📌 Today’s Highlights

Today we cover 50 IR announcements. Notable among them: エスプール (2471), 出前館 (2484), IKホールディングス (2722). Use the table of contents below to navigate to each company.

- 2471|エスプール

- 2484|出前館

- 2722|IKホールディングス

- 2752|フジオフードG本社

- 2882|イートアンドHD

- 2927|AFC-HD

- 2928|A-RIZAP G

- 2934|G-Jフロンティア

- 2936|G-ベースフード

- 3021|PCNET

- 3045|カワサキ

- 3086|Jフロント

- 135A|G-VRAIN

- 1418|インターライフ

- 190A|G-Chordia

- 244A|G-グロースエクスパ

- 245A|G-INGS

- 2798|Y’s

- 280A|G-TMH

- 304A|G-フォルシア

- 3198|SFPHD

- 3266|ファンドクリG

- 351A|P-アクシスITP

- 3675|クロスマーケティング

- 3697|SHIFT

- 4016|MITHD

- 414A|G-オーバーラップ

- 4197|アスマーク

- 4382|HEROZ

- 4415|G-ブロードエンター

- 4429|G-リックソフト

- 457A|P-ルリアン

- 4885|室町ケミカル

- 5527|G-propetec

- 6025|日本PCサービス

- 4413|ボードルア

- 274A|ガーデン

- 3189|ANAP

- 3290|R-Oneリート

- 4017|G-クリーマ

- 144A|P-エネルギーパワー

- 3557|G-U&C

- 3826|SI

- 4444|G-インフォネット

- 5574|G-ABEJA

- 329A|P-ジール

- 470A|P-ローカル

- 5025|G-マーキュリー

- 3823|WHY HOW DO

- 469A|G-フィットクルー

2471|エスプール

258.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Spool Inc. reported consolidated net revenue of ¥5,938 million for Q1 FY2026 (down 3.2% year-on-year) and operating profit of ¥36 million (down 85.9% year-on-year).

- Quarterly profit attributable to owners of the parent recorded a loss of ¥68 million (compared to a profit of ¥98 million in the same period last year).

- By segment, the Business Solutions segment posted net revenue of ¥3,755 million (up 1.8% year-on-year) but an operating profit of ¥408 million (down 26.0% year-on-year).

- The Environmental Management Support Service experienced a significant decrease in revenue and profit due to the absence of large-lot carbon credit sales, while the Support Service for Employment of Persons with Disabilities saw increased revenue, and the Wide-Area Administrative BPO Service achieved substantial sales growth.

- The full-year consolidated earnings forecast for FY2026 and the annual dividend forecast (¥10.00) remain unchanged from the most recently announced figures.

🤖 AI Perspective

While consolidated net revenue and profit decreased year-on-year, the company stated that profits exceeded initial plans, suggesting ongoing efforts in portfolio management. The mixed performance within the Business Solutions segment across different services indicates varied underlying dynamics. The continued progress in growth areas such as the Support Service for Employment of Persons with Disabilities and Wide-Area Administrative BPO Service could be key for achieving full-year targets.

2484|出前館

128.0

▲ +1.59%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Demae-Can Co., Ltd. announced its consolidated financial results for the second quarter (interim period) of the fiscal year ending August 2026 on April 14, 2026. The reporting period covered September 1, 2025, to February 28, 2026.

- For the interim period, net sales totaled JPY 17,979 million, marking a 13.9% decrease compared to the same period of the previous fiscal year.

- The company reported an operating loss of JPY 3,200 million (compared to an operating loss of JPY 1,286 million in the prior year interim period), an ordinary loss of JPY 3,174 million, and a net loss attributable to owners of parent of JPY 3,179 million.

- The consolidated full-year performance forecast for the fiscal year ending August 2026 remains unchanged from the forecast disclosed in the “Financial Results for the Fiscal Year Ended August 2025” on October 15, 2025 (Net sales: JPY 44,100 million, Operating loss: JPY 4,000 million, Net loss attributable to owners of parent: JPY 4,000 million).

- Effective from the second quarter of the fiscal year ending August 2025, the company has adopted an accounting treatment where sales promotion expenses for value-added coupons issued to specific users are deducted from net sales.

🤖 AI Perspective

The reported decline in net sales and expansion of losses for the interim period may reflect the impact of market competition, evolving consumer behavior, and the new accounting treatment for sales promotion expenses. Investors might consider the unchanged full-year forecast as an indication of the company’s expectations regarding its ongoing strategies for cost optimization and service enhancements. The increase in the self-capital ratio to 74.8% from the previous fiscal year-end could suggest a stable financial position despite the reported losses.

2722|IKホールディングス

390.0

▲ +0.00%

📎 Source:IKホールディングス Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the third quarter of FY2026 (June 1, 2025 – February 28, 2026), consolidated net sales were ¥11,120 million (down 2.9% year-on-year), operating profit was ¥199 million (down 42.5%), and ordinary profit was ¥173 million (down 48.6%).

- Net profit attributable to owners of parent was ¥253 million (down 3.4% year-on-year), benefiting from the recording of a deferred tax asset (income) of ¥230 million due to the completion of group reorganization.

- The consolidated full-year forecast for FY2026 has been revised to net sales of ¥14,700 million (down 3.4% year-on-year), operating profit of ¥260 million (down 38.8%), ordinary profit of ¥230 million (down 44.7%), and net profit attributable to owners of parent of ¥280 million (down 12.8%). This is a revision from the previous forecast announced on January 13, 2026.

- The year-end dividend forecast remains unchanged at ¥9.00 per share.

- During the cumulative third quarter, there was a significant change in the scope of consolidation, with Prime Direct Co., Ltd. being added and excluded as one new company.

🤖 AI Perspective

- While sales, operating profit, and ordinary profit declined year-on-year, the smaller decrease in net profit attributable to owners of parent appears to be influenced by the recording of a deferred tax asset from group reorganization.

- The revision of the full-year earnings forecast suggests that investors may focus on the progress of future business strategies and profit improvement measures.

- Segment-wise, the Direct Marketing business achieved a significant increase in operating profit despite a decrease in sales, whereas the Sales Marketing business saw increased sales but decreased operating profit, indicating evolving business dynamics.

2752|フジオフードG本社

1083.0

▼ -1.37%

📎 Source:フジオフードG本社 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Fujio Food System Co., Ltd. announced on April 14, 2026, the financial results of its unlisted parent company, FM Commercial Planning Co., Ltd., as of December 31, 2025.

- FM Commercial Planning Co., Ltd. holds 26.35% of Fujio Food System’s voting rights, and Masahiro Fujio serves as representative director for both companies.

- The summary balance sheet as of December 31, 2025, showed total assets of ¥2,213,554 thousand and total net assets of ¥501,763 thousand.

- For the fiscal year ended December 2025, the summary income statement reported a net loss of ¥43,464 thousand on sales revenue of ¥51,083 thousand.

- The major shareholders of FM Commercial Planning Co., Ltd. are Hideo Fujio (60.0%) and Sachiko Taka (40.0%).

🤖 AI Perspective

* The disclosure of financial information for an unlisted parent company of a listed entity is considered important for enhancing transparency regarding corporate governance and control relationships.

* While the parent company’s financials are not consolidated, its financial health, business activities, and major shareholder structure may be relevant for understanding the indirect control structure of the listed company.

* The reported net loss by the parent company, alongside its business overview and asset composition, could serve as a data point for investors monitoring the broader corporate group’s situation.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

2882|イートアンドHD

1978.0

▼ -0.75%

📎 Source:イートアンドHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended February 2026, Eat & And Holdings reported consolidated net sales of ¥40,456 million (up 8.4% year-on-year), operating profit of ¥1,142 million (up 4.7%), and ordinary profit of ¥1,101 million (up 11.6%), achieving record-high profits since listing.

- Net profit attributable to owners of parent decreased by 58.0% to ¥373 million, primarily due to the recording of “insurance income from fire” in the previous fiscal year.

- The food business segment achieved sales of ¥23,197 million (up 8.1% year-on-year) and segment profit of ¥1,288 million (up 14.4%).

- The consolidated earnings forecast for the fiscal year ending February 2027 projects net sales of ¥43,000 million (up 6.3% year-on-year), operating profit of ¥1,250 million (up 9.4%), and net profit attributable to owners of parent of ¥455 million (up 21.9%).

- The annual dividend per share for FY2026/2 was ¥15.00, with the forecast for FY2027/2 also set at ¥15.00.

🤖 AI Perspective

- The company achieved record-high net sales, operating profit, and ordinary profit in FY2026/2, suggesting that the core food business was a significant driver of performance.

- The decrease in net profit appears to be primarily attributable to a one-off gain in the prior year, indicating that the underlying profitability from operations remained robust.

- The positive outlook for FY2027/2, projecting continued revenue and profit growth, could be supported by ongoing initiatives such as new factory construction and the introduction of cooking robots aimed at enhancing production capabilities and profitability.

2927|AFC-HD

874.0

▼ -0.34%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- AFC-HD AMS Life Science Co., Ltd. announced an upward revision to its consolidated full-year earnings forecast for the fiscal year ending August 2026 (September 1, 2025 – August 31, 2026) on April 14, 2026.

- Net income attributable to owners of parent is revised upward by JPY 83 million (5.7% increase) from the previous forecast of JPY 1,462 million to the revised forecast of JPY 1,545 million.

- Earnings per share (EPS) is revised upward by JPY 2.40 (2.3% increase) from the previous forecast of JPY 103.73 to the revised forecast of JPY 106.13.

- There were no revisions to the forecasts for net sales, operating profit, or ordinary profit.

- The revision is attributed to an increase in deferred tax assets of a subsidiary, which is expected to result in a higher net income attributable to owners of parent due to the application of tax effect accounting.

🤖 AI Perspective

This earnings forecast revision, while not altering revenue or operating profit figures indicative of core business performance, suggests a positive change in the company’s tax position. The increase in deferred tax assets of a subsidiary could imply an improved outlook for future taxable income or a more efficient tax structure. Investors might consider this tax-related adjustment as a factor influencing the reported net profit, and further details in future reports could provide additional context regarding the underlying business conditions.

2928|A-RIZAP G

—

▲ +0.00%

📎 Source:A-RIZAP G Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- RIZAP Group, Inc. (Code: 2928) announced on April 14, 2026, that it will hold an online financial results briefing for the fiscal year ending March 2026.

- The financial results will be released on Thursday, May 14, 2026, with the online briefing scheduled for the same day from 17:00 to 18:00 JST (tentative).

- To view the briefing, pre-registration is required via a dedicated URL (https://us06web.zoom.us/webinar/register/WN_fWGwD5UhTOyWgK08pUFSaA). An archived video will be made available on the company’s website after the live broadcast.

- The company is accepting questions in advance for the briefing, with the submission period from 15:30 JST on Tuesday, April 14, 2026, to 18:00 JST on Monday, May 11, 2026.

- Questions can be submitted via a dedicated form or email (qa@rizapgroup.com), with priority given to inquiries regarding financial results, business operations, and future management policies.

🤖 AI Perspective

This announcement aims to provide prompt and fair information disclosure to shareholders and investors, with the online format potentially enhancing accessibility for a wider audience. The acceptance of pre-submitted questions may also indicate the company’s commitment to addressing specific investor concerns, which could be seen as an effort to improve transparency in its investor relations activities.

2934|G-Jフロンティア

1616.0

▲ +0.06%

📎 Source:G-Jフロンティア Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the nine months ended February 28, 2026 (Q3 FY2026 cumulative), consolidated net sales were ¥16,381 million, representing a 0.2% increase year-on-year.

- During the same period, consolidated EBITDA increased by 18.7% to ¥777 million, operating profit by 50.8% to ¥304 million, and ordinary profit by 99.9% to ¥351 million.

- Net profit attributable to owners of parent decreased by 30.3% to ¥84 million.

- By segment, the Healthcare Marketing business reported sales of ¥8,303,394 thousand (+14.7% year-on-year) and segment EBITDA of ¥236,683 thousand (+41.8% year-on-year).

- The consolidated earnings forecast for the full fiscal year ending May 2026, including net sales of ¥23,600 million and operating profit of ¥327 million, remains unchanged from the previously announced figures.

- shake-hands Inc. was newly added to the scope of consolidation during this cumulative quarter.

2936|G-ベースフード

328.0

▼ -1.20%

📎 Source:G-ベースフード Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended February 2026, net sales were ¥15,191 million (down 0.3% YoY), while operating profit rose significantly by 59.3% to ¥217 million, ordinary profit increased by 116.2% to ¥267 million, and net profit surged by 140.8% to ¥262 million.

- Sales through the company’s own e-commerce channel increased by 3.2% YoY to ¥10,036 million, with the number of regular subscribers expanding to 235,000 and cumulative members surpassing 1 million.

- While wholesale channel sales decreased by 11.4% YoY to ¥3,949 million, sales via other e-commerce platforms grew by 12.1% YoY to ¥955 million, and overseas business sales increased by 18.8% YoY to ¥218 million.

- The company forecasts for the fiscal year ending February 2027 are net sales of ¥16,256 million (up 7.0% YoY) but operating profit of ¥62 million (down 71.4% YoY).

- The year-end dividend for both FY2026/2 and FY2027/2 (forecast) is ¥0.00.

🤖 AI Perspective

G-BASE FOOD’s FY2026/2 results show a significant improvement in profits despite a slight dip in sales, which may suggest effective cost management and optimized advertising strategies. For the upcoming fiscal year, the forecast of increased sales coupled with a sharp decline in operating profit could indicate planned strategic investments or changes in operational focus. Investors may want to monitor the impact of these factors on future profitability.

3021|PCNET

2402.0

▲ +3.18%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- PCNET announced on April 14, 2026, an upward revision to its consolidated earnings forecast for the fiscal year ending May 31, 2026 (June 1, 2025, to May 31, 2026).

- The revised forecast includes sales of JPY 10,300 million (+3.0% from previous), operating profit of JPY 1,350 million (+22.7%), ordinary profit of JPY 1,250 million (+25.0%), and profit attributable to owners of parent of JPY 846 million (+25.0%).

- The revision is attributed to strong performance across all segments, including the IT Subscription business and ITAD business, during the cumulative third quarter of the fiscal year ending May 2026.

- The IT Subscription business saw expanded orders driven by increasing demand for reduced IT equipment operation burdens, leading to stable growth in recurring revenue. The ITAD business benefited from increased used IT equipment arrivals due to OS upgrade demand and rising used PC prices amid new PC price hikes, improving profitability.

- The company anticipates that ongoing upfront investments in human capital and assets for future growth, as well as a planned special bonus payment to employees in Q4, can be fully absorbed by the current earnings progress.

🤖 AI Perspective

* The significant upward revision in profits, which outpaces the increase in sales, may suggest an improvement in the company’s overall profitability structure.

* The stable growth of the IT Subscription business and the ITAD business’s ability to capitalize on market opportunities appear to be key drivers behind this enhanced profitability.

* The company’s capacity to absorb upfront investments and a special bonus while still increasing profit could indicate robust underlying earnings power, making the execution of its ongoing business strategies noteworthy for investors.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

3045|カワサキ

1453.0

▲ +0.21%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the second quarter (interim period) of the fiscal year ending August 2026, Kawasaki (3045) reported net sales of ¥1,192 million (up 3.0% year-on-year), operating profit of ¥279 million (up 7.8% year-on-year), ordinary profit of ¥279 million (up 8.0% year-on-year), and interim net profit of ¥182 million (up 7.8% year-on-year).

- By segment, the Apparel Business recorded net sales of ¥302,915 thousand (up 3.5% year-on-year) and operating profit of ¥3,726 thousand (up 162.0% year-on-year). The Rental and Warehouse Business reported net sales of ¥695,559 thousand (up 0.9% year-on-year) and operating profit of ¥297,604 thousand (up 5.3% year-on-year). The Hotel Business’s net sales were ¥193,558 thousand (up 10.3% year-on-year), with an operating loss of ¥21,927 thousand, an improvement from the ¥24,917 thousand operating loss in the prior year period.

- The company’s financial position shows total assets of ¥7,981 million and net assets of ¥5,884 million, resulting in an equity ratio of 73.7% (up from 71.4% at the end of the previous fiscal year).

- The full-year forecast for the fiscal year ending August 2026 remains unrevised from the latest public announcement, projecting net sales of ¥2,233 million (down 2.5% from the previous fiscal year), operating profit of ¥432 million (down 16.1%), ordinary profit of ¥431 million (down 16.1%), and net profit of ¥279 million (down 17.5%).

- The interim dividend for FY2026 remains at ¥25.00, and the year-end dividend forecast is ¥25.00, maintaining the annual dividend forecast at ¥50.00.

🤖 AI Perspective

Kawasaki’s H1 FY2026 results show profit growth across all key metrics. The Apparel Business notably achieved significant profit improvement, and the Hotel Business reduced its losses, contributing to the overall positive performance. However, the full-year forecast anticipates a decrease in sales and profits compared to the previous fiscal year, suggesting that the company may be taking a cautious stance on the business environment in the latter half of the year, despite strong interim results. The high equity ratio indicates a stable financial foundation.

3086|Jフロント

2581.5

▲ +1.18%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended February 2026, J. Front Retailing Co., Ltd.’s consolidated gross transaction value was JPY 1,290.489 billion (up 1.7% year-on-year), and revenue was JPY 445.094 billion (up 0.7% year-on-year).

- Consolidated business profit was JPY 50.597 billion (down 5.4% year-on-year), operating profit was JPY 49.015 billion (down 15.8% year-on-year), and profit attributable to owners of the parent was JPY 28.282 billion (down 31.7% year-on-year).

- The annual dividend for FY2026/2 was announced at JPY 54 per share (up JPY 2 from the previous year), with a consolidated payout ratio of 47.8%.

- The consolidated earnings forecast for FY2027/2 projects gross transaction value of JPY 1,347.0 billion (up 4.4% year-on-year), revenue of JPY 469.0 billion (up 5.4% year-on-year), and profit attributable to owners of the parent of JPY 29.0 billion (up 2.5% year-on-year).

- A resolution for the acquisition of treasury shares was made at the Board of Directors meeting held on April 14, 2026.

🤖 AI Perspective

While revenue increased in FY2026/2, business profit, operating profit, and profit attributable to owners of the parent decreased. The annual dividend, however, increased for the period and is forecast to increase further next fiscal year. For the next fiscal year, although revenue is projected to grow, operating profit is expected to decline while profit attributable to owners of the parent is forecast to increase, which may reflect the impact of the treasury share acquisition.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

135A|G-VRAIN

2913.0

▲ +4.75%

📎 Source:G-VRAIN Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-VRAIN (VRAIN Solution, Inc.) reported record-high sales and operating profit for the fiscal year ended February 2026. Sales reached JPY 3,278 million (up 52.9% year-on-year), operating profit JPY 914 million (up 53.8% year-on-year), and net profit JPY 652 million (up 53.4% year-on-year).

- During FY2026, the company expanded its operational base by opening Sendai and Sapporo sales offices, operating Tokyo and Osaka factories, and releasing a new AI X-ray inspection machine, PX-1000N.

- The cumulative number of client companies increased by 104 from the previous fiscal year-end, totaling 337. Sales from recurring customers amounted to JPY 1,476 million, accounting for 45.0% of total sales. Order backlog reached JPY 1,269 million, an increase of 225.5% from the previous fiscal year-end.

- For the fiscal year ending February 2027, the company forecasts sales of JPY 4,823 million (up 47.1% year-on-year), operating profit of JPY 1,449 million (up 58.5% year-on-year), and net profit of JPY 972 million (up 49.2% year-on-year).

- The company plans to open five new sales offices in Utsunomiya, Nagano, Kanazawa, Hiroshima, and Fukuoka, and commence global expansion in FY2027.

🤖 AI Perspective

The strong performance in FY2026, with record-high sales and operating profit, suggests that the company’s strategic investments in operational expansion and new product development may be yielding positive results. The substantial increase in cumulative client companies, recurring customer sales, and order backlog could indicate robust underlying business growth. The ambitious forecasts for FY2027, coupled with planned domestic office expansions and the initiation of global expansion, highlight the company’s commitment to sustaining its growth trajectory.

1418|インターライフ

486.0

▼ -0.61%

📎 Source:インターライフ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Interlife Holdings announced its consolidated financial results for the fiscal year ended February 2026 (March 1, 2025, to February 28, 2026), reporting net sales of JPY 16,336 million, a 3.6% decrease from the previous fiscal year.

- For the same period, consolidated operating profit increased by 33.3% to JPY 1,166 million, ordinary profit rose by 32.1% to JPY 1,156 million, and profit attributable to owners of parent grew by 17.4% to JPY 828 million, marking a record-high profit.

- The annual dividend for the fiscal year ended February 2026 was JPY 30.00 per share (interim dividend of JPY 10.00 and year-end dividend of JPY 20.00), an increase from JPY 20.00 in the previous fiscal year.

- The consolidated earnings forecast for the fiscal year ending February 2027 projects net sales of JPY 17,000 million (up 4.1%), operating profit of JPY 1,200 million (up 2.8%), ordinary profit of JPY 1,190 million (up 2.9%), and profit attributable to owners of parent of JPY 800 million (down 3.4%).

- During the consolidated fiscal year, the company executed a business portfolio reorganization, divesting all shares of Tamako Kogyo Co., Ltd., which was involved in the equipment and maintenance business, resulting in its exclusion from the scope of consolidation.

🤖 AI Perspective

Despite a decrease in net sales, the significant increase in operating, ordinary, and net profits, with net profit reaching a record high, appears to be a key highlight for investors. This performance could suggest the positive impact of business portfolio restructuring and the completion of high-margin large-scale construction projects. While the forecast for the next fiscal year anticipates increased revenues and operating profits, a slight decrease in profit attributable to owners of parent is projected, which may warrant further attention in understanding the company’s future strategic direction.

190A|G-Chordia

128.0

▼ -0.78%

📎 Source:G-Chordia Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the H1 FY2026 (interim period), G-Chordia reported an operating loss of 662 million yen, an improvement of 334 million yen compared to 996 million yen in the previous year.

- Net loss for the period was 633 million yen (previous year: 976 million yen), showing an improvement of 343 million yen.

- R&D expenses decreased to 510 million yen (previous year: 799 million yen), primarily due to reduced raw material and formulation costs for rogocekib.

- The lead pipeline “rogocekib (CTX-712)” completed patient registration for 102 patients in Japan and the US by the end of February 2026, and the expansion cohort was initiated in the US.

- Cash and deposits stood at 2,447 million yen, supported by 499 million yen from the exercise of stock options.

🤖 AI Perspective

- The H1 FY2026 financial results indicate a significant reduction in losses compared to the previous year, primarily driven by decreased R&D and administrative expenses.

- Steady progress in the lead pipeline rogocekib’s clinical trials, including patient registration completion and the initiation of an expansion cohort in the US, suggests a transition to subsequent development phases.

- The company’s maintained cash and deposit levels, partly due to stock option exercises, could provide a stable financial foundation for ongoing pipeline development.

244A|G-グロースエクスパ

1192.0

▲ +0.08%

📎 Source:G-グロースエクスパ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-GROWTH EXPA Co., Ltd. announced its consolidated financial results for the second quarter of the fiscal year ending August 2026 (interim period, September 1, 2025 – February 28, 2026).

- Consolidated net sales were ¥2,402 million (down 1.7% year-on-year from the previous interim period), operating profit was ¥228 million (down 40.0%), ordinary profit was ¥253 million (down 35.7%), and net profit attributable to owners of parent was ¥155 million (down 39.2%).

- By business segment, sales in the “DX Promotion Support Business” decreased, while sales in the “DX Support Product and Service Business” expanded.

- As of the end of the interim period, consolidated total assets were ¥4,887 million, net assets were ¥3,643 million, and the equity ratio was 74.5%.

- The full-year consolidated performance forecast for the fiscal year ending August 2026 remains unchanged from the most recently announced figures: net sales of ¥5,608 million (up 10.3% year-on-year from the previous full year), operating profit of ¥801 million (up 3.6%), ordinary profit of ¥828 million (down 4.8%), and net profit attributable to owners of parent of ¥516 million (down 13.9%).

🤖 AI Perspective

The interim results showed a slight decrease in net sales but significant declines in operating profit and other profit items compared to the prior year. This appears to be mainly due to delays in some projects within the DX Promotion Support Business and strategic withdrawals from certain less profitable projects. Conversely, the expansion of the DX Support Product and Service Business helped to mitigate the overall sales decline. As the full-year consolidated earnings forecast remains unchanged, a recovery in the core business and further contributions from the product and service business in the second half are likely anticipated.

245A|G-INGS

2340.0

▼ -0.21%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-INGS announced its financial results for the second quarter of the fiscal year ending August 2026.

- For the interim accounting period (September 1, 2025 – February 28, 2026), consolidated net sales were ¥4.447 billion (up 22.5% year-on-year), operating income was ¥254 million (up 52.3% YoY), ordinary income was ¥244 million (up 78.4% YoY), and interim net income was ¥159 million (up 125.6% YoY).

- By segment, the Ramen business reported net sales of ¥2.423 billion (up 27.2% YoY) and segment profit of ¥212.822 million (up 45.4% YoY).

- The Restaurant business reported net sales of ¥2.024 billion (up 17.3% YoY) and segment profit of ¥41.363 million (up 101.5% YoY).

- The full-year forecast for the fiscal year ending August 2026 remains unchanged, projecting net sales of ¥9.590 billion (up 24.0% YoY) and net income of ¥339 million (up 24.8% YoY).

🤖 AI Perspective

The reported interim results indicate significant year-on-year increases across key profit metrics, suggesting continued business expansion. Both the Ramen and Restaurant segments showed growth in existing store sales and expansion in store count, which appears to be driving performance. The unchanged full-year forecast may suggest management’s confidence in their current projections.

2798|Y’s

2953.0

▼ -0.14%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

Y’s Co., Ltd. (code 2798) announced its consolidated financial results for the fiscal year ended February 2026 (March 1, 2025 – February 28, 2026).

* Consolidated revenue reached JPY 13,046 million, an increase of 7.6% compared to the previous fiscal year.

* Consolidated operating profit significantly increased by 109.5% year-on-year, totaling JPY 249 million.

* Consolidated ordinary profit was JPY 345 million, up 39.1% from the previous year.

* Profit attributable to owners of parent decreased by 21.3% to JPY 205 million, primarily due to the reversal of deferred tax assets.

* For the fiscal year ending February 2027, the company forecasts consolidated revenue of JPY 15,446 million (up 18.4% year-on-year), operating profit of JPY 424 million (up 70.4% year-on-year), and profit attributable to owners of parent of JPY 422 million (up 105.7% year-on-year).

🤖 AI Perspective

The FY2026 results indicate robust growth in revenue and operating profit, with the decline in net profit attributed to a specific accounting adjustment rather than operational performance. This suggests an improvement in underlying business profitability, while highlighting the impact of non-operating factors on the bottom line. The strong full-year guidance for FY2027, anticipating significant increases across key profit metrics, could suggest management’s confidence in continued operational recovery and expansion.

280A|G-TMH

1563.0

▲ +1.82%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- *

- G-TMH announced its supplementary financial materials for the first quarter of the fiscal year ending November 2026 (December 1, 2025 – February 28, 2026) on April 14, 2026.

- For Q1, consolidated net sales were 814 million JPY, operating loss was 44.3 million JPY, and ordinary loss was 44.9 million JPY.

- Sales represented 13% of the full-year plan; however, the company states that many bids for used equipment projects are scheduled for the latter half of H1 and beyond, indicating a performance heavily weighted towards H2.

- G-TMH plans to establish a subsidiary in Shanghai, China, around June 2026, as part of efforts to strengthen global sales capabilities.

- As of the end of Q1 FY2026, the real equity ratio on the consolidated balance sheet was 60.2%.

🤖 AI Perspective

**

While G-TMH reported consolidated net sales of 814 million JPY and an operating loss of 44.3 million JPY for the first quarter, the company indicates that this performance is in line with its full-year plan, which anticipates a significant weighting towards the second half. This suggests that large used equipment sales projects are expected to concentrate from Q2 onwards, and aggressive upfront investments for future growth have increased in the first half. The announcement of a Chinese subsidiary may be seen as a concrete step towards future overseas expansion and new business development.

304A|G-フォルシア

1890.0

▲ +5.00%

📎 Source:G-フォルシア Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-FORCIA announced on April 14, 2026, a significant variance between its earnings forecast and actual results for the fiscal year ending February 2026 (March 1, 2025, to February 28, 2026).

- Net sales for FY2026 were JPY 2,197 million against an initial forecast of JPY 2,492 million, representing an 11.8% decrease.

- Operating profit for the same period was JPY 71 million (71.4% decrease from forecast JPY 249 million), ordinary profit was JPY 74 million (70.2% decrease from JPY 249 million), and net profit was JPY 48 million (71.7% decrease from JPY 171 million).

- The primary reason for the sales variance was a change in revenue recognition for a large project; following discussions with auditors, revenue for this project will now be recognized upon customer acceptance in the next fiscal year.

- The decrease in profits was attributed to higher cost of sales from upfront investments in development system expansion and new feature development for the large project, which were impacted by the deferred revenue recognition into the following fiscal year.

🤖 AI Perspective

- G-FORCIA’s FY2026 financial results indicate that a reassessment of revenue recognition policies, combined with strategic upfront investments, significantly impacted performance below initial forecasts.

- The deferral of revenue recognition for the major project, despite its order and contract completion with no change in project progress, may suggest potential future revenue recognition, which could be a point of interest for investors.

- The ongoing investments in development and new functionalities, aimed at strengthening mid-to-long-term growth and product competitiveness, could be seen as foundational for future performance and warrant monitoring in subsequent financial reports.

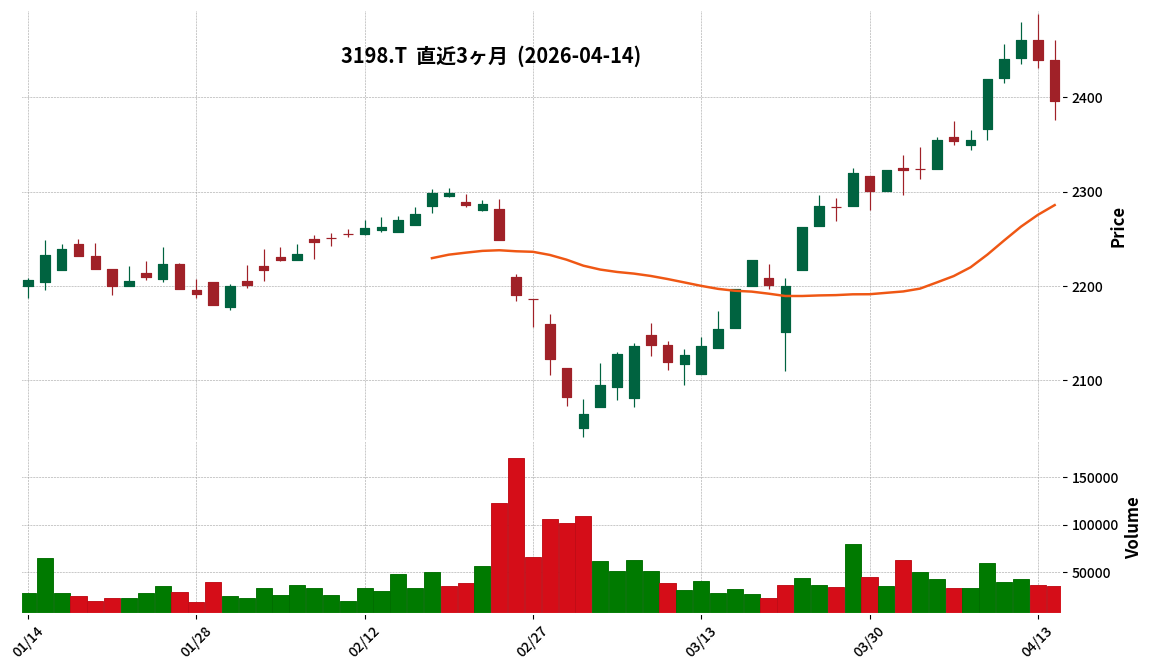

3198|SFPHD

2396.0

▼ -1.76%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SFP Holdings (SFPHD) signed an absorption merger agreement with Create Restaurants Holdings (CRH) on April 14, 2026.

- CRH will be the surviving company, while SFPHD will be the absorbed company in this merger.

- The merger is scheduled to take effect on July 1, 2026, contingent on approval at SFPHD’s ordinary general meeting of shareholders planned for May 21, 2026.

- SFPHD’s common shares are slated for delisting from the Tokyo Stock Exchange on June 29, 2026, with the final trading day set for June 26, 2026.

- The stated purpose of the merger is to address structural challenges in the restaurant industry, respond to calls for strengthened governance of listed subsidiaries, and integrate management resources for quicker decision-making.

🤖 AI Perspective

This merger appears to be a strategic move by the parent company, Create Restaurants Group, to more efficiently and rapidly leverage SFPHD’s resources to navigate the rapidly changing restaurant market. While SFPHD’s public shareholders will receive CRH shares as consideration for the delisting, this step aims to accelerate synergy creation across the entire group, with the goal of enhancing corporate value. The restructuring of group management and the evolution of business strategies following this merger will be worth monitoring.

3266|ファンドクリG

89.0

▲ +0.00%

📎 Source:ファンドクリG Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of fiscal year 2026 (December 1, 2025, to February 28, 2026), consolidated net sales increased by 175.9% year-on-year to JPY 1,183 million.

- The company reported an operating loss of JPY 17 million (compared to a loss of JPY 71 million in the prior year period), an ordinary loss of JPY 65 million (vs. JPY 77 million loss), and a net loss attributable to parent of JPY 45 million (vs. JPY 59 million loss).

- By segment, the Investment Bank business recorded sales of JPY 1,060 million (up 252.7% YoY) and a segment profit of JPY 101 million (up 329.1% YoY).

- The Asset Management business posted sales of JPY 123 million (down 4.1% YoY) and a segment loss of JPY 8 million (vs. JPY 2 million loss in the prior year period).

- The full-year consolidated earnings forecast for FY2026 remains unchanged, projecting net sales of JPY 6,200 million, operating profit of JPY 580 million, ordinary profit of JPY 530 million, and net profit attributable to parent of JPY 345 million.

🤖 AI Perspective

The substantial year-on-year increase in consolidated net sales for the quarter, largely driven by the Investment Bank segment, indicates strong operational activity in that area. Conversely, the Asset Management segment experienced a decline in sales and an increased loss, which may warrant monitoring in subsequent periods. With the full-year forecast remaining unchanged, market attention could focus on the company’s ability to maintain its projected performance and the relative contributions of its business segments throughout the fiscal year.

351A|P-アクシスITP

1760.0

▲ +0.00%

📎 Source:P-アクシスITP Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- P-AXIS ITP announced its interim financial results for the fiscal year ending August 2026 (September 1, 2025, to February 28, 2026). Sales reached JPY 1,469 million, operating profit JPY 8 million, ordinary profit JPY 15 million, and interim net profit JPY 95 million. Interim net earnings per share were JPY 77.61.

- Due to a company merger, the company transitioned to non-consolidated financial reporting from this interim period, thus no year-on-year comparisons or percentage changes are provided.

- As of the end of the interim period, total assets stood at JPY 2,032 million, net assets at JPY 1,345 million, and the equity ratio was 66.2%.

- The full-year forecast for FY2026 remains unchanged, projecting sales of JPY 3,352 million (up 5.1% year-on-year), operating profit of JPY 182 million (up 74.2% year-on-year), and net profit of JPY 237 million (up 321.8% year-on-year). Full-year earnings per share are forecasted at JPY 192.11.

- The projected annual dividend remains 0.00 JPY for both interim and year-end, with no revisions from the latest publicly announced forecast.

🤖 AI Perspective

The transition to non-consolidated reporting from this fiscal year means direct year-on-year comparisons are not available, which may require investors to consider the underlying business changes. However, the company’s focus on DX initiatives across construction, corporate, and regional sectors, coupled with a significantly increased full-year net profit forecast, could indicate confidence in its strategic direction.

3675|クロスマーケティング

611.0

▲ +0.16%

📎 Source:クロスマーケティング Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Cross Marketing Group resolved to acquire shares (making it a subsidiary) of Startling Inc. at its Board of Directors meeting held on April 14, 2026.

- The execution date for the share acquisition is scheduled for April 28, 2026.

- Startling Inc.’s business involves the planning, design, OEM production, and sale of apparel and other goods utilizing IP, as well as its own brand products.

- Through this acquisition, Cross Marketing Group will acquire all 200 outstanding shares of Startling Inc., making it a wholly-owned subsidiary with 100.0% voting rights.

- The company anticipates that the impact of this acquisition on its consolidated financial performance will be minor.

🤖 AI Perspective

Cross Marketing Group’s acquisition of Startling Inc. appears to align with its mid-term management strategy, “Unite & Generate,” aiming for synergistic growth within the group. Startling Inc.’s expertise in IP merchandising, design capabilities, and extensive collaboration history could enhance the Group’s promotion business, particularly in synergy with existing subsidiary Tokio Gets Co., Ltd. While the immediate impact on consolidated earnings is projected to be minor, the strategic implications for expanding business domains and creating new value in the mid-to-long term may be worth monitoring.

3697|SHIFT

657.2

▲ +4.65%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SHIFT Inc. reported record-high revenues of ¥37.2 billion (up 118.0% YoY) and gross profit of ¥12.8 billion (up 114.3% YoY) for the second quarter of the fiscal year ending August 2026.

- Operating profit for the quarter was ¥4.1 billion (down 90.1% YoY), reflecting a decrease attributed to strategic upfront investments in AI.

- The company disclosed approximately ¥2.5 billion in AI investments during the first half, stating that equivalent orders have already been secured.

- For the third quarter of FY2026, the company projects revenues of around ¥40.5 billion (approx. 120% YoY) and operating profit of around ¥5.0 billion (exceeding 125% YoY), with AI investment recovery anticipated to commence in the second half.

- SHIFT is advancing an AI strategy targeting a gross profit margin of 40% in the “With AI” era and 60-70% in the “Native AI” era, promoting AI Modernization services like “DQS for RE.”

🤖 AI Perspective

The upfront AI investments, while impacting operating profit, appear to be strategically aimed at future growth, as evidenced by the immediate securing of equivalent orders. The company’s focus on “Native AI” era initiatives such as AI Modernization and AI BPaaS may suggest a significant transformation in its revenue structure. Investors will likely monitor the anticipated recovery of AI investment in the latter half of the fiscal year for insights into the financial impact of these strategies.

4016|MITHD

927.0

▼ -1.07%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- MITHD’s consolidated financial results for Q1 FY2026 (ended November) show net sales of JPY 1,228 million (down 8.4% YoY), operating profit of JPY 59 million (down 32.4% YoY), ordinary profit of JPY 58 million (down 32.8% YoY), and net profit attributable to parent company shareholders of JPY 34 million (down 39.9% YoY).

- Gross profit was JPY 289 million, representing a 35.0% increase quarter-on-quarter, but an 11.8% decrease year-on-year.

- Segment sales were JPY 1,070 million for System Integration (down 5.7% YoY) and JPY 157 million for DX Solutions (down 23.1% YoY).

- Key factors contributing to the decrease in operating profit include a reactionary decline from a large project in the transport and logistics sector that concluded in Q1 of the previous year, a temporary decrease in operational man-hours due to group reorganization and business integration, and increased personnel costs related to securing and training human resources, as well as compensation improvements.

- The progress rates against the full-year FY2026 forecasts (net sales JPY 5,700 million, operating profit JPY 285 million) are 21.5% for net sales and 20.8% for operating profit based on Q1 results. The planned annual dividend for FY2026 is JPY 8.

🤖 AI Perspective

While year-on-year figures showed declines, it is noteworthy that gross profit, operating profit, ordinary profit, and net profit all significantly increased quarter-on-quarter. The reactionary decline from a large project and human resource investments appear to have impacted year-on-year performance, but some DX Solutions services are showing signs of recovering orders and increasing new projects. Although the progress rate against full-year forecasts is typical for the first quarter, further developments in DX Solutions, including functional enhancements and new project acquisitions, could influence future performance.

414A|G-オーバーラップ

1023.0

▲ +1.69%

📎 Source:G-オーバーラップ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Overlap Holdings announced its consolidated financial results for the second quarter (cumulative: September 1, 2025 – February 28, 2026) of the fiscal year ending August 2026.

- Revenue reached ¥4,143 million (up 13.3% year-on-year), operating profit was ¥1,200 million (up 4.8% year-on-year), and interim profit attributable to owners of the parent totaled ¥792 million (up 3.7% year-on-year).

- The increase in revenue and profit is attributed to continuous efforts in creating new IPs and enhancing the value of existing IPs, alongside focusing on media mix developments including the broadcasting of three anime titles such as “Campfire Cooking in Another World with My Absurd Skill Season 2”.

- The year-end dividend forecast for the fiscal year ending August 2026 has been revised to ¥44.00, marking a change from the previously disclosed forecast.

- The consolidated full-year performance forecast for the fiscal year ending August 2026 remains unchanged from the figures announced on October 15, 2025, including revenue of ¥9,209 million and profit attributable to owners of the parent of ¥2,232 million.

🤖 AI Perspective

The reported increase in revenue and profits for the second quarter cumulative period may suggest that the company’s IP strategy and media mix initiatives are contributing to its earnings. The revision of the year-end dividend forecast could indicate a proactive stance towards shareholder returns. With the full-year forecast maintained, the company’s performance in the latter half of the fiscal year will be worth monitoring.

4197|アスマーク

2383.0

▼ -0.04%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of fiscal year 2026 (December 1, 2025 – February 28, 2026), ASMARQ reported consolidated net sales of ¥1,199 million (down 1.3% year-over-year) and operating profit of ¥54 million (down 52.4% year-over-year).

- The decrease in operating profit was primarily attributed to an increase in the outsourcing ratio (up 3.0 percentage points) and planned human capital investments (personnel expenses up 6.0%) aimed at future growth.

- The Q1 achievement rate against the full-year forecast (disclosed on January 14, 2026) was 25.5% for net sales and 27.0% for operating profit, with the company expecting to recover full-year operating profit from the second quarter onward.

- By business segment, the HR Tech business within the standalone research segment recorded sales of ¥48 million (up 18.1% year-over-year), showing steady progress, while Global Research saw a 78.1% decrease in sales year-over-year.

- Regarding M&A and alliances, ASMARQ acquired shares of Lean Nishikata Co., Ltd. in January 2026 and continues to explore partnership opportunities.

🤖 AI Perspective

While Q1 saw a decline in profit, this appears to be a strategic outcome of investments in human capital and the data analytics business, positioning the period as a foundation for future re-growth and business structural transformation. The strong growth in the HR Tech business may suggest successful diversification of revenue streams. Investors might closely monitor the company’s progress in the second quarter and beyond, particularly how it aims to recover its full-year operating profit target.

4382|HEROZ

869.0

▲ +1.40%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- HEROZ Corporation (Code: 4382) and VarioSecure Inc. (Code: 4494) have decided to execute a management integration through a share exchange and signed a share exchange agreement today.

- Under this share exchange, HEROZ will become the wholly-owning parent company, and VarioSecure will become the wholly-owned subsidiary.

- The effective date of the share exchange is scheduled for June 30, 2026, and VarioSecure is expected to be delisted from the Tokyo Stock Exchange Standard Market on June 26, 2026.

- Following the share exchange, HEROZ plans to transition to a holding company structure, intending to succeed its AI solution business and other operations to its wholly-owned subsidiaries via an absorption-type company split.

- HEROZ intends to maintain its listing on the Tokyo Stock Exchange Standard Market after the effectiveness of this management integration and the subsequent absorption-type company split.

🤖 AI Perspective

This management integration may suggest HEROZ’s aim to expand its business domains and strengthen its competitiveness by linking its AIX business with VarioSecure’s AI Security business. In a landscape of rapid AI technology advancement and increasing cybersecurity demands, the mutual utilization of management resources, including personnel and technology from both companies, could enable a broader range of solution offerings. HEROZ’s planned transition to a holding company structure might indicate an effort to streamline overall group management and enhance the specialization of each business unit.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

4415|G-ブロードエンター

1321.0

▲ +1.38%

📎 Source:G-ブロードエンター Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- On April 14, 2026, G-Broadenter’s Board of Directors resolved to borrow funds.

- The company will borrow a total of ¥1,100,000 thousand from Kiyo Bank.

- The purpose of this borrowing is to fund the acquisition of shares (full subsidiary status) of Nippon Chuo Management Co., Ltd., related acquisition expenses, and working capital.

- The loan is scheduled for execution on April 20, 2026, with a repayment period of 10 years and a maturity date of April 30, 2036.

- The interest rate is variable, repayment will be on a level principal payment basis, no collateral will be provided, and the acquired subsidiary will provide a joint guarantee.

- A financial covenant requires the company to maintain net assets in the balance sheet from the December 2027 fiscal year onward at or above 75% of the net assets from the December 2026 fiscal year-end balance sheet.

🤖 AI Perspective

This announcement provides clarity on the financing method for the full acquisition of Nippon Chuo Management Co., Ltd. A 10-year loan with a variable interest rate may suggest the need for investors to monitor potential impacts from future interest rate fluctuations on the company’s long-term financial planning. The inclusion of a financial covenant could indicate a strategic focus on maintaining financial health and stability post-acquisition.

4429|G-リックソフト

1010.0

▲ +2.43%

📎 Source:G-リックソフト Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Ricksoft’s consolidated financial results for the February 2026 fiscal year reported revenue of JPY 10,892 million, an increase of 20.4% year-on-year.

- Operating income decreased by 17.8% to JPY 376 million, ordinary income by 22.7% to JPY 357 million, and profit attributable to owners of parent by 25.8% to JPY 263 million.

- Total assets amounted to JPY 9,632 million (up 44.2% from the previous fiscal year-end), net assets to JPY 3,316 million (up 9.5%), with an equity ratio of 34.4%.

- Cash flows from operating activities generated an income of JPY 697 million (up 84.8% year-on-year), and cash and cash equivalents at the end of the period increased to JPY 3,939 million.

- For the February 2027 fiscal year, the company forecasts consolidated revenue of JPY 12,195 million (up 12.0% from the previous period) but anticipates a decrease in operating income to JPY 200 million (down 46.7%).

457A|P-ルリアン

4130.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- P-Lien Co., Ltd. announced its interim financial results for the fiscal year ending August 2026 (September 1, 2025 – February 28, 2026).

- For the interim period, net sales were ¥721 million (up 17.1% year-on-year), operating income was ¥40 million (up 90.8%), ordinary income was ¥33 million (up 59.7%), and interim net income was ¥22 million (up 58.3%).

- By business segment, net sales for Primary Support increased by 15.8% year-on-year to ¥521,049 thousand, and Secondary Support increased by 30.9% to ¥177,724 thousand.

- Key Performance Indicators (KPIs) showed an increase in effective information cases to 33,095 (up 11.1% year-on-year) and a rise in accepted cases to 3,236 (up 13.1%).

- The full-year forecast for FY2026 remains unchanged from the most recently announced figures: net sales of ¥1,439 million, operating income of ¥61 million, ordinary income of ¥61 million, and net income of ¥40 million.

🤖 AI Perspective

P-Lien’s interim results show substantial year-on-year increases across net sales and various profit metrics, suggesting ongoing business growth. The strong performance of its core Primary and Secondary Support services, coupled with increases in effective information cases and accepted cases, could indicate successful expansion of the company’s business foundation. Investors may wish to monitor the pace of achieving full-year targets and the balance between increased personnel and operational costs, and the top-line revenue growth in future reports.

4885|室町ケミカル

1000.0

▼ -4.58%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Muromachi Chemical Co., Ltd. announced on April 14, 2026, a revision to its full-year earnings forecast for the fiscal year ending May 2026.

- The revised full-year forecast for FY2026 projects net sales of 7,700 million yen (up 2.7% from the previous forecast), operating profit of 700 million yen (up 27.3%), ordinary profit of 660 million yen (up 29.4%), and net profit of 470 million yen (up 34.3%).

- The revision is primarily attributed to strong order intake in both the chemical products business and the pharmaceutical business, along with lower-than-expected withdrawal-related costs for the health food business.

- The company also resolved to increase the year-end dividend for the fiscal year ending May 31, 2026, from the previously forecast 15 yen to 16 yen per share.

- This adjustment results in a projected total annual dividend of 26 yen per share for FY2026.

🤖 AI Perspective

- The upward revision in earnings may suggest robust performance in the company’s core businesses and effective cost management related to its business restructuring efforts.

- The decision to increase dividends, consistent with the company’s progressive dividend policy, could indicate a commitment to balancing shareholder returns with investments for future growth.

- Investors may monitor the evolving revenue structure post-health food business withdrawal and the progress of growth strategies in the pharmaceutical and chemical segments for future insights.

5527|G-propetec

737.0

▲ +0.55%

📎 Source:G-propetec Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of the fiscal year ending November 2026 (December 1, 2025 – February 28, 2026), consolidated net sales increased by 11.1% year-on-year to JPY 11,488 million.

- During the same period, consolidated operating profit was JPY 405 million (down 3.2% year-on-year), consolidated ordinary profit was JPY 298 million (down 11.1% year-on-year), and net profit attributable to owners of the parent was JPY 150 million (down 20.7% year-on-year).

- The full-year consolidated earnings forecast for the fiscal year ending November 2026 remains unchanged from the latest public announcement, with projected net sales of JPY 58,000 million, operating profit of JPY 2,500 million, ordinary profit of JPY 2,100 million, and net profit attributable to owners of the parent of JPY 1,300 million.

- The consolidated equity ratio as of the end of the first quarter of FY2026 stood at 19.4% (compared to 19.3% at the end of FY2025).

- The company implemented a 3-for-1 stock split for its common shares, effective August 1, 2025.

🤖 AI Perspective

While net sales saw an increase in the first quarter, the decline in profits during the same period may be a point of focus for investors. The unchanged full-year consolidated earnings forecast could suggest that the company anticipates a recovery in profitability in subsequent quarters or has already accounted for the first-quarter performance in its annual projections. Investors may monitor how the company’s strategies, particularly in its renovated housing and detached housing segments, will contribute to future financial results.

6025|日本PCサービス

—

▲ +0.00%

📎 Source:日本PCサービス Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the second quarter (interim period) of the fiscal year ending August 2026, consolidated net sales reached ¥4,103 million, marking a 26.9% increase compared to the same period last year.

- During the same interim period, consolidated operating income was ¥116 million (compared to ¥2 million profit in the prior year), consolidated ordinary income was ¥113 million (compared to ¥1 million profit in the prior year), and net income attributable to owners of parent was ¥44 million (compared to a loss of ¥12 million in the prior year), indicating a return to profitability for all profit items.

- As of the end of the current interim accounting period, consolidated total assets stood at ¥3,033 million and consolidated net assets at ¥317 million.

- The consolidated full-year earnings forecast for the fiscal year ending August 2026 has been revised from the most recently announced forecast.

🤖 AI Perspective

The significant increase in net sales and the return to profitability across all income items in the interim period are noteworthy. This trend may suggest a positive impact from the company’s strategic initiatives, such as “growth investment for brand recognition,” in response to the accelerating DX in the information and communication services industry and the emerging digital divide. However, with a revision to the full-year consolidated earnings forecast, the company’s future business developments and performance will warrant continued monitoring.

4413|ボードルア

1975.0

▲ +1.23%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Baudroie Co., Ltd. announced its consolidated financial results for the fiscal year ended February 2026, reporting revenue of ¥17,423 million (up 49.6% year-on-year) and profit attributable to owners of the parent of ¥2,457 million (up 36.6% year-on-year).

- The company issued a consolidated earnings forecast for the fiscal year ending February 2027, projecting revenue of ¥23,500 million (up 34.9% year-on-year) and profit attributable to owners of the parent of ¥3,134 million (up 27.5% year-on-year).

- The year-end dividend for FY2026/2 was set at ¥7.58 per share, with the total annual dividend being the same. The forecasted year-end dividend for FY2027/2 is ¥10.10 per share.

- Four companies, SPIN TECHNOLOGY Co., Ltd., Goku Technologies Co., Ltd., ONE-TECH Co., Ltd., and Lixol Co., Ltd., were newly included in the scope of consolidation from the current fiscal year.

- As of the end of FY2026/2, total assets increased to ¥14,024 million (up 63.0% from the previous fiscal year), and equity attributable to owners of the parent increased to ¥7,718 million (up 68.8% from the previous fiscal year).

🤖 AI Perspective

The significant increase in revenue and net profit for the fiscal year ended February 2026 appears to be influenced by the addition of new consolidated subsidiaries and robust demand in the IT infrastructure sector. The projected continued growth for the next fiscal year may suggest a sustained positive business trend. Investors might monitor the company’s ability to integrate its new subsidiaries and capitalize on ongoing IT and DX investment trends.

274A|ガーデン

2277.0

▼ -0.48%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Garden Co., Ltd. has released its financial results presentation for the fiscal year ended February 2026.

- For the fiscal year ended February 2026, the company reported revenue of 17,895 million yen, marking a 4.3% increase year-over-year.

- However, operating profit decreased by 29.6% to 1,301 million yen, and net profit fell by 48.2% to 625 million yen.

- Key factors cited for the profit decline include a reduction in customer traffic due to extreme heat and price increases, temporary expenses related to M&A activities, and an increase in impairment losses.

- The total number of stores increased by 4 from the end of the previous period, reaching 199.

- For the fiscal year ending February 2027, the company forecasts an increase in both revenue and profit, anticipating contributions from “Manbaken” and “Takadaya.”

🤖 AI Perspective

While revenue recorded growth, the significant decline in both operating and net profits is likely to draw investor attention. The results indicate that external factors such as prolonged hot weather and price adjustments, along with one-off M&A and international expansion expenses, and increased impairment losses, weighed on profitability. Moving forward, the company’s ability to achieve its FY2027 revenue and profit growth forecast will likely depend on the successful integration and contribution of acquired businesses like “Manbaken” and “Takadaya,” as well as effective strategies to recover customer traffic in existing stores.

3189|ANAP

180.0

▼ -2.70%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the second quarter of the fiscal year ending August 2026, ANAP Holdings reported consolidated net sales of ¥1,086 million, marking an 86.6% increase compared to the prior year’s interim period.

- The company recorded an operating loss of ¥1,216 million (vs. ¥534 million loss in the prior year’s interim period) and an ordinary loss of ¥9,227 million (vs. ¥561 million loss in the prior year’s interim period), resulting in a net loss attributable to owners of parent of ¥9,355 million (vs. ¥825 million net income in the prior year’s interim period).

- As of the end of the interim period, consolidated total assets were ¥16,074 million, net assets were ¥5,533 million, and the equity ratio stood at 34.3% (compared to an equity ratio of 68.9% at the end of August 2025).

- The consolidated earnings forecast for the full fiscal year ending August 2026 is scheduled to be disclosed promptly once it becomes available.

- A significant uncertainty regarding the going concern assumption has been noted in the financial statements.

🤖 AI Perspective

While ANAP Holdings reported a substantial increase in net sales, the significant expansion of operating and ordinary losses, leading to a large net loss attributable to owners of parent, may suggest challenges in converting sales growth into profitability. The considerable decline in net assets and the equity ratio, coupled with the going concern uncertainty note, could raise concerns regarding the company’s financial stability and operational viability among investors. The forthcoming disclosure of the full-year earnings forecast and the specific measures to address the going concern issues will likely be key points for investors to monitor.

3290|R-Oneリート

80900.0

▲ +0.25%

📎 Source:R-Oneリート Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- R-One REIT reported results for the fiscal period ended February 2026 (September 1, 2025 – February 28, 2026), with operating revenue of JPY 4,690 million (down 12.0% YoY), operating profit of JPY 2,353 million (down 17.9% YoY), ordinary profit of JPY 1,923 million (down 22.6% YoY), and net income of JPY 1,922 million (down 22.4% YoY).

- Distribution per unit was JPY 2,386, with a payout ratio of 99.9%.

- As of the end of the period, total assets stood at JPY 134,898 million, net assets at JPY 61,682 million, and the equity ratio at 45.7%.

- An investment unit split was implemented on September 1, 2025 (record date August 31, 2025), at a ratio of three units for every one unit.

- For the fiscal period ending August 2026, the forecast distribution per unit is JPY 2,170 (assuming JPY 300 million is drawn from retained earnings). For the fiscal period ending February 2027, the forecast distribution per unit is also JPY 2,170 (assuming JPY 280 million is drawn from retained earnings).

🤖 AI Perspective

The decline in revenue and profit for the February 2026 period may be partly attributed to the investment unit split and asset replacement strategies, including the transfer of some properties aimed at enhancing portfolio quality. Forecasts for subsequent periods indicate distributions per unit that rely on drawing from retained earnings, suggesting ongoing efforts toward portfolio optimization. How these factors will influence the future earnings structure is worth monitoring.

4017|G-クリーマ

218.0

▼ -1.36%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-CREEMA announced its full-year financial results for the fiscal year ended February 2026. Full-year revenue reached ¥2,535 million (+1% YoY), with fourth-quarter revenue increasing by 107% YoY.

- Full-year operating profit was ¥42 million (+41% YoY), ordinary profit ¥66 million (+63% YoY), and profit attributable to owners of parent ¥27 million (+27% YoY).

- The company launched its subscription service “Creator Push” in July 2025 and the anonymous delivery service “Creema Anshin Anonymous Delivery” in September 2025.

- “Creema GIFT CATALOG” began service in Q2, and “Gift Tab” and “e-gift functions” were added to “Creema” in Q3. A comprehensive point linkage between “Creema” and “Creema SPRINGS” also commenced in September 2025.

- G-CREEMA is actively investigating and negotiating M&A opportunities totaling ¥700-800 million, with a target for execution within the next two years. Cash and deposits increased to ¥3,015 million (+24% YoY), maintaining a stable financial foundation.

🤖 AI Perspective

While full-year revenue growth was modest, the significant 107% YoY increase in Q4 revenue suggests a positive turnaround for G-CREEMA’s marketplace services. The company’s consistent investment in strategic initiatives, such as expanding gift-related services, introducing anonymous shipping, and enhancing group synergy through point linkages, appears to be laying a foundation for future growth. Investors may find it worthwhile to monitor the impact of these new services and the progress of their M&A strategy on the company’s mid-to-long-term performance.

144A|P-エネルギーパワー

450.0

▲ +0.00%

📎 Source:P-エネルギーパワー Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- P-Energy Power reported non-consolidated interim results for the fiscal year ending August 2026 (September 1, 2025 – February 28, 2026), with net sales of ¥6,583 million (up 208.5% year-on-year), operating profit of ¥1,506 million (up 690.2% YoY), ordinary profit of ¥1,428 million (up 310.3% YoY), and interim net profit of ¥944 million (up 288.5% YoY).

- Interim net earnings per share were ¥118.08.

- By segment, the Engineering business recorded net sales of ¥6,070 million (up 267.2% YoY) and segment profit of ¥1,577 million (up 459.5% YoY).

- The Grid Battery Storage business commenced operations during this interim period, generating sales of ¥146 million and segment profit of ¥59 million.

- The full-year performance forecast and dividend forecast (¥0.00 for both interim and year-end) remained unchanged from the most recently announced figures.

🤖 AI Perspective

The significant increase in sales and profits during this interim period appears to be primarily driven by the robust performance of the Engineering business, particularly through the steady progress of grid battery storage facility installation projects, as well as resilient self-consumption solar power generation and EV charging facility installations. Furthermore, the newly launched Grid Battery Storage business began contributing to revenue in this period, which may suggest a shift in the company’s business structure impacting its performance. With the full-year forecast remaining unchanged, future developments could be worth monitoring.

3557|G-U&C

964.0

▼ -0.21%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- United & Collective Inc. (G-U&C) announced its non-consolidated financial results for the fiscal year ended February 28, 2026 (FY2026/2).

- For the period, net sales were ¥6.46 billion (down 0.5% year-on-year). The company reported an operating loss of ¥15 million (compared to a profit of ¥115 million in the prior year), an ordinary loss of ¥48 million (prior year profit of ¥87 million), and a net loss of ¥227 million (prior year profit of ¥59 million).

- As of February 29, 2026, net assets increased by ¥184 million year-on-year to ¥527 million, improving the equity ratio to 12.7% from 7.9%. This was primarily due to an increase in capital stock and capital surplus from the exercise of share options, as well as changes in other capital surplus and retained earnings from capital reduction and deficit compensation.

- Cash flow from operating activities increased to ¥199 million in the current fiscal year, up from ¥122 million in the prior year.

- For FY2027/2, the company forecasts a return to profitability with net sales of ¥6.96 billion (up 7.7% year-on-year), operating profit of ¥58 million, ordinary profit of ¥23 million, and net profit of ¥2 million.

🤖 AI Perspective

While net sales saw only a minor decrease, the significant shift from profit to loss across all profitability metrics for FY2026/2 stands out as a key aspect of this financial announcement. Conversely, the substantial increase in net assets and improved equity ratio, driven by financial maneuvers such as share option exercise and deficit compensation, could indicate efforts to strengthen the company’s financial foundation. The company’s forecast for a return to profitability in FY2027/2 suggests management is focused on recovery, and the execution of their plans for existing store performance and operational efficiency may be worth monitoring.

3826|SI

482.0

▲ +2.55%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- System Integrator Co., Ltd. (Code: 3826) announced a revision to its dividend forecast (increase) on April 14, 2026.

- The company revised its year-end dividend forecast for the fiscal year ending February 2026, increasing the dividend per share from the previously announced ¥11.00 to ¥13.00.

- This revision brings the total annual dividend per share for the fiscal year ending February 2026 to ¥13.00, up from the previous forecast of ¥11.00.

- The total annual dividend for the previous fiscal year (FY2025/2) was ¥10.00 per share.

- The revision was made based on the full-year consolidated financial results for the fiscal year ending February 2026, which were announced today.

🤖 AI Perspective

- This dividend increase may suggest that the company’s recently announced full-year consolidated financial results for the fiscal year ending February 2026 were strong enough to warrant an upward revision from the previous dividend forecast.

- The revised annual dividend also represents an increase compared to the previous fiscal year’s payout, indicating the company’s commitment to shareholder returns.

- This move, aligning with the company’s financial performance, could be a point of interest for investors.

4444|G-インフォネット

883.0

▼ -0.56%

📎 Source:G-インフォネット Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-INFONET (株式会社インフォネット) announced today that its Board of Directors resolved to conduct an absorption-type merger of its consolidated subsidiary, SATSUGEI-TIVE Co., Ltd. (株式会社撮影ティブ), effective July 1, 2026 (scheduled).

- G-INFONET will be the surviving company, and SATSUGEI-TIVE Co., Ltd. will be dissolved as a result of this merger.

- The purpose of the merger is to maximize the utilization of management resources, enhance management efficiency, and accelerate decision-making processes.

- As G-INFONET owns all outstanding shares of SATSUGEI-TIVE Co., Ltd., no shares or other consideration will be delivered or allotted in connection with the merger.

- A special loss (loss on cancellation of treasury stock) is expected to arise from this merger, but its impact on G-INFONET’s consolidated financial results is stated to be minor.

🤖 AI Perspective

This merger, involving a parent company absorbing its wholly-owned subsidiary, appears to be an internal reorganization aimed at optimizing operational efficiencies within the group. While the company anticipates a special loss, the announced minor impact on consolidated performance suggests a strategic focus on achieving long-term synergies. Investors may consider monitoring how this structural change contributes to the overall business strategy and operational agility.

5574|G-ABEJA

3200.0

▲ +3.90%

📎 Source:G-ABEJA Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-ABEJA (5574) announced its Q2 FY2026 (non-consolidated) financial results on April 14, 2026.

- For the interim period, net sales were ¥2,351 million (up 30.0% year-on-year), operating profit was ¥384 million (up 32.6% YoY), ordinary profit was ¥389 million (up 33.3% YoY), and net income attributable to owners of parent was ¥336 million (up 37.6% YoY), marking record highs for an interim accounting period.

- The full-year earnings forecast has been revised, projecting net sales of ¥4,500 million (up 25.5% YoY) and net income of ¥540 million (up 20.5% YoY).

- As of the end of the interim accounting period, total assets stood at ¥5,553 million, with an equity ratio of 88.0%.

- The company initiated collaboration discussions with Fujisan Magazine Service Co., Ltd. and ANREALAGE Co., Ltd. regarding AI utilization, and made investments in both companies during the period.

🤖 AI Perspective