📌 Today’s Highlights

Today we cover 159 IR announcements. Notable among them: G-ROXX (241A), メディシノバ (4875), G-Arent (5254). Use the table of contents below to navigate to each company.

- 241A|G-ROXX

- 4875|メディシノバ

- 5254|G-Arent

- 3059|ヒラキ

- 1815|鉄建建設

- 6472|NTN

- 7988|ニフコ

- 2780|コメ兵HD

- 3551|ダイニック

- 5105|TOYO TIRE

- 5237|ノザワ

- 5287|イトーヨーギョー

- 6699|ダイヤHD

- 8018|三共生興

- 9405|朝日放送グループHD

- 5471|大同特鋼

- 1301|極洋

- 173A|G-ハンモック

- 1860|戸田建

- 2173|G-博展

- 357A|P-エフアンドエフ

- 3927|フーバーブレイン

- 4375|G-セーフィー

- 4847|IWI

- 4933|Ine

- 5125|G-ファインズ

- 5582|G-グリッド

- 6089|ウィルグループ

- 6942|ソフィアHD

- 7371|G-Zenken

- 9761|東海リース

- 5619|G-マーソ

- 1786|オリエンタル白石

- 2222|寿スピリッツ

- 253A|ETSグループ

- 261A|日水コン

- 279A|P-インターグ

- 3423|エスイー

- 3930|G-はてな

- 4020|G-ビートレンド

- 4099|四国化成HD

- 4169|G-エネチェンジ

- 5616|G-雨風太陽

- 6635|大日光

- 6982|リード

- 7350|おきなわFG

- 9245|G-リベロ

- 2875|東洋水産

- 5869|早稲田学習研究会

- 3909|ショーケース

- 147A|G-ソラコム

- 7037|テノ.

- 8157|都築電気

- 9244|G-デジタリフト

- 1822|大豊建

- 2806|ユタカフーズ

- 2874|ヨコレイ

- 2876|デルソーレ

- 3047|Q-トラックワン

- 3397|トリドールHD

- 3845|アイフリーク

- 4074|G-ラキール

- 4165|G-プレイド

- 4754|トスネット

- 4767|TOW

- 5923|高田機工

- 7270|SUBARU

- 7327|第四北越FG

- 7369|G-メイホーHD

- 7376|G-BCC

- 8362|福井銀

- 9212|G-GEI

- 9663|ナガワ

- 3710|ジョルダン

- 565A|P-FFFHD

- 8066|三谷商

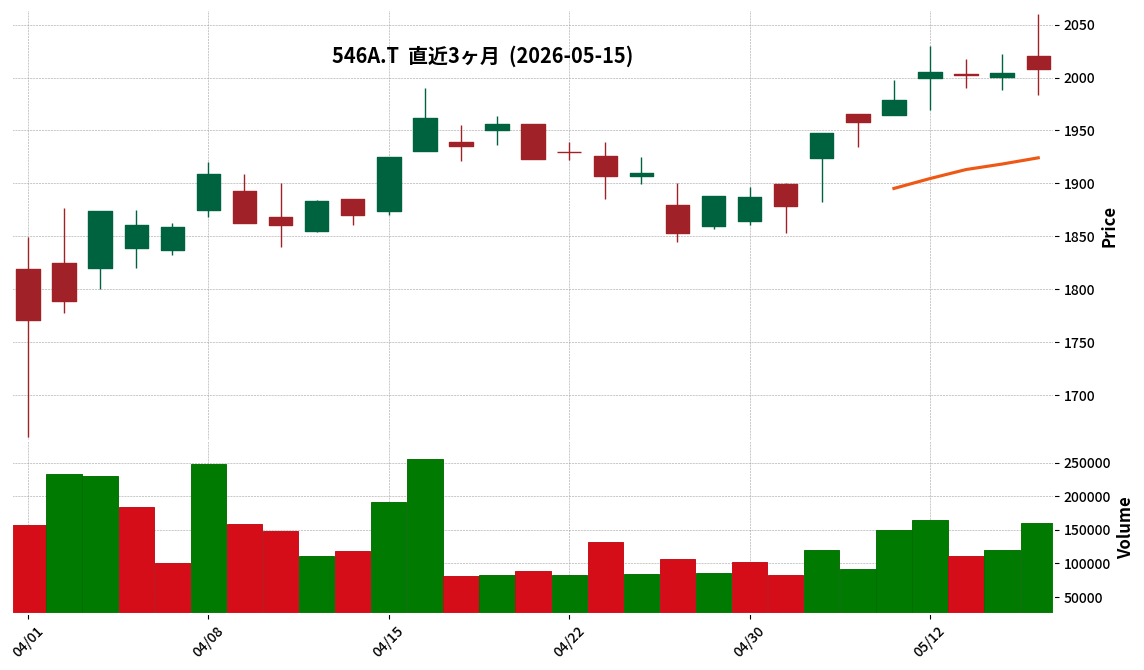

- 546A|MIRAINI

- 3277|サンセイランディック

- 3299|ムゲンエステート

- 3683|サイバーリンクス

- 3861|王子HD

- 4990|昭和化

- 5101|浜ゴム

- 5966|京都機械工具

- 6858|小野測器

- 6977|日抵抗器

- 7272|ヤマハ発

- 8076|カノークス

- 8163|SRSHD

- 8388|阿波銀

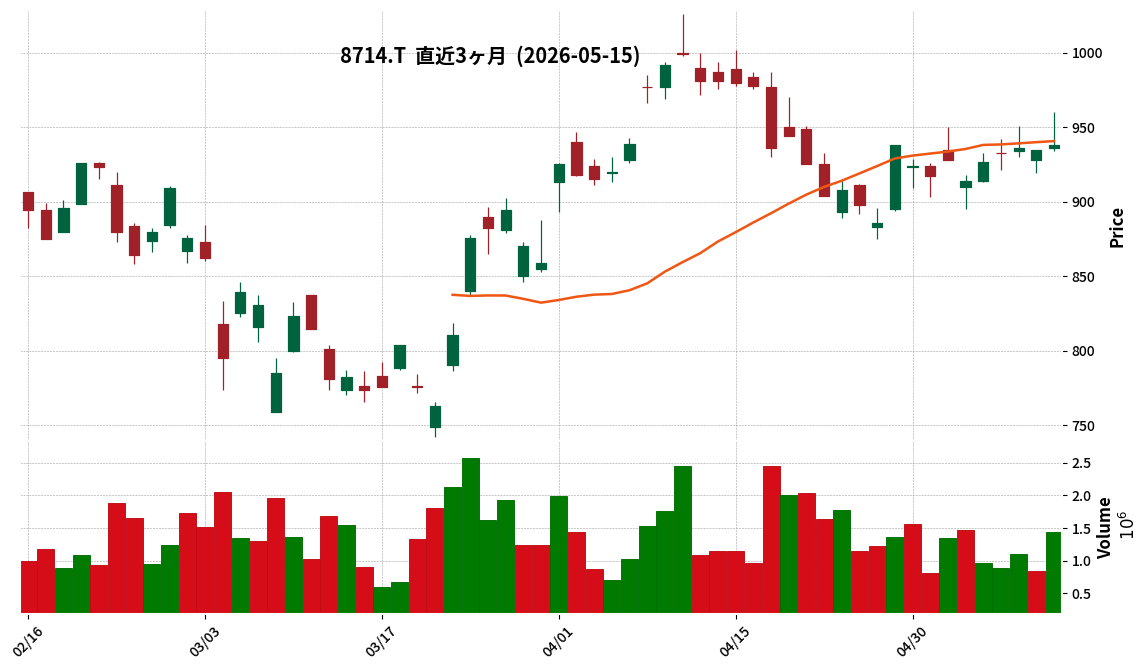

- 8714|池田泉州

- 4116|大日精化

- 6151|日東工器

- 1979|大気社

- 406A|P-環境のミカタHD

- 5074|テスホールディングス

- 5724|アサカ理研

- 5918|滝上工

- 6144|西部電機

- 6331|菱化工機

- 6376|日機装

- 6400|不二精機

- 6457|グローリー

- 2376|サイネックス

- 4391|G-ロジザード

- 6190|G-PXB

- 6291|エアーテック

- 352A|G-LOIVE

- 3769|GMOPG

- 4051|GMO-FG

- 9449|GMO

- 153A|G-カウリス

- 1716|第一カッター

- 1376|カネコ種苗

- 2498|オリコンHD

- 5983|イワブチ

- 6637|寺崎電気

- 1783|fantasista

- 2160|G-GNI

- 2388|G-ウェッジHD

- 2585|ライフドリンクC

- 2597|ユニカフェ

- 3150|グリムス

- 3156|レスター

- 3187|G-ミラタップ

- 3359|G-cotta

- 3469|デュアルタップ

- 3652|G-DMP

- 3667|enish

- 3670|協立情報通信

- 3719|AIストーム

- 3763|プロシップ

- 3772|ウェルス

- 2652|まんだらけ

- 7699|G-OPS

- 3664|G-WIZE

- 2323|fonfun

- 6566|要興業

- 7837|アールシーコア

- 8771|Eギャランティ

- 3358|Trailhead

- 4771|エフアンドエム

- 6554|G-エスユーエス

- 6794|フォスター電

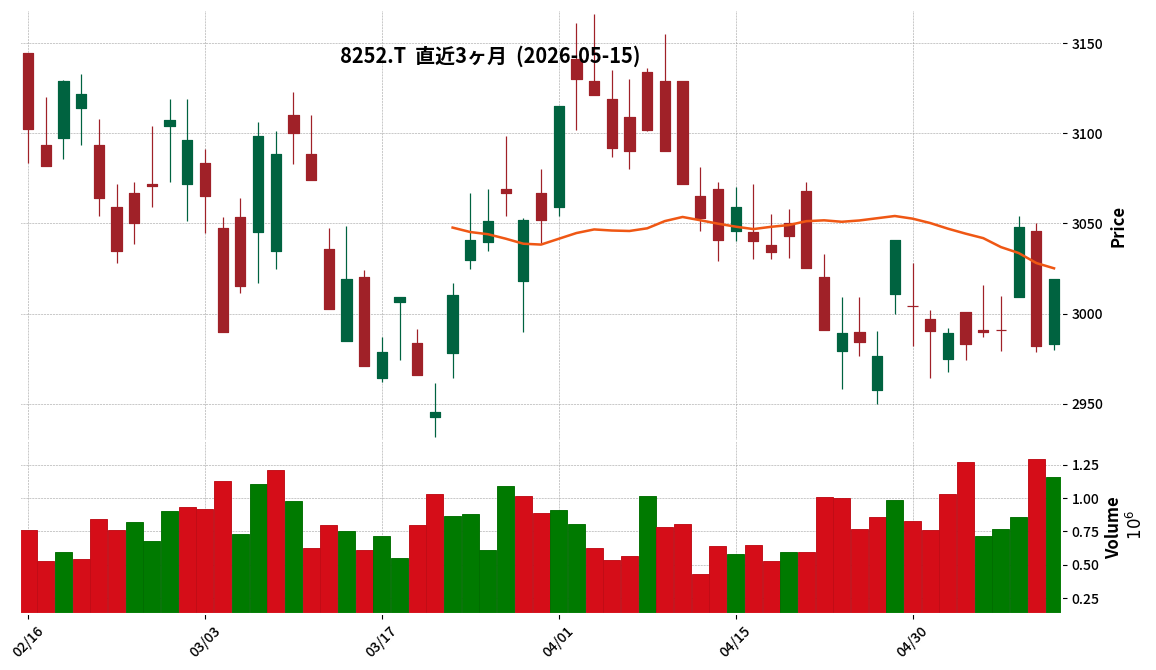

- 8252|丸井G

- 9211|G-エフ・コード

- 4258|G-網屋

- 3392|デリカフーズHD

- 4499|Speee

- 5856|エルアイイーエイチ

- 5868|ロココ

- 6579|G-ログリー

- 6912|菊水HD

- 7383|ネットプロHD

- 7790|バルコス

- 6890|フェローテック

- 4192|G-スパイダープラス

- 9984|ソフトバンクグループ

- 8591|オリックス

241A|G-ROXX

476.0

▲ +1.49%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- ROXX Inc. released its “Q2 FY2026 Earnings Briefing Transcript” on May 15, 2026.

- For the second quarter of the fiscal year ending September 2026, revenue reached approximately ¥940 million, marking a 28.2% increase year-on-year.

- The operating loss for the same period was approximately ¥160 million, representing a ¥440 million improvement compared to the same period in the previous year.

- The company aims for full-year revenue of ¥5 billion and full-year profitability, with Q2 revenue achieving a 37.5% progress rate against the full-year target.

- Key topics for Q2 included the introduction of Z Career AI Interviewer to SOMPO Himawari Life Insurance Co., Ltd., and reinforced development of AI-related products.

🤖 AI Perspective

G-ROXX’s Q2 FY2026 results show robust revenue growth and significant improvement in operating loss, which could be positive signals for investors. The company’s business model anticipates losses in the first half due to upfront investments, with a focus on recovery and achieving full-year profitability in the latter half. The emphasis on AI-related product development and deployment may indicate a strategic direction to enhance future revenue streams and operational efficiency.

4875|メディシノバ

223.0

▲ +3.72%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Medicinova, Inc. announced its consolidated financial results for the first quarter of fiscal year 2026 (January 1, 2026, to March 31, 2026).

- Revenue for the quarter was $186,984.

- Net loss attributable to shareholders was $2,586,258, resulting in a net loss per share of $0.05.

- Total assets as of March 31, 2026, stood at $42,704,854, with total equity at $39,407,234, and an equity ratio of 92.3%.

- The consolidated earnings forecast for the fiscal year ending December 2026 has not been provided, as a reasonable prediction is currently difficult.

🤖 AI Perspective

Medicinova operates as a biopharmaceutical company focused on novel drug development, a sector characterized by significant initial investment and a prolonged path to commercialization. The reported net loss, despite some revenue, may suggest ongoing substantial research and development expenditures typical for companies in this stage. For investors, monitoring the progress of their drug development pipeline rather than immediate profitability could be a key focus.

5254|G-Arent

3900.0

▼ -7.58%

📎 Source:G-Arent Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Arent Co., Ltd. announced on May 15, 2026, the release of the Q&A transcript and archived video from its Q3 FY2026 earnings call.

- The company stated a strategic shift from its previous M&A-centric approach to focusing on “in-house product development” leveraging generative AI, in light of AI’s advancements.

- This strategic change may accelerate the achievement of the product business’s target profit margin of 40-50%.

- It was stated that sales and profits showed improved underlying profitability due to the resolution of temporary factors in Q2, progressing steadily towards full-year targets.

- The company indicated that preliminary investments related to the traditional M&A strategy would conclude in FY226, with a transition to a profit recovery phase from FY227 onwards.

🤖 AI Perspective

The release of G-Arent’s earnings call Q&A highlights a significant strategic pivot for the company. The shift towards in-house development driven by generative AI could potentially lead to increased development efficiency and an earlier achievement of profit margin targets. Investors may find it worthwhile to monitor how this new strategy translates into future financial performance and the specific progress made.

3059|ヒラキ

770.0

▼ -0.90%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hiraki Co., Ltd. announced its consolidated financial results for the fiscal year ended March 2026 (April 1, 2025, to March 31, 2026).

- Consolidated net sales amounted to ¥11,895 million, a decrease of 8.2% compared to the previous fiscal year.

- The company reported an operating loss of ¥320 million, an ordinary loss of ¥313 million, and a net loss attributable to parent company shareholders of ¥426 million.

- Sales for the Mail Order Business segment were ¥5,219 million (down 15.0% YoY), resulting in a segment loss of ¥31 million.

- The Store Sales Business segment recorded sales of ¥6,535 million (down 1.4% YoY) and a segment profit of ¥134 million (down 24.0% YoY).

- The Wholesale Business segment’s sales were ¥141 million (down 26.1% YoY), leading to a segment loss of ¥3 million.

- For the fiscal year ending March 2027 (April 1, 2026, to March 31, 2027), the company forecasts consolidated net sales of ¥12,500 million (up 5.1% YoY), operating profit of ¥150 million, ordinary profit of ¥140 million, and net profit attributable to parent company shareholders of ¥100 million.

- The annual dividend per share for FY2026 March and FY2027 March (forecast) remains unchanged at ¥20.

🤖 AI Perspective

The reported results indicate a decline in net sales and losses at all profit stages for the past fiscal year, primarily influenced by the underperformance of the mail-order business segment. However, the company projects a return to revenue and profit growth for the fiscal year ending March 2027, which may suggest anticipated improvements in business operations or the effectiveness of strategic initiatives. Investors might observe how the company plans to achieve these forward-looking targets amidst the current economic landscape.

1815|鉄建建設

4980.0

▲ +0.30%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tekken Kensetsu Co., Ltd. announced a correction to its “Update on Medium-Term Management Plan 2028 (Upward Revision of Numerical Targets and Change in Dividend Policy)” which was originally disclosed on May 14, 2026.

- The correction primarily addresses errors in the disclosure content, with no changes to numerical targets, dividend policy, or other substantive aspects of the plan.

- Specific corrections include wording in the P.2 “INDEX” header, the unit for D/E Ratio on P.11 (from “0.96%” to “0.96 times”), a photo caption on P.13, and descriptions on P.22 (Architecture Business), P.26 (DX Strategy), P.27 (Environmental Strategy), and P.44 (Dialogue with Shareholders/Investors).

- Additionally, issues with missing logo displays due to PDF conversion errors were resolved.

- A revised version of the document has been republished to reflect these corrections.

🤖 AI Perspective

This correction clarifies that the previously announced Medium-Term Management Plan 2028 has not undergone any substantive changes regarding its numerical targets or dividend policy. For investors, this ensures that the core details of the plan remain consistent with the initial announcement, focusing on document accuracy rather than strategic shifts.

6472|NTN

439.7

▼ -3.60%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- NTN reported consolidated financial results for the fiscal year ended March 31, 2026, with net sales of 825.6 billion JPY (+0.1% YoY), operating income of 31.0 billion JPY (+8.1 billion JPY YoY), and net income attributable to owners of the parent of 12.9 billion JPY (compared to a loss of 23.8 billion JPY in the prior year), marking increased revenue, increased profit, and a return to profitability.

- Sales increased due to rising demand in the aftermarket and industrial machinery sectors, coupled with the impact of the yen’s depreciation, despite sluggish demand in the automotive sector. Operating income rose due to sales price improvements, cost reductions, and the yen’s depreciation.

- For the fiscal year ending March 31, 2027, the company forecasts net sales of 810.0 billion JPY (-2.0% YoY), operating income of 33.0 billion JPY (+2.0 billion JPY YoY), and net income attributable to owners of the parent of 15.0 billion JPY (+2.1 billion JPY YoY), anticipating decreased revenue but increased profit.

- By business segment for FY2027, “Bearings and Others” is expected to see increased revenue of 357.0 billion JPY (+8.1 billion JPY YoY) and increased operating income of 14.5 billion JPY (+2.3 billion JPY YoY). In contrast, “CVJ Axles” is projected to experience decreased revenue of 453.0 billion JPY (-24.5 billion JPY YoY) and decreased operating income of 18.5 billion JPY (-0.3 billion JPY YoY).

- The “DRIVE NTN100” Final structural reform initiative is progressing ahead of schedule, with 18.9 billion JPY in expenses and 10.4 billion JPY in effects recorded for FY2025. For FY2026, 5.1 billion JPY in expenses and 5.3 billion JPY in effects are planned.

🤖 AI Perspective

The strong performance in FY2026 appears to reflect the results of structural reforms, including sales price improvements and cost reductions, in addition to the impact of the depreciating yen. While a revenue decline is anticipated for FY2027 due to sluggish automotive demand, the plan to achieve profit growth through continued structural reforms, sales price pass-throughs, and cost reductions is noteworthy. The projected profit increase in the “Bearings and Others” segment and ongoing initiatives in capacity expansion and new product development may suggest shifts in the company’s future business structure.

7988|ニフコ

4513.0

▲ +3.37%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nifco announced a partial correction to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 [Japanese GAAP]”, originally disclosed on May 14, 2026.

- The reason for the correction is due to a stock split at a ratio of two shares for every one common share, with a record date of September 30, 2026, and an effective date of October 1, 2026.

- The corrected sections include page 1 of the document and page 4 of the attached materials, specifically “(5) Basic Policy on Profit Distribution and Dividends for the Current and Next Fiscal Years”.

- The dividend forecast for the fiscal year ending March 2027 was revised from a previously planned annual dividend of 112 yen per share to an interim dividend of 56 yen and a year-end dividend of 28 yen (after considering the stock split).

- Converted to pre-stock split terms, the year-end dividend would be 56 yen per share, resulting in an annual dividend of 112 yen per share.

🤖 AI Perspective

Nifco’s correction to its financial results highlights the company’s efforts to ensure clarity regarding its future dividend policy following the recently announced stock split. By providing the dividend forecast for the fiscal year ending March 2027 on a post-split basis, investors can better understand the per-share dividend impact of the split. This move could potentially enhance stock accessibility for a broader range of investors by lowering the price per investment unit.

2780|コメ兵HD

5030.0

▼ -8.55%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Komehyo Holdings Inc. announced on May 15, 2026, a correction to a part of its “FY2026 March Earnings Presentation Material.”

- The correction addresses errors found on page 47 of the material released on May 14, 2026.

- The projected revenue increase for FY2027 March was revised from 7,070 million yen to 7,039 million yen.

- The projected gross profit increase for FY2027 March was revised from 4,597 million yen to 4,372 million yen.

- The projected gross profit margin improvement for FY2027 March was revised from 1.1 percentage points to 1.9 percentage points.

🤖 AI Perspective

This correction modifies previously disclosed financial projections within the earnings presentation material. Notably, while the revenue increase and gross profit increase were revised downward, the gross profit margin improvement was revised upward, potentially highlighting an increased focus on profitability. Investors may consider these revised figures when evaluating Komehyo HD’s future outlook and the potential implications for its financial performance.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

3551|ダイニック

1060.0

▲ +2.42%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Dynic Corporation has announced a year-end dividend for the fiscal year ending March 31, 2026.

- The dividend per share will be ¥46, an increase of ¥11 from the previously projected ¥35 (announced May 15, 2025).

- The previous fiscal year’s (March 2025) dividend per share was ¥30.

- The total dividend amount is stated as ¥377 million, compared to ¥251 million in the previous fiscal year.

- The dividend source is retained earnings, with an effective date of June 29, 2026.

- The company attributes the increase to the fiscal year ending March 2026’s performance exceeding initial plans, in line with its revised dividend policy announced on May 15, 2025.

🤖 AI Perspective

- This decision aligns with the company’s updated dividend policy, which emphasizes a minimum dividend payout ratio of 15% and maintaining a consolidated total return ratio of 30% or more.

- The upward revision of the dividend forecast, driven by better-than-expected performance, may be seen as a positive sign regarding the company’s commitment to shareholder returns.

- A consecutive dividend increase from the prior year could indicate stable business growth and a consistent approach to shareholder value.

5105|TOYO TIRE

3857.0

▲ +0.23%

📎 Source:TOYO TIRE Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- TOYO TIRE announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026, to March 31, 2026).

- Net sales amounted to JPY 130,951 million, a 3.4% decrease compared to the same period of the previous year. Operating profit was JPY 20,610 million, an 8.1% decrease year-on-year.

- Ordinary profit increased by 17.0% to JPY 21,352 million, and net profit attributable to owners of the parent rose by 14.6% to JPY 15,476 million.

- Basic earnings per share for the quarter were JPY 100.50, up from JPY 87.71 in the prior year’s first quarter.

- The full-year consolidated earnings forecast and the year-end dividend forecast (JPY 135.00 per share) remain unchanged from the most recently published figures.

🤖 AI Perspective

While net sales and operating profit decreased year-on-year, the increase in ordinary profit and net profit attributable to owners of the parent suggests potential positive impacts from non-operating income/expenses or extraordinary gains/losses. The improvement in the equity ratio from 69.4% to 72.5% could indicate a strengthening of the company’s financial position, which investors may find noteworthy.

5237|ノザワ

1154.0

▲ +2.58%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nozawa reported consolidated net sales of JPY 22,312 million for the fiscal year ended March 2026, marking an increase of JPY 358 million from the previous year.

- Operating profit reached JPY 1,993 million (up JPY 313 million YoY) and ordinary profit reached JPY 2,166 million (up JPY 328 million YoY), indicating increased revenue and profit at these levels.

- Net profit attributable to owners of parent decreased by JPY 551 million year-on-year to JPY 605 million. This decline was primarily due to increased special losses, including a JPY 948 million increase in litigation losses, an impairment loss of JPY 271 million for “MineMag” products, and JPY 91 million in inventory write-downs.

- Sales of the flagship “Asloc” product decreased by JPY 503 million to JPY 10,098 million, while sales of extruded cement boards for residential use increased by JPY 793 million to JPY 7,394 million.

- Consolidated cash flows showed JPY 236 million from operating activities, a decrease of JPY 790 million from investing activities, and a decrease of JPY 478 million from financing activities. Cash and cash equivalents at the end of the period decreased by JPY 1,032 million year-on-year to JPY 5,723 million.

🤖 AI Perspective

Nozawa’s FY2026/3 financial results indicate solid performance in revenue and ordinary profit, but the significant special losses appear to have heavily impacted the final net profit. Investors may consider these special losses, particularly litigation and impairment charges, as points of interest for future strategic monitoring. Conversely, the growth in residential product sales could suggest resilience in specific segments of the construction market, which is worth noting.

5287|イトーヨーギョー

1006.0

▲ +0.10%

📎 Source:イトーヨーギョー Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- ITOYOGYO announced its financial results for the fiscal year ended March 31, 2026.

- Net sales reached ¥3,933 million, representing a 15.6% increase compared to the previous fiscal year.

- Operating profit was ¥336 million (+66.9% year-on-year), and ordinary profit was ¥334 million (+68.9% year-on-year).

- Net income for the period was ¥320 million, marking an 8.1% decrease from the previous fiscal year.

- Earnings per share (EPS) for the fiscal year were ¥108.80.

- The company plans a year-end dividend of ¥22.00, totaling ¥22.00 for the year (compared to ¥20.00 in the previous year).

- For the fiscal year ending March 31, 2027, the company forecasts net sales of ¥4,000 million (+1.7%), operating profit of ¥270 million (-19.8%), ordinary profit of ¥274 million (-18.1%), net income of ¥200 million (-35.8%), and EPS of ¥67.85.

🤖 AI Perspective

ITOYOGYO’s FY2026/3 results show significant growth in sales, operating profit, and ordinary profit, while net income decreased. This could suggest a combination of strong operational performance alongside factors impacting non-operating or extraordinary items. The forecast for FY2027/3 anticipates continued revenue growth but a decline in profits, which might indicate a cautious outlook on future market conditions or increased investments, making it a point for investors to monitor.

6699|ダイヤHD

496.0

▼ -7.46%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Diamond Electric Holdings Co., Ltd. announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 to March 31, 2026).

- Consolidated net sales totaled ¥96,768 million, representing a 5.5% increase compared to the previous fiscal year.

- Consolidated operating profit was ¥2,753 million, up 21.3% year-on-year.

- Consolidated ordinary profit reached ¥2,738 million, marking an 86.6% increase from the prior fiscal year.

- Net income attributable to owners of parent was ¥819 million, a 99.1% increase year-on-year.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥99,400 million (up 2.7%), operating profit of ¥1,750 million (down 36.4%), ordinary profit of ¥510 million (down 81.4%), and net income attributable to owners of parent of ¥10 million (down 98.8%).

- The annual dividend for the fiscal year ended March 31, 2026, was ¥25.00 per share, consistent with the previous year. The forecast for FY2027/3 is also ¥25.00 per share.

8018|三共生興

836.0

▼ -0.59%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sankyo Seikō announced its consolidated financial results for the fiscal year ended March 31, 2026. Net sales were ¥23,984 million (down 2.5% year-on-year), operating profit was ¥750 million (down 57.5%), ordinary profit was ¥2,085 million (down 21.0%), and net income attributable to owners of parent was ¥2,069 million (down 1.9%).

- The company recorded a loss on valuation of inventories of ¥531 million and impairment losses on trademarks and goodwill of ¥1,526 million for its “DAKS” and “LEONARD” brands to mitigate future loss recognition risks.

- A gain on sale of investment securities of ¥3,162 million was recorded as an extraordinary gain.

- The annual dividend for FY2026 remained unchanged at ¥27.00 per share (interim ¥13.50, year-end ¥13.50).

- For the fiscal year ending March 31, 2027, the consolidated performance forecast projects net sales of ¥24,000 million (up 0.1% year-on-year), operating profit of ¥1,500 million (up 100.0%), ordinary profit of ¥2,600 million (up 24.7%), and net income attributable to owners of parent of ¥2,000 million (down 3.3%).

🤖 AI Perspective

The FY2026 consolidated results indicate that significant valuation and impairment losses on key brands substantially impacted operating and ordinary profits. However, the extraordinary gain from the sale of investment securities appears to have mitigated the decline in net income. The projected substantial recovery in operating profit for FY2027 suggests that investors may focus on the potential for business recovery following the previous year’s special losses.

9405|朝日放送グループHD

787.0

▲ +0.38%

📎 Source:朝日放送グループHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Asahi Broadcasting Group Holdings Corporation announced a partial correction to its “FY2026/3 Financial Results [Japanese GAAP] (Consolidated)” on May 15, 2026.

- The reason for the correction was an error in the scheduled date for the online briefing for institutional investors and analysts.

- The previously stated date for the briefing was Monday, May 18, 2026.

- The corrected date for the briefing has been changed to Wednesday, May 20, 2026.

- The scheduled time for the release of materials for the briefing, which is 10:00 AM on the day of the event on the company’s website, remains unchanged.

🤖 AI Perspective

This correction pertains to the scheduling of the investor briefing, not to the financial figures themselves. For investors and analysts, accurate scheduling information is crucial for planning their engagement and information gathering. The prompt correction of the date may help ensure that stakeholders can attend the briefing as planned and receive timely information.

5471|大同特鋼

1910.0

▼ -3.12%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Daido Steel Co., Ltd. announced its consolidated financial results for the fiscal year ended March 31, 2026.

- Revenue increased by 0.6% year-on-year to ¥578,129 million.

- Profit attributable to owners of the parent company increased by 15.2% year-on-year to ¥32,605 million.

- Adjusted operating profit was ¥39,920 million, representing a 9.2% decrease from the previous fiscal year.

- The annual dividend per share was set at ¥49 (¥22 interim, ¥27 year-end).

- For the fiscal year ending March 31, 2027, the company forecasts consolidated revenue of ¥630,000 million (up 9.0% year-on-year) and profit attributable to owners of the parent company of ¥27,500 million (down 15.7% year-on-year), with an annual dividend of ¥52.

🤖 AI Perspective

Daido Steel’s FY2026/3 results show an increase in both revenue and profit attributable to owners of the parent, which indicates overall growth. However, the decrease in adjusted operating profit suggests a potential shift in profit structure or impact from cost factors that could be worth further examination. Additionally, the company’s forecast for the next fiscal year anticipates higher revenue but lower profit, which may warrant attention when assessing future business prospects.

1301|極洋

4445.0

▲ +1.02%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kyokuyo Co., Ltd. announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- Consolidated net sales reached ¥334,612 million, representing a 10.5% increase from the previous fiscal year.

- Net profit attributable to owners of parent increased by 1.5% to ¥6,841 million.

- Consolidated operating profit was ¥10,731 million (down 3.1% year-on-year), and consolidated ordinary profit was ¥10,031 million (down 7.6% year-on-year).

- The annual dividend for the fiscal year ended March 31, 2026, is set at ¥150.00 per share (an increase of ¥20 from the previous year).

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥365,000 million (up 9.1%), operating profit of ¥12,000 million (up 11.8%), ordinary profit of ¥11,000 million (up 9.7%), and net profit attributable to owners of parent of ¥7,200 million (up 5.2%).

🤖 AI Perspective

Kyokuyo’s FY2026/3 results show an increase in revenue and net profit, while operating and ordinary profits declined. This suggests that while sales volume grew, factors impacting profit margins may have been present. The increase in the dividend payment and the positive outlook for FY2027/3, forecasting growth across all key metrics, could indicate management’s confidence in future performance and strategic initiatives.

173A|G-ハンモック

1416.0

▲ +2.16%

📎 Source:G-ハンモック Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 2026, sales were ¥4,889 million (up 3.9% YoY), operating profit was ¥834 million (up 5.5% YoY), ordinary profit was ¥867 million (up 4.7% YoY), and net profit was ¥685 million (up 10.9% YoY).

- Earnings per share for the fiscal year ended March 2026 were ¥162.93, and the equity ratio was 45.2%.

- The annual dividend per share for the fiscal year ended March 2026 increased to ¥40 (from ¥30 in the previous fiscal year).

- For the full-year forecast of the fiscal year ending March 2027, the company expects sales of ¥5,287 million (up 8.1% YoY), net profit of ¥585 million (down 14.6% YoY), and earnings per share of ¥138.98.

- In Network Solutions, a new version of AssetView Cloud+ was released, adding ChatGPT submission log acquisition functionality and strengthening external system integration options.

🤖 AI Perspective

G-HAMMOCK achieved increased revenue and profit for the fiscal year ended March 2026, with all key financial metrics showing year-over-year growth. The 10.9% increase in net profit and the higher dividend per share may indicate a strong financial performance and a commitment to shareholder returns. However, the forecast for the next fiscal year (ending March 2027) projects an increase in sales but a decrease in net profit, which could warrant closer examination by investors regarding the underlying factors.

1860|戸田建

1386.0

▲ +0.65%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Toda Corporation announced consolidated financial results for the fiscal year ended March 31, 2026, reporting net sales of ¥645,737 million (up 10.1% year-on-year), operating profit of ¥38,215 million (up 43.5%), ordinary profit of ¥43,984 million (up 51.2%), and profit attributable to owners of parent of ¥36,981 million (up 46.8%).

- Diluted earnings per share (EPS) for the fiscal year was ¥123.34, an increase from ¥83.59 in the prior year.

- The annual dividend for FY2026 totaled ¥58.00 per share, consisting of an interim dividend of ¥20.00 and a year-end dividend of ¥38.00.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥753,000 million (up 16.6% year-on-year), operating profit of ¥39,000 million (up 2.1%), ordinary profit of ¥40,000 million (down 9.1%), and profit attributable to owners of parent of ¥35,000 million (down 5.4%).

- Total assets increased to ¥998,399 million, net assets to ¥403,161 million, and the equity ratio improved to 39.1%.

🤖 AI Perspective

Toda Corporation’s FY2026 results show significant growth across key financial metrics, with operating profit notably increasing by over 40%. The substantial increase in the annual dividend payment may indicate a commitment to shareholder returns. However, while the FY2027 outlook projects continued revenue growth, a forecasted decrease in ordinary and net profit suggests that the company may be factoring in potential impacts from ongoing investments or evolving market conditions.

2173|G-博展

893.0

▲ +0.56%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of the fiscal year ending December 2026 (January 1, 2026, to March 31, 2026), consolidated net sales increased by 13.5% year-on-year to ¥4,811 million.

- Consolidated operating profit was ¥138 million (down 53.2% year-on-year), ordinary profit was ¥140 million (down 51.9% year-on-year), and net profit attributable to owners of parent was ¥101 million (down 47.3% year-on-year).

- Basic earnings per share for the quarter were ¥6.49.

- As of the end of the quarter, consolidated total assets were ¥8,516 million (down ¥1,666 million from the end of the previous fiscal year), net assets were ¥4,785 million (down ¥217 million), and the equity ratio was 56.1%.

- The full-year consolidated earnings forecast and dividend forecast for the fiscal year ending December 2026 remain unchanged from the most recently announced figures.

🤖 AI Perspective

Hakuten Corp.’s Q1 FY2026 results show a notable increase in sales, while key profit metrics experienced significant declines. This could suggest a compression in profit margins relative to sales. The company has maintained its full-year earnings forecast, which may indicate that the first-quarter performance is largely in line with its internal projections. Investors may monitor future quarters for trends in profitability and margin improvements.

357A|P-エフアンドエフ

6240.0

▲ +0.00%

📎 Source:P-エフアンドエフ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- P-F&F reported consolidated results for the fiscal year ended March 2026: net sales of ¥6,283 million (up 12.1% year-on-year), operating profit of ¥353 million (up 29.6%), ordinary profit of ¥374 million (up 4.1%), and profit attributable to owners of parent of ¥243 million (up 16.9%).

- As of the end of March 2026, consolidated total assets were ¥3,295 million (down 5.1% from the previous fiscal year-end), net assets were ¥815 million (up 33.5%), and the equity ratio was 24.7%.

- Consolidated cash flows showed net cash provided by operating activities of ¥235 million, net cash used in investing activities of ¥41 million, and net cash used in financing activities of ¥356 million. Cash and cash equivalents at the end of the period stood at ¥522 million.

- The annual dividend for the fiscal year ended March 2026 was ¥130.00 per share (year-end), totaling ¥130.00 annually, with a payout ratio of 16.0%.

- For the fiscal year ending March 2027, the company forecasts consolidated net sales of ¥6,291 million (up 0.1% year-on-year), operating profit of ¥300 million (down 15.2%), ordinary profit of ¥304 million (down 18.9%), profit attributable to owners of parent of ¥197 million (down 19.0%), and earnings per share of ¥656.2.

🤖 AI Perspective

While P-F&F achieved increased revenue and profit for the fiscal year ended March 2026, investors may note the forecast for a decrease in profit for the upcoming fiscal year ending March 2027. This could indicate the company’s anticipation of adapting to changes in the pharmacy industry, such as revisions to medical service fees and the promotion of medical DX. The cash flow statement, showing strong cash generation from operating activities but outflows from investing and financing, may suggest ongoing strategic investments and debt management.

3927|フーバーブレイン

1105.0

▼ -1.43%

📎 Source:フーバーブレイン Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Fuva Brain Co., Ltd. reported consolidated results for the fiscal year ended March 2026: Net sales of JPY 5,641 million (up 29.0% year-on-year), Operating income of JPY 203 million (up 8.7%), Ordinary income of JPY 205 million (up 23.9%), and Net income attributable to owners of parent of JPY 308 million (up 181.9%).

- Adjusted net sales amounted to JPY 6,057 million (up 38.5% year-on-year), adjusted operating income was JPY 734 million (up 152.7%), and adjusted ordinary income was JPY 736 million (up 173.5%).

- The year-end dividend for FY2026/3 was JPY 15 per share, resulting in a total annual dividend of JPY 15 per share and an aggregate dividend of JPY 80 million.

- For the fiscal year ending March 2027, the company forecasts consolidated net sales of JPY 7,915 million (up 40.3% year-on-year), operating income of JPY 449 million (up 120.4%), ordinary income of JPY 420 million (up 104.2%), and net income attributable to owners of parent of JPY 330 million (up 7.0%).

- The company’ transitioned to the Standard Market of the Tokyo Stock Exchange on February 6, 2026.

🤖 AI Perspective

Fuva Brain’s FY2026/3 results show significant growth in both net sales and net income, with a particularly strong increase in adjusted profits. This trend may suggest the effectiveness of its growth strategies, including organic expansion and M&A activities, which appear to have positively impacted sales from investment securities. The initiation of dividends and the forecast for a further increase could indicate a commitment to enhanced shareholder returns.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

4375|G-セーフィー

737.0

▲ +0.96%

📎 Source:G-セーフィー Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Safie Inc. announced its Q1 FY2026 consolidated financial results for the period from January 1, 2026, to March 31, 2026.

- Consolidated net sales reached 5,107 million JPY, an increase of 20.9% from 4,223 million JPY in the same period last year.

- Consolidated operating income turned positive at 105 million JPY, compared to an operating loss of 20 million JPY in the prior year.

- Consolidated ordinary income also turned positive to 201 million JPY from a loss of 26 million JPY, and profit attributable to owners of parent became 165 million JPY from a loss of 62 million JPY.

- Basic earnings per share for the quarter were 2.97 JPY, a significant improvement from a loss of 1.13 JPY in the previous year.

- As of March 31, 2026, Annual Recurring Revenue (ARR) stood at 14,996 million JPY (up 21.5% YoY), and the number of billed cameras reached 370,000 units (up 20.9% YoY).

- The consolidated full-year forecast for FY2026 remains unchanged, with projected net sales of 23,215 million JPY and adjusted operating income of 450-650 million JPY.

4847|IWI

928.0

▼ -1.07%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- IWI released its Q3 FY2026 earnings presentation materials on May 15, 2026.

- For the cumulative Q3 FY2026 period, net sales were ¥12,497 million, an increase of 8.4% year-on-year.

- Operating profit for the same period was ¥1,361 million (down 5.8% YoY), ordinary profit was ¥1,391 million (down 4.7% YoY), and net income attributable to owners of parent was ¥951 million (down 7.1% YoY).

- The decrease in profits was attributed to quality control measures and the product mix within the security segment.

- The full-year forecast was revised downwards, with projected net sales of ¥17,200 million (a ¥200 million decrease from the initial forecast) and operating profit of ¥2,000 million (a ¥400 million decrease from the initial forecast).

🤖 AI Perspective

While sales showed robust growth, the company’s profits declined due to quality response measures and changes in product mix, as indicated in the report. The downward revision of the full-year earnings forecast appears to stem from prolonged quality control efforts for specific client projects. Investors may wish to monitor the ongoing IT investment resilience in the payment market and the progress of corrective actions addressing overall company challenges.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

4933|Ine

1071.0

▲ +1.42%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- I-ne Corporation announced its consolidated financial results for the fiscal year ended December 31, 2025 (January 1, 2025 to December 31, 2025).

- Consolidated net sales reached ¥48,975 million, representing an 8.8% increase compared to the previous fiscal year.

- EBITDA was ¥5,626 million, an 8.3% increase year-over-year.

- Operating profit was ¥3,880 million (a 14.4% decrease year-over-year), and ordinary profit was ¥3,830 million (a 16.2% decrease year-over-year).

- Net income attributable to owners of parent amounted to ¥2,097 million, down 28.9% from the previous fiscal year.

- Basic earnings per share stood at ¥119.64.

- A year-end dividend of ¥15.00 per share is planned for the fiscal year ended December 2025 (total annual dividend of ¥15.00 per share).

- For the fiscal year ending December 2026, the company forecasts consolidated net sales of ¥52,000 million to ¥54,000 million, EBITDA of ¥1,200 million to ¥2,700 million, and operating profit of -¥500 million to ¥1,000 million.

5125|G-ファインズ

639.0

▲ +4.07%

📎 Source:G-ファインズ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-FINES announced its Q3 FY2026 financial results for the period from July 1, 2025, to March 31, 2026.

- For the nine months ended March 31, 2026, consolidated net sales were ¥1,843 million, operating profit was ¥61 million, ordinary profit was ¥67 million, and net profit attributable to owners of the parent was ¥43 million.

- Consolidated quarterly financial statements were prepared starting from Q3 FY2026, thus year-on-year percentage changes are not provided.

- The company has included Olupura Co., Ltd. and Nexil Co., Ltd. within its scope of consolidation from this period.

- The full-year consolidated earnings forecast includes net sales of ¥2,747 million, operating profit of ¥131 million, ordinary profit of ¥136 million, net profit attributable to owners of the parent of ¥81 million, and basic earnings per share of ¥18.33.

🤖 AI Perspective

The transition to consolidated financial statements from this period marks a significant change in reporting, making direct comparisons to previous individual results not feasible. The inclusion of Olupura and Nexil in the consolidation scope indicates a strategic shift towards a “talent platform” business model, which may suggest a new direction for the company’s growth. Investors might focus on how the accelerated provision of RPO services, leveraging AI technology, contributes to future performance within the expanding DX market.

5582|G-グリッド

2368.0

▼ -0.92%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- GRID Inc. reported ¥1,951 million in revenue for the third quarter of the fiscal year ending June 2026, marking a 28.7% increase year-over-year. Operating profit reached ¥310 million, a 3.5% increase year-over-year.

- Segment-wise, revenue from the Power domain was ¥1,041 million (+14.5% YoY), Urban & Transportation was ¥351 million (+164.1% YoY), and Energy Management was ¥160 million (none in the prior period). Manufacturing & Logistics revenue was ¥340 million (-26.1% YoY).

- As of the end of Q3, the company had 133 employees (86 AI engineers, 3 energy storage engineers, 44 sales/admin staff), achieving its initial hiring plan.

- Third-quarter revenue exceeded the initial plan by 0.3%, and operating profit surpassed the initial plan by 57.5%.

- The company anticipates achieving its full-year performance targets due to steady progress in the AI business and projected revenue contributions from energy storage development starting in Q4.

🤖 AI Perspective

GRID Inc.’s Q3 FY2026 results indicate robust growth in both revenue and operating profit, primarily driven by strong performance in the power and urban & transportation sectors. The ability to increase operating profit despite rising personnel and office relocation costs may suggest effective revenue growth strategies. The commencement of energy storage development in Q4 is projected to be a key factor in achieving full-year targets, making its future contribution worth monitoring.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

6089|ウィルグループ

1044.0

▼ -5.43%

📎 Source:ウィルグループ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- WILL GROUP reported consolidated results for the fiscal year ended March 2026, with revenue of ¥146.85 billion (+5.1% year-on-year) and operating profit of ¥3.27 billion (+40.2% year-on-year).

- Consolidated revenue achieved a new record high since the fiscal year ended March 2023, and operating profit saw a significant increase.

- Normalized operating profit was ¥3.00 billion (+32.8% year-on-year), and EBITDA was ¥5.63 billion (+15.0% year-on-year).

- The Domestic Working business recorded revenue of ¥88.26 billion (+6.2% year-on-year) and segment profit of ¥3.57 billion (+10.1% year-on-year).

- The Overseas Working business reported revenue of ¥58.50 billion (+3.6% year-on-year) and segment profit of ¥2.42 billion (+69.4% year-on-year). Normalized segment profit increased by 50.8% year-on-year.

- The new medium-term management plan, “WILL-being 2029,” was announced.

🤖 AI Perspective

WILL GROUP’s FY2026/3 results, particularly the record-high revenue and significant increase in operating profit, may suggest strong operational performance. Factors such as the expansion in the construction engineer sector within the Domestic Working business and cost controls in the Overseas Working business appear to have contributed to this growth. The launch of the new medium-term management plan, “WILL-being 2029,” could indicate a clear strategic direction for future growth, which will be worth monitoring.

6942|ソフィアHD

1299.0

▼ -0.46%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Consolidated revenue for the fiscal year ended March 31, 2026, was ¥8,329 million, a decrease of 0.4% compared to the previous fiscal year.

- The company reported a consolidated operating loss of ¥60 million for the period, a decline from the operating profit of ¥344 million in the prior fiscal year.

- Profit attributable to owners of the parent company resulted in a loss of ¥34 million.

- The equity attributable to owners of the parent ratio was 41.5% as of March 31, 2026, an increase from 40.6% at the end of the previous fiscal year.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated revenue of ¥8,928 million (a 7.2% increase year-on-year) and an operating profit of ¥159 million, marking a return to profitability.

🤖 AI Perspective

Sophia Holdings’ FY2026 results indicate a slight revenue decline and a shift to an operating loss, which may be attributed to factors such as the sale of a subsidiary in the internet-related business and intensified competition in the MVNO sector. However, the company projects a return to revenue growth and operating profitability for FY2027, suggesting potential recovery driven by its telecommunications and pharmacy businesses. Investors may want to monitor the progress of these segments in the upcoming fiscal year.

7371|G-Zenken

676.0

▼ -2.31%

📎 Source:G-Zenken Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Zenken announced its consolidated financial results for the third quarter of the fiscal year ending June 2026 (July 1, 2025, to March 31, 2026).

- Cumulative consolidated net sales for the period were ¥4,298 million, representing a 1.9% increase compared to the same period of the previous fiscal year.

- Operating income reached ¥498 million (up 54.9% year-on-year), ordinary income was ¥540 million (up 60.8% year-on-year), and net income attributable to owners of the parent was ¥372 million (up 26.4% year-on-year).

- Basic earnings per share for the quarter were ¥30.63.

- There were no revisions to the full-year consolidated earnings forecast or the annual dividend forecast for the fiscal year ending June 2026 from the most recently published figures.

🤖 AI Perspective

G-Zenken’s Q3 FY2026 results show solid revenue growth and significant improvement in profitability. This performance could indicate effective operational management and cost control initiatives. The reaffirmation of the full-year earnings forecast suggests management’s confidence in achieving its previously announced targets, which may be a point of focus for investors.

9761|東海リース

2290.0

▼ -1.21%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tokai Lease Co., Ltd. made a partial correction to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 [Japanese GAAP]” disclosed on May 14, 2026.

- The correction pertains to “Attachment Page 3 (4) Future Outlook, Consolidated Business Forecast Period.”

- The original consolidated business forecast period was stated as “April 1, 2024 – March 31, 2025.”

- The corrected consolidated business forecast period is now “April 1, 2026 – March 31, 2027.”

- This correction addresses an error in the content of the financial results brief.

🤖 AI Perspective

The revision of the consolidated business forecast period to a future fiscal year is a key detail for investors to understand which accounting period the company’s future performance outlook pertains to. Such corrections are typically made to ensure the accuracy of disclosed information. It is advisable to review the entire financial results brief to confirm that this correction does not impact other parts of the disclosed information.

5619|G-マーソ

847.0

▼ -1.74%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-マーソ’s consolidated net sales for Q1 FY2026 (January 1, 2026 to March 31, 2026) increased by 3.6% year-over-year to ¥291 million.

- During the same period, the consolidated operating loss was △¥10 million (compared to △¥12 million in the prior-year quarter), consolidated ordinary loss was △¥8 million (compared to △¥12 million), and net loss attributable to owners of the parent was △¥5 million (compared to △¥10 million).

- Loss per share for the quarter was △¥1.45 (compared to △¥2.95 in the prior-year quarter).

- As of the end of the first consolidated fiscal quarter, total assets stood at ¥2,157 million, net assets at ¥1,944 million, and the equity ratio was 90.1%.

- The full-year consolidated earnings forecast for FY2026 (net sales ¥1,262 million, operating loss △¥76 million, ordinary loss △¥75 million, and net loss attributable to owners of the parent △¥76 million) remains unchanged.

🤖 AI Perspective

G-Marso’s Q1 results indicate a year-over-year revenue increase and a narrowing of losses across all reporting levels, which may suggest improving operational performance. This performance is likely driven by sustained growth in both “reservation sales” and “advertising sales” within its HealthTech business. The reaffirmation of the full-year forecast could indicate that the company perceives its progress to be generally on track with initial plans.

1786|オリエンタル白石

332.0

▼ -3.49%

📎 Source:オリエンタル白石 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Oriental Shiraishi announced a partial correction to its “Consolidated Financial Results for the Fiscal Year Ended March 2026 [Japanese Standards]” published on May 14, 2026.

- The correction pertains to the consolidated financial forecast for the fiscal year ending March 2027.

- The original consolidated financial forecast for the fiscal year ending March 2027 was sales of ¥75 billion, operating income of ¥4.3 billion, ordinary income of ¥4.9 billion, and profit attributable to owners of parent of ¥3.0 billion.

- The revised consolidated financial forecast for the fiscal year ending March 2027 is sales of ¥75 billion, operating income of ¥4.0 billion, ordinary income of ¥4.5 billion, and profit attributable to owners of parent of ¥2.75 billion.

- While the sales forecast remains unchanged, operating income has decreased by ¥0.3 billion, ordinary income by ¥0.4 billion, and profit attributable to owners of parent by ¥0.25 billion.

🤖 AI Perspective

This correction to the recently announced consolidated earnings forecast for the fiscal year ending March 2027, specifically regarding profit figures, warrants attention from investors to understand its implications compared to the initial projections. The downward adjustment of profit metrics while the sales forecast remains constant may suggest a revised outlook on profitability. This information is crucial for investors to assess the company’s perspective on its future performance, based on the officially released facts.

2222|寿スピリッツ

2112.0

▲ +1.71%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kotobuki Spirits reported record-high full-year financial results for the fiscal year ended March 2026, with net sales of ¥78,781 million, operating income of ¥18,598 million, ordinary income of ¥18,733 million, and net income of ¥12,557 million. All figures represent the fourth consecutive year of record highs.

- Inbound sales (international terminal sales) increased by 6.8% year-on-year to ¥10,701 million, despite impacts from Japan-China relations.

- The company opened 11 new stores, including new brands such as “SALTRA” at Hanshin Umeda Main Store in November 2025, “VANISTA” at Seibu Ikebukuro Main Store in November 2025, and “HELLO MAPLI” at JR Nagoya Takashimaya in February 2026. Concurrently, 9 stores were closed, including 3 stores in Tokyo Station due to renovation.

- Kotobuki Spirits is strengthening its Okinawa operations, with sales to Okinawa reaching ¥1,977 million. A new factory in Miyakojima, Okinawa, with an investment of ¥2.9 billion and a production capacity of ¥5.0 billion in sales, is under preparation for operation in June 2027.

- The actual full-year results for FY2026 achieved 98.9% of the initial forecast for net sales and 95.0% for ordinary income.

🤖 AI Perspective

The announced financial results, featuring record-high sales and profits for the fourth consecutive year, may suggest a sustained growth trajectory for the company. The continued increase in inbound sales despite external factors, coupled with aggressive new brand rollouts and strategic investments like the Okinawa factory, could indicate robust future business development. However, it is worth monitoring that the company did not fully meet its initial forecasts for both net sales and ordinary income, suggesting that execution against plans could be a point of focus for investors.

253A|ETSグループ

1385.0

▲ +3.28%

📎 Source:ETSグループ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- ETS Group announced its consolidated financial results for the second quarter (interim period) of the fiscal year ending September 2026.

- Consolidated net sales for the cumulative period reached 5,687 million yen, marking a 12.2% increase compared to the previous interim period.

- Operating profit grew to 722 million yen (up 88.8%), ordinary profit to 709 million yen (up 90.6%), and profit attributable to owners of parent to 433 million yen (up 89.9%).

- By segment, the Electrical Engineering business reported sales of 4,845 million yen (up 13.7%) and segment profit of 637 million yen (up 123.7%). The Real Estate-related business recorded sales of 835 million yen (up 4.1%) and segment profit of 76 million yen (up 1.2%).

- The full-year consolidated performance forecast remains unchanged from the most recently announced figures, projecting net sales of 11,850 million yen and operating profit of 777 million yen.

🤖 AI Perspective

This earnings report indicates a significant increase in both revenue and profit for ETS Group compared to the previous interim period. The substantial growth in profit, particularly within the Electrical Engineering segment, may suggest positive developments in project profitability in the power business. With the full-year forecast remaining unrevised, the company’s future performance and project execution will be worth monitoring.

261A|日水コン

2256.0

▲ +2.13%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nippon Suiko Consultants reported Q1 FY2026 results with orders received at ¥2.813 billion (down 55.5% year-on-year) and net sales at ¥7.409 billion (up 4.0% year-on-year).

- Operating profit was ¥1.234 billion (down 8.7% year-on-year), and net income attributable to owners of the parent was ¥843 million (down 8.5% year-on-year).

- The decline in orders received is attributed to the booking of a large 10-year contract (¥3.120 billion) in Q1 FY2025; excluding this, orders received were down 12.0% year-on-year.

- The decrease in operating profit is explained by an increase in the provision for business compensation (¥129 million increase), and excluding this special factor, the underlying operating profit was ¥1.364 billion, comparable to the previous year.

- The company announced the signing of a capital and business alliance agreement with Liberaware Inc. on May 15, 2026, involving an investment of approximately ¥500 million.

🤖 AI Perspective

While Q1 sales increased, operating profit declined. This was primarily due to an increase in the provision for business compensation, calculated based on the average of the past three years, rather than new defects in current business activities. The decrease in orders received was a reactionary effect from a large contract in the previous year, but sufficient order backlog remains, suggesting a progress towards full-year order and sales targets when accounting for seasonal variations. The capital and business alliance with Liberaware Inc. may indicate a strategic investment towards strengthening DX solutions in the water infrastructure sector.

279A|P-インターグ

1550.0

▲ +0.00%

📎 Source:P-インターグ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- P-Interg announced its non-consolidated financial results for the fiscal year ended March 2026.

- Net sales reached 8,706 million yen, marking a 47.5% increase compared to the previous fiscal year.

- Operating profit was 222 million yen (+22.4% YoY), ordinary profit was 249 million yen (+29.4% YoY), and net profit was 165 million yen (+23.5% YoY).

- Diluted earnings per share were 82.60 yen (adjusted for a 1-for-10,000 stock split on June 28, 2024).

- For the fiscal year ending March 2027, the company forecasts consolidated net sales of 9,894 million yen, operating profit of 85 million yen, ordinary profit of 118 million yen, and net profit attributable to parent company shareholders of 76 million yen, as it transitions to consolidated financial statements.

🤖 AI Perspective

P-Interg’s strong performance in FY2026, with significant growth across all key profit metrics, suggests robust demand within its media business. The planned transition to consolidated financial statements from FY2027 could indicate an expansion of its business scope and potentially a more comprehensive view of its overall financial health for investors. The notable increase in cash outflow from investing activities may suggest a strategic focus on future growth initiatives, which is worth monitoring in subsequent reports.

3423|エスイー

271.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SE Corporation announced its consolidated financial results for the fiscal year ended March 2026.

- Consolidated net sales were ¥25,401 million (down 1.9% year-on-year), operating income was ¥599 million (down 29.5% year-on-year), and ordinary income was ¥591 million (down 33.2% year-on-year).

- Net loss attributable to owners of the parent company was ¥(434) million, a significant decline from the ¥543 million net income recorded in the previous fiscal year.

- Basic earnings per share stood at ¥(14.40).

- For the fiscal year ending March 2027, the company projects consolidated net sales of ¥25,000 million (down 1.6% year-on-year), operating income of ¥603 million (up 0.7%), ordinary income of ¥600 million (up 1.4%), and net income attributable to owners of the parent company of ¥159 million (no percentage change due to prior year loss), with basic EPS of ¥5.29.

- The annual dividend per share for FY2026/3 was ¥13.00 (year-end), and the forecast for FY2027/3 is ¥12.00 (year-end).

🤖 AI Perspective

The FY2026/3 consolidated results show a slight decline in sales, coupled with significant decreases in operating and ordinary income, culminating in a net loss attributable to parent company shareholders. This shift to a loss position, particularly from the previous year’s profit, warrants attention from investors. While the company forecasts a return to profitability for the upcoming fiscal year, the impact of the stated reasons for the current year’s individual performance, such as increased selling, general and administrative expenses due to R&D reinforcement and deferred tax asset derecognition, on future performance remains a factor to monitor.

3930|G-はてな

843.0

▲ +1.57%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hatena Co., Ltd. announced on May 15, 2026, the “Notice Regarding Commemorative Shareholder Benefit.”

- This announcement confirms that the “10th Anniversary Shareholder Special Benefit,” initially announced on April 14, 2026, will proceed as originally planned, despite the “Notice Regarding the Occurrence of a Fund Outflow Incident” published on April 24, 2026.

- The benefit targets shareholders holding 3 units (300 shares) or more of the company’s stock as recorded in the shareholder register as of July 31, 2026. They will receive a Digital Gift® worth ¥25,000 provided by Digital Plus Co., Ltd.

- For this specific benefit, all shareholders holding 3 units or more are eligible, regardless of their continuous holding period.

- The gifts are scheduled to be sent in October 2026, enclosed with the notice of the General Meeting of Shareholders.

- The company is currently reviewing the impact of this matter, including its effect on the company’s financial results for the fiscal year ending July 2026, and will promptly disclose any material developments.

🤖 AI Perspective

- This announcement may be seen by investors as a reaffirmation of the company’s commitment to shareholder returns, even after the recent fund outflow incident.

- The clarity regarding the eligibility (no continuous holding period requirement) and the specific value of the digital gift could be a point of interest for current and potential shareholders.

- Investors might continue to monitor for further updates on the financial impact of both the fund outflow incident and this shareholder benefit on the company’s performance.

4020|G-ビートレンド

675.0

▼ -2.17%

📎 Source:G-ビートレンド Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Betrend Corporation announced its unaudited financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026 – March 31, 2026).

- Consolidated net sales for the quarter totaled ¥264 million, representing a 7.1% decrease compared to the same period last year.

- The company reported an operating loss of ¥62 million (compared to an operating income of ¥4 million in the prior year), an ordinary loss of ¥62 million (compared to an ordinary income of ¥5 million), and a net loss of ¥62 million (compared to a net income of ¥2 million).

- Total CRM service ARR was ¥955,208 thousand (down 1.5% year-on-year). Smart CRM service contracts increased by 4 companies to 185, while email marketing service contracts decreased by 53 companies to 353.

- The full-year earnings forecast and dividend forecast for the fiscal year ending December 2026 remain unchanged from the most recently announced figures.

🤖 AI Perspective

Betrend’s Q1 FY2026 results show a decline in revenue and reported losses, which appears to be attributed to strategic investments in infrastructure and increased personnel costs as part of its ongoing mid-term management plan. While the smart CRM service saw an increase in client contracts, a notable decrease in email marketing service contracts could suggest a shift in business focus or market dynamics. Investors may find it worthwhile to monitor the company’s progress in its investment phase and the evolution of its service offerings.

4099|四国化成HD

5840.0

▼ -3.15%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of the fiscal year ending December 2026 (January 1, 2026 – March 31, 2026), consolidated results were: net sales of JPY 19,868 million (up 18.2% year-on-year), operating income of JPY 4,240 million (up 39.6%), ordinary income of JPY 4,520 million (up 60.8%), and net income attributable to owners of parent of JPY 3,041 million (up 58.0%).

- Net sales, operating income, ordinary income, and net income attributable to owners of parent all reached record highs for a first quarter.

- The Chemicals business reported net sales of JPY 14,611 million (up 26.2% year-on-year) and segment income of JPY 3,756 million (up 39.0%), driven by strong performance in fine chemicals.

- The Building Materials business recorded net sales of JPY 4,997 million (up 1.7% year-on-year) and segment income of JPY 359 million (up 31.0%).

- The consolidated full-year forecast for the fiscal year ending December 2026 has been revised: net sales of JPY 88,000 million (up 24.5% from previous year), operating income of JPY 14,400 million (up 32.5%), ordinary income of JPY 14,500 million (up 21.6%), and net income attributable to owners of parent of JPY 10,000 million (up 18.2%).

🤖 AI Perspective

Shikoku Chemicals HD’s Q1 results indicate a very strong start to the fiscal year, with record-high sales and profits across key metrics. The significant contribution from the fine chemicals segment within the Chemicals business, driven by expanded sales both domestically and internationally, appears to be a primary growth driver. The upward revision of the full-year forecast could suggest management’s increased confidence in continued positive performance.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

4169|G-エネチェンジ

364.0

▲ +2.54%

📎 Source:G-エネチェンジ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-ENECHANGE reported consolidated net sales of ¥6,697 million for the fiscal year ended March 2026.

- The consolidated operating profit for the same period was ¥592 million, with a net profit attributable to owners of parent of ¥130 million.

- This marks a return to profitability, as the previous fiscal year (ended March 2025) reported an operating loss of ¥3,630 million and a net loss attributable to owners of parent of ¥1,273 million.

- Adjusted EBITDA for the fiscal year ended March 2026 stood at ¥653 million.

- For the fiscal year ending March 2027, the company forecasts consolidated net sales of ¥6,800 million (1.5% increase year-on-year), operating profit of ¥600 million (1.2% increase), and net profit attributable to owners of parent of ¥550 million (320.1% increase).

- Dividends for both the fiscal years ended March 2025 and March 2026 were ¥0.00 per share, and the forecast for March 2027 remains undecided.

🤖 AI Perspective

G-ENECHANGE’s FY2026/3 results show a notable shift from a net loss in the previous period to profitability in operating income and net profit attributable to owners of parent, which may suggest a transition to a more profitable operational phase. The robust forecast for net profit attributable to owners of parent in FY2027/3, despite a modest increase in sales, could indicate an expectation of improved profitability and operational efficiency in the coming year.

5616|G-雨風太陽

748.0

▲ +1.08%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Amekazetaiyo announced its financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026 – March 31, 2026).

- The non-consolidated financial performance shows sales of ¥232 million (down 1.1% year-on-year), an operating loss of ¥17 million (compared to an operating loss of ¥19 million in the prior year quarter), an ordinary loss of ¥17 million (compared to an ordinary loss of ¥17 million), and a net loss for the quarter of ¥17 million (compared to a net loss of ¥17 million).

- By segment, personal services recorded sales of ¥135 million (down 17.9% year-on-year) and an operating profit of ¥27 million (down 22.3% year-on-year). Corporate services achieved sales of ¥97 million (up 38.5% year-on-year) and an operating profit of ¥15 million (up 93.4% year-on-year).

- As of the end of the quarter, total assets stood at ¥830 million (down ¥176 million from the end of the previous fiscal year), and net assets at ¥327 million (down ¥17 million from the end of the previous fiscal year), with an equity ratio of 39.5% (compared to 34.3% at the end of the previous fiscal year).

- The full-year forecast for the fiscal year ending December 2026 remains unchanged from the forecast published on February 13, 2026.

🤖 AI Perspective

G-Amekazetaiyo’s Q1 results indicate a mixed performance, with overall revenue decline and continued losses. However, the strong growth in both revenue and profit for the corporate services segment suggests a potential area of strength for future development. Investors may consider monitoring the company’s strategies to address the declining revenue in personal services, which could be crucial for achieving the unchanged full-year targets.

6635|大日光

651.0

▼ -2.84%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Dainippon Light (6635) announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026 – March 31, 2026).

- Net sales reached ¥9,557 million, representing a 7.6% increase compared to the same quarter of the previous year.

- Operating profit was ¥58 million, a decrease of 68.7% from the prior year’s first quarter.

- Ordinary profit stood at ¥80 million, down 62.0% year-on-year.

- Net income attributable to parent company shareholders increased by 34.4% to ¥262 million.

- A significant change in the scope of consolidation includes the addition of TROIS TAKAYA ELECTRONICS (THAILAND) Co.,Ltd.

🤖 AI Perspective

While sales increased, the substantial decline in operating and ordinary profit suggests potential impacts from rising costs or changes in product mix with lower profit margins. The increase in net income attributable to parent shareholders, driven by special gains, indicates that investors may want to monitor the nature and sustainability of these gains. The contribution of the newly consolidated subsidiary to future performance is also worth monitoring.

6982|リード

612.0

▲ +1.16%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Lead Co., Ltd. has released its financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- For FY2026/3, net sales were ¥5,141 million (up 22.8% year-on-year), operating loss was ¥111 million, ordinary loss was ¥79 million, and net loss was ¥69 million.

- Sales in the Automotive Parts division were ¥4,619 million (up 19.9% year-on-year), and sales in the Company Products division were ¥494 million (up 125.9% year-on-year).

- As of March 31, 2026, total assets were ¥8,705 million, net assets were ¥2,545 million, and the equity ratio was 29.2%.

- For the fiscal year ending March 31, 2027 (April 1, 2026 – March 31, 2027), the company forecasts full-year net sales of ¥6,660 million (up 29.5% year-on-year), operating income of ¥80 million, ordinary income of ¥80 million, and net income of ¥60 million.

- The company forecasts a year-end dividend of ¥12.00 per share for FY2027/3 (compared to ¥10.00 per share for FY2026/3).

7350|おきなわFG

5780.0

▼ -0.17%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Okinawa Financial Group Inc. announced an upward revision to its final year targets (FY2027/3) for the 2nd Mid-Term Business Plan (April 2024 – March 2027).

- The consolidated ordinary revenue target has been raised from ¥71,000 million to ¥80,000 million, and the consolidated net income target from ¥11,000 million to ¥12,000 million.

- The consolidated ROE target has been revised from approximately 6.20% to approximately 6.70%, while the consolidated Common Equity Tier 1 ratio target remains unchanged at approximately 11%.

- The year-end dividend for the fiscal year ending March 31, 2026, has been increased from the most recent forecast of ¥70.00 per share to ¥100.00 per share.

- This results in an annual dividend per share of ¥170 for the fiscal year ending March 2026, with a forecasted annual dividend of ¥200 for the fiscal year ending March 2027.

- The reasons for the upward revision include solid performance, driven by increased average loan balances and service revenue at Okinawa Bank, coupled with market interest rates trending higher than at the time of the previous revision.

🤖 AI Perspective

Okinawa FG’s simultaneous announcement of revised upward business targets and a significant dividend increase is noteworthy for investors. This move suggests confidence in achieving management goals, supported by strong core business performance and a favorable market interest rate environment. The continuation of a progressive dividend policy, alongside explicit annual dividend forecasts, could further enhance investor expectations regarding future shareholder returns.

9245|G-リベロ

1800.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Libero announced its Q1 FY2026 consolidated financial results for the period from January 1, 2026, to March 31, 2026.

- Consolidated net sales reached ¥1,544 million, representing a 23.8% increase compared to the same period of the previous year.

- Consolidated operating profit was ¥535 million and ordinary profit was ¥538 million, marking increases of 90.3% and 90.9% respectively year-over-year.

- Net income attributable to owners of the parent recorded ¥369 million, an increase of 101.1% from the prior year’s first quarter.

- Basic earnings per share for the quarter were ¥69.72, and diluted earnings per share were ¥62.75.

🤖 AI Perspective

G-Libero’s Q1 FY2026 results show significant year-over-year growth across all key financial metrics, suggesting robust operational performance. The substantial increase in net income attributable to owners of the parent, up by 101.1%, could indicate improved profitability. The expansion of current assets and total assets in the consolidated financial position may reflect the company’s ongoing business expansion efforts.

2875|東洋水産

10520.0

▲ +1.69%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Toyo Suisan Kaisha, Ltd. announced on May 15, 2026, that its Board of Directors resolved to increase the year-end dividend for shareholders of record as of March 31, 2026.

- The per-share dividend for the year-end will be JPY 140.00, an increase of JPY 20.00 from the latest dividend forecast of JPY 120.00 announced on January 30, 2026.

- The total dividend amount will be JPY 13,635 million.

- The effective date for the dividend payment is June 26, 2026, with the source of funds being retained earnings.