📌 Today’s Highlights

Today we cover 50 IR announcements. Notable among them: G-ELEMENTS (5246), G-ホープ (6195), U-NEXT (9418). Use the table of contents below to navigate to each company.

- 5246|G-ELEMENTS

- 5892|G-yutori

- 6195|G-ホープ

- 9418|U-NEXT

- 3260|エスポア

- 464A|G-QPSHD

- 7815|東京ボード工業

- 3030|ハブ

- 4920|日本色材

- 2303|ドーン

- 3323|レカム

- 9948|アークス

- 1407|ウエストHD

- 8011|三陽商

- 9837|モリト

- 3930|G-はてな

- 7608|SKジャパン

- 7805|プリントネット

- 8614|東洋証

- 9381|エーアイテイー

- 6521|G-オキサイド

- 3935|エディア

- 7065|ユーピーアール

- 1430|ファーストコーポ

- 209A|P-小野谷機工

- 3892|岡山製紙

- 4015|G-ペイクラウドHD

- 8887|シーラHD

- 3177|ありがとうS

- 3536|アクサスHD

- 5078|セレコーポレーション

- 3683|サイバーリンクス

- 5817|JMACS

- 6897|ツインバード

- 7601|ポプラ

- 9601|松竹

- 3181|買取王国

- 5076|インフロニアHD

- 1887|日本国土開発

- 6142|富士精工

- 6150|タケダ機械

- 7520|エコス

- 9778|昴

- 3174|ハピネス&D

- 138A|G-光フードサービス

- 156A|G-マテリアルG

- 189A|G-D&Mカンパニー

- 205A|G-ロゴスHD

- 2168|パソナグループ

- 2292|S FOODS

5246|G-ELEMENTS

632.0

▲ +0.00%

📎 Source:G-ELEMENTS Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-ELEMENTS (5246) announced its consolidated financial results for the first quarter of the fiscal year ending November 2026 (December 1, 2025, to February 28, 2026).

- Net sales reached 1,291 million yen, marking an 80.6% increase compared to the same period of the previous fiscal year.

- Operating income turned profitable at 119 million yen, from a loss of 13 million yen in the prior year, and net income attributable to owners of parent also turned profitable at 100 million yen, from a loss of 51 million yen.

- EBITDA grew by 185.7% year-over-year to 261 million yen.

- The consolidated full-year earnings forecast for the fiscal year ending November 2026 remains unchanged from the most recently announced projections.

🤖 AI Perspective

G-ELEMENTS achieved significant growth in net sales and a return to profitability across key earnings metrics in its first quarter of fiscal year 2026. This performance may suggest the company’s strategic focus on expanding its core services in Japan is progressing effectively. The reported market expansion for AI cloud platform-based personal identification and optimization solutions appears to be a key driver for these positive results.

5892|G-yutori

2173.0

▼ -0.14%

📎 Source:G-yutori Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-yutori Co., Ltd. resolved at its Board of Directors meeting on April 13, 2026, to acquire all shares of its subsidiary, heart relation Co., Ltd., making it a wholly-owned subsidiary.

- The number of heart relation shares acquired is 49,000, with an acquisition price of JPY 1,960 million for the common shares of the target company, plus an estimated JPY 1.5 million for advisory fees, totaling approximately JPY 1,961.5 million.

- The acquisition price will be paid through bank borrowings, and the share transfer execution date is scheduled for April 30, 2026.

- It was also decided to issue 53,600 new shares through a third-party allotment to Ms. Haruna Kojima, Representative Director of heart relation, at an issue price of JPY 2,176 per share.

- For the issuance of new shares, a portion of Ms. Kojima’s claims from the transfer of heart relation shares to G-yutori (JPY 116,633,600) will be used as property for in-kind contribution. The payment due date is April 30, 2026.

- This transaction will not impact G-yutori’s consolidated results for the fiscal year ending March 2026, and the impact on the fiscal year ending March 2027 is currently under review.

🤖 AI Perspective

The complete acquisition of profitable heart relation by G-yutori is expected to strengthen the group’s revenue base and improve capital efficiency. The third-party allotment of new shares to Ms. Haruna Kojima, heart relation’s representative, may also aim to enhance her commitment to group management and contribute to business growth. While this will result in dilution for existing shareholders, the stated objective of enhancing corporate value could be a key focus for investors.

6195|G-ホープ

212.0

▼ -0.47%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-HOPE announced on April 13, 2026, that its Board of Directors resolved to merge two consolidated subsidiaries.

- The surviving company will be Jichitai Works Co., Ltd., and the absorbed company will be Jichitai Creation Technology Lab Co., Ltd.

- The effective date for this merger is scheduled for July 1, 2026.

- The merger’s objective is to maximize synergies and accelerate business growth, as collaboration in resolving local government issues, which materialized over approximately one year post-subsidiary acquisition, largely involved Jichitai Works.

- This merger is between wholly-owned subsidiaries, involves no allocation of shares or other financial consideration, and is expected to have a minor impact on the company’s consolidated earnings for the fiscal year ending March 2027.

🤖 AI Perspective

This merger, involving existing consolidated subsidiaries, appears to be a strategic move to maximize synergy effects within the public-private partnership business through internal restructuring. The decision to make Jichitai Creation Technology Lab a wholly-owned subsidiary before the merger suggests an aim to streamline integration. While the short-term impact on consolidated earnings is expected to be minor, its contribution to strengthening the mid-to-long-term business foundation could be a point of interest for investors.

9418|U-NEXT

1611.0

▲ +1.13%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the second quarter of the fiscal year ending August 2026 (September 1, 2025 – February 28, 2026), U-NEXT Holdings reported consolidated revenue of ¥212,823 million, representing a 13.9% increase compared to the prior interim period.

- Operating profit increased by 9.1% to ¥18,116 million, ordinary profit rose by 2.8% to ¥17,087 million, and net income attributable to owners of parent grew by 4.7% to ¥9,884 million, indicating growth in both revenue and profit.

- Interim net income per share stood at ¥54.80, and EBITDA was ¥24,269 million, an increase of 10.6% year-on-year.

- The forecast for the annual dividend for FY2026 remains ¥17.00 per share (¥8.50 for Q2-end, ¥8.50 for fiscal year-end), with no revisions from the latest public forecast.

- The full-year consolidated earnings forecast for FY2026 is maintained, projecting revenue of ¥424,000 million (an 8.6% increase year-on-year) and operating profit of ¥33,500 million (a 6.1% increase year-on-year), with no changes from the previous forecast.

🤖 AI Perspective

U-NEXT Holdings demonstrated solid financial performance in the second quarter of its fiscal year ending August 2026, with growth across key revenue and profit metrics. This suggests that the company’s diversified business portfolio, including content distribution and solutions for businesses, may be effectively contributing to stable earnings and expansion. The decision to maintain the full-year earnings forecast could indicate management’s confidence in their current strategic initiatives and market positioning.

3260|エスポア

—

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- ESPAC Co., Ltd. (Code: 3260, Nagoya Stock Exchange NEXT Market) announced on April 13, 2026, a delay in the disclosure of its financial results for the fiscal year ending February 2026.

- The company will be unable to disclose the results within 45 days after the fiscal year-end, as originally planned.

- The reason for the delay is that the auditing firm has requested additional confirmation regarding revenue recognition for certain transactions related to the February 2026 financial statements.

- ESPAC stated that responding to the additional procedures requested by the auditing firm, including submission of relevant documents and verification with related parties, and ongoing discussions with the auditor, will require an unspecified amount of time.

- The company currently anticipates disclosing the financial results on April 20, 2026, but will make a prompt announcement once the date is finalized.

- ESPAC also stated its commitment to strengthening its internal accounting systems and enhancing collaboration with its auditing firm to prevent any recurrence of such issues.

🤖 AI Perspective

A delay in financial results disclosure can be a significant point of interest for investors, particularly when it stems from an auditor’s request for additional confirmation on revenue recognition. Such situations may suggest increased scrutiny over the company’s accounting practices and internal controls. The company’s stated commitment to strengthening its internal accounting systems and improving auditor collaboration indicates an awareness of the need for improved transparency and governance.

464A|G-QPSHD

2787.0

▼ -1.59%

📎 Source:G-QPSHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-QPSHD reported its Q3 FY2026 consolidated cumulative results (June 1, 2025, to February 28, 2026), with net sales of ¥1,611 million, operating loss of ¥1,450 million, ordinary loss of ¥182 million, and net loss attributable to owners of parent of ¥187 million.

- As of the end of the same period, consolidated financial position showed total assets of ¥23,284 million, net assets of ¥15,034 million, and an equity ratio of 64.6%.

- The company revised its full-year consolidated earnings forecast for FY2026, projecting net sales of ¥4,000 million, operating loss of ¥1,200 million, ordinary income of ¥600 million, and net income attributable to owners of parent of ¥500 million.

- Four commercial small SAR satellites (QPS-SAR 11 “Yamatsumi-I” on June 12, 12 “Kushinada-I” on August 5, 14 “Yachihoko-I” on November 6, and 15 “Sukunami-I” on December 21) were successfully launched in 2025. Commercial operation of QPS-SAR 5 “Tsukuyomi-I” also recommenced, bringing the total operational satellites to nine.

- Financial foundation for satellite constellation construction was strengthened through a syndicated loan agreement on January 30, 2026, and a third-party allotment on March 23, 2026.

🤖 AI Perspective

- As G-QPSHD was established on December 1, 2025, direct year-on-year comparisons are not available for this inaugural quarterly report.

- Despite reporting a net loss, the successful satellite launches, recommencement of operations, and strengthening of the financial base suggest the company is in a foundational phase of building its business for future growth.

- The revised full-year forecast, projecting a return to net profit, could indicate that ongoing business developments are expected to translate into improved financial performance, making future progress worth monitoring.

7815|東京ボード工業

373.0

▲ +1.08%

📎 Source:東京ボード工業 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tokyo Board Industries, Inc. (Code: 7815 TSE Standard) announced a delay in its financial results announcement for the fiscal year ending February 2026.

- The original scheduled date for the announcement of the “Financial Report for the Fiscal Year Ending February 2026” was April 13, 2026.

- The new scheduled date for the announcement is April 20, 2026.

- The reason for the delay is that careful examination of certain accounting treatments is required, necessitating additional time to finalize the financial figures.

🤖 AI Perspective

A delay in financial results announcements can typically introduce a degree of uncertainty for investors. The specified reason, “careful examination of certain accounting treatments,” suggests that the nature of these accounting matters may be a point of focus in the forthcoming disclosure. However, the relatively short one-week postponement could also indicate that the issue may be limited in scope.

3030|ハブ

959.0

▼ -1.03%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- HUB Co., Ltd. reported non-consolidated financial results for the fiscal year ended February 2026 (March 1, 2025, to February 28, 2026), with net sales of ¥11,335 million (up 6.6% year-on-year), operating income of ¥534 million (up 17.9%), ordinary income of ¥528 million (up 19.8%), and net income of ¥609 million (up 36.7%).

- As of the end of the fiscal year, total assets were ¥6,653 million (up ¥469 million from the previous fiscal year-end), net assets reached ¥3,407 million (up ¥512 million), and the equity ratio stood at 50.7%.

- The company declared a year-end dividend of ¥11 per share for the fiscal year ended February 2026 (total annual dividend), comprising an ordinary dividend of ¥10 and a special dividend of ¥1.

- For the fiscal year ending February 2027 (March 1, 2026, to February 28, 2027), the company projects full-year net sales of ¥12,000 million (up 5.9% year-on-year), operating income of ¥600 million (up 12.3%), ordinary income of ¥580 million (up 9.8%), and net income of ¥330 million (down 45.9%).

- During the fiscal year, three new stores were opened: “HUB JEF UNITED PUB Perie Chiba Ekinaka Store,” “HUB Amu Plaza Miyazaki Store” (first in Miyazaki Prefecture), and “HUB Toyama Maroot Store” (first in Toyama Prefecture), increasing the total store count to 110. New store openings are also planned for the Shizuoka Station area and Oita Station area in the next fiscal year.

🤖 AI Perspective

The fiscal year ended February 2026 saw growth in sales and all profit metrics, with a notable 36.7% increase in net income, suggesting positive effects from new store openings and existing store initiatives under the “SmasH47” strategy. However, while sales and operating/ordinary income are projected to rise for the fiscal year ending February 2027, the forecast indicates a significant year-on-year decrease in net income, which investors may wish to monitor for further explanation of contributing factors.

4920|日本色材

1100.0

▲ +3.48%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the consolidated fiscal year ended February 2026, Shikizai reported net sales of ¥16,643 million, representing a 5.6% decrease from the previous year.

- Consolidated operating profit was ¥180 million (down 63.2% year-on-year), and consolidated ordinary profit was ¥151 million (down 58.6% year-on-year).

- Net profit attributable to owners of the parent increased by 55.1% year-on-year, reaching ¥335 million.

- The annual dividend per share was set at ¥30.00, an increase of ¥10.00 from ¥20.00 in the prior year.

- For the fiscal year ending February 2027, the company forecasts consolidated net sales of ¥18,361 million (up 10.3% year-on-year), operating profit of ¥394 million (up 118.9% year-on-year), and net profit attributable to owners of the parent of ¥187 million (down 44.0% year-on-year).

🤖 AI Perspective

- The significant increase in net profit attributable to owners of the parent, despite decreases in net sales, operating profit, and ordinary profit, may suggest a shift in the company’s profit structure that could attract investor scrutiny.

- While the forecast for the next fiscal year indicates a substantial recovery in sales and operating profit, the projected decline in net profit attributable to owners of the parent could be a key point for investors to monitor for underlying reasons.

- The increase in the annual dividend may be viewed as a positive signal regarding the company’s commitment to shareholder returns.

2303|ドーン

2711.0

▼ -1.13%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Dawn Inc. (2303) resolved to implement a stock split and a partial amendment to its Articles of Incorporation at a Board of Directors meeting held on April 13, 2026.

- The stock split will be executed at a ratio of 2 shares for every 1 share of common stock, with May 31, 2026, designated as the record date and June 1, 2026, as the effective date.

- Following the split, the total number of outstanding shares will increase from 3,300,000 to 6,600,000.

- A partial amendment to Article 6 of the Articles of Incorporation will also be made, changing the total number of authorized shares from 9,000,000 to 18,000,000, effective June 1, 2026.

- There will be no change in the amount of stated capital as a result of this stock split.

🤖 AI Perspective

This stock split is announced with the objective of lowering the per-unit investment amount, thereby creating an environment where more investors can invest in the company’s shares. This action may contribute to enhancing stock liquidity and expanding the investor base. Generally, stock splits are considered a measure to improve accessibility for individual investors.

3323|レカム

90.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Recomm Inc.’s subsidiary, Recomm Business Solutions (Dalian) Co., Ltd. (RBD), announced on April 13, 2026, that its annual financial results for the fiscal year ended December 31, 2025 (January 1, 2025 – December 31, 2025) have been finalized. This information is based on public disclosures made by RBD, which is listed on China’s NEEQ market.

- For FY2025, consolidated revenue was 44,744,870 Yuan, a 4.3% decrease year-on-year. However, operating profit increased by 4.1% to 2,837,568 Yuan, ordinary profit rose by 5.7% to 2,865,236 Yuan, and net profit for the period increased by 0.1% to 2,577,301 Yuan. The gross profit margin improved by 1.3 percentage points to 40.1% from the previous year.

- By segment, BPO outsourcing revenue decreased by 11.2% year-on-year to 30,538,900 Yuan. In contrast, IT equipment sales increased by 46.4% to 1,516,469 Yuan, LED sales grew by 2.8% to 11,194,314 Yuan, and SPACECOOL sales newly recorded 1,352,001 Yuan.

- Consolidated total assets decreased by 15.7% to 33,318,644 Yuan, and consolidated net assets also declined by 15.7% to 27,073,146 Yuan. Operating cash flow increased by 22.9% to 3,723,378 Yuan.

- As RBD’s fiscal year (December end) differs from Recomm’s consolidated fiscal year (September end), this information is not yet reflected in Recomm’s consolidated financial statements. Recomm has stated that it will make appropriate disclosures if it determines that an impact on its consolidated earnings forecast will arise.

🤖 AI Perspective

RBD’s FY2025 results indicate that while revenue saw a decline, operating and net profits increased, which may suggest improvements in profitability or cost efficiency, possibly driven by an enhanced gross profit margin and reduced selling, general, and administrative expenses. A shift in the business portfolio could be observed, with growth in IT equipment and LED sales, alongside contributions from new SPACECOOL sales, offsetting a decrease in the core BPO outsourcing segment. Investors will likely monitor future disclosures from Recomm concerning how these results will be incorporated into its consolidated financial forecasts.

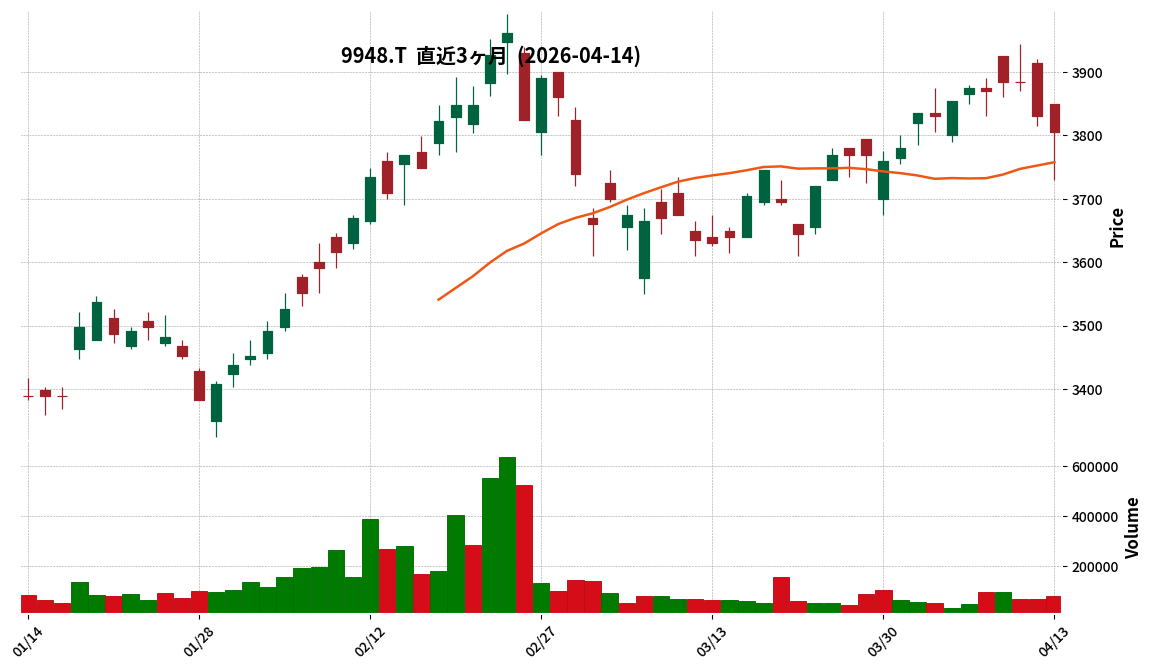

9948|アークス

3805.0

▼ -0.65%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended February 2026, ARCS Group reported consolidated net sales of ¥626.9 billion and operating income of ¥17.6 billion, marking new record highs. This represents a 3.1% increase in net sales and a 10.6% increase in operating income year-over-year.

- Existing store sales grew by 2.9% year-over-year, with existing store customer count increasing by 0.4%. This growth was attributed to the strengthening of local products, deli-related offerings, and sales of rice at competitive prices.

- The gross profit margin improved by 0.1 percentage points to 25.2% year-over-year. Selling, general, and administrative (SG&A) expenses were controlled to ¥140.1 billion, a 2.3% increase year-over-year, remaining within budget.

- The forecast for the fiscal year ending February 2027 projects new record highs with net sales of ¥648.0 billion and operating income of ¥18.0 billion. The company plans to open 4 new stores and renovate 20 stores, aiming for a 3.5% increase in existing store sales.

- In terms of shareholder returns, the annual dividend for FY2026/2 was ¥82 per share (¥41 interim, ¥41 year-end), marking the sixth consecutive year of dividend increases. ARCS also executed a share repurchase of ¥2.29 billion, and forecasts an annual dividend of ¥82 for FY2027/2.

🤖 AI Perspective

The strong performance in FY2026/2 appears to be driven by effective cost management through supply chain integration and SG&A expense control, alongside strategies to attract customers through competitive pricing in response to inflation. The FY2027/2 forecast, targeting new record highs, highlights strategic investments in new stores and renovations, coupled with initiatives such as AI-driven ordering and multi-skilling for employees to enhance productivity. The consistent dividend increases and the target dividend payout ratio of 40% suggest a commitment to enhancing shareholder value.

1407|ウエストHD

1808.0

▼ -2.53%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- West Holdings Co., Ltd. announced its consolidated financial results for the second quarter (interim) of the fiscal year ending August 2026.

- For the interim period (September 1, 2025 to February 28, 2026), consolidated net sales increased by 2.1% year-on-year to 15,180 million yen. Operating profit decreased by 9.5% to 1,301 million yen, ordinary profit decreased by 49.4% to 563 million yen, and net profit attributable to owners of the parent decreased by 34.6% to 357 million yen.

- By segment, the Renewable Energy Business recorded net sales of 8,085 million yen (down 29.0% year-on-year) and an operating loss of 150 million yen.

- In contrast, the Storage Battery Business, which commenced full-scale operations in the fiscal year ending August 2025, recorded sales of 3,046 million yen and an operating profit of 911 million yen.

- The full-year consolidated earnings forecast for the fiscal year ending August 2026 (September 1, 2025 to August 31, 2026) remains unchanged from the most recently announced figures: net sales of 54,460 million yen (up 15.3% year-on-year), operating profit of 11,376 million yen (up 31.6%), ordinary profit of 9,676 million yen (up 21.5%), and net profit attributable to owners of the parent of 6,602 million yen (up 23.2%).

🤖 AI Perspective

While revenue increased in the interim period, profits declined. This appears to be influenced by non-FIT solar power plant development sales in the Renewable Energy Business falling short of plans. Conversely, the Storage Battery Business, which began full-scale operations, made a significant contribution, suggesting an ongoing shift in the business portfolio. The unchanged full-year earnings forecast might indicate the company’s expectation of a performance recovery in the latter half of the fiscal year.

8011|三陽商

4025.0

▲ +0.12%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sanyo Shokai Co., Ltd. reported consolidated financial results for the fiscal year ended February 2026, with net sales of ¥58,448 million (down 3.4% year-on-year), operating profit of ¥1,298 million (down 52.2%), and ordinary profit of ¥1,436 million (down 49.2%).

- Profit attributable to owners of parent increased by 2.7% to ¥4,113 million, and the annual dividend per share was raised to ¥139 from ¥129 in the previous fiscal year.

- For the fiscal year ending February 2027, the company forecasts consolidated net sales of ¥60,000 million (up 2.7% year-on-year), operating profit of ¥2,100 million (up 61.7%), ordinary profit of ¥2,000 million (up 39.3%), and profit attributable to owners of parent of ¥4,020 million (down 2.3%).

- A stock split at a ratio of three shares for every one common share will be implemented, effective September 1, 2026. This adjustment means the forecast for basic earnings per share for the fiscal year ending February 2027 is ¥136.13 (after considering the stock split).

🤖 AI Perspective

The financial results for FY2026/2 indicate a decline in net sales and operating/ordinary profits, but an increase in net profit attributable to owners of parent and a higher annual dividend. The FY2027/2 forecast suggests significant profit growth, however, the announced stock split requires careful consideration when comparing per-share metrics. This stock split could potentially broaden the investor base.

9837|モリト

1922.0

▲ +0.10%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Morito Co., Ltd. announced its consolidated financial results for the first quarter of the fiscal year ending November 2026 (December 1, 2025 to February 28, 2026).

- Net sales reached JPY 16,681 million (up 37.2% year-on-year), operating profit JPY 1,038 million (up 68.1%), ordinary profit JPY 1,046 million (up 51.8%), and profit attributable to owners of parent JPY 660 million (up 9.8%).

- Key drivers for the sales increase include the consolidation of Ms.ID Co., Ltd. and Mitsuboshi Corporation, as well as strong performance in health-related products, game-related products, and kitchen equipment related service businesses.

- As of the end of the first quarter, total assets stood at JPY 57,210 million (up JPY 1,711 million from the previous consolidated fiscal year-end), net assets at JPY 40,526 million (up JPY 694 million), and the equity ratio was 70.8%.

- There are no revisions to the consolidated full-year earnings forecast for the fiscal year ending November 2026 or the annual dividend forecast of JPY 72.00 per share.

🤖 AI Perspective

Morito’s first quarter results indicate substantial year-on-year growth in both net sales and operating profit. This performance appears to be driven by the consolidation of acquired companies and robust performance in specific business segments. Despite the noted market uncertainties, the company’s diversified business portfolio may be contributing to risk mitigation, making future quarterly developments worth monitoring.

3930|G-はてな

1072.0

▲ +1.61%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hatena Co., Ltd. (TSE Growth, code: 3930) resolved on April 14, 2026, to implement a special shareholder benefit to commemorate its 10th anniversary of listing.

- Eligible shareholders are those holding 3 (300) or more units of the company’s shares as recorded in the shareholder register as of the record date of July 31, 2026, regardless of continuous holding period.

- The special shareholder benefit consists of a digital gift® worth JPY 25,000, provided by Digital Plus Co., Ltd., to be presented to eligible shareholders.

- The digital gifts are scheduled for delivery in October 2026, to be enclosed with the convocation notice for the General Meeting of Shareholders, with selection made via a dedicated website. Exchange options include PayPay Money Light, Amazon Gift Card, and Bitcoin, among others.

- This 10th-anniversary special shareholder benefit is a one-time offering, though the company states it will continue to consider enhancing shareholder returns.

🤖 AI Perspective

This one-time special shareholder benefit may serve to express gratitude to shareholders and enhance the investment appeal of Hatena stock following its 10th anniversary of listing. The offering of a JPY 25,000 digital gift for holding 300 shares or more could attract short-term investor interest. However, as the benefit is explicitly stated as “one-time,” the company’s future long-term shareholder return policies will be a key area for investors to monitor.

7608|SKジャパン

773.0

▼ -1.65%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SK Japan announced its consolidated financial results for the fiscal year ended February 2025 (FY2025). Net sales reached JPY 16,232 million (up 22.3% year-on-year), operating profit was JPY 1,859 million (up 51.3%), ordinary profit was JPY 1,882 million (up 49.3%), and profit attributable to owners of parent was JPY 1,333 million (up 43.5%).

- Diluted earnings per share were JPY 79.54 (calculated assuming the stock split effective March 1, 2025).

- The annual dividend for FY2025 was JPY 47.00 per share, an increase of JPY 20.00 from the previous year’s JPY 27.00.

- For the fiscal year ending February 2026 (FY2026), the company forecasts consolidated net sales of JPY 17,000 million (up 4.7% year-on-year), operating profit of JPY 1,950 million (up 4.8%), and profit attributable to owners of parent of JPY 1,370 million (up 2.7%).

- The annual dividend forecast for FY2026, considering the 1-for-2 stock split effective March 1, 2025, is JPY 24.00 per share (JPY 12.00 interim, JPY 12.00 year-end). Without considering the stock split, the annual dividend would be JPY 48.00 per share.

🤖 AI Perspective

SK Japan’s FY2025 results show significant growth across sales and all profit metrics, suggesting a robust performance compared to prior periods. The substantial increase in the annual dividend may indicate a commitment to shareholder returns. The company’s forecast for continued sales and profit growth in FY2026 could suggest a confident outlook for its ongoing business trajectory.

7805|プリントネット

757.0

▲ +1.34%

📎 Source:プリントネット Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the second quarter (interim) of the fiscal year ending August 2026 (September 1, 2025 – February 28, 2026), Printnet reported net sales of ¥4,574 million, marking a 1.7% increase compared to the prior interim period.

- Operating profit surged by 26.5% to ¥319 million, and ordinary profit increased by 26.2% to ¥320 million.

- Interim net profit, however, decreased by 7.0% to ¥216 million.

- Regarding the financial position, the equity ratio at the end of the second quarter of FY2026 improved to 55.9%, up 0.3 percentage points from 55.6% at the end of the previous fiscal year.

- The full-year forecast for FY2026 remains unchanged, projecting net sales of ¥9,867 million (up 7.1% year-on-year) and net profit of ¥373 million (down 13.8% year-on-year) from the most recently published figures.

🤖 AI Perspective

Investors may note the double-digit growth in operating and ordinary profits despite a modest increase in net sales, while interim net profit recorded a decline. This situation could suggest a focus on profitability improvement strategies, as indicated by increased sales from non-major clients in the net printing e-commerce segment, offsetting a decrease in major client sales. The unchanged full-year outlook implies that the company anticipates a specific performance trajectory for the second half of the fiscal year, which will be worth monitoring, particularly concerning net profit recovery.

8614|東洋証

660.0

▼ -0.60%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Toyo Securities announced its preliminary consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026) on April 14, 2026. The official announcement is scheduled for April 28, 2026.

- Consolidated operating revenue reached ¥13,576 million, an increase of 20.2% year-on-year.

- Consolidated operating profit surged by 307.2% year-on-year to ¥2,827 million, while consolidated ordinary profit increased by 214.9% to ¥3,266 million.

- Net profit attributable to owners of parent was ¥3,944 million, up 48.6% from the previous fiscal year.

- The company attributed the significant increase in operating and ordinary profits to higher commissions from investment trusts (subscription and agency fees), domestic and Chinese stock brokerage fees, and solution-related revenues, noting that a decrease in gain on sale of investment securities (extraordinary income) led to a lower growth rate for net profit attributable to owners of parent compared to operating and ordinary profits.

🤖 AI Perspective

- The preliminary results for Toyo Securities’ FY2026/3 highlight a substantial year-on-year increase in both consolidated operating and ordinary profits, which may suggest a favorable market environment for brokerage activities and strong performance in their core fee-based businesses.

- However, the comparatively lower growth in net profit attributable to owners of parent, as explained by a decrease in extraordinary income from investment securities sales, could indicate a shift in profit drivers from one-off gains to recurring revenue.

- As a financial instruments business, Toyo Securities’ performance is sensitive to market fluctuations, making the sustainability of these revenue streams and the impact of future market conditions key areas for investors to monitor.

9381|エーアイテイー

2169.0

▼ -1.18%

📎 Source:エーアイテイー Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- AIT Co., Ltd. reported consolidated financial results for the fiscal year ended February 2026, with operating revenue of ¥58,399 million (up 5.0% year-on-year), operating profit of ¥4,196 million (up 3.0%), ordinary profit of ¥4,680 million (up 3.3%), and net profit attributable to owners of parent of ¥3,175 million (up 4.2%).

- The annual dividend for the fiscal year ended February 2026 was ¥100.00 (compared to ¥80.00 for the previous period).

- For the fiscal year ending February 2027, the company forecasts consolidated operating revenue of ¥62,500 million (up 7.0% year-on-year), operating profit of ¥4,530 million (up 7.9%), ordinary profit of ¥4,960 million (up 6.0%), and net profit attributable to owners of parent of ¥3,390 million (up 6.7%).

- The forecast for the annual dividend for the fiscal year ending February 2027 is ¥110.00.

- Key factors contributing to the results include expanded international cargo transport volumes, increased orders for ancillary import/export services, robust movement of apparel-related goods, a significant increase in customs clearance orders (152,656 cases, up 9.6% year-on-year), and higher sea freight rates in the first half of the period.

🤖 AI Perspective

The reported financial results for the fiscal year ended February 2026 show positive growth across all key revenue and profit metrics, which may suggest a stable performance in its international cargo transport business. The increase in both cargo handling volumes and customs clearance orders could indicate effective business expansion strategies. Furthermore, the optimistic outlook for the upcoming fiscal year, including projected increases in revenue, profit, and dividends, might be viewed by investors as a signal of management’s confidence in sustained growth.

6521|G-オキサイド

5280.0

▲ +4.55%

📎 Source:G-オキサイド Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended February 2026, consolidated net sales reached ¥10,040 million, marking a 19.6% increase year-on-year.

- Consolidated operating profit for the period was ¥542 million (up 329.7% year-on-year), and ordinary profit was ¥674 million (up 192.7% year-on-year). The net loss attributable to owners of parent narrowed to ¥538 million, compared to a loss of ¥2,703 million in the prior fiscal year.

- Sales in the Semiconductor business amounted to ¥5,002 million (up 6.3% year-on-year), Healthcare business ¥1,997 million (up 62.9% year-on-year), and New Domains business ¥3,040 million (up 23.4% year-on-year), with each segment achieving record-high sales.

- A significant change in the scope of consolidation occurred in February 2026, with the exclusion of Raicol Crystals Ltd.

- The consolidated earnings forecast for the fiscal year ending February 2027 projects net sales of ¥9,828 million (down 2.1% year-on-year), operating profit of ¥933 million (up 71.9% year-on-year), ordinary profit of ¥788 million (up 16.9% year-on-year), and a net profit attributable to owners of parent of ¥597 million, indicating a return to profitability.

🤖 AI Perspective

The significant increase in sales and operating profit, along with a narrower net loss, are key highlights from the FY2026/2 results. The forecast for FY2027/2, projecting a return to net profitability, may suggest a positive trajectory for the company’s financial performance. Record-high sales across the Semiconductor, Healthcare, and New Domains businesses indicate diversified growth drivers contributing to the overall improvement.

3935|エディア

685.0

▼ -2.84%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Edia Corporation reported consolidated financial results for the fiscal year ended February 2026, with net sales of JPY 4,659 million (up 29.2% year-on-year), operating profit of JPY 444 million (up 69.2%), ordinary profit of JPY 416 million (up 75.4%), and net profit attributable to owners of parent of JPY 476 million (up 103.5%).

- The year-end dividend for the fiscal year was increased to JPY 13.00 from JPY 7.00 in the previous fiscal year, making the total annual dividend JPY 13.00.

- For the fiscal year ending February 2027, the company forecasts consolidated net sales of JPY 5,300 million (up 13.8% year-on-year), operating profit of JPY 550 million (up 23.9%), ordinary profit of JPY 540 million (up 29.8%), and net profit attributable to owners of parent of JPY 500 million (up 5.0%).

- Performance in the fiscal year was primarily driven by its IP business, particularly online lottery services “Marukuji” and “Kujicolle,” with game services and e-books also performing well.

- The company launched a new animation business during the consolidated fiscal year, aiming to promote anime adaptation of its own IPs and acquire new IPs through investment in production committees.

🤖 AI Perspective

- Edia’s significant growth in key profit metrics for FY2026/2 suggests strong operational performance, largely attributable to its robust IP business.

- The improved equity ratio of 58.0% indicates enhanced financial stability, although the decrease in total assets due to lower cash and deposits may warrant attention regarding future cash flow management.

- The positive outlook for FY2027/2, coupled with the new animation business venture, could indicate a strategic expansion aimed at further maximizing IP value and revenue streams.

7065|ユーピーアール

931.0

▲ +1.86%

📎 Source:ユーピーアール Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- UPR Corporation has announced its consolidated financial results for the second quarter (interim) of the fiscal year ending August 2026.

- Consolidated cumulative performance shows net sales of ¥7,632 million (up 1.7% year-on-year), operating profit of ¥581 million (up 245.5%), ordinary profit of ¥808 million (up 139.9%), and net income attributable to owners of parent of ¥514 million (up 257.9%).

- EBITDA reached ¥2,153 million (up 16.2% year-on-year).

- There are no revisions to the consolidated full-year performance forecast for the fiscal year ending August 2026, nor to the annual dividend forecast (¥35.00 for year-end, total ¥35.00).

- Regarding changes in accounting estimates, the useful life of plastic pallets was extended by one year from the beginning of the current fiscal period, resulting in reduced depreciation expenses and a positive impact on profit.

🤖 AI Perspective

The announced interim results indicate a significant improvement in profitability, with operating, ordinary, and net profits showing substantial increases despite a modest rise in net sales. This suggests that the company’s efforts in improving cost efficiency, alongside the accounting estimate change regarding pallet depreciation, have had a material impact. The robust demand for integrated palletization in the logistics segment and steady performance in solution services for existing clients appear to be contributing factors to the stable business foundation.

1430|ファーストコーポ

1069.0

▲ +0.19%

📎 Source:ファーストコーポ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- First Corporation’s Board of Directors resolved on April 14, 2026, to revise its consolidated financial forecast and per-share dividend forecast for the fiscal year ending May 2026.

- The full-year consolidated net sales forecast was revised downward by 9.3% from the previously announced ¥40,000 million to ¥36,300 million.

- Conversely, the operating profit forecast was revised upward by 3.6% from ¥2,800 million to ¥2,900 million, ordinary profit by 6.7% from ¥2,530 million to ¥2,700 million, and profit attributable to owners of parent by 5.2% from ¥1,750 million to ¥1,840 million.

- The downward revision in net sales is attributed to the real estate business focusing on high-profit margin projects, resulting in fewer-than-expected sales of development land.

- The upward revisions in profits stem from successful negotiations for improved profitability in the construction business and the accumulation of high-margin contracts in the real estate business.

- The year-end dividend forecast was revised upward by ¥2 to ¥46.00 per share, from the previous forecast of ¥44.00, in conjunction with the upward revision of the full-year consolidated earnings forecast.

🤖 AI Perspective

First Corporation’s latest announcement indicates a strategic emphasis on profitability, as evidenced by the downward revision in net sales alongside upward revisions in all key profit metrics. The improved profitability in the construction segment and the success in securing high-margin projects within the real estate business appear to be key drivers for the enhanced profit outlook. This stronger profit performance is noted as the basis for the increased year-end dividend.

209A|P-小野谷機工

780.0

▲ +0.00%

📎 Source:P-小野谷機工 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- P-小野谷機工 (209A) announced its consolidated interim results for the fiscal year ending August 2026 (September 1, 2025 – February 28, 2026), reporting net sales of ¥4,293 million (up 4.3% year-on-year) and operating profit of ¥317 million (up 2.7% year-on-year).

- Ordinary profit for the period was ¥310 million (down 7.7% year-on-year), and net profit attributable to owners of parent was ¥200 million (down 12.4% year-on-year). The decline in ordinary profit was due to the absence of a surrender value from insurance contracts, which had been recorded in the prior interim period.

- By segment, the Tire Service Equipment business recorded net sales of ¥2,517 million (up 5.4%) but operating profit of ¥162 million (down 4.1%). The Tire Manufacturing and Sales business reported net sales of ¥1,775 million (up 2.8%) and operating profit of ¥145 million (up 12.2%).

- As of the end of the interim consolidated accounting period, total assets stood at ¥10,266 million, net assets at ¥5,161 million, and the equity ratio at 50.3%.

- The full-year consolidated earnings forecast for the fiscal year ending August 2026 remains unchanged from the forecast announced on October 14, 2025.

🤖 AI Perspective

P-小野谷機工’s interim results for FY2026 show an increase in net sales and operating profit, but a decline in ordinary and net profit. This was primarily attributed to the absence of an insurance surrender value, which had contributed to profits in the prior interim period. The company’s decision to maintain its full-year earnings forecast suggests that management views the interim performance as consistent with its annual projections. While the Tire Manufacturing and Sales segment demonstrated strong performance, the Tire Service Equipment business saw sales growth but a decrease in operating profit due to rising costs, a trend that may warrant continued observation.

3892|岡山製紙

1665.0

▼ -0.12%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the third quarter of the fiscal year ending May 2026 (June 1, 2025 to February 28, 2026), Okayama Seishi reported non-consolidated net sales of ¥8,268 million (down 4.7% year-on-year), operating profit of ¥717 million (down 19.8%), ordinary profit of ¥848 million (down 14.7%), and net profit attributable to owners of parent of ¥618 million (down 9.2%).

- The decline in net sales was due to a decrease in paperboard sales volume compared to the prior year, while the profit reduction was attributed to lower sales and an increase in labor and other fixed costs.

- In terms of financial position, total assets at the end of the third quarter amounted to ¥18,656 million, an increase of ¥2,062 million from the end of the previous fiscal year. The primary driver for this increase was a ¥2,067 million rise in the valuation of investment securities.

- The self-equity ratio improved from 78.0% at the end of the previous fiscal year to 79.1%.

- The full-year forecast for the fiscal year ending May 2026 remains unchanged from the previously announced figures on July 14, 2025: net sales of ¥11,600 million (up 0.7% year-on-year), operating profit of ¥900 million (down 12.8%), ordinary profit of ¥1,000 million (down 12.9%), and net profit attributable to owners of parent of ¥700 million (down 12.4%).

🤖 AI Perspective

Okayama Seishi’s Q3 FY2026 results indicate a decrease in both sales and profits year-on-year, primarily influenced by a downturn in domestic paperboard demand and rising fixed costs. Conversely, the company’s financial position showed improvement, with total assets and net assets increasing, largely due to an appreciation in investment securities. This led to an enhanced self-equity ratio, suggesting sustained financial stability. The decision to maintain the full-year earnings forecast suggests management is prudently assessing the evolving market conditions and its progress toward initial targets.

4015|G-ペイクラウドHD

455.0

▲ +1.34%

📎 Source:G-ペイクラウドHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-PayCloud Holdings, Inc. announced its consolidated financial results for the second quarter of the fiscal year ending August 2026.

- For the six months ended February 28, 2026, consolidated net sales were ¥4,723 million (down 2.4% year-on-year), operating profit was ¥327 million (down 19.1%), and net profit attributable to owners of parent was ¥137 million (down 35.5%).

- By segment, the Cashless Service business recorded net sales of ¥1,925 million (up 2.1% year-on-year) and segment profit of ¥463 million (up 11.6%).

- The Digital Signage Related business reported net sales of ¥2,413 million (down 6.0% year-on-year) and segment profit of ¥330 million (down 12.8%), with the company stating that “delivery delays occurred for some customers.”

- The full-year consolidated earnings forecast for the fiscal year ending August 2026 remains unchanged from the most recently announced forecast, projecting net sales of ¥11,500 million and net profit attributable to owners of parent of ¥360 million.

🤖 AI Perspective

These results show a decline in overall revenue and profit for the interim period, yet segment-specific trends differ. The Cashless Service business demonstrates steady growth, while delivery delays in the Digital Signage Related business appear to have impacted overall performance. The unchanged full-year forecast could suggest that the company anticipates a recovery in the latter half of the fiscal year.

8887|シーラHD

419.0

▲ +1.70%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the nine months ended February 29, 2026 (Q3 FY2026), SYLA Holdings reported consolidated net sales of JPY 27,741 million, operating profit of JPY 2,376 million, and ordinary profit of JPY 1,539 million.

- Net income attributable to owners of parent was JPY 6,373 million. This figure includes a special gain from negative goodwill of JPY 7,909 million and a special loss from step acquisition of JPY 2,259 million, both resulting from the business integration with SYLA Technologies Co., Ltd.

- The consolidated full-year earnings forecast for FY2026 and the annual dividend forecast (totaling JPY 12.00) remain unchanged from the most recently announced projections.

- As of February 29, 2026, total assets stood at JPY 66,729 million, net assets at JPY 18,601 million, and the equity ratio at 26.6%.

- During the current cumulative quarter, SYLA Technologies Co., Ltd. was initially included in the scope of consolidation through a share exchange and subsequently excluded due to an absorption-type merger.

🤖 AI Perspective

SYLA Holdings began preparing consolidated quarterly financial statements from Q1 FY2026, thus no year-over-year comparisons are provided in this release. The significant net income attributable to owners of parent appears to be substantially influenced by the recorded special gain from negative goodwill. The comprehensive real estate business continues to be the primary revenue driver, while the real estate management business may be viewed as a core contributor to stable earnings.

3177|ありがとうS

3610.0

▲ +2.70%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the consolidated fiscal year ended February 2026, Arigato S reported net sales of JPY 11,398 million (up 7.4% year-on-year), operating profit of JPY 944 million (up 7.3%), and ordinary profit of JPY 1,033 million (up 8.3%), achieving increased revenue and profit.

- Net profit attributable to owners of the parent company amounted to JPY 492 million, representing a 2.2% decrease from the previous fiscal year.

- Earnings per share (EPS) were JPY 533.84.

- The year-end dividend was set at JPY 135.00 per share, with the total annual dividend also at JPY 135.00 (same as previous year). The forecast for FY2027/2 also projects an annual dividend of JPY 135.00 per share.

- The consolidated earnings forecast for FY2027/2 is JPY 11,398 million for net sales, JPY 944 million for operating profit, JPY 1,033 million for ordinary profit, and JPY 492 million for net profit attributable to owners of the parent, maintaining the same figures as the actual results for FY2026/2.

🤖 AI Perspective

- While Arigato S achieved growth in net sales, operating profit, and ordinary profit for FY2026/2, the slight decrease in net profit attributable to owners of the parent may suggest the influence of factors such as profit quality or tax implications.

- Maintaining the FY2027/2 consolidated earnings forecast at the same level as the FY2026/2 actual results could indicate a conservative outlook or a cautious stance by the company given future uncertainties.

- The marginal increase in the dividend payout ratio from 24.7% in the previous period to 25.3% may also be a point of interest for investors.

3536|アクサスHD

136.0

▲ +3.82%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Axas Holdings Co., Ltd. announced its consolidated financial results for the second quarter (interim period) of the fiscal year ending August 2026.

- Sales reached JPY 6,382 million (up 5.7% year-on-year for the interim period), and operating income was JPY 96 million (up 94.6% year-on-year).

- The company reported an ordinary loss of JPY 3 million (compared to JPY 50 million loss in the prior interim period) and a net loss attributable to owners of the parent of JPY 20 million (compared to JPY 100 million loss in the prior interim period), indicating a narrowed loss.

- The full-year consolidated earnings forecast (sales of JPY 13,172 million, operating income of JPY 432 million, and net income attributable to owners of the parent of JPY 250 million) remains unchanged from the most recently published forecast.

- During the interim period, Axas Holdings opened three new stores, including “Alex Sports Yamashiro Main Store” and two “O-Sake no Bijutsukan” franchise stores, bringing the total group store count to 41.

🤖 AI Perspective

- The reported increase in sales and substantial growth in operating income may suggest an improvement in the company’s business operations.

- The narrowing of the ordinary loss and net loss attributable to owners of the parent could indicate a positive trend in the company’s profitability.

- Maintaining the full-year earnings forecast might reflect management’s confidence in achieving its annual targets, which is a point worth monitoring for investors.

5078|セレコーポレーション

4870.0

▲ +1.46%

📎 Source:セレコーポレーション Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended February 2026, Cel Corporation reported consolidated net sales of ¥20,190 million (down 15.6% year-on-year), operating income of ¥1,692 million (down 16.2% year-on-year), and net income attributable to owners of parent of ¥1,147 million (down 19.0% year-on-year).

- As of the end of February 2026, the consolidated financial position showed a capital adequacy ratio of 85.9% (up 3.8 percentage points from the previous fiscal year-end), with net assets reaching ¥21,116 million (up ¥698 million from the previous fiscal year-end).

- The annual dividend per share for the fiscal year ended February 2026 was ¥135, maintained at the same level as the previous year.

- For the fiscal year ending February 2027, the company forecasts consolidated net sales of ¥23,580 million (up 16.8% year-on-year), operating income of ¥2,016 million (up 19.2% year-on-year), and net income attributable to owners of parent of ¥1,342 million (up 16.9% year-on-year).

- The forecast annual dividend per share for the fiscal year ending February 2027 is ¥160, an increase of ¥25 from the previous year.

🤖 AI Perspective

Cel Corporation’s FY2026/2 results showed a decline in sales and profits; however, the company maintained a high capital adequacy ratio of 85.9%. The forecast for FY2027/2 indicates a double-digit recovery in both sales and profits, alongside a projected increase in the annual dividend. This forward-looking guidance may suggest management’s confidence in improving business conditions and a commitment to shareholder returns.

3683|サイバーリンクス

1009.0

▲ +1.41%

📎 Source:サイバーリンクス Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Cyberlinks Co., Ltd. announced a partial correction to its “FY2025 Financial Results Presentation Material” on April 14, 2026.

- The reason for the correction was the discovery of an error in a portion of the content of the presentation material originally published on March 4, 2026.

- The correction specifically applies to page 55 of the “FY2025 Financial Results Presentation Material.”

- The detailed corrections are presented on page 55 of the disclosed correction document, showing both the “before correction” and “after correction” versions.

🤖 AI Perspective

Corrections to financial presentation materials are a critical aspect of ensuring transparent and accurate information for investors. This correction may suggest Cyberlinks’ commitment to maintaining high standards in its disclosures by rectifying identified inaccuracies in previously published material. Investors are advised to review page 55 of the official correction document for the precise details of the amendments.

5817|JMACS

1832.0

▲ +2.63%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- JMACS announced that its full-year performance for the fiscal year ending February 2026 exceeded the previously announced forecasts (published January 14, 2026).

- For FY2026, net sales reached ¥6,028 million against a forecast of ¥5,850 million (a 3.0% increase), and operating profit was ¥501 million against a forecast of ¥308 million (a 62.9% increase).

- Ordinary profit stood at ¥543 million compared to a forecast of ¥354 million (a 53.6% increase), and net income was ¥400 million against a forecast of ¥244 million (a 64.1% increase).

- The reasons for the discrepancy include minimizing the impact of raw material supply in the fourth quarter, strong sales for plant projects, robust sales of high value-added products, and improved manufacturing efficiency at factories, leading to better profit margins.

- The company decided to increase the per-share dividend for FY2026 from the previously forecasted ¥10.00 to ¥15.00, with an effective date of May 28, 2026.

🤖 AI Perspective

JMACS’s FY2026 results show a significant outperformance across all profit metrics, not just sales, compared to initial expectations. The substantial increases in operating, ordinary, and net income, each exceeding 50%, may suggest the effectiveness of operational efficiencies and strategic focus on high value-added products. The announcement of a dividend increase alongside the upward earnings revision could be viewed as a positive signal regarding the company’s commitment to shareholder returns.

6897|ツインバード

400.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- TWINBIRD Co., Ltd. (6897) reported its non-consolidated financial results for the fiscal year ended February 2026, with net sales of ¥8,998 million (down 10.5% year-on-year) and an operating loss of ¥855 million (compared to an operating profit of ¥4 million in the previous fiscal year).

- The company recorded an ordinary loss of ¥896 million (vs. ordinary profit of ¥42 million previously) and a net loss of ¥1,218 million (vs. net loss of ¥101 million previously).

- A decision was made to scale back the household refrigerator and washing machine business, leading to the recording of ¥60 million in disposal costs for products and parts and ¥356 million in inventory write-downs in the cost of sales.

- For the full fiscal year ending February 2027, the company forecasts net sales of ¥9,600 million (up 6.7% year-on-year), an operating profit of ¥100 million, an ordinary profit of ¥75 million, and a net profit of ¥45 million, indicating a projected return to profitability.

- The annual dividend is planned to remain ¥13.00 (interim ¥3.00, year-end ¥10.00) for both FY2026/2 (actual) and FY2027/2 (forecast).

7601|ポプラ

177.0

▲ +2.31%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the consolidated fiscal year ended February 2026, operating revenue was ¥11,654 million (down 3.1% YoY), operating profit was ¥134 million (down 64.2% YoY), and net profit attributable to parent company shareholders was ¥63 million (down 26.0% YoY).

- Consolidated cash flow from operating activities turned negative at ¥-405 million, compared to ¥433 million in the previous fiscal year.

- Same-store sales increased by 4.9% year-on-year, while sales in the frozen food segment grew by 234% year-on-year, and sales to external retailers increased by 197% year-on-year.

- For the consolidated fiscal year ending February 2027, the company forecasts operating revenue of ¥12,532 million (up 7.5% YoY), operating profit of ¥140 million (up 3.7% YoY), and net profit attributable to parent company shareholders of ¥72 million (up 13.5% YoY).

- The annual dividend for common shares is ¥0.00 for both the fiscal year ended February 2026 and the forecast for the fiscal year ending February 2027.

🤖 AI Perspective

Poplar’s FY2026/2 results appear to have been significantly impacted by decreased customer traffic due to consumer’s cost-saving mindset amid rising prices, along with soaring raw material (particularly rice and nori) and energy costs. However, strong growth in frozen prepared foods and sales to external retailers suggests strategic focus areas that could contribute to future profitability. Investors may monitor whether the company’s initiatives in these growing segments can successfully drive the projected revenue and profit increases for FY2027/2.

9601|松竹

11100.0

▼ -4.88%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Shochiku Co., Ltd. announced on April 14, 2026, a revision to its dividend forecast per share for the fiscal year ending February 2026 (160th fiscal year), as resolved by its Board of Directors.

- The year-end dividend forecast has been revised to a total of ¥40.00, comprising an ordinary dividend of ¥30.00 and a special dividend of ¥10.00, from the previously announced forecast (published April 14, 2025).

- The total annual dividend is also projected to be ¥40.00, with no dividend for the second quarter and a year-end dividend of ¥40.00.

- The reason for the revision is to return profits to shareholders, considering the financial results for the 160th fiscal year, the company’s profitability, strengthening of its management foundation, and future business development.

- This matter is scheduled to be deliberated at the Ordinary General Meeting of Shareholders, expected to be held in late May 2026, following a resolution by the Board of Directors regarding dividend distribution in late April 2026.

🤖 AI Perspective

- The revised dividend forecast, including a special dividend, suggests the company’s commitment to enhancing shareholder returns in the current fiscal year.

- The decision to include a special dividend, taking into account the performance of the 160th fiscal year, could be seen as an indication of robust financial performance.

- Investors may consider this adjustment as a signal of the company balancing its stable dividend policy with additional returns based on profitability.

3181|買取王国

966.0

▲ +5.69%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended February 2026, net sales reached ¥9,330 million (+19.3% YoY), operating profit was ¥507 million (+20.1% YoY), ordinary profit ¥546 million (+17.3% YoY), and net profit ¥358 million (+9.0% YoY).

- As of the end of February 2026, total assets were ¥5,957 million, net assets ¥3,400 million, and the equity ratio was 57.1%.

- During the fiscal year, Kaitori Okoku opened 7 “Tool Kaitori Okoku” stores, 2 “My Shu Sagarl” stores, and 2 “KOV” vintage clothing stores, in addition to renovating the Kaitori Okoku Takabata store into a hobby specialty store.

- The full-year forecast for the fiscal year ending February 2027 projects net sales of ¥10,012 million (+7.3% YoY), operating profit of ¥600 million (+18.5% YoY), ordinary profit of ¥610 million (+11.8% YoY), and net profit of ¥403 million (+12.6% YoY).

- The company forecasts an annual dividend of ¥11 per share for the fiscal year ending February 2027, an increase of ¥1 from the previous fiscal year.

🤖 AI Perspective

The financial results for FY2026 suggest that new store strategies and diversification of product categories contributed to business expansion. The focus on specialized business formats and new store openings appears to have driven overall growth, alongside increased sales at existing stores. The positive outlook for FY2027, including projected increases in earnings and dividends, could indicate an expectation for the continued success of these strategic initiatives.

5076|インフロニアHD

2094.5

▼ -0.17%

📎 Source:インフロニアHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Infroneer Holdings Corporation resolved to acquire all shares of Suing Co., Ltd. and make it a wholly-owned subsidiary, as decided by its extraordinary board meeting on April 14, 2026.

- The share transfer agreement was signed on the same date, with shares being acquired from Ebara Corporation, JGC Holdings Corporation, and Mitsubishi Corporation.

- Following this transaction, Suing will become a specified subsidiary of Infroneer HD.

- The acquisition’s stated rationale is to advance Infroneer HD’s strategy as a “Comprehensive Infrastructure Service Company” and strengthen its infrastructure operation business, a key growth segment.

- Suing operates in water treatment EPC & O&M and public-private partnership water utility management, reporting consolidated net sales of 82,937 million yen and consolidated operating profit of 6,817 million yen for the fiscal year ended March 2025.

🤖 AI Perspective

This acquisition appears to be a strategic move by Infroneer HD to bolster its infrastructure operation business, a core pillar of its “INFRONEER Medium-term Vision 2027” medium-term management plan. The integration of Suing’s leading water treatment engineering capabilities and maintenance bases with Infroneer HD’s project management expertise and civil engineering know-how could enable the group to offer comprehensive services across the entire water and wastewater lifecycle. Furthermore, leveraging Suing’s operational footprint may facilitate expansion into other public infrastructure management areas like roads and public facilities.

1887|日本国土開発

589.0

▼ -1.01%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nippon Kodo Kaihatsu announced on April 14, 2026, revisions to its consolidated and non-consolidated earnings forecasts and dividend forecast for the full fiscal year ending May 2026 (June 1, 2025 – May 31, 2026).

- For the consolidated forecast, net sales were revised upward from JPY 132,000 million to JPY 136,000 million, operating profit from JPY 5,000 million to JPY 6,000 million, and profit attributable to owners of parent from JPY 3,500 million to JPY 4,000 million.

- The non-consolidated forecast saw net sales revised from JPY 108,000 million to JPY 113,000 million, ordinary profit from JPY 4,100 million to JPY 5,100 million, and net income from JPY 2,700 million to JPY 3,800 million.

- The primary reasons for the earnings forecast revision are cited as the smooth progress of orders received and ongoing projects, particularly large-scale projects, in the construction business, which has led to a significant improvement in profitability, driven by highly profitable large-scale works.

- The year-end dividend forecast for the fiscal year ending May 2026 was revised upward by JPY 1.00 from the previous forecast of JPY 12.00 to JPY 13.00 per share, making the total annual dividend JPY 23.00 per share, including the interim dividend of JPY 10.00.

🤖 AI Perspective

The substantial upward revision in earnings, particularly a 20.0% increase in consolidated operating profit from the previous forecast, may suggest robust operational performance. The company attributes this to successful large-scale construction projects and improved profitability, which could indicate effective project management and favorable conditions within the construction sector. The accompanying increase in the dividend forecast may signal a commitment to enhancing shareholder returns.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

6142|富士精工

—

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended February 2026, consolidated net sales increased by 4.2% year-on-year to JPY 20,465 million.

- The company returned to profitability, reporting an operating profit of JPY 233 million (compared to an operating loss of JPY 368 million in the prior year), an ordinary profit of JPY 481 million (up 343.8% year-on-year), and a net profit attributable to owners of parent of JPY 692 million (compared to a net loss of JPY 3,761 million in the prior year).

- The annual dividend for the fiscal year ended February 2026 was JPY 15.00 per share.

- For the fiscal year ending February 2027, the consolidated performance forecast includes net sales of JPY 20,880 million (up 2.0% year-on-year), operating profit of JPY 300 million (up 28.3% year-on-year), and net profit attributable to owners of parent of JPY 80 million (down 88.5% year-on-year).

- The forecast for the annual dividend for the fiscal year ending February 2027 is JPY 50.00 per share (JPY 25.00 interim, JPY 25.00 year-end).

🤖 AI Perspective

FUJISEIKO’s consolidated results for FY2026/2 demonstrate a significant turnaround, moving from losses to profitability in both operating and net income. This suggests that the company’s business restructuring and productivity improvement initiatives may be yielding positive results. However, the forecast for FY2027/2 indicates a substantial decline in net profit attributable to owners of parent, despite projected increases in sales and operating profit, which could warrant closer monitoring by investors regarding the underlying drivers of future profitability.

6150|タケダ機械

3315.0

▼ -1.04%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Takeda Machinery announced its consolidated financial results for the third quarter of the fiscal year ending May 2026 (June 1, 2025 to February 28, 2026).

- Consolidated net sales amounted to ¥3,146 million (down 13.8% year-on-year), operating profit was ¥236 million (down 30.4%), ordinary profit ¥245 million (down 29.7%), and profit attributable to owners of parent was ¥163 million (down 28.9%).

- As of the end of the third consolidated accounting period, total assets stood at ¥7,398 million, net assets at ¥5,328 million, and the equity ratio was 72.0%.

- The consolidated earnings forecast for the full fiscal year ending May 2026, projecting net sales of ¥5,000 million and operating profit of ¥360 million, remains unchanged from the most recently announced forecast.

- By product category, sales of steel structure processing machines were ¥2,030 million (down 12.2% year-on-year) and circular saw cutting machines were ¥151 million (down 31.5%), while dies and molds increased by 3.3% to ¥315 million and services increased by 2.7% to ¥89 million.

🤖 AI Perspective

While the consolidated results for the third quarter showed a decline in both revenue and profit, the company’s decision to maintain its full-year earnings forecast may suggest an expectation for recovery in the final quarter. The challenging business environment, particularly the restraint on corporate capital expenditure, has been cited as a contributing factor. The impact of ongoing initiatives, such as the implementation of an ERP system for productivity enhancement, could be a key area for investors to monitor going forward.

7520|エコス

2415.0

▲ +1.22%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- ECOS Co., Ltd. resolved to increase its surplus dividend for the fiscal year ending February 28, 2026, at a Board of Directors meeting held on April 14, 2026.

- The per-share dividend for the fiscal year ending February 2026 will be ¥70.00, representing an increase of ¥5.00 from the previous fiscal year’s ¥65.00.

- The total dividend amount has been determined to be 786 million yen, with an effective date of May 21, 2026, and the source of funds being retained earnings.

- This matter is scheduled to be submitted for approval at the 61st Annual General Meeting of Shareholders, slated for May 20, 2026.

- The announced per-share dividend of ¥70.00 is consistent with the most recent dividend forecast issued on April 11, 2025.

🤖 AI Perspective

- This dividend increase suggests ECOS prioritizes shareholder returns as a key management policy, aiming for continued stable dividend payments.

- The ¥5.00 per-share increase from the previous fiscal year may reflect the company’s comprehensive consideration of its earnings and financial position, indicating a commitment to shareholder value.

- The alignment of the announced dividend amount with the latest forecast could be seen as an outcome in line with the company’s previous expectations for investors.

9778|昴

5670.0

▲ +0.53%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Subaru Co., Ltd. (Code: 9778) announced its non-consolidated financial results for the fiscal year ended February 2026 (March 1, 2025 – February 28, 2026) on April 14, 2026.

- For the reported period, net sales were JPY 3,375 million (down 2.2% year-on-year). Operating profit increased by 19.6% to JPY 112 million, and ordinary profit rose by 13.4% to JPY 121 million. However, net income for the period decreased by 29.6% to JPY 40 million.

- The company declared a year-end dividend of JPY 120.00 per share, with the annual dividend totaling JPY 120.00 per share.

- For the full fiscal year ending February 2027, Subaru forecasts net sales of JPY 3,459 million (up 2.4% year-on-year), operating profit of JPY 195 million (up 74.1%), ordinary profit of JPY 204 million (up 67.5%), and net income of JPY 133 million (up 232.5%).

- Key business developments during the fiscal year included the consolidation and closure of several group classrooms (Nishimiyakonojo, Kaseda, Makurazaki schools), the relocation of an individual tutoring classroom (Individual Tutoring Taniyama classroom), the opening of the New Nakayama School, and the launch of “Subaru Individual Tutoring Online.”

🤖 AI Perspective

The fiscal year ended February 2026, while experiencing a decline in net sales, showed an increase in both operating and ordinary profits, which may suggest improvements in operational efficiency. The decrease in net income, despite gains at the operating and ordinary levels, is a point worth further examination to understand the underlying factors. Looking ahead, the strong guidance provided for the fiscal year ending February 2027, projecting significant increases across all profit metrics, indicates the company anticipates substantial recovery and growth, potentially driven by strategic initiatives highlighted in the report.

3174|ハピネス&D

573.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Happiness & D Co., Ltd. announced its consolidated financial results for the second quarter of the fiscal year ending August 2026 (interim period: September 1, 2025, to February 28, 2026).

- Consolidated net sales amounted to ¥4,387 million (down 7.2% year-on-year), but operating profit turned positive to ¥4 million (compared to an operating loss of ¥81 million in the prior interim period).

- Ordinary loss narrowed to ¥16 million (from ¥97 million ordinary loss year-on-year), and net loss attributable to owners of parent significantly reduced to ¥36 million (from ¥205 million net loss year-on-year).

- In terms of consolidated financial position, the equity ratio improved from 2.7% at the end of August 2025 to 7.7%, and net assets increased from ¥198 million to ¥495 million.

- Regarding business strategies, the company promoted expanding sales of vintage products, strengthening jewelry and precious metal products (including the acquisition of a pure gold jewelry business), and initiating brand-name product purchasing. Happiness & D’s standalone existing store sales increased by 0.9% year-on-year, and gross profit by 9.5% year-on-year.

🤖 AI Perspective

The Q2 FY2026 results show an improvement in profitability, with operating profit turning positive and a substantial reduction in ordinary and net losses, despite a decrease in net sales. This improvement appears to be driven by restructuring efforts, including the closure of unprofitable stores, reduction in selling, general and administrative expenses, robust sales of vintage products and jewelry/precious metals (supported by rising gold prices), and a shift towards higher-margin product categories. The enhanced equity ratio also indicates a strengthening of the financial structure, suggesting that the business restructuring is progressing as planned.