📌 Today’s Highlights

Today we cover 63 IR announcements. Notable among them: タスキHD (166A), G-スマレジ (4431), 神島化学工業 (4026). Use the table of contents below to navigate to each company.

- 166A|タスキHD

- 4431|G-スマレジ

- 4026|神島化学工業

- 181A|MX米債1-3ヘ無

- 182A|MX米債20超ヘ無

- 183A|MX米債20超ヘ有

- 2517|MXSJリートコア

- 2560|MXSカーボン日本株

- 2838|MX米債7-10ヘ無

- 2839|MX米債7-10ヘ有

- 9235|G-売れるネットG

- 254A|AIフュージョンCG

- 7782|シンシア

- 8303|SBI新生銀行

- 9556|G-INTLOOP

- 2294|柿安本店

- 3434|アルファCo

- 9262|シルバーライフ

- 2998|G-クリアル

- 3195|ジェネパ

- 3388|明治電機

- 7690|P-カレント自動車

- 8714|池田泉州

- 1840|土屋HD

- 189A|G-D&Mカンパニー

- 2345|HODL1

- 2424|ブラス

- 2978|G-ツクルバ

- 3134|Hamee

- 3166|OCHI・HD

- 3287|R-星野

- 3309|R-積水ハウスリート

- 3415|トウキョウベース

- 3565|アセンテック

- 3804|システム ディ

- 4260|G-ハイブリッドテク

- 442A|G-クラシコ

- 4592|G-サンバイオ

- 4811|G-ドリーム・アーツ

- 4840|トライアイズ

- 556A|G-犬猫生活

- 6125|岡本工機

- 5971|共和工業

- 132A|P-アイエヌHD

- 184A|G-学びエイド

- 278A|G-テラドローン

- 3823|WHY HOW DO

- 4441|トビラシステムズ

- 456A|G-ヒューマンメイド

- 500A|TOブックス

- 6838|多摩川HD

- 7502|プラザHD

- 8113|ユニチャーム

- 9913|日邦産業

- 3547|ユニシアHD

- 410A|G-GMOコマース

- 4380|G-Mマート

- 8894|REVOLUTION

- 415A|G-GMOTE-HD

- 7680|P-軽自動車館

- 9149|P-大友ロジスティク

- 9760|進学会HD

- 1417|ミライト・ワン

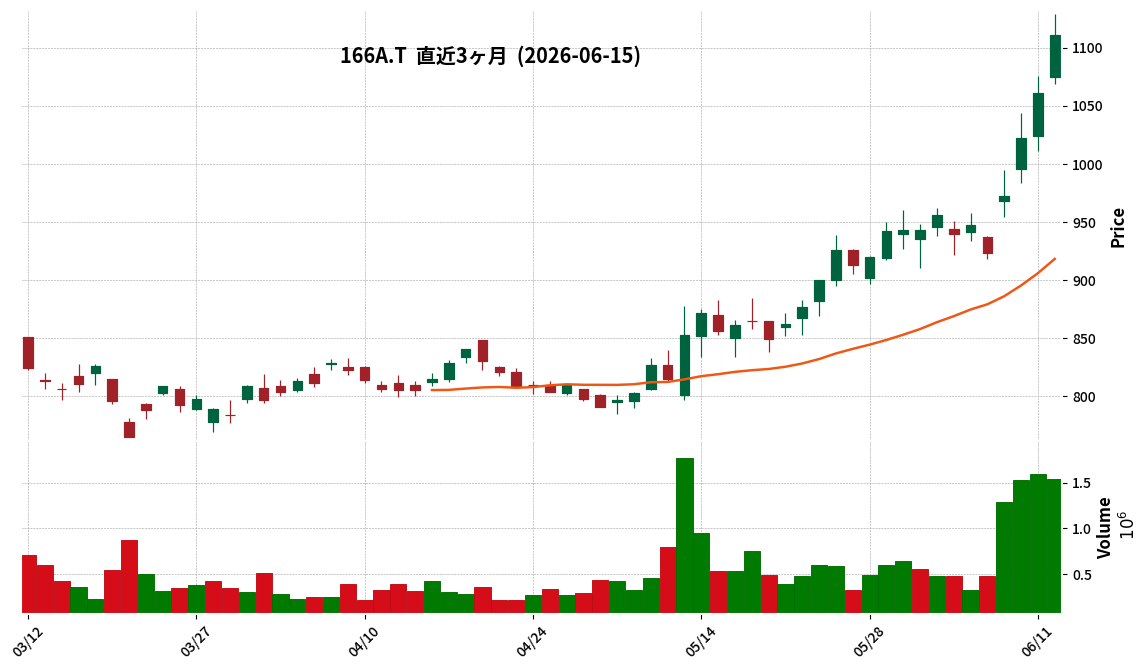

166A|タスキHD

1111.0

▲ +4.71%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tasuki Holdings Co., Ltd. resolved to revise its dividend forecast for the fiscal year ending September 2026 at a board meeting held on June 15, 2026.

- The revised year-end dividend per share is 50 yen, an increase of 10 yen from the previous forecast of 40 yen.

- This 50 yen comprises a 40 yen ordinary dividend and a 10 yen commemorative dividend.

- The revision is attributed to the company’s gratitude to shareholders following its market segment change from the Tokyo Stock Exchange Growth Market to the Prime Market.

- The company’s shareholder return policy is based on progressive dividends, targeting a dividend payout ratio of 40% or more.

🤖 AI Perspective

This dividend increase includes a commemorative dividend to mark Tasuki HD’s transition from the Growth Market to the Prime Market. The move to the Prime Market may suggest an increased recognition of the company’s governance and stability. The enhanced shareholder return policy in conjunction with this market change could be seen as an acknowledgment of rising market expectations. Investors may find it worthwhile to monitor the company’s commitment to its 40% or more payout ratio and its progress towards mid-term management plan targets.

4431|G-スマレジ

2523.0

▲ +5.17%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-SMAREREGI announced a partial correction to its “Consolidated Financial Results for the Fiscal Year Ended April 2026 (Japanese GAAP)”.

- The revised consolidated results for FY2026 show net sales of ¥13,345 million (up 20.6% year-on-year) and operating profit of ¥3,216 million (up 35.2% year-on-year).

- Consolidated ordinary profit was corrected to ¥3,186 million (up 34.9% year-on-year), and profit attributable to owners of parent was revised to ¥2,228 million (up 35.5% year-on-year).

- Revised EPS is ¥115.71, and diluted EPS is ¥115.56.

- Annual dividends were corrected to ¥24.00 per share for the year-end, totaling ¥24.00, with a total dividend amount of ¥462 million and a payout ratio of 20.7%.

🤖 AI Perspective

This correction, which revises key consolidated financial figures for G-SMAREREGI’s FY2026 upwards, may be perceived positively by investors. The significantly higher growth rates in net sales and various profit metrics could indicate that the company’s business performance is exceeding initial expectations. It is worth monitoring how these revised figures might influence future earnings forecasts and market valuations.

4026|神島化学工業

1573.0

▲ +1.88%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kamishima Chemical Industry announced its consolidated results for the fiscal year ended April 2026, reporting net sales of ¥28,008 million (+2.2% YoY), operating profit of ¥2,679 million (+50.0% YoY), ordinary profit of ¥2,563 million (+49.2% YoY), and net profit of ¥1,850 million (+29.1% YoY).

- By segment, the Building Materials business recorded net sales of ¥15,356 million (+1.8% YoY) and segment profit of ¥1,466 million (+61.2% YoY). The Chemical Products business reported net sales of ¥12,652 million (+2.7% YoY) and segment profit of ¥2,135 million (+27.9% YoY).

- Key factors contributing to the increase in operating profit included a reversal of retirement benefit provisions of ¥262 million, increased sales volumes, price pass-through effects, expanded sales of high value-added products, and cost improvements through factory efforts.

- The company has stated that the earnings forecast for the fiscal year ending April 2027 is currently undetermined due to increased uncertainty regarding raw material procurement, cost increases, and demand trends stemming from the situation in the Middle East.

- While the performance plans for the medium-term management plan (FY2027/4-FY2029/4) are also undecided, the Ceramics division of the Chemical Products business is focusing on new development and mass production of ceramic materials required in the high-power laser field.

🤖 AI Perspective

The strong performance in FY2026/4, with significant increases in sales and profits, appears to be driven by robust sales in key segments and effective cost management. However, the decision to leave the FY2027/4 earnings forecast undisclosed due to geopolitical uncertainties in the Middle East suggests potential challenges related to raw material procurement and costs. Investors may find it worthwhile to monitor how the company navigates these external factors and the progress of its strategic initiatives, particularly in the Chemical Products segment’s ceramics division.

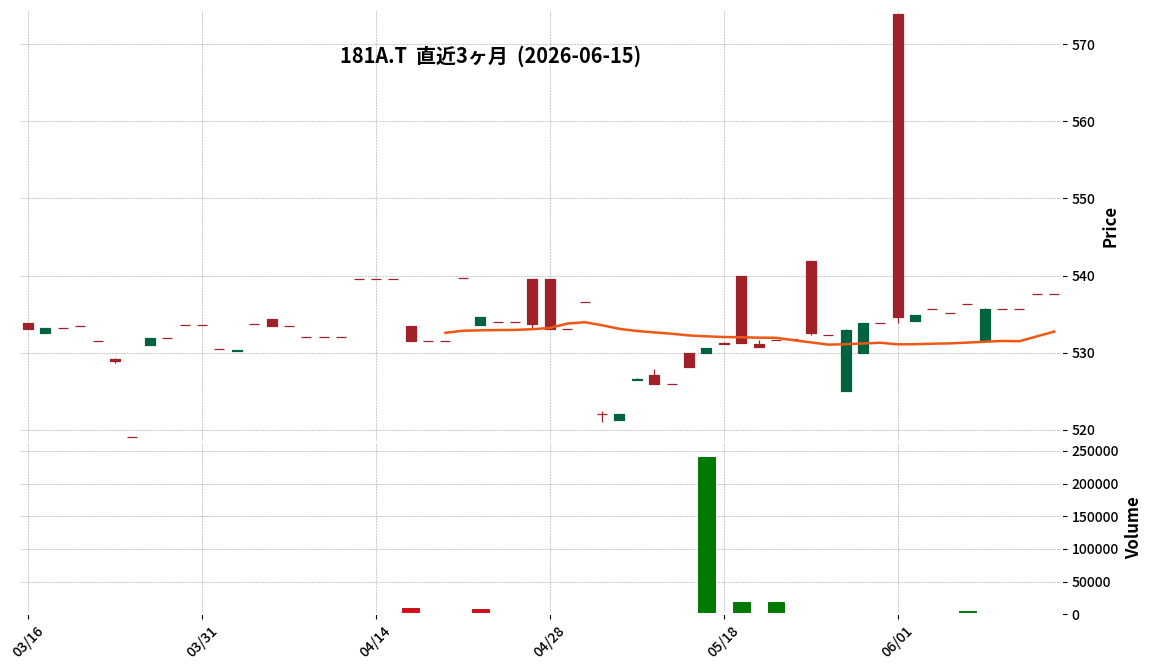

181A|MX米債1-3ヘ無

537.6

▲ +0.00%

📎 Source:MX米債1-3ヘ無 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- MAXIS US Treasury 1-3 Year ETF (no FX hedge) (Code: 181A) announced its financial results for the May 2026 fiscal period (November 11, 2025 – May 10, 2026).

- Total net assets at the end of the current period reached ¥5,423 million, up from ¥3,969 million at the end of the previous period.

- Major investment assets totaled ¥5,449 million, while cash, deposits, and other assets (net of liabilities) were -¥26 million.

- Outstanding units at the end of the current period increased to 10,311 thousand units, from 7,695 thousand units at the end of the previous period.

- The NAV per 100 units was ¥52,595 (previous period: ¥51,591), and the distribution per 10 units was ¥59 (previous period: ¥74).

🤖 AI Perspective

The latest financial results indicate an increase in net assets and outstanding units, suggesting a potential influx of capital from investors. The rise in NAV per 100 units also points to favorable operational performance during the period. However, the distribution per 10 units decreased compared to the previous period. Given that this ETF has no currency hedge, investors may want to monitor how foreign exchange fluctuations could influence its net asset value and unit price moving forward.

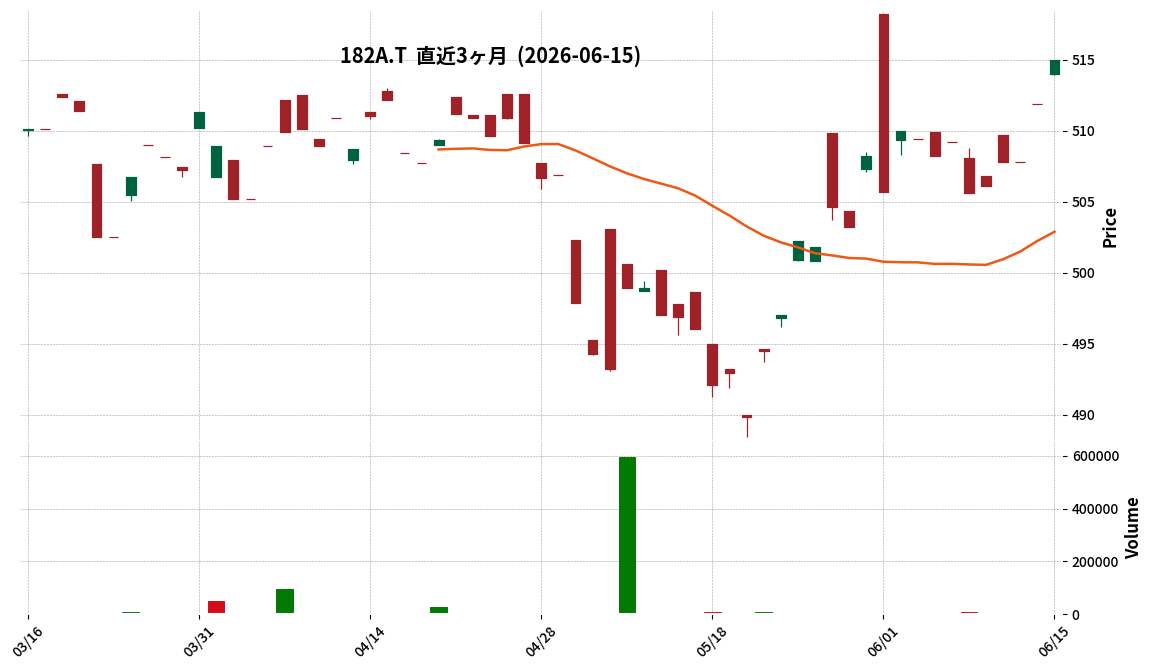

182A|MX米債20超ヘ無

515.0

▲ +0.61%

📎 Source:MX米債20超ヘ無 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- The MAXIS US Treasury 20yr+ ETF (Unhedged, 182A) announced its financial results for the May 2026 fiscal period (November 11, 2025 – May 10, 2026).

- Total net assets for the May 2026 period were ¥286 million (100.0% composition), and the net asset value per 100 units was ¥49,887.

- During the same period, 310 thousand units were created, 300 thousand units were redeemed, and the total outstanding units at the end of the period were 574 thousand units.

- The distribution per 10 units for the May 2026 period was announced as ¥108.

- Total operating revenue was ¥544,331, total operating expenses were ¥293,385, and net income for the period was ¥250,946.

🤖 AI Perspective

The financial results for the MAXIS US Treasury 20yr+ ETF (Unhedged) for the May 2026 period show net assets of ¥286 million, with a distribution of ¥108 per 10 units, indicating an increase compared to the previous period. The creation and redemption figures, alongside operating income and expenses, provide objective data for investors to assess the ETF’s operational trends and performance.

183A|MX米債20超ヘ有

453.5

▲ +2.07%

📎 Source:MX米債20超ヘ有 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- MAXIS US Treasury 20+ Year ETF (Hedged) (Code: 183A) announced its financial results for the May 2026 fiscal period (November 11, 2025, to May 10, 2026) on June 15, 2026.

- As of the end of the May 2026 period, net assets totaled ¥4,898 million (down from ¥6,229 million in the previous period), and the NAV per 100 units was ¥44,824 (down from ¥47,638 in the previous period).

- The total number of outstanding units at the end of the current period was 10,928 thousand units (down from 13,076 thousand units previously), with new subscriptions of 3,278 thousand units and redemptions of 5,426 thousand units.

- The dividend per 10 units for the May 2026 period was reported as ¥97 (up from ¥92 in the previous period).

- The net loss for the current period was ¥248,813,587, and the retained earnings at period-end were △¥565,582,881.

🤖 AI Perspective

The financial results for the MAXIS US Treasury 20+ Year ETF (Hedged) (183A) for the May 2026 period indicate a decrease in both net assets and outstanding units, primarily driven by redemptions exceeding new subscriptions. Conversely, the dividend per 10 units increased, which could be a point of interest for investors. The continued dynamics between subscriptions and redemptions may be worth monitoring in future periods.

2517|MXSJリートコア

1096.5

▲ +0.32%

📎 Source:MXSJリートコア Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- MAXIS J-REIT Core ETF (Code: 2517) announced its financial results for the May 2026 fiscal period (November 11, 2025, to May 10, 2026).

- Net assets at the end of the period stood at ¥58,056 million, down from ¥70,372 million at the end of the November 2025 period.

- The net asset value per 10 units was ¥112,543, a decrease from ¥119,516 in the previous period.

- The distribution per 10 units increased to ¥280, compared to ¥239 in the previous period.

- The fund reported an operating loss of △¥2,001 million for the current period (compared to an operating profit of ¥10,420 million in the previous period), primarily due to a loss on sales and purchases of securities totaling △¥3,394 million.

🤖 AI Perspective

While net assets and net asset value per unit declined during the period, the distribution per 10 units increased. This could suggest that despite a reduction in the fund’s scale, dividend income was allocated to distributions in line with its distribution policy. The shift to an operating loss, mainly driven by losses on securities trading, appears to reflect market conditions as investment securities are valued at fair market prices.

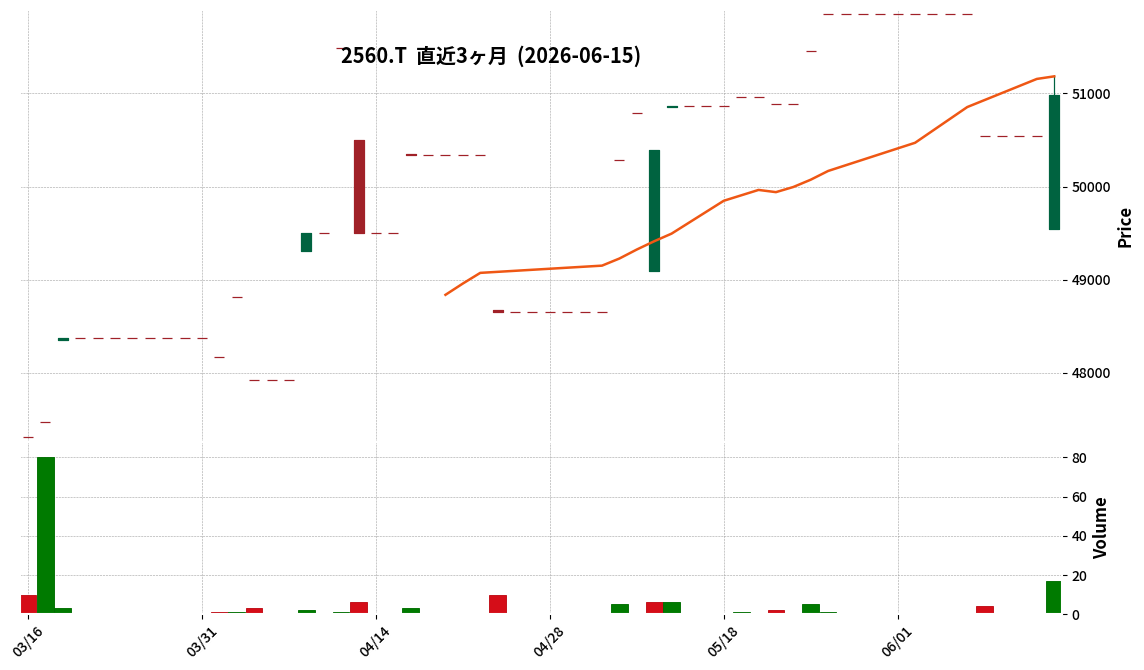

2560|MXSカーボン日本株

50980.0

▲ +0.87%

📎 Source:MXSカーボン日本株 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- MAXIS Carbon-Efficient Japan Stock ETF (Code: 2560) announced its Q3 2026 financial results for the period from November 11, 2025, to May 10, 2026.

- As of May 10, 2026, total net assets were ¥2,661 million, representing a decrease of ¥922 million from the previous period.

- The composition of major investment assets was 97.1% (¥2,584 million), with cash, deposits, and other assets (net of liabilities) at 2.9% (¥76 million).

- The net asset value per unit was ¥50,450 (an increase of ¥6,257 from the previous period), and the distribution per unit was ¥503 (an increase of ¥83).

- The number of outstanding units decreased from 81 thousand units at the end of the previous period to 52 thousand units at the end of the current period.

🤖 AI Perspective

The decrease in net assets during the period, alongside an increase in both net asset value per unit and distribution per unit, suggests a significant reduction in outstanding units. This shift, coupled with an operating revenue of ¥391 million, which includes gains from securities trading, might indicate a strategic adjustment or market impact on the fund’s structure. Investors may wish to monitor the fund’s distribution policy and asset allocation in future reports.

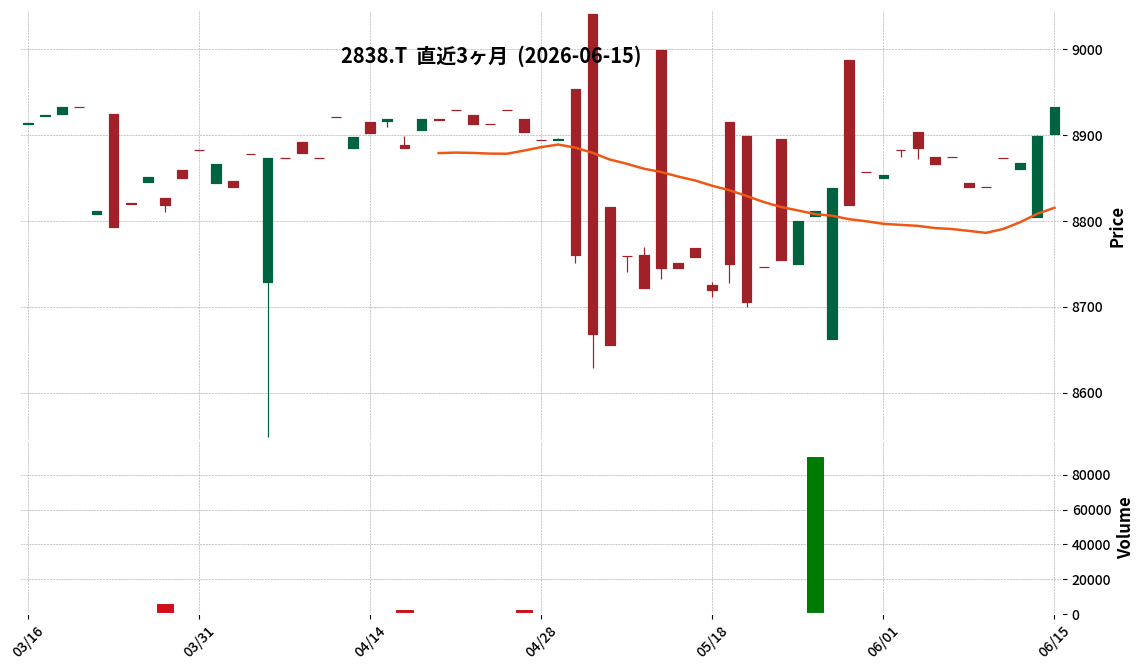

2838|MX米債7-10ヘ無

8933.0

▲ +0.38%

📎 Source:MX米債7-10ヘ無 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- MAXIS US Treasury 7-10 Year ETF (Hedge-Free) (Code: 2838) announced its financial results for the May 2026 period (November 11, 2025 – May 10, 2026).

- Net assets for the current period reached ¥9,885 million, an increase from ¥5,887 million in the previous period (November 2025).

- The number of outstanding units at the end of the current period rose to 1,131 thousand units, up from 674 thousand units in the previous period.

- The net asset value per unit was ¥8,740 for the current period, compared to ¥8,729 in the previous period.

- The distribution per unit for the current period was ¥151, a decrease from ¥186 in the previous period.

🤖 AI Perspective

The increase in net assets and outstanding units for the period suggests an inflow of capital from investors. Conversely, the decrease in the distribution per unit compared to the previous period may warrant attention for insights into the fund’s revenue structure and distribution policy. The fluctuation in NAV per unit likely reflects movements in the US Treasury market and the characteristics of the unhedged foreign exchange exposure.

2839|MX米債7-10ヘ有

5073.0

▲ +0.63%

📎 Source:MX米債7-10ヘ有 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Net assets for the fiscal year ended May 2026 (November 11, 2025 – May 10, 2026) amounted to ¥6,165 million, a decrease from ¥8,303 million in the November 2025 period.

- The primary investment asset, bonds, totaled ¥6,103 million (99.0% of the portfolio), with cash, deposits, and other assets (net of liabilities) at ¥61 million (1.0%).

- Outstanding units at the end of the current period were 1,209 thousand units, a decrease of 361 thousand units from 1,570 thousand units in the previous period.

- The net asset value (NAV) per unit was ¥5,099, a decline of ¥189 from ¥5,288 in the November 2025 period.

- The distribution per unit was ¥95, a decrease of ¥12 from ¥107 in the November 2025 period.

- Operating income for the current period was an operating loss of △¥95,612,708.

🤖 AI Perspective

The financial results for MAXIS US Treasury 7-10 Year ETF (Hedged) for the May 2026 period indicate a decrease in net assets and outstanding units, alongside a decline in NAV per unit. These trends may suggest a contraction in fund size and performance. Additionally, the decrease in distribution per unit compared to the previous period could impact investor returns.

9235|G-売れるネットG

501.0

▼ -6.53%

📎 Source:G-売れるネットG Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Ureru Net Advertising Group has signed a basic agreement to acquire all shares of Light Inc., an AI service development and operation company, making it a wholly owned subsidiary.

- Light Inc. engages in digital content operation support, operational verification and testing, and AI service development and operation.

- Key financial highlights for Light Inc. include sales ranging from ¥165 million to ¥254 million, a consistent black operating profit, and an increasing trend in net assets.

- The reasons for this M&A include synergy with the group’s AEO (AI Search Optimization) business, establishing a comprehensive AI-related service deployment system, and building a next-generation AI platform.

- Ureru Net Advertising Group states that this agreement will serve as a catalyst to foster AI service development and operation as a new growth driver, aiming to evolve into an AI-native company.

🤖 AI Perspective

This basic agreement suggests a strategic pivot by Ureru Net Advertising Group towards strengthening its AI-related business segments. The integration of Light Inc.’s AI development capabilities and its “Tacit Hub” concept, which aims to visualize and leverage tacit knowledge into AI assets, could enhance the group’s overall AI solution offerings. This move may position the company to accelerate its transformation into an “AI-native enterprise,” as outlined in its long-term vision.

254A|AIフュージョンCG

972.0

▼ -0.72%

📎 Source:AIフュージョンCG Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- AI Fusion Capital Group’s consolidated subsidiary, Mirai Service Holdings (MSH), has resolved to acquire shares in Saiji Japan Inc. and make it a consolidated subsidiary.

- MSH will acquire 51 shares (51.0% of the total outstanding shares) of Saiji Japan for ¥51,000,000.

- Saiji Japan, established on May 8, 2026, operates comprehensive wagashi pop-up event businesses, planning three segments: original brand business, franchise business, and OEM/wholesale business.

- The payment and acquisition of shares are scheduled for early July 2026.

- The acquisition price was determined based on a shareholder valuation (DCF method) by a third party, Route Inc.

🤖 AI Perspective

This acquisition is noteworthy as AI Fusion CG Group, centered on “AI x Finance” growth support, integrates a new distribution model in wagashi pop-up events. The combination of Saiji Japan’s expertise in wagashi events and AI Fusion CG Group’s strengths in AI/DX operational efficiency, SNS marketing, and B2B sales channel development could generate significant business synergies. This move may also suggest a strategic approach to addressing challenges in the wagashi industry, such as business succession and labor shortages, through M&A and franchise models.

7782|シンシア

461.0

▼ -2.12%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SINCERITY, INC. resolved to change its dividend policy and revise its FY2026 dividend forecast (increase) at the Board of Directors meeting held on June 15, 2026.

- The dividend policy will change from a performance-linked dividend targeting a consolidated payout ratio of approximately 40% to a policy with a minimum DOE (Dividend on Equity) of 4.0% of consolidated shareholders’ equity.

- The new dividend policy aims to further enhance the predictability and stability of dividends for shareholders.

- In the event of significant changes in capital structure due to large-scale M&A or similar, shareholder return, including the dividend policy, may be reviewed again.

- The year-end dividend forecast for FY2026 has been revised upwards by ¥2, from the previously announced ¥16 to ¥18 per share.

- The new dividend policy will apply starting from the dividends for the fiscal year ending December 2026.

🤖 AI Perspective

SINCERITY’s shift in dividend policy from a profit-linked model to one based on DOE (Dividend on Equity) as a minimum suggests a strategic move to enhance the stability and predictability of shareholder returns. The introduction of DOE could be perceived as a commitment to more consistent dividends, less susceptible to fluctuations in net profit, which may be viewed favorably by the market. Furthermore, the upward revision of the FY2026 dividend forecast illustrates a concrete step towards strengthening returns under the new policy.

8303|SBI新生銀行

1496.5

▲ +2.50%

📎 Source:SBI新生銀行 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SBI Shinsei Bank announced a partial correction to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 [Japanese GAAP]” originally disclosed on May 1, 2026.

- The corrections affect the summary information, as well as pages 3, 10, and 11 of the attached materials.

- Specific numerical data for “Consolidated Cash Flows” within the FY2026 March consolidated results were revised as follows:

- Cash flows from operating activities: From ¥1,895,839 million (before correction) to ¥1,914,143 million (after correction), an increase of ¥18,304 million.

- Cash flows from investing activities: From △¥1,170,988 million (before correction) to △¥1,189,291 million (after correction), an increase in outflow of ¥18,303 million.

- The year-end balance of cash and cash equivalents remains unchanged at ¥4,623,613 million.

- The reason for the correction was stated as the discovery of errors in the descriptions after the submission of the original financial results.

🤖 AI Perspective

This correction primarily adjusts the figures for cash flows from operating and investing activities, with no impact on the reported year-end balance of cash and cash equivalents. For investors, understanding the specific adjustments within the cash flow statement can be important for an accurate assessment of the bank’s financial liquidity and operational efficiency. The accuracy of financial reporting is a key indicator of corporate governance, and such corrections warrant attention in the context of future disclosures.

9556|G-INTLOOP

1739.0

▲ +5.52%

📎 Source:G-INTLOOP Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- On June 15, 2026, G-INTLOOP Inc. released supplementary materials for its “FY26/7 Q3 Third Quarter Financial Results Briefing.”

- For the full-year FY27/7 (consolidated) financial forecast, the company projects net sales of 48,000 million yen to 50,500 million yen, representing an increase of 20.0% to 26.3% compared to the FY26/7 forecast.

- Operating profit for the same period is forecast to be 3,500 million yen to 4,600 million yen (an increase of 150.0% to 228.6% compared to the FY26/7 forecast), and profit attributable to owners of parent is expected to be 2,300 million yen to 3,000 million yen (an increase of 253.8% to 361.5% compared to the FY26/7 forecast).

- The target operating profit margin for FY27/7 is set at 7.3% to 9.1%, with a commitment to maintaining this target while planning investments in AI-related new businesses.

- For the achievement image of the FY27/7 full-year forecast, the company states that an operating profit of 3.2 billion yen is achievable by merely maintaining current profitability levels, with an expected range of 3.5 billion yen to 4.6 billion yen due to revenue contributions from newly hired personnel and other factors.

🤖 AI Perspective

This supplementary document provides a more detailed breakdown and achievement image for the FY27/7 full-year performance forecast, complementing the previously disclosed earnings materials. The focus on leveraging enhanced human capital and transitioning to an AI-centric operational structure appears to be key drivers for future revenue growth and profitability improvement. Furthermore, the company’s stated intent to balance new business investments with sustained profitability may indicate the strategic direction of its growth.

2294|柿安本店

2535.0

▼ -0.20%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kakiyasu Honten’s consolidated financial results for the fiscal year ended April 2026 reported net sales of ¥36,072 million (△0.1% year-on-year) and operating profit of ¥1,426 million (△4.9% year-on-year).

- Net profit attributable to owners of the parent increased by 15.7% year-on-year to ¥811 million.

- By segment, the Meat Business recorded net sales of ¥13,573 million (△1.7% year-on-year) and segment profit of ¥1,020 million (+31.3% year-on-year). The Prepared Foods Business reported net sales of ¥12,821 million (+0.1% year-on-year) and segment profit of ¥916 million (△21.8% year-on-year).

- The year-on-year decrease in operating profit by △¥74 million for FY2026/4 was primarily due to a △¥385 million impact from rising raw material costs, partially offset by increased profits from existing stores and the effects of new store openings/renovations/closures (+¥155 million).

- For FY2027/4, the company forecasts net sales of ¥36,000 million (△0.2% year-on-year), operating profit of ¥1,400 million (△1.9% year-on-year), and net profit attributable to owners of the parent of ¥800 million (△1.4% year-on-year).

🤖 AI Perspective

Kakiyasu Honten’s FY2026/4 results show a slight decline in net sales and operating profit, but a double-digit increase in net profit attributable to owners of the parent. The Meat Business significantly boosted profits, while the Prepared Foods Business saw a decline, suggesting shifts in business dynamics. The company’s efforts to mitigate rising raw material costs through existing store growth and expansion strategies, alongside future initiatives like multi-format stores and enhanced e-commerce, could be key areas for investors to monitor when evaluating its medium-term growth strategy.

3434|アルファCo

1194.0

▼ -0.08%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- ALPHA Corporation announced its consolidated financial results for the fiscal year ended March 31, 2026. Net sales were ¥72,699 million (down 1.1% year-on-year), and operating profit was ¥843 million (down 7.7% year-on-year).

- Ordinary profit increased significantly to ¥1,618 million (up 165.5% year-on-year), and net profit attributable to parent company shareholders was ¥1,383 million (compared to a loss of ¥301 million in the previous year). This was primarily due to ¥837 million in foreign exchange gains and ¥278 million in extraordinary income, including the liquidation gain of a Chinese subsidiary.

- By segment, the Automotive Parts Business reported net sales of ¥57,430 million (up 0.2% YoY) and operating profit of ¥383 million (up ¥308 million YoY). The Security Equipment Business recorded net sales of ¥15,269 million (down 5.8% YoY) and operating profit of ¥2,033 million (down ¥499 million YoY).

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥73,000 million (up 0.4% from previous year), operating profit of ¥1,500 million (up 77.9% from previous year), ordinary profit of ¥1,300 million (down 19.7% from previous year), and net profit attributable to parent company shareholders of ¥1,000 million (down 27.7% from previous year).

- The annual dividend for FY2026 was ¥48 (interim ¥20, year-end ¥28), and the forecast for FY2027 is ¥51 (interim ¥21, year-end ¥30).

9262|シルバーライフ

646.0

▼ -0.62%

📎 Source:シルバーライフ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Silver Life Co., Ltd. resolved on June 15, 2026, at its Board of Directors meeting, to acquire all shares of Narita Refrigeration Co., Ltd., making it a subsidiary.

- Narita Refrigeration Co., Ltd. is located in Minato-ku, Nagoya, Aichi Prefecture, and engages in ice manufacturing, refrigerated warehousing, and frozen food sales. It was established on March 25, 1960, with a capital of 36 million JPY.

- The acquisition aims to strengthen Silver Life Group’s frozen food storage and logistics functions for its frozen bento manufacturing/mail-order and OEM businesses, complement its cold chain network in the Tokai/Kansai regions via bonded warehouses near Nagoya Port, and enhance stability in the supply chain including raw material procurement and import/export.

- The acquisition price is 150 million JPY (estimated), to be funded by Silver Life’s own capital. The share transfer execution date is scheduled for June 23, 2026.

- This marks Silver Life’s first M&A transaction, and its impact on the consolidated financial results for the fiscal year ending July 2026 is expected to be minor.

🤖 AI Perspective

This acquisition appears to be part of Silver Life’s strategy to bolster its manufacturing, logistics, and sales capabilities to meet the growing demand for meal delivery services in an aging society. The integration of Narita Refrigeration’s cold logistics and frozen storage capabilities could lead to improved delivery efficiency and a more stable supply system. As Silver Life’s inaugural M&A, it may indicate a strategic commitment to strengthening its business foundation and enhancing long-term corporate value.

2998|G-クリアル

471.0

▲ +8.53%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-CREAL resolved to change and expand its shareholder benefits program at the Board of Directors meeting held on June 15, 2026.

- Effective from the September 2026 record date, the shareholder benefit item will be changed from the traditional QUO card to “Digital Gift®” provided by Digital Plus Co., Ltd.

- Digital Gift® exchange options include various electronic money and points such as PayPay Money Light, Amazon Gift Card, and Bitcoin.

- From the September 2026 record date onwards, shareholders holding 500 shares to less than 1,000 shares will receive 5,000 JPY equivalent per period, and those holding 1,000 shares or more will receive 12,000 JPY equivalent per period.

- From the September 2027 record date onwards, shareholders holding company shares for one year or more will receive enhanced benefits: 6,000 JPY equivalent for 500 shares to less than 1,000 shares, and 13,000 JPY equivalent for 1,000 shares or more.

🤖 AI Perspective

The shift to Digital Gift® as a benefit item may enhance shareholder convenience by offering a wider range of redemption options. The introduction of increased benefits for holders of 1,000 shares or more, along with incentives for long-term holding, could suggest a strategy to foster a more stable shareholder base and encourage sustained investment. These adjustments appear designed to strengthen shareholder returns and improve the company’s investment appeal.

3195|ジェネパ

417.0

▲ +1.71%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Genepa announced its consolidated financial results for the second quarter (interim) of the fiscal year ending October 2026.

- Net sales reached ¥9,655 million, marking a 15.8% increase compared to the same period of the previous year.

- Operating profit was ¥153 million, representing a substantial increase of 92.8% year-over-year.

- Ordinary profit stood at ¥146 million (+15.0% YoY), while net income attributable to owners of the parent was ¥119 million (-2.0% YoY).

- The full-year consolidated performance forecast remains unchanged from the most recently published forecast, projecting net sales of ¥18,600 million, operating profit of ¥250 million, ordinary profit of ¥240 million, and net income attributable to owners of the parent of ¥180 million.

🤖 AI Perspective

The interim results suggest that the expansion of D2C product sales in the EC Marketing business and the rapid growth of recovery wear in the Product Planning related business were key drivers for the significant increases in consolidated net sales and operating profit. The decrease in net income attributable to owners of the parent, despite strong operational performance, appears to be primarily due to a reduction in foreign exchange gains compared to the prior interim period. With the full-year forecasts remaining constant, the company’s progress in achieving these targets in the latter half of the fiscal year will be a point of interest for investors.

3388|明治電機

2105.0

▲ +3.29%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Meiji Electric Industries, Ltd. announced on June 15, 2026, a correction to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 (Japanese GAAP)” initially published on May 15, 2026.

- The reason for the correction was an aggregation error in “Loss on extinguishment of share-based payment expenses” and “Other” within non-operating expenses for the prior consolidated fiscal year (April 1, 2024, to March 31, 2025) in the consolidated statement of income.

- The “Loss on extinguishment of share-based payment expenses” for the prior consolidated fiscal year was corrected from 1,803 thousand yen to 380 thousand yen.

- The “Other” non-operating expense for the prior consolidated fiscal year was corrected from 1,051 thousand yen to 2,474 thousand yen.

- Despite these individual corrections, the total non-operating expenses for the prior consolidated fiscal year remained unchanged at 12,295 thousand yen.

🤖 AI Perspective

This correction stems from an aggregation error in specific non-operating expenses for a past fiscal year, and the announced revisions indicate no change to the total non-operating expenses. Therefore, the direct impact on the company’s overall profitability or financial position appears to be limited. For investors, it may be worth monitoring how the background and outcome of this correction might influence perceptions of the accuracy of future disclosures.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

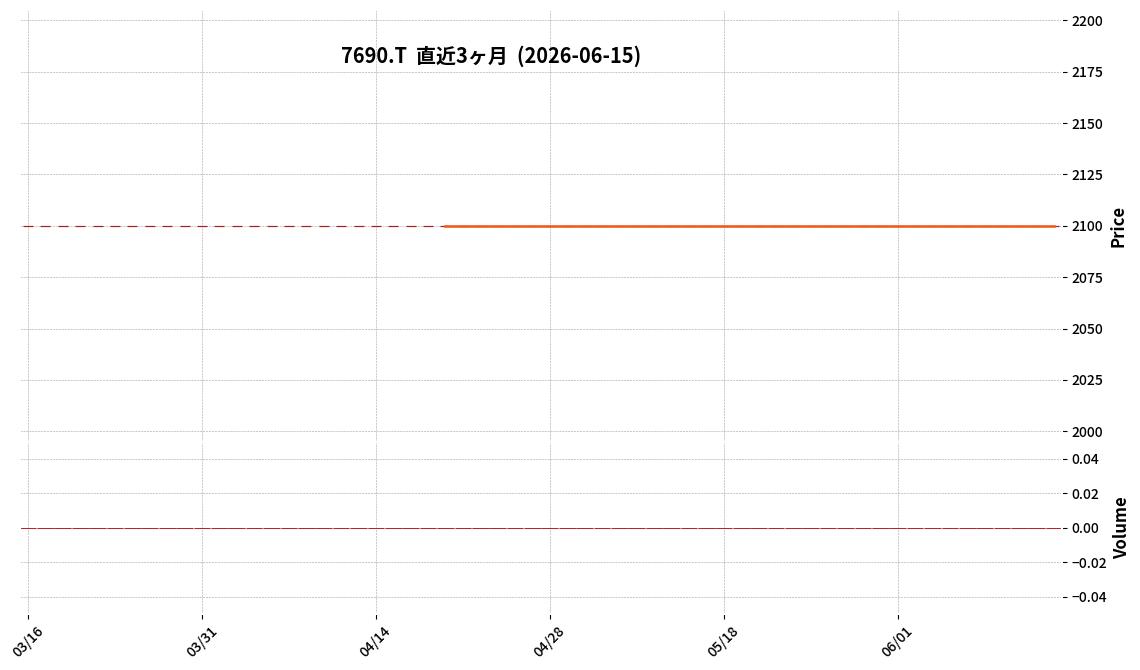

7690|P-カレント自動車

2100.0

▲ +0.00%

📎 Source:P-カレント自動車 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- P-Current Motor announced its interim financial results for the fiscal year ending October 2026 (November 1, 2025 – April 30, 2026).

- For the interim period, net sales were ¥5,533 million, representing a 0.3% increase year-on-year.

- Operating profit reached ¥416 million (up 93.5% year-on-year), ordinary profit was ¥413 million (up 89.8% year-on-year), and net income for the interim period was ¥271 million (up 89.2% year-on-year).

- Diluted earnings per share for the interim period were ¥460.39.

- The full-year forecast (Net Sales: ¥10,310 million, Operating Profit: ¥352 million, Ordinary Profit: ¥339 million, Net Income: ¥220 million) remains unchanged from the previously announced figures.

- As of the end of the interim accounting period, total assets were ¥2,440 million, net assets were ¥1,273 million, and the equity ratio was 52.2%.

🤖 AI Perspective

While net sales showed a slight increase, the significant surge in operating profit, ordinary profit, and net income for the interim period suggests a marked improvement in profitability for P-Current Motor. The substantial 93.5% increase in operating profit compared to the prior year period may indicate successful operational efficiencies or focused business strategies. With the full-year forecast remaining unchanged, investor attention may now turn to the company’s performance in the latter half of the fiscal year to meet these targets.

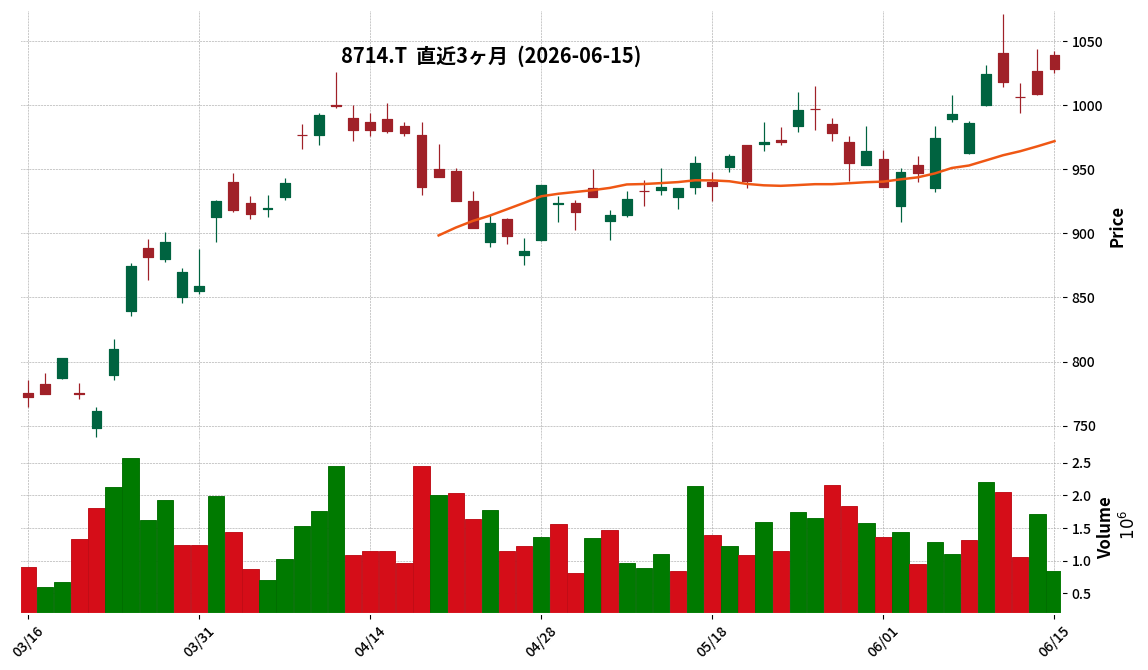

8714|池田泉州

1028.0

▲ +1.88%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- **Deposit Strategy**: The company plans an increase of JPY 110 billion in individual deposits through “foundation/empathy” (non-interest bearing) methods and JPY 30 billion via interest-bearing deposits. Corporate deposits are planned to increase by JPY 60 billion, aiming to maintain debtor deposits in line with lending share.

- **01 Bank**: The JPY 30 billion consolidated net income planned for FY2028 does not include profit from 01 Bank, which is viewed as break-even. The bank aims for profitability within three years of opening, focusing on increasing the number of borrowers, enhancing recognition through offline sales, and advanced credit modeling.

- **Securities**: The portfolio is constructed with a balance between held-to-maturity and other securities, considering liquidity risk.

- **Ikeda Senshu-Shiga Alliance**: A capital alliance with an ownership ratio of 0.5-1% has been established. There is a possibility of increasing this ratio based on future discussions.

- **Digital Talent**: Under the 6th Medium-Term Management Plan, the company plans to increase approximately 200 “digital base personnel” who possess IT Passport qualifications and sufficient business experience. This increase will be achieved through internal training rather than mid-career hires.

🤖 AI Perspective

The Q&A summary from Ikeda Senshu Holdings highlights a multi-faceted approach to deposit acquisition in a changing interest rate environment, progress on its key growth driver 01 Bank, and a commitment to digital talent development for long-term competitiveness. The strategy to balance deposit quality and quantity, especially with a loan-to-deposit ratio of 83%, appears crucial for future profitability management. The successful realization of 01 Bank’s profitability target within three years could significantly impact the achievement of the medium-term management plan.

1840|土屋HD

237.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the second quarter (interim period) of the fiscal year ending October 2026, consolidated net sales were ¥14,018 million, an increase of 10.9% compared to the same period in the previous year.

- The company reported an operating loss of ¥1,190 million (compared to an operating loss of ¥823 million in the prior year interim period) and an ordinary loss of ¥1,150 million (compared to an ordinary loss of ¥813 million in the prior year interim period).

- Net loss attributable to owners of the parent expanded to ¥896 million, from a loss of ¥697 million in the previous year interim period.

- By segment, housing business sales increased by 25.7% year-on-year to ¥9,656 million, while renovation business sales decreased by 17.0% to ¥1,096 million, and real estate business sales decreased by 7.4% to ¥3,392 million.

- The full-year consolidated earnings forecast for the fiscal year ending October 2026 remains unchanged, with projected net sales of ¥35,000 million, operating profit of ¥400 million, ordinary profit of ¥400 million, and net profit attributable to owners of the parent of ¥260 million.

🤖 AI Perspective

Tsuchiya HD’s Q2 FY2026 results show increased net sales year-on-year, but operating, ordinary, and net losses all widened. This suggests that while significant non-housing project sales in the housing segment boosted overall revenue, factors like reduced detached housing deliveries, declining revenue in the renovation and real estate segments, and a lower gross profit margin likely impacted profitability. Given the company’s stated seasonal fluctuation where a larger proportion of construction is completed in the second half due to winter, the progress towards its full-year forecast will be worth monitoring.

189A|G-D&Mカンパニー

913.0

▲ +0.33%

📎 Source:G-D&Mカンパニー Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-D&M Company resolved to partially amend and expand its shareholder benefit program at a Board of Directors meeting held on June 15, 2026.

- The revised shareholder benefit program will take effect from the shareholder benefits based on the record date of May 31, 2027.

- The record date will change from annually on November 30 to semi-annually on May 31 and November 30.

- The total annual benefit fund will be expanded from JPY 10 million to JPY 20 million (JPY 10 million per record date).

- From the May 31, 2027 record date onwards, the system will eliminate the 1-unit/2-unit grant categories and continuous holding conditions, instead calculating the equivalent benefit amount per shareholder based on the number of eligible shareholders at each record date.

- Eligible shareholders are those holding 300 or more shares of the company’s common stock on each record date.

- The benefit content remains electronic gifts.

- The shareholder benefits for the November 30, 2026 record date will be implemented as announced on May 11, 2026, without changes.

🤖 AI Perspective

The announced changes appear to aim at broadening the shareholder base and enhancing stock liquidity, with the increased frequency and annual fund potentially attracting a wider range of individual investors. The simplification of the benefit calculation method could make the value of the benefits more transparent and easily understood by shareholders. This move may be interpreted as the company reinforcing its commitment to shareholder returns.

2345|HODL1

198.0

▲ +2.06%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- HODL1 announced its consolidated financial results for the second quarter (interim period) of the fiscal year ending October 2026.

- For the interim period, net sales were 47 million yen (up 234.3% year-on-year), EBITDA was -202 million yen, operating loss was -202 million yen, ordinary loss was -184 million yen, and net loss attributable to parent company shareholders was -244 million yen.

- Interim net loss per share was -13.17 yen.

- As of the end of the interim period, total assets were 331 million yen, net assets were 244 million yen, and the equity ratio was 52.8%.

- The company launched its AI Management Agent business in May 2026.

- There are material events or conditions that may cast significant doubt on the company’s ability to continue as a going concern.

2424|ブラス

613.0

▲ +2.17%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Brass Co., Ltd. has announced its consolidated financial results for the third quarter of the fiscal year ending July 2026.

- For the nine months ended April 30, 2026, net sales were ¥10,514 million, representing a 5.0% increase compared to the same period of the previous year.

- Operating profit decreased by 27.6% year-on-year to ¥419 million, and ordinary profit decreased by 33.7% to ¥395 million.

- Net profit attributable to owners of parent declined by 45.3% year-on-year to ¥223 million.

- The number of weddings and receptions held was 2,418 (up 1.2% year-on-year), with an average unit price of ¥4,095 thousand (up 2.9% year-on-year).

- The number of orders received significantly increased to 3,018 (up 16.1% year-on-year).

- The full-year consolidated earnings forecast remains unchanged from the announcement made on March 13, 2026.

🤖 AI Perspective

Brass’s Q3 FY2026 results show a notable increase in net sales, but a decline in various profit metrics compared to the previous year. The growth in the number of weddings, average unit price, and order backlog suggests a healthy underlying business activity. However, rising labor costs and raw material prices, as noted for the wedding industry, appear to be impacting profit margins, which is a key area for investors to monitor.

2978|G-ツクルバ

382.0

▲ +5.52%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the nine months ended April 30, 2026 (Q3 FY2026), consolidated net sales amounted to ¥7,902 million, representing a 36.6% increase compared to the prior year period.

- During the same period, the company reported an operating loss of ¥39 million (compared to an operating profit of ¥149 million in the prior year), an ordinary loss of ¥147 million (compared to an ordinary profit of ¥93 million in the prior year), and a net loss attributable to owners of parent of ¥84 million (compared to a net profit of ¥0 million in the prior year).

- Total assets increased by ¥1,438 million from the end of the previous fiscal year to ¥7,580 million, primarily due to a ¥1,652 million increase in real estate for sale.

- The consolidated full-year forecast for FY2026 has been revised: Net sales are projected at ¥11,500 million (a 42.0% increase year-on-year), operating income at ¥130 million (a 52.6% decrease year-on-year), and net income attributable to owners of parent is expected to range from a loss of ¥50 million to ¥0 million.

- During the third quarter, Cowcamo Komuten Inc. was newly included in the scope of consolidation.

🤖 AI Perspective

G-Tsukuruba’s Q3 FY2026 results show robust sales growth, but a shift to losses across various profit metrics. This divergence may suggest increased investment in marketing activities for its core service “cowcamo” and higher procurement costs associated with an increase in real estate for sale. The revised full-year forecast, which upgrades sales but downgrades profit expectations, indicates a strategic focus on expanding operations, making the balance between growth and profitability a key area for investors to monitor.

3134|Hamee

399.0

▼ -1.48%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hamee Corporation announced its consolidated financial results for the fiscal year ended April 2026. Net sales were ¥22,073 million (down 3.6% YoY), operating profit was ¥983 million (down 58.2% YoY), ordinary profit was ¥761 million (down 67.6% YoY), and profit attributable to owners of parent was ¥541 million (down 57.6% YoY).

- Profit attributable to owners of parent for FY2026/4 was ¥541 million, with basic earnings per share of ¥33.85.

- Consolidated financial position showed total assets of ¥13,574 million, net assets of ¥7,319 million, and an equity ratio of 53.5%.

- During the period, NE Corporation was deconsolidated, and its contribution to the Platform segment’s performance was limited to the interim consolidated accounting period.

- The consolidated earnings forecast for FY2027/4 projects net sales of ¥22,817 million (up 3.4% YoY), operating profit of ¥502 million (down 48.9% YoY), ordinary profit of ¥369 million (down 51.5% YoY), profit attributable to owners of parent of ¥230 million (down 57.4% YoY), and basic earnings per share of ¥14.13.

🤖 AI Perspective

Hamee’s consolidated financial results for FY2026/4 show a decrease in sales and profits across all categories, which may be attributed to the structural impact of NE Corporation’s deconsolidation. While the cosmetics business performed strongly due to the expansion of its base makeup category and improved cost of goods sold, the mobile life business faced intensified competition. The FY2027/4 forecast projects increased revenue but decreased profit, suggesting an ongoing restructuring of the business following the deconsolidation of NE Corporation.

3166|OCHI・HD

1384.0

▲ +0.80%

📎 Source:OCHI・HD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 2026, consolidated net sales were ¥120,432 million (up 2.9% year-on-year), and operating profit was ¥1,669 million (up 13.5% year-on-year).

- The Engineering segment showed significant growth, with net sales up 48.7% and operating profit up 159.4% year-on-year, primarily due to M&A effects from the previous fiscal year and completion of large-scale projects.

- By segment, the Building Materials, Processing, and Environmental Amenity segments experienced profit decreases, while the Engineering and Other segments saw profit increases.

- The consolidated performance forecast for the fiscal year ending March 2027 projects net sales of ¥125,000 million (up 3.8% year-on-year) and operating profit of ¥1,850 million (up 10.8% year-on-year).

- For FY2027/3, segment-wise operating profit forecasts show a 71.2% increase for Building Materials and a 30.4% increase for Processing, while the Engineering segment is projected to decrease by 18.7%.

🤖 AI Perspective

The FY2026/3 results highlight that M&A-driven expansion in the Engineering segment was a key factor in overall revenue and profit growth. However, the profit decline in traditional core businesses like the Building Materials segment suggests that the progress of initiatives for business portfolio transformation may be crucial. For the FY2027/3 forecast, as the profit growth of the Engineering segment is expected to stabilize, the planned recovery in the Building Materials and Processing segments will be a focus for investors, indicating a shift in segment contributions.

3287|R-星野

239600.0

▲ +0.76%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- R-Hoshino reported operating revenue of ¥9,344 million for the 2026 April fiscal period, marking a 7.5% increase compared to the 2025 October period.

- Operating income for the same period was ¥4,855 million (+12.3%), ordinary income was ¥3,998 million (+12.4%), and net income was ¥3,997 million (+12.4%).

- Earnings per unit were ¥6,823, and distribution per unit (excluding distribution in excess of earnings) amounted to ¥6,832.

- Total assets stood at ¥257,260 million, net assets at ¥146,322 million, and the equity ratio was 56.9%.

- For the 2026 October fiscal period, the forecast operating revenue is ¥9,422 million with a distribution per unit of ¥6,700, and for the 2027 April fiscal period, the forecast operating revenue is ¥9,563 million with a distribution per unit of ¥6,850.

🤖 AI Perspective

R-Hoshino’s 2026 April fiscal results show consistent growth across key financial metrics, including operating revenue and net income, indicating robust operational performance. The reported distribution per unit exceeding earnings per unit suggests a strategy that may involve the utilization of a portion of retained earnings from compression reserves for distributions. The positive outlook for the upcoming fiscal periods, with projected increases in revenue and stable distributions, could be a point of interest for investors.

3309|R-積水ハウスリート

79600.0

▲ +0.00%

📎 Source:R-積水ハウスリート Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- R-Sekisui House Reit announced its financial results for the April 2026 fiscal period (November 1, 2025, to April 30, 2026) on June 15, 2026.

- Operating revenue reached ¥22,350 million, representing a 15.3% increase compared to the previous period.

- Operating income grew by 25.2% to ¥13,526 million, ordinary income by 26.6% to ¥12,050 million, and net income by 26.6% to ¥12,047 million.

- Distribution per unit (including excess distribution) was ¥3,407, up from ¥2,329 in the previous period.

- Forecasts for the October 2026 and April 2027 fiscal periods project operating revenues of ¥17,416 million and ¥17,457 million, respectively.

🤖 AI Perspective

The financial results for the April 2026 fiscal period indicate substantial growth across all key profitability metrics, with double-digit increases year-over-year. The significant rise in distribution per unit could be a key factor for investor attention. However, the subsequent period forecasts for October 2026 and April 2027 suggest a potential decrease in operating revenue and profits compared to the current period, which may warrant monitoring by investors.

3415|トウキョウベース

373.0

▲ +8.75%

📎 Source:トウキョウベース Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- TOKYO BASE Co., Ltd. announced its consolidated financial results for the first quarter of FY2027 (February 1, 2026 – April 30, 2026).

- Consolidated performance showed net sales of ¥6,134 million (up 24.1% year-on-year), operating profit of ¥415 million (up 10.1% YoY), ordinary profit of ¥480 million (up 89.1% YoY), and net income attributable to owners of parent of ¥235 million (up 23.7% YoY).

- Sales from domestic physical stores increased by 121.4% year-on-year, with inbound sales specifically increasing by 147.4% YoY.

- Overseas business sales grew by 137.2% year-on-year, while EC business sales saw a 126.5% increase for self-operated EC and a 154.9% increase for ZOZO.

- The consolidated full-year forecast for FY2027 remains unchanged, projecting net sales of ¥28,000 million (up 17.4% from previous year) and net income attributable to owners of parent of ¥1,500 million (up 29.9% from previous year).

3565|アセンテック

405.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Ascentec reported consolidated net sales of ¥3,410,092 thousand for the first quarter of FY2027 (February 1, 2026 – April 30, 2026), representing a 45.5% decrease compared to the same period in the previous year.

- Operating profit was ¥571,347 thousand (down 26.7% YoY), ordinary profit was ¥363,285 thousand (down 68.2% YoY), and net profit attributable to owners of the parent was ¥249,343 thousand (down 68.5% YoY).

- The primary reason for the decrease in revenue was attributed to the rebound effect from a large virtual desktop software project recorded in the same quarter of the previous fiscal year.

- While there were positive factors for profit, such as steady adoption of the company’s “Remote PC Array” in local governments and increased sales of high-margin zero-trust security products to large enterprises, the overall profit declined due to reduced gross profit in the virtual desktop business segment resulting from lower revenue.

- A foreign exchange loss of ¥239,715 thousand was recorded, which impacted ordinary profit and net profit.

- The forecast for the full-year dividend, adjusted for the stock split, is ¥15.00 per share (interim ¥7.00, year-end ¥8.00).

🤖 AI Perspective

Ascentec’s Q1 FY2027 results indicate a significant impact from the absence of a large project recorded in the prior year’s comparable quarter, affecting both revenue and profit. However, the steady performance of its proprietary “Remote PC Array” and the zero-trust business segment could suggest a potential shift in future revenue structures. The substantial foreign exchange loss also highlights the importance of monitoring currency fluctuations’ impact on the company’s financial performance.

3804|システム ディ

483.0

▲ +2.99%

📎 Source:システム ディ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- System d Co., Ltd. announced its consolidated financial results for the second quarter of the fiscal year ending October 2026.

- Net sales for the interim period reached ¥3,027 million, an increase of 8.2% compared to the same period last year.

- Operating income was ¥652 million (0.0% increase year-on-year), and ordinary income was ¥655 million (0.1% increase year-on-year).

- Net income attributable to owners of parent for the interim period was ¥410 million, a decrease of 8.1% from the prior year.

- The full-year consolidated earnings forecast and dividend forecast remain unchanged from previously announced figures.

🤖 AI Perspective

System d’s Q2 FY2026 results show an increase in net sales but flat operating profit and a decline in net income compared to the previous year. This could suggest that while revenue growth was driven by major project deliveries and steady recurring sales, certain cost factors may have impacted profitability. The unchanged full-year forecast indicates that the company believes its performance is progressing in line with initial plans.

4260|G-ハイブリッドテク

248.0

▼ -1.20%

📎 Source:G-ハイブリッドテク Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hybrid Technologies Co., Ltd. resolved to absorb and merge with its wholly-owned subsidiary, MCP35 Corporation, at a Board of Directors meeting held on June 15, 2026.

- The effective date of the merger is August 15, 2026.

- The merger will be conducted as an absorption-type merger, with Hybrid Technologies Co., Ltd. as the surviving company and MCP35 Corporation as the absorbed company.

- The stated purpose of the merger is to rationalize the organization and business operations, and to optimize the efficient use of management resources across the group.

- This merger qualifies as a simplified absorption-type merger and a short-form merger, meaning shareholder approval procedures will not be required for either company.

🤖 AI Perspective

- This merger involves a wholly-owned subsidiary, suggesting an internal reorganization aimed at enhancing operational efficiency within the group.

- The IR announcement indicates that the impact of this merger on the company’s consolidated financial performance is expected to be minor.

- MCP35 Corporation’s business includes fundraising, financial consulting, and investment activities, which may complement Hybrid Technologies’ core system development and consulting business, potentially creating group-wide synergies.

442A|G-クラシコ

1372.0

▼ -6.28%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Classico announced its unaudited non-consolidated financial results for the second quarter (interim period) of the fiscal year ending October 2026.

- For the interim period, net sales were ¥1,560 million, representing a 7.9% decrease compared to the same period of the previous year.

- The company reported an operating loss of ¥188 million (compared to an operating profit of ¥45 million in the prior interim period), an ordinary loss of ¥194 million (compared to an ordinary profit of ¥36 million), and an interim net loss of ¥197 million (compared to an interim net profit of ¥30 million).

- Diluted earnings per share for the interim period were △¥95.98.

- Total assets stood at ¥2,434 million, net assets at ¥1,628 million, and the equity ratio improved to 66.9%.

- The full-year forecast for the fiscal year ending October 2026 remains unchanged, projecting net sales of ¥4,250 million, operating profit of ¥233 million, ordinary profit of ¥214 million, and net profit of ¥150 million.

🤖 AI Perspective

G-Classico’s Q2 FY2026 results show a year-on-year decrease in sales and a shift to losses across key profit metrics, primarily attributed to a heavier delivery schedule for domestic corporate sales in the latter half of the fiscal year. Despite the interim losses, the company’s total assets and net assets increased, leading to an improved equity ratio, which may suggest a strengthening of its financial structure. The unchanged full-year forecast indicates that the company anticipates a recovery in the second half of the fiscal year, a point worth monitoring for investors.

4592|G-サンバイオ

1210.0

▲ +0.75%

📎 Source:G-サンバイオ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SanBio Co., Ltd. announced its consolidated financial results for the first quarter of the fiscal year ending January 2027 (February 1, 2026, to April 30, 2026).

- The operating loss for the first quarter was ¥953 million, an improvement from the operating loss of ¥1,007 million in the same period of the previous year.

- Ordinary loss narrowed to ¥779 million, down from ¥1,750 million in the previous year’s first quarter, partly due to the recording of ¥177 million in foreign exchange gains.

- Net loss attributable to parent company shareholders was ¥836 million, a decrease from ¥1,531 million in the prior year’s period.

- Research and development expenses amounted to ¥680 million, primarily attributed to costs related to the partial amendment approval for manufacturing and marketing of Akugo®.

- In May 2026, “Akugo® for intracerebral injection” was listed on the drug price standard, with a drug price of ¥72 million, and sales have commenced.

- There are no changes to the full-year and second-quarter consolidated earnings forecasts.

🤖 AI Perspective

G-SanBio’s Q1 FY2027 results show an improvement in operating loss, ordinary loss, and net quarterly loss compared to the previous year. This performance appears to be influenced by foreign exchange gains and the progress in expenses related to the manufacturing and marketing approval of Akugo®. As the company enters a new phase with the commencement of Akugo® sales, its future business revenue trends will be worth monitoring.

4811|G-ドリーム・アーツ

738.0

▲ +1.65%

📎 Source:G-ドリーム・アーツ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Dream Arts Co., Ltd. resolved to enter into a capital and business alliance with Cocoo Co., Ltd. at its board meeting held on June 15, 2026.

- The purpose of this alliance is to expand the support system for the utilization and adoption of the “SmartDB®” no-code development platform for large enterprises following its introduction.

- Both companies aim to train a cumulative total of 100 SmartDB® Certified Specialists (SCS) within three years from the start of the alliance.

- Dream Arts plans to acquire a minority stake in Cocoo by subscribing to a third-party allocation of new shares issued by Cocoo.

- The share acquisition date is June 19, 2026, and Cocoo is not expected to become a consolidated subsidiary or equity-method affiliate of Dream Arts.

🤖 AI Perspective

This alliance is positioned as a concrete measure for Dream Arts’ medium-term management plan’s key success factor “EC2 (External Capability & Capacity),” suggesting an intent to leverage external capabilities to enhance post-introduction utilization and adoption support for SmartDB®, a critical growth driver. The focus on joint DX talent development and the establishment of an accompanying support service “Smadevi® Girls (tentative name)” could indicate a strategic move to strengthen the recurring revenue (ARR) growth foundation of the SmartDB® business while maintaining profitability. This model, designed to scale support without significantly increasing fixed costs, is worth monitoring for its potential impact on future business expansion.

4840|トライアイズ

720.0

▲ +0.28%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tri-Eyes Co., Ltd. announced on June 15, 2026, a strategic partnership with Fungry Inc. aimed at expanding recognition and sales for the “CLATHAS” brand.

- This partnership follows the resolution made at the Board of Directors meeting on May 14, 2026, regarding the “Transfer of Trademark Rights and Recognition of Extraordinary Income,” establishing a framework for both companies to jointly hold brand ownership and commence collaboration after the trademark transfer.

- The collaboration is set to begin on July 1, 2026. Tri-Eyes will continue brand supervision and new sales channel acquisition, while Fungry Inc. will be responsible for digital content planning and production, official digital channel development, and sales promotion support.

- Key initiatives include strengthening the brand’s official portal site, producing and providing promotional digital assets, establishing common customer touchpoints (LINE, email newsletters, etc.) for the brand, and leveraging marketing data.

- The financial impact of this matter has been incorporated into the revised earnings forecasts announced on May 14, 2026, for the second quarter and full fiscal year.

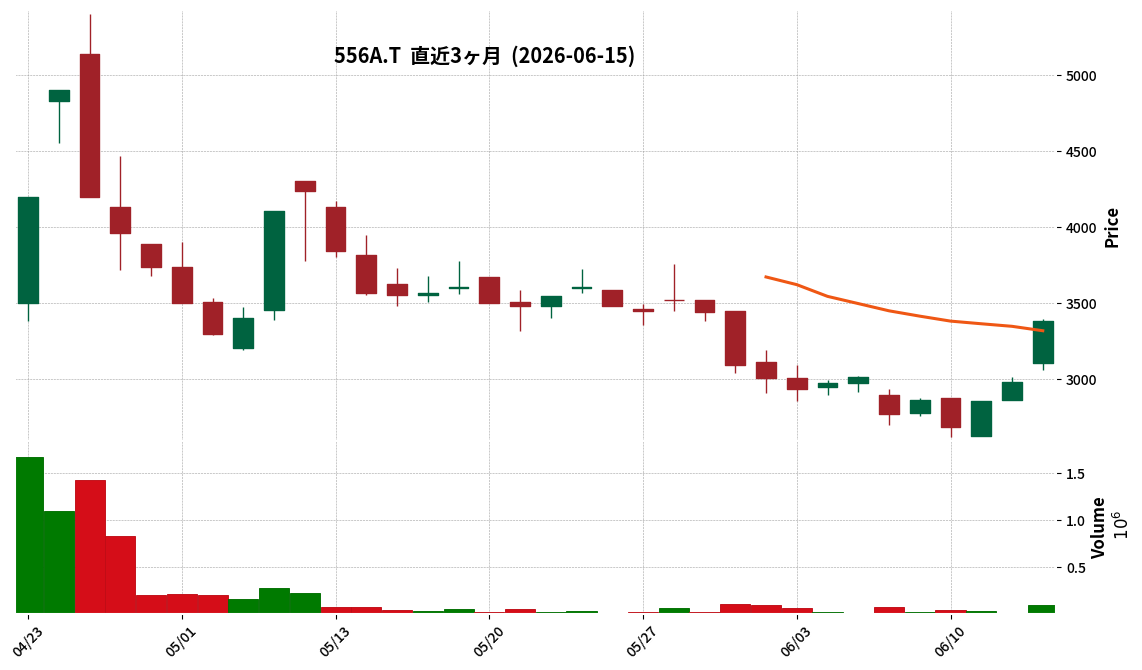

556A|G-犬猫生活

3380.0

▲ +13.23%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Inuneko-Seikatsu reported record-high results for FY2026/4, with net sales of ¥4,494 million (+54.9% YoY) and operating profit of ¥606 million (+550.6% YoY).

- The number of regular subscription members reached 70,186, an increase of +23.5% from the previous fiscal year.

- During the period, the company acquired Masuda Pet Clinic in Shimane Prefecture, expanding its “life services” business area, and was newly listed on the Tokyo Stock Exchange Growth Market in April 2026.

- The operating profit margin improved to 13.4% (+10.2 percentage points YoY), and the equity ratio rose to 74.5% (+33.2 percentage points YoY).

- Donations to animal welfare activities for the period totaled ¥23,277,088 (equivalent to 26% of ordinary profit for FY2025/4).

🤖 AI Perspective

The significant increase in both net sales and operating profit, along with record-high figures for FY2026/4, suggests robust business expansion. The substantial improvement in operating profit margin and equity ratio indicates enhanced profitability and financial stability, which investors may find noteworthy. The execution of strategic initiatives such as M&A and the IPO could be viewed as key drivers for future growth, and their impact will likely continue to be monitored.

6125|岡本工機

5280.0

▲ +8.31%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Okamoto Machine Tool Works reported net sales of ¥42,513 million and operating profit of ¥1,518 million for the fiscal year ended March 2026.

- Net sales decreased year-on-year, despite semiconductor-related equipment sales exceeding the previous year, due to a decline in domestic large-scale surface grinding machine sales.

- Order performance showed an increase in semiconductor-related equipment orders, particularly for final polishers in Japan and East Asia, surpassing the previous year. Domestic machine tool orders also increased year-on-year due to strong replacement demand for small and medium-sized surface grinding machines.

- For the fiscal year ending March 2027, the company forecasts net sales of ¥50,000 million (+17.6% YoY) and operating profit of ¥3,000 million (+97.6% YoY).

- The company aims to achieve the mid-term management plan “INOFINITY700” target of consolidated net sales of ¥50,000 million in FY2027/3, one year later than initially targeted for FY2026/3.

🤖 AI Perspective

The fiscal year ended March 2026 saw a decline in both net sales and profits compared to the previous year, with semiconductor-related equipment order recovery and domestic machine tool replacement demand providing some support. The significant projected increases for the fiscal year ending March 2027, with net sales expected to reach ¥50,000 million and operating profit ¥3,000 million, could draw investor attention. While the achievement of the mid-term management plan’s sales target is delayed by one fiscal year, the company’s commitment to reaching it in the upcoming period is a key point to monitor.

5971|共和工業

6950.0

▼ -0.86%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kyowa Kogyosho announced its consolidated financial results for the fiscal year ended April 2026. Net sales totaled ¥10,828 million, representing a 3.5% increase year-on-year.

- Operating income reached ¥1,088 million (up 32.9% YoY), ordinary income ¥1,256 million (up 34.9% YoY), and net income attributable to owners of parent ¥863 million (up 21.8% YoY).

- Earnings per share (EPS) for the period was ¥663.09, an increase of ¥127.43 from the previous year.

- The year-end dividend was ¥80.00, resulting in a total annual dividend of ¥80.00, unchanged from the prior year.

- For the fiscal year ending April 2027, the company forecasts consolidated net sales of ¥10,740 million (down 0.8% YoY), operating income of ¥720 million (down 33.8% YoY), and net income attributable to owners of parent of ¥610 million (down 29.3% YoY).

🤖 AI Perspective

Kyowa Kogyosho reported significant year-on-year increases across all key profitability metrics for the fiscal year ended April 2026, with operating and ordinary income growing over 30%. This indicates a robust performance in the past period and an improvement in profitability. However, the company’s forecast for the fiscal year ending April 2027 projects a decline in both revenue and profit, with profits expected to decrease by around 30%. This projected downturn may suggest that the company anticipates challenging market conditions, particularly within its main construction machinery sector, which is influenced by factors such as demand stagnation and trade policies. Investors may wish to monitor the company’s strategies to mitigate these anticipated headwinds.

132A|P-アイエヌHD

220.0

▲ +0.00%

📎 Source:P-アイエヌHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Consolidated net sales for the first half of FY2026 reached ¥5,412.8 million, an increase of 8.6% compared to the same period last year.

- Operating profit was ¥100.438 million, a decrease of 0.6% year-on-year.

- Ordinary profit was ¥111.771 million, representing a 6.8% decrease from the prior year.

- Net profit attributable to owners of the parent for the interim period was ¥96.357 million, an increase of 9.3% year-on-year.

- Basic earnings per share for the interim period stood at ¥12.17.

- Total assets at the end of the interim period were ¥9,664 million, net assets were ¥1,302 million, and the equity ratio was 13.5%.

- The full-year consolidated earnings forecast for FY2026 remains unchanged, projecting net sales of ¥11,861 million (up 16.6% year-on-year) and net profit attributable to owners of the parent of ¥34 million (down 62.3% year-on-year).

🤖 AI Perspective

P-IN Holdings’ H1 FY2026 results show a solid 8.6% increase in revenue, while operating and ordinary profits saw slight declines. This could indicate the impact of rising operational costs, such as labor and fuel expenses, within the logistics sector. However, the 9.3% growth in net profit attributable to parent shareholders suggests the company was able to manage these costs effectively enough to secure final profitability.

184A|G-学びエイド

311.0

▲ +0.00%

📎 Source:G-学びエイド Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Manabieid reported net sales of ¥366,074 thousand for the fiscal year ended April 2026, marking a 26.3% increase from the previous fiscal year.

- The company posted an operating loss of ¥171,739 thousand, an ordinary loss of ¥178,797 thousand, and a net loss of ¥179,129 thousand for FY2026/4.

- Service-specific sales showed “Manabieid Master forSchool” sales increased to ¥194,783 thousand (up 148.0% YoY), while “Manabieid forEnterprise” sales decreased to ¥89,258 thousand (down 23.6% YoY).

- As of April 2026, total assets were ¥619,014 thousand (up ¥399,342 thousand from previous year-end), net assets were ¥536,399 thousand (up ¥401,059 thousand from previous year-end), and the equity ratio was 86.7%.

- For the fiscal year ending April 2027, the company forecasts sales of ¥708,000 thousand (up 93.5% YoY), an operating profit of ¥105,000 thousand, an ordinary profit of ¥106,000 thousand, and a net profit of ¥83,000 thousand.

🤖 AI Perspective

While sales increased for the fiscal year ended April 2026, the company reported losses, which appears to be influenced by the strong growth of “Manabieid Master forSchool” counterbalanced by the impact of lost projects in “Manabieid forEnterprise.”

However, the forecast for FY2027/4 projects a significant increase in sales and a return to profitability for operating, ordinary, and net income, suggesting that the “Manabieid Master forSchool” service may drive future performance.

The substantial increase in total and net assets, primarily due to higher cash and deposits, along with an improved equity ratio, could indicate a strengthening of the company’s financial foundation.

278A|G-テラドローン

7250.0

▼ -10.49%

📎 Source:G-テラドローン Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Terra Drone Corporation announced its consolidated financial results for the first quarter of FY2027 (February 1, 2026 – April 30, 2026).

- Net sales for the quarter reached ¥1,010 million, representing a 6.6% increase compared to the same period last year.

- The company reported an operating loss of ¥434 million (compared to ¥283 million loss in the prior year period), an ordinary loss of ¥325 million (compared to ¥173 million loss), and a net loss attributable to owners of parent of ¥249 million (compared to ¥149 million loss).

- Total assets stood at ¥6,580 million, with net assets at ¥4,672 million, and an equity ratio of 68.1%.

- Two new companies, Sora Consulting GmbH and Euro USC Netherlands, were added to the scope of consolidation during this quarter.

- The full-year consolidated performance forecast for FY2027 remains unchanged, projecting net sales of ¥5,073 million, operating loss of ¥1,658 million, ordinary loss of ¥1,419 million, and net loss attributable to owners of parent of ¥1,266 million.

🤖 AI Perspective

Terra Drone’s Q1 FY2027 results show revenue growth, yet a widened operating loss compared to the previous year. This could suggest ongoing strategic investments, such as the full-scale entry into the defense business, the establishment of “Terra Defense” in the U.S., and overseas expansion in UTM (Unmanned Aircraft System Traffic Management) solutions, which may incur upfront costs for future growth. The addition of two new consolidated entities may also influence future business performance and financial structure.

3823|WHY HOW DO

33.0

▲ +3.12%

📎 Source:WHY HOW DO Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- THE WHY HOW DO COMPANY Co. Ltd. announced its consolidated financial results for the fiscal year ended April 2026 (September 1, 2025 to April 30, 2026).

- The company changed its fiscal year end from August to April, resulting in an irregular 8-month reporting period for the current fiscal year.

- Consolidated results show net sales of JPY 2,332 million, operating loss of JPY 502 million, ordinary loss of JPY 870 million, and net loss attributable to parent company shareholders of JPY 902 million.

- Adjusted EBITDA achieved a positive JPY 27 million.

- The company pursued an M&A strategy, adding five new subsidiaries to its consolidated scope: Still Anne Co., Ltd., Goodman Co., Ltd., Iiyama Doken Co., Ltd., Cowell Co., Ltd., and Nihon Jun Kin Kou Co., Ltd.

- The company announced a policy of maintaining no dividend for the current fiscal year.

🤖 AI Perspective

WHY HOW DO’s fiscal year ending April 2026 is an irregular 8-month period due to a change in the fiscal year end, making direct comparisons with the previous period challenging. The report indicates an aggressive M&A strategy, expanding its business portfolio with five new consolidated subsidiaries. However, one-time expenses related to acquisition costs for new consolidated subsidiaries and allowances for doubtful accounts contributed to the operating loss, ordinary loss, and net loss for the period. Investors may wish to monitor how these one-time expenses will impact future earnings.

4441|トビラシステムズ

1347.0

▲ +6.57%

📎 Source:トビラシステムズ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tobila Systems disclosed a Q&A summary regarding its Q2 FY2026 financial results on June 15, 2026.

- Regarding the individual disclosure of TobilaPhone Biz Lite sales units, the company stated it is currently limited as a proportion of total sales and will be considered based on future sales trends.

- The gross profit margin for TobilaPhone Biz is higher than that of TobilaPhone Biz Lite.

- The company recognizes that the revised Labor Policy Comprehensive Promotion Act, mandating customer harassment measures from October 1, 2026, could lead to increased interest and demand for its services.

- A loan of 50 million yen recorded in the interim cash flow statement was for a company director to acquire company shares, with the aim of strengthening commitment to future business expansion.

🤖 AI Perspective