previous period), with the year-end dividend set at ¥137.00.

- For the fiscal year ending March 2027, the company forecasts Net Sales of ¥24,000 million (up 32.8% year-on-year), Operating Profit of ¥610 million (up 5.8%), Ordinary Profit of ¥800 million (up 3.1%), and Net Profit of ¥2,170 million (up 20.3%).

- The projected annual dividend for FY2027/3 is ¥230.00 (interim dividend of ¥115.00, year-end dividend of ¥115.00).

- An earnings briefing for institutional investors and analysts is scheduled for April 24, 2026.

🤖 AI Perspective

Japan Pure Chemical’s financial results for FY2026/3 show substantial year-on-year increases across revenue and various profit metrics. This strong performance appears to be primarily driven by expanded demand for plating chemicals in semiconductor packages and modules, especially those related to generative AI. The company’s outlook for the next fiscal year, projecting continued growth and an increased dividend based on sustained AI infrastructure investment and a recovery in high-end smartphone demand, could indicate a positive trajectory for investors to monitor.

5423|東製鉄

1729.0

▼ -0.40%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tokyo Steel Manufacturing Co., Ltd. announced its non-consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- For FY2026, net sales were ¥268,095 million (down 18.0% year-on-year), operating profit was ¥7,230 million (down 76.0%), ordinary profit was ¥8,632 million (down 72.7%), and net profit was ¥11,557 million (down 45.5%).

- The company declared an annual dividend of ¥50.00 per share for FY2026 (interim ¥25.00, year-end ¥25.00).

- For the upcoming fiscal year ending March 31, 2027, the company forecasts net sales of ¥315,000 million (up 17.5% year-on-year), but projects an operating loss of ¥4,000 million, an ordinary loss of ¥2,500 million, and a net profit of ¥0 million (net loss of ¥0 million).

- The equity ratio improved to 75.8% at the end of the fiscal year (from 71.7% at the end of the previous fiscal year).

🤖 AI Perspective

The significant decline in operating and ordinary profits for FY2026 suggests the challenging market environment for steel products, with falling product prices and increased fixed costs due to lower production volumes. The projection of operating and ordinary losses for FY2027, despite an anticipated increase in net sales, indicates that market uncertainties are expected to persist. However, the improvement in the equity ratio to 75.8% may be seen as a positive sign regarding the company’s financial stability.

3181|買取王国

976.0

▲ +1.35%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- KAITORI OKOKU Co., Ltd. achieved record-high results for the fiscal year ended February 2026, with net sales of ¥9,330 million, operating profit of ¥507 million, and ordinary profit of ¥546 million.

- Net sales have continuously set new records for 48 consecutive months since March 2022.

- During the fiscal year ended February 2026, the company opened 7 new Tool stores, 2 new Myu Shusaga-ru stores, and 2 new KOV stores (one more than planned), and renovated one KAITORI OKOKU (general store) into a Hobby KAITORI OKOKU (specialty store).

- For the fiscal year ending February 2027, the company forecasts net sales of ¥10,012 million (107.3% year-on-year), operating profit of ¥600 million (118.5% year-on-year), ordinary profit of ¥610 million (111.8% year-on-year), and net profit of ¥403 million (112.6% year-on-year).

- Future business expansion initiatives include preparations for opening stores in Southeast Asia and launching cross-border e-commerce within the fiscal year ending February 2027, as well as continued exploration of new business opportunities, including M&A.

🤖 AI Perspective

KAITORI OKOKU’s achievement of record-high sales and profits for the fiscal year ended February 2026, along with its consistent sales growth, is a notable point for investors. The growth appears to be driven by a combination of new store openings, business acquisitions, and increased sales from existing stores. While the gross profit margin decreased due to an increased proportion of precious metals, the improvement in operating profit margin through selling, general and administrative expenses control may indicate effective operational management. The company’s projections for further growth in FY2027/2, supported by overseas expansion, specialization of store formats, and M&A strategies, could be key drivers for future performance.

1814|大末建

3290.0

▼ -0.75%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Daisue Construction Co., Ltd. has revised its consolidated earnings forecast upwards for the fiscal year ending March 2026. The revised forecast projects net sales of JPY 105.5 billion (up 4.5% from previous forecast), operating profit of JPY 6.57 billion (up 28.3%), ordinary profit of JPY 6.6 billion (up 28.7%), and profit attributable to owners of parent of JPY 3.8 billion (up 5.0%).

- The upward revision in consolidated earnings is attributed to strong orders and steady progress in existing projects, leading to increased net sales, as well as an improvement in gross profit margin and reduction in selling, general, and administrative expenses.

- The company announced an increase in its year-end dividend forecast for the fiscal year ending March 2026, from JPY 87 to JPY 96 per share, an increase of JPY 9. This results in an annual dividend of JPY 183 per share, with an expected dividend payout ratio of 50.06%.

- A special loss of approximately JPY 1.4 billion is expected to be recorded in the consolidated financial statements, representing an impairment loss on technology-related assets of its consolidated subsidiary, Kamishima Gumi Co., Ltd.

- In the non-consolidated financial statements, an impairment loss on shares of affiliates totaling approximately JPY 2.8 billion is expected due to a significant decline in the actual value of Kamishima Gumi’s shares. However, this loss will be eliminated in the consolidated financial statements, thus having no impact on consolidated earnings.

🤖 AI Perspective

This announcement indicates that Daisue Construction’s consolidated performance for the fiscal year ending March 2026 is robust, with net sales and all profit metrics exceeding previous forecasts. The decision to increase the dividend, consistent with the company’s policy of a total shareholder return ratio of 50% or more and a DOE of 4.0% or more, could be a key point of interest for investors. While a special loss of approximately JPY 1.4 billion related to a consolidated subsidiary is recognized in the consolidated financial statements, the upward revision of operating and ordinary profits suggests that profit attributable to owners of parent is also projected to increase, indicating a limited impact on the overall consolidated performance.

1972|三晃金

1273.0

▼ -0.93%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sanko Metal Co., Ltd. announced its non-consolidated financial results for the fiscal year ended March 31, 2026, reporting a 3.7% increase in net sales to ¥47,058 million.

- Operating profit declined by 8.1% to ¥3,778 million, ordinary profit by 7.1% to ¥3,843 million, and net profit by 10.1% to ¥2,645 million.

- The company’s equity ratio improved to 68.1% (from 65.4% in the prior year), and the order backlog reached a new record high of ¥36,462 million, up 2.5% from the previous year.

- For the fiscal year ended March 31, 2026, the total annual dividends paid amounted to ¥1,330 million, representing a payout ratio of 50.3%.

- For the fiscal year ending March 31, 2027, the company forecasts net sales of ¥47,000 million (down 0.1% YoY), operating profit of ¥3,500 million (down 7.4% YoY), and net profit of ¥2,450 million (down 7.4% YoY).

🤖 AI Perspective

Sanko Metal’s FY2026 results indicate that while sales grew, profits faced pressure from increased construction costs, manufacturing/construction strengthening expenses, and higher general administrative costs, including those related to head office relocation. However, the record-high order backlog could suggest a robust foundation for future business. The FY2027 forecast anticipates a slight decrease in both sales and profits, which may suggest that market conditions and cost management will be key factors for investors to monitor going forward.

2804|ブルドックソース

1796.0

▼ -0.17%

📎 Source:ブルドックソース Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Bull-Dog Sauce announced on April 24, 2026, an upward revision to its dividend forecast for the fiscal year ending March 2027, specifically an increase in its ordinary dividend.

- The projected annual dividend per share for FY2027 is 45.00 yen, comprising an interim dividend of 20.00 yen and a year-end dividend of 25.00 yen.

- This dividend forecast reflects a 5-yen increase in the ordinary dividend, setting the annual ordinary dividend at 45 yen.

- The company aims for a total shareholder return ratio of 60% as part of its management strategy, focusing on capital cost and share price awareness.

- The interim dividend for FY2027 is scheduled to be proposed at a Board of Directors meeting in November 2026, and the year-end dividend at an Annual Shareholders’ Meeting in June 2027.

🤖 AI Perspective

Bull-Dog Sauce’s decision to increase its ordinary dividend, while maintaining the overall annual payout level, may signal a strong commitment to shareholder returns. The establishment of a 60% total shareholder return ratio target could indicate a management focus on capital efficiency. Investors may view the shift to maintaining returns through ordinary dividends rather than relying on special dividends as a move towards a more stable shareholder return policy.

8059|第一実業

3195.0

▲ +0.63%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Dainippon Jitsugyo Co. has revised upward its consolidated earnings forecast for the fiscal year ending March 2026. Consolidated ordinary profit is now expected to be ¥14,300 million, a 5.9% increase from the previous forecast of ¥13,500 million.

- Net profit attributable to owners of the parent company has been revised upward by 3.1% from ¥9,600 million to ¥9,900 million, with EPS revised from ¥300.84 to ¥310.06.

- Consolidated net sales are projected to decrease by 2.7% from the previous forecast of ¥225,000 million to ¥219,000 million. Non-consolidated net sales are also expected to be lower than previously forecasted.

- The primary reason for the revision is improved profitability across many business segments, including Energy Solutions and Aerospace & Infrastructure, with foreign exchange rate fluctuations having a minor impact.

- The year-end dividend forecast for FY2026 has also been revised, increasing by ¥3 to ¥74 per share from the previous forecast of ¥71. This results in a projected annual dividend of ¥125 per share.

🤖 AI Perspective

This upward revision in the earnings forecast, despite a projected decrease in net sales, highlights an improvement in the company’s profitability. This suggests that efficiency enhancements or a shift towards higher-value activities within its business segments may be contributing factors, as indicated by the company citing “improved profitability” as the main reason. The increased dividend forecast could be viewed as a positive signal regarding the company’s commitment to shareholder returns and confidence in its sustained profit growth.

8395|佐賀銀

5080.0

▲ +0.99%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Saga Bank Co., Ltd. has revised its consolidated ordinary revenue forecast for the fiscal year ending March 2026 (April 1, 2025 – March 31, 2026) upwards from 56,000 million yen to 71,000 million yen (an increase of 15,000 million yen, +26.7%).

- The non-consolidated ordinary revenue forecast for the same period was also revised upwards from 48,000 million yen to 63,000 million yen (an increase of 15,000 million yen, +31.2%).

- The forecasts for consolidated and non-consolidated ordinary profit, profit attributable to owners of parent (consolidated), and net profit (non-consolidated) remain unchanged from the previous announcement.

- The primary reason for the revision of the earnings forecast is the recognition of a gain on sale of shares, following the sale of Hisamitsu Pharmaceutical Co., Inc. shares.

- Ordinary profit and net profit remained unchanged mainly due to the impact of unrealized losses from securities portfolio restructuring, which was funded by the gain on sale of shares.

- The company announced a revision of its year-end dividend forecast for the fiscal year ending March 2026, increasing it by 10 yen per share from 50 yen to 60 yen.

- This revision is expected to result in an annual dividend of 110 yen per share for the fiscal year ending March 2026, including the interim dividend of 50 yen.

🤖 AI Perspective

Saga Bank’s announcement highlights a significant upward revision in consolidated and non-consolidated ordinary revenues, along with an increased year-end dividend. While a one-time gain from the sale of shares significantly improved ordinary revenues, the decision to allocate these profits towards portfolio restructuring resulted in unchanged ordinary and net profit forecasts. This strategic allocation may draw investor attention regarding its long-term impact on the bank’s earnings structure. The dividend increase, made within the context of the bank’s public nature and stable dividend policy, could be interpreted as a positive signal towards shareholder returns.

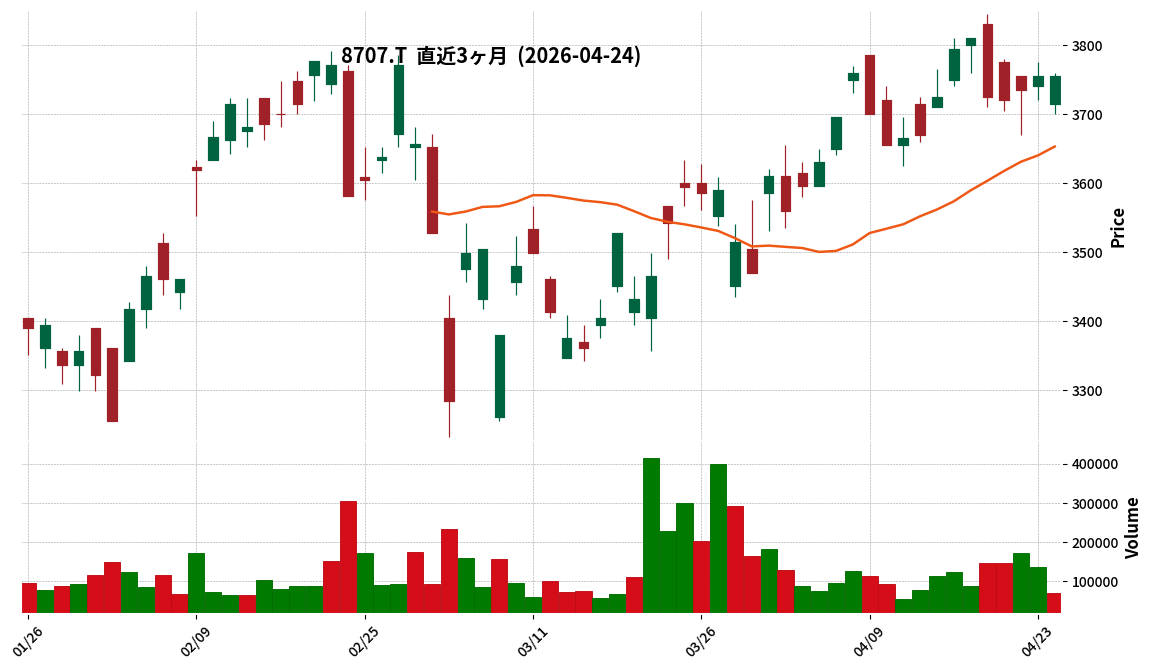

8707|岩井コスモ

3755.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026 (consolidated), operating revenue reached ¥32,260 million, representing a 25.3% increase compared to the previous fiscal year.

- Net profit attributable to owners of parent was ¥10,443 million, marking a significant 55.3% increase year-over-year.

- Basic earnings per share (EPS) for the period stood at ¥444.61.

- The annual dividend for FY2026 was set at ¥225 per share (up from ¥145 in the prior year), with total dividends amounting to ¥5,284 million.

- The consolidated earnings forecast for the fiscal year ending March 31, 2027, has not been disclosed due to the significant influence of economic and market fluctuations.

🤖 AI Perspective

Iwai Cosmo Holdings reported substantial growth in both operating revenue and net profit attributable to owners of parent for FY2026. The 55.3% increase in net profit is a notable highlight that may suggest robust operational performance. Furthermore, the significant increase in the annual dividend could indicate the company’s commitment to enhancing shareholder returns.

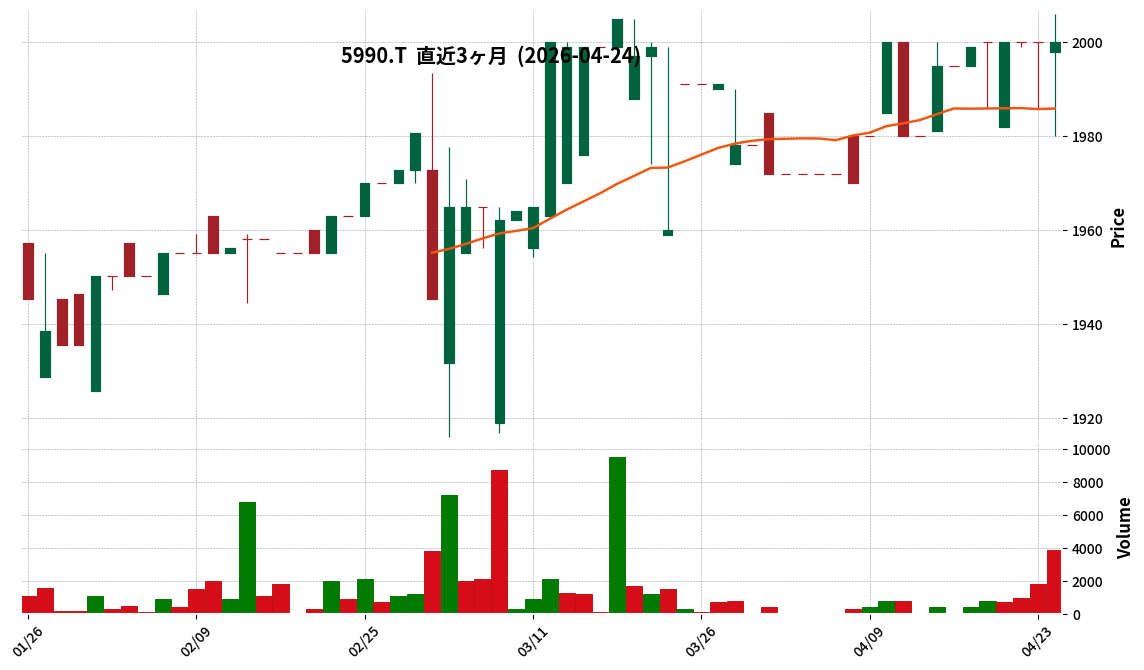

5990|スーパーツール

2000.0

▲ +0.00%

📎 Source:スーパーツール Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 2026, consolidated net sales reached ¥5,437 million, representing a 3.7% increase compared to the previous fiscal year.

- Consolidated operating profit for FY2026 was ¥287 million (a 23.7% decrease year-on-year), and ordinary profit was ¥300 million (a 20.6% decrease year-on-year).

- Net profit attributable to owners of parent for FY2026 turned positive at ¥198 million, compared to a loss of ¥238 million in the previous fiscal year.

- The annual dividend for FY2026 is set at ¥70.00 (¥35.00 for year-end), and for FY2027 (forecast), the annual dividend is projected to be ¥60.00 (¥30.00 for year-end).

- For the fiscal year ending March 2027, the company forecasts consolidated net sales of ¥5,500 million (up 1.2% year-on-year), operating profit of ¥390 million (up 35.5% year-on-year), and net profit attributable to owners of parent of ¥170 million (down 14.3% year-on-year).

🤖 AI Perspective

While Supertool reported an increase in net sales for FY2026, the decline in operating and ordinary profits is a notable aspect. However, the company successfully returned to profitability for net profit attributable to owners of parent. The forecast for FY2027, projecting a significant recovery in operating and ordinary profits alongside a slight increase in sales, may be a key focus for investors. Additionally, the announced withdrawal from the environmental business and changes in accounting policies could influence the future business structure.

6345|アイチ

1351.0

▼ -0.37%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Aichi Corporation announced its consolidated financial results for the fiscal year ended March 31, 2026, reporting net sales of ¥59,613 million (+0.5% year-on-year) and net income attributable to owners of parent of ¥6,658 million (+5.1% year-on-year).

- Segment-wise, net sales for Special Purpose Vehicles decreased by 3% to ¥44,652 million, while Parts and Repair sales increased by 11% to ¥14,061 million.

- The annual dividend for the fiscal year ended March 31, 2026, was set at ¥60.00 per share (interim ¥30.00, year-end ¥30.00), an increase from ¥55.00 in the previous fiscal year.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥63,000 million (+5.7% year-on-year) and net income attributable to owners of parent of ¥6,700 million (+0.6% year-on-year). The projected annual dividend is ¥65.00 per share (interim ¥33.00, year-end ¥32.00).

- Total number of shares outstanding (including treasury stock) at March 31, 2026, was 64,570,000 shares, a decrease from 74,570,000 shares at March 31, 2025.

🤖 AI Perspective

Aichi Corporation’s FY2026 results show a stable performance with increases in both net sales and net income, which may suggest resilience despite challenging economic conditions. The growth in the Parts and Repair segment, offsetting a decline in Special Purpose Vehicle sales, could indicate a strategic shift or growing demand for after-sales services. The announced dividend increase for FY2026 and the projected further increase for FY2027 are noteworthy and may be viewed as a commitment to shareholder returns.

7102|日車輌

3515.0

▼ -2.77%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, consolidated results show net sales of ¥99,971 million (up 3.8% year-on-year), operating profit of ¥11,615 million (up 67.5%), ordinary profit of ¥11,986 million (up 64.2%), and profit attributable to owners of parent of ¥11,661 million (up 81.8%).

- The annual dividend for FY2026/3 was increased to ¥45.00 (from ¥35.00 in the previous fiscal year), and the forecast for FY2027/3 is ¥50.00.

- The consolidated earnings forecast for FY2027/3 projects net sales of ¥107,000 million (up 7.0% year-on-year), but operating profit of ¥8,800 million (down 24.2%), ordinary profit of ¥9,300 million (down 22.4%), and profit attributable to owners of parent of ¥7,500 million (down 35.7%).

- In the segment overview, the Railway Rolling Stock business reported sales of ¥48,556 million (up 8.5% year-on-year), driven by contributions from N700S Shinkansen trains and 315 series trains for JR Central, among others.

- A significant change in the scope of consolidation includes the exclusion of “NIPPON SHARYO MANUFACTURING,LLC” during the fiscal year.

🤖 AI Perspective

The strong performance in FY2026/3, with significant profit increases, may suggest successful operational efficiency and revenue growth, particularly in the Railway Rolling Stock business. However, the FY2027/3 forecast indicates an expected decline in profits despite projected revenue growth, which could point to anticipated cost pressures or changes in project mix worth monitoring. The proposed consecutive dividend increases for FY2026/3 and FY2027/3 may signal a consistent commitment to shareholder returns.

7422|東邦レマック

421.0

▲ +0.48%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Toho Lamac announced its non-consolidated financial results for the first quarter of the fiscal year ending December 2026 (December 21, 2025, to March 20, 2026).

- Net sales were 1,143 million yen (down 0.7% year-on-year), operating loss was 20 million yen (compared to an operating loss of 30 million yen in the prior-year quarter), ordinary loss was 56 million yen (compared to an ordinary loss of 18 million yen), and net loss for the quarter was 57 million yen (compared to a net loss of 19 million yen).

- By segment, the Shoes Business recorded net sales of 1,105 million yen (down 2.2% year-on-year), while the Real Estate Business recorded net sales of 37 million yen (up 81.0% year-on-year).

- As of the end of the first quarter of FY2026, total assets stood at 6,940 million yen, net assets at 4,432 million yen, and the equity ratio at 63.9%.

- The full-year earnings forecast (net sales of 5,104 million yen, net income of 71 million yen) and annual dividend forecast (11.40 yen) remain unrevised from the latest public announcement.

🤖 AI Perspective

While Toho Lamac’s Q1 results showed a slight decrease in net sales, the operating loss narrowed due to reduced selling, general and administrative expenses from the restructuring of unprofitable businesses. However, the ordinary loss and net loss for the quarter expanded, primarily due to a decrease in non-operating income and the recording of cryptocurrency valuation losses and special investigation expenses. Within the core Shoes Business, performance varied, with women’s and men’s shoes struggling, but the Real Estate business and sneakers segment demonstrating notable growth, which may suggest a shift in business focus.

1436|G-グリーンエナジー

4115.0

▲ +4.18%

📎 Source:G-グリーンエナジー Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Green Energy Co., Ltd. announced on April 24, 2026, adjustments to its conversion prices, exercise prices, and other terms following a stock split.

- The stock split involves dividing ordinary shares at a ratio of 1 share into 3 shares, with the record date set for April 30, 2026, and an effective date of May 1, 2026.

- The conversion price for the 1st unsecured convertible bond will be adjusted from JPY 2,193 to JPY 731.

- For the 7th stock acquisition rights, the exercise price per share will be adjusted from JPY 2,284 to JPY 761.3, and the number of shares subject to each right will change from 100 shares to 300 shares.

- These adjustments will apply to conversion requests and the exercise of stock acquisition rights made from May 1, 2026, onwards.

🤖 AI Perspective

These adjustments are a standard procedure following a stock split, aiming to maintain the economic value of existing convertible bonds and stock acquisition rights. Investors holding these instruments will see their conversion and exercise terms updated to reflect the increased number of shares post-split. This ensures that the terms are fair and consistent with the company’s capital structure changes, providing clarity for future exercises.

3932|アカツキ

2808.0

▲ +0.14%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Akatsuki Inc. resolved at its Board of Directors meeting on April 24, 2026, to acquire all shares of Groove Holdings Inc. (GHD), making it a subsidiary.

- Through this acquisition, Groove Direction Inc. (GD), a wholly-owned subsidiary of GHD, is scheduled to become a consolidated sub-subsidiary of Akatsuki.

- The acquisition price for GHD common shares is ¥4,500 million, with advisory fees and other related costs (estimated) totaling ¥168 million, for a grand total of approximately ¥4,668 million.

- The share transfer execution date is scheduled for April 30, 2026.

- GD has an established track record in planning and manufacturing artist live goods and has expanded its business into related areas such as anime and VTuber merchandise.

🤖 AI Perspective

This acquisition suggests Akatsuki’s strategy to expand its engagement in the growing IP-driven merchandise and event market, leveraging GD’s expertise in real goods manufacturing. Integrating GD’s capabilities with Akatsuki’s IP creation and marketing strengths could enhance the value of their existing IPs and improve fan engagement. This move appears consistent with Akatsuki’s vision for diversified business development. The full financial impact on Akatsuki’s consolidated performance for the fiscal year ending March 2027 is currently under review, which may be a key point for investors to monitor.

2134|キタハマキャピタル

30.0

▼ -3.23%

📎 Source:キタハマキャピタル Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- On April 24, 2026, Kitahama Capital Partners Co., Ltd. resolved at its Board of Directors meeting to make DIA Food Management LLC a consolidated subsidiary and commence a new restaurant business.

- The new restaurant business is scheduled to start in May 2026, aiming to capture inbound demand, promote regional revitalization, expand business domains, and strengthen the group’s overall revenue base.

- A renowned chef with experience in famous French restaurants and highly-rated domestic establishments will be brought in as an external partner to lead the business.

- Approximately JPY 90 million is anticipated for the restaurant’s opening costs, which will be funded through the company’s own capital.

- This initiative is projected to contribute JPY 166 million in sales to the consolidated results for the fiscal year ending March 2027, which will be included in the financial forecast to be announced on May 15, 2026.

🤖 AI Perspective

This announcement suggests Kitahama Capital Partners is strategically expanding its business scope beyond traditional investment activities, directly entering the hospitality sector with a focus on growing inbound tourism and regional revitalization trends. The recruitment of an experienced chef and the plan to integrate the restaurant business with existing golf courses and future accommodations could indicate an intent to enhance service quality and create synergistic value within the group. Investors may wish to monitor the operational performance of the newly consolidated subsidiary and the updated financial forecasts.

2481|タウンニュース

699.0

▲ +1.30%

📎 Source:タウンニュース Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Townnews Co., Ltd. (Code 2481) announced its non-consolidated financial results for the third quarter of FY2026 (July 1, 2025 – March 31, 2026).

- For the nine months ended March 31, 2026, net sales were ¥3,152 million (up 10.6% year-on-year), operating profit was ¥608 million (up 25.8%), ordinary profit was ¥652 million (up 10.9%), and quarterly net profit was ¥431 million (up 10.8%).

- As for the financial position, total assets stood at ¥6,329 million and net assets at ¥5,547 million, with an equity ratio of 87.6%. Key changes include an increase of ¥368 million in investment securities, ¥191 million in accounts receivable, and ¥148 million in cash and deposits.

- While paper media sales slightly decreased year-on-year, overall sales and profits increased due to solid performance in promotion-related, digital-related, and PPP (Public-Private Partnership) businesses. Specifically, the timing of non-paper business projects concentrating at the fiscal year-end contributed to sales growth in Q3.

- The full-year earnings forecast and the annual dividend forecast of ¥20.00 per share, as announced on August 15, 2025, remain unchanged.

🤖 AI Perspective

Townnews’ strategy of diversifying beyond its core paper media business into digital and PPP ventures appears to be contributing to its revenue and profit growth in the third quarter. The company’s high equity ratio of 87.6% relative to total assets could indicate a strong financial foundation. Investors may look to monitor the progress against the full-year forecast and the potential impact of the newly launched “JichiCa” digital service on April 1st.

2801|キッコマン

1434.0

▼ -1.04%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kikkoman Corporation announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025, to March 31, 2026) on April 24, 2026.

- For the period, consolidated revenue was 745,539 million JPY, representing a 5.2% increase from the previous fiscal year, and business profit reached 79,512 million JPY, a 2.9% increase year-on-year.

- Profit attributable to owners of the parent company amounted to 61,615 million JPY, a slight decrease of 0.1% compared to the previous fiscal year.

- The annual dividend for the fiscal year ended March 31, 2026, was 25.00 JPY per share, comprising an interim dividend of 10.00 JPY and a year-end dividend of 15.00 JPY.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated revenue of 799,100 million JPY (up 7.2% YoY), business profit of 82,300 million JPY (up 3.5% YoY), and profit attributable to owners of the parent company of 61,300 million JPY (down 0.5% YoY).

🤖 AI Perspective

While Kikkoman reported increases in revenue and business profit, the slight decrease in profit attributable to owners of the parent company in the current fiscal year may be a point of interest for investors examining profitability. The forecast for the fiscal year ending March 31, 2027, indicates continued revenue and business profit growth, yet projects another slight decrease in net profit attributable to owners, which could warrant closer examination of the underlying factors.

3236|プロパスト

333.0

▼ -0.89%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Propast Co., Ltd. disclosed the financial results of its non-listed parent company, Shinoken Group Co., Ltd., for the fiscal year ended December 31, 2025 (from January 1, 2025, to December 31, 2025) on April 24, 2026.

- Shinoken Group Co., Ltd. reported consolidated net sales of ¥130,975,299 thousand and consolidated operating profit of ¥10,727,112 thousand for the fiscal year ended December 2025.

- The company’s consolidated ordinary profit for the same period was ¥10,483,664 thousand, and net profit attributable to parent company shareholders amounted to ¥4,921,888 thousand.

- As of December 31, 2025, Shinoken Group’s consolidated balance sheet shows total assets of ¥71,124,308 thousand, total net assets of ¥29,764,802 thousand, and total shareholders’ equity of ¥29,435,239 thousand.

- As of November 30, 2025, Shinoken Group directly holds 37.43% of Propast Co., Ltd.’s voting rights and dispatches five officers to Propast.

🤖 AI Perspective

The disclosure of a non-listed parent company’s financial results by its listed subsidiary, Propast, is considered important for investors to understand the control situation by the non-listed parent. Clarification of the parent company’s consolidated performance and financial status may provide insights into the overall health and operational backdrop of the entire group. The established capital and personnel relationships with Propast are also noteworthy, potentially enhancing transparency in group governance.

3762|テクマト

1835.0

▲ +0.11%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tecmatrix Corporation and its consolidated subsidiary PSP Corporation have reached an agreement with shareholders for the acquisition of shares in Medmain Inc.

- Through this share acquisition, Medmain Inc. is expected to become a consolidated subsidiary of Tecmatrix.

- The total acquisition price is approximately JPY 2.3 billion, with PSP contributing approximately JPY 1.14 billion and Tecmatrix contributing approximately JPY 1.16 billion.

- Tecmatrix will acquire 8,427 shares of common stock, 14,077 shares of S-class preferred stock, and 22,867 shares of A-class preferred stock of Medmain. PSP will acquire 7,145 shares of common stock, 19,864 shares of S-class preferred stock, and 17,295 shares of A-class preferred stock.

- The agreement date for the share transfer is April 24, 2026, and the scheduled execution date (effective date) for the share transfer is April 30, 2026 (the actual execution date may vary for individual shareholders).

🤖 AI Perspective

This announcement marks a progression from the basic agreement disclosed in February 2026, indicating the concretization of Tecmatrix Group’s business strategy. The consolidation of Medmain Inc. could be viewed as part of Tecmatrix Group’s efforts to strengthen its business portfolio in the medical and healthcare sectors. Potential synergies between the two companies in the future may be a point of interest for investors.

4056|G-ニューラル

307.0

▼ -0.32%

📎 Source:G-ニューラル Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Neural Group Inc. (G-Neural, stock code: 4056) announced the termination of its business alliance agreement with Sony Corporation, effective April 25, 2026.

- The alliance, originally disclosed on April 26, 2023, encompassed cooperation in signage-related businesses, AI-based human behavior detection businesses, and personnel exchange.

- The termination was decided by mutual agreement, considering the progress of research and development and the optimal allocation of both companies’ management resources.

- G-Neural stated that this termination is based on the strategic judgment of both companies.

- G-Neural anticipates that the impact of this termination on its consolidated financial performance will be minor.

🤖 AI Perspective

This termination of the business alliance may suggest a strategic realignment by both companies. G-Neural’s stated focus on the social implementation of AI cameras and digital signage, alongside M&A for business expansion, indicates a concentrated effort on its core strategies. The assessment of a minor impact on consolidated financial performance is a key point for investors to monitor.

4307|NRI

5092.0

▲ +0.33%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, NRI reported consolidated revenue of JPY 814,708 million, marking a 6.5% increase from the previous fiscal year.

- Operating profit, however, decreased by 56.8% to JPY 58,273 million, and profit attributable to owners of parent declined by 83.7% to JPY 15,257 million.

- Business profit, which excludes temporary factors such as impairment losses on goodwill and fixed assets, increased by 16.3% year-on-year to JPY 156,673 million.

- The annual dividend for FY2026/3 was JPY 77.00 per share, an increase of JPY 14 from the previous fiscal year, with a consolidated payout ratio of 289.9%.

- The consolidated earnings forecast for FY2027/3 projects revenue of JPY 850,000 million (+4.3% YoY), operating profit of JPY 175,000 million (+200.3% YoY), and profit attributable to owners of parent of JPY 119,000 million (+679.9% YoY), with an annual dividend of JPY 84.00 per share.

🤖 AI Perspective

While NRI’s revenue grew in FY2026/3, a substantial decline in operating profit and profit attributable to owners of parent was observed. This significant reduction in profits appears to be primarily driven by temporary factors, such as impairment losses on goodwill and fixed assets, given that business profit (excluding these factors) actually increased. The strong recovery projected for FY2027/3 in both revenue and profits may suggest that the underlying business performance is expected to normalize, which could be a key focus for investors.

4571|G-NANO

141.0

▼ -1.40%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- NANO MRNA Co., Ltd., a strategic subsidiary of G-NANO (NANO Holdings Co., Ltd.), resolved at its Board of Directors meeting on April 24, 2026, to make Luna RD Co., Ltd. a consolidated subsidiary.

- NANO MRNA Co., Ltd. will subscribe to a third-party allotment of shares by Luna RD Co., Ltd., acquiring 200,040 common shares for JPY 200,040,000, resulting in a voting rights ownership of 66.67%.

- Luna RD Co., Ltd. possesses next-generation LNP (Lipid Nanoparticle) technology, including patents for novel ionized lipids and unique technology to prepare LNPs without using PEG (polyethylene glycol).

- The purpose of this share acquisition is to strengthen NANO MRNA’s platform technology foundation, intending to acquire patents held by Luna RD and the know-how of its founder, Professor Tomohiro Asai.

- The company states that Luna RD’s LNP technology is expected to generate sales relatively early through providing solutions to pharmaceutical companies and other entities.

🤖 AI Perspective

This acquisition underscores the strategic importance of LNP delivery technology and intellectual property in the nucleic acid drug sector for enhancing corporate competitiveness. The integration of Luna RD’s patented technology into NANO MRNA’s platform could lead to new revenue opportunities and expanded business collaborations. Consequently, this move may suggest an expected contribution to the long-term strengthening of the technology base and business growth.

5609|日鋳造

907.0

▲ +3.89%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)