📌 Today’s Highlights

Today we cover 35 IR announcements. Notable among them: P-フェリエスト (557A), G-アクセルスペース (402A), G-JRC (6224). Use the table of contents below to navigate to each company.

- 557A|P-フェリエスト

- 402A|G-アクセルスペース

- 6224|G-JRC

- 3557|G-U&C

- 4238|ミライアル

- 293A|P-BABY JOB

- 7524|マルシェ

- 3810|サイバーステップHD

- 3788|GMOGSHD

- 5250|GMOプライム

- 1716|第一カッター

- 2999|ホームポジション

- 3353|メディ一光G

- 3996|サインポスト

- 4382|HEROZ

- 4565|ネクセラファーマ

- 6995|東海理電

- 7815|東京ボード工業

- 8572|アコム

- 8708|アイザワ証G

- 7357|ジオコード

- 3492|R-MIRARTH

- 5244|G-jig.jp

- 7287|日本精機

- 8309|三井住友トラストG

- 1711|SDSHD

- 5721|エスクリプトエナジー

- 3024|クリエイト

- 7603|ジーイエット

- 9435|光通信

- 9993|ヤマザワ

- 2769|ヴィレッジV

- 8143|ラピーヌ

- 3260|エスポア

- 2160|G-GNI

557A|P-フェリエスト

—

▲ +0.00%

📎 Source:P-フェリエスト Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- P-FERIEST Inc. (Code: 557A) listed its shares on the TOKYO PRO Market of the Tokyo Stock Exchange today, April 20, 2026.

- For the full fiscal year ending August 31, 2026, the company forecasts consolidated net sales of JPY 840 million (up 52.8% year-on-year), operating profit of JPY 102 million (up 184.4% year-on-year), ordinary profit of JPY 115 million (up 171.4% year-on-year), and net profit of JPY 83 million (up 274.1% year-on-year).

- The company’s core businesses are SNS account management and short video production. The projected increase in sales is predicated on acquiring new clients, expanding services to existing clients (such as short video production and ad integration), an increase in the number of client companies and average client spend, and strengthened operational capacity.

- For the interim period of FY2026 (September 1, 2025 – February 28, 2026), the company reported net sales of JPY 389 million, operating profit of JPY 49 million, ordinary profit of JPY 49 million, and interim net profit of JPY 37 million.

- The forecast for the annual dividend per share for the fiscal year ending August 31, 2026, is JPY 0.00.

🤖 AI Perspective

- The announcement of the FY2026 full-year earnings forecast, coinciding with its listing, indicates substantial growth across all profit metrics, with net profit projected to increase by 274.1% year-on-year.

- The stated assumptions for the earnings forecast, including the expanding SNS marketing market and business growth driven by new client acquisition and service expansion, could suggest key drivers for the company’s future performance.

- A comparison with the interim results suggests that further business acceleration in the second half of the fiscal year may be anticipated to achieve the full-year targets.

402A|G-アクセルスペース

687.0

▼ -2.14%

📎 Source:G-アクセルスペース Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Axelspace Holdings Inc. (Code: 402A) announced on April 20, 2026, “Correction and Addition to ‘Q3 FY2026 Earnings Supplementary Materials’.”

- The correction was made due to numerical errors found in a graph on page 31 of the “Q3 FY2026 Earnings Supplementary Materials,” which was originally published on April 14, 2026. The corrected areas are marked with a red frame, and additional explanations for calculation methods are indicated by a blue frame.

- A new page, page 32, was added to the “Q3 FY2026 Earnings Supplementary Materials” to include a comparison of the full-year earnings forecast for FY2026. This addition aims to prevent misunderstandings arising from the aforementioned corrections.

- The corrected and appended “Q3 FY2026 Earnings Supplementary Materials” will be available on the company’s investor relations website (https://www.axelspacehd.com/ja/ir/).

🤖 AI Perspective

The announced corrections and additions to the earnings supplementary materials may suggest the company’s commitment to providing accurate and transparent information to its investors. Correcting numerical errors and adding details on full-year earnings forecasts could enhance investors’ ability to precisely assess the company’s financial performance. Such swift amendments in financial disclosures can be viewed as an effort to maintain high standards of information accuracy in investor relations.

6224|G-JRC

1205.0

▲ +1.86%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-JRC’s Q&A summary from the FY2026/2 full-year earnings briefing held on April 15, 2026, was released on April 20, 2026.

- The medium-term management plan is largely on track for the Conveyor, Environment & Energy, and Robot SI businesses.

- The company recognizes that the Environment & Energy company’s growth is accelerating beyond expectations due to the integration with Takahashi Kikan Kogyo.

- The new factory in Vietnam is projected to start mass production and shipment within the current fiscal year, targeting profitability in approximately three years.

- For the current fiscal year, the company prioritizes building a foundation for future growth through proactive upfront investments such as human capital and the Vietnam factory launch. Several M&A deals are also actively being considered for execution within the year.

🤖 AI Perspective

The planned full-scale operation of the new Vietnam factory and its long-term profitability target may indicate the company’s focus on expanding its overseas business and enhancing cost competitiveness. The accelerated growth of the Environment & Energy company through integration and the continued high growth of Robot SI could be key drivers for operating profit growth towards FY2028/2. The prioritization of upfront investments also suggests a strategic emphasis on long-term corporate value enhancement over immediate profit growth.

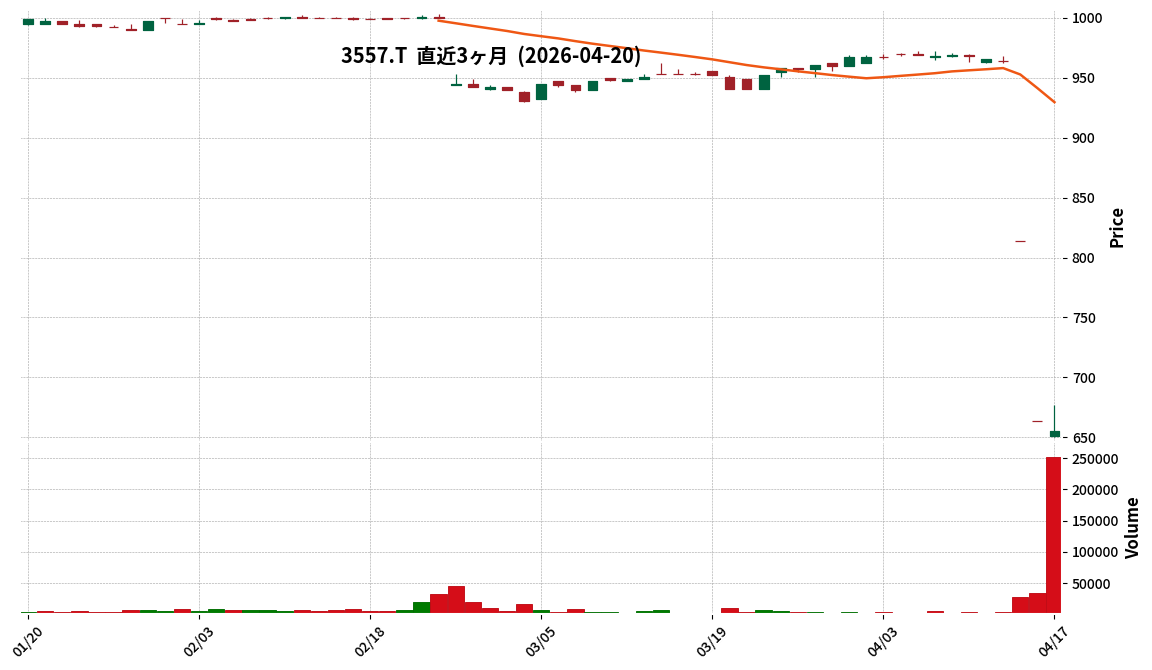

3557|G-U&C

655.0

▼ -1.36%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- United & Collective Co., Ltd. (Code: 3557) published key questions and answers regarding partial changes to its shareholder benefit program on April 20, 2026.

- The changes to the shareholder benefit program will be effective from December 1, 2026, applying to all shareholder benefits valid as of that date.

- Benefit tickets can be used at a rate of one ticket per JPY 1,000 (tax included) of the total bill, based on the amount after any other discounts are applied.

- These benefit tickets can be combined with other coupons, such as those from official apps.

- They are valid for course menus, all-you-can-drink options, and lunch menus at izakaya-style establishments, and can be used at all company-operated brand stores including “Teketeke,” “the 3rd Burger,” and “Shintaro.”

4238|ミライアル

1200.0

▼ -0.66%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- MiraiAl Corporation resolved on April 20, 2026, at its Board of Directors meeting, to acquire all outstanding shares of Funaya Marine Instrument Industry Co., Ltd., making it a consolidated subsidiary.

- Following this acquisition, Funaya Marine Instrument Industry’s subsidiaries, Funaya Keiki Seisakusho Co., Ltd. and Osaka Funaya Seiki Co., Ltd., will become MiraiAl’s sub-subsidiaries.

- Funaya Marine Instrument Industry, primarily engaged in the sale of marine navigation instruments such as magnetic compasses, is categorized under the “Social Infrastructure Business” field within MiraiAl’s Mid-term Growth Strategy 2028.

- The acquisition involves 9,611,505 shares, representing a 100% voting rights ownership. The share transfer is scheduled for April 30, 2026.

- The impact of this acquisition on MiraiAl’s consolidated financial results and financial position is currently under review, with the deemed acquisition date anticipated to be June 30, 2026.

🤖 AI Perspective

This M&A announcement by MiraiAl suggests an intention to establish a new pillar in the “Social Infrastructure Business” sector, diversifying beyond its current core semiconductor-related field, as part of its Mid-term Growth Strategy 2028 to expand and stabilize its business portfolio. The technical domain of “products functioning in special environments” shared by Funaya Marine Instrument Industry could potentially lead to synergy with MiraiAl’s existing technologies and foster new product development. Investors may find it worthwhile to monitor the forthcoming disclosures regarding the specific financial impact on consolidated results and the progress of this business diversification.

293A|P-BABY JOB

950.0

▲ +0.00%

📎 Source:P-BABY JOB Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- P-BABY JOB reported for the fiscal year ended February 2026, net sales of ¥4,104 million (up 44.9% year-on-year), operating profit of ¥313 million (up 142.6% year-on-year), and net profit attributable to parent company shareholders of ¥220 million (up 47.7% year-on-year).

- The number of contracted parents for its core diaper subscription service reached 127,773 (up 43.3% from the end of the previous fiscal year), and contracted facilities reached 9,300 (up 30.9% from the end of the previous fiscal year).

- In March 2025, the number of users of its diaper subscription service surpassed 100,000.

- The “Anyone Payment” cashless service for childcare facilities has been introduced in over 986 facilities.

- The company decided to pay a year-end dividend of ¥7.50 per share for the fiscal year ended February 2026, with a target payout ratio of 10%, scheduled for May 22, 2026.

🤖 AI Perspective

P-BABY JOB’s strong financial performance for the fiscal year ended February 2026 appears to be driven by the significant expansion of its core diaper and related subscription service. The substantial growth in both contracted parents and facilities suggests a robust market penetration. The announcement of its first dividend payment could also be viewed as a positive signal regarding the company’s commitment to shareholder returns.

7524|マルシェ

166.0

▼ -0.60%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Marche Co., Ltd. concluded a business alliance agreement with Sunrise Service Co., Ltd. on April 20, 2026, following a resolution by its Board of Directors on the same date.

- The alliance aims for Marche, primarily operating izakaya restaurants, to expand into the noodle business by leveraging the brand power and operational know-how of “Echigo Tsukemen,” developed by Sunrise Service.

- Under the agreement, Sunrise Service will provide Marche with know-how regarding product development, recipe management, store operations, and brand management for “Echigo Tsukemen,” and grant permission to use the brand and related trademarks.

- Marche will be responsible for the store development, operation, and sales management of “Echigo Tsukemen” in the Western Japan area, utilizing the provided know-how and trademark usage permission.

- Sunrise Service Co., Ltd. is a wholly-owned subsidiary of TempoS Holdings Co., Ltd., which is identified as a related party to Marche.

🤖 AI Perspective

This business alliance appears to be a strategic move for Marche to diversify its revenue streams by entering the noodle business, building on its core izakaya operations. The utilization of the established “Echigo Tsukemen” brand know-how may suggest an approach to minimize initial risks while pursuing business expansion. Furthermore, given that both companies are related parties, the alliance could indicate a focus on creating synergies and efficiently leveraging management resources within the group.

3810|サイバーステップHD

242.0

▲ +3.86%

📎 Source:サイバーステップHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Cyberstep Holdings Inc. announced a partial correction to its “Quarterly Financial Report for Q3 FY2026 (Consolidated, Japanese GAAP)” initially disclosed on April 14, 2026.

- The reason for the correction was stated as an error in some of the descriptions within the financial report.

- The quarterly net loss per share for Q3 FY2026 was revised from ¥-31.95 before correction to ¥-30.87 after correction.

- Net assets per share for the same period were revised from ¥89.61 before correction to ¥84.42 after correction.

- Total shares outstanding (including treasury stock) at the end of Q3 FY2026 were revised from 65,013,082 shares to 69,013,082 shares, and the average number of shares outstanding for the cumulative period was also corrected.

🤖 AI Perspective

These corrections primarily impact per-share financial indicators and the number of outstanding shares, which investors may consider when assessing the company’s per-share valuation. The decrease in net assets per share and the increase in total shares outstanding could be viewed as factors affecting capital structure or potential dilution. It is worth noting that the core revenue and profit/loss figures from the original financial report remain unchanged, suggesting that the fundamental operational performance details are consistent.

3788|GMOGSHD

2101.0

▼ -2.42%

📎 Source:GMOGSHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- GMO GlobalSign Holdings K.K. resolved to acquire shares of Strategit Inc. and make it a subsidiary at its Board of Directors meeting on April 20, 2026.

- Strategit Inc. develops and provides an API connector-equipped MCP construction platform and “JOINT,” a data integration platform that links generative AI, SaaS, and on-premise systems.

- The purpose of this acquisition is to promote the connection between Strategit’s data integration platform and GMO Sign and GMO Trust Login, accelerate the evolution to next-generation enterprise services for the AI agent era, and create synergies within the GMO Group.

- The number of shares acquired is 81,254, with an acquisition price of 434 million JPY, resulting in GMO GlobalSign Holdings’ voting rights ownership ratio of 96.44%.

- Subject to an additional private placement subscription (130 million JPY for 24,340 shares), the total investment will be 564 million JPY, and the voting rights ownership ratio after the subsidiary conversion is expected to be 97.24%.

🤖 AI Perspective

This acquisition appears to be a strategic move by GMO GlobalSign Holdings to strengthen its business in the AI and SaaS integration domain. Strategit’s “JOINT” platform, which supports corporate AI utilization and DX promotion, aligns with the GMO Group’s “Next2040” mid-term strategy focusing on the AI infrastructure market. Enhanced integration with existing GMO services and contributions to overall group productivity are anticipated, which could potentially contribute to long-term corporate value.

5250|GMOプライム

1128.0

▲ +0.89%

📎 Source:GMOプライム Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- GMO Prime Strategy Co., Ltd. disclosed its Q&A summary for the Q1 FY2026 earnings briefing on April 20, 2026.

- Regarding overseas expansion, the company reported initial success in test marketing and is currently confirming its reproducibility.

- For its flagship product KUSANAGI, the company stated that there are no technically identical competitors, and KUSANAGI Managed Service by GMO is differentiated in terms of technology and service.

- Development of generative AI products is progressing as planned, with test sales completed and the company actively seeking sales collaboration partners.

- The North American patent application for “WEXAL” remains under examination, with delays in the start of examination by the USPTO and multiple rounds of notifications requiring time for response.

🤖 AI Perspective

This Q&A summary highlights the competitive advantages of GMO Prime’s core “KUSANAGI” business and its growth strategies, particularly in international expansion and the generative AI sector. The reported test marketing successes and progress in generative AI products may suggest positive momentum for future business developments. Additionally, the mention of synergy effects with the GMO Internet Group could indicate potential for business expansion through strengthened group collaboration.

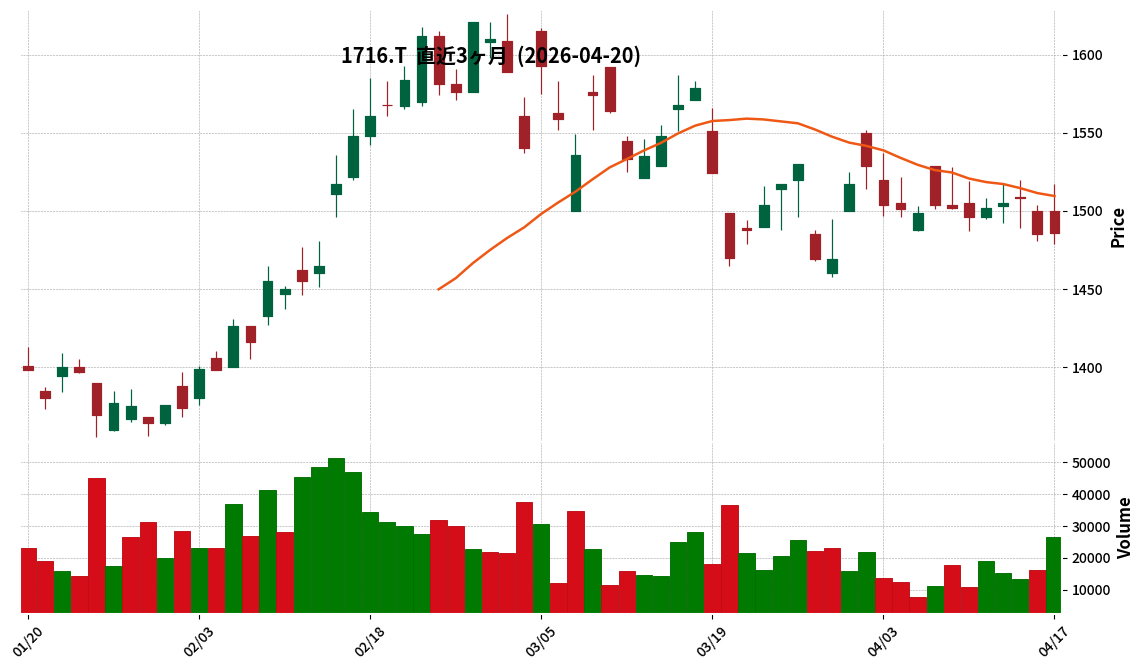

1716|第一カッター

1486.0

▲ +0.07%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Daiichi Cutter Kogyo Co., Ltd. resolved at its Board of Directors meeting today to absorb-merge its non-consolidated subsidiary, Kyokuyo Aquarec Co., Ltd.

- The effective date of the merger is scheduled for July 1, 2026, with Daiichi Cutter Kogyo as the surviving company and Kyokuyo Aquarec dissolving through an absorption-type merger.

- This merger qualifies as a simplified merger for Daiichi Cutter Kogyo under Article 796, Paragraph 2 of the Companies Act, and a short-form merger for Kyokuyo Aquarec under Article 784, Paragraph 1 of the Companies Act, thus no shareholder resolutions are required for either company.

- As Kyokuyo Aquarec is a wholly-owned subsidiary of Daiichi Cutter Kogyo, no shares will be issued, and no cash or other assets will be delivered in connection with this merger.

- The merger’s objective is to enhance corporate value by integrating Kyokuyo Aquarec’s specialized expertise and technological capabilities in the water jet business, thereby strengthening and expanding Daiichi Cutter Kogyo Group’s water jet business, accelerating and maximizing synergies, and efficiently utilizing management resources.

- The company has stated that the impact of this merger on its consolidated financial results will be minor.

🤖 AI Perspective

This transaction represents an absorption-type merger of a wholly-owned subsidiary by its parent company, which is commonly observed as part of group organizational restructuring. The move suggests an aim to integrate the specialized water jet technology of the subsidiary into the parent company to enhance overall group technical capabilities and streamline management resources. Given that the merger occurs after a period of subsidiary integration, it could be interpreted as a strategic step to further leverage operational and human resource synergies.

2999|ホームポジション

576.0

▲ +0.17%

📎 Source:ホームポジション Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Home Position Co., Ltd. reported for the second quarter of the fiscal year ending August 2026 (September 1, 2025, to February 28, 2026) net sales of 9,051 million JPY (up 25.9% year-on-year), operating profit of 478 million JPY (up 128.8% year-on-year), and interim net profit of 264 million JPY (up 1577.9% year-on-year).

- As of the end of the second quarter, the progress rates against the full-year forecast for FY2026 were 47.6% for net sales, 95.6% for operating profit, 105.5% for ordinary profit, and 110.2% for net profit.

- The company reported a recovery to conventional sales levels, with 101 units sold in the Kanto area and 117 units in the Tokai area, attributed to the reduction of long-term sales inventory. Work-in-progress real estate for sale increased to 8,617 million JPY due to active land acquisitions, primarily in the Kanto area.

- To expand its business in the Kanto area, Home Position opened the Tama branch on March 1, 2026, and the Yokohama Minami branch on April 1, 2026.

- As part of its sustainability initiatives, the company concluded a “Positive Impact Finance” agreement with Aichi Bank, Ltd. on March 31, 2026, securing a 200 million JPY loan over five years for working capital.

🤖 AI Perspective

The significant year-on-year increases in net sales and profits in the second quarter, with net profit already exceeding the full-year forecast, may suggest effective inventory management and successful sales activities. The strategic expansion in the Kanto area through new branch openings and the engagement in sustainability-linked financing could indicate a focus on both operational growth and corporate social responsibility. These factors are worth monitoring for their potential impact on future performance.

3353|メディ一光G

2865.0

▼ -0.35%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Medical Ikkou Group announced a correction to its “FY2026 Financial Results [Japanese GAAP] (Consolidated)” which was initially released on April 6, 2026, due to errors in some descriptions and numerical data.

- The reason for the correction was the discovery of errors in the fair value assessment of investment securities and in segment information detailed in the notes to the consolidated financial statements.

- The company has attached the full revised document, with corrected sections indicated by underlining.

- The revised consolidated results for FY2026 show net sales of JPY 54,982 million, operating profit of JPY 1,788 million, and profit attributable to owners of parent of JPY 1,275 million.

- For FY2027, the company forecasts consolidated net sales of JPY 56,500 million, operating profit of JPY 1,800 million, and profit attributable to owners of parent of JPY 1,300 million.

🤖 AI Perspective

- Corrections to financial statements are significant events for investors, underscoring the importance of accurate financial reporting and transparency.

- Errors in critical areas such as the fair value assessment of investment securities and segment information may prompt investors to re-evaluate the reliability of the company’s previously reported financial data.

- Investors may need to consider these revised figures to properly assess the company’s current financial health and its future prospects.

3996|サインポスト

222.0

▼ -1.33%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- **FY2026/2 Financial Results**: Net sales were ¥3,138 million (up 3.8% YoY), operating profit was ¥98 million (down 50.8% YoY), and net income was ¥76 million (down 70.4% YoY).

- **Performance vs. Plan**: Operating profit exceeded the plan by 40.6% reaching ¥98 million, and ordinary profit exceeded by 68.3% reaching ¥92 million. Net income decreased by 10.3% from the plan to ¥76 million due to a partial write-down of deferred tax assets.

- **Segment Performance**: The Consulting business recorded net sales of ¥3,010 million (up 3.3% YoY), and the DX & Local Co-creation business recorded net sales of ¥77 million (up 36.5% YoY).

- **Sale of TOUCH TO GO Shares**: Signpost sold 10,839 shares of TOUCH TO GO to Secure Co., Ltd. for ¥561 million, with a gain on sale of shares of ¥19 million to be recorded in Q1 FY2027/2.

- **FY2027/2 Outlook**: The company forecasts net sales of ¥3,850 million (up 22.7% YoY), operating profit of ¥56 million (down 43.1% YoY), and net income of ¥66 million (down 13.4% YoY). Increased hiring costs and development investments are expected to concentrate in the first half.

🤖 AI Perspective

Signpost’s FY2026/2 results showed a revenue increase, primarily driven by strong performance in the consulting business, yet profit was impacted by rising hiring costs and the write-down of deferred tax assets. The divestment of TOUCH TO GO shares suggests a strategic reallocation of resources towards core growth areas. The FY2027/2 outlook indicates substantial revenue growth, but with an anticipated temporary decline in profit due to upfront investments in human resources and innovation, which could be a focus for investors monitoring the company’s strategic pivot.

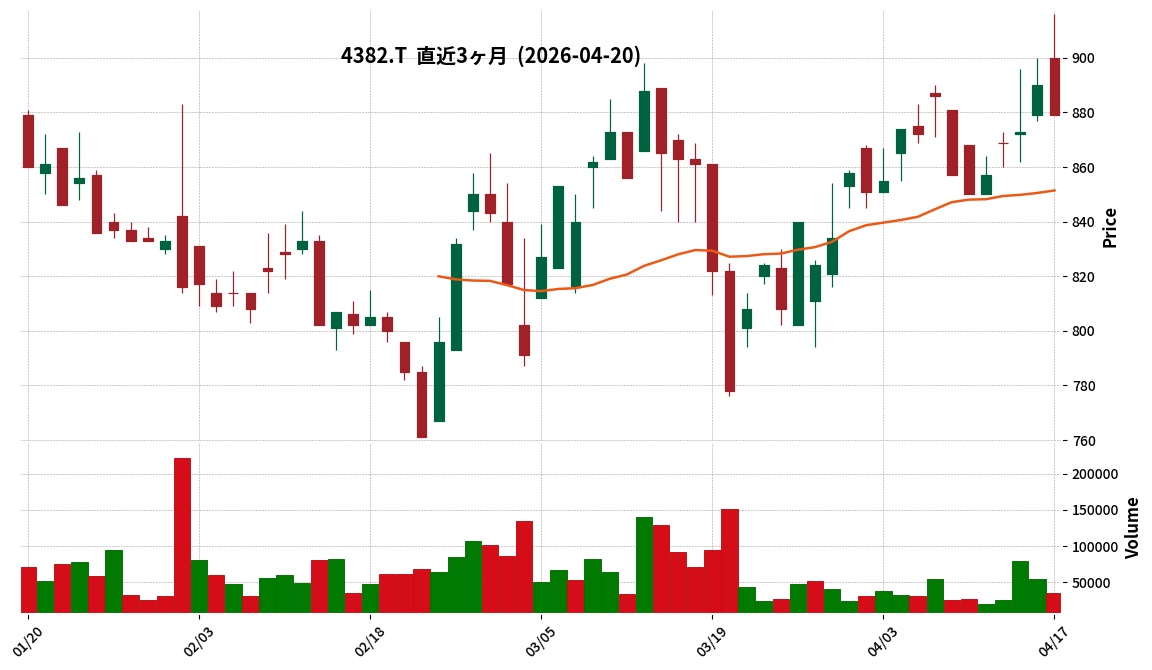

4382|HEROZ

879.0

▼ -1.24%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- HEROZ Inc. acquired 70% of AKM Consulting Co., Ltd. shares, making it a subsidiary.

- AKM Consulting provides “BAKUNAGE,” a back-office BPO service covering over 500 items across accounting, labor, and legal matters.

- BAKUNAGE achieved approximately 13-fold sales growth in three years, leveraging generative AI and RPA.

- Through this M&A, HEROZ aims to realize its core HEROZ 3.0 strategy of AI BPaaS in the back-office domain.

- HEROZ plans to transform its AI BPaaS model through AI agents, expanding their application to back-office operations.

🤖 AI Perspective

This acquisition appears to be a significant move for HEROZ, signaling a concrete expansion of its AI BPaaS strategy into a new business sector. AKM Consulting’s proven growth trajectory and expertise in real-world back-office processes leveraging AI could potentially enhance the precision of HEROZ’s AI models. The integration of a high-profitability business utilizing generative AI and RPA might be seen as a step towards achieving HEROZ’s long-term vision of “HEROZ ASK Cowork.”

4565|ネクセラファーマ

1013.0

▼ -3.06%

📎 Source:ネクセラファーマ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nexelapharma Inc. announced the receipt of a $10 million (approximately JPY 1,595 million) milestone payment from AbbVie Inc. under their drug discovery collaboration for neurological diseases.

- This milestone marks the third achievement in the research phase and relates to the identification of validated, differentiated hit molecules targeting neurological diseases.

- Revenue recognition for this milestone is planned primarily for 2026, with the remainder in 2027 and beyond.

- Under the agreement, Nexelapharma is eligible to receive up to $40 million in initial development milestones, additional milestones of up to $1.2 billion upon option exercise and achievement of development and commercialization goals, and tiered royalties on global sales.

- The impact of this milestone on the consolidated financial results for the fiscal year ending December 2026 has already been incorporated into the earnings forecast disclosed on February 13, 2026.

🤖 AI Perspective

- The achievement of a third research-phase milestone in the collaboration with AbbVie for neurological diseases may suggest a steady advancement in the pipeline development.

- The successful identification of validated hit molecules could indicate progress towards future development stages within the partnership.

- While the milestone’s impact for the fiscal year 2026 is already factored into the company’s forecast, its continuous achievement could be seen as an indicator of the long-term value of the collaboration.

6995|東海理電

3020.0

▼ -0.33%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tokai Rika Co., Ltd. announced on April 20, 2026, the postponement of its earnings release for the fiscal year ending March 2026, originally scheduled for April 24, 2026.

- The reason for the postponement is the discovery of an error in the accounting treatment of deferred tax assets related to retirement benefits for prior periods, leading to an overstatement of deferred tax assets as of March 31, 2025.

- This necessitates additional time for the restatement of consolidated financial statements and financial statements for the fiscal years from March 2019 to March 2025.

- The company states that the impact of these corrections on its FY2026 March performance is expected to be minor, as the adjustment will be reflected as an increase in income taxes – deferred for prior periods.

- The new earnings release date will be announced promptly once it is determined.

🤖 AI Perspective

* The postponement of financial results due to accounting errors may lead investors to closely evaluate a company’s financial reporting accuracy and internal controls.

* While the company anticipates a minor impact on its FY2026 performance from these past period corrections, the specifics of the restated financial statements will be a key area for investors to monitor.

* The market will likely await further announcements regarding the revised release date and the detailed nature of the accounting adjustments.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

7815|東京ボード工業

361.0

▲ +0.00%

📎 Source:東京ボード工業 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tokyo Board Industries Co., Ltd. (7815) has announced its consolidated financial results for the fiscal year ending February 2026. Due to a change in the fiscal year end date from March 31 to February 28, the current period covers 11 months from April 1, 2025, to February 28, 2026.

- For this 11-month period, the company reported consolidated net sales of JPY 6,625 million, an operating loss of JPY 81 million, an ordinary loss of JPY 190 million, and a net loss attributable to owners of parent of JPY 777 million.

- A significant factor contributing to the decline in performance was a minor fire at the Sakura plant’s production line on November 1, 2025, which led to a halt in operations, reduced product shipments, and a substantial impact on sales and profits.

- Regarding the consolidated financial position, total net assets at the end of the period were JPY 1,652 million (down JPY 750 million from the previous fiscal year end), and the equity ratio stood at 7.0% (down from 12.3% previously).

- The annual dividend for the fiscal year ending February 2026 is JPY 0.00 (no dividend), and the consolidated earnings forecast for the fiscal year ending February 2027 remains “undetermined” at this point. Furthermore, the company has noted the existence of material uncertainties regarding its ability to continue as a going concern.

🤖 AI Perspective

Tokyo Board Industries’ FY2026 results highlight the significant impact of the Sakura plant fire on its financial performance, leading to substantial losses across key profitability metrics. While a direct year-over-year comparison is not possible due to the fiscal year change, the reported net loss and reduction in the equity ratio suggest a challenging financial landscape. The “going concern” note and the undisclosed FY2027 outlook may raise questions about the company’s future operational stability, which investors might consider monitoring closely.

8572|アコム

484.0

▲ +0.81%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- ACOM Co., Ltd. has revised its consolidated earnings forecast for the fiscal year ending March 31, 2026.

- Consolidated operating profit is revised upward by 13.2% (¥11.7 billion) from the previous forecast of ¥88.6 billion to ¥100.3 billion, and net profit attributable to owners of parent is revised upward by 10.2% (¥7.4 billion) from ¥72.2 billion to ¥79.6 billion.

- The revisions are attributed to operating loan interest income exceeding plans, positive foreign exchange effects from the yen’s depreciation, and operating expenses (including doubtful account-related expenses, interest repayment expenses, and other operating expenses) falling below plans.

- The annual dividend forecast for the fiscal year ending March 31, 2026, has also been revised, increasing by ¥2.00 from the previous forecast of ¥20.00 to ¥22.00 per share.

- The year-end dividend per share is raised from the previous forecast of ¥10.00 to ¥12.00.

🤖 AI Perspective

According to the company’s announcement, the significant upward revision to the consolidated earnings forecast for FY2026 appears to be primarily driven by increased operating revenue and reduced operating expenses. The upward revision of the annual dividend forecast, based on the comprehensive consideration of current full-year performance, may indicate the company’s commitment to shareholder returns. The positive impact from higher operating loan interest income and foreign exchange effects, coupled with lower-than-planned expenses, could be seen as key factors influencing the company’s improved profitability.

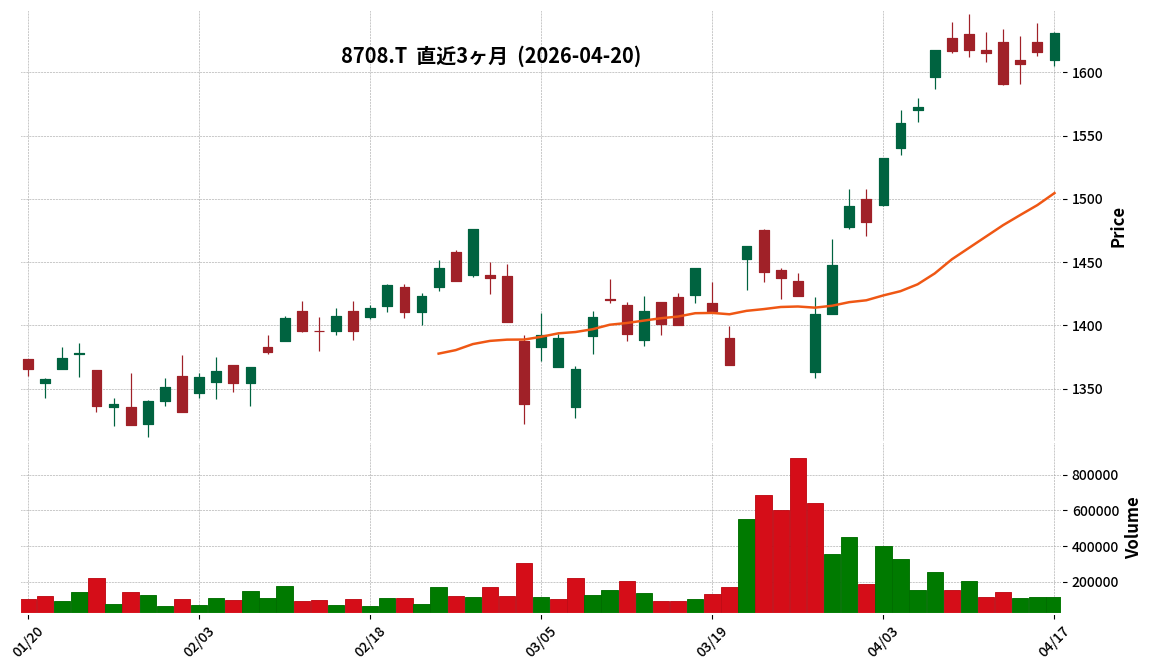

8708|アイザワ証G

1631.0

▲ +0.93%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Aizawa Securities Group announced its preliminary consolidated financial results for the fiscal year ended March 31, 2026, on April 20, 2026.

- For FY2026, operating revenue increased by 1.9% year-on-year to JPY 20,973 million.

- Operating income decreased by 98.6% to JPY 26 million, ordinary income by 74.1% to JPY 666 million, and net income attributable to owners of the parent by 13.2% to JPY 2,752 million.

- The increase in operating revenue was primarily due to higher stock brokerage commissions and trust fees.

- The decline in profits was attributed to an increase in selling, general, and administrative expenses associated with the expansion of the platform business, and losses recognized on unlisted assets in investment funds.

🤖 AI Perspective

The preliminary results show a notable divergence where operating revenue increased while profits significantly declined, which may attract investor attention. This trend could suggest that upfront investments for business expansion or specific investment losses have temporarily impacted profitability. Investors might consider monitoring the detailed official announcement scheduled for April 28th (Tuesday) for further insights.

7357|ジオコード

1618.0

▲ +1.63%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Geocode Co., Ltd. has announced the dispatch date for the “Shareholder Benefit Guide,” a document detailing how to receive the “Digital Gift” shareholder benefit.

- The dispatch date for this document is set for Wednesday, May 13, 2026, and it will be sent to the address registered in the shareholder registry, enclosed with the notice of the 22nd Ordinary General Meeting of Shareholders and dividend-related documents.

- Eligible shareholders are those recorded in the shareholder registry as of February 29, 2026, who hold two units (200 shares) or more of the company’s stock.

- The content of the benefit is a “Digital Gift” worth 5,000 yen.

- The redemption period for the “Digital Gift” is from Thursday, May 14, 2026, to Friday, July 31, 2026.

🤖 AI Perspective

- The provision of shareholder benefits is generally aimed at expressing gratitude to shareholders, enhancing the attractiveness of the company’s shares as an investment, and improving liquidity.

- The specific announcement of the dispatch date and the redemption period for the digital gift provides clarity for eligible shareholders to anticipate and plan for receiving their benefits.

- Such detailed information disclosure can contribute to transparency for investors and may reinforce their confidence in the company’s communication practices.

3492|R-MIRARTH

88300.0

▼ -1.12%

📎 Source:R-MIRARTH Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal period ending February 2026, operating revenue was ¥5,562 million (down 0.6% from the previous period), and net income was ¥2,593 million (down 3.8% from the previous period).

- Distribution per unit (DPU) was ¥2,800 (excluding excess distributions), with a payout ratio of 98.3%.

- MIRARTH REIT acquired “TOSEI HOTEL & SEMINAR Makuhari” for ¥4.725 billion on January 30, 2026.

- At the end of the period, total assets stood at ¥192,291 million, net assets at ¥90,438 million, and the unitholders’ equity ratio was 47.0%.

- The projected DPU for the August 2026 and February 2027 fiscal periods is ¥2,700 for both.

🤖 AI Perspective

While operating revenue and profit saw slight decreases, the DPU was maintained for the current period, which may be a key point for unitholders. The acquisition of a new property suggests continued efforts to expand asset size, and the forward-looking DPU projection implies a strategy to stabilize distributions by utilizing retained earnings, as it is set below the projected net income per unit. Given the favorable rental market conditions, the balance between strategic property transactions and a stable distribution policy could be an important factor for investors to monitor.

5244|G-jig.jp

231.0

▲ +0.87%

📎 Source:G-jig.jp Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- jig.jp Co., Ltd. resolved to acquire all shares of Bachelor Date Inc., making it a wholly owned subsidiary, at a Board of Directors meeting held on April 20, 2026.

- The total acquisition cost is estimated at JPY 3,483 million, comprising JPY 3,480 million for common shares and JPY 3 million for advisory fees.

- Bachelor Date Inc., established in 2021, develops and operates the “Bachelor Date” matching service, reporting sales of JPY 1,395 million and operating profit of JPY 265 million for the fiscal year ended June 2025.

- jig.jp stated the acquisition aims to accelerate Bachelor Date Inc.’s growth and establish a new revenue base, contributing to jig.jp Group’s mid-to-long-term corporate value enhancement.

- The share transfer is scheduled for May 11, 2026.

🤖 AI Perspective

This acquisition suggests jig.jp’s strategic move to diversify its revenue streams beyond its core live streaming service “Fuwacchi” by integrating the matching app business. Given Bachelor Date Inc.’s consistent performance growth in recent years, the integration of jig.jp’s marketing and operational expertise could potentially drive further business expansion. Investors may want to monitor how this acquisition contributes to jig.jp’s overall corporate value and potential synergies with existing operations in the mid to long term.

7287|日本精機

2537.0

▼ -0.63%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nippon Seiki Co., Ltd. resolved at its Board of Directors meeting on April 20, 2026, to acquire all outstanding shares of Toyo Denso Co., Ltd., making it a wholly-owned subsidiary, and signed a share transfer agreement on the same date.

- The purpose of this acquisition is to expand Nippon Seiki Group’s product portfolio with Toyo Denso’s in-vehicle input devices, create technological synergies in the HMI domain, and improve overall group operational efficiency.

- Toyo Denso Co., Ltd. designs, manufactures, and sells various switches, HMI systems, and electronic control units for automobiles, motorcycles, and general-purpose products globally, with consolidated net sales of JPY 100,038 million for the fiscal year ended March 2025.

- The total acquisition cost is estimated at JPY 50,550 million, comprising JPY 49,850 million for Toyo Denso’s common shares and an estimated JPY 700 million for advisory fees.

- The scheduled execution date for the share acquisition is October 1, 2026, and the entire acquisition fund is planned to be procured through borrowings from financial institutions.

🤖 AI Perspective

This acquisition suggests Nippon Seiki’s proactive approach to achieving its mid-term management plan goal of “new customer development and new product development” by expanding its business portfolio. The integration of both companies’ HMI technologies could enhance their competitiveness in the market. Investors may also want to monitor the impact of the acquisition, valued over JPY 50 billion, and its financing method on Nippon Seiki’s future financial performance.

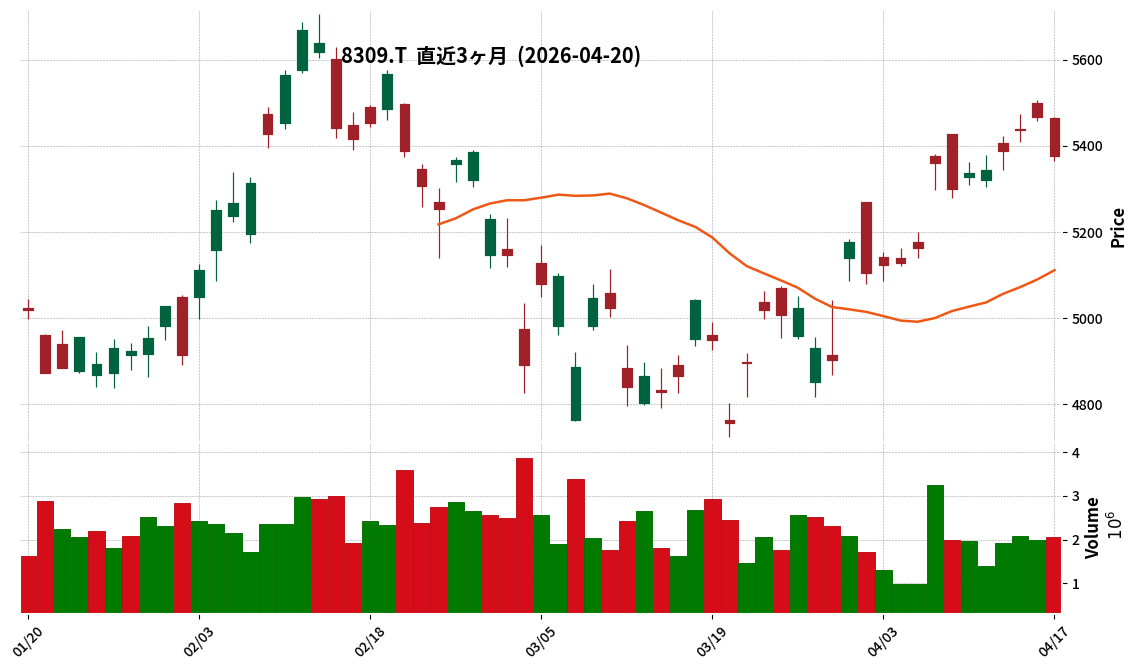

8309|三井住友トラストG

5376.0

▼ -1.65%

📎 Source:三井住友トラストG Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sumitomo Mitsui Trust Holdings, Inc. announced on April 20, 2026, a partial correction to its “Third Quarter FY2026 Financial Results Briefing Material.”

- The corrected material was attached as supplementary information to the “Consolidated Financial Results for the Third Quarter of FY2026 (Japanese GAAP)” released on January 30, 2026.

- The correction specifically pertains to page 9 of the briefing material, titled “(Reference) Sumitomo Mitsui Trust Bank (Non-consolidated) Financial Statements etc. ③ Trust Assets Balance Table.”

- In this table, the figure for “Money in Trust” as of December 2025 was corrected from an erroneous ¥29,630 billion to the correct ¥31,770 billion. The change from September 2025 was also adjusted accordingly.

- Additionally, the figure for “Loans” as of December 2025 was corrected from an erroneous ¥260,494 billion to the correct ¥258,354 billion. The change from September 2025 was also adjusted accordingly.

🤖 AI Perspective

This announced correction appears to address specific numerical inaccuracies within previously disclosed financial results briefing materials, aiming to ensure the precision of the information provided to investors. Rectifications made to particular line items such as “Money in Trust” and “Loans” within the trust assets balance table are intended to uphold the accuracy of financial disclosures. Such prompt corrections of past errors are generally viewed as contributing to enhanced transparency and reliability in corporate reporting.

1711|SDSHD

281.0

▼ -1.06%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SDSHD signed a business alliance agreement with eScrypt Energy Co., Ltd. on April 20, 2026.

- The alliance aims to create growth opportunities in the digital asset (crypto asset) sector and AI data center-related fields, leveraging the mutual knowledge and information networks of both companies.

- This partnership does not involve capital tie-ups, and specific commercialization, investment execution, or crypto asset acquisition are not determined at this stage.

- eScrypt Energy will provide advice and support to SDSHD regarding crypto asset (mainly Bitcoin, etc.) acquisition and management systems, including acquisition policies, custody, accounting, and risk management.

- SDSHD will advise eScrypt Energy on the construction and operation of AI data centers, covering aspects such as design, facility construction, power procurement, and operational structure.

🤖 AI Perspective

This collaboration may suggest SDSHD’s strategic move to enhance its expertise and know-how in crypto asset acquisition and management, which is deemed necessary for its advancement in the AI data center business. The primary objective appears to be strengthening the company’s capabilities in managing financial settlement processes within the AI data center operations by leveraging the respective strengths of both partners. Investors may wish to monitor the future progress of concrete business initiatives and their potential impact on financial performance.

5721|エスクリプトエナジー

100.0

▼ -1.96%

📎 Source:エスクリプトエナジー Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SCrypto Energy Co., Ltd. resolved on April 20, 2026, to make an advisory investment in SDS Holdings Co., Ltd. (TSE Standard Market: Code 1711) and to enter into a business alliance agreement.

- The advisory investment involves the acquisition of a portion of SDS Holdings’ 10th series share options with a put option for exercise price adjustment, with a total investment amount expected to be approximately ¥1.4 billion.

- Upon full exercise of these share options, SCrypto Energy would hold a 27.68% voting rights stake in SDS Holdings; however, the investment is positioned as a pure investment for financial returns, with no intent to be involved in management.

- The business alliance agreement aims to create new business opportunities in the digital asset (cryptocurrency) and AI data center-related sectors by mutually leveraging both companies’ expertise and information networks.

- The alliance includes SCrypto Energy providing advice to SDS Holdings on crypto asset acquisition and management systems, and SDS Holdings advising SCrypto Energy on AI data center construction and operation.

🤖 AI Perspective

This investment and business alliance appear to align with SCrypto Energy’s mid-term management plan to enter and expand its business in the crypto asset and AI data center fields. SDS Holdings is also advancing its business development in these same growth areas, suggesting a potential for synergy through the mutual utilization of both companies’ expertise and management resources. Investors may consider monitoring the progress of future discussions, as specific business implementations or investments are yet to be determined at this stage.

3024|クリエイト

1148.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- CREATE Co., Ltd. resolved at its Board of Directors meeting on April 20, 2026, to absorb its consolidated subsidiary, CRITECH Co., Ltd.

- The effective date of the merger is scheduled for July 1, 2026.

- The merger aims to accelerate the “material & construction order” strategy in the mid-term management plan, consolidate group management resources, expedite decision-making, integrate CRITECH’s construction management capabilities and network to respond flexibly to customer needs, accelerate CRITECH’s rebuilding plan, and create early synergies.

- The merger will be an absorption-type merger with CREATE as the surviving company and CRITECH dissolving. As it qualifies as a simplified merger for CREATE and a short-form merger for CRITECH, no shareholder meeting will be held.

- CRITECH Co., Ltd., the absorbed company, is a wholly-owned subsidiary of CREATE Co., Ltd., and reported for the fiscal year ended March 2025, non-consolidated net sales of 135 million yen, operating loss of 13 million yen, and net loss of 10 million yen.

🤖 AI Perspective

This merger, involving CREATE’s wholly-owned subsidiary CRITECH, appears to be a strategic move for intra-group reorganization. It suggests an intent to streamline management resources and accelerate decision-making processes to efficiently drive the “material & construction order” strategy outlined in the mid-term management plan. By directly integrating the dissolved company’s construction management capabilities and network, CREATE aims to strengthen business collaboration and enhance corporate value.

7603|ジーイエット

112.0

▼ -0.88%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- On April 20, 2026, Geeiet Co., Ltd. announced a correction to its “Non-Consolidated Financial Results for the Fiscal Year Ended February 29, 2026 [Japanese GAAP],” originally released on April 14, 2026, at 5:00 PM (JST), due to errors in its contents.

- The corrected total current assets as of February 28, 2026, were revised from 5,960 million yen to 5,769 million yen (an increase of 658 million yen compared to the end of the previous fiscal year).

- The corrected total non-current assets as of the same date were revised from 1,132 million yen to 1,323 million yen (a decrease of 868 million yen compared to the end of the previous fiscal year).

- The total assets on the balance sheet, amounting to 7,093 million yen, remained unchanged before and after the correction.

- Specifically, within the asset section of the balance sheet, “Other” current assets were revised from 672 million yen to 681 million yen, and an “Allowance for doubtful accounts” of △200 million yen was newly recorded under current assets. Concurrently, under “Investments and other assets” within non-current assets, “Deposits and guarantees” were adjusted from 1,363 million yen to 1,354 million yen, and the “Allowance for doubtful accounts” was revised from △289 million yen to △89 million yen.

🤖 AI Perspective

This correction addresses errors identified subsequent to the initial disclosure of the financial results, primarily involving adjustments to the classification and amounts of current and non-current assets, particularly the allowance for doubtful accounts, on the balance sheet. While the total asset figure remains constant, suggesting no fundamental alteration to the company’s overall financial position, it signifies a refinement in the accuracy of reported financial information.

9435|光通信

40000.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hikari Tsushin, Inc. resolved at its Board of Directors meeting on April 20, 2026, to enter into a simplified share exchange agreement to make IC Corporation a wholly-owned subsidiary.

- The purpose of this share exchange is to deepen collaboration within the Hikari Tsushin Group’s corporate-oriented businesses and strengthen sales capabilities, which is judged to contribute to the enhancement of both companies’ corporate value.

- The effective date for this share exchange is scheduled for May 15, 2026.

- The share exchange ratio is 217 shares of Hikari Tsushin common stock for one share of IC Corporation stock. An estimated 21,700 treasury shares held by Hikari Tsushin are planned to be allotted for the exchange.

- The valuation for this share exchange was conducted by Aoyama Trust Accounting Co., Ltd., an independent third-party calculation agent.

🤖 AI Perspective

This move appears to be part of Hikari Tsushin’s strategy to bolster its corporate-oriented businesses. Integrating IC Corporation, which specializes in information and communication equipment sales, could potentially lead to strengthened sales collaborations and new synergies across Hikari Tsushin’s diverse business portfolio, including electricity/gas, telecommunications, and solutions. The decision to use treasury shares for the exchange may suggest an effort to mitigate dilution for existing shareholders.

9993|ヤマザワ

1180.0

▲ +0.94%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended February 2026, consolidated net sales reached ¥105,405 million, marking a 2.8% increase year-over-year.

- Consolidated operating income was ¥1,142 million, ordinary income was ¥1,231 million, and profit attributable to owners of parent was ¥1,237 million, all representing a return to profitability from losses in the previous fiscal year.

- The annual dividend for FY2026/2 was set at ¥27.00 per share (interim ¥13.50, year-end ¥13.50), consistent with the previous year. The forecast for FY2027/2 also projects an annual dividend of ¥27.00.

- Effective February 20, 2026, Yamazawa transferred its “Yoneya business” (comprising 6 supermarket stores, fitness business, and real estate business in Akita Prefecture) to Tohoku Nice Co., Ltd. through a company split (simplified absorption-type company split).

- The consolidated earnings forecast for FY2027/2 predicts net sales of ¥99,700 million (down 5.4% YoY), operating income of ¥700 million (down 38.7% YoY), ordinary income of ¥800 million (down 35.1% YoY), and profit attributable to owners of parent of ¥450 million (down 63.6% YoY).

🤖 AI Perspective

Yamazawa’s significant return to profitability in FY2026/2, following an increase in net sales, may suggest positive outcomes from its operational strategies. However, the projected decline in sales and profits for FY2027/2 appears to be a direct consequence of the recent business restructuring, particularly the company split of the Yoneya business. Investors may consider monitoring how this strategic business separation impacts the company’s long-term financial health and competitiveness.

2769|ヴィレッジV

950.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- On April 20, 2026, Village Vanguard Corporation announced a correction to a portion of its disclosure made on April 10, 2026, concerning a business and capital alliance and the issuance of its 7th series of share options and 1st series of unsecured convertible bond-type share options.

- The correction primarily pertains to the section “6. Reasons for Selecting Allottees (1) Outline of Allottees” regarding the GP Fund.

- Specifically, the description of the GP Fund’s “Contributors’ Overview” was changed from “Domestic operating company 1” to “Corporate entity 1”, and in the note, “domestic operating companies 27” was corrected to “corporate entities 27”.

- The most significant correction involves the “Total amount of investment” by Growth Partners LLP, the managing partner of the GP Fund, which was revised from “JPY 7,382,700,000” to “JPY 14,430,000”.

🤖 AI Perspective

The substantial revision in the total investment amount of the managing partner of the GP Fund represents a material change from the initially announced details of the capital alliance. This adjustment may prompt investors to re-evaluate the financial structure and commitment of the GP Fund involved, potentially impacting their perception of the alliance’s underlying strength.

8143|ラピーヌ

192.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Lapine Co., Ltd. announced its consolidated financial results for the fiscal year ended February 28, 2026 (March 1, 2025, to February 28, 2026).

- Consolidated net sales amounted to 1,873 million yen, representing an 8.3% decrease compared to the previous fiscal year.

- Operating loss narrowed to 275 million yen, an improvement from a loss of 360 million yen in the prior fiscal year.

- However, net loss attributable to owners of parent expanded to 259 million yen, compared to a loss of 129 million yen in the previous fiscal year.

- The consolidated equity ratio at the end of the period declined to 23.0% from 27.8% in the prior fiscal year, and the financial report includes disclosures regarding “important events concerning going concern assumption.”

- For the full fiscal year ending February 28, 2027, the company forecasts consolidated net sales of 1,890 million yen (up 0.9% year-on-year), but expects to continue reporting operating, ordinary, and net losses.

🤖 AI Perspective

The reduction in operating loss may suggest that efforts to control selling, general, and administrative expenses have shown some effect. However, the expansion of ordinary loss and net loss attributable to owners of parent, along with the decline in the equity ratio, could indicate ongoing financial challenges. Investors may find the “important events concerning going concern assumption” disclosure particularly relevant in this context. With the forecast for the fiscal year 2027 still projecting losses, the focus is likely to be on the company’s concrete measures for profit improvement and their implementation progress.

3260|エスポア

—

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Espoir Co., Ltd. (Code: 3260, Nagoya Stock Exchange Next market) announced on April 20, 2026, a second postponement of its financial results announcement for the fiscal year ending February 2026.

- The announcement, previously scheduled for April 20, 2026 (Monday) as per the April 13, 2026 disclosure, has been rescheduled again to April 24, 2026 (Friday).

- The reason for this re-postponement is the necessity for additional confirmation and review by the accounting auditors regarding the validity of revenue recognition for specific transactions, specifically the correspondence between service content and consideration.

- This decision was made based on discussions and guidance from their auditing firm and the Nagoya Stock Exchange, deeming further scrutiny period necessary for accurate disclosure.

- The company stated it is working company-wide to promptly complete the audit procedures and is diligently preparing for the financial results announcement on April 24, 2026.

🤖 AI Perspective

A repeated postponement of financial results can typically raise questions among investors regarding a company’s financial reporting processes and internal controls. Issues surrounding the validity of revenue recognition are particularly sensitive, as they can directly impact the accuracy of reported earnings and the company’s overall financial health. Investors may wish to monitor the detailed outcome of the audit and the subsequent financial report closely for clarity on these specific transactions.

2160|G-GNI

3370.0

▼ -0.30%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Gyre Pharmaceuticals Co., Ltd., a consolidated subsidiary of G-GNI, announced the completion of the first patient enrollment in April 2026 for its Phase 2/3 clinical trial of pirfenidone capsules (product name: Aisuluoy).

- This trial is for a new indication: radiation-induced lung injury (RILI), irrespective of the presence of immune checkpoint inhibitor-related pneumonia (CIP).

- The clinical trial application for this study was approved by the China National Medical Products Administration (NMPA) in March 2025.

- Pirfenidone is one of the few globally approved small molecule drugs for idiopathic pulmonary fibrosis (IPF), possessing broad anti-inflammatory, antioxidant, and anti-fibrotic properties.

- G-GNI has stated that the progress of this clinical trial is expected to have a minor impact on its consolidated business performance.

🤖 AI Perspective

This announcement suggests a progression in Gyre Pharmaceuticals’ clinical development for pirfenidone into a new indication area. Radiation-induced lung injury (RILI) represents a field with high unmet medical needs due to limited current treatment options, making this development potentially significant. While the current impact on consolidated earnings is stated as minor, the long-term implications of expanding an approved drug’s indications into areas of high medical need could be worth monitoring.

💡 Start investing with IR insights

※ 本ページには広告が含まれます(PR)

Disclaimer: This article is for informational purposes only and does not constitute investment advice. All investment decisions are at your own risk.

コメント