📌 Today’s Highlights

Today we cover 135 IR announcements. Notable among them: G-リネットジャパン (3556), P-ディープラス (567A), MDM (7600). Use the table of contents below to navigate to each company.

- 3556|G-リネットジャパン

- 567A|P-ディープラス

- 7600|MDM

- 4436|G-ミンカブ

- 2815|アリアケ

- 4061|デンカ

- 6963|ローム

- 8111|ゴルドウイン

- 9005|東急

- 9698|クレオ

- 5076|インフロニアHD

- 5393|ニチアス

- 3040|ソリトンシステムズ

- 3197|すかいらーくHD

- 3968|セグエ

- 4205|日ゼオン

- 4680|ラウンドワン

- 6417|SANKYO

- 6638|Mimaki

- 1802|大林組

- 3632|グリーHD

- 3682|エンカレッジ

- 3773|G-AMI

- 3979|G-うるる

- 4172|Hiクラテス

- 4595|ミズホメディー

- 6059|ウチヤマHD

- 6800|ヨコオ

- 7561|ハークスレイ

- 7864|フジシール

- 1711|SDSHD

- 194A|G-WOLVES

- 1982|日比谷設

- 3402|東レ

- 6269|三井海洋

- 8075|神鋼商

- 3405|クラレ

- 4005|住友化

- 4114|日触媒

- 4183|三井化学

- 4367|広栄化学

- 4506|住友ファーマ

- 4792|山田コンサル

- 7276|小糸製

- 8032|紙パル商

- 9438|エムティーアイ

- 9904|ベリテ

- 9956|バローHD

- 1795|マサル

- 3099|ミツコシイセタン

- 4188|三菱ケミカルグループ

- 8560|宮崎太銀

- 9428|クロップス

- 8594|中道リース

- 1662|石油資源

- 2587|サントリーBF

- 3032|ゴルフ・ドゥ

- 3723|G-ファルコム

- 4997|日農薬

- 5962|浅香工業

- 6342|太平製作所

- 8051|山善

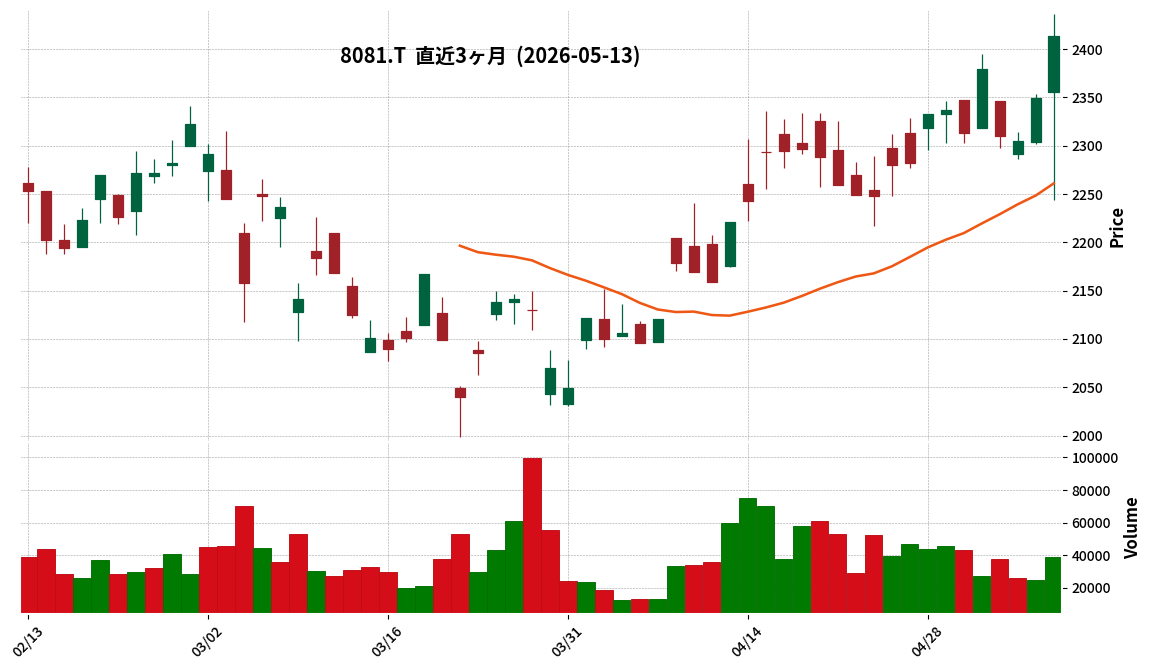

- 8081|カナデン

- 8129|東邦HD

- 9090|AZ-COM丸和HD

- 9643|中日興

- 6570|共和コーポレーション

- 1966|高田工業所

- 7337|ひろぎんHD

- 1788|三東工業

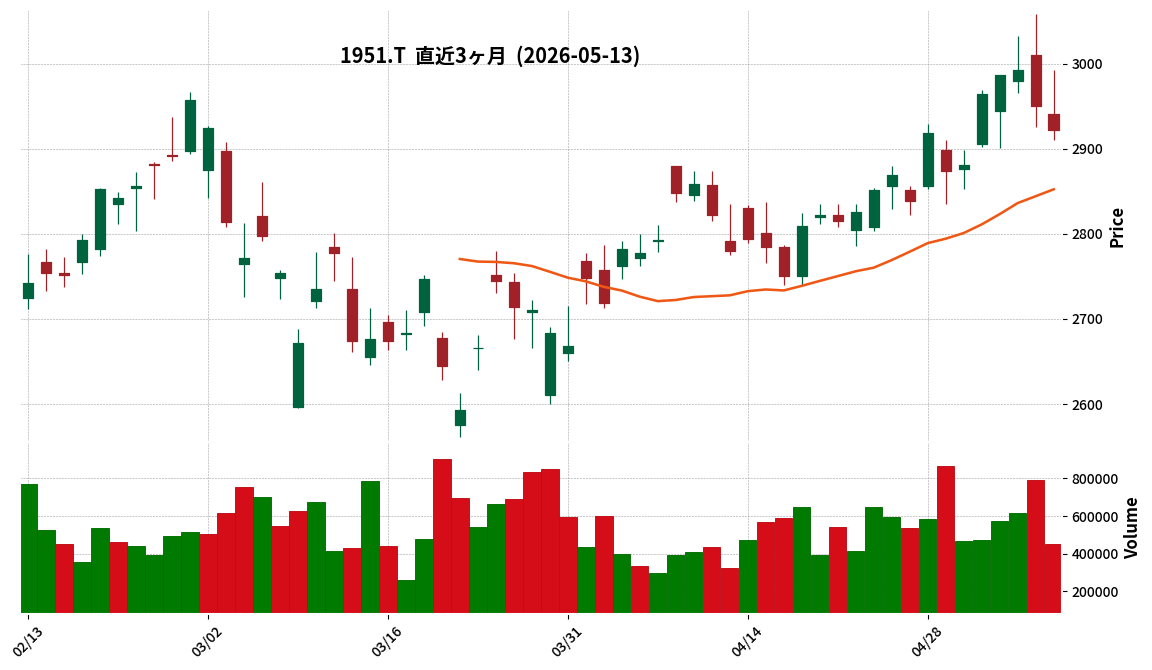

- 1951|エクシオグループ

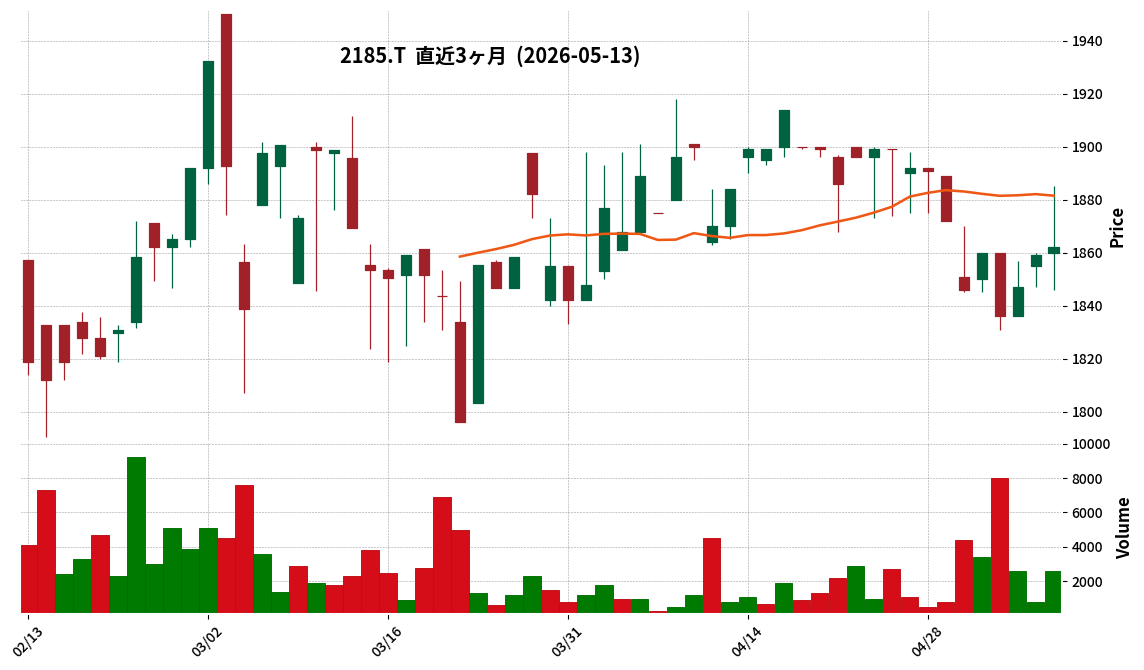

- 2185|シイエム・シイ

- 2919|マルタイ

- 3131|シンデンハイテク

- 3947|ダイナパック

- 4072|電算システムHD

- 4471|三洋化成

- 5570|G-ジェノバ

- 5632|三菱製鋼

- 5974|中国工

- 6768|タムラ製

- 7611|ハイデ日高

- 9435|光通信

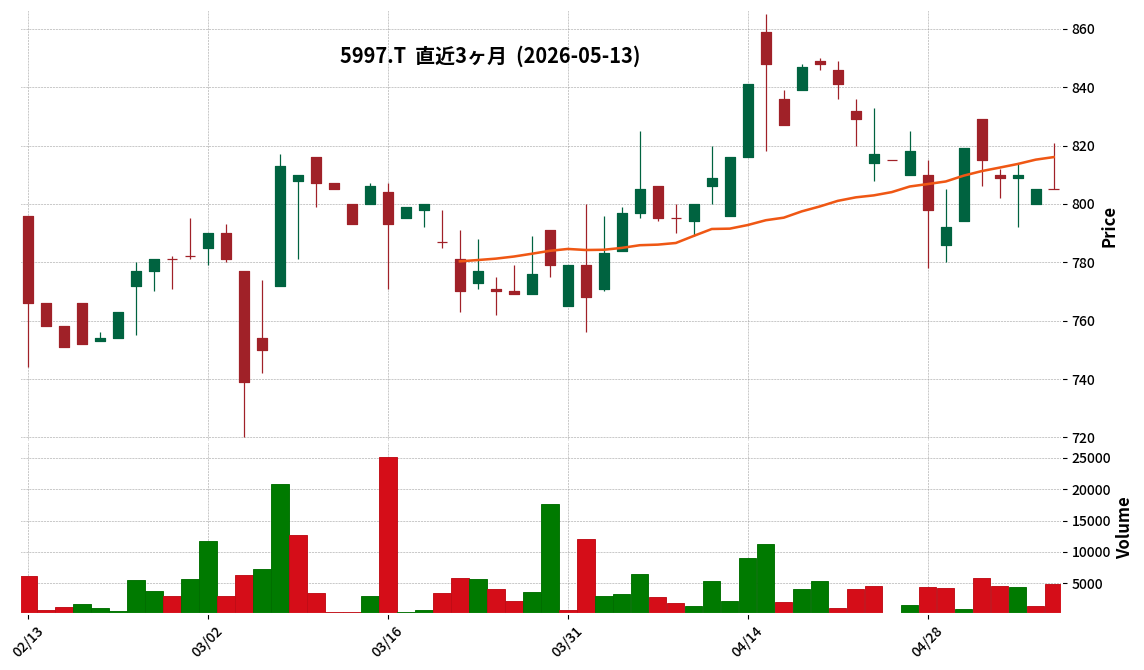

- 5997|協立エアテク

- 6497|ハマイ

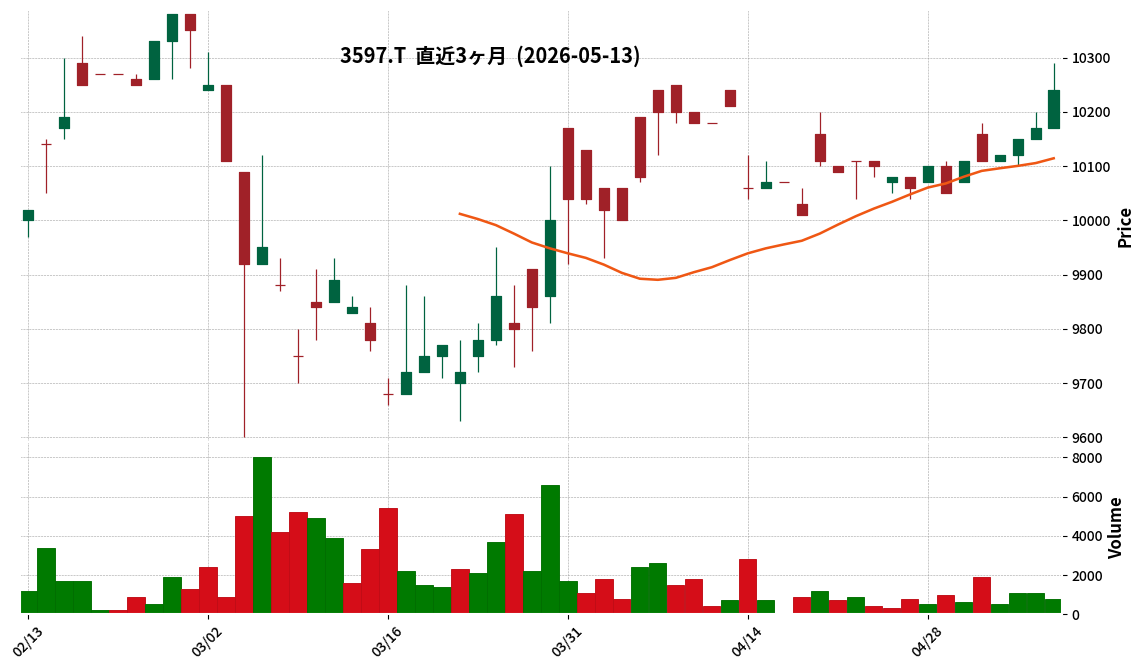

- 3597|自重堂

- 4488|G-AIinside

- 6645|オムロン

- 1605|INPEX

- 1799|第一建設

- 2124|JAC

- 2136|ヒップ

- 2385|G-総医研

- 2429|ワールドHD

- 2540|養命酒

- 268A|リガク

- 2820|やまみ

- 301A|P-インデックス

- 3088|マツキヨココカラ

- 3457|And Do HLD

- 2342|トランスジェニックG

- 7760|IMV

- 2984|ヤマイチ

- 3992|ニーズウェル

- 6339|新東工

- 4258|G-網屋

- 1518|三井松島HD

- 1663|K&Oエナジー

- 1793|大本組

- 2654|アスモ

- 2975|スター・マイカHD

- 3416|ピクスタ

- 3521|テルマー湯HD

- 3817|SRAHD

- 3848|データアプリ

- 3944|古林紙工

- 5301|東海カーボン

- 7305|新家工

- 9341|GENOVA

- 2180|サニーサイドアップ

- 3932|アカツキ

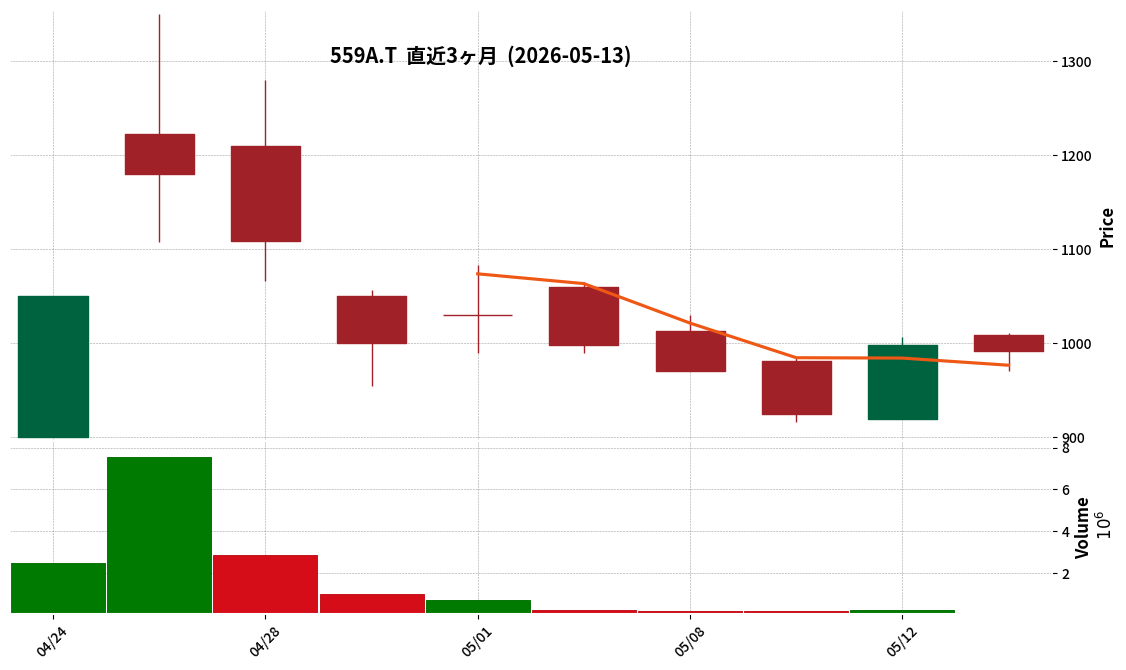

- 559A|梅乃宿酒造

- 2122|Iスペース

- 3205|ダイドー

- 3350|メタプラネット

- 3392|デリカフーズHD

- 3939|カナミックN

- 9888|UEX

- 1326|SPDRゴール

- 3775|ガイアックス

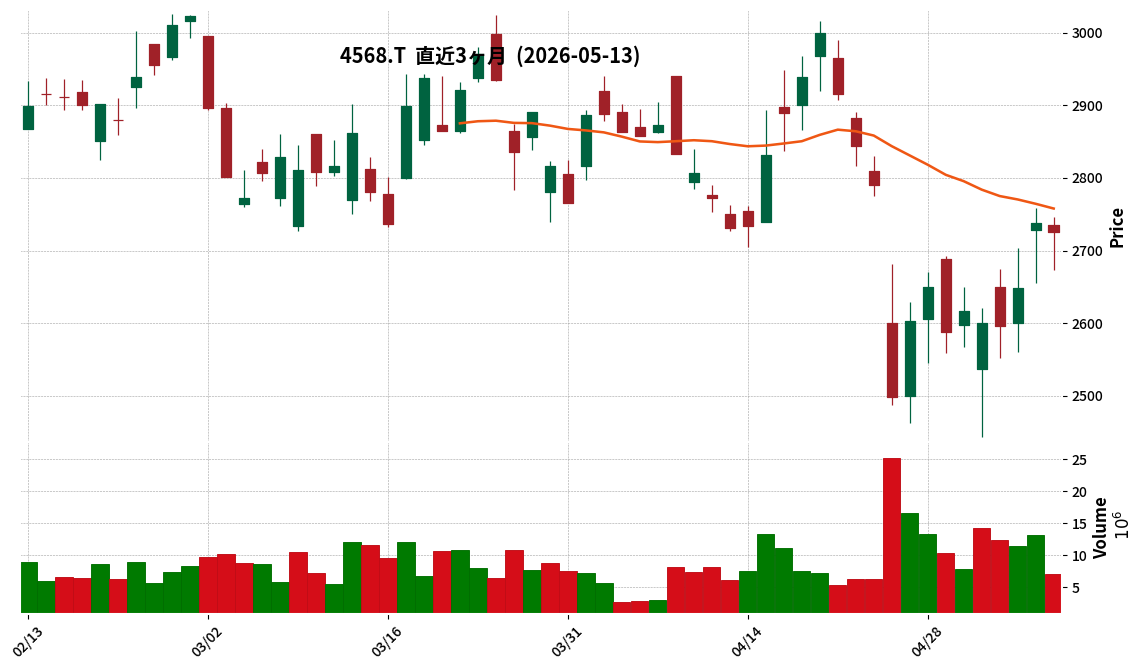

- 4568|第一三共

- 7031|G-インバウンド

- 7164|全国保証

- 7729|東精密

- 4417|G-グローバルセキュ

3556|G-リネットジャパン

954.0

▼ -0.73%

📎 Source:G-リネットジャパン Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Recycle Japan Group Corporation announced on May 13, 2026, that its Board of Directors resolved to revise upward its consolidated earnings forecast for the full fiscal year ending September 2026 for a second time.

- The revised forecast now projects net sales at JPY 16.2 billion (up 1.3% from the previous forecast of JPY 16.0 billion), operating profit at JPY 1.7 billion (up 30.8% from JPY 1.3 billion), and ordinary profit at JPY 1.7 billion (up 30.8% from JPY 1.3 billion).

- Net income attributable to owners of parent is revised to JPY 1.2 billion (up 33.3% from JPY 0.9 billion in the previous forecast), resulting in earnings per share of JPY 82.13, up from JPY 61.59.

- The upward revision is primarily attributed to incorporating certain high-certainty projects from the GIGA device trade in the recycling business and an upward trend in both collection volume and sales unit price for existing BtoC collection.

- This marks a second upward revision, following the previous one announced on February 9, 2026, and covers the fiscal period from October 1, 2025, to September 30, 2026.

🤖 AI Perspective

This repeated upward revision within a short period may suggest a stronger than anticipated performance and an improving business environment for the company. The significantly higher percentage increase in operating profit, ordinary profit, and net income attributable to owners of parent compared to sales could indicate an enhancement in profit margins or operational efficiency. The sustained strength in the GIGA device trade and BtoC collection within the recycling business appears to be a key factor worth monitoring for future performance.

567A|P-ディープラス

—

▲ +0.00%

📎 Source:P-ディープラス Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- D-Plus Co., Ltd. was listed on the TOKYO PRO Market of the Tokyo Stock Exchange on May 13, 2026.

- For the fiscal year ending November 2026, the company forecasts net sales of ¥11,000 million (an 18.8% increase year-on-year), operating profit of ¥548 million (a 195.0% increase), ordinary profit of ¥501 million (a 232.9% increase), and net profit of ¥328 million (a 256.8% increase).

- For the previous fiscal year ended November 2025, actual results were net sales of ¥9,258 million, operating profit of ¥186 million, ordinary profit of ¥150 million, and net profit of ¥92 million.

- The company operates solely in the car leasing business, with a growth strategy focused on maintaining stable profits in the Tokai area and accelerating expansion into the Kansai region.

- A 1-for-5,000 stock split was conducted for common shares on February 5, 2026.

🤖 AI Perspective

- Listing on the TOKYO PRO Market may enhance the company’s credibility and potentially broaden its access to capital.

- The significant year-on-year growth projected for net sales and all profit figures in the FY2026/11 forecast could indicate that the company is in a phase of robust expansion.

- Given the anticipated increase in the personal car leasing market, the alignment of the company’s growth strategy, particularly its expansion into the Kansai region, could be a key area for investors to monitor.

7600|MDM

446.0

▼ -4.09%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the full fiscal year ended March 2026, consolidated net sales were JPY 23,917 million, marking a 4.8% decrease compared to the previous fiscal year.

- Consolidated operating profit reached JPY 574 million (a 63.1% decrease year-on-year), and consolidated ordinary profit was JPY 534 million (a 64.1% decrease year-on-year).

- Net income attributable to owners of the parent amounted to JPY 263 million, representing a turn to profitability from a loss of JPY 461 million in the prior fiscal year.

- The primary factors for the decrease in operating profit were a reduction in gross profit due to lower sales (JPY -1.2 billion) and worsening manufacturing costs (JPY -0.26 billion), which could not be fully offset by the suppression of selling, general, and administrative expenses (JPY +0.43 billion).

- Domestic sales in Japan decreased by 3.8% to JPY 13,109 million, with a reduction in acquired cases for artificial joints influenced by media reports. U.S. sales declined by 5.9% to JPY 10,807 million (USD 71.5 million, down 5.0% on a USD basis), primarily due to supply constraints for artificial knee joint products, although new artificial hip joint products showed growth.

🤖 AI Perspective

* Despite reporting a decline in both net sales and operating profit, the return to positive net income attributable to owners of the parent may suggest underlying resilience or successful cost management in certain areas.

* The identified impacts from media reports in Japan and product supply constraints in the U.S. highlight significant external and operational challenges that could continue to influence future performance, warranting ongoing monitoring.

* The company’s commentary on worsening manufacturing costs, even with efforts to curb SG&A, could indicate that supply chain optimization and production efficiency might be critical areas for improving profitability moving forward.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

4436|G-ミンカブ

432.0

▼ -0.92%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Minkabu announced a revision to its earnings forecast.

- Net income attributable to owners of parent reflects the reassessment of deferred tax asset recoverability, based on a review of its business portfolio and new business development utilizing AI.

- The company has finalized its decision to relocate its head office in July 2026.

- Consequently, in the fourth quarter of the fiscal year ending March 2026, ¥31 million will be recorded as accelerated depreciation of existing head office-related fixed assets, classified under operating expenses.

- Additionally, ¥123 million will be recorded as a special loss, comprising provisions for restoration costs of the current office, overlapping rent for new and existing offices, and other temporary relocation-related expenses.

🤖 AI Perspective

The upward revision to the earnings forecast, although specific figures are not detailed in the provided text, generally suggests positive business performance expectations. The special losses and expenses associated with the HQ relocation represent a one-time cost in the current period, which is stated to be for future cost efficiency. The reassessment of deferred tax asset recoverability, impacting net income, could indicate a revised outlook on the company’s future taxable income potential.

2815|アリアケ

5510.0

▲ +3.57%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Ariake announced its consolidated financial results for the fiscal year ended March 31, 2026, with sales of JPY 66,957 million (+2.4% year-on-year), operating profit of JPY 11,782 million (+6.0% year-on-year), and net profit attributable to owners of parent of JPY 9,458 million (+15.3% year-on-year).

- Diluted earnings per share (EPS) for the fiscal year ended March 31, 2026, was JPY 296.96.

- The annual dividend for the fiscal year ended March 31, 2026, was JPY 180.00, including a year-end dividend of JPY 120.00 (an increase of JPY 50.00 from the previous year).

- For the fiscal year ending March 31, 2027, the company forecasts consolidated sales of JPY 69,232 million (+3.4% year-on-year), operating profit of JPY 11,251 million (-4.5% year-on-year), and net profit attributable to owners of parent of JPY 9,548 million (+1.0% year-on-year).

- The annual dividend for the fiscal year ending March 31, 2027, is projected to be JPY 300.00 (interim dividend of JPY 60.00, year-end dividend of JPY 240.00, including a special dividend of JPY 120.00), with a projected payout ratio of 98.5%.

🤖 AI Perspective

Ariake achieved increased sales and profits for the fiscal year ended March 31, 2026. For the fiscal year ending March 31, 2027, while an increase in sales is projected, a decrease in operating profit is anticipated, alongside a significant dividend increase, including a special dividend for its 60th anniversary. This might be interpreted as the company’s commitment to shareholder returns.

4061|デンカ

4101.0

▼ -6.58%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Denka Co., Ltd. reported consolidated net sales of 384,247 million yen for the fiscal year ended March 31, 2026, a 4.0% decrease year-on-year.

- Operating profit significantly increased by 82.0% to 26,225 million yen, and ordinary profit surged by 153.1% to 19,295 million yen compared to the previous fiscal year.

- Net profit attributable to owners of parent turned positive to 15,695 million yen, from a loss of △12,300 million yen in the prior fiscal year.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of 450,000 million yen (up 17.1% year-on-year), operating profit of 30,000 million yen (up 14.4%), ordinary profit of 20,000 million yen (up 3.7%), and net profit attributable to owners of parent of 16,000 million yen (up 1.9%).

- The annual dividend per share is 100.00 yen for both FY2026 (actual) and FY2027 (forecast).

🤖 AI Perspective

The significant recovery in operating, ordinary, and net profits, leading to a return to profitability for FY2026, appears to be a key highlight despite a decline in net sales. This turnaround could be attributed to increased sales volume in the Electronic & Advanced Products segment and improved profitability in the Elastomer & Infrastructure Solutions segment due to the temporary suspension of manufacturing facilities at a U.S. subsidiary. The positive outlook for FY2027, projecting further revenue and profit growth, suggests that the company anticipates continued progress in its various business initiatives.

6963|ローム

3909.0

▼ -1.46%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- ROHM Co., Ltd. reported consolidated net sales of JPY 481.1 billion for the full fiscal year 2025 (up 7.3% year-on-year) and an operating profit of JPY 10.8 billion (reversing a loss from the previous year), but a net loss of JPY 158.4 billion.

- The net loss in FY2025 was primarily due to impairment losses totaling JPY 163.2 billion, mainly on fixed assets related to the SiC business. This was attributed to factors such as a slowdown in BEV market growth, past over-investment, emergence of Chinese SiC device manufacturers, and a contraction of the SiC substrate external sales business.

- For the full fiscal year 2026, ROHM projects consolidated net sales of JPY 510.0 billion (up 6.0% year-on-year), an operating profit of JPY 30.0 billion (up 176.1% year-on-year), and a net profit of JPY 29.0 billion.

- The significant improvement in operating and net profit projected for FY2026 is primarily due to a substantial reduction in depreciation expenses resulting from the impairment losses recorded in FY2025.

- The company has commenced due diligence for integration with Toshiba D&S’s semiconductor business and continues discussions regarding integration with Mitsubishi Electric Power Device Business.

🤖 AI Perspective

ROHM’s FY2025 results show increased net sales, but a net loss due to significant impairment losses in its SiC business. However, for FY2026, the company anticipates a substantial improvement in operating and net profits, projecting a return to profitability, primarily driven by reduced depreciation expenses stemming from the prior year’s impairment. This may suggest a recalibration of SiC business investment strategies and an adaptation to evolving market conditions.

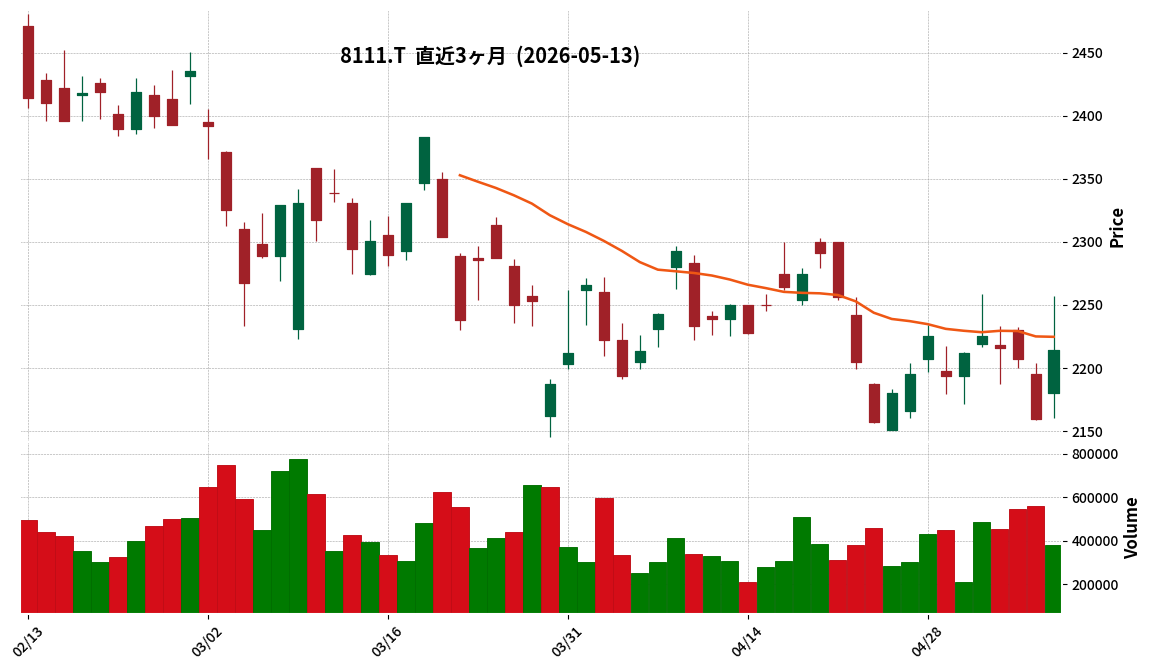

8111|ゴルドウイン

2214.0

▲ +2.52%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the consolidated fiscal year ended March 2026, Goldwin reported a 3.9% increase in net sales, reaching JPY 137,516 million.

- Operating profit grew by 18.0% to JPY 25,859 million, and ordinary profit increased by 10.1% to JPY 33,904 million.

- Net profit attributable to owners of parent decreased by 1.4% to JPY 24,094 million.

- A stock split of 1-for-3 ordinary shares took effect on October 1, 2025.

- The consolidated forecast for the fiscal year ending March 2027 projects net sales of JPY 145,400 million (up 5.7% year-on-year), operating profit of JPY 26,100 million (up 0.9%), and net profit attributable to owners of parent of JPY 25,600 million (up 6.3%).

🤖 AI Perspective

While Goldwin achieved growth in net sales, operating profit, and ordinary profit for FY2026/3, the slight decrease in net profit attributable to owners of parent may warrant attention. The 1-for-3 stock split implemented in October 2025 could be a relevant factor for investors evaluating per-share metrics and future dividend policies. The positive outlook for FY2027/3, forecasting increases in both revenue and profit, suggests an anticipated continuation of business growth.

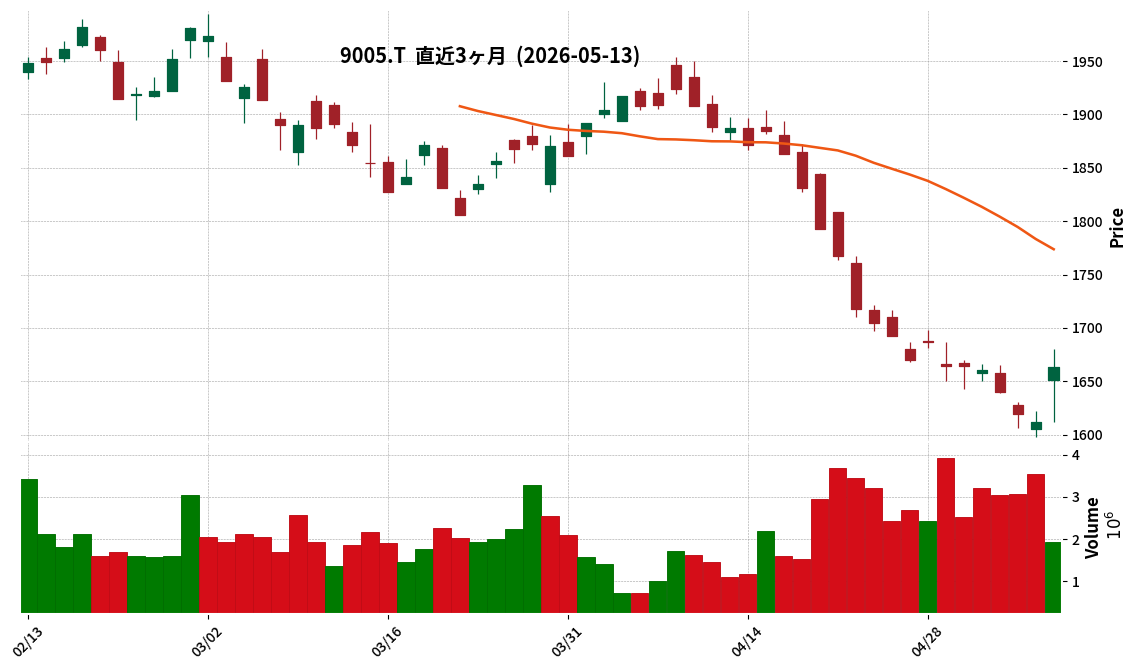

9005|東急

1663.5

▲ +3.23%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tokyu Corporation released its financial results briefing material for the fiscal year ending March 2026 on May 13, 2026.

- Consolidated operating revenue for FY2025 reached ¥1,086.1 billion, representing a 3.0% (¥31.1 billion) increase year-on-year.

- Consolidated operating profit for FY2025 was ¥103.1 billion, a 0.3% (¥0.2 billion) decrease year-on-year, remaining largely flat. This was influenced by a reaction to large-scale property sales in the real estate sales business in the prior fiscal year.

- Net profit attributable to owners of parent for FY2025 increased by 9.3% (¥7.3 billion) year-on-year to ¥87.0 billion. This was primarily due to the recording of negative goodwill from additional investment unit acquisitions of Tokyu Real Estate Investment Corporation and an increase in equity method investment income.

- For FY2026, the company forecasts consolidated operating revenue of ¥1,140.0 billion (a 5.0% increase year-on-year) and operating profit of ¥110.0 billion (a 6.6% increase year-on-year).

🤖 AI Perspective

The flat operating profit for FY2025, despite revenue growth, suggests that strong performance in some segments like hotels and resorts was partially offset by a decline in real estate sales. The significant rise in net profit, driven by one-off gains and equity method income, indicates the impact of specific financial strategies. The FY2026 forecast for increased revenue and operating profit may reflect confidence in sustained positive business conditions across various segments, requiring careful monitoring.

9698|クレオ

1212.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- CREO CO., LTD. announced its financial results briefing for the fiscal year ended March 2026 on May 13, 2026.

- For the fiscal year ended March 2026, consolidated net sales were 14,569 million JPY (YoY +0.3%), consolidated operating profit was 1,194 million JPY (YoY +5.7%), and profit attributable to owners of parent was 807 million JPY (YoY +15.9%).

- The Solution Services segment reported sales of 5,342 million JPY (YoY +5.6%) and segment profit of 1,019 million JPY (YoY +12.8%), driven by strong performance in recurring revenue services.

- For the fiscal year ending March 2027, the company forecasts consolidated net sales of 15,100 million JPY (YoY +3.6%), operating profit of 1,240 million JPY (YoY +3.8%), and profit attributable to owners of parent of 820 million JPY (YoY +1.5%), projecting renewed record high operating, ordinary, and net profits.

- The projected dividend per share for FY2027 is 56.00 JPY (YoY +1.00 JPY), targeting a new record high.

🤖 AI Perspective

- The FY2026 results indicate a positive trend of increasing revenue and profit, primarily driven by the robust performance of the Solution Services segment’s recurring revenue business.

- The company’s FY2027 forecast anticipates continued growth and new record highs, with planned investments in AI-powered services potentially signaling future strategic direction.

- Investors may want to monitor the segment-specific performance, particularly in contract development and support services, where some declines were observed in the past fiscal year.

5076|インフロニアHD

2377.5

▼ -0.48%

📎 Source:インフロニアHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Infroneer Holdings has announced its consolidated financial results for the fiscal year ended March 31, 2026.

- For the period, consolidated net sales were ¥1,124,878 million (up 32.7% year-on-year), and profit attributable to owners of the parent was ¥76,573 million (up 136.2% year-on-year). Business profit reached ¥84,134 million (up 73.3%), and profit before tax was ¥107,245 million (up 115.5%).

- The annual dividend per share for common stock for FY2026 was set at ¥120.00, comprising an interim dividend of ¥30.00 and a year-end dividend of ¥90.00. This is an increase from ¥60.00 in the previous fiscal year.

- The consolidated earnings forecast for the fiscal year ending March 31, 2027, projects net sales of ¥1,366,000 million (up 21.4% year-on-year) and profit attributable to owners of the parent of ¥60,000 million (down 21.6% year-on-year). An annual dividend of ¥100.00 for common stock is also forecast.

- During the fiscal year, 22 new companies, including Sumitomo Mitsui Construction Co., Ltd., became consolidated subsidiaries.

🤖 AI Perspective

The current fiscal year results show significant growth across revenue and all profit metrics, with profit attributable to owners of the parent more than doubling from the previous year. This strong performance appears to be considerably influenced by the consolidation of Sumitomo Mitsui Construction Co., Ltd. While the forecast for the next fiscal year anticipates continued revenue growth, a projected decrease in profit could indicate strategic shifts or increased investments for future development.

5393|ニチアス

3628.0

▼ -4.02%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nichias Corporation reported consolidated financial results for the fiscal year ended March 31, 2026 (FY2026), with net sales of ¥251.9 billion (down 1.8% year-on-year), operating profit of ¥37.0 billion (down 6.8%), ordinary profit of ¥39.4 billion (down 5.6%), and profit attributable to owners of parent of ¥31.6 billion (down 1.4%).

- By segment, Automotive Parts recorded an operating profit of ¥5.3 billion (up 17.0% year-on-year), and Building Materials recorded an operating profit of ¥2.7 billion (up 91.8%), both showing improved profitability. In contrast, High-Performance Products (semiconductor-related products) saw net sales of ¥39.1 billion (down 12.3%) and operating profit of ¥6.9 billion (down 32.5%).

- The effective tax rate for FY2026 was reduced to 18.0% due to a decrease in corporate tax from the definitive waiver of receivables related to a subsidiary (Kimitsu RW) and the recognition of deferred tax assets in NRI/Indonesia.

- For shareholder returns, the company implemented a total annual dividend of ¥164 per share for FY2026, marking 17 consecutive years of dividend increases, achieving a DOE (Dividend on Equity) of 5.1% and a total return ratio of 58.1%.

- The consolidated financial forecast for the fiscal year ending March 31, 2027 (FY2027) projects net sales of ¥270.0 billion (up 7.2% year-on-year), operating profit of ¥45.0 billion (up 21.6%), ordinary profit of ¥45.0 billion (up 14.3%), and profit attributable to owners of parent of ¥32.0 billion (up 1.2%). This forecast includes ¥2.5 billion for new core system construction costs and anticipates record-high performance driven by the recovery in the semiconductor market.

🤖 AI Perspective

While FY2026 saw a decline in revenue and profit, improved profitability in the Automotive Parts and Building Materials segments, along with special gains/losses and reduced tax burden, appear to have supported net profit. For FY2027, the company anticipates record-high earnings, bolstered by a recovery in the semiconductor market; however, the inclusion of new core system construction costs in the profit plan may warrant attention. The continuation of shareholder return policies, including consecutive dividend increases, could also be a key point of interest for investors.

3040|ソリトンシステムズ

1939.0

▲ +1.52%

📎 Source:ソリトンシステムズ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Soliton Systems announced its consolidated financial results for Q1 FY2026 (January 1 to March 31, 2026), with net sales of ¥5,165 million (up 12.7% YoY), operating profit of ¥908 million (up 53.2% YoY), ordinary profit of ¥949 million (up 79.7% YoY), and net profit attributable to owners of parent of ¥685 million (up 71.1% YoY).

- By segment, the IT Security business recorded net sales of ¥4,850 million (up 12.6% YoY) and segment profit of ¥1,169 million (up 45.2% YoY). Strong sales of “NetAttest EPS” and alliances with IIJ and NEC were noted.

- The Video Communication business reported net sales of ¥267 million (up 18.1% YoY) but a segment loss of ¥60 million (compared to a loss of ¥36 million in the prior year). While “Smart-telecaster series” sales were solid, higher server prices were cited as an impact.

- The full-year consolidated earnings forecast for FY2026 remains unchanged, projecting net sales of ¥21,200 million, operating profit of ¥3,150 million, ordinary profit of ¥3,200 million, and net profit attributable to owners of parent of ¥2,350 million.

- The annual dividend forecast for FY2026 is ¥60.00 per share, comprising an interim dividend of ¥30.00 and a year-end dividend of ¥30.00, an increase from ¥54.00 in the previous year.

🤖 AI Perspective

The company’s Q1 results showed significant year-on-year growth across all key financial metrics, suggesting a strong start to the fiscal year. The robust performance of the IT Security business appears to be a primary driver of this improved profitability. Investors may monitor the company’s progress against its unchanged full-year guidance and the implications of the increased dividend forecast.

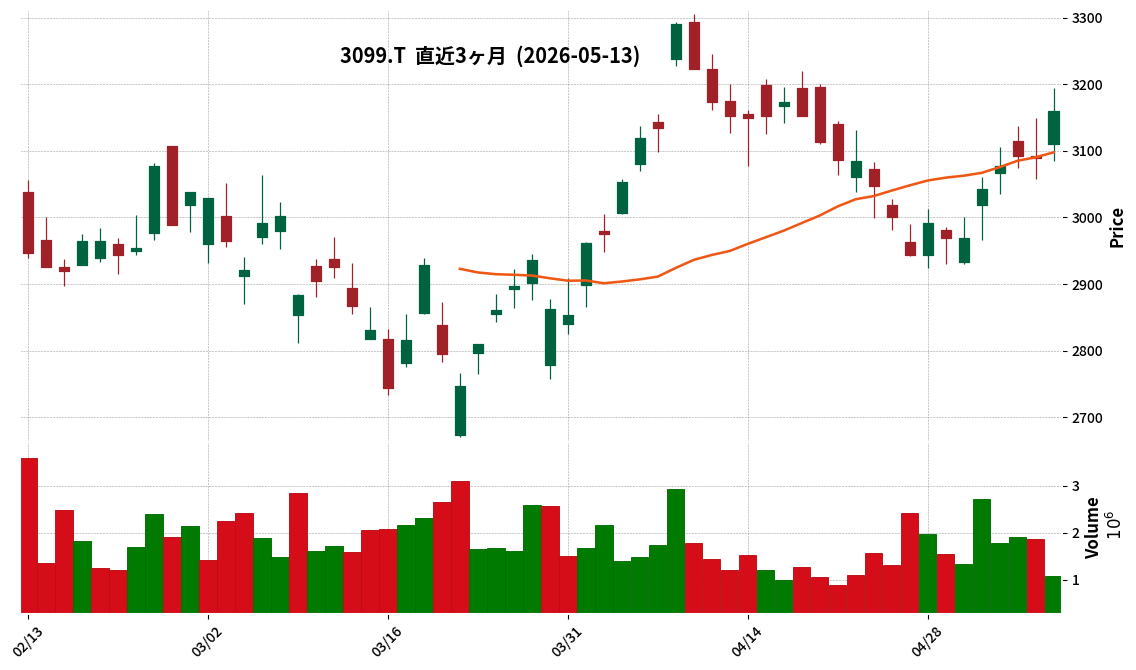

3197|すかいらーくHD

3119.0

▲ +2.36%

📎 Source:すかいらーくHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of the fiscal year ending December 2026 (January 1, 2026 – March 31, 2026), consolidated revenue reached ¥121.26 billion, marking an 8.6% increase compared to the same period in the previous year.

- Profit attributable to owners of the parent company amounted to ¥5.52 billion, representing a 27.0% increase year-on-year.

- Operating profit was ¥9.09 billion (up 10.6% YoY), and ordinary profit was ¥8.91 billion (up 17.0% YoY).

- Existing store sales increased by 6.0% compared to the prior year, with 5 new stores opened, 14 store conversions, and 50 store renovations completed during the first quarter.

- There are no revisions to the consolidated full-year performance forecast for the fiscal year ending December 2026, nor to the annual dividend forecast (¥16.00 at fiscal year-end, total ¥26.00).

🤖 AI Perspective

Skylark Holdings’ Q1 FY2026 results show double-digit growth not only in revenue but also in operating profit, ordinary profit, and profit attributable to owners of the parent compared to the same period last year. This performance may suggest that the company’s strategies, including deepening store-centric management and promoting menu and promotion strategies, are contributing to solid existing store sales growth. The reaffirmation of full-year performance and dividend forecasts could also be a point of interest for investors evaluating the company’s future business trajectory.

3968|セグエ

547.0

▲ +1.30%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Segue’s consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026 to March 31, 2026) showed revenue of ¥9,184 million (up 91.8% year-on-year), operating profit of ¥1,449 million (up 541.2%), ordinary profit of ¥1,418 million (up 482.6%), and profit attributable to owners of parent of ¥882 million (up 527.5%).

- The VAD business recorded sales from the final phase of a large-scale GSS project, while the System Integration business saw contributions from major service industry projects and university/government agency projects. The In-House Development business achieved significant revenue and profit growth through deliveries of large-scale RevoWorks projects for government agencies and continued growth in recurring revenue models.

- As of the end of the first consolidated accounting period, total assets stood at ¥23,095 million, net assets at ¥7,400 million, and the equity ratio at 30.8%, all showing increases compared to the end of the previous consolidated fiscal year.

- The full-year consolidated earnings forecast for the fiscal year ending December 2026 remains unchanged from the announcement on February 13, 2026, projecting revenue of ¥30,000 million (up 19.6% year-on-year) and operating profit of ¥2,300 million (up 24.0%).

- The projected annual dividend for the fiscal year ending December 2026 is ¥18.00 (interim ¥9.00, year-end ¥9.00), with no revisions from the latest publicly announced dividend forecast.

🤖 AI Perspective

The substantial year-on-year increase in Q1 revenue and profits suggests strong performance, likely driven by significant contributions from large-scale VAD projects and robust growth in in-house developed businesses. The unchanged full-year forecast could imply that management views the strong Q1 results as generally in line with their internal plans. Improvements in asset conditions and an increased equity ratio may indicate a strengthening of the company’s financial foundation.

4205|日ゼオン

2026.0

▲ +1.81%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nippon Zeon Co., Ltd. has decided on a year-end dividend of ¥40 per share for the surplus, with a record date of March 31, 2026.

- This declared amount represents an increase from the most recent dividend forecast of ¥36 (announced April 25, 2025) and the actual dividend of ¥35 for the previous fiscal year (ended March 2025).

- Consequently, the total annual dividend for the fiscal year ended March 31, 2026, will be ¥76 per share, including an interim dividend of ¥36, marking a ¥6 increase compared to the previous fiscal year’s total dividend of ¥70.

- The total dividend amount is projected to be ¥7,707 million, indicating an increase from the previous fiscal year’s actual amount of ¥6,954 million.

- The dividend will be sourced from retained earnings, with an effective date of June 29, 2026.

🤖 AI Perspective

The company’s dividend policy targets a Dividend on Equity (DOE) of 4% or more, and this increase appears to be a result of a comprehensive consideration of full-year business performance and financial position. The upward revision beyond the latest forecast may signal a strong commitment to shareholder returns. Furthermore, the continuous increase in the dividend amount from the previous year suggests an adherence to the company’s objective of providing stable shareholder distributions.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

4680|ラウンドワン

874.8

▲ +1.56%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the consolidated fiscal year ended March 31, 2026, Round One reported revenue of ¥189,548 million (up 7.1% year-on-year), operating profit of ¥28,773 million (up 9.7% year-on-year), and profit attributable to owners of the parent of ¥16,621 million (up 7.9% year-on-year).

- The annual dividend for FY2026 was announced as ¥18.00 per share (compared to ¥16.00 in the previous fiscal year), with total dividends amounting to ¥4,727 million.

- The consolidated forecast for the fiscal year ending March 31, 2027, projects revenue of ¥219,090 million (up 15.6% year-on-year), operating profit of ¥33,050 million (up 14.9% year-on-year), and profit attributable to owners of the parent of ¥18,260 million (up 9.9% year-on-year).

- EBITDA for FY2026 was disclosed as ¥72,049 million, and adjusted EBITDA as ¥73,490 million.

- The company reported opening the Sendai Izumi store in Japan in December 2025, the Willowbrook store (Texas) in December 2025 and the Menlo Park store (New Jersey) in February 2026 in the U.S., and the Shenzhen Futian IN City Plaza store (Guangdong) in April 2025 in China.

🤖 AI Perspective

Round One’s FY2026 results demonstrated increased revenue and profit, with the FY2027 forecast anticipating continued growth, which may be a key point for investors. The increase in the annual dividend from the previous fiscal year could suggest a proactive stance towards shareholder returns. The company’s strategic store openings and initiatives at existing locations, both domestically and internationally, appear to be contributing to its performance.

6417|SANKYO

1861.5

▲ +2.56%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SANKYO Co., Ltd. announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026) on May 13, 2026.

- For the consolidated operating results, net sales were ¥179,211 million (down 6.6% year-on-year), operating profit was ¥62,484 million (down 15.1% year-on-year), and net income attributable to owners of parent was ¥46,752 million (down 13.4% year-on-year).

- The annual dividend for the fiscal year ended March 31, 2026, was ¥90.00 per share (compared to ¥100.00 in the previous fiscal year), with total dividends of ¥18,138 million and a consolidated dividend payout ratio of 39.5%.

- Regarding the consolidated financial position, total assets at the end of March 2026 were ¥287,458 million, net assets were ¥250,155 million, and the equity ratio was 86.5%.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥174,000 million (down 2.9% year-on-year), net income attributable to owners of parent of ¥40,000 million (down 14.4% year-on-year), and basic earnings per share of ¥202.52.

🤖 AI Perspective

The FY2026 results indicated a decline in net sales and all profit metrics compared to the previous fiscal year. While the company achieved top market share in its pachinko machine related business for the fourth consecutive period, broader market conditions may have influenced overall performance. The FY2027 forecast also anticipates further decreases in revenue and profit, suggesting that future market trends and new product strategies could be worth monitoring.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

6638|Mimaki

1767.0

▲ +0.91%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Consolidated net sales for the fiscal year ended March 31, 2026, amounted to 83,725 million yen, marking a slight decrease of 0.3% year-on-year.

- During the same period, consolidated operating profit reached 9,431 million yen (up 3.5% year-on-year), and profit attributable to owners of parent was 6,741 million yen (up 9.5% year-on-year).

- The consolidated equity ratio improved to 48.1% at the end of March 2026, an increase of 5.8 percentage points from the previous fiscal year-end.

- The annual dividend for the fiscal year ended March 31, 2026, was 55.00 yen per share, which includes a commemorative dividend of 5.00 yen for the fiscal year-end.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of 91,000 million yen (up 8.7% year-on-year), operating profit of 9,500 million yen (up 0.7% year-on-year), and profit attributable to owners of parent of 6,100 million yen (down 9.5% year-on-year).

🤖 AI Perspective

- The results for the fiscal year ended March 31, 2026, suggest a positive trend in profitability, as operating and net profits increased despite a marginal decline in net sales.

- The significant improvement in the consolidated equity ratio to 48.1% could indicate a strengthening of the company’s financial foundation, which may be a noteworthy point for investors.

- While the forecast for the fiscal year ending March 31, 2027, projects an increase in revenue, the anticipated decrease in profit attributable to owners of parent warrants close monitoring for further insights into its underlying causes.

1802|大林組

3955.0

▲ +1.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Obayashi Corporation announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025, to March 31, 2026).

- Consolidated net sales totaled 2,586,258 million yen, a 0.2% decrease from the previous fiscal year.

- Consolidated operating profit reached 194,678 million yen (up 36.6%), consolidated ordinary profit was 204,195 million yen (up 34.1%), and profit attributable to owners of parent was 173,759 million yen (up 19.5%).

- The annual dividend for the fiscal year ended March 31, 2026, was increased to 88.00 yen from 81.00 yen in the previous year.

- For the fiscal year ending March 31, 2027, consolidated financial forecasts include net sales of 2,945,000 million yen (up 13.9%), operating profit of 180,000 million yen (down 7.5%), ordinary profit of 183,000 million yen (down 10.4%), and profit attributable to owners of parent of 157,000 million yen (down 9.6%). The annual dividend is forecast to be 94.00 yen.

🤖 AI Perspective

The fiscal year 2026 results indicate a notable improvement in profitability, with significant increases across all profit metrics despite a slight dip in net sales. The continuous increase in annual dividends may suggest a strong commitment to shareholder returns. For fiscal year 2027, while sales are projected to grow, a decrease in profit is anticipated, making the balance between business growth and shareholder returns a point worth monitoring.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

3632|グリーHD

368.0

▲ +1.38%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the third quarter of the fiscal year ending June 2026, consolidated net sales were ¥38,444 million (down 10.9% year-on-year), and operating profit was ¥2,420 million (down 34.7% year-on-year).

- Net profit attributable to owners of parent for the same period was ¥1,912 million, marking a 112.4% increase compared to the previous fiscal year’s third quarter.

- The year-end dividend forecast for the fiscal year ending June 2026 has been revised to ¥21.50 per share.

- The consolidated business forecast for the fiscal year ending June 2026 has been withheld, citing difficulties in calculating appropriate and rational figures due to rapid changes in the business environment and the impact of market conditions on the investment business.

- By segment, the VTuber business performed strongly, reporting net sales of ¥6,686 million (up 7.9% year-on-year) and operating profit of ¥892 million (up 60.6% year-on-year).

🤖 AI Perspective

The significant increase in net profit attributable to owners of parent despite decreases in consolidated net sales and operating profit could suggest the positive influence of other financial factors, such as increased foreign exchange gains. The decision to withhold the full-year earnings forecast indicates the company’s assessment of high market volatility and uncertainty, particularly concerning its investment business. However, the upward revision of the year-end dividend forecast may be interpreted as a positive signal regarding shareholder returns.

3682|エンカレッジ

637.0

▲ +0.95%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Encore Technologies’ non-consolidated financial results for the fiscal year ended March 31, 2026, reported net sales of ¥2,584 million (up 3.3% year-on-year), operating profit of ¥303 million (up 1.7%), and ordinary profit of ¥315 million (up 4.1%). However, net profit for the period decreased by 3.4% to ¥212 million.

- Regarding sales breakdown, while license sales fell below target, consulting service sales increased by 20.5% year-on-year, and cloud service sales grew by 39.7%. Maintenance and support service sales achieved a 96% renewal rate.

- The annual dividend for the fiscal year ended March 31, 2026, was ¥26.00 (year-end dividend of ¥26.00), an increase from ¥25.00 in the previous fiscal year. The company forecasts an annual dividend of ¥27.00 (year-end dividend forecast of ¥27.00) for the fiscal year ending March 31, 2027.

- For the fiscal year ending March 31, 2027, the company forecasts net sales of ¥2,800 million (up 8.3% year-on-year), operating profit of ¥320 million (up 5.6%), ordinary profit of ¥326 million (up 3.5%), and net profit of ¥223 million (up 5.2%).

- To address the growing customer preference for cloud-based solutions, the company launched “ESS AdminONE Cloud,” a cloud version of its privileged ID management product “ESS AdminONE,” in April 2026.

🤖 AI Perspective

While net sales showed continued growth for the fiscal year ended March 31, 2026, the decrease in net profit is a notable point. This could be attributed to license sales falling short of the initial plan, though significant growth in consulting and cloud services suggests a shift in the company’s business structure. The forecast for increased sales and profits in the fiscal year ending March 31, 2027, positions the launch of the cloud-based product as a critical factor for investors to monitor regarding future earnings contributions.

3773|G-AMI

1051.0

▲ +1.94%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Advanced Media, Inc. (G-AMI) announced consolidated results for the fiscal year ended March 2026, with net sales reaching ¥7,063 million (up 6.0% year-on-year), ordinary income ¥1,558 million (up 1.2% year-on-year), and net income attributable to owners of parent ¥1,739 million (up 23.5% year-on-year), all marking record highs.

- Operating income for the period was ¥1,440 million, a slight decrease of 0.2% compared to the previous fiscal year.

- The year-end dividend for FY2026/3 was set at ¥33.50 per share (including a commemorative dividend of ¥2.50), an increase from ¥27.50 in the previous fiscal year.

- The company announced its decision to voluntarily adopt International Financial Reporting Standards (IFRS) from FY2027/3, providing consolidated earnings forecasts under IFRS, including revenue of ¥10,000 million and net income attributable to owners of parent of ¥1,100 million.

- In terms of consolidated cash flows for FY2026/3, cash flows from operating activities were a net inflow of ¥1,853 million, cash flows from investing activities were a net inflow of ¥1,146 million, and cash and cash equivalents at the end of the period totaled ¥5,489 million.

🤖 AI Perspective

The FY2026/3 results show record highs in net sales, ordinary income, and net income attributable to owners of parent, suggesting strong business growth and improved profitability. While operating income saw a slight decrease, the increase in ordinary and net income could indicate positive contributions from non-operating income or extraordinary gains. The decision to voluntarily adopt IFRS for the next fiscal year may reflect the company’s commitment to aligning with international financial reporting standards.

3979|G-うるる

365.0

▲ +3.99%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-ULURU’s consolidated financial results for the full fiscal year ended March 31, 2026, exceeded the forecasts announced on February 13, 2026.

- Net sales reached JPY 7,751 million, marking a record high for 10 consecutive periods since the company’s listing.

- Profit attributable to owners of parent was JPY 737 million, surpassing the previous forecast (JPY 550-600 million) by 22.9% to 34.1%.

- The company announced a revision to its year-end dividend forecast for the fiscal year ended March 31, 2026, increasing it by JPY 1.00 from JPY 3.00 to JPY 4.00 per share.

- Per-share figures for both earnings and dividends are adjusted to reflect the 4-for-1 stock split that took effect on October 1, 2025.

🤖 AI Perspective

The company’s stronger-than-expected consolidated earnings and the upward revision of its year-end dividend may suggest solid operational performance and a commitment to shareholder returns. The growth in net sales, attributed to the core NJSS business, alongside optimized revenue structure and efficient marketing investments, appears to have contributed to the profit improvements. The stated dividend policy, aiming for progressive dividends with a payout ratio of 15% or more, could be a point of interest for long-term investors.

4172|Hiクラテス

2347.0

▲ +1.38%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hi-Crates Corporation announced its non-consolidated financial results for the second quarter of the fiscal year ending September 2026 on May 13, 2026.

- For the cumulative interim period (October 1, 2025 – March 31, 2026), the company reported net sales of ¥1,279 million (up 3.4% year-on-year), operating income of ¥379 million (up 10.0%), ordinary income of ¥424 million (up 3.3%), and net income for the interim period of ¥281 million (up 1.4%).

- The interim profit levels surpassed the revised Q2 forecasts announced on February 13, 2026, achieving a new record high.

- As of the end of the interim accounting period, total assets stood at ¥4,853 million, net assets at ¥4,361 million, and the equity ratio was 89.9%.

- The full-year forecast for FY2026 remains unrevised, projecting net sales of ¥2,484 million (up 3.2% year-on-year), operating income of ¥562 million (up 2.3%), ordinary income of ¥662 million (up 1.6%), and net income of ¥451 million (up 0.8%).

4595|ミズホメディー

1746.0

▲ +0.63%

📎 Source:ミズホメディー Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of fiscal year 2026 (January 1 to March 31, 2026), net sales were ¥2.208 billion (down 16.7% year-on-year), and operating income was ¥759 million (down 32.3% year-on-year).

- Quarterly net income reached ¥601 million (down 22.6% year-on-year), with quarterly net income per share at ¥31.57.

- The company’s financial position shows total assets of ¥20.934 billion, net assets of ¥18.333 billion, and an equity ratio of 87.6%.

- The full-year earnings forecast and annual dividend forecast (¥100) for fiscal year 2026 remain unchanged from the most recently published figures.

- The company noted that while overall sales of COVID-19 diagnostic drugs decreased, shipments of rapid antigen test kits for simultaneous detection of COVID-19 and influenza viruses increased.

🤖 AI Perspective

The decline in Q1 sales and profits year-on-year appears to be influenced by a normalization of COVID-19 related testing demand and a shift from gene testing to antigen testing. However, increased demand for combination test kits suggests adaptability to evolving market needs. The reaffirmation of full-year forecasts may indicate the company’s confidence in its strategic initiatives, including new product development such as the “QuickChaser CARBA RESIST-6 RUO” and “SmartGene H.pylori S” in the pipeline.

6059|ウチヤマHD

356.0

▲ +1.14%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, Uchiyama HD reported consolidated net sales of JPY 29,577 million (up 1.6% year-on-year), operating profit of JPY 551 million (up 164.6% year-on-year), and ordinary profit of JPY 851 million (up 50.6% year-on-year).

- Net profit attributable to owners of the parent decreased by 85.6% year-on-year to JPY 296 million.

- The annual dividend for FY2026/3 was set at JPY 10.00 per share (JPY 5.00 interim, JPY 5.00 year-end), consistent with the previous fiscal year. The company forecasts an annual dividend of JPY 10.00 per share for FY2027/3.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of JPY 30,084 million (up 1.7% year-on-year), operating profit of JPY 673 million (up 22.0% year-on-year), and net profit attributable to owners of the parent of JPY 293 million (down 0.8% year-on-year), with EPS of JPY 15.15.

- In its nursing care business, the company launched three new internal certification programs: “Excretion Care Specialist,” “Dementia Care Leader,” and “Care Creator,” and established “Rank 2 Up” certification.

- The company is advancing “INOVELBASE,” a next-generation nursing care research lab.

🤖 AI Perspective

- Uchiyama HD’s substantial increase in operating profit for FY2026/3, despite a modest rise in net sales, may suggest an improvement in operational efficiency.

- However, the significant decrease in net profit attributable to owners of the parent could be influenced by specific factors, such as the absence of extraordinary gains recorded in the prior year, warranting close monitoring of contributing elements.

- The FY2027/3 forecast indicates continued growth in sales and operating profit, while net profit attributable to owners of the parent is projected to remain relatively stable, suggesting ongoing efforts toward sustainable profitability.

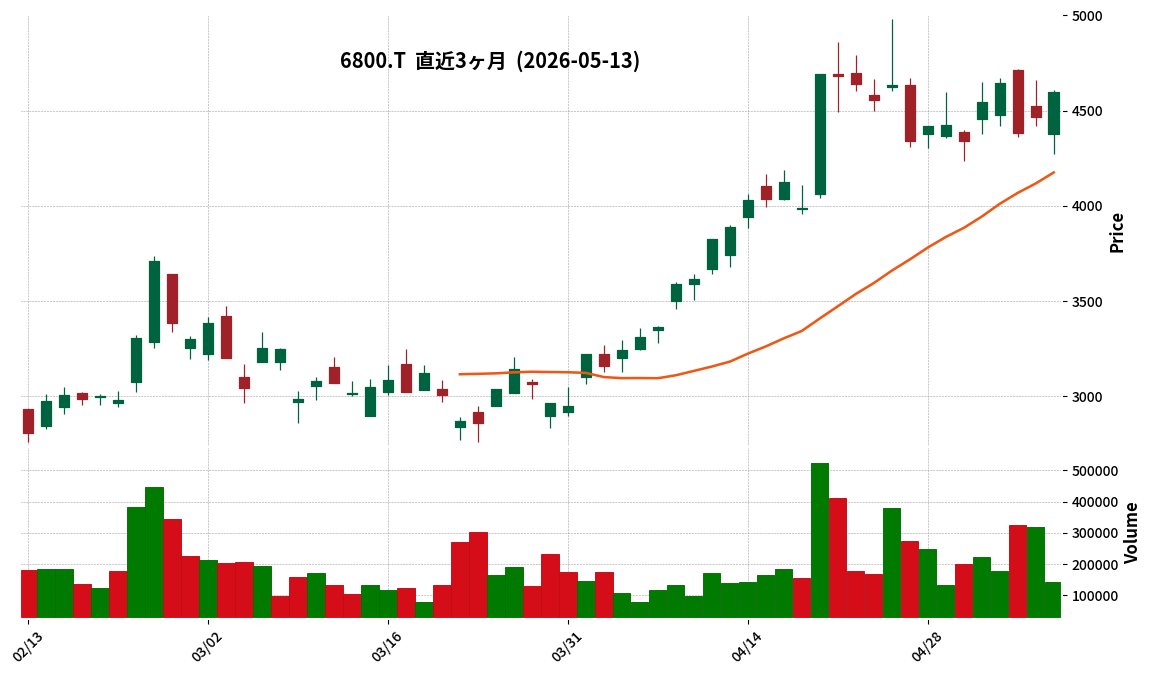

6800|ヨコオ

4600.0

▲ +3.02%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Yokowo’s consolidated net sales for the fiscal year ended March 31, 2026, totaled ¥90,090 million, marking an 8.7% increase year-on-year.

- For the same period, consolidated operating profit was ¥5,016 million (up 18.7%), ordinary profit was ¥5,528 million (up 40.8%), and net profit attributable to owners of parent reached ¥3,886 million (up 74.4%).

- The annual dividend for FY2026/3 was ¥56.00 per share, comprising an interim dividend of ¥25.00 and a year-end dividend of ¥31.00.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥97,000 million (up 7.7% year-on-year) and net profit attributable to owners of parent of ¥4,500 million (up 15.8% year-on-year).

- The projected annual dividend for FY2027/3 is ¥64.00 per share, with interim and year-end dividends each expected to be ¥32.00.

🤖 AI Perspective

Yokowo’s strong performance in FY2026/3, with significant increases across all profit lines, particularly a 74.4% rise in net profit, indicates a robust period for the company. The explanatory notes suggest that growth was driven by increased sales across all segments, a substantial improvement in the CTC segment’s profit, and foreign exchange gains, reflecting favorable market conditions and operational efficiencies. The positive outlook for FY2027/3, including projected continued revenue and profit growth, suggests the company anticipates sustained momentum in its business operations and a favorable market environment.

7561|ハークスレイ

658.0

▲ +1.70%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hurxley Co., Ltd. announced its consolidated financial results for the fiscal year ended March 31, 2026, reporting net sales of ¥52,427 million (up 16.1% year-on-year), operating profit of ¥3,057 million (up 58.3%), ordinary profit of ¥3,003 million (up 44.3%), and profit attributable to owners of parent of ¥1,483 million (up 23.2%). All profit items set new record highs.

- By segment, the Logistics & Food Processing Business recorded net sales of ¥23,758 million (up 31.3% year-on-year), showing significant growth. The Store Asset & Solution Business also performed robustly with net sales of ¥14,331 million (up 17.6%) and operating profit of ¥2,228 million (up 28.4%).

- The annual dividend for the fiscal year ended March 31, 2026, was ¥28.00 per share (¥14.00 interim, ¥14.00 year-end), an increase from ¥26.00 in the previous fiscal year.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥55,500 million (up 5.9% year-on-year), operating profit of ¥2,800 million (down 8.4%), ordinary profit of ¥2,600 million (down 13.4%), and profit attributable to owners of parent of ¥1,600 million (up 6.6%).

- An annual dividend of ¥30.00 per share (¥15.00 interim, ¥15.00 year-end) is planned for the fiscal year ending March 31, 2027.

🤖 AI Perspective

The strong performance in FY2026, with record high sales and profits, suggests robust growth driven by key segments like Logistics & Food Processing and Store Asset & Solution. While the FY2027 forecast anticipates continued revenue growth, the projected decline in operating and ordinary profit may indicate expected increases in operating costs or strategic investments. The planned consecutive dividend increase could be seen as a positive sign regarding shareholder returns.

7864|フジシール

2498.0

▲ +0.69%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Fujiseal International (7864) resolved to revise its dividend policy and adjust its FY2026 year-end dividend forecast at a Board of Directors meeting held on May 13, 2026.

- The revised dividend policy maintains a target consolidated payout ratio of 30% and includes a new provision to adjust for significant fluctuations in net profit caused by one-off or non-recurring factors.

- The year-end dividend forecast for FY2026 has been revised upward by ¥10, from the previously announced ¥36 (on February 12, 2026) to ¥46.

- Consequently, the full-year dividend forecast for FY2026 is expected to be ¥81, an increase of ¥10 from the previous forecast of ¥71.

- The reason for the policy change is to ensure stable and continuous dividends based on core earnings power, avoiding significant fluctuations driven by short-term, temporary profit variations.

🤖 AI Perspective

The new dividend policy, by adjusting for one-off profit fluctuations, may suggest the company’s intent to maintain a more stable dividend level in an environment of potentially volatile earnings. The removal of DOE (Dividend on Equity) as a specific consideration from the policy could indicate a shift towards prioritizing the payout ratio as a key metric for capital efficiency. This upward revision in the annual dividend forecast, alongside the new policy, can be seen as a proactive move towards shareholder returns while emphasizing stability.

1711|SDSHD

255.0

▲ +1.19%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SDS Holdings Co., Ltd. resolved on May 13, 2026, to fully acquire HARUMI TRUST Co., Ltd. (HT Co.), in which it currently holds a 35% stake.

- The company will acquire an additional 650 shares at a price of JPY 6.5 million, resulting in 100% ownership of HT Co.’s 1,000 shares.

- This transaction is classified as a related-party transaction, as SDS Holdings’ Chairman, Katsuhide Yoshino, held a 65% stake in HT Co., and was approved following deliberation by a compliance committee.

- HT Co.’s business scope includes renewable energy, real estate, investment, as well as the acquisition, holding, management, and trading of cryptocurrencies (Bitcoin, Ethereum, etc.), precious metals, and financial instruments.

- SDS Holdings positions M&A and investment strategies as core activities for its group investment company, with cryptocurrency acquisition aimed at payment processing for its AI data center business, and minority and equity investments (M&A) intended for portfolio diversification and new revenue opportunities.

🤖 AI Perspective

The full acquisition of HARUMI TRUST by SDS Holdings may suggest an intent to accelerate and consolidate its M&A and investment strategies, particularly in the cryptocurrency and broader investment sectors. The mention of cryptocurrency acquisition for AI data center payment processes could indicate a strategic move to integrate digital assets into core operations. Furthermore, the explicit disclosure and compliance committee review for this related-party transaction highlight the company’s efforts towards transparency in governance.

194A|G-WOLVES

1630.0

▲ +3.82%

📎 Source:G-WOLVES Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the nine months ended March 31, 2026, consolidated net sales reached ¥4,318 million (up 13.6% year-on-year), operating income was ¥674 million (up 43.6% year-on-year), and ordinary income was ¥687 million (up 34.7% year-on-year).

- Net income attributable to parent shareholders for the cumulative period was ¥597 million (up 98.5% year-on-year).

- Three companies, Asuka Medical Co., Ltd., See Co., Ltd., and Caltech Co., Ltd., were newly included in the scope of consolidation during this cumulative period.

- The equity ratio at the end of the third quarter of fiscal year 2026 improved to 51.8%, from 44.9% at the end of fiscal year 2025.

- The refinancing for LBO-related loans was completed in December 2025.

🤖 AI Perspective

The company’s performance for the quarter, with significant year-on-year growth across net sales and all profit metrics, particularly the near-doubling of net income attributable to parent shareholders, suggests the M&A strategy and existing business growth are yielding positive results. The reported operational efficiencies from group management may also be contributing to the improved profitability. Furthermore, the enhancement in the equity ratio and the completion of loan refinancing could indicate a strengthening financial position, potentially supporting future expansion plans.

1982|日比谷設

3260.0

▲ +2.03%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hibiya Set Co., Ltd. has resolved to distribute surplus dividends for the fiscal year ended March 31, 2026, with the record date set as March 31, 2026.

- The year-end dividend per share for FY2026 (post-stock split) is ¥50, resulting in an annual dividend of ¥75 when combined with the interim dividend of ¥25. This aligns with the dividend forecast announced on February 10, 2026, and represents an effective increase from the previous fiscal year’s (FY2025) annual dividend of ¥50 (post-stock split equivalent).

- For FY2027 (April 1, 2026, to March 31, 2027), the company forecasts an interim and year-end dividend of ¥55 per share each (ordinary dividend ¥50, commemorative dividend ¥5), bringing the total annual dividend forecast to ¥110.

- The commemorative dividend, consisting of an additional ¥5 each for interim and year-end, is planned to celebrate the company’s 60th anniversary in July 2026.

- All stated dividend amounts are presented post-stock split, following a 1-for-2 stock split of common shares effective April 1, 2026.

🤖 AI Perspective

This announcement indicates that the annual dividend for FY2026 has been set at ¥75 (post-stock split), representing an effective increase from the prior year. Furthermore, the company forecasts an annual dividend of ¥110 (post-stock split) for FY2027, including a commemorative dividend for its 60th anniversary, which could suggest a strong commitment to continuous shareholder returns. The implementation of a commemorative dividend, in particular, may be viewed by investors as a noteworthy initiative by the company to express gratitude to shareholders as it reaches a significant milestone.

3402|東レ

1161.0

▲ +1.35%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Toray announced its consolidated financial results for the fiscal year ended March 31, 2026, reporting revenue of JPY 2,585.1 billion, a 0.9% increase year-on-year.

- Business profit decreased by 0.6% to JPY 141.9 billion, and operating profit declined by 23.7% to JPY 97.2 billion. This decrease in operating profit was attributed primarily to impairment losses recorded in the battery separator film business of its Korean subsidiary.

- Profit attributable to owners of the parent increased by 2.1% year-on-year to JPY 79.5 billion.

- The annual dividend for FY2026 was raised to JPY 20.00 (JPY 10.00 interim, JPY 10.00 year-end) from JPY 18.00 in FY2025.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated revenue of JPY 2,830.0 billion (up 9.5% year-on-year), business profit of JPY 160.0 billion (up 12.7%), and profit attributable to owners of the parent of JPY 90.0 billion (up 13.2%).

🤖 AI Perspective

- While consolidated revenue saw a modest increase and operating profit decreased due to impairment losses, the growth in profit attributable to owners of the parent suggests that other factors, such as a significant positive swing in share of profit (loss) of investments accounted for using the equity method from a negative JPY 2.35 billion to a positive JPY 21.53 billion, supported the final profit figure.

- The increase in the annual dividend for FY2026 and the forecast for a further substantial increase, including a commemorative dividend, for FY2027 may indicate a strengthened focus on shareholder returns.

- The positive outlook for FY2027, projecting growth across all key profit metrics, will be a significant point for investors to monitor for future performance trends.

6269|三井海洋

12720.0

▼ -2.57%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Mitsui Ocean Development & Engineering Co., Ltd. (MODEC) announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026 to March 31, 2026).

- For the first quarter, revenue increased by 23.4% year-on-year to US$1,077,078 thousand, and operating profit rose by 63.2% to US$122,741 thousand.

- Profit attributable to owners of the parent was US$99,144 thousand, marking a 78.2% increase year-on-year, with basic earnings per share at US$1.45.

- The full-year consolidated earnings forecast for fiscal year 2026 remains unchanged, projecting revenue of US$4,600,000 thousand (up 0.4% year-on-year), operating profit of US$460,000 thousand (up 5.1% year-on-year), and profit attributable to owners of the parent of US$370,000 thousand (up 2.6% year-on-year).

- Order intake for the first quarter totaled US$129,315 thousand, a 97.3% decrease from the same period last year, while order backlog stood at US$17,859,461 thousand, down 3.9% from the end of the previous fiscal year.

🤖 AI Perspective

MODEC’s first-quarter results show significant increases in revenue and various profit metrics, largely driven by the steady progress of existing FPSO construction projects. However, the substantial year-on-year decline in new order intake could be a point of consideration when evaluating future performance. The company’s decision to maintain its full-year forecast may suggest that current project progress is aligning with their expectations.

8075|神鋼商

2304.0

▼ -0.65%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Shinsho Corporation reported consolidated financial results for the fiscal year ended March 31, 2026, with net sales of ¥608,142 million (down 1.5% year-on-year), operating profit of ¥11,577 million (down 12.4%), ordinary profit of ¥11,022 million (down 6.3%), and profit attributable to owners of parent of ¥8,286 million (down 3.2%).

- As of March 31, 2026, the consolidated financial position showed total assets of ¥383,623 million, net assets of ¥100,982 million, and an equity ratio of 25.8%.

- The annual dividend for the fiscal year ended March 31, 2026, was ¥106.00 per share (interim ¥53.00, year-end ¥53.00), adjusted for the stock split (1-for-3 on April 1, 2025).

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥686,000 million (up 12.8% year-on-year), operating profit of ¥12,100 million (up 4.5%), ordinary profit of ¥11,500 million (up 4.3%), and profit attributable to owners of parent of ¥9,000 million (up 8.6%).

- The forecast for the annual dividend for the fiscal year ending March 31, 2027, is ¥130.00 per share (interim ¥65.00, year-end ¥65.00), which includes a commemorative dividend of ¥13.00 for the year-end.

🤖 AI Perspective

The decline in results for the fiscal year 2026 may be attributed to a generally decelerating global economy and subdued domestic demand. However, the projected increase in both revenue and profits for the fiscal year 2027 suggests an anticipated recovery in business conditions or the expected fruition of strategic initiatives. The planned increase in the dividend for fiscal year 2027 could also indicate the company’s commitment to shareholder returns, which investors may find noteworthy.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

3405|クラレ

1740.0

▲ +3.57%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- **Q1 FY2026 Consolidated Results**: Kuraray reported net sales of JPY 200,913 million (up 3.1% year-on-year), while operating income decreased by 20.3% to JPY 14,870 million, ordinary income fell by 22.9% to JPY 13,745 million, and net profit attributable to owners of parent declined by 35.0% to JPY 7,802 million.

- **Full-Year Consolidated Forecast**: The full-year consolidated performance forecast for FY2026 remains unchanged, projecting net sales of JPY 850,000 million, operating income of JPY 70,000 million, ordinary income of JPY 64,000 million, and net profit attributable to owners of parent of JPY 40,000 million.

- **Annual Dividend Forecast**: The projected annual dividend for FY2026 is JPY 64.00 per share (JPY 32.00 for Q2, JPY 32.00 for year-end), which includes a regular dividend of JPY 54.00 and a commemorative dividend of JPY 10.00, with no changes from the most recently announced forecast.

- **Segment Performance**: The Vinyl Acetate segment saw increased sales but decreased operating income. The Isoprene segment reported increased sales and operating income. The Functional Materials segment achieved increased sales and operating income. The Fibers segment moved from an operating loss to a profit with increased sales.

- **Forecast Assumption**: The consolidated earnings forecast has not been revised at this time due to the difficulty in establishing a reasonable outlook given the worsening situation in the Middle East. The impact of the share buyback, which concluded on March 23, 2026, has been incorporated into the “EPS” forecast.

🤖 AI Perspective

While Kuraray achieved increased net sales in Q1, a significant decrease in key profit metrics year-on-year could indicate challenges in operational efficiency and pricing strategies, potentially exacerbated by global uncertainties. The decision to maintain the full-year forecast, despite the Q1 profit decline and the mention of Middle East uncertainties, may suggest management anticipates a recovery in later quarters or has already factored in these challenges. Investors may wish to monitor future updates regarding the impact of geopolitical factors and the progress of profit recovery in specific segments.

4005|住友化

548.8

▲ +4.85%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sumitomo Chemical Co., Ltd. announced on May 13, 2026, the signing of a share exchange agreement to make Koei Chemical Co., Ltd. a wholly owned subsidiary.

- The share exchange will be conducted as a simplified share exchange, with Sumitomo Chemical as the wholly owning parent company. The effective date is scheduled for August 1, 2026, and Koei Chemical is expected to be delisted from the Tokyo Stock Exchange Standard Market on July 30, 2026 (last trading day: July 29, 2026).

- Sumitomo Chemical first made a capital investment in Koei Chemical in 1951, making it a consolidated subsidiary in 1954. As of today, Sumitomo Chemical owns 55.74% (2,731,400 shares) of Koei Chemical’s common stock.

- The purpose of the wholly owned subsidiary conversion includes technological development through combining both companies’ expertise, expansion of Sumitomo Chemical’s advanced small-molecule CDMO business utilizing Koei Chemical’s multi-plants, and accelerated/efficient business operations through integrated management.

- Koei Chemical established a special committee on November 17, 2025, to ensure the fairness of the share exchange.

🤖 AI Perspective

This move by Sumitomo Chemical to fully integrate its long-standing consolidated subsidiary, Koei Chemical, suggests a strategic effort to streamline group management and maximize synergistic effects. The planned utilization of Koei Chemical’s multi-plants to strengthen Sumitomo Chemical’s advanced small-molecule CDMO business could be a key component of its future growth strategy. Koei Chemical’s general shareholders, receiving Sumitomo Chemical shares, may gain the opportunity to benefit from the increased corporate value of the combined group post-integration.

4114|日触媒

2227.0

▲ +1.81%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nippon Shokubai Co., Ltd. announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- Consolidated revenue for the period was ¥399,898 million, a 2.3% decrease from the previous fiscal year. Operating profit was ¥17,530 million, down 8.0%, and profit for the period attributable to owners of the parent was ¥16,764 million, a decrease of 3.6%.

- Key factors for the revenue decrease included a decline in selling prices due to overseas product market conditions and raw material prices, despite an increase in sales volume. The profit decline was primarily attributed to a shift from inventory valuation gains in the previous year to losses in the current period, along with increases in manufacturing fixed costs and selling, general, and administrative expenses.

- The annual dividend for the fiscal year ended March 31, 2026, was announced as ¥113.00 per share (interim ¥50.00, year-end ¥63.00).

- The consolidated earnings forecast for the fiscal year ending March 31, 2027 (April 1, 2026 – March 31, 2027), is currently undetermined due to the difficulty in reasonably calculating the impact of heightened tensions in the Middle East.

🤖 AI Perspective

The decline in revenue and profit appears to stem from a combination of fluctuating product market conditions, raw material prices, and inventory valuation effects. Maintaining the annual dividend at a similar level to the previous year may indicate the company’s commitment to shareholder returns. The undetermined outlook for the next fiscal year highlights the potential impact of geopolitical uncertainties in the Middle East, which investors may find worth monitoring.

4183|三井化学

1995.5

▲ +2.25%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Mitsui Chemicals announced its consolidated financial results for the fiscal year ended March 31, 2026. Revenue was JPY 1,668,754 million (down 7.8% year-on-year), profit attributable to owners of the parent was JPY 34,378 million (up 6.6% year-on-year), and core operating profit was JPY 100,028 million (down 0.9% year-on-year).

- Basic earnings per share for FY2026/3 were JPY 91.62.

- The total annual dividend for FY2026/3, without considering the stock split, was JPY 150.00 per share.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated revenue of JPY 1,900,000 million (up 13.9% year-on-year) and profit attributable to owners of the parent of JPY 45,000 million (up 30.9% year-on-year).

- The forecasted annual dividend for FY2027/3, on a post-stock split basis, is JPY 75.00 per share.

- A 2-for-1 stock split of common shares was implemented effective January 1, 2026.

🤖 AI Perspective

For the fiscal year 2026/3, the company reported a decrease in revenue and core operating profit, yet an increase in profit attributable to owners of the parent, which may suggest impacts from changes in profit structure or non-recurring items. The optimistic forecast for fiscal year 2027/3, projecting significant increases in both revenue and profit, could indicate the company’s expectation of business environment recovery or successful initiatives. The 2-for-1 stock split, effective January 1, 2026, might aim to reduce the per-share investment amount, potentially broadening the investor base.

4367|広栄化学

2217.0

▲ +2.12%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Koei Chemical Co., Ltd. reported for the fiscal year ended March 2026: net sales of ¥17,009 million (down 15.0% year-on-year), operating profit of ¥364 million (down 35.6% year-on-year), and ordinary profit of ¥255 million (down 28.3% year-on-year).

- Net income resulted in a loss of ¥5,135 million (compared to a profit of ¥288 million in the previous fiscal year) due to the recording of an impairment loss.

- The company’s financial position shows total assets decreased to ¥29,869 million (down ¥5,349 million from the previous fiscal year-end) and net assets decreased to ¥16,089 million (down ¥5,526 million). The equity ratio declined from 61.4% to 53.9%.

- The annual dividend for the fiscal year ended March 2026 was ¥80.00 (compared to ¥100.00 in the previous fiscal year).

- The company plans a share exchange with Sumitomo Chemical Co., Ltd. and is scheduled to be delisted on July 30, 2026. Consequently, no earnings or dividend forecast for the fiscal year ending March 2027 has been announced.

🤖 AI Perspective

The significant net loss, primarily driven by an impairment loss and decreased sales in pharmaceutical/agrochemical-related and optical material products, suggests challenges in core business areas. The decline in the equity ratio also indicates a weakening of the financial structure. The upcoming delisting due to the share exchange with Sumitomo Chemical signifies a major corporate transition, which will alter its status in the public market.

4506|住友ファーマ

1566.5

▼ -2.67%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sumitomo Pharma reported consolidated results (core basis) for FY2025 (ending March 2026), with revenue of ¥453.3 billion (up 13.7% year-on-year), core operating profit of ¥105.9 billion (up 145.4% year-on-year), and profit attributable to owners of parent of ¥106.9 billion (up 352.2% year-on-year).

- The increase in revenue was primarily driven by the growth of key products Orgovyx and Gemtesa in North America, as well as sales milestone revenue.

- Selling, general and administrative expenses, and research and development expenses decreased due to business structure improvement effects, partial divestiture of the Asia business, and reorganization of the regenerative medicine and cell therapy business.

- For FY22026 (ending March 2027), the company forecasts consolidated results (core basis) of ¥540.0 billion in revenue (up 19.1% year-on-year), ¥91.0 billion in core operating profit (down 14.1% year-on-year), and ¥77.0 billion in profit attributable to owners of parent (down 27.9% year-on-year).

- The company announced a change in its consolidated segment reporting structure from FY2026, transitioning from regional segments (Japan/North America/Asia) to a single Pharmaceutical Business segment.

🤖 AI Perspective

- FY2025 saw substantial profit growth, which appears to be a result of strong performance from key products and the positive impact of business structural reforms addressing previous challenges.

- While the FY2026 forecast anticipates continued revenue growth, the projected decline in core operating profit may reflect increased research and development expenses and the absence of one-time gains from the Asia business divestiture seen in the prior year.

- The company’s “Boost 2028” strategy, focusing on rapid launch of two oncology products, fostering next-generation growth engines, and strengthening its financial base, indicates key areas for future performance monitoring.

4792|山田コンサル

1646.0

▲ +0.61%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- YAMADA Consulting Group Co., Ltd. reported consolidated net sales of ¥26,711 million (+17.3% year-on-year) and gross profit of ¥20,500 million (+5.5% year-on-year) for the fiscal year ended March 2026, both reaching record highs.

- For the same period, operating profit was ¥3,740 million (-9.4% year-on-year) and ordinary profit was ¥3,712 million (-9.4% year-on-year). However, profit attributable to owners of parent increased to ¥2,895 million (+0.4% year-on-year).