📌 Today’s Highlights

Today we cover 54 IR announcements. Notable among them: 山洋電気 (6516), キムラユニティー (9368), 杉本商事 (9932). Use the table of contents below to navigate to each company.

- 441A|G-NE

- 336A|G-ダイナミクマップ

- 6516|山洋電気

- 9368|キムラユニティー

- 9932|杉本商事

- 3003|ヒューリック

- 7326|G-SBIインシュ

- 8628|松井証

- 2288|丸大食

- 6999|KOA

- 3778|さくらインターネット

- 8190|ヤマナカ

- 9979|大庄

- 4735|京進

- 2031|ハンセンブル

- 5410|合同鉄

- 5992|中央発条

- 6436|アマノ

- 8370|紀陽銀行

- 4507|塩野義薬

- 2286|林兼産

- 7247|ミクニ

- 1718|美樹工業

- 173A|G-ハンモック

- 1944|きんでん

- 2211|不二家

- 2327|NSSOL

- 2689|オルバヘルスケアHD

- 3796|いい生活

- 4498|G-サイバートラスト

- 4503|アステラス薬

- 5612|日鋳鉄管

- 6501|日立

- 6594|ニデック

- 6754|アンリツ

- 6810|マクセル

- 7093|G-アディッシュ

- 1960|サンテック

- 2462|ライク

- 3080|ジェーソン

- 3635|コーエーテクモ

- 3636|三菱総研

- 3967|G-エルテス

- 6092|エンバイオHD

- 6908|イリソ電子工業

- 6988|日東電

- 7278|エクセディ

- 7327|第四北越FG

- 8362|福井銀

- 9211|G-エフ・コード

- 558A|G-SQUEEZE

- 8059|第一実業

- 9697|カプコン

- 3856|Abalance

441A|G-NE

615.0

▲ +0.65%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-NE announced the initial selection of products to be offered on its dedicated shareholder website as part of the shareholder benefit program, previously announced on February 20, 2026.

- Examples of products include “shirousagi Double Fromage” from Inabaen Co., Ltd., “Yokohama Beer Can Beer 6 Varieties Tasting Set” from Yokohama Beer, and “2 Eels Kabayaki from Kagoshima Prefecture” from Shoku no Tatsujin Co., Ltd.

- The first record date for the shareholder benefit program is April 30, 2026, with subsequent record dates annually on April 30. Shareholders holding 100 shares (1 unit) or more are eligible, and preferential benefits are planned for those who continuously hold shares for three years or longer.

- Benefits will be provided as discount coupons for products from “Next Engine” user companies at discounted prices, along with a QR code for invitation to a dedicated website, mailed annually in July.

- Discount coupon values range from JPY 500 for shareholders holding 100 to less than 300 shares for less than three years, to JPY 4,000 for shareholders holding 1,000 shares or more for three years or longer.

🤖 AI Perspective

This shareholder benefit program is designed to express gratitude to shareholders while also aiming to contribute to the sales of user companies utilizing “Next Engine,” the company’s main service. The initiative may also encourage long-term shareholding and could potentially enhance stock liquidity and market recognition for the company. Further details on additional products and the shareholder benefit guide website are expected to be announced.

336A|G-ダイナミクマップ

701.0

▲ +1.74%

📎 Source:G-ダイナミクマップ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Dynamic Map completed the acquisition of all shares of Ricanos Co., Ltd. on April 1, 2026, making it an indirect consolidated subsidiary, following a Board of Directors resolution on March 27, 2026.

- Ricanos Co., Ltd., located in Yamagata City, Yamagata Prefecture, specializes in BIM/CIM-related operations, photo surveying and analysis using UAVs, and terrestrial laser measurement in the civil engineering and construction sectors.

- The acquisition aims to strengthen G-Dynamic Map’s business foundation and network in the surveying and spatial information fields, aligning with its “Modeling the Earth” vision.

- Ricanos’ capital of 16.5 million JPY represents over 10% of G-Dynamic Map’s capital, necessitating timely disclosure under Tokyo Stock Exchange rules.

- Ricanos’ financial performance for the latest fiscal year (October 2025) reported sales of 165 million JPY, operating income of 12 million JPY, and net income of 1 million JPY. The acquisition price was not disclosed, but advisory fees amounted to 25 million JPY.

🤖 AI Perspective

This acquisition appears to be a strategic move by G-Dynamic Map to enhance its competitive edge in the spatial information and surveying sector. Integrating Ricanos, with its expertise in UAV-based surveying technology, could potentially strengthen the group’s technological capabilities and expand its operational scope. While the impact on consolidated financial results is expected to be minor, the future synergies from this integration may be worth monitoring.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

6516|山洋電気

6000.0

▲ +6.38%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SANYO DENKI resolved to revise its dividend forecast per share for the fiscal year ending March 2026 at a Board of Directors meeting held on April 27, 2026.

- The company revised its year-end dividend forecast for FY2026/3 from the previous forecast of ¥36.67 per share to ¥70.00 per share, representing an increase of ¥33.33 per share.

- In terms of pre-stock split equivalent, the year-end dividend forecast is revised from ¥110.00 per share to ¥210.00 per share.

- The revision is attributed to the solid progress of the business performance against the forecast announced on April 25, 2025, and an updated dividend policy announced on March 19, 2026, focusing on management with an awareness of capital cost and stock price.

- The company conducted a 3-for-1 stock split of its common shares on October 1, 2025.

🤖 AI Perspective

- This dividend increase appears to reflect the company’s solid business performance and its commitment to a new dividend policy focused on capital efficiency and shareholder returns.

- The clear emphasis on enhancing shareholder returns could position the company favorably in the market, making its future initiatives for corporate value improvement noteworthy for investors.

9368|キムラユニティー

887.0

▲ +1.03%

📎 Source:キムラユニティー Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, consolidated net sales reached ¥64,546 million (up 5.6% year-on-year), operating profit was ¥4,957 million (up 7.7% year-on-year), and ordinary profit was ¥5,769 million (up 12.7% year-on-year).

- Net income attributable to owners of parent decreased by 2.9% year-on-year to ¥3,203 million.

- The annual dividend for FY2026/3 was ¥34.00 per share (interim ¥17.00, year-end ¥17.00), with a payout ratio of 43.6%.

- The consolidated earnings forecast for FY2027/3 projects net sales of ¥66,000 million (up 2.3% year-on-year) and net income attributable to owners of parent of ¥3,850 million (up 20.2% year-on-year), with an expected annual dividend of ¥38.00 per share (payout ratio 40.6%).

- The company conducted a 2-for-1 stock split on April 1, 2025, and all per-share figures are calculated assuming this split occurred at the beginning of the respective fiscal years.

🤖 AI Perspective

While net sales, operating profit, and ordinary profit increased in FY2026/3, net income attributable to owners of parent saw a decrease. The addition of a new subsidiary (Changshu Kimushin Logistics Co., Ltd.) to the scope of consolidation during the fiscal year may have influenced the results. The significant recovery in net income projected for FY2027/3, along with an expected dividend increase, could be key points for investors to monitor in evaluating the company’s future performance.

9932|杉本商事

1170.0

▼ -6.25%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sugimoto Shoji Co., Ltd. reported consolidated financial results for the fiscal year ended March 31, 2026, with revenue of ¥350.0 billion, operating profit of ¥12.0 billion, and net profit attributable to owners of parent of ¥8.5 billion.

- Earnings per share (EPS) for FY2026 stood at ¥250.00.

- The annual dividend for FY2026 was ¥120.00 per share (interim ¥60.00, year-end ¥60.00).

- For the fiscal year ending March 31, 2027, the company forecasts consolidated revenue of ¥360.0 billion, operating profit of ¥13.5 billion, and net profit attributable to owners of parent of ¥9.0 billion.

- The projected annual dividend for FY2027 is ¥130.00 per share (interim ¥65.00, year-end ¥65.00).

🤖 AI Perspective

The robust consolidated results for FY2026, showing solid performance across revenue, operating profit, and net profit, may suggest a healthy business environment for Sugimoto Shoji. Furthermore, the positive outlook for FY2027, with anticipated increases in both revenue and profit, coupled with an upward revision in the annual dividend forecast, could indicate the company’s confidence in its future performance and commitment to shareholder returns. These aspects are worth monitoring for investors.

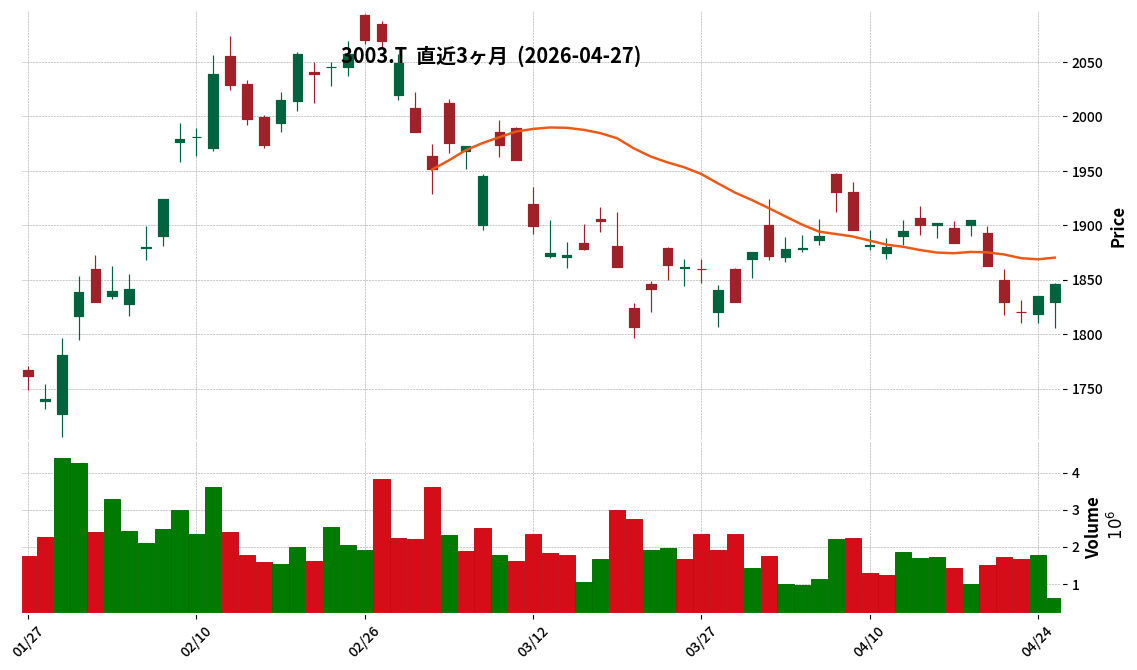

3003|ヒューリック

1846.0

▲ +0.60%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of FY2026, consolidated net sales increased by 44.8% year-on-year to ¥226,841 million.

- Net profit attributable to owners of parent rose by 5.6% year-on-year to ¥18,141 million.

- Operating income was ¥31,171 million (down 2.0% year-on-year), and ordinary income was ¥26,986 million (down 3.6% year-on-year).

- The real estate business recorded net sales of ¥191,360 million (up 43.4% year-on-year) and operating income of ¥38,534 million (up 15.4% year-on-year).

- The full-year dividend forecast for FY2026 remains unchanged from the previous forecast, totaling ¥67.00 (interim ¥33.50, year-end ¥33.50).

🤖 AI Perspective

While consolidated net sales showed a significant increase, operating and ordinary incomes experienced slight declines. This might suggest that despite robust sales growth in the real estate business, cost structures or other factors could have played a role. The increase in net profit attributable to owners of parent is a key positive, and with full-year profit forecasts anticipating growth, the company’s future performance is worth monitoring.

7326|G-SBIインシュ

2098.0

▼ -0.80%

📎 Source:G-SBIインシュ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SBI Insurance Group Co., Ltd. announced preliminary financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026) and a revision to its year-end dividend forecast on April 27, 2026.

- For the fiscal year 2026/3, preliminary operating revenue reached ¥140,362 million (+3.2% compared to previous forecast), ordinary income ¥13,164 million (+12.5%), and net income attributable to owners of parent ¥2,880 million (+2.9%), all exceeding the previously announced forecasts.

- These preliminary figures are expected to set new record highs for operating revenue, ordinary income, net income attributable to owners of parent, and basic earnings per share.

- The year-end dividend forecast for FY2026/3 was revised upwards from the previously announced ¥45.00 to ¥46.50, based on the dividend policy aiming for a consolidated payout ratio of approximately 40%. The total annual dividend will be ¥46.50.

- The consolidated payout ratio, reflecting this revision, is expected to be 40.1%.

🤖 AI Perspective

The preliminary financial results for G-SBI Ins show an upward revision across key performance indicators, including operating revenue and income, which are projected to reach record highs. This performance appears to be driven by a robust increase in insurance policies in force across all segments, suggesting ongoing business expansion. The upward revision of the year-end dividend, adhering to a 40% consolidated payout ratio guideline, could be seen as a consistent approach to shareholder returns.

8628|松井証

943.0

▲ +0.75%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026), operating revenue reached ¥52,660 million, marking a 34.3% increase year-on-year.

- Net profit for the period was ¥15,480 million, representing a significant 47.4% increase compared to the previous fiscal year.

- The annual dividend per share was announced at ¥50.00 (interim ¥25.00, year-end ¥25.00), an increase from ¥40.00 in the prior year.

- Return on Equity (ROE) achieved 19.6%, up from 13.8% in the previous fiscal year.

- Commission income totaled ¥25,963 million (up 30.0% year-on-year), trading gains were ¥5,819 million (up 55.1%), and financial income reached ¥17,306 million (up 29.0%).

🤖 AI Perspective

The substantial increase in operating revenue and various profit metrics may be attributed to a robust domestic stock market and expanded trading activity by individual investors during the period. Specifically, growth in commission income, strong trading gains from FX transactions, and higher financial income due to rising interest rates appear to be key contributors to the overall revenue uplift. The improvement in ROE could indicate progress in enhancing capital efficiency, which is a stated management goal.

2288|丸大食

2194.0

▼ -0.54%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Marudai Food Co., Ltd. announced on April 27, 2026, a revision to its consolidated earnings forecast for the fiscal year ending March 31, 2026.

- The revised consolidated earnings forecast includes net sales of 238,300 million yen (up 0.1% from previous forecast), operating income of 7,500 million yen (up 7.1%), ordinary income of 7,900 million yen (up 6.8%), and profit attributable to owners of parent of 9,700 million yen (up 7.8%).

- Reasons for the revision include steady sales in the processed food business (desserts) and meat business, coupled with price revisions, continuous cost reduction effects, and the recording of gains on sales of investment securities.

- The year-end dividend forecast for the fiscal year ending March 31, 2026, has been revised upward by 5 yen to 70 yen per share, from the previous forecast of 65 yen per share, making the annual dividend 70 yen.

- This dividend revision aligns with the company’s shareholder return policy (minimum 30 yen per share, target of maintaining a total return ratio of 30% or more) and the upward revision of the full-year earnings forecast.

🤖 AI Perspective

The upward revision of the earnings forecast suggests that, in addition to a slight increase in net sales, price revisions and continuous cost reductions significantly boosted profit levels. The expected 7.8% increase in profit attributable to owners of parent over the previous forecast could indicate improved business profitability, potentially aided by the recording of gains on sales of investment securities. The increased dividend payment appears to reflect the company’s policy of aiming for stable shareholder returns, supported by strong consolidated business performance.

6999|KOA

1751.0

▼ -12.93%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026 (FY2025), KOA Corporation reported consolidated net sales of ¥72.29 billion (up 12.7% year-on-year), operating profit of ¥3.65 billion (up 210.0% year-on-year), ordinary profit of ¥5.22 billion (up 320.1% year-on-year), and profit attributable to owners of parent of ¥3.95 billion (an increase of ¥3.69 billion year-on-year).

- By product, resistors accounted for 93% of total sales in FY2025 Q4, increasing 19.1% year-on-year for the same quarter. Geographically, Asia represented 40% of sales, and by application, automotive accounted for 52%.

- For the fiscal year ending March 31, 2027 (FY2026), the company forecasts net sales of ¥77.40 billion (up 7.1% year-on-year). However, operating profit is projected to decrease to ¥2.83 billion (down 22.4% year-on-year) and ordinary profit to ¥3.30 billion (down 36.8% year-on-year).

- The primary factors contributing to the projected decline in operating profit for FY2027 are an increase in material costs (estimated ¥2.2 billion negative impact) and increased fixed costs (estimated ¥1.1 billion negative impact).

- Profit attributable to owners of parent for FY2027 is expected to increase to ¥4.78 billion (up 21.0% year-on-year) due to the recognition of a special gain from the relocation compensation for a factory in China.

🤖 AI Perspective

KOA achieved substantial profit growth across all stages in FY2026, with operating profit more than doubling compared to the previous year. The FY2027 forecast anticipates continued revenue growth, but rising material costs and increased fixed costs are projected to lead to a decline in operating profit. This suggests external factors impacting profitability may warrant attention. However, the inclusion of a special gain from a factory relocation is expected to result in an overall increase in net profit attributable to owners of parent.

3778|さくらインターネット

3645.0

▲ +0.00%

📎 Source:さくらインターネット Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 2026, consolidated net sales increased by 12.4% year-on-year to JPY 35,301 million.

- Consolidated operating profit for the same period turned into a loss of JPY 403 million, compared to a profit of JPY 4,145 million in the previous fiscal year.

- Consolidated ordinary profit decreased by 97.4% to JPY 105 million, and profit attributable to owners of parent declined by 92.6% to JPY 216 million.

- The consolidated earnings forecast for the fiscal year ending March 2027 projects net sales of JPY 45,000 million (up 27.5% year-on-year), operating profit of JPY 1,500 million, and profit attributable to owners of parent of JPY 850 million (up 293.5% year-on-year).

- The year-end dividend for the fiscal year ended March 2026 was JPY 5.00 (total annual dividend JPY 5.00), an increase from JPY 4.00 in the previous year.

🤖 AI Perspective

While sales continued to grow in the fiscal year ended March 2026, increased expenses associated with expanded investment activities appear to have pressured profits. The shift to an operating loss may suggest aggressive upfront investment in business expansion. The significant recovery projected in the earnings forecast for the next fiscal year indicates that the impact of these investments on future profitability will be worth monitoring.

8190|ヤマナカ

—

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the consolidated fiscal year ended March 2026, Yamanaka reported operating revenue of ¥83,238 million (down 1.5% year-on-year) and an operating loss of ¥27 million, a deterioration from the ¥585 million operating profit in the previous year.

- Ordinary income stood at ¥146 million (down 79.9% year-on-year), and net income attributable to owners of parent was ¥102 million (down 65.5% year-on-year).

- The annual dividend for the fiscal year ended March 2026 was ¥10.00 per share, including a year-end dividend of ¥5.00, resulting in a consolidated payout ratio of 186.0%.

- The consolidated performance forecast for the fiscal year ending March 2027 projects operating revenue of ¥90,500 million (up 8.7% year-on-year), operating income of ¥480 million (a return to profit from a loss), ordinary income of ¥520 million (up 254.2% year-on-year), and net income attributable to owners of parent of ¥350 million (up 241.9% year-on-year).

🤖 AI Perspective

The fiscal year ended March 2026 saw a decline to an operating loss, with significant reductions in ordinary and net income. This downturn could be attributed to a challenging operating environment, including rising resource and raw material costs, yen depreciation, persistent consumer frugality, and increased personnel expenses due to minimum wage hikes. Investors may find it noteworthy that the company forecasts a substantial return to profitability and significant earnings growth across all profit categories for the fiscal year ending March 2027, potentially indicating an expectation of improved economic conditions or the effectiveness of ongoing strategic initiatives under their medium-term plan.

9979|大庄

1021.0

▲ +0.59%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the interim period of August 2026, consolidated net sales reached ¥26,617 million, representing a 1.6% increase compared to the same period last year.

- Consolidated operating profit was ¥446 million (-25.5% year-on-year), and net profit attributable to parent company shareholders was ¥367 million (-48.2% year-on-year).

- The Food & Beverage business saw existing store sales increase by 101.8% year-on-year, but operating profit decreased to ¥556 million due to rising raw material costs, among other factors.

- The Wholesale & Logistics business achieved increased revenue and profit, with net sales of ¥17,816 million (+¥703 million year-on-year) and operating profit of ¥504 million (+¥37 million year-on-year), driven by higher external sales.

- As of the end of February 2026, the number of directly managed stores was 229, a decrease from 236 stores at the end of the previous fiscal year’s corresponding period.

🤖 AI Perspective

While consolidated net sales increased, operating profit and net profit attributable to parent company shareholders decreased year-on-year. This appears to be primarily influenced by higher raw material costs impacting the Food & Beverage segment’s profitability, despite robust existing store sales, and an increase in company-wide expenses. The strong performance of the Wholesale & Logistics business, however, contributed to overall revenue growth.

4735|京進

321.0

▼ -0.31%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Segment profit for the language-related business decreased due to the Australian government’s tightened restrictions on international student entry, while domestic Japanese language schools saw increased revenue and profit.

- In the childcare and nursing care business, a significant reduction in caregiver turnover led to cost savings, including recruitment expenses, which is cited as an improvement in operational efficiency.

- The projected revenue and profit growth for the next fiscal year (FY2027/2) is primarily expected to be driven by the full-year contribution (estimated sales of 800-900 million JPY) from Linkheart Co., Ltd., a nursing care facility acquired via M&A in the current period (October 2025).

- The tutorial school business improved profitability through the consolidation of multiple schools into larger centers and operational efficiencies, optimizing staffing and reducing fixed costs such as rent and personnel expenses.

- For its medium-to-long-term strategy, the company plans to position the nursing care business as a core growth driver for the next 10 years, continuing aggressive investments in new facility openings and M&A. Additionally, in the language-related business, it is developing a comprehensive scheme from Japanese language education for local students in Nepal and other regions to talent placement and employment support for Japanese companies.

2031|ハンセンブル

—

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Details regarding the financial status of the guarantor, Nomura Holdings, Inc., for the fiscal year ended March 2026, are referenced to Nomura Holdings, Inc.’s earnings report released on April 24, 2026, with consolidated Common Equity Tier 1 ratio and other metrics to be disclosed separately upon finalization.

- As of April 23, 2026, the guarantor, Nomura Holdings, Inc., holds credit ratings including “BBB+ (Outlook: Positive)” from S&P Global Ratings and “A- (Outlook: Stable)” from Fitch Ratings, as reported by multiple agencies.

- The total self-issued amount of Exchange Traded Notes (ETNs) stands at 247,969 million JPY, representing 6.43% of net assets as of April 23, 2026.

- Between the previous disclosure (January 30, 2026) and March 31, 2026, specific ETNs experienced activity: NEXT NOTES Gold Futures Double Bull ETN saw 100,000 units issued and 90,000 units redeemed; NEXT NOTES Gold Futures Bear ETN had 1,000,000 units issued; and NEXT NOTES Dubai Crude Oil Futures Bear ETN had 10,000,000 units issued.

5410|合同鉄

3580.0

▲ +4.99%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the consolidated fiscal year ended March 31, 2026, Godo Steel reported net sales of ¥191,772 million (down 6.5% YoY), operating profit of ¥9,813 million (down 28.6% YoY), ordinary profit of ¥11,089 million (down 28.1% YoY), and profit attributable to owners of parent of ¥8,051 million (down 28.9% YoY).

- The annual dividend per share for FY2026 was ¥180, a reduction from ¥240 in the previous fiscal year.

- For the consolidated fiscal year ending March 31, 2027, the company projects net sales of ¥200,000 million (up 4.3% YoY), but forecasts declines in profit: operating profit of ¥6,500 million (down 33.8% YoY), ordinary profit of ¥7,000 million (down 36.9% YoY), and profit attributable to owners of parent of ¥4,300 million (down 46.6% YoY).

- Godo Steel anticipates an annual dividend per share of ¥100 for FY2027 (interim ¥40, year-end ¥60).

- The consolidated financial position as of March 31, 2026, showed total assets of ¥255,507 million, net assets of ¥144,249 million, and an equity ratio of 56.3%.

🤖 AI Perspective

The decline in performance for FY2026 appears to be influenced by factors such as a downturn in sales prices and volumes due to sluggish demand, as well as rising electricity costs, material prices, increasing steel scrap prices, and the impact of the depreciating yen. The FY2027 forecast, despite projecting increased sales, suggests that the company anticipates continued challenging market conditions for profitability. Investors may monitor future market developments closely.

5992|中央発条

3745.0

▲ +1.08%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, consolidated net sales reached a record high of 110,868 million yen, marking a 0.6% increase compared to the previous fiscal year.

- Consolidated operating profit decreased by 35.0% to 2,847 million yen, and consolidated ordinary profit declined by 12.7% to 4,496 million yen.

- Net profit attributable to owners of parent surged by 569.4% to 12,420 million yen, primarily driven by a gain of approximately 12.9 billion yen from the sale of investment securities.

- The annual dividend per share increased to 60 yen (from 40 yen in the previous fiscal year), with a forecast of 90 yen for the fiscal year ending March 31, 2027.

- The consolidated outlook for the fiscal year ending March 31, 2027, projects net sales of 110,000 million yen (down 0.8% year-on-year), operating profit of 3,300 million yen (up 15.9% year-on-year), and net profit attributable to owners of parent of 2,400 million yen (down 80.7% year-on-year).

🤖 AI Perspective

The substantial increase in net profit for FY2026 was largely influenced by a one-time gain from the sale of investment securities, while the core operating profit experienced a decline. Management attributed this operating profit decrease to “intentional fixed cost increases” for safety measures, equipment upgrades, and human capital investments, which could be viewed as strategic long-term investments for future growth. The FY2027 forecast indicates a recovery in operating profit, but a significant decrease in net profit, likely reflecting the absence of the previous year’s extraordinary gains.

6436|アマノ

3873.0

▲ +2.06%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026 (FY2026), Amano Co., Ltd. reported consolidated net sales of ¥176,467 million, a 0.6% increase year-on-year. Operating profit decreased by 2.1% to ¥22,551 million, and ordinary profit decreased by 1.2% to ¥24,358 million.

- Net profit attributable to owners of parent achieved a significant increase of 13.0% year-on-year, reaching ¥20,146 million.

- The annual dividend for FY2026 was set at ¥180.00 per share, combining an interim dividend of ¥55.00 and a year-end dividend of ¥125.00, marking an increase of ¥5.00 from the previous year’s ¥175.00. The payout ratio was 62.8%.

- For the fiscal year ending March 31, 2027 (FY2027), the company forecasts consolidated net sales of ¥184,000 million (up 4.3% year-on-year), operating profit of ¥24,000 million (up 6.4%), and ordinary profit of ¥25,600 million (up 5.1%). However, net profit attributable to owners of parent is projected to decline by 12.6% to ¥17,600 million.

- In terms of consolidated financial position, the equity ratio improved from 69.9% at the end of FY2025 to 71.8% at the end of FY2026.

🤖 AI Perspective

The substantial increase in net profit attributable to owners of parent, despite slight declines in operating and ordinary profits, may suggest the influence of non-operating factors or tax effects. The increased annual dividend and improved payout ratio could indicate the company’s commitment to shareholder returns. For the upcoming fiscal year, while sales, operating, and ordinary profits are forecast to grow, the projected decline in net profit attributable to owners of parent is a key point for investors to monitor.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

8370|紀陽銀行

3930.0

▲ +1.16%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kiyo Bank announced on April 27, 2026, revisions to its earnings forecast and year-end dividend forecast for the fiscal year ending March 31, 2026 (April 1, 2025, to March 31, 2026).

- For the consolidated earnings forecast, net profit attributable to parent company shareholders is revised upwards by JPY 3,300 million (17.8%), from the previous forecast of JPY 18,500 million to JPY 21,800 million.

- The revision in the non-consolidated earnings forecast is primarily attributed to higher-than-expected loan interest and securities interest and dividends, as well as lower-than-expected credit costs.

- The year-end dividend forecast for the fiscal year ending March 2026 has been revised upwards by JPY 21.00, from the previously announced JPY 58.00 to JPY 79.00 per share.

- Consequently, the total annual dividend for FY2026 will be JPY 137.00 per share, representing an increase of JPY 27.00 compared to the previous fiscal year (FY2025).

🤖 AI Perspective

- Kiyo Bank’s upward revision suggests that improved profitability and cost management in its standalone banking operations are significantly contributing to its consolidated performance.

- The direct correlation between the upward revision of the earnings forecast and the increased dividend, in line with the bank’s shareholder return policy aiming for a 40% payout ratio, may indicate a consistent commitment to shareholder returns.

- Specific factors driving the revision, such as increased loan interest, higher securities interest and dividends, and reduced credit costs, could point to favorable market conditions or successful operational strategies that warrant further observation.

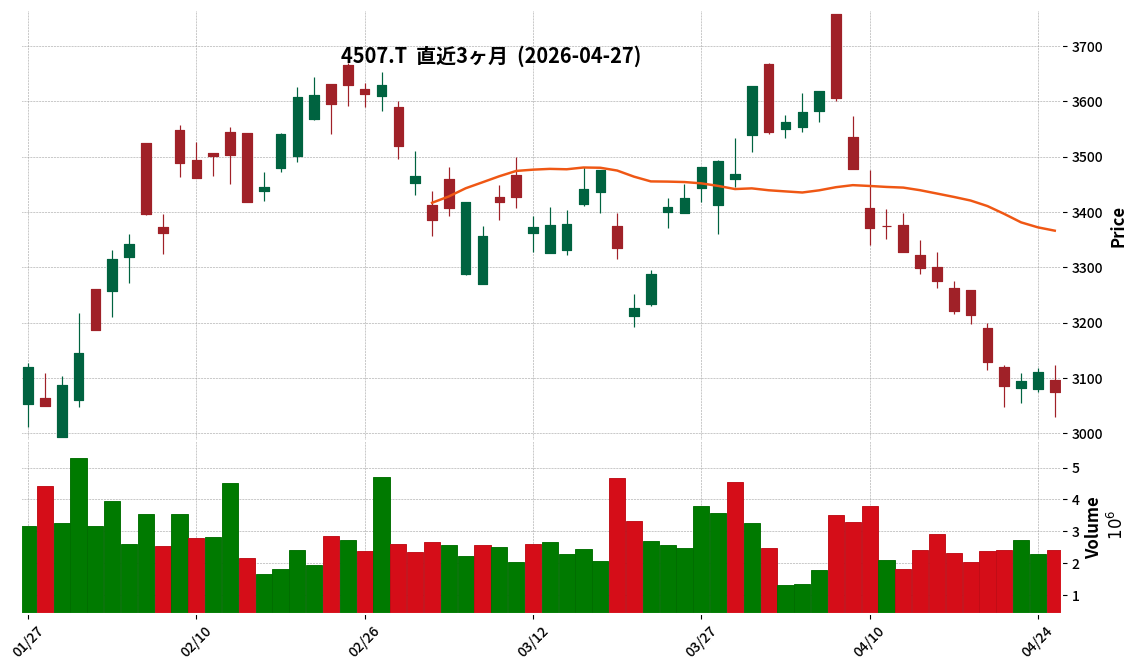

4507|塩野義薬

3099.0

▼ -0.35%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Shionogi & Co., Ltd. announced on April 27, 2026, that its Board of Directors resolved to revise (increase) the year-end dividend forecast for the fiscal year ending March 2026.

- The revised year-end dividend forecast is ¥38.00 per share, an increase of ¥5.00 from the previous forecast of ¥33.00.

- This revision brings the full-year dividend forecast to ¥71.00 per share, including the interim dividend of ¥33.00, an increase of ¥5.00 from the previous forecast of ¥66.00.

- For the fiscal year ended March 2025, the actual full-year dividend (after stock split) was ¥61.00 per share.

- This adjustment is expected to result in Shionogi’s 14th consecutive year of dividend increases.

- The company cited consistent progress in its HIV business, strategic M&A activities (including the JT Group’s pharmaceutical business and the edaravone business acquisition), and overall strong performance in domestic and international operations as reasons for the increase, aligned with its Mid-term Business Plan “STS2030 Revision” and its commitment to a Dividend on Equity (DOE) of 4% or more.

🤖 AI Perspective

- This dividend increase may suggest Shionogi’s commitment to enhancing long-term corporate value and shareholder returns.

- The company’s robust HIV business progress and strategic M&A activities appear to be contributing to stable revenue growth and strengthening its business foundation.

- The expected 14th consecutive year of dividend increases could be viewed by investors as a strong indication of sustained commitment to shareholder returns.

2286|林兼産

877.0

▼ -3.09%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hayashikane Sangyo Co., Ltd. will recognize an extraordinary loss of 481 million yen as an impairment loss on shares of an affiliated company in its individual financial statements for the fiscal year ending March 2026 (April 1, 2025 – March 31, 2026).

- This extraordinary loss results from the impairment processing of shares in Kirishima Dream Farm Co., Ltd., a consolidated subsidiary, after an evaluation determined a decline in its substantive value.

- The aforementioned impairment loss on shares of an affiliated company will be recorded only in the individual financial statements.

- There will be no impact on Hayashikane Sangyo Co., Ltd.’s consolidated financial results, as the loss will be eliminated in the consolidated financial statements.

🤖 AI Perspective

Hayashikane Sangyo’s announcement regarding the impairment of affiliate shares is noteworthy because while it records an extraordinary loss in its individual financial statements, there is no impact on consolidated earnings. This situation suggests that the impairment loss on a consolidated subsidiary is offset during the preparation of consolidated financial statements. Investors may wish to distinguish between the impacts on Hayashikane Sangyo’s individual and consolidated financial performance based on this disclosure.

7247|ミクニ

382.0

▼ -1.80%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Mikuni Co., Ltd. announced on April 27, Reiwa 8 (2026), the postponement of its full-year financial results for the fiscal year ending March Reiwa 8 (2026).

- The reason for the postponement is the discovery of fraudulent activities by an employee of an overseas consolidated subsidiary, with the impact assessment and audit procedures not yet completed.

- Confirmed fraudulent activities include recording fictitious transactions to disguise expenditures, misappropriating funds through improper handling of payment documents, and forging audit-related evidence.

- The financial results, originally scheduled for May 11, have been postponed, and the disclosure period may exceed 50 days after the end of the fiscal year.

- The specifics of the fraudulent acts, their impact amount, period, total damage, and whether past financial statements require correction are currently under investigation, and the impact on financial performance cannot be reasonably calculated at this time.

🤖 AI Perspective

The discovery of fraudulent activities at an overseas consolidated subsidiary may suggest potential challenges within the company’s internal control systems. The postponement of the financial results indicates that significant time is required to identify the full financial impact of the fraud, complete necessary accounting adjustments, and finalize audit procedures. Investors may find the progress of the ongoing investigation and the eventual disclosure of the financial impact to be key areas of focus.

1718|美樹工業

7490.0

▲ +2.74%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Mikikogyo Co., Ltd. announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1 to March 31, 2026).

- Net sales for the period increased by 43.4% year-on-year to ¥12,639 million, and net profit attributable to owners of parent rose by 8.5% year-on-year to ¥581 million.

- Operating profit decreased by 4.8% year-on-year to ¥833 million, while ordinary profit declined by 4.7% year-on-year to ¥820 million.

- The Construction Business segment reported a 77.8% increase in net sales to ¥8,995 million and a 7.1% increase in operating profit to ¥655 million year-on-year.

- The consolidated earnings forecasts for the full fiscal year ending December 2026 and for the second quarter cumulative period remain unchanged from the projections announced on February 13, 2026.

🤖 AI Perspective

While Mikikogyo reported significant growth in net sales and net profit for Q1, the decline in operating and ordinary profits suggests a shift in the profit structure. This could be influenced by increased cost of sales and personnel expenses, alongside a one-off gain from the sale of rental real estate boosting net profit. As the full-year forecasts remain unchanged, the company may view these factors as already incorporated into its projections.

173A|G-ハンモック

1406.0

▼ -2.50%

📎 Source:G-ハンモック Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Hammock resolved to enter into a capital and business alliance with Adish Inc. and acquire shares of Adish Inc. at a Board of Directors meeting held on April 27, 2026.

- The alliance aims to strengthen G-Hammock’s customer success domain and achieve mid-to-long-term business growth, not primarily short-term financial returns.

- The business alliance includes collaboration in customer success to increase sales of SaaS products, consideration of new services combining G-Hammock’s SaaS and Adish’s BPO, joint approaches to non-SaaS companies, and mutual utilization of both companies’ customer bases.

- G-Hammock plans to acquire 66,500 shares of Adish Inc. common stock, representing 3.07% of its outstanding shares, from existing shareholders. The scheduled acquisition date is May 1, 2026.

- The impact of this capital and business alliance on G-Hammock’s financial results for the fiscal year ending March 2027 is expected to be minor.

🤖 AI Perspective

This alliance may suggest G-Hammock’s strategic focus on addressing key SaaS business challenges, such as reducing churn rates and enhancing upselling/cross-selling to existing customers, through collaboration with Adish Inc., which specializes in customer success. The integration of G-Hammock’s SaaS expertise with Adish’s BPO capabilities could open avenues for new service offerings and joint market expansion into non-SaaS sectors, indicating a move towards broader market opportunities. While the immediate financial impact is projected to be minor, the long-term contribution to corporate value could be a point of interest for investors to monitor.

1944|きんでん

6932.0

▼ -3.90%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kinden Co., Ltd. resolved at its Board of Directors meeting on April 27, 2026, to pay a year-end dividend of ¥70.00 per share for the fiscal year ended March 31, 2026, with the record date of March 31, 2026.

- This approved dividend amount represents an increase of ¥5.00 from the most recent dividend forecast (revised on January 29, 2026) of ¥65.00 per share.

- Consequently, the total annual dividend for the fiscal year ending March 31, 2026, will be ¥130.00 per share, combining the interim dividend of ¥60.00 and the year-end dividend of ¥70.00 (compared to ¥90.00 for the previous fiscal year ended March 31, 2025).

- The total dividend amount is ¥13,859 million, an increase from ¥9,937 million in the previous fiscal year (ended March 31, 2025).

- Furthermore, the company plans an annual dividend of ¥240.00 per share for the next fiscal year ending March 31, 2027 (comprising ¥140.00 ordinary dividend + ¥100.00 special dividend for achieving medium-term management plan growth targets).

🤖 AI Perspective

Kinden’s announcement includes an upward revision to its year-end dividend, a significant increase in the annual dividend for the current fiscal year, and a robust forecast for the next fiscal year’s annual dividend. This development may suggest the company’s strong confidence in its financial performance and a proactive stance on shareholder returns. The planned special dividend for the next fiscal year, linked to achieving medium-term management plan growth targets, could also be interpreted as an indicator of progress in its strategic initiatives.

2211|不二家

2400.0

▲ +0.21%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of the fiscal year ending December 2026 (January 1 to March 31, 2026), Fujiya Co., Ltd. reported consolidated net sales of ¥29,558 million, representing a 5.4% increase year-on-year.

- However, operating profit significantly decreased by 59.0% to ¥414 million, ordinary profit by 66.3% to ¥395 million, and net income attributable to owners of parent by 96.1% to ¥30 million.

- The primary reason for the decline in profits was attributed to an increase in the cost of sales, due to the use of cocoa beans procured at peak prices.

- By segment, the Western Confectionery business recorded sales of ¥7,445 million (down 4.0% year-on-year), impacted by factors such as a decrease in the number of Western confectionery stores. The Confectionery business sales increased to ¥21,205 million (up 9.4% year-on-year), driven by strengthened core products and new product launches.

- The company stated that the Q1 results are largely in line with its initial full-year forecast, and there are no revisions to the latest full-year consolidated earnings forecast.

🤖 AI Perspective

The significant decline in profits across all categories below net sales, despite an increase in revenue, is a key point for investors. The company’s explanation that higher raw material costs, particularly for cocoa beans, are the primary factor and are already factored into the full-year forecast, may offer some clarity on future expectations. The contrasting performance between the Western Confectionery segment’s decrease in sales and the Confectionery segment’s growth could also indicate potential shifts in the company’s strategic focus for its business portfolio.

2327|NSSOL

3584.0

▼ -2.61%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026 (April 1, 2025, to March 31, 2026), NSSOL reported consolidated revenue of ¥381,340 million (up 12.7% year-on-year), operating profit of ¥44,242 million (up 14.9% year-on-year), and profit attributable to owners of the parent of ¥30,832 million (up 14.0% year-on-year).

- The annual dividend per share for FY2026 was ¥85.00 (interim ¥40.00, year-end ¥45.00), an increase from ¥74.00 in the previous fiscal year.

- For the fiscal year ending March 31, 2027 (April 1, 2026, to March 31, 2027), the company forecasts consolidated revenue of ¥417,000 million (up 9.4% year-on-year), operating profit of ¥47,500 million (up 7.4% year-on-year), and profit attributable to owners of the parent of ¥31,600 million (up 2.5% year-on-year).

- During FY2026, significant changes in the scope of consolidation included the addition of six new companies, including Infocom Corporation.

- As of March 31, 2026, equity attributable to owners of the parent was ¥279,203 million, with an equity ratio attributable to owners of the parent of 66.9%.

🤖 AI Perspective

The company’s strong performance in FY2026, with double-digit growth in key profit metrics, may suggest continued robust demand for DX solutions and the positive impact of its business model transformation initiatives. The increase in the annual dividend, alongside the significant expansion of the consolidation scope with six new companies including Infocom Corporation, could be worth monitoring as indicators of future growth strategy and operational developments.

2689|オルバヘルスケアHD

2085.0

▲ +0.10%

📎 Source:オルバヘルスケアHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Olba Healthcare Holdings announced its consolidated financial results for the third quarter of the fiscal year ending June 2026 (July 1, 2025 to March 31, 2026).

- Consolidated net sales reached ¥95,777 million, representing a 3.6% increase compared to the same period in the previous year.

- Consolidated operating profit was ¥1,244 million (a 3.8% decrease year-on-year), and net profit attributable to owners of the parent was ¥872 million (a 6.5% decrease year-on-year).

- Sales in the Medical Equipment business segment totaled ¥90,480 million (a 3.5% increase year-on-year), with consumables sales increasing by 3.7% year-on-year, notably orthopedic consumables by 6.1%.

- The full-year consolidated earnings forecast and the annual dividend forecast (¥80.00) for the fiscal year ending June 2026 remain unrevised from the most recently announced figures.

🤖 AI Perspective

While net sales increased in the cumulative third quarter, both operating profit and net profit attributable to owners of the parent decreased, which may suggest impacts from cost increases or other challenging business conditions. Within the Medical Equipment business, robust sales of consumables, particularly orthopedic consumables, appear to be a key growth driver worth monitoring. The unrevised full-year earnings forecast indicates that the company maintains its current outlook towards the fiscal year-end.

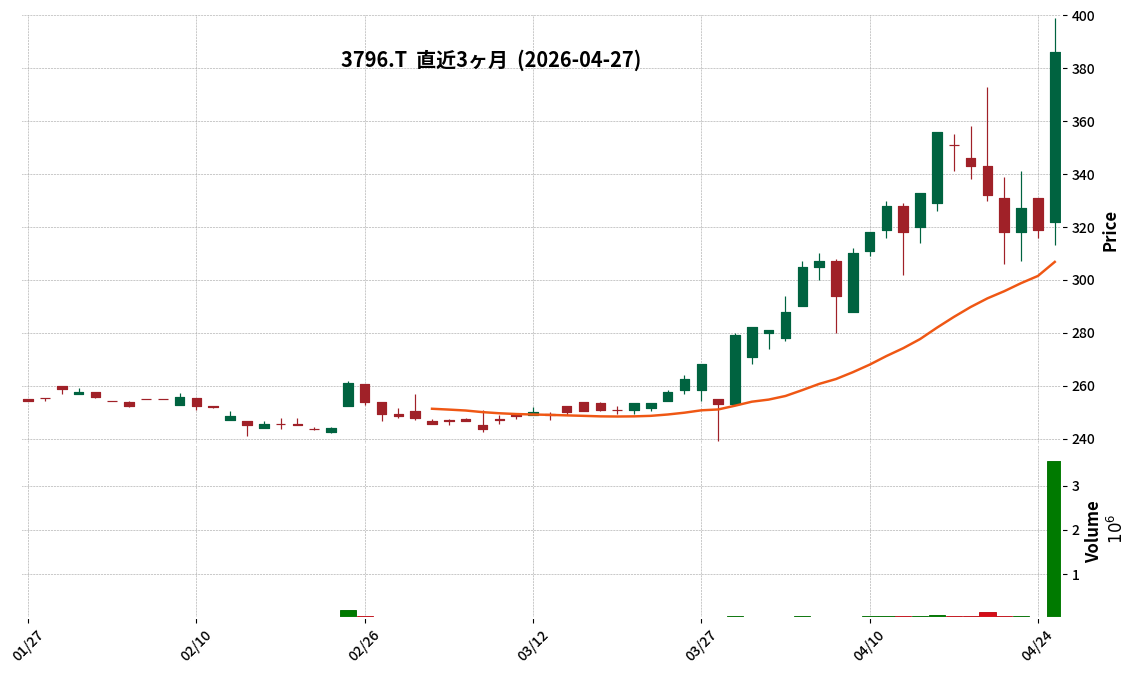

3796|いい生活

386.0

▲ +21.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- On April 27, 2026, Ii-Seikatsu Co., Ltd. (Code: 3796) announced an upward revision to its consolidated earnings forecast for the fiscal year ending March 2026.

- The revised full-year consolidated earnings forecast for FY2026 projects Net Sales of ¥3,232 million (up 1.0% from previous forecast), Operating Profit of ¥229 million (up 34.3%), Ordinary Profit of ¥236 million (up 34.3%), and Net Profit attributable to owners of parent of ¥151 million (up 33.6%).

- Earnings per share (before stock split) increased from the previous forecast of ¥16.40 to the revised forecast of ¥21.91.

- The company cited the successful implementation of various measures, including the utilization of AI technology for labor-saving, aimed at transitioning to a highly scalable business structure that suppresses cost increases associated with business expansion, as the reason for this revision.

- The dividend forecast remains unchanged from the announcement on February 24, 2026, with a year-end dividend of ¥3 per share after the stock split (¥6 before split).

🤖 AI Perspective

- This upward revision to the earnings forecast, particularly the significant increase in operating, ordinary, and net profits by over 30%, may suggest a substantial improvement in the company’s profitability.

- The successful integration of AI technology for labor-saving and the shift towards a scalable business model aimed at curbing cost increases alongside business expansion appear to be contributing to enhanced profit margins.

- Considering that the previous fiscal year (FY2025) recorded an operating loss, the projected return to profitability in the current fiscal year, coupled with a significant improvement in profit levels, could be a noteworthy development for investors.

4498|G-サイバートラスト

1248.0

▲ +3.48%

📎 Source:G-サイバートラスト Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Cybertrust Co., Ltd. has decided on a year-end dividend of ¥12.00 per share for the fiscal year ended March 31, 2026.

- This determined amount represents an increase of ¥0.50 from the most recent dividend forecast of ¥11.50 per share, which was announced on April 23, 2025.

- The company conducted a 2-for-1 stock split effective October 1, 2025; therefore, the previous fiscal year’s dividend (FY ended March 2025) of ¥23.00 per share was prior to this stock split.

- The annual dividend forecast for the fiscal year ending March 2027 is ¥14.00 per share, an increase of ¥2.00 from the FY March 2026 annual dividend of ¥12.00 per share.

- The effective date for this dividend payment is June 25, 2026, with the source of funds being retained earnings.

🤖 AI Perspective

The announced dividend, when adjusted for the stock split, represents an effective increase from the previous fiscal year’s dividend (¥11.50 equivalent), potentially signaling the company’s commitment to shareholder returns. The forward-looking dividend forecast also indicates a further increase, which may align with the company’s stated policy of stable and continuous dividends. This approach suggests a balance between prioritizing long-term business growth and enhancing corporate value, while also providing profit distribution to shareholders.

4503|アステラス薬

2385.5

▼ -3.34%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Consolidated revenue for the fiscal year ended March 2026 was JPY 2,139,245 million, representing an 11.9% increase compared to the previous fiscal year (FY2025 March).

- Consolidated operating profit reached JPY 382,633 million, a substantial increase of 832.4% year-on-year.

- Profit attributable to owners of the parent was JPY 291,535 million, achieving a 474.5% increase from the prior year.

- The annual dividend for the fiscal year ended March 2026 was JPY 78.00 per share (JPY 39.00 interim, JPY 39.00 year-end).

- For the fiscal year ending March 2027, the company forecasts consolidated revenue of JPY 2,220,000 million (up 3.8% year-on-year), operating profit of JPY 395,000 million (up 3.2% year-on-year), profit attributable to owners of the parent of JPY 300,000 million (up 2.9% year-on-year), and an annual dividend of JPY 80.00.

🤖 AI Perspective

Astellas Pharma’s fiscal year March 2026 results reveal robust growth in operating and net profit, alongside steady revenue expansion. This remarkable surge in profitability may suggest successful strategic initiatives or favorable shifts in cost management. For the upcoming fiscal year March 2027, while continued revenue and profit growth is projected, the deceleration in growth rates to single digits could lead investors to focus on the company’s detailed strategies for sustained future expansion.

5612|日鋳鉄管

1672.0

▼ -1.36%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, Nichu Tetsukan reported consolidated net sales of 15,942 million yen, a 5.8% decrease from the previous year.

- Net income attributable to owners of parent was 91 million yen, a significant turnaround from a loss of 230 million yen in the prior fiscal year.

- Operating profit decreased by 1.0% to 258 million yen, while ordinary profit fell by 19.4% to 215 million yen.

- The company announced an annual dividend of 25.00 yen per share for the fiscal year, with a total dividend payment of 80 million yen.

- The consolidated earnings forecast for the fiscal year ending March 31, 2027, has not been disclosed due to the difficulty of reasonable calculation at this time. The company is preparing for the establishment of a manufacturing joint venture with Kubota Corporation by December 2026, and achieved 100% electric furnace operation at its Kuki plant in October 2025.

🤖 AI Perspective

The turnaround to net profit attributable to owners of parent appears to be supported by the recognition of special income related to the preparation for a manufacturing joint venture. Despite a decrease in net sales, the limited decline in operating profit may suggest the effectiveness of efforts in passing on sales prices and cost reductions. The ongoing strategic initiatives, such as the joint venture with Kubota and the full electrification of its furnace aiming for CO2 reduction, could be crucial for the company’s mid-to-long-term earnings structure improvement.

6501|日立

5356.0

▲ +2.43%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hitachi Ltd. announced consolidated revenue of ¥10,586.7 billion for the fiscal year ended March 31, 2026, marking an 8.2% increase year-on-year.

- Net profit attributable to owners of the parent significantly rose by 30.3% from the previous period, reaching ¥802.3 billion.

- Adjusted Operating Profit stood at ¥1,199.2 billion (+23.4% year-on-year), and Adjusted EBITA was ¥1,311.4 billion (+21.0% year-on-year).

- The full-year dividend per share for FY2026/3 was ¥50.00, an increase from ¥43.00 in the prior fiscal year.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated revenue of ¥11,100.0 billion (+4.8% year-on-year) and net profit attributable to owners of the parent of ¥850.0 billion (+5.9% year-on-year).

🤖 AI Perspective

The significant increase in net profit attributable to owners of the parent and revenue exceeding ¥10 trillion for FY2026/3 may suggest strong operational performance and business growth. The raised annual dividend and the forecast for continued revenue and profit growth in the next fiscal year could indicate management’s confidence in future prospects. Improvements in profitability metrics such as Adjusted Operating Profit margin and ROE are also worth monitoring.

6594|ニデック

2448.0

▼ -0.69%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nidec Corporation announced on April 27, 2026, the postponement of its financial results announcement for the fiscal year ending March 2026.

- The delay is attributed to the “Third-Party Committee’s Investigation Report (Final Report)” received on April 17, 2026.

- Following the committee’s findings, the company is undertaking corrective work on its financial statements from the fiscal year ending March 2022 onwards.

- Simultaneously, Nidec is preparing its financial statements for the fiscal year ending March 2026, but these procedures are currently incomplete and are expected to require a significant amount of time.

- The company stated that the new scheduled date for the FY2026 financial results announcement will be communicated promptly once determined.

🤖 AI Perspective

Nidec’s postponement of its FY2026 financial results announcement highlights the complexity of addressing past financial statement corrections stemming from a third-party committee’s final report. The need to revise past financials from FY2022 onwards suggests that these adjustments are substantial and require thorough processing. The current lack of a firm announcement date could lead investors to monitor the eventual disclosure closely for insights into the impact of these corrective actions.

6754|アンリツ

3755.0

▲ +4.48%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Anritsu Corporation announced its consolidated financial results for the fiscal year ended March 31, 2026.

- Revenue increased by 4.0% year-on-year to ¥117,462 million. Operating profit rose by 22.3% to ¥14,828 million, and profit attributable to owners of parent increased by 26.1% to ¥11,677 million.

- Basic earnings per share for the period stood at ¥91.20.

- The annual dividend for the fiscal year ended March 31, 2026, was ¥50.00 per share (compared to ¥40.00 in the previous year), including a year-end dividend of ¥30.00 (ordinary dividend of ¥26.00 and commemorative dividend of ¥4.00).

- For the fiscal year ending March 31, 2027, the company forecasts consolidated revenue of ¥140,000 million (up 19.2% year-on-year), operating profit of ¥20,000 million (up 34.9%), and profit attributable to owners of parent of ¥15,000 million (up 28.4%). The annual dividend is projected to be ¥50.00 per share.

🤖 AI Perspective

Anritsu’s consolidated performance for the fiscal year ended March 31, 2026, showed significant growth across revenue and all profit metrics, with operating profit and profit attributable to owners of parent increasing by over 20%. This strong performance may be attributed to advancements in the communication measuring instrument business, particularly related to data center investments and 5G/IoT applications. The positive outlook for the fiscal year ending March 31, 2027, with continued high growth projections and a maintained annual dividend of ¥50, suggests ongoing momentum in the company’s operations.

6810|マクセル

2139.0

▼ -0.42%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Maxell announced its consolidated financial results for the fiscal year ended March 31, 2026. Net sales totaled ¥129,429 million (down 0.3% year-on-year), operating profit was ¥7,891 million (down 15.3%), and ordinary profit was ¥8,601 million (down 12.0%).

- Profit attributable to owners of parent significantly increased to ¥8,260 million (up 102.0%), primarily due to the recognition of extraordinary gains from the transfer of shares of a consolidated subsidiary.

- The annual dividend for the fiscal year ended March 31, 2026, is ¥50 per share (¥25 interim, ¥25 year-end), consistent with the previous year. For the fiscal year ending March 31, 2027, the company forecasts an annual dividend of ¥56 per share (¥28 interim, ¥28 year-end).

- For the fiscal year ending March 31, 2027, consolidated performance forecasts project net sales of ¥143,000 million (up 10.5% year-on-year) and operating profit of ¥10,000 million (up 26.7%). However, profit attributable to owners of parent is expected to decrease to ¥6,700 million (down 18.9%).

- Significant changes in the scope of consolidation occurred during the consolidated fiscal year, with Maxell Sakura Co., Ltd. newly consolidated and Wuxi Maxell Energy Co., Ltd. excluded.

🤖 AI Perspective

For the fiscal year ended March 31, 2026, while profit attributable to owners of parent showed a substantial increase due to extraordinary gains from the transfer of a consolidated subsidiary, net sales, operating profit, and ordinary profit all experienced declines. The forecast for the fiscal year ending March 31, 2027, suggests a recovery in core business with projected increases in net sales and operating profit. However, the anticipated decrease in net profit for the next fiscal year is expected to be a 反動 from this period’s extraordinary gains, indicating investors may wish to distinguish between one-off factors and underlying business performance. The announced increase in the dividend forecast may be viewed as a positive sign regarding shareholder returns.

7093|G-アディッシュ

541.0

▲ +0.00%

📎 Source:G-アディッシュ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Addish announced on April 27, 2026, the initiation of a capital and business alliance with Hammock Co., Ltd.

- The business alliance involves G-Addish providing expertise for Hammock’s SaaS products, including planning and executing churn prevention measures, supporting up-selling and cross-selling opportunities for existing customers, developing new services and business areas combining both companies’ knowledge, joint approaches to non-SaaS companies, and mutual utilization of their customer bases.

- As part of the capital alliance, Hammock Co., Ltd. plans to acquire 66,500 shares of G-Addish common stock, representing 3.07% of the total outstanding shares, from existing shareholders at the average price over the last three months as of today.

- Hammock Co., Ltd., the alliance partner, specializes in the development and sales of corporate software, reporting net sales of ¥4,707,880 thousand and operating profit of ¥791,514 thousand for the fiscal year ended March 2025.

- The alliance was resolved by the Board of Directors on April 27, 2026, with the share acquisition scheduled for May 1, 2026, and business collaboration expected to commence from May-June 2026.

🤖 AI Perspective

- This alliance may suggest a strategic move by G-Addish to expand its customer success and support BPO expertise by leveraging Hammock’s SaaS product portfolio and corporate client base, potentially leading to an expansion of both companies’ business domains and enhanced value for customers.

- The establishment of a capital relationship, beyond a simple business partnership, could indicate a commitment to a stable and sustained collaboration aimed at fostering medium-to-long-term growth for both entities.

- The exploration of joint approaches to non-SaaS companies and BPaaS offerings highlights a potential focus on diversifying revenue streams and capturing new market opportunities.

1960|サンテック

1373.0

▼ -1.29%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Suntec Co., Ltd. announced on April 27, 2026, revisions to its consolidated and non-consolidated earnings forecasts for the full fiscal year ending March 2026 (April 1, 2025 – March 31, 2026), as well as its year-end dividend forecast.

- For the consolidated earnings forecast, net sales were revised upward from ¥60,000 million to ¥61,077 million, operating profit from ¥2,000 million to ¥3,014 million, and net profit attributable to owners of parent from ¥2,000 million to ¥2,766 million.

- The primary reason cited for the earnings forecast revision is an increase in gross profit, attributed to thorough process and cost management.

- The year-end dividend forecast for the fiscal year ending March 2026 was revised from ¥40.00 per share to ¥65.00 per share, representing an increase of ¥25.00 per share.

- The dividend revision is based on the company’s fundamental policy of maintaining a stable financial base, securing necessary funds for growth investments, and providing appropriate shareholder returns, in line with the targets of a 30% dividend payout ratio and a DOE of 2.0% or more, as stated in its 14th Medium-Term Management Plan announced on March 27, 2026.

🤖 AI Perspective

Suntec’s significant upward revision of its full-year earnings forecast for the fiscal year ending March 2026, coupled with an increased dividend, may be a key point of interest for investors. The substantial increase in consolidated operating profit, exceeding 50% compared to the previous forecast, could indicate improved profitability and operational efficiency driven by enhanced process and cost management. Furthermore, the company’s move to revise its dividend in line with its mid-term management plan’s shareholder return policy might be perceived as a strong commitment to its shareholders.

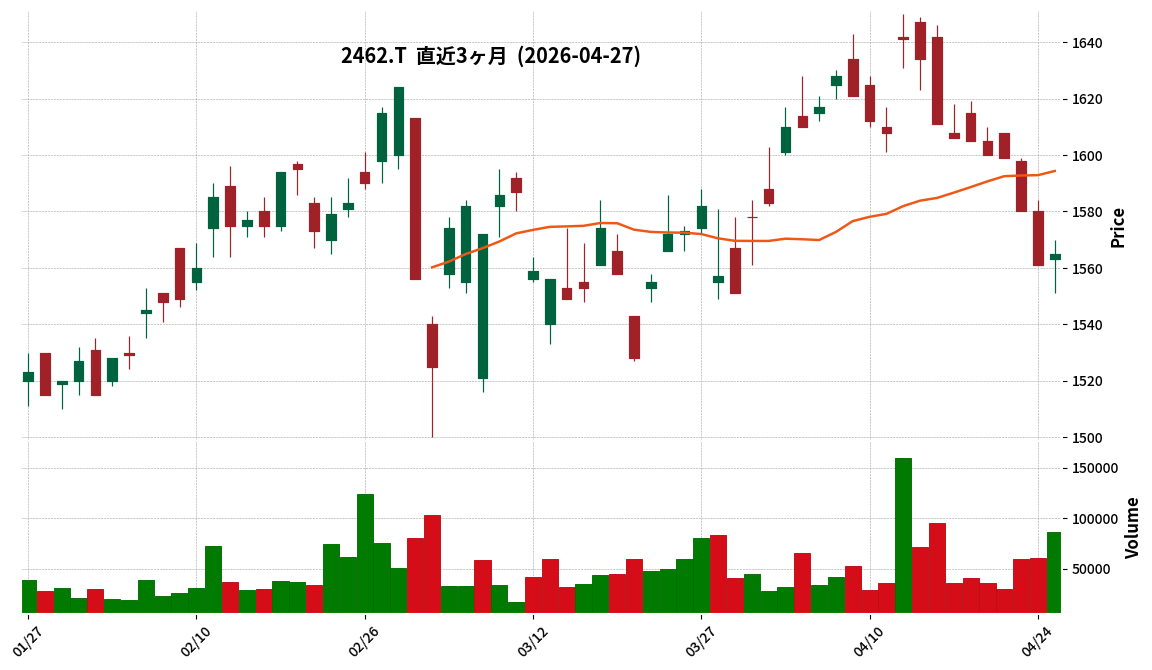

2462|ライク

1565.0

▲ +0.26%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Like Inc. resolved on April 27, 2026, to implement an additional enhancement to its shareholder benefit program, modifying the “Notice of Change in Shareholder Benefit Program” originally announced on April 13, 2026.

- The primary objective of this change is to review the shareholder benefit point system for continuous ownership of one year or more, based on shareholder feedback, thereby expanding returns for shareholders holding shares over the medium to long term.

- A new “Continuous Ownership Bonus Point Table” has been established, adding between 3,000 and 20,000 points to the regular shareholder benefit points for shareholders continuously holding 500 or more shares for at least one year.

- Eligibility for these bonus points requires continuous registration in the company’s shareholder registry with 500 or more shares and the same shareholder number as of May 31, 2025, November 30, 2025, and May 31, 2026.

- The revised shareholder benefit program will apply to shareholders listed in the shareholder registry as of May 31, 2026, with points scheduled to be awarded annually in July. Points can be exchanged for over 5,000 items, including food, electronics, and various e-money/points, via the “Like Premium Shareholder Club.”

🤖 AI Perspective

- This announcement is noteworthy as it represents a further revision to a previously declared change in the shareholder benefit program, incorporating shareholder feedback.

- The introduction of bonus points based on continuous ownership duration could suggest the company’s intent to encourage medium-to-long-term shareholding and secure a stable shareholder base.

- The flexibility offered by exchange options, including e-money and the common shareholder benefit coin “WILLsCoin,” might enhance the convenience and appeal of the benefit program for investors.

3080|ジェーソン

756.0

▼ -0.26%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended February 2026, sales increased by 1.1% year-on-year to 28,604 million yen, securing revenue growth. This growth was attributed to strong sales of Jason’s original (PB) products and the contribution from its subsidiary, Sunmall Co., Ltd.

- Operating profit decreased by 62.7% from the previous fiscal year to 200 million yen, and net loss attributable to owners of parent was 201 million yen, marking the company’s first net loss since listing. Key factors included M&A-related costs, increased depreciation due to vehicle purchases and capital investments, higher expenses at subsidiary Sunmall, and impairment losses on goodwill and certain tangible fixed assets related to Sunmall.

- The company stated that this special loss provision is a temporary deficit resulting from a conservative judgment aimed at maintaining financial soundness, with limited impact on cash flow and business operations.

- Subsidiary Sunmall recorded impairment losses due to slowed customer traffic amid intensified competition from new entrants. The company plans to improve profitability through management system reforms, operational efficiency enhancements, fundamental cost structure review, and applying Jason’s low-cost management expertise. Synergy reinforcement through joint store development and mutual product supplementation will also be promoted.

- For the fiscal year ending February 2027, the company forecasts a return to profitability with sales of 29,000 million yen, operating profit of 210 million yen, and net profit of 150 million yen. The annual dividend per share is planned to remain at 13 yen, consistent with the previous period, and the shareholder benefit program will continue.

🤖 AI Perspective

This Q&A session provides a clear explanation for Jason’s revenue growth alongside a significant profit decline and net loss in FY2026/2. The impairment loss related to subsidiary Sunmall is identified as a primary factor for the loss, though it is described as a temporary decision to maintain financial health. The company’s strategy for returning to profitability and strengthening earnings in the next fiscal year appears to focus on the turnaround of Sunmall, reinforcing private brand products, and upholding its “low-cost management” through DX initiatives.

3635|コーエーテクモ

1611.5

▲ +0.97%

📎 Source:コーエーテクモ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Koei Tecmo Holdings Co., Ltd. reported consolidated results for the fiscal year ended March 31, 2026, achieving revenue of ¥88,393 million (up 6.3% year-on-year), operating profit of ¥37,168 million (up 15.7% YoY), ordinary profit of ¥57,000 million (up 14.0% YoY), and net income attributable to owners of parent of ¥42,830 million (up 13.8% YoY).

- Revenue, ordinary profit, and net income attributable to owners of parent for the reported fiscal year reached record highs.

- The year-end dividend for the fiscal year ended March 31, 2026, was set at ¥66.00 per share (total annual dividend of ¥66.00), representing an increase from ¥60.00 in the previous fiscal year.

- The strong performance was attributed to the release of 14 packaged games and 2 new online/mobile games, including “Poka Poka Pokémon” surpassing 2.2 million global sales and “Nioh 3” achieving 1 million sales faster than any prior series title.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated revenue of ¥90,000 million (up 1.8% YoY), but anticipates a decrease in operating profit to ¥32,000 million (down 13.9% YoY), ordinary profit to ¥42,000 million (down 26.3% YoY), and net income attributable to owners of parent to ¥31,000 million (down 27.6% YoY).

🤖 AI Perspective

Koei Tecmo Holdings’ FY2026 results reflect robust performance, with key profitability metrics reaching record highs, which appears to be driven by the successful launch and strong sales of new game titles. The increase in the year-end dividend may also suggest a commitment to shareholder returns. However, the FY2027 forecast indicates a potential moderation in profitability despite expected revenue growth, suggesting that future business strategies and the performance of upcoming titles could be worth monitoring.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

3636|三菱総研

4790.0

▲ +0.42%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the second quarter (interim period) of the fiscal year ending September 2026, Mitsubishi Research Institute (MRI) reported consolidated net sales of ¥72,571 million (up 10.9% year-on-year), operating income of ¥9,293 million (up 36.3%), and ordinary income of ¥10,094 million (up 32.1%).

- Net profit attributable to owners of parent reached ¥8,470 million, marking a substantial increase of 73.5% year-on-year. This significant profit growth was primarily attributed to the recording of gain on sale of investment securities.

- The TTC (Think Tank & Consulting Services) segment achieved steady growth in key areas such as electric power/energy, healthcare/nursing care, and Business Analytics (BA)/AI. The ITS (Information Technology Services) segment is re-prioritizing resources towards industrial/public, financial/payment, and data AI sectors.

- In the ITS segment, new issues arose in a system development project, leading to the recording of a provision for loss on orders.

- MRI revised its consolidated full-year forecast for FY2026, projecting net sales of ¥125,000 million (up 2.9% year-on-year), operating income of ¥8,400 million (up 4.9%), ordinary income of ¥9,500 million (down 2.4%), and net profit attributable to owners of parent of ¥6,600 million (up 3.3%).

🤖 AI Perspective

- Mitsubishi Research Institute’s Q2 FY2026 interim results demonstrate substantial year-on-year growth across net sales and all profit stages. The significant increase in net profit attributable to owners of parent is noted to be influenced by the recording of gain on sale of investment securities, suggesting investors may wish to consider the balance between operational performance and one-off gains.

- The revised full-year outlook presents a nuanced picture, with ordinary income projected to decrease year-on-year despite growth in other income categories, which could be a point of interest for market observers monitoring overall profitability trends.

- Strategic shifts within the TTC and ITS segments, including identified growth areas and the recording of a provision for loss in a system development project, indicate ongoing business transformation and highlight potential areas for future monitoring regarding project execution and risk management within the IT services division.

3967|G-エルテス

583.0

▲ +0.17%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-ELTES resolved to transfer all shares (3,406 shares, 94.9% ownership) of its consolidated subsidiary, JAPANDX Co., Ltd., to Mr. Tsuyoshi Mikawa, its representative director, at a board meeting held on April 27, 2026. The transfer price is 5 million JPY.

- JAPANDX and its subsidiary, JDX Solutions Co., Ltd., are scheduled to be excluded from G-ELTES’s consolidated scope from the first quarter of the fiscal year ending February 2027, effective April 30, 2026.

- Concurrently, G-ELTES acquired all shares of its grand-subsidiaries, GloLing Co., Ltd. (acquisition price 126 million JPY) and PlayNextLab Co., Ltd. (acquisition price 473 million JPY), from JAPANDX, making them wholly-owned subsidiaries.

- The share acquisition execution dates were March 19, 2026, for GloLing, and April 28, 2026, for PlayNextLab, ensuring both companies remain within G-ELTES’s consolidated scope.

- The stated purpose of these changes is to maximize the company’s consolidated performance and corporate value, and to concentrate management resources on its core digital security business, as part of a review (carve-out) of its DX promotion business.

🤖 AI Perspective

This announcement may suggest G-ELTES’s strategic move to optimize its business portfolio by reorganizing part of its DX promotion business and focusing resources on its core digital security operations. The transfer of JAPANDX, which had less predictable profitability, while retaining GloLing and PlayNextLab, which offer stable revenue, could indicate an effort to balance profitability improvements with consistent performance. Investors may find it worthwhile monitoring how this resource reallocation impacts the growth of the digital security segment.

6092|エンバイオHD

799.0

▼ -2.80%

📎 Source:エンバイオHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Enbio Holdings disclosed the financial results for its non-listed parent company, CRE Inc., for the fiscal year ended January 2026, on April 27, 2026.

- CRE Inc. is engaged in the leasing, management, development, brokerage, and investment advisory of logistics facilities, with a capital of 5,391 million yen as of January 31, 2026.

- As of January 31, 2026, the major shareholders of CRE Inc. are SMFL Mirai Partners Co., Ltd., holding 50.1% (11,801,087 shares), and Kyobashi Kosan Co., Ltd., holding 49.9% (11,753,976 shares).

- According to the balance sheet as of January 31, 2026, CRE Inc.’s total assets were 173,925 million yen, total liabilities were 136,175 million yen, and total net assets were 37,749 million yen.

- Within current assets on the balance sheet, real estate for sale accounted for 71,550 million yen, and real estate for sale in progress for 30,926 million yen.

🤖 AI Perspective

The financial health of a parent company can indirectly influence the business strategy and operational stability of its listed subsidiary, Enbio Holdings. Given CRE Inc.’s business in real estate, the composition of current assets on its balance sheet may reflect the scale of its real estate development and leasing operations. Furthermore, the shareholder structure and executive board composition could indicate the nature of relationships with key investors.

6908|イリソ電子工業

3530.0

▼ -1.53%

📎 Source:イリソ電子工業 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Iriso Electronics Co., Ltd. resolved to establish a third-party committee on April 27, 2026, to investigate alleged “inappropriate financial disbursements” at an overseas subsidiary.

- The third-party committee, based on the Japan Federation of Bar Associations’ guidelines, aims to clarify facts, confirm the existence of similar incidents, examine the impact on consolidated financial statements, analyze causes, and propose recurrence prevention measures.