📌 Today’s Highlights

Today we cover 45 IR announcements. Notable among them: P-マークスライフ (561A), G-ニフティライフ (4262), ノジマ (7419). Use the table of contents below to navigate to each company.

- 561A|P-マークスライフ

- 4262|G-ニフティライフ

- 7419|ノジマ

- 8362|福井銀

- 2160|G-GNI

- 8255|アクシアル

- 4012|アクシス

- 6230|SANEI

- 5482|愛知鋼

- 4326|インテージHD

- 5445|東京鉄

- 2053|中部飼料

- 9701|東京会館

- 2489|ADWAYS

- 5261|リソル

- 9997|ベルーナ

- 2003|日東富士

- 203A|P-シュンビン

- 6395|タダノ

- 7711|助川電気

- 9353|桜島埠頭

- 1436|G-グリーンエナジー

- 1444|G-ニッソウ

- 1911|住友林

- 2802|味の素

- 2924|イフジ産業

- 3064|MRO

- 3496|アズーム

- 3549|クスリのアオキHD

- 3668|コロプラ

- 3984|ユーザーローカル

- 4151|協和キリン

- 4475|G-HENNGE

- 4746|東計電算

- 5187|クリエート

- 6549|ディーエムソリュ

- 6809|TOA

- 6853|共和電

- 8012|長瀬産

- 7609|ダイトロン

- 2335|キューブシステム

- 3175|APHD

- 3326|ランシステム

- 9425|ReYuuJapan

- 6200|インソース

561A|P-マークスライフ

—

▲ +0.00%

📎 Source:P-マークスライフ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- P-Marks Life Co., Ltd. (Code: 561A) was listed on the TOKYO PRO Market of the Tokyo Stock Exchange on May 7, 2026.

- For the fiscal year ended October 2025, the company reported consolidated net sales of JPY 7,894 million, operating profit of JPY 658 million, ordinary profit of JPY 570 million, and net profit of JPY 352 million.

- The company forecasts net sales of JPY 10,000 million for the fiscal year ending October 2026, representing a 26.7% increase year-on-year.

- For FY2026, the company projects operating profit of JPY 300 million (down 54.4% YoY), ordinary profit of JPY 150 million (down 73.7% YoY), and net profit of JPY 100 million (down 71.7% YoY), citing upfront investments in human resources and new branch openings.

- No dividends per share were paid for FY2025, and none are forecasted for FY22026.

🤖 AI Perspective

The listing on TOKYO PRO Market is expected to enhance the company’s transparency and provide opportunities for capital raising from the market. While the FY2026 forecast anticipates revenue growth, the projected decline in profits due to upfront investments suggests an aggressive strategy for future business expansion. How these investments will contribute to long-term corporate value improvement could be a key focus for investors.

4262|G-ニフティライフ

1390.0

▼ -1.14%

📎 Source:G-ニフティライフ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 2026, consolidated net sales reached ¥5,238 million (up 6.1% year-on-year), operating income was ¥1,189 million (up 18.5%), ordinary income was ¥1,195 million (up 20.1%), and profit attributable to owners of parent was ¥778 million (up 26.0%).

- Net sales for the current fiscal year marked a new record high for the eighth consecutive year since the company’s establishment.

- The annual dividend for the fiscal year ended March 2026 was ¥59.00, an increase of ¥27.00 from the previous year’s ¥32.00.

- For the fiscal year ending March 2027, the company forecasts consolidated net sales of ¥5,790 million (up 10.6% year-on-year), operating income of ¥1,313 million (up 10.4%), ordinary income of ¥1,307 million (up 9.3%), and profit attributable to owners of parent of ¥831 million (up 6.8%).

🤖 AI Perspective

G-NIFTY LIFESTYLE achieved double-digit growth in net sales and all profit metrics for the fiscal year ended March 2026, with profit attributable to owners of parent showing a substantial increase of 26.0%. The consistent achievement of record-high net sales for eight consecutive years since its establishment may suggest a robust and stable growth trajectory for the company. The significant increase in the annual dividend and the positive outlook for further sales and profit growth in the next fiscal year could be noteworthy points for investors to monitor.

7419|ノジマ

1211.0

▼ -0.66%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nojima Co., Ltd. resolved to increase its year-end dividend for the fiscal year ending March 31, 2026, at a Board of Directors meeting held on May 7, 2026.

- The per-share year-end dividend for the fiscal year ending March 2026 has been set at JPY 10.00.

- This represents an increase of JPY 2.00 per share from the previous dividend forecast of JPY 8.00 announced on January 29, 2026.

- The total dividend amount is JPY 2,918 million, with an effective date of June 5, 2026.

- The company implemented a 1-for-3 stock split for its common shares, effective October 11, 2025.

🤖 AI Perspective

- This dividend increase, based on the performance for the fiscal year ending March 2026, suggests the company’s commitment to strengthening its financial foundation and maintaining a stable dividend policy.

- It may also be seen as an indication of a proactive approach to shareholder returns.

8362|福井銀

3765.0

▲ +0.40%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Fukui Bank, Ltd. and Fukuho Bank, Ltd. completed their merger on May 2, 2026.

- The merged entity has commenced operations under the name “Fukui Bank, Ltd.” on the same date.

- Both banks had previously engaged in “F Project” initiatives aimed at regional development.

- Post-merger, Fukui Bank intends to integrate the strengths of both entities to evolve into a “regional issue-solving business.”

🤖 AI Perspective

The completion of this merger represents a tangible outcome of the “F Project” undertaken by both banks. Consolidation among regional financial institutions often aims to strengthen their operational foundations, enhance efficiency, and expand service offerings. The stated goal of evolving into a “regional issue-solving business” by leveraging combined strengths could indicate a strategic focus on addressing local needs and fostering sustainable growth within the region.

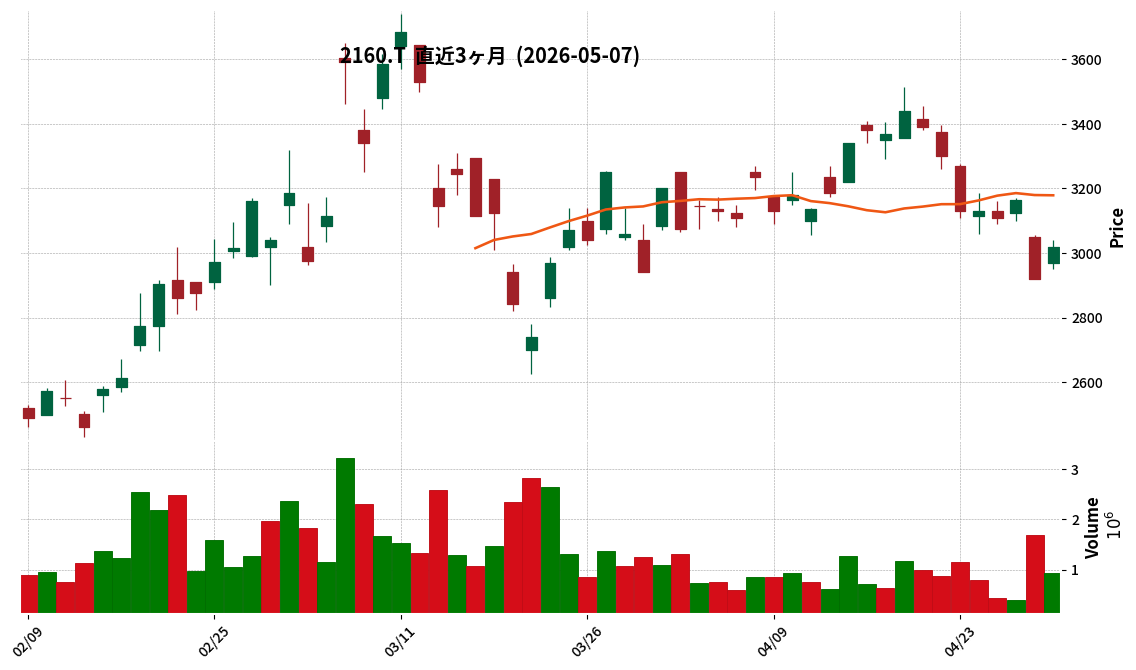

2160|G-GNI

3020.0

▲ +3.42%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- GNI Group’s consolidated subsidiary, Gyre Therapeutics, Inc., has completed the acquisition of Cullgen Inc., a privately held clinical-stage biopharmaceutical company, making it a wholly-owned subsidiary.

- The acquisition was executed through an all-stock exchange, with a transaction value of approximately USD 300 million. The integrated Gyre will operate as a fully integrated biopharmaceutical company based in the U.S. and China, maintaining its listing on the Nasdaq market under the ticker symbol “GYRE.”

- Dr. Ying Luo, formerly CEO of Cullgen, has been appointed President and CEO of Gyre, while Ping Zhang will serve as Chairman of Gyre.

- Through this integration, Gyre has gained revenue-generating commercial assets, including the lung fibrosis treatment Aisiqurui already marketed in China, and a robust product and development candidate pipeline primarily focused on fibrosis and inflammatory diseases.

- The expanded pipeline includes the lead development candidate F351 for chronic hepatitis B-induced liver fibrosis (granted priority review in China), as well as innovative preclinical and clinical programs such as Targeted Protein Degraders (TPD) and TPD Antibody Conjugates (DAC) acquired from Cullgen.

🤖 AI Perspective

* This acquisition of Cullgen by Gyre appears to strengthen GNI Group’s global operational footprint and enhance its research and development capabilities.

* The integration of Cullgen’s innovative drug discovery platform with Gyre’s existing commercial assets and late-stage pipeline could lead to diversification and acceleration in future drug development efforts.

* Alongside the progress of key development candidate F351, which received priority review, and the expansion of Aisiqurui’s indications, the outcomes from the newly acquired technology platform may influence the company’s long-term value.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

8255|アクシアル

1111.0

▼ -0.36%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Axial Retailiing Co., Ltd. reported consolidated results for the fiscal year ended March 31, 2026, with net sales of ¥295,536 million (up 4.8% year-on-year), operating income of ¥12,185 million (up 1.0%), and ordinary income of ¥12,799 million (up 0.7%).

- These net sales, operating income, and ordinary income represent record highs for a consolidated fiscal year.

- Net income attributable to owners of parent decreased by 2.3% year-on-year to ¥8,803 million.

- The annual dividend for the fiscal year ended March 31, 2026, was ¥29.00 per share (¥13.00 interim, ¥16.00 year-end), an increase of ¥2 from the previous fiscal year. The payout ratio was 29.2%.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥300,000 million (up 1.5% year-on-year), operating income of ¥11,700 million (down 4.0%), ordinary income of ¥12,000 million (down 6.2%), and net income attributable to owners of parent of ¥8,000 million (down 9.1%).

🤖 AI Perspective

For the fiscal year ended March 2026, while net sales, operating income, and ordinary income reached record highs, net income attributable to owners of parent experienced a decline. This could be attributed to strategies involving fierce price competition and operational improvements in a challenging environment with numerous new store openings and renovations by competitors. The forecast for the fiscal year ending March 2027 projects increased revenue but decreased profits, suggesting that managing the evolving business environment may remain a key challenge. The increased annual dividend payout might indicate a commitment to shareholder returns.

4012|アクシス

1549.0

▲ +1.31%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Axis Inc. has announced its financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026 to March 31, 2026).

- For the quarter, net sales reached ¥2,248 million (up 15.7% year-on-year), operating profit was ¥338 million (up 34.0%), ordinary profit was ¥344 million (up 29.7%), and quarterly net profit was ¥218 million (up 27.4%).

- Segment-wise, Systems Service business reported sales of ¥2,122 million (up 15.5% year-on-year), and IT Service business reported sales of ¥125 million (up 17.5% year-on-year).

- As of March 31, 2026, total assets stood at ¥5,419 million, net assets at ¥4,101 million, and the equity ratio at 75.7%.

- The full-year performance forecast for the fiscal year ending December 2026 and the annual dividend forecast of ¥57.00 remain unchanged from the most recently published figures.

🤖 AI Perspective

Axis Inc. has reported a robust start to its fiscal year, achieving double-digit growth in both sales and various profit metrics for the first quarter of FY2026. The substantial 34.0% increase in operating profit may suggest effective cost management or an increase in higher-margin projects. The growth across both System Services and IT Services business segments could indicate positive traction from strategic initiatives such as expanding high-value-added areas and acquiring new customers, as outlined in their medium-term management plan.

6230|SANEI

2101.0

▼ -0.99%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SANEI Ltd. reported consolidated net sales of JPY 29,042 million for the fiscal year ended March 31, 2026, an increase of 2.0% from the previous fiscal year.

- For the same period, consolidated operating profit was JPY 1,830 million (down 2.8% year-on-year), ordinary profit was JPY 1,803 million (down 2.1% year-on-year), and profit attributable to owners of parent was JPY 1,220 million (down 2.7% year-on-year).

- The annual dividend for the fiscal year ended March 31, 2026, totaled JPY 69.00 per share, including a year-end dividend of JPY 37.00 per share, with a total dividend payment of JPY 315 million.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of JPY 30.8 billion (up 6.1% year-on-year), operating profit of JPY 2.0 billion (up 9.2% year-on-year), and profit attributable to owners of parent of JPY 1.28 billion (up 4.8% year-on-year).

- The projected annual dividend for the fiscal year ending March 31, 2027, is JPY 75.00 per share, comprising an interim dividend of JPY 37.00 and a year-end dividend of JPY 38.00.

🤖 AI Perspective

While SANEI achieved increased net sales in FY2026/3, profits declined, reportedly due to rising raw material costs and energy expenses. The positive outlook for FY2027/3, with forecasts for both sales and profit growth, suggests a potential recovery in profitability in the upcoming fiscal year. Furthermore, the proposed increase in the annual dividend for FY2027/3 could indicate a consistent focus on shareholder returns.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

5482|愛知鋼

2935.0

▲ +1.73%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, Aichi Steel reported consolidated sales revenue of ¥304.3 billion (up 2% year-on-year) and operating profit of ¥17.3 billion (up 45% year-on-year), achieving record highs for both metrics.

- Profit attributable to owners of parent was ¥11.2 billion (up 44% year-on-year), and ROE increased by 1.6 percentage points to 4.8%.

- The full-year dividend for FY2026 was ¥145 per share, including an increased ordinary dividend due to better-than-expected performance and a special dividend.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated sales revenue of ¥310.0 billion (up 2% year-on-year), operating profit of ¥17.5 billion (up 1% year-on-year), and profit attributable to owners of parent of ¥11.3 billion (up 0% year-on-year).

- A full-year dividend of ¥150 per share is planned for FY2027, comprising an ordinary dividend of ¥72 and a special dividend of ¥78.

🤖 AI Perspective

Aichi Steel’s achievement of record-high sales revenue and operating profit in FY2026, alongside significant profit growth, stands out. This performance was notably supported by lower material purchase prices, reduced factory costs, and increased profits from consolidated subsidiaries. The company’s forecast for continued revenue and profit growth in FY2027 may suggest a sustained positive trajectory. Furthermore, operating profit has exceeded the mid-term management plan targets, which could indicate robust operational efficiencies and strategic execution worthy of monitoring by investors.

4326|インテージHD

1696.0

▲ +2.54%

📎 Source:インテージHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Intage Holdings, Inc. announced its consolidated financial results for the third quarter of the fiscal year ending June 2026 (July 1, 2025, to March 31, 2026).

- Cumulative net sales amounted to ¥51,874 million, representing a 1.8% increase year-on-year.

- Operating profit significantly rose by 30.5% year-on-year to ¥5,568 million, and ordinary profit increased by 33.4% year-on-year to ¥5,604 million.

- Profit attributable to owners of parent for the quarter decreased by 9.8% year-on-year to ¥3,414 million.

- The full-year consolidated earnings forecasts for the fiscal year ending June 2026 remain unchanged from the most recently announced figures, projecting net sales of ¥70,000 million, operating profit of ¥5,600 million, ordinary profit of ¥5,500 million, and profit attributable to owners of parent of ¥3,200 million.

🤖 AI Perspective

Intage Holdings reported a notable increase in operating and ordinary profits for Q3 FY2026, despite a modest rise in net sales. This performance may suggest improved operational efficiency and profitability within its core marketing support businesses. While profit attributable to owners of parent saw a decrease, the unchanged full-year consolidated earnings forecast indicates that this reduction is within the company’s initial projections.

5445|東京鉄

1856.0

▲ +2.03%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the consolidated fiscal year ended March 2026, Tokyo Tekko reported a decrease in both revenue and profits, with net sales reaching JPY 72,540 million (down 12.2% year-on-year) and net profit attributable to parent company shareholders at JPY 8,075 million (down 25.6% year-on-year).

- The consolidated earnings forecast for the fiscal year ending March 2027 projects net sales of JPY 76,000 million (up 4.8% year-on-year), but a decrease in net profit attributable to parent company shareholders to JPY 7,100 million (down 12.1% year-on-year).

- The annual dividend for FY2026 was JPY 300.00 per share. For FY2027 (forecast), after a 3-for-1 stock split effective April 1, 2026, the dividend is projected to be JPY 100.00 per share (equivalent to JPY 300.00 before the split).

- In terms of financial position, the equity ratio improved to 78.8% at the end of March 2026, compared to 73.5% at the end of the previous fiscal year.

- A 3-for-1 stock split for common shares was implemented, effective April 1, 2026.

🤖 AI Perspective

While Tokyo Tekko experienced a decline across all key profit metrics for FY2026, the company’s equity ratio showed an improvement. The FY2027 outlook indicates an anticipated increase in net sales, yet a continued downward trend in profits, which may suggest ongoing challenges in profitability. Additionally, the recently implemented stock split and its impact on per-share dividends and earnings per share will likely be a significant point of interest for investors.

2053|中部飼料

1730.0

▲ +2.85%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Chubu Shiryo Co., Ltd. announced its consolidated financial results for the fiscal year ended March 31, 2026, on May 7, 2026.

- For the fiscal year (April 1, 2025 – March 31, 2026), consolidated results were: Net Sales JPY 211,814 million (up 0.9% year-on-year), Operating Profit JPY 6,584 million (up 53.8% year-on-year), Ordinary Profit JPY 7,168 million (up 48.9% year-on-year), and Profit attributable to owners of parent JPY 5,551 million (up 58.5% year-on-year).

- Operating profit, ordinary profit, and profit attributable to owners of parent achieved three consecutive years of growth and marked a new record high in six years for all profit items.

- The annual dividend for FY2026 was JPY 65.00 per share (JPY 30.00 for interim, JPY 35.00 for year-end), an increase of JPY 13.00 from the previous year.

- The consolidated forecast for FY2027 projects Net Sales of JPY 221,000 million (up 4.3% year-on-year), Profit attributable to owners of parent of JPY 6,900 million (up 24.3% year-on-year), and an annual dividend of JPY 76.00 per share (JPY 38.00 for interim, JPY 38.00 for year-end).

🤖 AI Perspective

- The significant increase in key profit figures and the achievement of new record highs in the FY2026 results may suggest robust operational performance during the period.

- The company’s forecast for FY2027, anticipating further revenue growth and an increase in profit attributable to owners of parent, along with a higher dividend, could indicate a positive outlook despite potential industry challenges.

- Investors may find it worthwhile to monitor how Chubu Shiryo manages raw material price fluctuations and other market dynamics to sustain this growth trajectory in the upcoming fiscal year.

9701|東京会館

4560.0

▲ +5.92%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, Tokyo Kaikan reported net sales of ¥16,259 million (up 6.5% year-on-year), operating profit of ¥1,437 million (up 12.7%), ordinary profit of ¥1,480 million (up 18.8%), and net profit of ¥989 million (up 11.2%), achieving both revenue and profit growth.

- Earnings per share (EPS) for FY2026 increased to ¥299.93, and the year-end dividend was raised from ¥30.00 to ¥45.00 per share.

- As of March 31, 2026, total assets reached ¥30,173 million (up ¥2,675 million from the prior year-end), and net assets increased to ¥13,131 million (up ¥2,173 million), with the equity ratio improving to 43.5%.

- For the fiscal year ending March 31, 2027, the company forecasts full-year net sales of ¥16,330 million (up 0.4% year-on-year), net profit of ¥1,010 million (up 2.1% year-on-year), and EPS of ¥306.10.

- The projected annual dividend for FY2027 is ¥50.00 per share.

🤖 AI Perspective

Tokyo Kaikan’s significant profit growth across all key metrics and an increased dividend for FY2026 could suggest a strong operational performance, supported by robust demand in its core business segments. The improved financial health, as evidenced by a higher equity ratio and increased cash reserves, may indicate sound financial management and enhanced corporate stability. The forecast for continued growth and further dividend increases in FY2027 might reflect management’s positive outlook on future business prospects.

2489|ADWAYS

280.0

▼ -2.10%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- ADWAYS Co., Ltd. announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026, to March 31, 2026) on May 7, 2026.

- For the first quarter, consolidated net sales were ¥3,282 million (up 4.6% year-on-year), operating profit was ¥536 million (up 126.0%), ordinary profit was ¥601 million (up 73.6%), and profit attributable to owners of parent was ¥400 million (up 99.9%).

- The increase in net sales was primarily driven by increased advertising demand from financial-related companies for the affiliate advertising service “JANet” in the Ad Platform Business, and increased advertising demand from game and manga application advertisers in the Agency Business.

- Operating profit saw a significant year-on-year increase due to higher gross profit resulting from increased sales, coupled with the effective control of selling, general and administrative expenses.

- The consolidated full-year forecast for the fiscal year ending December 2026 remains unchanged, projecting net sales of ¥11,400 million (down 6.7% year-on-year), operating profit of ¥600 million (up 101.9%), and profit attributable to owners of parent of ¥530 million (up 109.6%). This full-year forecast incorporates the impact of the transfer of shares of a consolidated subsidiary, as announced on April 30, 2026.

🤖 AI Perspective

The first quarter results highlight ADWAYS’ strong performance, with significant year-on-year increases in operating, ordinary, and net profits, alongside solid sales growth. This performance is attributable to robust advertising demand in specific segments of both the Ad Platform and Agency Businesses, combined with effective cost management. While the full-year sales forecast anticipates a decline, the company projects substantial profit growth, which may suggest a strategic shift in its business portfolio or enhanced operational efficiencies. Investors might focus on how the company manages these strategic adjustments and continues to drive profitability throughout the fiscal year.

5261|リソル

7070.0

▲ +0.43%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- RESOL HOLDINGS Co., Ltd. announced its consolidated financial results for the fiscal year ended March 31, 2026.

- For FY2026/3, consolidated net sales were JPY 30,404 million (up 7.1% year-on-year), operating profit was JPY 3,303 million (up 23.2% year-on-year), ordinary profit was JPY 3,121 million (up 21.6% year-on-year), and profit attributable to owners of parent was JPY 2,708 million (up 38.9% year-on-year).

- The annual dividend for FY2026/3 was set at JPY 110.00 per share (compared to JPY 100.00 for the previous year).

- For FY2027/3, the company forecasts consolidated net sales of JPY 31,000 million (up 2.0% year-on-year), operating profit of JPY 3,400 million (up 2.9% year-on-year), ordinary profit of JPY 3,200 million (up 2.5% year-on-year), and profit attributable to owners of parent of JPY 1,950 million (down 28.0% year-on-year).

- The annual dividend for FY2027/3 is projected to be JPY 120.00 per share.

🤖 AI Perspective

RESOL HOLDINGS achieved double-digit growth in key profit figures for the fiscal year ended March 2026, which may reflect a favorable business environment driven by high inbound tourism and a shift towards “experience consumption.” While the FY2027/3 forecast indicates continued growth in net sales and operating profit, the projected decrease in profit attributable to owners of parent could be a point of interest for investors.

9997|ベルーナ

877.0

▲ +5.03%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Belluna Co., Ltd. announced on May 7, 2026, an upward revision to its consolidated earnings forecast for the fiscal year ending March 2026.

- Consolidated net profit is now projected to increase by JPY 2,000 million (21.1%) from the previous forecast of JPY 9,500 million to JPY 11,500 million.

- Key reasons for the revision include expanded sales in the domestic hotel business within the property segment due to increased domestic travel and inbound demand, a gain on sale of real estate for sale totaling JPY 1,042 million, and profitability-focused operations in the apparel and miscellaneous goods business.

- The dividend forecast for the fiscal year ending March 2026 has also been revised, with the year-end dividend per share increasing from JPY 15.00 to JPY 23.00, leading to a total annual dividend of JPY 38.00 from JPY 30.00.

- This dividend increase is based on the company’s policy of returning profits to shareholders through enhanced corporate value, in conjunction with the upward revision of the consolidated earnings forecast.

🤖 AI Perspective

The upward revision to the earnings forecast suggests a positive impact from the company’s property business, driven by factors such as strong domestic hotel performance and a one-time gain from real estate sales. The increased dividend, aligning with the revised earnings, could be viewed as a signal of the company’s commitment to shareholder returns. Investors may find these developments noteworthy as they assess Belluna’s financial outlook.

2003|日東富士

1865.0

▲ +5.07%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, Nitto Fuji’s consolidated net sales increased marginally by 0.6% year-on-year to 72,777 million yen. However, operating profit decreased by 25.1% to 3,816 million yen, ordinary profit by 21.1% to 4,386 million yen, and profit attributable to owners of parent by 6.5% to 3,319 million yen, reflecting a decline in profits.

- The annual dividend for the fiscal year ended March 31, 2026, was 280.00 yen (year-end dividend of 140.00 yen), maintained at the same level as the previous fiscal year.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of 73,000 million yen (up 0.3% year-on-year), operating profit of 4,200 million yen (up 10.1%), and ordinary profit of 4,700 million yen (up 7.2%). Profit attributable to owners of parent is projected to be 3,300 million yen (down 0.6%).

- A stock split of one common share into four shares was implemented on April 1, 2026. The forecast annual dividend for the fiscal year ending March 31, 2027, is 70.00 yen per share (35.00 yen interim, 35.00 yen year-end), reflecting the impact of this stock split.

- During the consolidated fiscal year, M&F Logistics Co., Ltd. (formerly Nitto Fuji Transport Co., Ltd.), which was a consolidated subsidiary, was excluded from the scope of consolidation.

203A|P-シュンビン

160.0

▲ +0.00%

📎 Source:P-シュンビン Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- P-Shunbin Co. announced its transition from consolidated financial statements to non-consolidated statements, effective from the fiscal year ending March 2026.

- This shift results from the absorption merger of its consolidated subsidiary, Musubino Co., Ltd., as the dissolving company, leading to no remaining consolidated subsidiaries.

- For the fiscal year ending March 2026, the company issued a standalone earnings forecast including Net Sales of ¥1,001 million, Operating Profit of ¥9 million, Ordinary Profit of ¥8 million, and Net Profit of ¥21 million.

- An extraordinary loss of ¥161 million, representing a loss on extinguishment of intercompany shares, was recorded due to the merger, and is reflected in the standalone earnings forecast.

- This standalone forecast replaces the previously disclosed consolidated earnings forecast for the fiscal year ending March 2026, which was initially announced on May 15, 2025.

🤖 AI Perspective

A company’s transition from consolidated to non-consolidated financial reporting often indicates a simplification of its corporate structure or a realignment of business operations. While the extraordinary loss from the subsidiary merger is a one-off event, the subsequent standalone earnings forecast could provide insights into the company’s future operational direction. Investors may wish to monitor how this change in reporting structure reflects on the company’s financial performance going forward.

6395|タダノ

1427.0

▲ +2.81%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of the fiscal year ending December 2026 (January 1, 2026 – March 31, 2026), consolidated net sales reached ¥85,845 million, marking a 6.6% increase year-on-year.

- During the same period, consolidated operating profit was ¥4,012 million (down 20.6% year-on-year), ordinary profit was ¥3,205 million (down 16.0%), and net profit attributable to owners of parent was ¥1,932 million (down 44.8%).

- The decline in profit was attributed, in part, to increased U.S. tariff costs.

- Sales in Japan increased by 29.2% to ¥30,631 million, boosted by the addition of transport machinery sales following the acquisition of IHI Transport Machinery’s transport system business (now Tadano Infra Solutions Co., Ltd., TIS) in July 2025.

- The full-year consolidated earnings forecast for the fiscal year ending December 2026 remains unchanged from the most recently announced forecast, projecting net sales of ¥400,000 million (up 14.5% year-on-year), operating profit of ¥25,000 million (up 34.7%), and net profit attributable to owners of parent of ¥14,000 million (down 23.5%).

🤖 AI Perspective

The first quarter results show a divergence where revenue grew but profits declined. This may suggest that while sales benefited from factors such as the TIS acquisition and increased sales in some regions, specific cost pressures like higher U.S. tariffs impacted profitability. The fact that the full-year earnings forecast remains unchanged could indicate that management anticipates a recovery or stronger performance in subsequent quarters to meet its annual targets. This dynamic between top-line growth and bottom-line contraction could be a key area for investors to monitor.

7711|助川電気

6320.0

▲ +6.76%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sukegawa Electric reported for the second quarter of the fiscal year ending September 2026 (October 1, 2025 – March 31, 2026) net sales of ¥3,108 million (up 5.0% year-on-year), operating profit of ¥784 million (up 12.1%), and net income of ¥561 million (up 13.2%).

- The energy-related business saw increased demand for nuclear-related products for research institutions and products related to the restart of nuclear power plants, resulting in net sales of ¥1,901 million (up 34.1% year-on-year) and segment profit of ¥663 million (up 45.6%).

- The full-year earnings forecast for the fiscal year ending September 2026 has been revised upwards, projecting net sales of ¥6,070 million (up 11.0% year-on-year), operating profit of ¥1,280 million (up 9.9%), and net income of ¥903 million (up 13.7%).

- The annual dividend forecast for FY2026 has been revised to ¥52.00 per share, comprising an interim dividend of ¥26.00 and a year-end dividend of ¥26.00.

- As of the end of the interim period, total assets stood at ¥8,802 million, net assets at ¥5,429 million, and the self-capital ratio was 61.7%.

🤖 AI Perspective

The interim period’s revenue and profit growth appears to be primarily driven by increased product demand in the energy-related business. The upward revision of the full-year earnings and annual dividend forecasts may suggest an improved outlook on business conditions and future prospects from the company’s perspective. While the industrial systems business experienced a decline in automotive-related products, the observed upturn in semiconductor manufacturing equipment could be a point of interest for future performance monitoring.

9353|桜島埠頭

2259.0

▲ +0.49%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sakurajima Futo Co., Ltd. announced on May 7, 2026, the finalization of the financial results for its affiliated company, Futo Justac Co., Ltd., for the January 2026 fiscal period.

- Futo Justac Co., Ltd. reported a net income of JPY 56,808 thousand and operating revenue of JPY 664,441 thousand for its January 2026 fiscal period.

- According to its balance sheet, Futo Justac Co., Ltd.’s total assets were JPY 988,088 thousand and total net assets were JPY 952,300 thousand as of January 31, 2026.

- Regarding its capital relationship with Sakurajima Futo Co., Ltd., Futo Justac Co., Ltd. holds a 19.1% voting rights ownership as of March 31, 2026.

- Futo Justac Co., Ltd. primarily operates in the port transportation and construction industries, with transactional relationships involving the entrustment of cargo handling and ordering of facility construction/repair from Sakurajima Futo.

🤖 AI Perspective

The financial results of Futo Justac Co., Ltd., classified as an “other affiliated company” for Sakurajima Futo, could indirectly influence Sakurajima Futo’s operational environment and business relationships. Given Futo Justac’s engagement in port transportation and construction, and its transactional ties with Sakurajima Futo for cargo handling and facility construction/repair, these results may suggest the health of their business collaboration. Stable performance from an affiliated company could contribute to the underlying stability of Sakurajima Futo’s business foundation.

1436|G-グリーンエナジー

1169.0

▼ -1.60%

📎 Source:G-グリーンエナジー Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Green Energy & Company announced on May 7, 2026, an upward revision to its consolidated earnings forecast for the fiscal year ending April 2026 (May 1, 2025 – April 30, 2026).

- The revised forecast projects net sales to increase by 8.2% from JPY 17,000 million to JPY 18,400 million, and operating profit to increase by 43.8% from JPY 800 million to JPY 1,150 million.

- Ordinary profit is expected to rise by 73.8% from JPY 610 million to JPY 1,060 million, and net profit attributable to parent company shareholders by 13.6% from JPY 440 million to JPY 500 million.

- The primary reasons for the upward revision include the grid-scale battery storage business outperforming initial plans, specifically due to better-than-expected progress in securing and delivering grid-scale battery storage projects, and operational revenue from the Hiroshima and Kirishima Battery Storage Power Plants.

- Additionally, the company expects lower financial costs due to efficient borrowing, and a reclassification of expenses related to the sale of healthcare facilities is noted to have a positive impact on net profit.

🤖 AI Perspective

The upward revision suggests that G-Green Energy’s core grid-scale battery storage business is a significant driver of revenue and profit growth, with specific project completions and operational earnings contributing to the improved outlook. The substantial increase in ordinary profit could indicate not only strong operational performance but also effective management of financial costs. The reclassification of expenses from an asset divestiture, impacting net profit, also warrants consideration as part of a broader portfolio strategy.

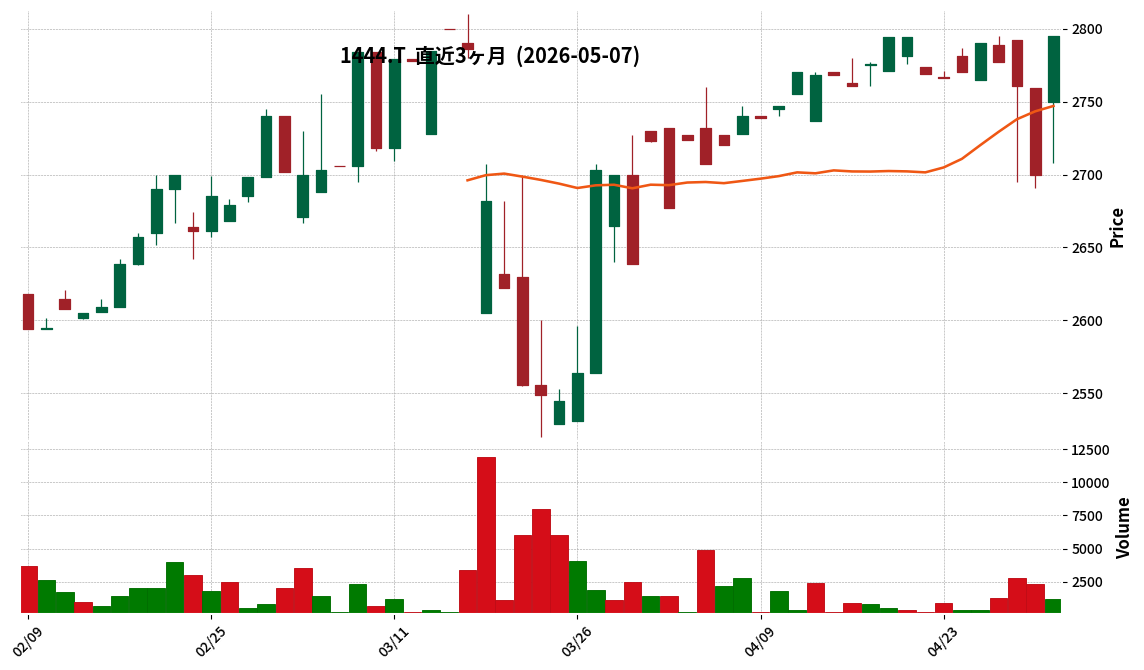

1444|G-ニッソウ

2795.0

▲ +3.52%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Nissho announced on May 7, 2026, the completion of its acquisition of all shares in Daikigiken Co., Ltd., making it a subsidiary.

- This acquisition is a follow-up disclosure to the “Announcement Regarding the Acquisition of Shares of Daikigiken Co., Ltd. (Making it a Subsidiary)” published on April 16, 2026.

- Daikigiken Co., Ltd., now a subsidiary, is located in Bunkyo-ku, Tokyo, and its business includes large-scale renovation work.

- G-Nissho has acquired 100% of Daikigiken Co., Ltd.’s shares, making it a wholly-owned subsidiary.

- The impact of this share acquisition on G-Nissho is already incorporated into the consolidated earnings forecast for the fiscal year ending July 2026, which was published on March 17, 2026, and no changes to the earnings forecast are being made at this time.

🤖 AI Perspective

This announcement confirms the successful and scheduled completion of the previously disclosed acquisition of Daikigiken Co., Ltd. As the impact is already factored into the consolidated earnings forecast for the fiscal year ending July 2026, immediate additional revisions to the forecast are not anticipated. The integration of Daikigiken’s large-scale renovation business could potentially strengthen G-Nissho’s overall business portfolio.

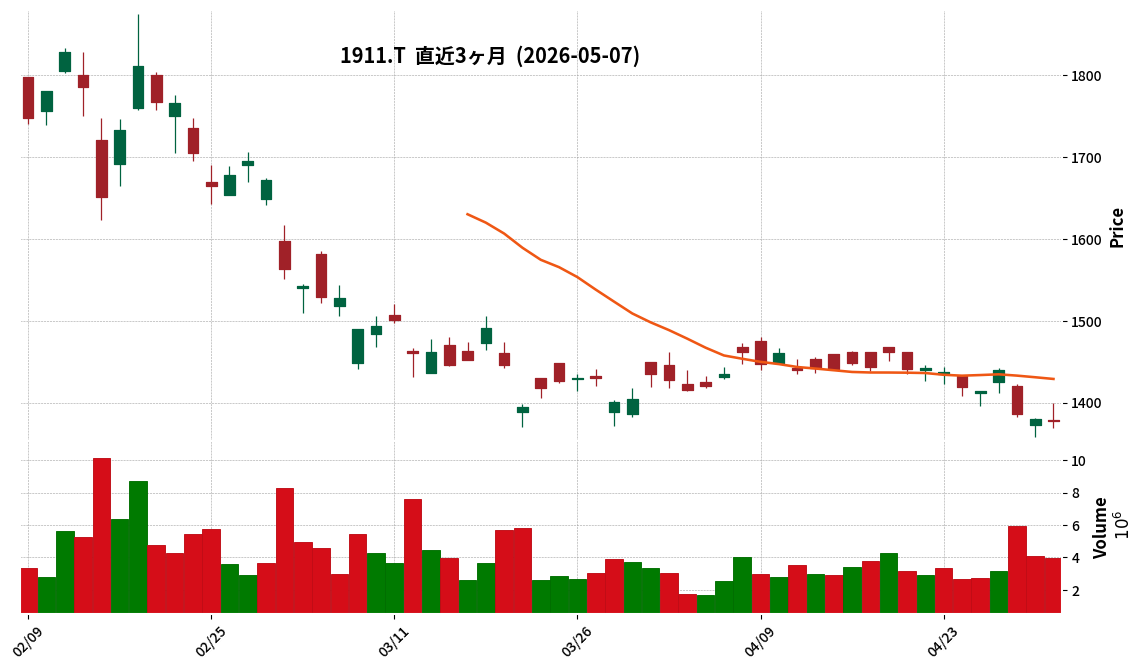

1911|住友林

1378.0

▼ -0.18%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sumitomo Forestry Co., Ltd. announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026 – March 31, 2026). Net sales increased by 4.0% year-on-year to ¥532,063 million, while operating profit decreased by 38.5% to ¥23,905 million, ordinary profit fell by 42.2% to ¥21,775 million, and profit attributable to owners of parent declined by 18.6% to ¥16,758 million.

- In the Overseas Housing Business segment, ordinary profit decreased by 39.1% year-on-year to ¥19,889 million. This was primarily attributed to a decrease in the number of homes sold in the U.S. detached housing business.

- The Timber and Building Materials Business reported an ordinary loss of ¥1,058 million, primarily due to production delays at a U.S. sawmill acquired in the previous fiscal year (compared to an ordinary profit of ¥564 million in the prior year period).

- Total assets at the end of the first consolidated accounting period increased by ¥40,766 million from the end of the previous consolidated fiscal year to ¥2,612,798 million, mainly due to the increase in the yen equivalent of foreign currency-denominated assets of overseas subsidiaries driven by the depreciation of the yen.

- The full-year consolidated earnings forecast for the fiscal year ending December 2026 remains unchanged, projecting net sales of ¥2,590,000 million (up 14.2% year-on-year), operating profit of ¥157,000 million (down 6.9% year-on-year), ordinary profit of ¥160,000 million (down 8.5% year-on-year), and profit attributable to owners of parent of ¥95,000 million (down 10.9% year-on-year).

🤖 AI Perspective

The first quarter results indicate a significant decline in profitability despite an increase in net sales. This downturn appears to be influenced by factors such as reduced sales in the U.S. overseas housing business and an ordinary loss recorded in the timber and building materials segment. However, the unchanged full-year earnings forecast might suggest that the company anticipates improvements or mitigating factors in the subsequent quarters.

2802|味の素

4998.0

▲ +2.38%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Ajinomoto Co., Inc. announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- Consolidated operating results show sales of JPY 1,583,719 million (up 3.5% year-on-year), business profit of JPY 181,163 million (up 13.7% year-on-year), and profit attributable to owners of parent of JPY 134,675 million (up 91.6% year-on-year). Basic earnings per share were JPY 138.36.

- The annual dividend for the fiscal year ended March 2026 was JPY 48.00 per share (interim dividend JPY 24.00, year-end dividend JPY 24.00), adjusted for the 2-for-1 stock split effective April 1, 2025.

- The consolidated earnings forecast for the fiscal year ending March 31, 2027 (April 1, 2026 – March 31, 2027) projects sales of JPY 1,723,000 million (up 8.8% year-on-year), business profit of JPY 197,000 million (up 8.7% year-on-year), and profit attributable to owners of parent of JPY 120,000 million (down 10.9% year-on-year). Basic earnings per share are forecasted at JPY 126.16.

- The annual dividend for the fiscal year ending March 2027 is projected to be JPY 50.00 per share (interim dividend JPY 25.00, year-end dividend JPY 25.00).

🤖 AI Perspective

The consolidated financial results for the fiscal year ended March 2026 showed increases in sales, business profit, and profit attributable to owners of parent, with a significant increase in the latter.

Conversely, the earnings forecast for the fiscal year ending March 2027 projects continued growth in sales and business profit, but a decrease in profit attributable to owners of parent compared to the previous fiscal year, which may draw investor attention to future profit structures. Furthermore, the forecast of an increased annual dividend for FY2027 suggests a continued commitment to shareholder returns.

2924|イフジ産業

1943.0

▲ +1.20%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Ifuji Sangyo announced its consolidated financial results for the fiscal year ended March 31, 2026, reporting record-high net sales of ¥32,572 million, a 27.4% increase year-on-year, marking the first time sales exceeded ¥30 billion.

- Operating profit declined by 6.9% to ¥2,790 million, ordinary profit fell by 6.3% to ¥2,857 million, and net income attributable to owners of parent decreased by 4.7% to ¥2,003 million.

- EBITDA (operating profit + depreciation + amortization of goodwill) reached a record high of ¥3,569 million, an increase of 0.8% year-on-year.

- Sales volume in the liquid egg business segment reached a record 66,660 tons, up 2.1% from the previous fiscal year.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥33,376 million (up 2.5%), operating profit of ¥2,913 million (up 4.4%), and net income attributable to owners of parent of ¥2,024 million (up 1.0%).

🤖 AI Perspective

Ifuji Sangyo’s FY2026 results highlight significant top-line growth with record sales and liquid egg volumes, alongside record EBITDA, which may suggest the company’s strategic capital investments are driving operational expansion. The decline in operating profit, despite sales growth, could be attributed to increased depreciation expenses from these investments, indicating a phase of significant upfront investment for future growth. The positive outlook for FY2027, forecasting growth in both sales and profits, implies an expectation for these investments to begin yielding returns.

3064|MRO

1818.0

▲ +0.69%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- MonotaRO Co., Ltd. announced its financial results for the first quarter of the fiscal year ending December 2026.

- Consolidated net sales reached JPY 95,582 million, representing a 20.8% increase year-on-year and exceeding the plan by 0.1%.

- Consolidated operating profit was JPY 13,170 million, a 22.6% increase year-on-year, surpassing the plan by 3.5%.

- MonotaRO standalone net sales totaled JPY 92,702 million, up 21.2% year-on-year, consistent with the plan.

- The Enterprise business segment recorded sales of JPY 32,926 million, a 25.6% increase year-on-year.

- The company attributed the consolidated net sales exceeding plan to higher-than-expected sales from overseas subsidiaries and increased demand for petroleum-derived products influenced by the situation in the Middle East.

🤖 AI Perspective

- MonotaRO’s Q1 results show both consolidated net sales and operating profit exceeding plans, with operating profit notably outperforming by 3.5% against the plan, which may suggest robust operational execution.

- The significant year-on-year growth of 25.6% in the Enterprise business segment could indicate expanding demand within the business-to-business indirect materials procurement market.

- However, it is worth monitoring that while office-related products underperformed, the overall sales beat was supported by strong overseas subsidiary performance and a demand surge for petroleum-derived products attributed to geopolitical factors.

3496|アズーム

4010.0

▼ -2.67%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- AZoom Co., Ltd. announced on May 7, 2026, a correction to its “Q2 FY2026 Financial Results Presentation Material,” which was originally disclosed on April 30, 2026.

- On page 5, the projected “Per-person operating profit (consolidated, year-end personnel)” for FY2028/9 was corrected from 11.5 to 8.8, and for FY2029/9, it was corrected from 18.2 to 11.5.

- On page 41, the “Number of domestic parking spaces (2020)” within “Expansion of existing domain (sublease) Stock: Trends in parking lot and automobile ownership” was corrected from 5,386 to 5,438.

- On page 44, the “Average for all sectors (2023)” (previously 146,760) and “Average for all sectors (2024)” (previously 152,194) under “Expansion of existing domain (sublease) Stock: Trends in e-commerce ratio” were deleted.

- On page 55, the “Growth potential ARR for monthly parking rental guarantee” within “Stock acquisition in related new areas: Real estate DX market and Iron Wall (parking rental guarantee) growth potential (TAM)” was corrected from ¥360 million (※1) to ¥170 billion (※3).

🤖 AI Perspective

These corrections encompass multiple key figures, including future planned values, market data, and growth potential estimates. Notably, the downward revision of the “per-person operating profit” in the medium-term management plan and the substantial upward revision of the “growth potential ARR for monthly parking rental guarantee” could indicate a shift in the company’s internal projections or strategic emphasis. Investors may find it worthwhile to assess how these updated figures align with AZoom’s overall long-term growth strategy.

3549|クスリのアオキHD

3905.0

▲ +4.55%

📎 Source:クスリのアオキHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kusuri no Aoki Holdings Co., Ltd. announced an enhancement to its shareholder benefit program, specifically establishing new long-term holding benefits.

- The stated purpose of this enhancement is to express further gratitude to shareholders, increase the investment attractiveness of its shares, and encourage mid-to-long-term shareholding.

- The new long-term holding benefits will be applicable starting from the shareholder benefit program with a record date of May 20, 2027, with no benefits granted for the fiscal year 2026.

- The benefits consist of additional novelty cards for shareholders who continuously hold 300 shares or more for at least one year as of the May 20 record date each year and apply for the shareholder benefits in the relevant fiscal year.

- The novelty cards will be valued at 2,500 yen for holdings of 300 shares to less than 3,000 shares, and 5,000 yen for holdings of 3,000 shares or more.

🤖 AI Perspective

- The introduction of long-term holding benefits for shareholders may suggest the company’s aim to foster a stable and dedicated shareholder base.

- For investors, these enhanced benefits, which vary based on holding period and share count, could serve as an incentive for mid-to-long-term investment considerations.

- This strategic move could indicate the company’s intention to stabilize its ownership structure and enhance management sustainability by encouraging prolonged share retention.

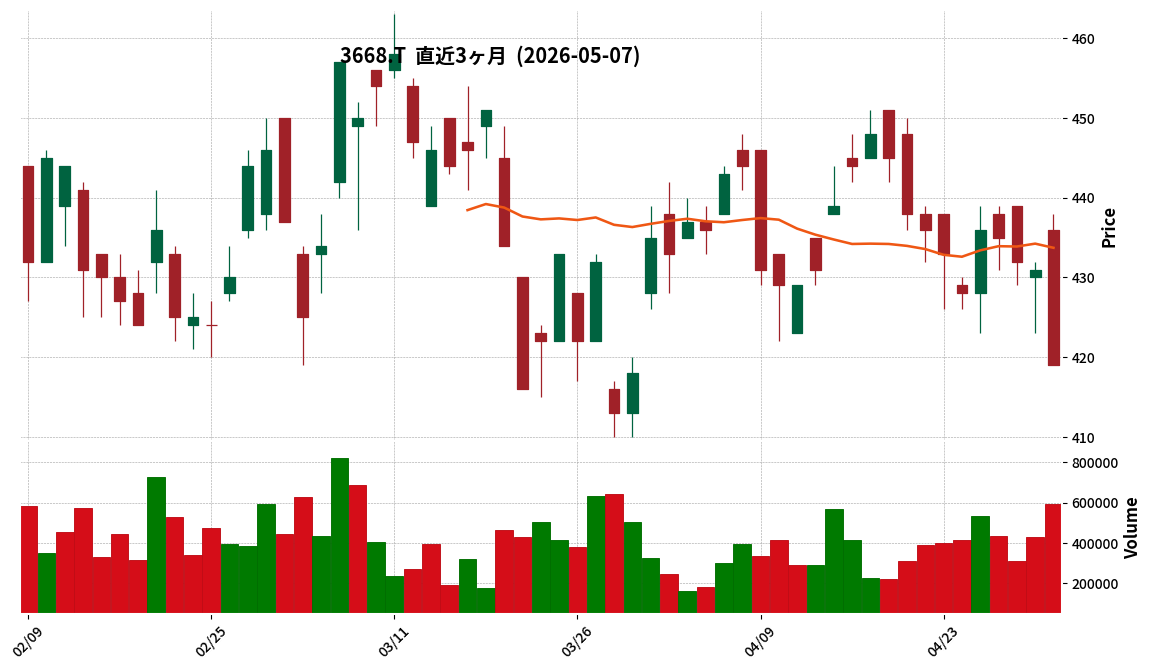

3668|コロプラ

419.0

▼ -2.78%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the second quarter of the fiscal year ending September 2026, Colopl reported consolidated net sales of ¥5.3 billion (down 39.1% year-on-year), operating profit of ¥0.6 billion (down 71.1% year-on-year), and ordinary profit of ¥0.9 billion (down 51.7% year-on-year).

- The Entertainment business segment recorded net sales of ¥5.1 billion (down 24.1% year-on-year) but achieved an operating profit of ¥0.7 billion (up 49.0% year-on-year) due to reduced advertising expenses.

- The Investment & Incubation business segment reported net sales of ¥0.1 billion (down 90.9% year-on-year) and an operating loss of ¥0.09 billion, reflecting the absence of a large exit seen in the prior year’s second quarter.

- The PC/console game “STEINS;GATE RE:BOOT” is scheduled for release on August 20, 2026.

- Colopl announced the development of a new app, “COLOPL Contents Protector,” aimed at protecting creations in the AI era.

🤖 AI Perspective

While consolidated results show a decline in revenue and profit largely due to the high base from a significant exit in the Investment & Incubation segment in the previous year, the Entertainment segment’s improved profitability through reduced advertising expenses suggests a potential shift in operational focus. The announcement of new titles like “STEINS;GATE RE:BOOT” and the “COLOPL Contents Protector” app could indicate strategic efforts towards diversifying revenue streams and addressing emerging industry challenges. The company’s high equity ratio of 92.5% points to a strong financial foundation, which may provide stability amidst these business shifts.

3984|ユーザーローカル

1600.0

▲ +3.90%

📎 Source:ユーザーローカル Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- User Local K.K. resolved to revise its year-end dividend forecast and introduce a shareholder benefit program at a Board of Directors meeting held on May 7, 2026.

- The year-end dividend forecast for the fiscal year ending June 2026 has been revised from the previous forecast of ¥10 to ¥14 per share, resulting in a total annual dividend forecast of ¥24.

- A new shareholder benefit program will be introduced, targeting shareholders who hold 100 shares (one unit) or more as of the record date (June 30th each year).

- The shareholder benefit consists of a uniform ¥3,000 digital gift®, redeemable for various options such as Amazon Gift Cards and Rakuten Point Gifts.

- The digital gift will be delivered within approximately three months from the record date (end of June) via mail, with recipients completing the selection process online.

🤖 AI Perspective

This announcement may suggest User Local’s enhanced commitment to shareholder returns. The revision of the dividend forecast combined with the introduction of a new shareholder benefit program could be seen as an effort to increase the appeal to individual investors and encourage long-term stock ownership. The digital gift format offers diverse choices, which is expected to enhance convenience for shareholders.

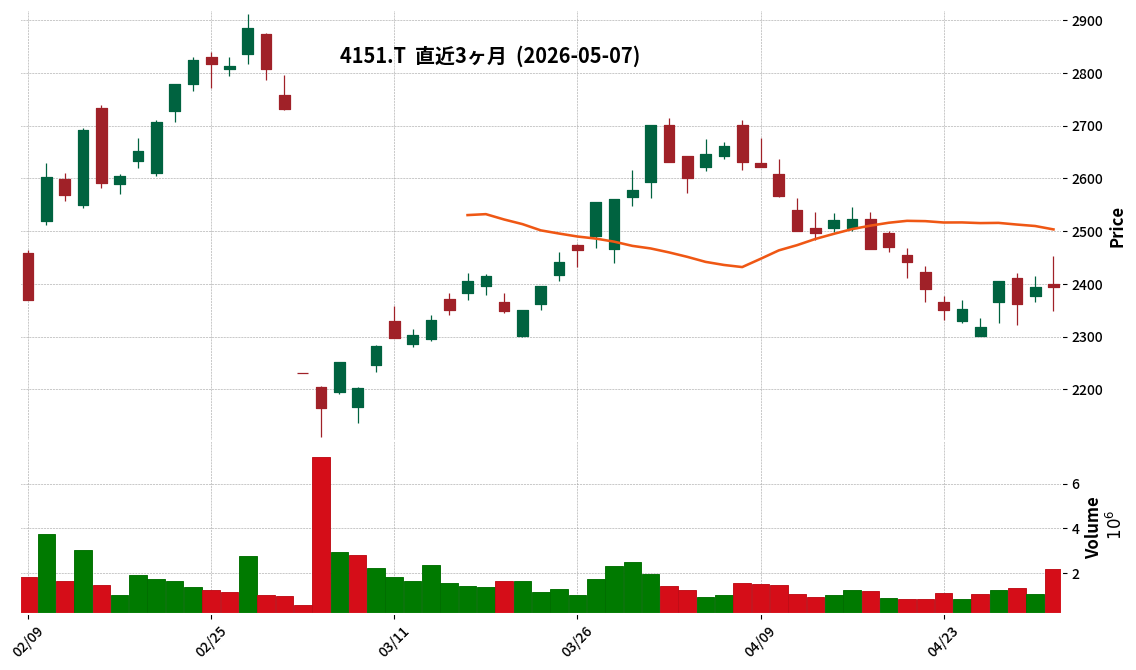

4151|協和キリン

2393.5

▼ -0.02%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kyowa Kirin announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1 to March 31, 2026).

- Revenue reached JPY 118,467 million (up 13.1% year-on-year), Core Operating Profit was JPY 20,014 million (up 78.3% year-on-year), and Net Profit attributable to owners of the parent company was JPY 12,034 million (up 95.1% year-on-year).

- The increase in revenue was primarily driven by the strong performance of global strategic products, mainly in North America and EMEA, as well as an increase in technology revenue. Foreign exchange had a positive impact of JPY 2.6 billion on revenue.

- The rise in Core Operating Profit was due to an increase in gross profit, stemming from higher overseas revenue and technology revenue, coupled with a decrease in R&D expenses. Foreign exchange had a positive impact of JPY 0.9 billion on Core Operating Profit.

- The consolidated full-year forecast for FY2026 has been revised, projecting revenue of JPY 520,000 million (up 4.7% year-on-year) and Core Operating Profit of JPY 130,000 million (up 18.4% year-on-year). The annual dividend forecast remains unchanged at JPY 70.00 per share (JPY 35.00 for year-end).

🤖 AI Perspective

The significant increase in key profit indicators for Kyowa Kirin’s first quarter suggests strong operational performance, potentially driven by its global strategic product portfolio. Investors may also note the revised definition of core performance indicators, which has been applied retrospectively for comparison. The revision of the full-year consolidated earnings forecast could indicate the company’s updated outlook on market conditions and business prospects for the remainder of the fiscal year.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

4475|G-HENNGE

955.0

▲ +0.00%

📎 Source:G-HENNGE Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the six months ended March 31, 2026 (Q2 FY2026), consolidated net sales reached JPY 6,129 million, representing a 17.7% increase year-on-year. Revenue from the HENNGE One business specifically grew by 19.2% to JPY 5,792 million.

- Consolidated operating profit was JPY 810 million, up 10.8% year-on-year, and net profit attributable to owners of the parent was JPY 884 million, a 11.7% increase.

- HENNGE One’s Annual Recurring Revenue (ARR) reached JPY 11.90 billion, an increase of JPY 770 million from the end of the previous fiscal year. The number of contracted companies increased by 304 to 3,731, and contracted users grew by 164,000 to 2.964 million.

- The average monthly churn rate for HENNGE One over the past 12 months improved by 0.06 percentage points from the end of the previous fiscal year, reaching 0.26%.

- The company launched a new service, “HENNGE Endpoint & Managed Security,” in March 2026 and added e-learning functions to “HENNGE Tadrill” in February 2026. Financial cash flow was impacted by expenditures related to treasury stock acquisition.

🤖 AI Perspective

The strong performance of the HENNGE One business, demonstrated by robust growth in revenue, ARR, contracted companies, and users, appears to be the primary driver of the company’s overall financial results. The consistently low average monthly churn rate of 0.26% could indicate a stable revenue base and high customer retention. The introduction of new services and enhanced functionalities suggests ongoing investment in future business expansion.

4746|東計電算

4320.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Toukei Computer recorded consolidated net sales of 5,483 million yen for the first quarter of the fiscal year ending December 2026 (January 1, 2026 to March 31, 2026), marking a 4.3% increase year-on-year.

- During the same period, operating profit rose to 1,695 million yen (+6.7%), ordinary profit to 1,836 million yen (+7.6%), and net profit attributable to owners of the parent company to 1,475 million yen (+18.0%).

- By segment, Information Processing and Software Development Services reported sales of 5,003 million yen (+4.0%), and Equipment Sales recorded sales of 396 million yen (+11.3%).

- The Leasing and Other Businesses segment reported an operating profit of 3 million yen (-80.7%), influenced by brokerage fees from the partial sale of rental properties.

- The consolidated earnings forecasts for the fiscal year ending December 2026 (full year and second quarter cumulative) remain unchanged from the most recently announced figures.

🤖 AI Perspective

Toukei Computer’s first quarter results show solid growth, particularly in its core Information Processing and Software Development Services, driven by robust system operation services. The increase in hardware replacement demand also supported strong performance in the Equipment Sales segment. The decline in operating profit for Leasing and Other Businesses appears to be due to specific, possibly one-off, transactions related to real estate sales. The reaffirmation of the full-year forecast indicates that the company maintains its outlook despite these segment-specific developments.

5187|クリエート

1202.0

▲ +0.59%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- CREATE MEDIC’s consolidated net sales for the first quarter of the fiscal year ending December 2026 amounted to 3,364 million yen, marking a 4.5% increase year-on-year.

- For the same quarter, consolidated operating profit was 140 million yen (down 36.6% YoY), ordinary profit was 169 million yen (down 21.3% YoY), and net profit for the quarter was 153 million yen (down 26.7% YoY).

- While net sales performed strongly due to new urology products in self-sales and increased urology product exports, profit declined due to higher cost of sales (impact of foreign exchange and sales mix) and an increase in selling, general and administrative expenses from upfront investments in new businesses, overseas strategies, information systems, and logistics.

- The company established an Indian sales subsidiary, “CREATE MEDIC INDIA PVT.LTD.,” on April 7, 2026, aiming to develop the Indian market as part of its medium-term priority of strengthening overseas business.

- The consolidated full-year forecast for the fiscal year ending December 2026 projects net sales of 13,960 million yen (up 2.5% YoY) and operating profit of 1,060 million yen (up 5.5% YoY). The company also revised its shareholder return policy, aiming to increase the dividend on equity (DOE) to 4% over the medium to long term, while maintaining a consolidated payout ratio of approximately 50.0%.

🤖 AI Perspective

CREATE MEDIC’s first quarter results for FY2026 indicate robust revenue growth, but profits were temporarily pressured by increased costs due to foreign exchange fluctuations and strategic investments. Nonetheless, the establishment of an Indian sales subsidiary and plans for new product launches underscore the company’s commitment to strengthening its overseas business, in line with its medium- to long-term management plan. The revised shareholder return policy, targeting a higher DOE while maintaining a payout ratio, also suggests a focus on enhancing shareholder value.

6549|ディーエムソリュ

1720.0

▲ +0.00%

📎 Source:ディーエムソリュ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- DM Solutions Co., Ltd. announced on May 7, 2026, a resolution by its Board of Directors to revise the dividend forecast for the fiscal year ending March 2026.

- The year-end dividend forecast for the fiscal year ending March 2026 has been revised upward by 6 yen, from the previously announced 15 yen (published August 8, 2025) to 21 yen per share.

- Consequently, the full-year dividend for the fiscal year ending March 2026 is projected to be 36 yen, an increase from the previously forecast 30 yen.

- The revision is based on the company’s fundamental dividend policy, which prioritizes growth investment for mid-to-long-term business expansion and enhancement of corporate value, alongside a comprehensive consideration of factors including the upward revision of the consolidated earnings forecast for FY2026 announced on the same day.

🤖 AI Perspective

This dividend forecast revision, coinciding with an upward revision of the full-year earnings forecast for FY2026, may suggest the company’s commitment to enhancing shareholder returns in line with its stated dividend policy. The increased annual dividend could be viewed as a positive indicator of the company’s financial health and its intent to share profit growth with investors. This development is worth monitoring for investors considering the company’s approach to capital allocation.

6809|TOA

1780.0

▲ +1.89%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- TOA Corporation resolved to revise its year-end dividend forecast (an increase) for the fiscal year ending March 2026 at a Board of Directors meeting held on May 7, 2026.

- The revised year-end dividend forecast is JPY 50.00 per share (JPY 45.00 as stable dividend + JPY 5.00 as performance-linked dividend). This represents an increase of JPY 2.00 from the previous forecast of JPY 48.00 announced on March 18, 2026.

- Consequently, the revised annual dividend forecast for the fiscal year ending March 2026 is JPY 90.00 per share, an increase of JPY 2.00 from the previous forecast of JPY 88.00.

- The reason for the dividend forecast revision is the upward adjustment of the performance-linked dividend, reflecting the consolidated operating results for the fiscal year ending March 2026 exceeding previous expectations, in conjunction with a consolidated dividend payout ratio of 85%.

- The company’s dividend policy is to maintain a stable annual dividend of JPY 85.00 as a base, and to determine the dividend based on either this stable amount or a consolidated dividend payout ratio of 85%, whichever is higher. The stable dividend is to be 5% or more of the consolidated dividend on equity (DOE).

🤖 AI Perspective

This upward revision of the dividend forecast suggests that TOA Corporation’s consolidated performance for the fiscal year ending March 2026 has been stronger than initially anticipated. The company’s policy to link dividends to a consolidated payout ratio of 85% and maintain a stable dividend based on a DOE of 5% or more indicates a commitment to shareholder returns that are responsive to both business performance and capital efficiency. This structured approach to shareholder distribution may be a point of interest for investors monitoring the company’s financial management.

6853|共和電

777.0

▲ +4.86%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of the fiscal year ending December 2026 (January 1 to March 31, 2026), Kyowa Electronic Instruments reported consolidated net sales of JPY 4,653 million, a 3.2% increase year-on-year.

- Operating profit decreased by 10.7% to JPY 633 million, and ordinary profit decreased by 7.2% to JPY 647 million, primarily due to rising raw material costs and increased selling, general, and administrative expenses.

- Net income attributable to owners of parent increased by 15.5% to JPY 551 million, largely attributed to the recognition of gain on sale of investment securities as an extraordinary profit.

- The company maintains its full-year consolidated earnings forecast (net sales JPY 16,500 million, net income attributable to owners of parent JPY 1,200 million) and annual dividend forecast of JPY 21.00 per share, with no revisions from the previously announced figures.

- By segment, the Measurement Instruments segment recorded sales of JPY 4,231 million (up 4.1%), while the Consulting segment saw sales of JPY 421 million (down 5.0%).

🤖 AI Perspective

Kyowa Electronic Instruments’ Q1 results show continued revenue growth, but operating and ordinary profits declined, which may suggest pressure from rising raw material costs and increased selling, general, and administrative expenses. The significant increase in net income was supported by an extraordinary gain from the sale of investment securities, indicating a one-time factor in the overall profitability. As the full-year earnings forecast remains unchanged, the company’s ability to manage ongoing cost challenges and progress in order intake could be worth monitoring.

8012|長瀬産

1203.5

▲ +2.29%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026 (consolidated), Nagase & Co. reported net sales of JPY 972,783 million (up 2.9% year-on-year), operating profit of JPY 44,727 million (up 14.5%), ordinary profit of JPY 44,096 million (up 14.9%), and profit attributable to owners of parent of JPY 33,119 million (up 29.8%).

- The annual dividend for the fiscal year ended March 31, 2026, was JPY 100.00 per share, including a year-end dividend of JPY 55.00 (compared to JPY 90.00 in the previous fiscal year).

- The consolidated earnings forecast for the fiscal year ending March 31, 2027, includes net sales of JPY 1,000,000 million (up 2.8% year-on-year), operating profit of JPY 45,000 million (up 0.6%), and profit attributable to owners of parent of JPY 34,500 million (up 4.2%).

- A stock split at a ratio of four shares for every one common share was implemented on April 1, 2026.

- Significant changes in the scope of consolidation during the period included the addition of 8 companies and the exclusion of 6 companies.

🤖 AI Perspective

Nagase & Co.’s financial results for the fiscal year ended March 31, 2026, indicate a robust performance with increases across sales and all profit metrics, notably a significant rise in profit attributable to owners of parent. The forecast for the next fiscal year suggests an expectation of continued revenue and profit growth, which may be viewed as a positive sign regarding ongoing business expansion. Additionally, the execution of a stock split could enhance stock liquidity and broaden the investor base by making individual investment units more accessible.

7609|ダイトロン

3380.0

▲ +7.64%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of the fiscal year ending December 2026 (January 1 to March 31, 2026), Daitron Corporation reported consolidated net sales of ¥30,338 million, representing a 29.9% increase compared to the same period last year.

- Consolidated operating income increased by 57.0% to ¥2,465 million, ordinary income by 68.2% to ¥2,531 million, and net income attributable to owners of parent by 67.2% to ¥1,740 million year-on-year.

- The company has revised its full-year consolidated earnings forecast for the fiscal year ending December 2026 upwards, projecting net sales of ¥110,000 million and net income attributable to owners of parent of ¥5,250 million.

- A 2-for-1 stock split of common shares was implemented effective January 1, 2026. The revised annual dividend forecast for FY2026 (post-split) is ¥95.00 per share.

- In terms of segment performance, the domestic sales segment recorded net sales of ¥23,721 million (up 36.1% year-on-year) and segment profit of ¥2,034 million (up 73.4% year-on-year).

🤖 AI Perspective

Daitron’s robust first-quarter results, demonstrating significant year-on-year growth across all key profitability metrics and an upward revision of the full-year forecast, may suggest a strong operational start to the fiscal year. This performance could be attributed to resilient demand in the electronics industry, particularly for advanced semiconductors and manufacturing equipment, driven by the expanding generative AI market. The implemented stock split could aim to enhance share liquidity and broaden the company’s investor base.

2335|キューブシステム

1021.0

▲ +1.09%

📎 Source:キューブシステム Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Cube System Co., Ltd. re-resolved at its Board of Directors meeting held on May 7, 2026, to amend and increase its year-end dividend for the fiscal year ended March 2026.

- The year-end dividend per share has been revised from the initially determined ¥22.00 to ¥26.00. This brings the total annual dividend, including the interim dividend of ¥20.00, to ¥46.00.

- The total dividend amount will be ¥409 million, an increase from the ¥346 million announced on April 28, 2026.

- The reason for the dividend increase is attributed to the corporate tax burden falling below expectations due to tax effect accounting procedures, resulting in net income attributable to parent company shareholders exceeding the initial forecast.

- The consolidated dividend payout ratio based on the re-resolved dividend is 44.5%.

🤖 AI Perspective

This re-resolution to increase the dividend is understood to be a result of lower corporate tax burden from tax effect accounting, which boosted net income, leading to enhanced shareholder returns. The upward revision from the initial decision may signal to investors a proactive stance towards shareholder remuneration. The reported consolidated dividend payout ratio of 44.5% could be seen as a move closer to the company’s stated basic policy of targeting a consolidated payout ratio of approximately 50%.

3175|APHD

917.0

▲ +0.11%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- APHD (A.P. Holdings Co., Ltd.) announced an upward revision to its consolidated full-year earnings forecast for the fiscal year ending March 2026, from the figures previously disclosed on May 15, 2025.

- The revised forecast includes Net Sales of ¥21.8 billion (an increase of 9.0% from the previous forecast), Operating Profit of ¥840 million (up 75.0%), Ordinary Profit of ¥720 million (up 89.5%), and Profit attributable to owners of parent of ¥1.08 billion (up 66.2%).

- Key reasons for the revision include successful operations focused on existing domestic restaurants, strong results from year-end and New Year reservation strategies, the Hong Kong business achieving monthly profitability following restructuring, and improved profit structure through optimized personnel allocation and cost reductions.

- The company recorded approximately ¥438 million in gain on sale of shares of affiliated companies as extraordinary income, resulting from the transfer of all shares in its consolidated subsidiary, Real Taste Co., Ltd., to FS.shake Co., Ltd.

- The timing of this upward revision, ahead of the financial results announcement, was due to the finalization of various expenses and end-of-period results, which allowed for a reasonable calculation, despite multiple uncertainties that remained during the fourth quarter (e.g., renovation/store closure costs, final costs of overseas business restructuring).

🤖 AI Perspective

- This upward revision to the earnings forecast may suggest the positive impact of robust domestic dining operations and the progress of structural reforms in overseas businesses on the company’s profitability.

- The recognition of an extraordinary gain of approximately ¥438 million from the sale of shares in an affiliated company appears to be a significant factor contributing to the increase in net profit.

- The announcement, made after various uncertainties from the fourth quarter were resolved, indicates the company’s commitment to providing accurate information to investors.

3326|ランシステム

685.0

▼ -1.30%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Runsystem Co., Ltd. announced its consolidated financial results for the fiscal year ended March 2026. Net sales were ¥5,430 million (up 0.4% year-on-year), and operating profit reached ¥173 million (up 38.3% year-on-year).

- Net profit attributable to owners of the parent significantly increased by 134.5% year-on-year to ¥101 million, while ordinary profit was ¥106 million (down 4.8% year-on-year).

- By segment, the Entertainment business reported a segment profit of ¥267 million (up 42.0% year-on-year), and the System business recorded a segment profit of ¥184 million (up 24.4% year-on-year).

- As of March 31, 2026, consolidated total assets stood at ¥4,177 million, net assets at ¥321 million, and the equity ratio improved to 7.7% (from 5.8% at the end of the previous fiscal year).

- For the fiscal year ending March 2027, the company forecasts consolidated net sales of ¥4,800 million (down 11.6% year-on-year), while expecting operating profit of ¥180 million (up 3.5% year-on-year) and net profit attributable to owners of the parent of ¥110 million (up 8.1% year-on-year).

🤖 AI Perspective

The FY2026/3 results indicate a notable improvement in operating and net profit despite modest sales growth, which may suggest enhanced operational efficiency. The strong segment profit growth in both the Entertainment and System businesses appears to have been a key contributor to the overall profit increase. The improvement in the equity ratio could also be viewed as a positive development for the company’s financial stability. While the FY2027/3 forecast anticipates a decrease in sales, the projected increase in profits may imply a continued focus on profitability and optimized operations.

9425|ReYuuJapan

353.0

▲ +29.30%

📎 Source:ReYuuJapan Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- ReYuu Japan announced the signing of a Memorandum of Understanding (MOU) with Super Micro Computer, Inc. (Supermicro) on April 28, 2026, aimed at exploring a business alliance for AI infrastructure.

- Under this MOU, both companies will explore sharing business and technical know-how related to AI servers and infrastructure, the possibility of entering the AI data center business utilizing Supermicro’s GPU servers, and cooperation for sales and business development of AI servers and related infrastructure in the Japanese market.

- Supermicro is a global provider of servers, storage, networking, and comprehensive IT solutions for AI, cloud, and data centers.

- ReYuu Japan, primarily engaged in the reuse business for communication and IT equipment, seeks to explore business expansion opportunities in the AI infrastructure sector through this MOU.

- The company stated that this MOU is expected to have a minor impact on its current fiscal year’s performance, and the specific timing for business commencement is yet to be determined.

🤖 AI Perspective

- This MOU suggests ReYuu Japan’s strategic move to explore entry into the rapidly growing AI infrastructure sector, complementing its existing reuse business.

- Collaboration with Supermicro, a globally recognized leader in high-performance GPU servers, could potentially enhance ReYuu Japan’s capabilities and market position in this domain.

- Investors may view this as an initial step towards building new business models to meet expanding AI computing infrastructure demand in Japan, making future developments worth monitoring.

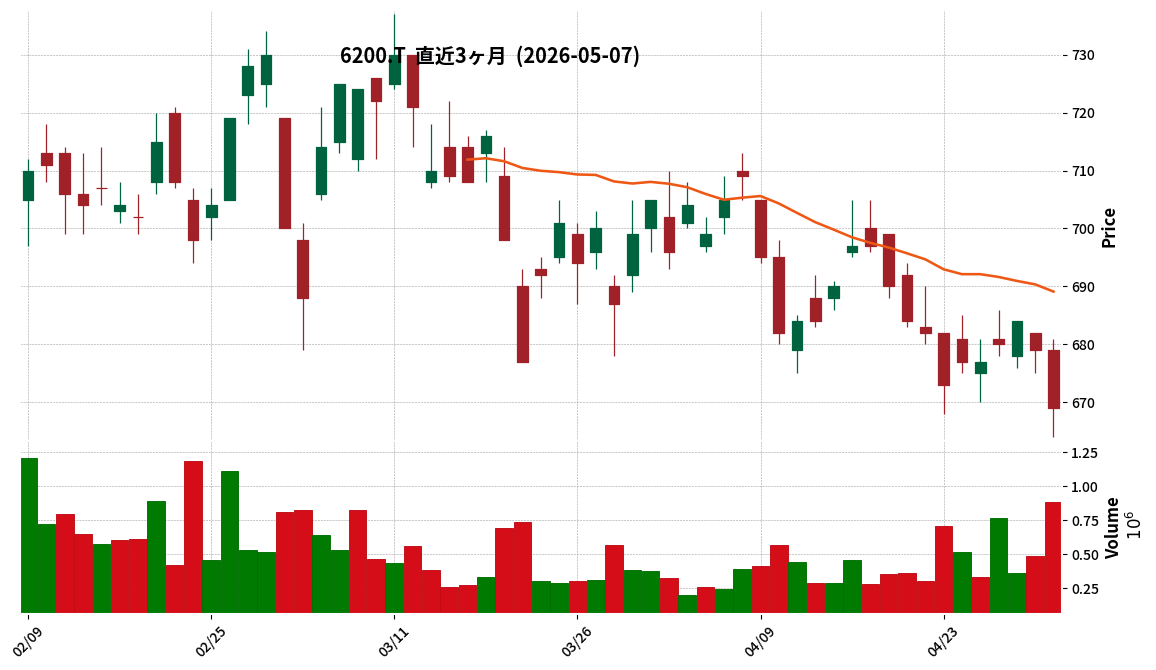

6200|インソース

669.0

▼ -1.47%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Insource Inc. announced its consolidated financial results for the second quarter of the fiscal year ending September 2026 on May 7, 2026.

- For the cumulative period (October 1, 2025 – March 31, 2026), consolidated net sales were ¥7,584 million (up 8.0% year-on-year), operating profit was ¥2,951 million (up 0.3% year-on-year), ordinary profit was ¥2,972 million (up 0.5% year-on-year), and net profit attributable to parent company shareholders was ¥2,027 million (up 3.1% year-on-year).