📌 Today’s Highlights

Today we cover 105 IR announcements. Notable among them: 東洋炭素 (5310), ips (4390), 芝浦機械 (6104). Use the table of contents below to navigate to each company.

- 5310|東洋炭素

- 4390|ips

- 6104|芝浦機械

- 5576|オービーシステム

- 5969|ロブテックス

- 6806|ヒロセ電

- 5947|リンナイ

- 1969|高砂熱

- 1994|高橋ウォール

- 3105|日清紡HD

- 4828|ビーエンジ

- 6460|セガサミーHD

- 6658|シライ電子

- 7012|川崎重

- 7326|G-SBIインシュ

- 7806|G-MTG

- 9744|メイテックGHD

- 9991|ジェコス

- 2602|日清オイリオ

- 7939|研創

- 9170|成友興業

- 9343|G-アイビス

- 9476|中央経済社HD

- 8393|宮崎銀

- 3058|三洋堂HD

- 3407|旭化成

- 3802|エコミック

- 6073|アサンテ

- 2433|博報堂DY

- 5201|AGC

- 5563|新日本電工

- 8349|東北銀

- 9259|G-タカヨシHD

- 7011|三菱重

- 8544|京葉銀

- 1820|西松建

- 1905|テノックス

- 2674|ハードオフ

- 3176|三洋貿易

- 4901|富士フイルム

- 5142|アキレス

- 6989|北電工業

- 7565|萬世電機

- 7743|シード

- 8424|芙蓉リース

- 9045|京阪HD

- 9171|栗林船

- 9438|エムティーアイ

- 9441|ベルパーク

- 4247|ポバール興業

- 5570|G-ジェノバ

- 2267|ヤクルト

- 1417|ミライト・ワン

- 1798|守谷商会

- 3461|パルマ

- 5533|エリッツHD

- 6282|オイレス工

- 6459|大和冷機

- 6546|フルテック

- 7013|IHI

- 8386|百十四銀

- 1333|Umios

- 1431|G-リブワーク

- 2120|LIFULL

- 2154|オープンアップG

- 2418|ツカダグローバルHD

- 2477|手間いらず

- 2483|翻訳センター

- 2533|オエノンHD

- 2607|不二製油

- 2676|高千穂交

- 3028|アルペン

- 3082|きちりHD

- 3154|メディアスHD

- 3360|シップHD

- 3494|マリオン

- 3671|ソフトMAX

- 3679|じげん

- 3837|アドソル日進

- 387A|G-フラー

- 3964|オークネット

- 4023|クレハ

- 3741|セック

- 6402|兼松エンジニア

- 7435|ナ・デックス

- 7927|ムトー精工

- 1717|明豊ファシリティ

- 1768|ソネック

- 1866|北野建

- 3179|シュッピン

- 3634|ソケッツ

- 3958|笹徳印刷

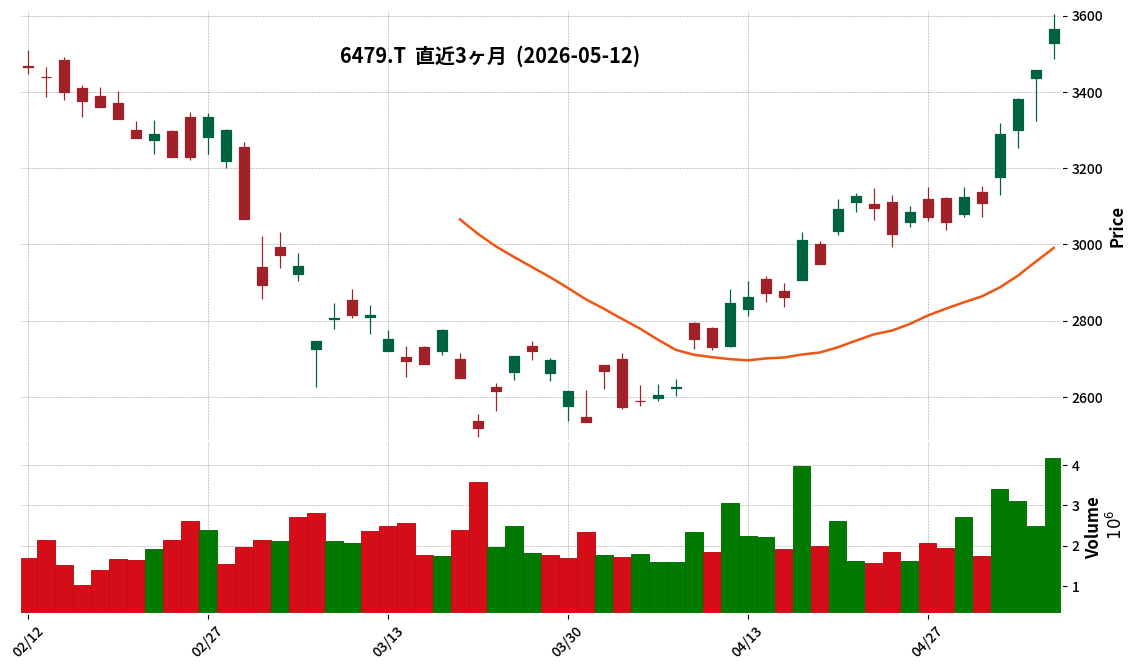

- 6479|ミネベアミツミ

- 519A|G-ベーシック

- 4554|富士製薬

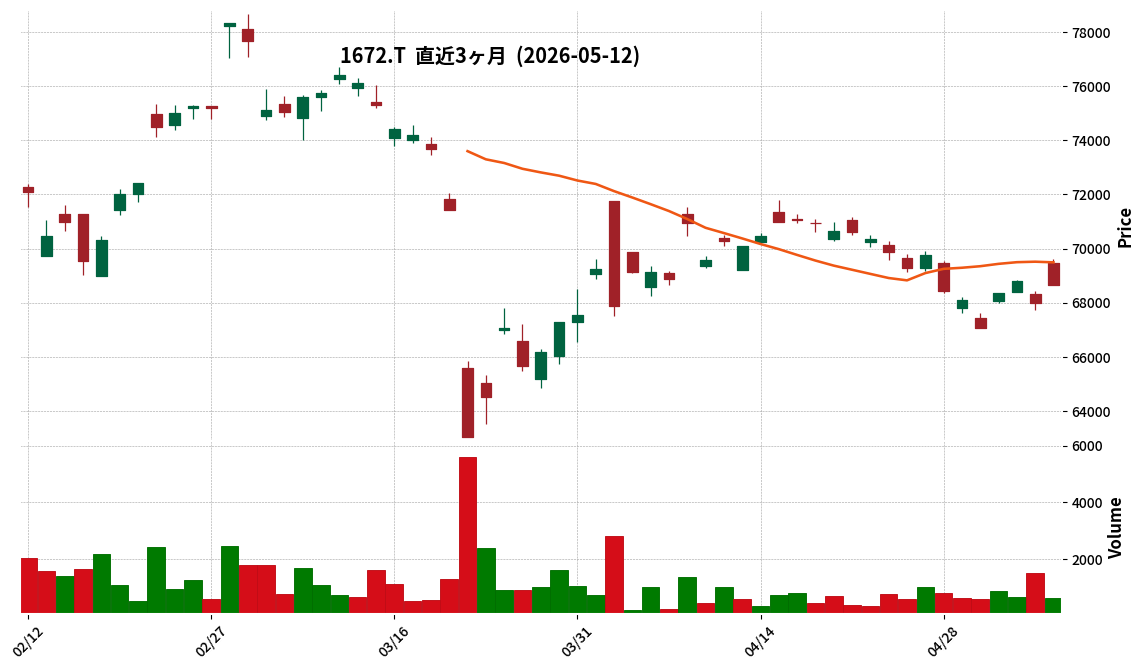

- 1672|金ETF

- 4056|G-ニューラル

- 6862|ミナトHD

- 6946|日アビオ

- 7080|G-スポーツフィール

- 9433|KDDI

- 6445|ジャノメ

- 9036|東部ネット

- 3948|光ビジネス

- 4819|デジタルガレージ

5310|東洋炭素

6770.0

▼ -1.02%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Toyo Tanso Co., Ltd. reported its Q1 FY2026 results, with net sales of ¥10,576 million (a 7.8% decrease year-on-year) and operating income of ¥634 million (a 70.3% decrease year-on-year).

- Net income attributable to owners of the parent for the quarter was ¥609 million (a 52.3% decrease year-on-year), with basic earnings per share at ¥29.05.

- The decline in operating income was primarily attributed to a decrease in marginal profit due to reduced sales in semiconductor applications, partly resulting from front-loaded demand in the previous fiscal year. However, positive impacts from foreign exchange, raw material price fluctuations, reduced fixed costs, and inventory-related factors were also noted.

- By product and application, sales in the electronics segment of Special Graphite Products decreased by 24.0% year-on-year to ¥1,544 million, and sales of the three main Composite Material & Other Products declined by 23.2% year-on-year to ¥2,464 million. These reductions were influenced by ongoing inventory adjustments for single crystal silicon and compound semiconductor wafers, alongside a significant decrease in SiC semiconductor applications.

- The full-year consolidated earnings forecast for FY226 remains unchanged, projecting net sales of ¥49,000 million, operating income of ¥6,200 million, and net income attributable to owners of the parent of ¥5,464 million. The company also announced an increase in its dividend payout ratio target to 40% as part of its shareholder return policy.

🤖 AI Perspective

The first quarter results, showing significant year-on-year declines in sales and profits, appear to be largely influenced by reduced sales in semiconductor-related fields and ongoing inventory adjustments. The performance of the electronics segment within Special Graphite Products and the key three Composite Material & Other Products may be crucial indicators for investors monitoring a market recovery. The company’s decision to maintain its full-year earnings forecast could suggest an expectation for market improvement in the latter half of the fiscal year or robust performance in other sectors, which is worth monitoring.

4390|ips

3995.0

▲ +14.14%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- IPS Inc. reported consolidated results for the fiscal year ended March 2026, with net sales of ¥16,999 million (up 11.4% year-on-year), operating profit of ¥5,370 million (up 21.7%), ordinary profit of ¥5,787 million (up 42.1%), and profit attributable to owners of parent of ¥4,196 million (up 64.9%).

- The company achieved 8 consecutive years of revenue and profit growth since listing, with operating cash flow reaching ¥4.59 billion.

- For the fiscal year ending March 2027, the company forecasts net sales of ¥20,080 million (up 18.1% year-on-year) and operating profit of ¥6,100 million (up 13.6%).

- In the international telecommunications business, IPS decided to participate in the new international subsea cable “Candle” and commenced construction of the Baler Landing Station.

- The domestic telecommunications business saw improved profitability due to the expiration of special factors from the previous fiscal year, such as retroactive adjustments for interconnection fees, while the Medical & Healthcare business achieved profitability in Q4 FY2026/3 due to increased human dock revenue.

🤖 AI Perspective

The financial results for the fiscal year ended March 2026 suggest that growth in the international telecommunications business, coupled with improved profitability in domestic telecommunications and medical & healthcare segments, contributed significantly to overall profit expansion. Continued investment in international telecommunications infrastructure, such as the Candle subsea cable, may indicate the company’s commitment to long-term growth and market position. Furthermore, the company’s assessment that macroeconomic risks in the Philippine economy have limited direct impact on its operations could be seen as a positive sign regarding business stability.

6104|芝浦機械

4595.0

▼ -2.34%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Shibaura Machine Co., Ltd. announced the postponement of its financial results announcement for the fiscal year ending March 2026.

- The announcement, originally scheduled for May 12, 2026, has been delayed.

- The reason provided for the postponement is the time required to finalize the financial figures.

- The new scheduled date for the financial results announcement is May 18, 2026.

- The company expressed a deep apology to its shareholders, investors, and other stakeholders for any inconvenience caused.

🤖 AI Perspective

Postponing financial results typically means investors will have to wait longer for crucial performance data, which can sometimes raise questions regarding the underlying reasons. While the company stated the delay is due to the time needed to finalize figures, it could suggest a need for extensive verification or complex adjustments. Investors may find it beneficial to monitor the upcoming announcement closely for any further details or explanations.

5576|オービーシステム

2782.0

▼ -0.29%

📎 Source:オービーシステム Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- OBS Company announced on May 12, 2026, a partial correction to its “Consolidated Financial Results for the Fiscal Year Ended March 2026 (Japanese GAAP)”.

- The reason for the correction is that some errors were found in the descriptions of the financial results report disclosed on April 22, 2026, during the detailed review process for finalizing the financial statements.

- For the consolidated financial results of March 2026, ordinary profit was corrected from 728 million yen to 727 million yen, profit attributable to owners of parent from 601 million yen to 599 million yen, and basic earnings per share from 259.43 yen to 258.81 yen.

- Regarding the dividend situation for the fiscal year ended March 2026, the consolidated dividend payout ratio was revised from 40.5% to 40.6%.

- In the consolidated performance forecast for the fiscal year ending March 2027, the year-on-year change rate for profit attributable to owners of parent was corrected from 19.8% to 20.1%, while the absolute amount remains unchanged at 720 million yen.

🤖 AI Perspective

The announced corrections entail minor adjustments to certain figures in the consolidated financial results for the fiscal year ended March 2026 and the forecast for the fiscal year ending March 2027. Notably, the absolute figures for the fiscal year 2027 consolidated performance forecast remain unchanged, with adjustments primarily affecting the decimal places of year-on-year growth rates. While these changes may not indicate a fundamental shift in the company’s financial position or business outlook, investors may find it beneficial to thoroughly review the disclosed corrected information to ensure informed decision-making.

5969|ロブテックス

1251.0

▲ +1.30%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Lobtex Co., Ltd. announced its consolidated financial results for the fiscal year ended March 31, 2026.

- Consolidated net sales for FY2026/3 were ¥5,711 million, marking a slight increase of 0.1% compared to the previous fiscal year.

- Profit attributable to owners of parent surged by 58.9% year-on-year to ¥122 million, primarily due to the absence of the partial reversal of deferred tax assets recorded in the prior year.

- Conversely, operating income decreased by 11.5% to ¥182 million, and ordinary income fell by 14.1% to ¥191 million.

- The consolidated earnings forecast for FY2027/3 projects net sales of ¥5,730 million (up 0.3% YoY) and profit attributable to owners of parent of ¥120 million (down 2.3% YoY).

- The annual dividend for FY2026/3 was ¥30.00 per share (year-end), with the same ¥30.00 per share (year-end) forecast for FY2027/3.

🤖 AI Perspective

- The significant increase in profit attributable to owners of parent for FY2026/3, despite nearly flat net sales, appears primarily driven by the resolution of a specific prior-year factor related to deferred tax assets.

- Investors may wish to scrutinize the divergence between the decreased operating and ordinary income and the increased net profit, suggesting a careful evaluation of underlying business profitability versus tax effects is warranted.

- The forecast for FY2027/3 indicates a slight increase in sales but a projected decline in operating, ordinary, and net profits, making future strategies for profit improvement and market condition impacts key areas for ongoing observation.

6806|ヒロセ電

23150.0

▲ +3.21%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 2026, consolidated net sales reached ¥211.26 billion (up 11.5% year-on-year), and operating profit was ¥42.99 billion (up 0.8% year-on-year).

- Orders received totaled ¥224.98 billion, marking a 16.8% increase compared to the previous fiscal year.

- The operating profit margin stood at 20.4%, a decrease of 2.1 percentage points from 22.5% in the prior fiscal year.

- By sector sales (connectors), the general industrial machinery market achieved ¥62.0 billion, a significant increase of 32% year-on-year, surpassing its annual forecast.

- Key factors influencing operating profit included a positive impact of ¥42.7 billion from increased sales volume, while increased material/procurement costs of ¥6.5 billion and personnel costs of ¥3.8 billion were negative factors.

🤖 AI Perspective

The reported financial results show net sales and operating profit exceeding initial forecasts. However, the operating profit growth was modest relative to the increase in net sales, which may suggest the impact of rising material and personnel costs. The strong performance in the general industrial machinery market appears to have been a key driver for the overall results.

5947|リンナイ

3653.0

▲ +2.07%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Rinnai reported consolidated results for the fiscal year ended March 31, 2026, with net sales of ¥470.39 billion (+2.2% year-on-year), operating income of ¥50.53 billion (+9.8%), ordinary income of ¥57.69 billion (+14.6%), and net income attributable to owners of parent of ¥36.16 billion (+21.8%). Both net sales and operating income reached record highs.

- The annual dividend for the fiscal year ended March 31, 2026, was ¥100.00, an increase from ¥80.00 in the previous fiscal year, with the year-end dividend set at ¥50.00.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥500.00 billion (+6.3% year-on-year), but projects operating income of ¥50.50 billion (-0.1%), and ordinary income of ¥54.10 billion (-6.2%). Net income attributable to owners of parent is expected to be ¥36.30 billion (+0.4%).

- The forecasted annual dividend for the fiscal year ending March 31, 2027, is ¥106.00, an increase of ¥6.00 from the prior year.

- The fiscal year ended March 31, 2026, was the final year of the medium-term management plan “New ERA 2025,” and the company achieved both revenue and profit targets set in the plan.

🤖 AI Perspective

Rinnai’s achievement of record-high net sales and operating income in FY2026/3, along with the successful completion of its medium-term management plan targets, stands out. The increased dividend payout may suggest a commitment to shareholder returns. However, the FY2027/3 outlook, while projecting revenue growth, also anticipates a slight decline in operating and ordinary income, which could be a point of interest for investors.

1969|高砂熱

4967.0

▲ +6.27%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Takasago Thermal Engineering reported consolidated results for the fiscal year ended March 31, 2026, with sales of JPY 423,923 million (up 11.1% year-on-year), operating profit of JPY 47,745 million (up 47.3% year-on-year), ordinary profit of JPY 50,642 million (up 44.8% year-on-year), and net profit attributable to parent company shareholders of JPY 37,470 million (up 35.6% year-on-year).

- Diluted earnings per share for FY2026 was JPY 285.73, calculated assuming a 2-for-1 stock split effective October 1, 2025.

- The year-end dividend for FY2026 was JPY 72.00 per share (post-split), with a total annual dividend payout of JPY 15,336 million and a consolidated dividend payout ratio of 40.2%. The total annual dividend before the stock split was JPY 230.00 per share.

- The consolidated financial position as of March 31, 2026, showed total assets of JPY 381,823 million, net assets of JPY 215,056 million, and an equity ratio of 55.0%.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated sales of JPY 440,000 million (up 3.8% year-on-year), operating profit of JPY 50,000 million (up 4.7% year-on-year), and net profit attributable to parent company shareholders of JPY 40,000 million (up 6.7% year-on-year). The projected order intake is JPY 520,000 million.

- A 2-for-1 stock split of common shares was implemented on October 1, 2025. Additionally, two new companies, THS INNOVATIONS CO., LTD. and PROMPT TECHNO SERVICE CO., LTD., were included in the scope of consolidation during the period.

🤖 AI Perspective

The substantial year-on-year increases across all key profitability metrics for FY2026, particularly the significant surge in operating profit, may indicate strong operational performance and effective management in a favorable business environment. The strengthening of the financial position, evidenced by growth in total and net assets, an improved equity ratio, and a robust increase in cash flow from operating activities, suggests healthy internal cash generation and a solid balance sheet. The positive outlook for FY2027, forecasting continued increases in sales and profits, implies management’s confidence in sustained business momentum, making the execution against these projections a key aspect for investors to monitor.

1994|高橋ウォール

569.0

▲ +0.71%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of fiscal year 2026 (January 1, 2026, to March 31, 2026), Takahashi Curtain Wall Industry reported consolidated net sales of JPY 2,026 million (up 10.2% year-on-year), operating profit of JPY 340 million (compared to an operating loss of JPY 57 million in the prior year), ordinary profit of JPY 358 million (compared to an ordinary loss of JPY 40 million), and profit attributable to owners of parent of JPY 231 million (compared to a loss of JPY 64 million).

- The PC Curtain Wall business segment achieved sales of JPY 1,788 million (up 17.2% year-on-year) and segment profit of JPY 325 million, turning profitable from a JPY 91 million loss in the same period of the previous year.

- As of the end of the first quarter, consolidated total assets stood at JPY 12,570 million, net assets at JPY 10,960 million, and the equity ratio at 87.2%.

- The consolidated full-year forecast for fiscal year 2026 has been revised, projecting net sales of JPY 8,250 million (up 12.4% from the previous fiscal year), operating profit of JPY 450 million (up 299.3%), ordinary profit of JPY 530 million (up 183.9%), and profit attributable to owners of parent of JPY 347 million (up 82.1%).

- The forecast for annual dividends for FY2026 remains unchanged from the most recently announced forecast, with an interim dividend of JPY 10.00 and a year-end dividend of JPY 10.00, totaling JPY 20.00 per share.

🤖 AI Perspective

Takahashi Curtain Wall Industry’s Q1 FY2026 results show a notable increase in sales and a significant return to profitability, primarily driven by its PC Curtain Wall business. The upward revision of the full-year earnings forecast could indicate management’s increased confidence in the company’s future performance. This strong first quarter, especially compared to a loss in the previous year’s corresponding period, suggests a positive operational turnaround and momentum.

3105|日清紡HD

2083.0

▲ +0.85%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nisshinbo Holdings Inc. announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026 – March 31, 2026).

- Consolidated net sales amounted to ¥147,692 million (down 2.3% year-on-year), operating profit was ¥20,316 million (down 4.6%), ordinary profit was ¥20,672 million (down 3.6%), and net profit attributable to parent company shareholders was ¥12,991 million (down 15.1%).

- The Radio & Communication segment achieved substantial growth, with net sales of ¥89,860 million (up 10.8% year-on-year) and segment profit of ¥19,088 million (up 53.8%).

- The consolidated full-year forecast for FY2026 remains unchanged, projecting net sales of ¥511,000 million (up 1.7% from the previous fiscal year) and net profit attributable to parent company shareholders of ¥10,000 million (down 28.2%).

- The estimated annual dividend for FY2026 is ¥36.00 per share (¥18.00 interim, ¥18.00 year-end), with no revisions from the most recently announced forecast.

🤖 AI Perspective

Nisshinbo Holdings’ Q1 FY2026 results showed a decline in consolidated sales and profits compared to the previous year. However, the Radio & Communication segment demonstrated significant growth, driven by robust demand in disaster prevention, defense, and the new shipbuilding market, highlighting its key role in the company’s portfolio. While the overall results were impacted by a decrease in the real estate business following large-scale spot sales in the prior year, the unchanged full-year forecasts suggest the company anticipates stabilization or recovery in other segments. Investors may want to monitor the performance of each business segment to assess the company’s trajectory towards its annual targets.

4828|ビーエンジ

1255.0

▲ +1.21%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the consolidated fiscal year ended March 31, 2026, Beenos (4828) reported net sales of 24,442 million yen (up 17.6% year-on-year), operating profit of 6,411 million yen (up 37.1%), ordinary profit of 6,435 million yen (up 37.5%), and profit attributable to owners of parent of 4,890 million yen (up 46.8%).

- Diluted earnings per share for the period was 81.78 yen.

- The year-end dividend for the fiscal year ended March 31, 2026, was 26.00 yen per share after accounting for the stock split. While the total annual dividend is stated as “-”, it translates to 208 yen per share before the stock split, with a consolidated dividend payout ratio of 50.9%.

- The company implemented a stock split at a ratio of five shares for every one common share, effective January 1, 2026.

- For the consolidated fiscal year ending March 31, 2027, the company forecasts net sales of 26,800 million yen (up 9.6% year-on-year), operating profit of 6,900 million yen (up 7.6%), ordinary profit of 6,900 million yen (up 7.2%), and profit attributable to owners of parent of 4,600 million yen (down 5.9%), with diluted earnings per share of 77.05 yen.

🤖 AI Perspective

- Beenos’s fiscal year ended March 2026 demonstrated robust performance with double-digit growth across all key revenue and profit indicators, particularly a significant increase of over 40% in profit attributable to owners of parent, suggesting strong operational results.

- However, the consolidated earnings forecast for the fiscal year ending March 2027, while projecting continued growth in net sales, operating profit, and ordinary profit, anticipates a modest decline in profit attributable to owners of parent compared to the previous year, which may attract investor attention.

- The maintenance of a high dividend payout ratio coupled with a stock split could indicate the company’s commitment to shareholder returns, a factor that might be considered by investors.

6460|セガサミーHD

2282.0

▼ -1.19%

📎 Source:セガサミーHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, consolidated net sales were ¥487,542 million, an increase of 13.7% year-on-year.

- Consolidated operating profit for the period was ¥47,128 million (down 2.1% year-on-year), and net loss attributable to owners of parent was ¥5,756 million.

- The annual dividend per share is projected to be ¥55 (interim ¥27, year-end ¥28).

- Impairment losses on goodwill and other intangible assets of Rovio Entertainment Ltd, and goodwill and tangible fixed assets of Stakelogic B.V., were recorded as extraordinary losses.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥510,000 million (up 4.6% year-on-year) and net income attributable to owners of parent of ¥32,500 million.

🤖 AI Perspective

While consolidated net sales showed growth, the recording of impairment losses notably impacted the final profit/loss, resulting in a net loss. However, the announced increase in annual dividends and the forecast for a return to profitability in FY2027/3 may suggest management’s confidence in future recovery.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

6658|シライ電子

702.0

▼ -0.43%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Shiraidenshi Corporation announced its consolidated financial results for the fiscal year ended March 31, 2026. Net sales were JPY 29.118 billion (down 0.7% year-on-year), operating profit was JPY 2.030 billion (down 21.2%), ordinary profit was JPY 1.822 billion (down 29.7%), and net income attributable to owners of the parent was JPY 1.309 billion (down 36.9%), resulting in a decrease in both revenue and profit.

- The Printed Wiring Board business, the core segment, recorded net sales of JPY 28.549 billion (down 0.5% year-on-year) and segment profit of JPY 2.038 billion (down 21.4%). While the recovery in car electronics was delayed and raw material and energy costs surged, orders for home appliances performed favorably.

- As of the end of the fiscal year March 2026, consolidated total net assets increased by JPY 1.054 billion from the previous year-end to JPY 11.109 billion, leading to an improvement in the equity ratio from 51.0% to 57.1%.

- The year-end dividend for the fiscal year ended March 2026 was JPY 35 per share, making the annual dividend JPY 35 (compared to JPY 30 in the previous fiscal year).

- For the fiscal year ending March 2027, the consolidated earnings forecast projects net sales of JPY 29.000 billion (down 0.4% year-on-year), operating profit of JPY 850 million (down 58.1%), ordinary profit of JPY 800 million (down 56.1%), and net income attributable to owners of the parent of JPY 600 million (down 54.2%), indicating a significant decline in profit. The forecasted annual dividend is JPY 20 per share.

🤖 AI Perspective

The financial results for the fiscal year ended March 2026 show a slight decrease in net sales but a double-digit decline in various profit figures. This appears to be largely influenced by the surging costs of raw materials and energy within the Printed Wiring Board business. Conversely, the increase in net assets and the improved equity ratio may suggest a strengthening of the company’s financial foundation. The forecast for the fiscal year ending March 2027 indicates a substantial drop in both profit and dividends, making it worth monitoring the future business environment and the effectiveness of their profit improvement measures.

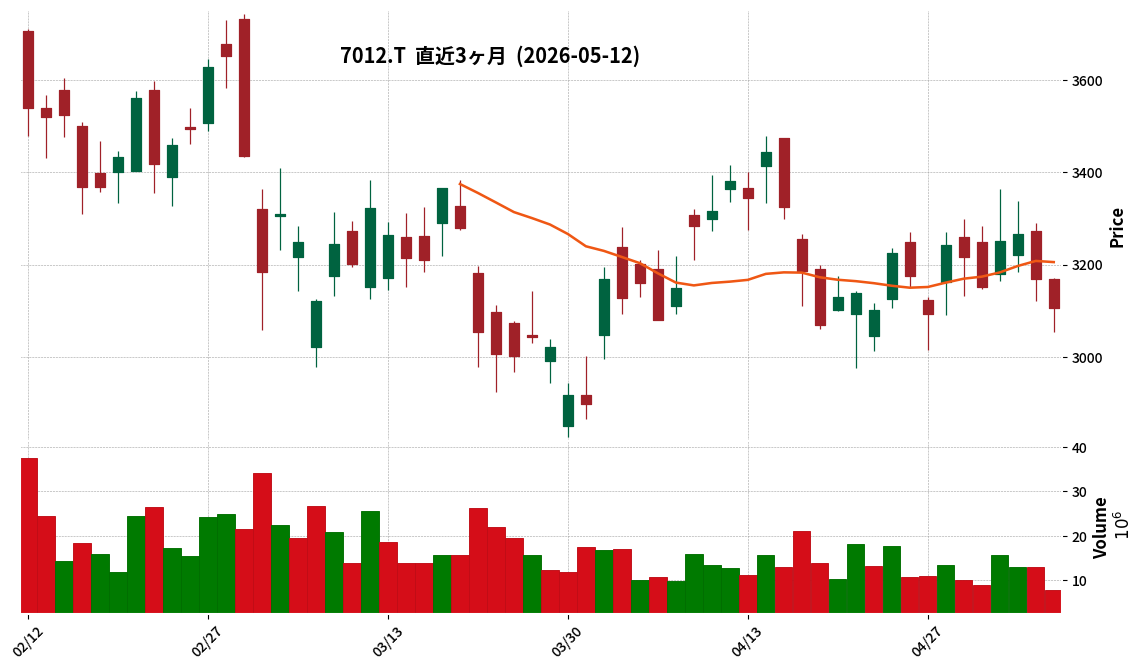

7012|川崎重

3106.0

▼ -2.02%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- On May 12, 2026, Kawasaki Heavy Industries resolved at its Board of Directors meeting to increase the year-end dividend for shareholders of record as of March 31, 2026.

- The year-end dividend per share for the fiscal year ending March 2026 is set at JPY 96.00, an increase of JPY 5.00 from the previous forecast of JPY 91.00 announced on February 9, 2026.

- This revision brings the annual dividend per share for the fiscal year ending March 2026 to JPY 171.00, an increase of JPY 5.00 from the previous forecast of JPY 166.00.

- The total dividend amount is JPY 16,115 million, with an effective date of June 26, 2026, pending approval at the 203rd Ordinary General Meeting of Shareholders on June 25, 2026.

- The company stated the increase is in line with its shareholder return policy, which targets a Dividend on Equity (DOE) of 4% to balance long-term shareholder value enhancement and stable dividends, considering the company’s performance for the current fiscal year.

🤖 AI Perspective

Kawasaki Heavy Industries’ decision to raise its dividend, exceeding its previous forecast, may suggest a positive outlook on its financial performance and a commitment to shareholder returns. The adherence to a 4% DOE target as part of its shareholder return policy could be viewed as a signal of management’s confidence in the company’s earnings trajectory. Investors might find the stability offered by such a policy worth monitoring.

7326|G-SBIインシュ

2059.0

▲ +0.93%

📎 Source:G-SBIインシュ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the consolidated fiscal year ended March 31, 2026, G-SBI Insurance Group reported ordinary revenue of JPY 140,362 million (up 18.5% year-on-year), ordinary income of JPY 13,164 million (up 39.0%), and net profit attributable to parent company shareholders of JPY 2,880 million (up 44.8%).

- These figures for ordinary revenue, ordinary income, and net profit attributable to parent company shareholders all represent new record highs for the company.

- The annual dividend for FY2026 was JPY 46.50 per share, an increase from JPY 23.00 in the previous fiscal year.

- The consolidated earnings forecast for FY2027 projects ordinary revenue of JPY 150,000 million (up 6.9% year-on-year), ordinary income of JPY 16,000 million (up 21.5%), and net profit attributable to parent company shareholders of JPY 3,620 million (up 25.7%).

- The company expects an annual dividend of JPY 59.00 per share for FY2027.

🤖 AI Perspective

The strong performance in FY2026, marked by record-high profits, appears to be driven by robust growth in contract numbers across all business segments and ongoing operational efficiency improvements. The substantial increase in the annual dividend, alongside a positive outlook for FY2027 with projected profit growth and further dividend increases, may suggest a strong commitment to shareholder returns and confidence in future business expansion.

7806|G-MTG

6770.0

▲ +3.83%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-MTG announced on May 12, 2026, an upward revision to its full-year consolidated earnings forecast and dividend forecast for the fiscal year ending September 2026 (October 1, 2025 – September 30, 2026).

- Consolidated net sales are revised from the previous forecast of JPY 128,000 million to JPY 135,000 million, and operating profit from JPY 14,000 million to JPY 15,000 million.

- Net profit attributable to owners of parent increased from JPY 9,500 million to JPY 10,000 million.

- Earnings per share are revised from JPY 241.82 to JPY 254.30.

- The year-end dividend forecast has been raised from JPY 30.00 to JPY 33.00 per share, resulting in a total annual dividend of JPY 33.00.

- The revision is attributed to strong sales performance across ReFa, SIXPAD, and ReD brands, coupled with increased gross profit due to higher sales and enhanced brand power.

🤖 AI Perspective

This revision may suggest that the company’s key brands continue to perform strongly in the market, contributing positively to overall corporate profitability. The increase in the dividend forecast, following the upward revision of earnings, could indicate a consistent approach to shareholder returns. As the fiscal year ending September 2026 is still in progress, the upward adjustment of multiple financial metrics might be a point of interest for market participants.

9744|メイテックGHD

2965.0

▼ -2.40%

📎 Source:メイテックGHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Meitec Group Holdings Inc. reported consolidated results for the fiscal year ended March 31, 2026, with net sales of ¥137,686 million (up 3.5% year-on-year), operating profit of ¥19,903 million (up 5.7%), ordinary profit of ¥20,101 million (up 6.3%), and net profit attributable to owners of parent of ¥15,051 million (up 18.1%).

- The annual dividend for the fiscal year ended March 31, 2026, was ¥196 per share (interim ¥90, year-end ¥106).

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥140,800 million (up 2.3% from previous year) and operating profit of ¥20,500 million (up 3.0%), while net profit attributable to owners of parent is projected to be ¥13,900 million (down 7.7%).

- The forecasted annual dividend for the fiscal year ending March 31, 2027, is ¥181 per share (interim ¥85, year-end ¥96).

- As of May 12, 2026, it is noted that audit procedures are ongoing in relation to the disclosure made on May 11, 2026, regarding “Interim Dividends Exceeding Distributable Amount for the Previous Fiscal Year.”

🤖 AI Perspective

The increase in consolidated sales and profits for the fiscal year ended March 2026 appears to be driven by solid order intake and utilization rates in the core Engineering Solution business, coupled with a special gain from the sale of a large training facility. For the upcoming fiscal year ending March 2027, while an increase in sales and operating profit is projected, the forecast for a decrease in net profit attributable to owners of parent and a lower annual dividend plan compared to the prior year may be a key point of interest for investors. Furthermore, the ongoing audit procedures, as noted in the disclosure, could also be a factor for investor consideration.

9991|ジェコス

1626.0

▼ -1.87%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- GECOSS Corporation reported record-high consolidated operating profit of ¥8,012 million (+16.9% year-over-year) and net profit attributable to parent company shareholders of ¥5,853 million (+28.8% year-over-year) for the fiscal year ended March 31, 2026.

- Consolidated net sales for FY2026 totaled ¥115,680 million (+3.7% year-over-year), primarily driven by steady progress in temporary construction projects.

- Return on Equity (ROE) reached a record 8.5%, an increase of 1.5 percentage points from the prior fiscal year.

- For the fiscal year ending March 31, 2027, the company forecasts an operating profit of ¥8,400 million (+4.8% year-over-year). However, net profit attributable to parent company shareholders is projected to decrease to ¥5,700 million (-2.6% year-over-year), due to a reduction in one-time special gains from the sale of policy-held shares, among other factors.

- The company expects to maintain an ROE of approximately 8.0% for FY2027, despite a temporary decline due to an increase in net assets.

🤖 AI Perspective

The strong performance in FY2026, marked by record profits, appears to be a result of steady progress in construction projects and continuous efforts to improve profitability. While the forecast for FY2027 indicates a slight decline in net profit due to the absence of one-time factors, the projected increase in operating profit may suggest ongoing operational strength in its core businesses. The business environment is influenced by factors such as the “National Resilience Plan” and robust demand from large-scale urban redevelopment projects in the Tokyo metropolitan area, which could continue to support the company’s activities.

2602|日清オイリオ

1797.0

▲ +0.50%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nisshin OilliO Group announced its consolidated financial results for the fiscal year ended March 31, 2026, with net sales of ¥554,251 million, representing a 4.4% increase year-on-year.

- Operating profit was ¥17,027 million (down 11.7% year-on-year), and ordinary profit was ¥16,030 million (down 11.4% year-on-year).

- Profit attributable to owners of parent significantly increased by 86.7% year-on-year to ¥23,988 million.

- The company conducted a 1-for-3 stock split of its common shares effective April 1, 2026.

- For the fiscal year ending March 31, 2027, the consolidated forecast projects net sales of ¥590,000 million (up 6.4% year-on-year), operating profit of ¥19,000 million (up 11.6% year-on-year), and ordinary profit of ¥18,000 million (up 12.3% year-on-year). However, profit attributable to owners of parent is forecast to decrease by 50.0% to ¥12,000 million.

🤖 AI Perspective

- For FY2026/3, while net sales increased, a notable point is the decrease in operating and ordinary profits alongside a significant rise in profit attributable to owners of parent. This divergence could be influenced by factors such as a turnaround in equity method investment gains/losses and a substantial increase in comprehensive income.

- The 1-for-3 stock split effective April 1, 2026, may aim to reduce the per-share investment unit, potentially making the shares more accessible to a broader range of investors.

- The FY2027/3 forecast indicates revenue and profit growth at the operating and ordinary levels, but a projected decline in net profit attributable to owners of parent suggests potential impacts from non-operating or extraordinary items, or tax expenses, that investors may wish to monitor.

7939|研創

570.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kensoh Co., Ltd. announced its non-consolidated financial results for the fiscal year ended March 2026. Sales reached ¥6,411 million, representing a 9.3% increase year-over-year.

- Operating profit was ¥257 million (down 2.4% YoY), and ordinary profit was ¥248 million (down 3.3% YoY). However, net income for the period increased by 18.2% to ¥206 million.

- The year-end dividend for FY2026 was set at ¥22 (total annual dividend of ¥22), and the company forecasts an annual dividend of ¥23 for FY2027.

- For the fiscal year ending March 2027, the company projects sales of ¥6,555 million (up 2.2% YoY), operating profit of ¥333 million (up 29.3% YoY), ordinary profit of ¥329 million (up 32.7% YoY), and net income of ¥222 million (up 7.6% YoY).

- The equity ratio as of the end of March 2026 improved to 60.8% from 58.8% at the end of the previous fiscal year.

🤖 AI Perspective

While Kensoh achieved revenue growth in FY2026, operating and ordinary profits saw slight declines. This could be attributed to factors such as rising material costs and labor shortages in the construction industry, as noted in the attached materials. However, net income increased year-over-year, and the equity ratio improved, suggesting enhanced financial stability. For FY2027, the company anticipates growth in sales and all profit metrics, along with an increased dividend forecast, as it enters the final year of its medium-term management plan.

9170|成友興業

—

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the second quarter (interim period) of the fiscal year ending September 2026, consolidated results show revenue of ¥9.086 billion (+15.4% year-on-year), operating profit of ¥857 million (+30.3% year-on-year), ordinary profit of ¥804 million (+32.8% year-on-year), and net profit attributable to owners of parent of ¥420 million (+27.6% year-on-year).

- Interim earnings per share stood at ¥149.11.

- By segment, the Environmental Business reported revenue of ¥4.861 billion (+19.8%) and segment profit of ¥993 million (+40.3%). The Environmental Engineering Business also saw significant growth with revenue of ¥519 million (+155.7%) and segment profit of ¥42 million (+144.6%).

- The Construction Business recorded a 2.4% year-on-year decrease in segment profit, partly due to the delay in the start of large-scale projects until the third quarter or later.

- The consolidated full-year earnings forecast for the fiscal year ending September 2026 remains unchanged from the figures announced on November 7, 2025.

🤖 AI Perspective

The overall increase in revenue and profit appears to be driven by M&A activities and reforms in existing businesses. The strong performance of the Environmental and Environmental Engineering segments can be seen as a significant contributor to these results. While project delays in the Construction segment impacted short-term profit, their progress in the latter half of the fiscal year will be worth monitoring. The unchanged full-year forecast may suggest that the company anticipates making up for any delays and achieving its targets in the second half.

9343|G-アイビス

724.0

▲ +1.97%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of fiscal year 2026 (January 1, 2026 – March 31, 2026), G-ibis reported consolidated net sales of JPY 1,460 million (up 25.7% year-on-year), operating income of JPY 373 million (up 22.1%), ordinary income of JPY 383 million (up 25.9%), and net income attributable to owners of parent of JPY 278 million (up 33.7%).

- The flagship mobile paint app “ibisPaint” reached 537.91 million cumulative downloads as of March 31, 2026 (up 14.9% year-on-year), with 40 million monthly active users (MAU).

- A major update, Ver.14.0.0, for “ibisPaint” was released on March 31, 2026, introducing new features such as CMYK output and brush categories.

- Zeroichistart Co., Ltd., which became a wholly-owned subsidiary in November 2025, began to be consolidated into the statement of income from this first consolidated quarter.

- The consolidated full-year earnings forecast for fiscal year 2026 and the annual dividend forecast (JPY 12.00 at fiscal year-end) remain unchanged from the most recently announced figures.

🤖 AI Perspective

G-ibis’s Q1 FY2026 results indicate robust growth, with net sales and all profit categories increasing by over 20% year-on-year. This performance may be attributed to the continued expansion of the global user base and feature enhancements of its flagship mobile app “ibisPaint,” alongside the contribution from a subsidiary whose profit and loss began to be consolidated this quarter. With the full-year earnings forecast remaining unchanged, further developments will be worth monitoring.

9476|中央経済社HD

999.0

▲ +0.10%

📎 Source:中央経済社HD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Chuo Keizai-Sha Holdings Co., Ltd. has announced its consolidated financial results for the second quarter (interim period) of the fiscal year ending September 2026.

- For the period from October 1, 2025, to March 31, 2026, consolidated net sales were ¥1,666 million, a 1.8% decrease compared to the previous interim period.

- Net profit attributable to owners of parent increased by 54.7% year-on-year to ¥201 million for the interim period.

- Operating profit reached ¥148 million (up 8.1% year-on-year), and ordinary profit was ¥159 million (up 9.0% year-on-year).

- The full-year consolidated performance forecast for the fiscal year ending September 2026 remains unchanged, projecting net sales at ¥3,096 million and net profit attributable to owners of parent at ¥126 million.

🤖 AI Perspective

Despite a slight decrease in net sales, the company reported increases in operating profit, ordinary profit, and a significant rise in net profit attributable to owners of parent, suggesting an improvement in profitability. The substantial increase in interim net profit appears to be influenced by non-operating factors such as gains on sales of investment securities. Investors may want to monitor the full-year forecast, as the interim net profit has already surpassed the full-year projection.

8393|宮崎銀

2027.0

▲ +1.86%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Miyazaki Bank announced its dividend forecast for the fiscal year ending March 2027 (April 1, 2026, to March 31, 2027).

- The projected annual dividend for the fiscal year ending March 2027 is 56.00 yen per share.

- This forecast represents an increase of 16 yen (40%) compared to the previous fiscal year’s (FY2026) actual annual dividend of 40.00 yen per share.

- The dividend forecast is based on the shareholder return policy announced on April 24, 2026.

- The previous fiscal year’s actual dividend amount has been converted based on the 1-for-5 stock split of common shares effective April 1, 2026.

🤖 AI Perspective

This dividend forecast aligns with Miyazaki Bank’s shareholder return policy, announced on April 24, 2026, which targets a dividend payout ratio of approximately 40% by the final year of its medium-term management plan (FY2029). Such a concrete step toward increasing per-share dividends may be seen by investors as a reaffirmation of the bank’s commitment to shareholder returns.

3058|三洋堂HD

700.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sanyodo Holdings Co., Ltd. announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025, to March 31, 2026).

- For the consolidated results, net sales were ¥17,249 million (up 3.9% year-on-year), operating income was ¥268 million (up 117.2%), ordinary income was ¥279 million (up 65.8%), and profit attributable to owners of parent was ¥340 million (up 91.4%).

- Segment sales showed significant increases in the Trading Card segment (up 26.6%), Surugaya segment (up 80.7%), and Stationery, Miscellaneous Goods, and Food segment (up 15.4%). Conversely, the Bookstore segment decreased by 5.7% and the Rental segment by 11.0%.

- As of March 31, 2026, the company operated 67 stores and 2 schools, with 32 stores implementing smart unmanned operations.

- The consolidated earnings forecast for the fiscal year ending March 31, 2027 (April 1, 2026, to March 31, 2027), projects net sales of ¥17,500 million (up 1.5% year-on-year), operating income of ¥200 million (down 25.5%), ordinary income of ¥200 million (down 28.5%), and profit attributable to owners of parent of ¥150 million (down 55.9%).

🤖 AI Perspective

The strong profit growth in fiscal year 2026/3, particularly in segments like Trading Cards and Surugaya, may suggest a successful adaptation to evolving market demands. However, the projected decline in profits for fiscal year 2027/3, despite an anticipated increase in sales, could indicate potential challenges such as increased operational costs or strategic investments. Investors might consider monitoring the company’s initiatives for profit margin improvement and competitive positioning.

3407|旭化成

1552.0

▲ +1.27%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Asahi Kasei has decided to set the year-end dividend for the fiscal year ending March 2026 at ¥22 per share. This represents an increase from the most recent dividend forecast (¥20) and the previous fiscal year’s performance (¥20).

- Consequently, the total annual dividend per share for the fiscal year ending March 2026 will be ¥42, including the interim dividend of ¥20.

- The forecast for the annual dividend per share for the fiscal year ending March 2027 is ¥44 (¥22 for interim, ¥22 for year-end).

- The company’s “Mid-Term Management Plan 2027 ~Trailblaze Together~” outlines a policy to pursue progressive dividends over the medium to long term, with a target DOE of 3%, aiming for continuous improvement in shareholder returns.

- The source of the dividend is retained earnings.

🤖 AI Perspective

Asahi Kasei’s latest dividend announcement appears to reflect its commitment to shareholder returns, aligning with the progressive dividend policy outlined in its Mid-Term Management Plan. The forecast of increased dividends for both FY2026 and FY2027 suggests a continued focus on stable shareholder returns. This move, based on financial performance, indicates that the progress of its future management strategies will be worth monitoring.

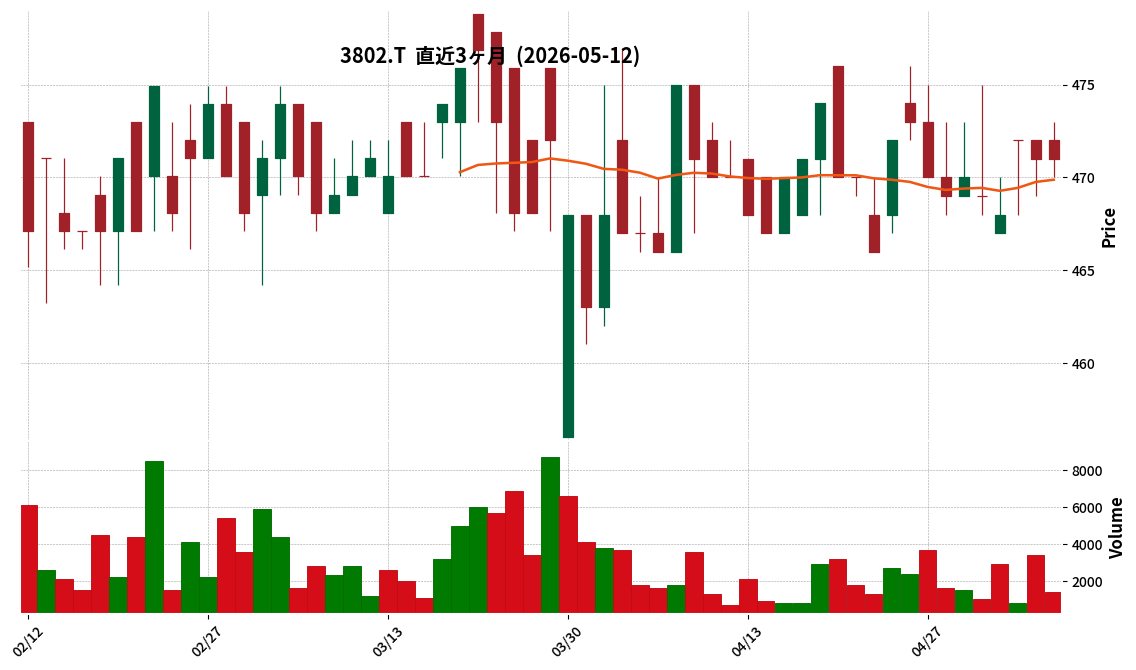

3802|エコミック

471.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Ecomic Co., Ltd. reported consolidated results for the fiscal year ended March 2026, with net sales of ¥2,345 million (up 10.6% year-on-year), operating profit of ¥173 million (up 271.0% year-on-year), ordinary profit of ¥159 million (up 158.3% year-on-year), and net profit attributable to owners of parent of ¥109 million (up 152.8% year-on-year).

- The increase in net sales was primarily due to a rise in processing volume and average unit price for year-end adjustment BPaaS services, an increase in the average unit price for payroll calculation BPaaS services, and the consolidation of its Shanghai-based subsidiary (Eiko Mirai Joho Gijutsu (Shanghai) Co., Ltd.).

- The gross profit margin improved by 4.7 percentage points, from 27.8% in the previous fiscal year to 32.5%.

- For the fiscal year ending March 2027, the company forecasts consolidated net sales of ¥2,400 million (up 2.3% year-on-year), operating profit of ¥180 million (up 3.7% year-on-year), and net profit attributable to owners of parent of ¥141 million (up 29.1% year-on-year).

- The number of treasury shares at the end of March 2026 significantly increased to 1,263,060 shares, compared to 60 shares at the end of the previous fiscal year.

🤖 AI Perspective

These results indicate that Ecomic achieved significant profit growth in addition to solid sales expansion, suggesting an improvement in the profitability of its BPaaS business. The improved gross profit margin may suggest that the company’s continuous efforts in operational efficiency have been successful. Furthermore, the substantial increase in treasury shares could be noteworthy as part of its capital policy.

6073|アサンテ

1494.0

▲ +2.26%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Asante Co., Ltd. announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- Sales increased by 2.4% year-over-year to JPY 14,355 million. However, operating profit decreased by 31.9% to JPY 835 million, ordinary profit fell by 27.9% to JPY 837 million, and profit attributable to owners of parent declined by 60.1% to JPY 274 million.

- The net profit included an impairment loss of JPY 284 million recognized as an extraordinary loss, related to the cessation of operations at the Inawashiro General Training Center.

- The annual dividend per share was maintained at JPY 62, consistent with the previous fiscal year.

- For the fiscal year ending March 31, 2027 (April 1, 2026 – March 31, 2027), the company forecasts consolidated sales of JPY 13,660 million (down 4.8% YoY), operating profit of JPY 200 million (down 76.1% YoY), and profit attributable to owners of parent of JPY 35 million (down 87.2% YoY), indicating a significant decrease in profitability.

🤖 AI Perspective

Despite an increase in sales for FY2026, the company’s profitability was impacted by upfront investments for growth and the recognition of an impairment loss, which may suggest a focus on future strategic development over short-term earnings. The significant decline in the FY2027 profit forecast could indicate that these strategic investments or changes in market conditions are expected to continue influencing financial performance. While the dividend payout ratio is high at 220.7%, reflecting a commitment to shareholder returns, the company’s path to future profit recovery will be a key area for investors to monitor.

2433|博報堂DY

1064.5

▲ +2.50%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hakuhodo DY Holdings, Inc. announced its consolidated financial results for the fiscal year ended March 31, 2026.

- For the fiscal year 2026 (April 1, 2025 – March 31, 2026), consolidated revenue was JPY 861,003 million (down 9.7% year-on-year), while operating profit increased by 18.9% to JPY 44,675 million, ordinary profit rose 8.0% to JPY 46,061 million, and net profit attributable to owners of the parent significantly increased by 55.8% to JPY 16,775 million.

- The decline in revenue was attributed to factors such as the exclusion of United Inc. from consolidation and a reactionary decrease in government and public sector work, resulting in sales of JPY 1,580,460 million (down 2.0%) based on previous accounting standards. Conversely, successful profitability improvement measures implemented both domestically and internationally led to a 2.4% increase in adjusted gross profit for the full fiscal year.

- Special losses of JPY 10,559 million, including structural reform-related expenses, were recorded, but the increase in operating profit mitigated their impact.

- The annual dividend per share is projected to be JPY 32.00 (JPY 16.00 interim, JPY 16.00 year-end) for both the fiscal year 2026 and the forecast for fiscal year 2027.

- For the fiscal year 2027 (April 1, 2026 – March 31, 2027), the company forecasts consolidated revenue of JPY 910,000 million (up 5.7% year-on-year), operating profit of JPY 46,700 million (up 4.5% year-on-year), and net profit attributable to owners of the parent of JPY 26,000 million (up 55.0% year-on-year), projecting growth in both revenue and profit.

🤖 AI Perspective

Despite a decrease in consolidated revenue, the substantial increases in operating profit, ordinary profit, and net profit attributable to owners of the parent suggest an improvement in profitability. This could indicate the positive impact of successful profitability improvement measures and cost control initiatives implemented across the company’s domestic and international operations. The forecast for revenue and profit growth in fiscal year 2027 suggests a continuation of the recovery trend, which may be a point for investors to monitor.

5201|AGC

5634.0

▼ -0.04%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- AGC Corporation announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026 – March 31, 2026) on May 12, 2026.

- Sales reached ¥537,965 million, representing a 7.7% increase year-on-year, while operating profit was ¥38,472 million, up 48.9% from the previous year.

- Net profit attributable to owners of the parent significantly increased by 243.8% year-on-year to ¥22,844 million.

- Basic earnings per share for the quarter stood at ¥107.73 (compared to ¥31.35 in the same period of the prior year).

- The consolidated full-year earnings forecast for the fiscal year ending December 2026 and the annual dividend forecast of ¥210.00 remain unchanged from the most recently announced figures.

🤖 AI Perspective

AGC’s Q1 FY2026 results demonstrate robust growth across key financial metrics, with significant year-on-year increases in sales, operating profit, and net profit attributable to owners of the parent. The substantial 243.8% rise in net profit attributable to owners of the parent is particularly noteworthy. This strong start to the fiscal year could be seen as a positive indicator for the company’s progress towards its full-year consolidated earnings targets.

5563|新日本電工

468.0

▲ +1.08%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nippon Denko announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1 to March 31, 2026) on May 12, 2026.

- For the first quarter, consolidated net sales were JPY 19.4 billion (unchanged year-on-year), and ordinary profit was JPY 1.1 billion (up JPY 0.7 billion year-on-year).

- “Core recurring profit,” which excludes inventory effects and one-off factors, increased by JPY 1.1 billion year-on-year to JPY 1.6 billion. This was primarily driven by an an increase in ash processing volume in the Waste Incineration Ash Recycling business and stable high prices for molten metal.

- By segment, the Waste Incineration Ash Recycling business achieved a core recurring profit of JPY 0.9 billion (up JPY 0.6 billion year-on-year), showing significant growth. The Functional Materials business also saw an increase in profit to JPY 0.7 billion (up JPY 0.2 billion year-on-year), supported by robust demand for electronic materials.

- The consolidated full-year forecast for the fiscal year ending December 2026 remains unchanged, with projected net sales of JPY 80.0 billion (up JPY 2.7 billion year-on-year) and ordinary profit of JPY 7.0 billion (up JPY 4.3 billion year-on-year). Core recurring profit is expected to be JPY 6.0 billion (up JPY 0.7 billion year-on-year).

🤖 AI Perspective

The first quarter results show significant profit increases for both reported ordinary profit and “core recurring profit,” an independent indicator reflecting the company’s underlying performance. The strong performance of the Waste Incineration Ash Recycling business notably boosted overall profit, suggesting a shift in the revenue structure due to portfolio changes. The full-year outlook anticipates a substantial improvement in reported ordinary profit, driven by a positive reversal in inventory effects linked to rising manganese ore prices, highlighting the significant impact of market fluctuations on the company’s financial results.

8349|東北銀

1478.0

▲ +1.09%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Net profit attributable to owners of parent for the fiscal year ended March 2026 (consolidated) was ¥1,004 million, a decrease of ¥435 million compared to the previous fiscal year.

- Ordinary income for the fiscal year ended March 2026 (consolidated) was ¥1,433 million, a decrease of ¥202 million compared to the previous fiscal year.

- Consolidated core business profit for the fiscal year ended March 2026 increased by ¥217 million year-over-year to ¥3,155 million.

- Tohoku Bank’s non-consolidated total gross margin on funds for the fiscal year ended March 2026 improved by 0.01 percentage points year-over-year to 0.12%.

- Non-consolidated gains/losses on equity securities for the fiscal year ended March 2026 increased by ¥338 million year-over-year to ¥503 million.

🤖 AI Perspective

While an improvement in core business profit and interest margins is noted, the decrease in net profit attributable to owners of parent and ordinary income may be a focal point for investors. The significant increase in gains/losses on equity securities within securities-related profits and losses could have influenced the overall profit and loss structure. The ongoing performance trends would be worth monitoring.

9259|G-タカヨシHD

925.0

▲ +1.76%

📎 Source:G-タカヨシHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-TAKAYOSHI HD has announced its consolidated financial results for the second quarter of the fiscal year ending September 2026.

- For the interim period, consolidated operating revenue was 4,020 million yen (down 1.0% year-on-year), operating profit was 517 million yen (up 12.0% year-on-year), ordinary profit was 517 million yen (up 13.2% year-on-year), and interim net profit attributable to owners of parent was 280 million yen (up 41.8% year-on-year).

- Total transaction volume reached 12,937,553 thousand yen. The number of stores at the end of the interim period was 196, following 24 new openings and 10 closures.

- The number of registered producers increased by 1,142 from the end of the previous fiscal year, reaching 35,048.

- There are no revisions to the consolidated full-year earnings forecast for the fiscal year ending September 2026 or the annual dividend forecast (30.00 yen at year-end).

🤖 AI Perspective

While operating revenue saw a slight decrease, significant increases in operating profit, ordinary profit, and net profit year-on-year may suggest improved profitability. The growth in total transaction volume, store count, and registered producers indicates concrete efforts in business expansion, which could be strengthening the foundation for future business development.

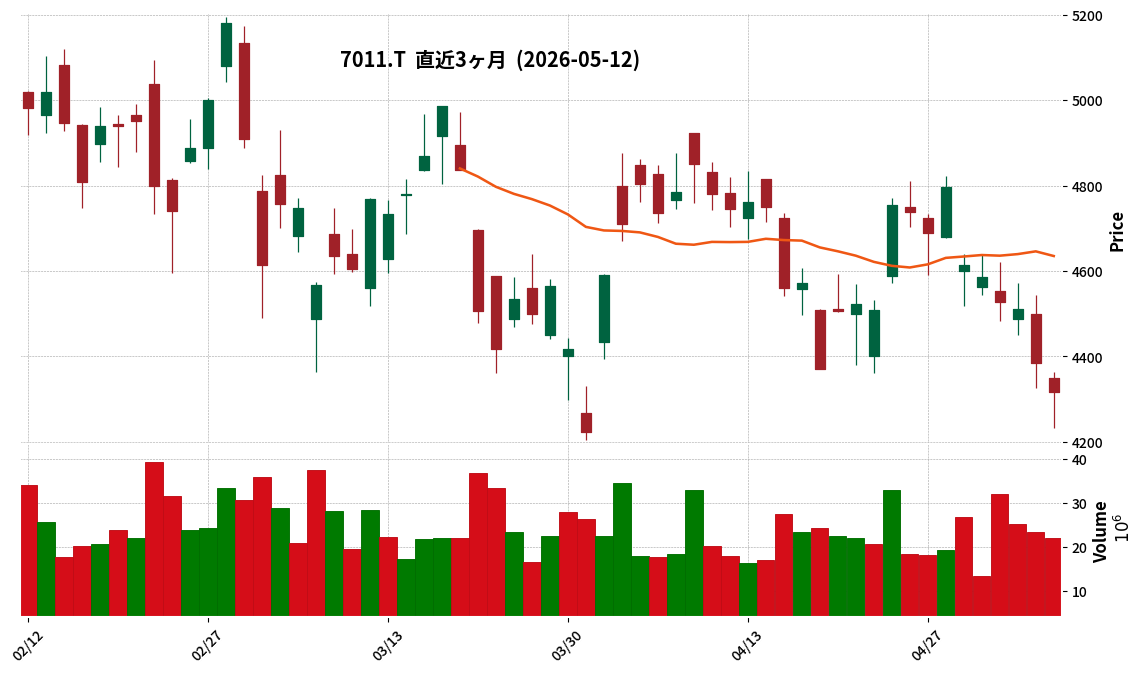

7011|三菱重

4317.0

▼ -1.53%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Mitsubishi Heavy Industries reported consolidated net sales of ¥4,974.1 billion for the fiscal year ended March 31, 2026, marking a 14.1% increase from the previous fiscal year.

- Operating profit (事業利益) reached ¥432.2 billion, up 21.8% year-over-year, and profit attributable to owners of the parent surged by 35.3% to ¥332.1 billion.

- The annual dividend for FY2026 was set at ¥25.00 per share (interim ¥12.00, year-end ¥13.00), an increase from ¥23.00 in the prior fiscal year.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥5,400.0 billion (an 8.6% increase) and profit attributable to owners of the parent of ¥380.0 billion (a 14.4% increase), projecting continued growth.

- The projected annual dividend for FY2027 is ¥29.00 per share (interim ¥14.00, year-end ¥15.00).

🤖 AI Perspective

The significant increase in both net sales and profits for FY2026, especially the over 35% growth in profit attributable to owners of the parent, may suggest robust business performance. The forecast for sustained revenue and profit growth in FY2027, coupled with a planned increase in the annual dividend, could be noteworthy for investors. The substantial rise in cash flow from operating activities may also indicate improved operational efficiency.

8544|京葉銀

2267.0

▲ +4.33%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Keiyo Bank resolved at its Board of Directors meeting on May 12, 2026, to increase the year-end dividend and transfer funds from its separate reserve, with March 31, 2026, as the record date.

- The year-end dividend per share has been set at JPY 23.00, an increase of JPY 2.00 from the previously forecasted JPY 21.00. This results in a total annual dividend per share of JPY 42.00, including the interim dividend of JPY 19.00.

- The total dividend amount is JPY 2,792 million, with an effective date of June 25, 2026.

- The bank decided to transfer JPY 30 billion from its separate reserve to retained earnings. The stated purpose is to enable flexible capital policies, including shareholder returns, in response to changes in the business environment.

- These proposals are scheduled to be submitted for approval at the 120th Ordinary General Meeting of Shareholders, slated for June 24, 2026.

🤖 AI Perspective

- The announced dividend increase may reflect the bank’s adherence to its profit distribution policy, which aims to achieve sound management and enhance internal reserves while providing appropriate returns to stakeholders, considering its performance and financial condition.

- The transfer of funds from the separate reserve to retained earnings could be interpreted as a strategic move to enhance the flexibility of future capital policies, including shareholder returns, in anticipation of evolving business environments.

- While these actions are stated to have no impact on total net assets or profit/loss as they are inter-account transfers within the net assets section, they might indicate an effort to optimize the bank’s capital structure for greater agility.

1820|西松建

5950.0

▲ +4.08%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nishimatsu Construction Co., Ltd. announced that its consolidated net profit attributable to parent company for the full year ended March 31, 2026, was JPY 24,066 million, surpassing the previous forecast of JPY 18,800 million by 28.0%.

- Consolidated operating profit reached JPY 28,029 million (7.8% above forecast) and ordinary profit was JPY 27,384 million (9.5% above forecast), both exceeding prior estimates. Consolidated net sales were JPY 396,030 million, slightly below the JPY 400,000 million forecast.

- The company attributed the profit variance primarily to improved profitability in domestic construction projects, gains from the sale of investment securities (special income), and higher profit margins in the real estate business, despite a delay in real estate sales projects affecting net sales.

- A year-end dividend of JPY 130.00 per share has been decided for the fiscal year ended March 31, 2026, an increase of JPY 10 from the most recent forecast of JPY 120.00.

- This brings the total annual dividend for FY2026 to JPY 230.00 per share, including the interim dividend of JPY 100.00.

🤖 AI Perspective

The significant upward revision in consolidated net profit, driven by improved project profitability and gains from asset sales despite a slight miss on sales, stands out in this announcement. The decision to increase the year-end dividend, aligning with the company’s DOE 5% dividend policy, may suggest a commitment to shareholder returns. Investors might monitor how the company balances its strengthened financial health with aggressive growth investments, including M&A, as outlined in “Nishimatsu-Vision 2035.”

1905|テノックス

1489.0

▲ +0.54%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tenox Co., Ltd. announced on May 12, 2026, revisions to its consolidated earnings forecast and dividend forecast for the fiscal year ending March 2026.

- For the fiscal year ending March 2026, the company revised its full-year consolidated net sales forecast downward to JPY 21,090 million (△1.9% from previous forecast). However, operating profit was revised upward to JPY 1,280 million (+42.2%), ordinary profit to JPY 1,330 million (+40.0%), and profit attributable to owners of parent to JPY 930 million (+43.1%).

- The downward revision in net sales is attributed to delays in the start timing of some large-scale construction projects. The upward revision in profits is due to improved construction revenue from enhanced construction efficiency and the non-occurrence of some expenses as a result of a review of accounting classifications based on the nature of selling, general and administrative expenses.

- The annual dividend forecast was revised upward from the previously announced JPY 52.00 per share to JPY 60.50 per share (interim dividend JPY 26.00, year-end dividend JPY 34.50).

- The reason for the dividend revision is the company’s commitment to shareholder returns as a key management issue, with the Dividend on Equity (DOE) ratio being a significant indicator, combined with consideration of the consolidated business performance for the fiscal year ending March 2026.

🤖 AI Perspective

The announced information suggests an improvement in profit margins, driven by enhanced construction efficiency and expense review, despite a decrease in net sales. Furthermore, the decision to increase dividends while emphasizing the Dividend on Equity (DOE) ratio as a key indicator could be seen as a proactive stance towards shareholder returns. These factors may be noteworthy for investors to consider.

2674|ハードオフ

2146.0

▲ +3.67%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hard Off Corporation (2674.T) announced on May 12, 2026, a revision to its dividend forecast for the fiscal year ending March 2026, indicating an increase.

- The year-end and annual dividend forecast per share has been revised upward by ¥7, from the previously announced ¥78 to ¥85.

- The revision is attributed to the company’s commitment to “returning profits to shareholders” as a key management policy, with a target DOE (Dividend on Equity ratio based on consolidated net assets) of approximately 6%.

- This decision was made after comprehensively considering recent business performance and internal reserves.

- The revised dividend forecast results in a DOE of 6.1%.

- The final resolution for the dividend per share is scheduled to be made at the Board of Directors meeting on May 25, 2026.

🤖 AI Perspective

This upward revision to the dividend forecast may suggest Hard Off Corporation’s strong commitment to its “shareholder return” policy, a key management principle. The explicit mention of a DOE (Dividend on Equity ratio) target of approximately 6%, with the revised forecast resulting in 6.1%, could indicate a transparent and consistent approach to dividend distribution. The consideration of recent business performance and internal reserves in this decision might imply a balanced strategy aimed at both financial stability and enhancing shareholder value.

3176|三洋貿易

1589.0

▲ +1.86%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sanyo Trading announced on May 12, 2026, that its Board of Directors resolved to increase the interim dividend for the period ended March 31, 2026.

- The per-share interim dividend will be ¥30.00, representing a ¥1.00 increase from the most recent forecast (announced on November 10, 2025) of ¥29.00, and also an increase from the previous fiscal year’s (September 2025) ¥28.00.

- The total amount of dividends will be ¥864 million, with an effective date of June 12, 2026.

- This interim dividend will be sourced from retained earnings and will be distributed based on the number of shares prior to the planned stock split (2-for-1 ratio) effective July 1, 2026.

- The company stated that the increase is based on its fundamental policy of continuous and stable dividend increases, considering consolidated business performance and financial position, as shareholder returns are positioned as one of its most important management priorities.

🤖 AI Perspective

This interim dividend increase appears to align with the company’s “SANYO VISION 2028” policy, which aims for progressive dividends with a dividend payout ratio of 30% or more. The decision, based on a comprehensive assessment of business performance and financial conditions, may suggest a continued commitment to active shareholder returns.

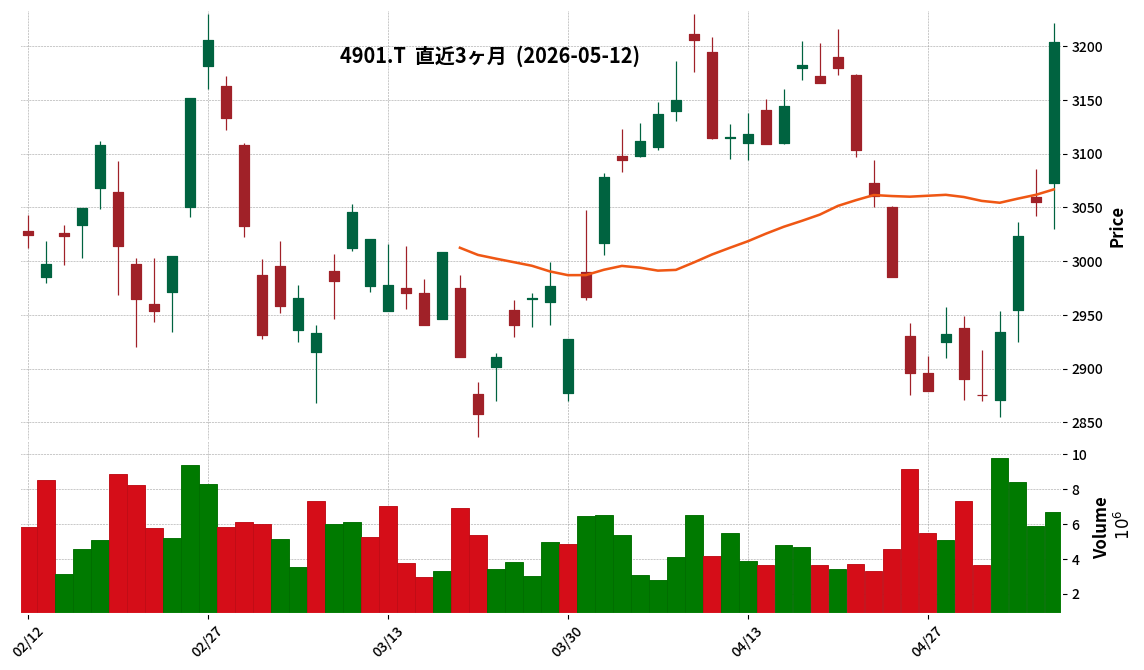

4901|富士フイルム

3204.0

▲ +4.88%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Fujifilm Holdings reported consolidated net sales of JPY 3,356,969 million for the fiscal year ended March 31, 2026, representing a 5.0% increase from the previous fiscal year.

- Operating profit reached JPY 350,210 million (+6.1% YoY), and net income attributable to shareholders of Fujifilm Holdings was JPY 276,735 million (+6.0% YoY).

- The Imaging segment recorded sales of JPY 627.1 billion (+15.7% YoY) and operating profit of JPY 160.0 billion (+14.9% YoY).

- The Electronics segment also contributed positively, with sales of JPY 456.2 billion (+11.9% YoY) and operating profit of JPY 100.9 billion (+34.4% YoY).

- The annual dividend per share for FY2026/3 was increased to JPY 70, up from JPY 65 in the prior fiscal year.

🤖 AI Perspective

- The reported consolidated results indicate a consistent growth trajectory across key financial metrics for the fiscal year, reflecting stable business operations.

- Strong performances in the Imaging and Electronics segments appear to be significant drivers of the overall positive financial outcomes, suggesting growth in these specific business areas.

- The company’s forward guidance for FY2027/3, projecting increases in sales, profit, and an anticipated dividend hike, may suggest a continued focus on sustainable growth and shareholder returns.

5142|アキレス

1659.0

▲ +5.27%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Achilles announced its consolidated financial results for the full year ended March 31, 2026, significantly exceeded its previous forecasts (announced on February 9, 2026). Consolidated net sales increased by 1.0% from JPY 81,000 million to JPY 81,802 million, operating income rose by 29.3% from JPY 2,300 million to JPY 2,972 million, ordinary income surged by 53.7% from JPY 2,550 million to JPY 3,919 million, and net income attributable to owners of parent increased by 46.0% from JPY 1,450 million to JPY 2,116 million.

- The upward revision in consolidated results was attributed to factors including an improved sales mix of high-profitability medical films and industrial materials, ongoing cost reduction activities, and price revisions in individual results, combined with foreign exchange gains of JPY 693 million due to the yen’s depreciation and equity method investment income of JPY 181 million.

- Despite recording extraordinary losses, including an impairment loss of JPY 905 million, the net income attributable to owners of parent still surpassed the previous forecast.

- The company resolved to pay a year-end dividend of JPY 40.00 per share for the fiscal year ended March 31, 2026. This represents an increase of JPY 10.00 from the most recent dividend forecast of JPY 30.00 (announced on February 9, 2026) and an increase of JPY 20.00 from the previous year’s dividend of JPY 20.00.

- The dividend revision was based on the company’s mid-term management plan, which aims for a dividend payout ratio of 30% or more and a dividend of JPY 50 per share, taking into account the performance of the fiscal year ended March 31, 2026. The resulting dividend payout ratio for FY2026 is 25.8%.

🤖 AI Perspective

Achilles’ financial results for the fiscal year ended March 31, 2026, significantly exceeded previous forecasts, particularly in ordinary income and net income attributable to owners of parent. This performance appears to be driven by improvements in business structure, such as an enhanced sales mix of high-profit products and persistent cost reduction efforts, augmented by foreign exchange gains from the yen’s depreciation. The decision to increase the year-end dividend, in line with the mid-term management plan’s shareholder return policy, may be seen as a positive signal regarding the company’s financial health and commitment to investors.

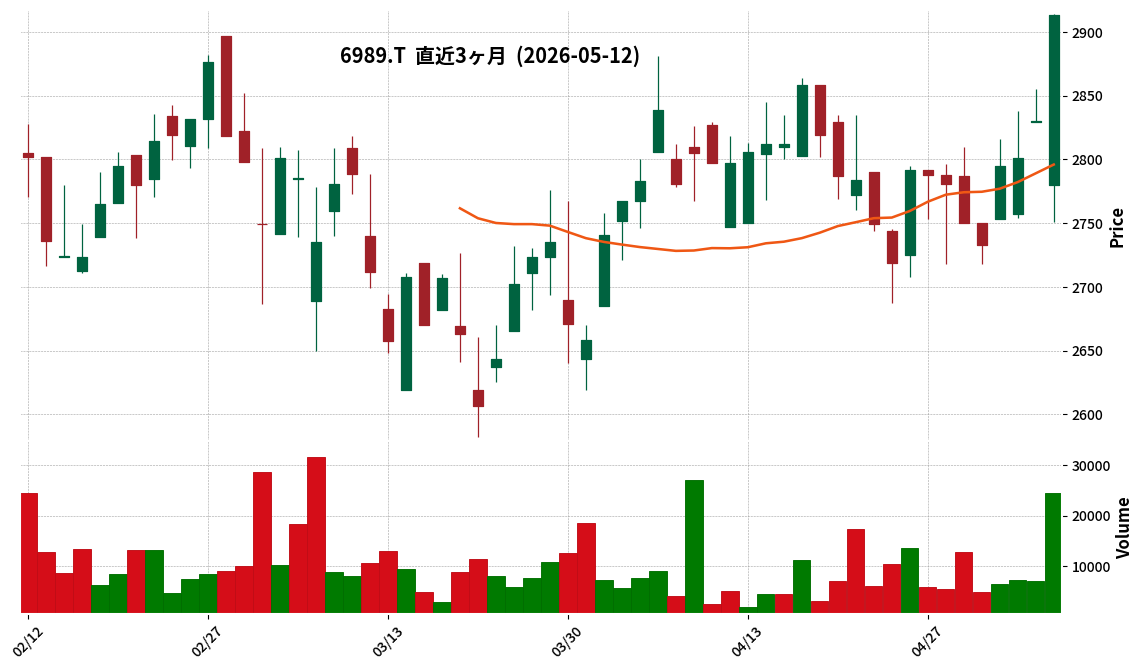

6989|北電工業

2913.0

▲ +2.93%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hokuriku Electric Industry announced an increase in its year-end dividend for the fiscal year ended March 31, 2026, from the previously forecast ¥90.00 per share to ¥95.00 per share (ordinary dividend).

- The total dividend amount for this period will be ¥745 million, with an effective date of June 5, 2026.

- The increase in dividend is attributed to the net profit for the fiscal year ended March 2026 exceeding expectations, consistent with the company’s dividend policy targeting a Dividend on Equity (DOE) ratio of 3.0% or more and a payout ratio of approximately 35%.

- Starting from the fiscal year ending March 2027, the company will introduce interim dividends to enhance opportunities for shareholder returns, transitioning from a single annual year-end dividend to twice-yearly payouts (interim and year-end).

- The record date for interim dividends will be September 30 of each year, and the projected annual dividend for FY2027 is ¥95.00, comprising an interim dividend of ¥47.50 and a year-end dividend of ¥47.50.

🤖 AI Perspective

This announcement suggests that Hokuriku Electric Industry is reinforcing its commitment to shareholder returns, evidenced by the increased dividend for FY2026 and the planned introduction of interim dividends from FY2027. The company’s explicit dividend policy, based on specific DOE and payout ratio targets, could indicate a stable and transparent approach to profit distribution. The shift to semi-annual dividend payments may enhance liquidity for investors and align with broader market expectations for more frequent shareholder returns.

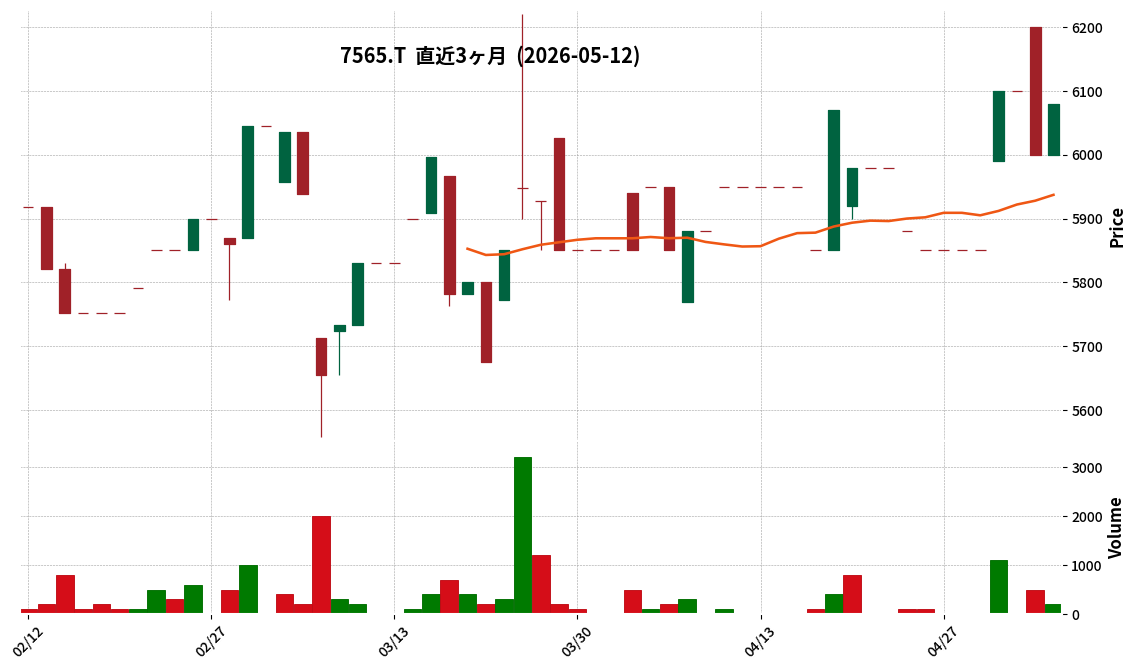

7565|萬世電機

6080.0

▲ +1.33%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Mansei Denki Co., Ltd. announced its consolidated financial results for the fiscal year ended March 31, 2026, reporting net sales of ¥26,992 million, an increase of 10.5% year-on-year.

- Consolidated operating profit reached ¥1,572 million (up 38.6%), ordinary profit ¥1,609 million (up 36.7%), and profit attributable to owners of parent ¥1,114 million (up 27.6%).

- Diluted earnings per share (EPS) were ¥686.30, and the annual dividend per share increased by ¥70 to ¥200 (including a ¥40 commemorative dividend).

- By segment, Electrical Equipment & Industrial Systems sales rose 12.6% to ¥12,017 million, and Equipment sales increased 28.0% to ¥6,444 million.

- The consolidated earnings forecast and dividend forecast for the fiscal year ending March 31, 2027, are currently under review and will be promptly disclosed once finalized.

🤖 AI Perspective

The fiscal year 2026 results demonstrate strong growth across key financial metrics, with all major profit figures showing double-digit year-on-year increases. This performance may suggest positive impacts from favorable business conditions, such as increased investment in FA equipment and industrial/logistics facilities, alongside the company’s efforts to expand its sales areas and strengthen its revenue base. The increase in the annual dividend could also be viewed as a signal of the company’s commitment to shareholder returns.

7743|シード

504.0

▼ -8.70%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)