📌 Today’s Highlights

Today we cover 37 IR announcements. Notable among them: ニチハ (7943), タクマ (6013), 小野建 (7414). Use the table of contents below to navigate to each company.

- 3070|G-ジェリービーンズ

- 7943|ニチハ

- 6013|タクマ

- 7414|小野建

- 9235|G-売れるネットG

- 6167|冨士ダイス

- 490A|P-センス・トラスト

- 4735|京進

- 7213|レシップHD

- 7590|タカショー

- 7120|SHINKO

- 2323|fonfun

- 2311|エプコ

- 265A|G-エイチエムコム

- 3252|地主

- 4389|G-プロパティDBK

- 4570|G-免疫生物研究所

- 4689|LINEヤフー

- 6584|三桜工

- 6615|UMCエレ

- 8181|東天紅

- 9060|日ロジテム

- 3495|香陵住販

- 7176|P-シンプレクスFH

- 7247|ミクニ

- 7425|初穂商事

- 9828|ゲンキGDC

- 8059|第一実業

- 3063|G-jGroup

- 5573|P-働楽HD

- 4069|G-BlueMeme

- 8143|ラピーヌ

- 3905|G-データセクション

- 4060|G-rakumo

- 9348|G-ispace

- 5821|平河ヒューテ

- 6574|G-コンヴァノ

3070|G-ジェリービーンズ

86.0

▲ +4.88%

📎 Source:G-ジェリービーンズ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Jellybeans Group’s subsidiary, JB BLOCK Co., Ltd., signed a business alliance agreement with MY-ONE Co., Ltd. (MYONE) on May 28, 2026.

- This alliance aims to build a strategic partnership for the metaverse platform business in the Japanese market, following the acquisition of operating rights for the metaverse platform ‘MYONE’ on May 22, 2026.

- The partnership encompasses joint planning and execution of experiential marketing and event strategies, joint promotion of sales strategies utilizing the metaverse platform, joint development and execution of marketing strategies, and joint consideration of product and brand strategies.

- G-Jellybeans Group seeks to create new revenue opportunities through synergies with existing lifestyle and entertainment businesses, expansion into the healthcare sector, and strengthening mid-to-long-term business foundations by collaborating with local governments.

- MYONE Co., Ltd. is based in Seoul, Korea, with a capital of 55 million JPY, and reported sales of 1,697 million JPY and operating profit of 44 million JPY for the fiscal year ended December 2025.

🤖 AI Perspective

G-Jellybeans, through its subsidiary’s business alliance with MYONE, is making a full-scale entry into the metaverse business. This move follows the recent announcement of acquiring operating rights for the ‘MYONE’ platform, indicating an acceleration of their metaverse platform deployment in the Japanese market. The company explicitly outlines plans for diverse applications beyond lifestyle and entertainment, extending into healthcare and regional revitalization, which may suggest a broad strategy for revenue generation.

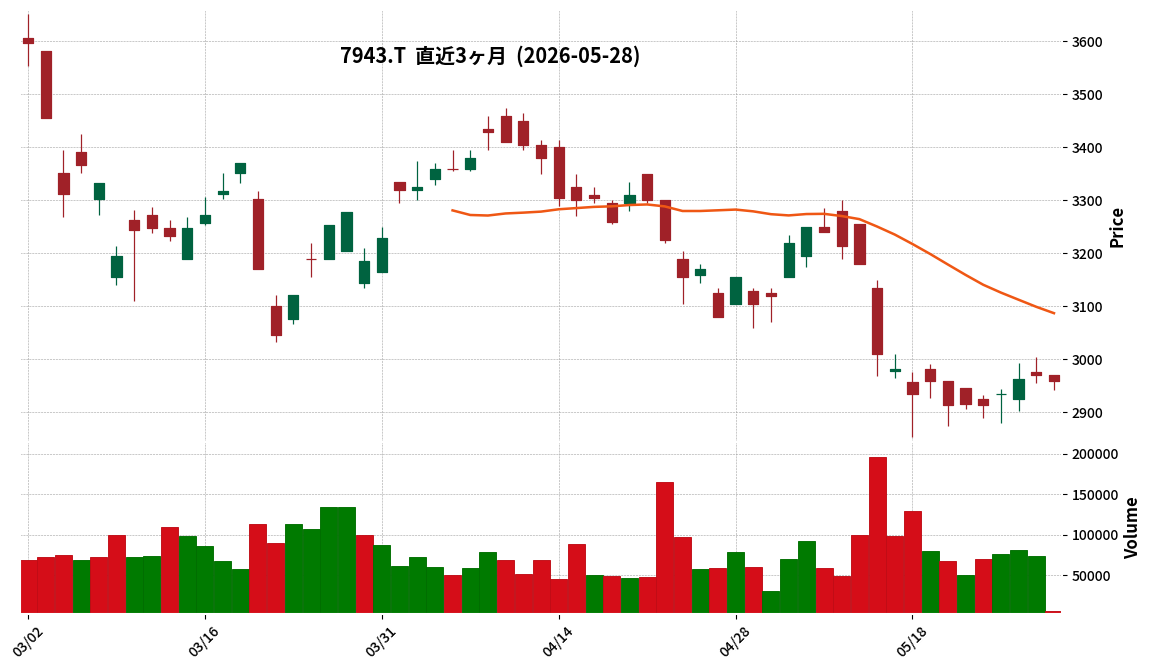

7943|ニチハ

2960.0

▼ -0.37%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nichiha announced its consolidated financial results for the fiscal year ended March 2026. Net sales totaled ¥143,740 million, a decrease of 3.2% year-over-year.

- Operating profit increased by 34.6% year-over-year to ¥9,355 million. Ordinary profit was ¥10,246 million (+41.3% YoY), while net profit attributable to parent company shareholders decreased by 8.1% to ¥2,486 million.

- The company recognized a special loss of ¥5,401 million in its U.S. business due to the withdrawal from the residential general-purpose exterior material business.

- Operating profit in the domestic business increased by ¥2,020 million year-over-year, reaching ¥6,560 million. Key contributing factors included sales factors (reduced sales volume, price revisions, domestic subsidiaries, etc.) with a positive contribution of ¥1,020 million, and inventory fluctuations (manufacturing fixed costs) with a positive contribution of ¥430 million.

- For the fiscal year ending March 2027, the company forecasts consolidated net sales of ¥141,000 million (-1.9% YoY), operating profit of ¥9,100 million (-2.7% YoY), and net profit attributable to parent company shareholders of ¥7,000 million (+181.7% YoY).

🤖 AI Perspective

Despite a decline in net sales, Nichiha achieved a significant increase in operating profit for the fiscal year ended March 2026, suggesting that the company was able to absorb special losses from its U.S. business restructuring while improving profitability in its domestic operations. The positive contributions from sales factors and inventory management in the domestic segment appear to be key drivers. The forecast for fiscal year 2027, which anticipates a substantial increase in net profit despite continued revenue decline, could indicate expected benefits from ongoing structural reforms.

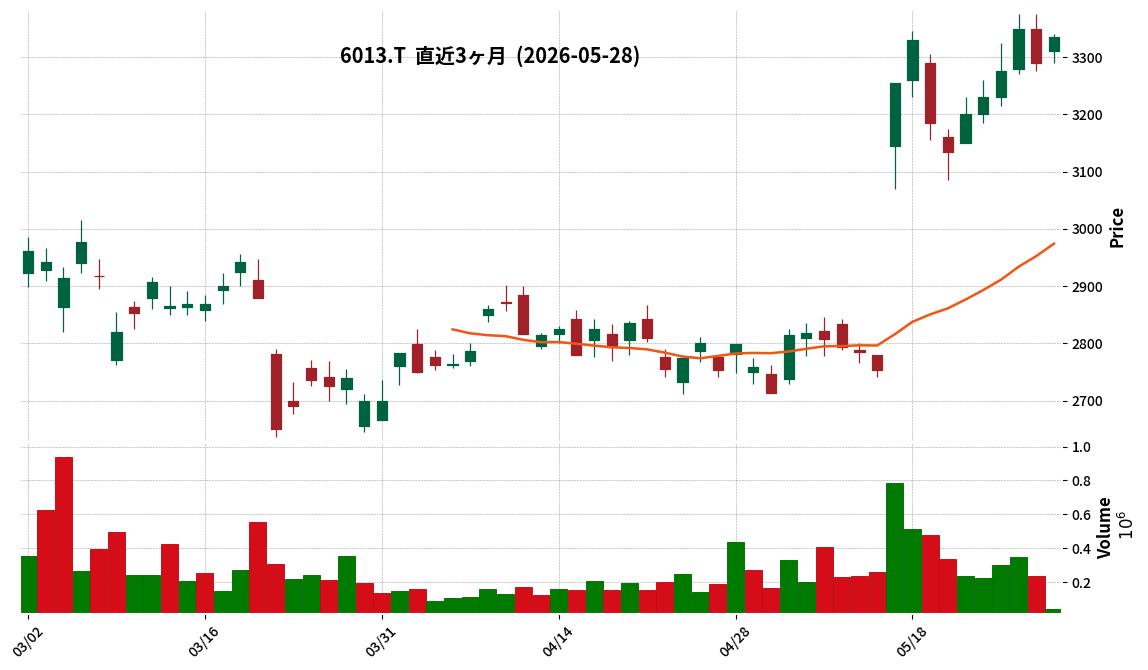

6013|タクマ

3335.0

▲ +1.37%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- TAKUMA CO., LTD. reported that its order intake for the fiscal year ended March 31, 2026 (FY2026) reached ¥333.0 billion, significantly exceeding its initial target of ¥250.0 billion, marking a second consecutive year of record-high order intake.

- For FY2026, net sales were ¥165.6 billion, operating profit was ¥15.4 billion, and net profit attributable to parent company shareholders was ¥13.7 billion, achieving a record-high net profit for the second consecutive year.

- The increase in order intake was primarily driven by five new municipal solid waste treatment plant renewal projects and two major renovation projects in the domestic Environment & Energy business, as well as the consolidation of IHI General Boiler Co., Ltd. in the Civil Thermal Energy business.

- For the fiscal year ending March 31, 2027 (FY2027), the company forecasts net sales of ¥191.0 billion, operating profit of ¥17.8 billion, and net profit attributable to parent company shareholders of ¥15.4 billion, which would represent the highest net sales since FY2002 and a third consecutive year of record-high net profit.

🤖 AI Perspective

TAKUMA’s FY2026 results, featuring record-high order intake and net profit, may suggest robust business expansion. The strong order performance in the domestic Environment & Energy segment could indicate a strengthening of its long-term revenue base. The projected third consecutive year of record-high net profit for FY227 may further underscore the company’s growth trajectory.

7414|小野建

1342.0

▲ +0.30%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Onoken reported net sales of 253,115 million yen (down 6.9% year-on-year) and operating profit of 4,740 million yen (down 30.4% year-on-year) for the fiscal year ended March 2026.

- The company recorded a net loss attributable to owners of the parent of 2,218 million yen, marking its first net loss since listing.

- The primary cause for the net loss was the recognition of impairment losses on fixed assets in the Kyushu and Chugoku regions as extraordinary losses.

- Despite the net loss, Onoken declared a dividend of 69 yen per share for FY2026, adhering to its minimum dividend policy.

- For the fiscal year ending March 2027, the company forecasts an increase in revenue and profit, a return to net profitability, and plans to maintain a minimum annual dividend of 69 yen per share.

🤖 AI Perspective

The net loss for FY2026 appears to be significantly impacted by a one-time impairment loss on fixed assets, in addition to subdued steel demand. However, the projected return to profitability and increase in both revenue and profit for FY2027, driven by rising steel market prices and large project orders, could be a key point for investors. The company’s commitment to maintaining its minimum dividend policy, even after reporting a net loss, may suggest a stable approach to shareholder returns.

9235|G-売れるネットG

582.0

▼ -1.02%

📎 Source:G-売れるネットG Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-UrerunetG has resolved to enter a basic agreement for the acquisition of shares in Parrotebeak Inc., a mobile system and telecommunications company, making it a wholly-owned subsidiary.

- Parrotebeak Inc. reported sales of 1,463 million JPY, operating income of 6 million JPY, ordinary income of 8 million JPY, and net income of 7 million JPY for the fiscal year ended September 2025.

- Parrotebeak Inc. specializes in “mobile systems for local governments” and “mobile communication services,” with its government-向け mobile systems business characterized by stable, recurring revenue from long-term contracts.

- G-UrerunetG aims to strengthen and expand its business foundation in the telecommunications infrastructure sector through synergy with its consolidated subsidiary, JCNT Co., Ltd.

- The planned execution date for this share acquisition is August 1, 2026, with the acquisition price expected to be 15% or more of G-UrerunetG’s net assets from the immediately preceding fiscal year.

🤖 AI Perspective

This announcement suggests G-UrerunetG’s strategic move to bolster its existing telecommunications businesses and secure new revenue streams. The stable, recurring revenue from Parrotebeak’s government-向け mobile systems and the growth potential in its mobile communication sector could contribute to the group’s overall business portfolio stability and expansion. Investors may want to monitor how the stated synergies, particularly in enhancing JCNT’s SIM/eSIM capabilities and addressing inbound demand, translate into future corporate value.

6167|冨士ダイス

1008.0

▼ -0.40%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Fuji Die Co., Ltd. reported consolidated results for the fiscal year ended March 2026, with net sales of ¥17,446 million (up 5.1% year-on-year) and operating profit of ¥822 million (up 68.5% year-on-year).

- Operating profit for the period exceeded the company’s forecast of ¥600 million by 37.1%, attributed to increased sales, reduced outsourcing costs, and lower electricity and fuel expenses.

- For the fiscal year ending March 2027, the company forecasts net sales of ¥26,000 million (up 49.0% year-on-year) and operating profit of ¥700 million (down 14.9% year-on-year). While sales are expected to increase due to price revisions for higher raw material costs, operating profit is anticipated to decrease due to the impact of surging raw material costs and a projected reduction in sales volume following price adjustments.

- The company highlighted changes in the business environment, specifically China’s enhanced export controls on critical minerals, including tungsten.

- Fuji Die announced the initiation of discussions with Dijet Industrial Co., Ltd. regarding a business alliance for alloys with reduced tungsten and cobalt content. This collaboration aims to expand sales channels by leveraging both companies’ networks and mitigate geopolitical risks.

🤖 AI Perspective

Fuji Die’s fiscal year 2026/3 results show a significant increase in operating profit, largely exceeding forecasts, driven by cost efficiencies despite sales slightly missing targets. The outlook for fiscal year 2027/3, projecting increased revenue but decreased profit, suggests that the impact of rising raw material costs and subsequent price adjustments on sales volumes is a key concern. The proposed alliance with Dijet Industrial for alloys with reduced critical mineral content appears to be a proactive strategic move to address geopolitical risks related to tungsten supply and enhance long-term corporate value.

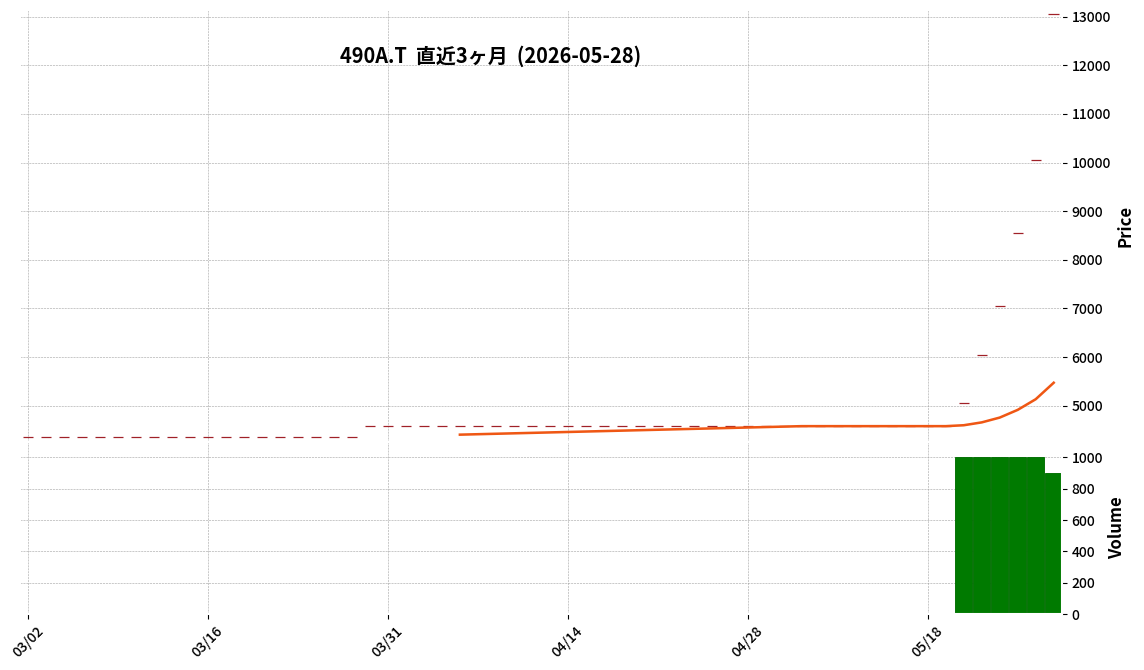

490A|P-センス・トラスト

13050.0

▲ +29.85%

📎 Source:P-センス・トラスト Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- P-Sense Trust announced on May 28, 2026, a partial correction to its Non-consolidated Financial Results for the fiscal year ended March 2026.

- The reason for the correction is that errors were found in the financial statements and main notes included in the earnings report initially disclosed on May 15, 2026.

- The correction specifically pertains to the “Total changes during the period” section within “(3) Statement of Changes in Equity.”

- Prior to the correction, “Total changes during the period” for “Total shareholders’ equity” and “Total net assets” was ¥1,257,447 thousand.

- Following the correction, “Total changes during the period” for “Total shareholders’ equity” and “Total net assets” has been revised to ¥1,107,447 thousand.

- The “Balance at end of current period” for “Total shareholders’ equity” and “Total net assets” remains unchanged at ¥2,901,564 thousand after the correction.

🤖 AI Perspective

This correction primarily concerns specific figures within the “Total changes during the period” in the Statement of Changes in Equity, while the final balance at the end of the period remains unaffected. Such revisions to financial statements are significant for investors, suggesting a need to carefully review the detailed announcement. This action can be seen as an effort by the company to ensure the accuracy of its disclosed financial information.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

4735|京進

320.0

▼ -0.31%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kyoshin Co., Ltd. changed its fiscal year-end from May to February, effective with the resolution at the Ordinary General Meeting of Shareholders on August 28, 2025. The fiscal year ending February 2026 covers an irregular 9-month period from June 1, 2025, to February 28, 2026.

- Consolidated results for the fiscal year ending February 2026 (irregular 9-month period) reported net sales of ¥20,286 million, operating profit of ¥481 million, and ordinary profit of ¥470 million, exceeding initial forecasts.

- The increase in net sales was driven by a smooth intake of new students in the Japanese language education business and the contribution from Linkheart Co., Ltd. in the nursing care business.

- By segment, the childcare and nursing care business significantly contributed with sales of ¥9,274 million, an increase of ¥527 million compared to the adjusted prior-year period, while the language-related business also grew by ¥80 million to ¥3,336 million.

- In the cram school business, segment profit increased by ¥74 million to ¥1,326 million compared to the adjusted prior-year period, attributed to cost structure optimization through the consolidation and abolition of unprofitable locations.

🤖 AI Perspective

Kyoshin’s latest IR release highlights its ability to exceed initial forecasts despite an irregular fiscal year due to a change in the financial reporting period. The strong performance in Japanese language education and the growth of the childcare and nursing care businesses appear to be key drivers, suggesting a successful shift in the company’s business portfolio. Furthermore, the profit improvement in the cram school business, resulting from cost optimization through consolidation, could indicate effective resource management and potential for sustained profitability.

7213|レシップHD

582.0

▲ +0.52%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- LECIP HOLDINGS reported consolidated net sales of ¥23,898 million for the full year ended March 2026, marking a decrease of ¥2,033 million (7.8%) from the previous fiscal year.

- Consolidated operating income for the full year was ¥1,268 million, a decrease of ¥2,263 million (64.1%) year-over-year.

- Consolidated ordinary income was ¥1,508 million (down 56.7% YoY), and net income attributable to owners of the parent was ¥1,177 million (down 47.8% YoY).

- By segment, the Transport Equipment business recorded sales of ¥20,034 million (down 7.6% YoY) and operating income of ¥1,190 million (down 65.2% YoY).

- The Industrial Equipment business reported sales of ¥3,825 million (down 9.0% YoY) and operating income of ¥137 million (down 9.8% YoY).

🤖 AI Perspective

LECIP HOLDINGS’ FY2026/3 results indicate a significant year-over-year decline in both revenue and profit across its segments. The decrease in the Transport Equipment business was attributed to lower sales related to new banknote-compatible products and LED lighting for trains in the US, while the Industrial Equipment business saw reduced sales of battery-powered forklift chargers. These factors suggest that specific project cycles and market demand shifts may have notably impacted the company’s financial performance.

7590|タカショー

391.0

▲ +0.77%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Takasho’s consolidated net sales for the first quarter of FY2027 were ¥5.651 billion (97.4% compared to the same period last year).

- Ordinary profit reached ¥161 million (compared to a loss of ¥72 million in the prior year), and net profit was ¥48 million (compared to a loss of ¥136 million in the prior year), both returning to profitability.

- The non-residential sector within the Pro-Use business expanded, increasing by 113.5% year-on-year.

- A foreign exchange gain of ¥68 million, resulting from strategic currency risk hedging, and thorough scrutiny of selling, general, and administrative expenses contributed significantly to the profit increase.

- For the full fiscal year 2027, the company forecasts a 113.4% increase in net sales and a ¥282 million increase in operating profit year-on-year, projecting two consecutive years of revenue and profit growth.

🤖 AI Perspective

The reported V-shaped recovery in ordinary and net profits, leading to a return to profitability in the first quarter, suggests that the company’s profitability improvement measures are yielding results despite a challenging business environment. While overall sales saw a slight decrease, the expansion in the non-residential Pro-Use segment, the recognition of foreign exchange gains, and optimized SGA expenses appear to have been key drivers for the profit turnaround. Investors may monitor the continued growth of the Pro-Use business, new product introductions, and overseas expansion efforts as the company aims to achieve its full-year revenue and profit growth targets.

7120|SHINKO

988.0

▼ -2.18%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SHINKO Co., Ltd. resolved to acquire all shares of TAC Co., Ltd., making it a subsidiary, at a board meeting held on May 28, 2026.

- The number of shares acquired is 200, resulting in SHINKO holding 100.0% of the voting rights post-acquisition.

- The acquisition cost is JPY 615 million for TAC’s common shares, plus approximately JPY 91 million for advisory fees, totaling approximately JPY 706 million.

- TAC’s business activities include the sale of CAD design systems and CAD-related consulting.

- The scheduled share transfer date is July 1, 2026.

🤖 AI Perspective

This acquisition of TAC by SHINKO is positioned as a significant investment aimed at achieving growth and improving profitability, key themes in SHINKO’s new mid-term management plan. TAC’s subscription-based business model is noted for establishing a stable revenue base, and SHINKO’s hiring capabilities are expected to contribute to TAC’s future growth. Furthermore, entering a business domain distinct from existing operations may offer new revenue streams and diversify risk away from reliance on specific businesses.

2323|fonfun

413.0

▲ +8.40%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- fonfun Co., Ltd. has released the archive video and a transcript including Q&A from its full-year online earnings briefing for the fiscal year ended March 2026, held on May 25, 2026.

- The significant increase in net sales from Q3 to Q4 of FY2026/3 was primarily due to the M&A of Microwave Digital Co., Ltd., which became a consolidated subsidiary from an equity method affiliate and was absorbed by the end of March.

- The approximately 140 million yen increase in net income as of March 2026 is attributed to the early recording of deferred tax assets based on future taxable income projections, described as an accounting treatment rather than a strategic intent.

- The current performance forecast (net sales of approximately 3.6 billion yen, EBITDA of 720 million yen) does not include the impact of future M&A transactions. However, M&A deals involving YNP Co., Ltd. and the Sales Performer business are incorporated.

- The company aims to actively promote M&A to achieve a market capitalization of 30 billion yen and net sales of 10 billion yen in three years, and has indicated potential entry into AI-related businesses under its “AI-Driven Management” second mid-term management plan.

🤖 AI Perspective

This release offers specific insights into fonfun’s performance drivers, particularly the impact of M&A on FY2026/3 results and the company’s forward-looking growth strategies in M&A and AI-related fields. The clarification regarding deferred tax asset accounting provides transparency for investors analyzing net income. Furthermore, the flexible stance on future shareholder returns, alongside strengthened IR activities for institutional investors, could be worth monitoring.

2311|エプコ

806.0

▲ +0.50%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- EPCO Inc. announced on May 28, 2026, a “Correction to a portion of the ‘Q1 FY2026 Financial Results Presentation Materials’.”

- The correction pertains to information stated on page 22 of the “Q1 FY2026 Financial Results Presentation Materials” originally released on May 14, 2026.

- The reason for the correction was an error in calculating the application rate for the 2025 second-half lottery-based shareholder benefit program.

- Specifically, the denominator for the application rate was incorrectly based on the total number of shareholders instead of the correct number of shareholders owning 100 shares or more, who are eligible to apply for the benefit.

- The company has rectified this error by recalculating the application rate using the correct denominator.

265A|G-エイチエムコム

639.0

▼ -0.93%

📎 Source:G-エイチエムコム Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hmcomm achieved a turnaround to an ordinary profit of 5.9 million yen in the first quarter of the fiscal year ending December 2026 (January-March). This was primarily due to strong progress in enterprise-向け implementation projects for its “AI Products (e.g., Terry2)” and “AI Solutions.”

- Q1 revenue was 332 million yen, representing an approximately 24.2% progress rate against the full-year target of 1.37 billion yen, which is considered to be a strong pace exceeding initial plans given the company’s seasonality.

- For the second quarter (April-June), the company strategically incorporates one-time expenses related to M&A, thus projecting an expanded ordinary loss for the first half of the fiscal year.

- Regarding the M&A of Collabora Techno Inc., goodwill amortization expenses will occur, but the company anticipates early investment recovery and business contribution through synergies between both companies.

- The flagship product, conversational AI agent “Terry2,” is experiencing a sharp increase in clients transitioning from Proof-of-Concept (PoC) to full-scale operational use in real business environments, accelerating the shift towards a stock-based business model with “AI usage fees” based on processing volume.

🤖 AI Perspective

Hmcomm’s return to profitability in Q1 suggests that its core AI businesses are gaining traction in enterprise adoption, indicating that prior strategic investments are beginning to yield returns. The Q1 revenue progress rate exceeding seasonal trends could be an encouraging sign for full-year performance. While the M&A of Collabora Techno Inc. incurs short-term costs, it is positioned as a strategic investment aimed at a complete shift to AI-driven development, and its contribution to long-term corporate value will be worth monitoring.

3252|地主

2867.0

▼ -2.02%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- JINUSHI Co., Ltd. released a Q&A on its Q1 FY2026 financial results (announced on May 8, 2026) on May 28, 2026.

- Despite a decrease in revenue and profit for Q1 FY2026, the company stated that its full-year net profit forecast of ¥8 billion is “achievable.”

- The company clarified that procurement and sales are progressing as planned towards achieving the full-year target, with property sales primarily concentrated in the fourth quarter.

- Sales to JINUSHI REIT are described as having a “high probability,” and JINUSHI REIT’s fundraising environment is “continuously strong,” having achieved capital increases for 10 consecutive years since its inception.

- Regarding interest rate hikes, the company stated that the FY2026 plan “already incorporates interest rate levels assuming a total of two rate hikes,” emphasizing that the JINUSHI business model is not affected by rising construction costs or inflation.

🤖 AI Perspective

The company’s detailed response regarding the achievability of its full-year target, despite a Q1 decline, offers insights into its operational strategy. The concentration of sales in Q4 and the high probability of transactions with JINUSHI REIT suggest a planned execution, which may be worth monitoring for investors. Furthermore, the extensive explanation of the JINUSHI business’s resilience against external factors like rising interest rates, inflation, and construction costs highlights the company’s confidence in its business model amidst evolving market conditions.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

4389|G-プロパティDBK

865.0

▼ -1.14%

📎 Source:G-プロパティDBK Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Property DBK reported consolidated financial results for the fiscal year ended March 2026: Revenue of JPY 3,721 million (+12.1% YoY), Operating Profit of JPY 1,112 million (+18.8% YoY), Ordinary Profit of JPY 1,127 million (+20.1% YoY), and Net Income of JPY 716 million (+12.9% YoY).

- Both revenue and all profit items increased year-on-year, reaching record highs.

- By service, Cloud Services revenue was JPY 1,958 million (+9.0% YoY), Solution Services revenue was JPY 1,230 million (+15.0% YoY), and New Services revenue was JPY 306 million (+46.3% YoY).

- While revenue of JPY 3,721 million fell short of the initial forecast of JPY 4,000 million, Operating Profit of JPY 1,112 million and Ordinary Profit of JPY 1,127 million both exceeded the initial forecasts of JPY 1,040 million respectively.

- The company’s “@property” business management system maintained its No. 1 industry share of 44.0% in the real estate asset management sector, according to a survey by Monthly Property Management magazine.

🤖 AI Perspective

The FY2026/3 results show G-Property DBK achieving record high revenue and profits, despite revenue falling slightly below initial forecasts. The over-performance in profits, driven by large solution service contracts, accumulation of high-margin projects, and cost control, may be of interest to investors. The continued market leadership of “@property” in real estate asset management also suggests a stable foundation for future growth.

4570|G-免疫生物研究所

1078.0

▼ -4.35%

📎 Source:G-免疫生物研究所 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Immuno-Biological Laboratories announced its consolidated financial results for the fiscal year ended March 2026 (44th fiscal year).

- Consolidated net sales reached ¥1,004.987 million, a 3.7% increase year-over-year (YoY). Operating profit was ¥281.277 million, a 34.4% increase YoY.

- Ordinary profit was ¥300.562 million (+43.2% YoY), and net profit attributable to owners of parent was ¥329.015 million (+32.1% YoY).

- By segment, the antibody-related business recorded sales of ¥1,002.307 million (+3.9% YoY) and segment profit of ¥281.886 million (+35.4% YoY). The cosmetics-related business saw sales of ¥2.679 million (-48.1% YoY) and a segment loss of ¥0.609 million.

- For the fiscal year ending March 2027 (45th fiscal year), the company projects net sales of ¥1,087 million (+¥83 million YoY) and operating profit of ¥322 million (+¥41 million YoY).

4689|LINEヤフー

414.5

▲ +0.48%

📎 Source:LINEヤフー Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- LINEヤフー Corporation announced on May 28, 2026, a correction to a portion of its “Consolidated Financial Results for the Fiscal Year Ending March 31, 2026 [IFRS]” initially released on May 8, 2026.

- The reason for the correction was the discovery of an error in part of the disclosed information after the initial announcement.

- The specific correction relates to Page 3, “1. [Analysis of Operating Results and Financial Position] (1) Qualitative Information on Consolidated Operating Results 2. Segment Operating Overview (April 2025 – March 2026) ③ Strategic Businesses for the Current Consolidated Fiscal Year.”

- The original disclosure stated PayPay Corporation’s consolidated transaction volume as ¥19.3 trillion (a 22.9% increase year-on-year).

- The corrected figure for PayPay Corporation’s consolidated transaction volume is ¥19.4 trillion (a 23.4% increase year-on-year).

- The company has stated that this correction has no impact on its financial statements.

🤖 AI Perspective

This correction primarily involves a minor adjustment to the reported consolidated transaction volume for PayPay, with no stated impact on the overall financial statements, which may be a key point for investors. Updating a key metric within a strategic business segment can provide a more accurate picture of business progress. Such corrections are typically made to maintain the reliability of corporate disclosures and can be viewed as an effort to improve information accuracy.

6584|三桜工

873.0

▲ +0.92%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sanoh Industrial Co., Ltd. announced its FY2026 financial results, with consolidated net sales decreasing due to a sales decline in Europe and China and negative foreign exchange translation impact from the strong yen in North and South America, despite increased sales from new launches in Japan.

- Operating profit decreased by 787 million yen year-on-year, primarily due to the impact of US tariffs, import trouble costs, and increased startup costs in North and South America.

- Ordinary profit decreased by 1,562 million yen year-on-year, attributed to the decline in operating profit and the recognition of foreign exchange losses.

- Net profit increased by 787 million yen year-on-year, driven by a 2,554 million yen gain from negative goodwill on the acquisition of a Mexican subsidiary, which offset liquidation losses from a Chinese subsidiary (▲1,268 million yen) and special severance payments for personnel restructuring at a German subsidiary (▲1,283 million yen).

- Regionally, Japan saw increased sales and profit, Europe increased profit (with decreased sales), and Asia saw decreased profit (with increased sales), while North & South America and China recorded operating losses.

🤖 AI Perspective

Sanoh Industrial’s FY2026 results reflect a mixed performance influenced by both regional market dynamics and structural reforms. While the reported increase in net profit was significantly boosted by a one-off gain from negative goodwill related to a subsidiary acquisition, it may suggest that the underlying operational profitability faces ongoing challenges, particularly given the decline in operating profit. Investors might monitor how the company’s new management initiatives, focusing on capital cost, stock price awareness, and the development of new businesses like data centers, will address core business profitability and drive sustainable growth beyond such one-off gains.

6615|UMCエレ

243.0

▼ -0.82%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- UMC Electronics announced a partial correction to its “Consolidated Financial Results for the Fiscal Year Ending March 2026 (Japanese GAAP)” initially disclosed on May 15, 2026.

- The corrections stem from two main reasons: misclassification of right-of-use assets as lease assets by its consolidated subsidiary, UMC Electronics Vietnam Limited (a transfer of 224 million yen), and an omission in accounting for deferred tax liabilities and deferred tax assets corresponding to tax-deductible temporary differences (91 million yen each recorded).

- As a result of these corrections, the total assets on the consolidated balance sheet for the fiscal year ended March 2026 were revised from 75,808 million yen to 75,900 million yen.

- There are no changes to net assets or net assets per share (March 2026: 17,143 million yen, 393.66 yen).

- The corrections have no impact on net profit attributable to parent company shareholders in the consolidated statements of income.

🤖 AI Perspective

This correction primarily affects the asset side of the consolidated balance sheet due to specific accounting errors and omissions by a subsidiary. The fact that there is no impact on net profit attributable to parent company shareholders may suggest limited concern for investors regarding the company’s profitability. However, the integrity of the subsidiary’s accounting practices and internal controls could be a point worth monitoring in future disclosures.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

8181|東天紅

982.0

▼ -0.10%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Totenko Co., Ltd.’s non-listed parent company, Koizumi Group Co., Ltd., has finalized its financial results for the fiscal year ended February 2026.

- As of February 28, 2026, the balance sheet shows total assets of ¥25,373,758,395 and net assets of ¥7,229,388,492.

- For the period from March 1, 2025, to February 28, 2026, the income statement reports operating revenue of ¥963,101,112 and operating income of ¥280,975,487.

- Ordinary income was ¥323,860,344, profit before income taxes was ¥277,548,324, and net income was ¥73,472,396.

- Koizumi Group Co., Ltd.’s business activities include real estate leasing, brokerage, buying, selling, and management, as well as business consulting, with a capital of ¥200,000,000.

🤖 AI Perspective

The disclosure of a non-listed parent company’s financial results can provide indirect insights into the business foundation and management stability of its listed subsidiary, Totenko. The parent company’s asset position and profitability might influence future group strategies and financing, making this information worth monitoring for a comprehensive understanding of the overall group health.

9060|日ロジテム

4125.0

▲ +0.12%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nippon Logitem Co., Ltd. announced a partial revision to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 [Japanese GAAP]” originally published on May 14, 2026.

- The reason for the revision was an error discovered in the calculation of deferred tax liabilities related to retained earnings of subsidiaries during consolidation.

- As a result of the revision, net income attributable to parent company shareholders decreased from ¥765,277 thousand to ¥684,753 thousand (a decrease of ¥80,523 thousand).

- Earnings per share (EPS) were revised downwards from ¥565.11 to ¥505.65 (a decrease of ¥59.46).

- Net assets decreased from ¥16,697,149 thousand to ¥16,616,625 thousand (a decrease of ¥80,523 thousand), and the equity ratio also slightly decreased from 32.4% to 32.2% (a decrease of 0.2 percentage points).

🤖 AI Perspective

This revision appears to stem from a specific accounting error rather than a change in the company’s operational performance. While the reduction in net income and net assets, along with a slight dip in the equity ratio, may be noted by investors assessing financial health, the company’s core business performance outlined in the original release remains unchanged. Investors might consider monitoring future financial disclosures for similar adjustments to ensure consistency in reporting.

3495|香陵住販

2398.0

▼ -0.04%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Koryojyuhan released its financial presentation for the second quarter of the fiscal year ending September 2026 (October 1, 2025 – March 31, 2026).

- Real estate sales for the quarter increased by 10.2% year-on-year, primarily due to strong sales of its proprietary investment property series, “Regabene.”

- The sale of the “KORYO Eco Power Moritocho” solar power generation business was completed in March 2026, resulting in a special gain on the sale of fixed assets of approximately ¥255 million in Q2.

- The interim dividend forecast has been revised upwards to ¥31.00 (from ¥27.00 in the previous period), with the annual dividend forecast remaining at ¥61.00.

- The number of rental management units expanded to 24,984, and coin parking operations exceeded plans.

🤖 AI Perspective

Koryojyuhan’s strong performance in real estate sales, particularly its proprietary investment properties, appears to be a key driver for the company’s results. The divestiture of the solar power business and the resulting special gain may indicate a strategic move towards optimizing its business portfolio. The expansion of rental management units and the increase in interim dividends could suggest a focus on stable recurring revenue and shareholder returns.

7176|P-シンプレクスFH

464.0

▲ +0.00%

📎 Source:P-シンプレクスFH Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- P-Simplex Financial Holdings announced its consolidated financial results for the fiscal year ended March 31, 2026.

- Operating revenue for FY2026/3 reached ¥22,512 million, representing a 38.5% increase year-over-year.

- Operating profit stood at ¥13,970 million (up 49.6% YoY) and ordinary profit at ¥14,276 million (up 51.1% YoY).

- Net income attributable to owners of the parent increased by 50.7% to ¥10,631 million.

- Basic earnings per share were ¥317.33, an increase from ¥137.14 in the prior period (adjusted for stock split).

- The company has not provided a consolidated earnings forecast or dividend forecast for FY2027/3, citing the nature of its business.

🤖 AI Perspective

P-Simplex FH’s FY2026/3 results show substantial growth across operating revenue and all profit segments, with net income attributable to owners of the parent increasing by over 50%. This robust performance is notable, especially given the inherent volatility of the investment management and advisory business which is influenced by economic and market conditions. The absence of a forward-looking forecast for FY2027/3 suggests the company’s recognition of this market sensitivity, and future market developments will be a key factor for investors to monitor.

7247|ミクニ

338.0

▲ +0.60%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Mikuni Corporation has determined the new release date for its Fiscal Year ending March 2026 financial results.

- The new earnings announcement date is Friday, May 29, Reiwa 8 (2026).

- The announcement of the FY2026 March earnings was previously postponed, as disclosed in the notice dated April 27, Reiwa 8 (2026), regarding the “Discovery of Misconduct by an Employee of a Consolidated Subsidiary and Postponement of Full-Year Financial Results Announcement for the Fiscal Year Ending March 2026.”

- Mikuni’s representative is Hisataka Ikuta, Representative Director and President, with stock code 7247 on the Tokyo Stock Exchange Standard market.

7425|初穂商事

2353.0

▼ -0.51%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hatsuko Shoji announced on May 28, 2026, that its Board of Directors resolved a stock split, an amendment to its Articles of Incorporation, and a revision of its dividend forecast.

- The stock split will be conducted at a ratio of 2 shares for every 1 common share, with a record date of June 30, 2026, and an effective date of July 1, 2026.

- Following the split, the total number of outstanding shares will increase by 3,480,660 to 6,961,320 shares, and the total number of authorized shares will change from 4,680,000 to 9,360,000 shares.

- There will be no change in the amount of stated capital as a result of this stock split.

- The year-end dividend forecast for the fiscal year ending December 2026 has been revised from ¥80.00 per share (pre-split) to ¥40.00 per share (post-split), with no substantial change to the actual dividend amount.

🤖 AI Perspective

This stock split appears to aim at reducing the investment unit per share, potentially making the company’s shares more accessible to a broader range of investors. This move could lead to improved liquidity and an expansion of the investor base for Hatsuko Shoji. It is worth noting that the dividend forecast revision is a technical adjustment due to the split, indicating no actual change in the dividend per pre-split share, which is a key consideration for income-focused investors.

9828|ゲンキGDC

2750.0

▲ +1.03%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Genki Global Dining Concepts reported record-high sales for FY2026/3, with net sales reaching 73.7 billion yen (up 9.2% YoY) and total sales 141.5 billion yen (up 7.4% YoY).

- Operating profit decreased to 4.7 billion yen (down 29.4% YoY) and net income to 3.4 billion yen (down 29.6% YoY), primarily due to increased costs from rising rice prices and minimum wages.

- The domestic segment saw increased sales but decreased profit, while the global segment achieved both increased sales and profit. Total store count was 448 (194 domestic, 254 overseas).

- For FY2027/3, the company forecasts consolidated net sales of 103.0 billion yen (up 39.7% YoY) and operating profit of 6.0 billion yen (up 25.1% YoY). However, net income is projected to decrease to 3.3 billion yen (down 5.5% YoY).

- The dividend forecast for FY2027/3 is set at 70 yen per share annually, maintaining the same level as FY2026/3.

8059|第一実業

3045.0

▼ -1.77%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- First Jitsugyo Co. Ltd. resolved to establish a new shareholder benefit program at a Board of Directors meeting held on May 28, 2026.

- The program targets shareholders recorded on the company’s shareholder register as of September 30 each year, starting from 2026, who hold 100 shares (1 unit) or more.

- Shareholders will receive points via a dedicated website, “First Jitsugyo Premium Yu-tai Club,” based on the number of shares held. Points range from 600 for 100-199 shares to 55,000 for 1,000 shares or more.

- These points can be exchanged for over 5,000 items, including gourmet foods, sweets, and electronic appliances, or converted into “WILLsCoin,” which can be combined with points from other Premium Yu-tai Club participating companies.

- Points can be carried over for a maximum of two times, provided the shareholder is recorded with the same shareholder number for at least two consecutive times as of September 30 and continuously holds 100 shares or more.

🤖 AI Perspective

The establishment of this new shareholder benefit program is stated to aim at enhancing shareholder returns, improving stock liquidity, and expanding and stabilizing the shareholder base. The introduction of the “Premium Yu-tai Club” and its integration with “WILLsCoin” could potentially increase the appeal and flexibility for shareholders. The conditions for point rollover may also suggest an intent to encourage long-term shareholding.

3063|G-jGroup

819.0

▲ +0.86%

📎 Source:G-jGroup Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- J-Group Holdings Co., Ltd. announced a revision to its dividend forecast on May 28, 2026.

- The revision pertains to the interim dividend forecast for the fiscal year ending February 2027 (March 1, 2026 – February 28, 2027).

- The reason for the revision is the implementation of a commemorative dividend celebrating the company’s 30th anniversary in March 2026.

- The interim dividend forecast per share has been revised from ¥2.00 (ordinary dividend ¥2.00) to ¥3.00, including an additional ¥1.00 commemorative dividend (ordinary dividend ¥2.00, commemorative dividend ¥1.00).

- Consequently, the annual dividend forecast has been revised from the previous forecast of ¥4.00 to ¥5.00.

🤖 AI Perspective

This dividend forecast revision is notable for including a special dividend to commemorate the company’s 30th anniversary. Maintaining the ordinary dividend while adding a commemorative payout may suggest a commitment to shareholder returns. Such commemorative dividends are generally recognized as a way for companies to celebrate historical milestones and express gratitude to their shareholders.

5573|P-働楽HD

1700.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, consolidated net sales were ¥3,649 million, representing a 9.7% increase year-over-year.

- Consolidated operating profit for the same period was ¥62 million (down 28.1% YoY), ordinary profit was ¥71 million (down 33.6% YoY), and profit attributable to owners of parent was ¥50 million (down 50.1% YoY).

- The decline in profit was attributed to factors within the system development business, including errors in estimating development man-hours for a contract software development project, leading to delivery delays and increased costs.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥3,900 million (up 6.9% YoY), operating profit of ¥119 million (up 91.4% YoY), ordinary profit of ¥128 million (up 78.5% YoY), and profit attributable to owners of parent of ¥110 million (up 116.4% YoY).

- The year-end dividend for both FY2025/3 and FY2026/3 remained at ¥9.00 per share. The dividend forecast for FY2027/3 is currently undecided.

🤖 AI Perspective

P-DORAKU HD’s FY2026/3 results show revenue growth but a significant decline in profit, primarily impacted by project-specific issues. However, the company’s robust profit forecast for FY2027/3 suggests an expectation of overcoming these challenges and capitalizing on future opportunities. Investors may observe how the company addresses past project management issues and integrates new business, while the increased operating cash flow indicates improved internal fund generation.

4069|G-BlueMeme

883.0

▲ +1.49%

📎 Source:G-BlueMeme Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-BlueMeme has announced preliminary estimated impacts on its financial statements from FY2020 to FY2025 due to issues concerning the appropriateness of accounting treatment, following a previously announced change in the FY2026 Q3 earnings release schedule.

- The company discovered on February 19, 2026, prompted by information from its accounting auditor Aoi Audit Corporation, that there were errors in the timing of revenue recognition, accounting treatment for sales, and related procurement transactions with a specific client.

- A preliminary report from an external expert investigation indicates that a March 2020 license sale (30 million yen) and subsequent increases in outsourced dispatch costs with the same client should be treated as a series of transactions, effectively equating to a sales return. This suggests that the revenue recognition criteria, including receipt of cash or cash equivalents, were not met. Additionally, 27 million yen of the March 2020 sales should have been recognized in April 2020.

- Preliminary estimated revisions for FY2020 include sales decreasing by 57 million yen (from 1,800 million yen to 1,742 million yen), operating profit decreasing by 33 million yen (from 31 million yen to -1 million yen), and net assets decreasing by 33 million yen (from 358 million yen to 324 million yen).

- For FY2025, preliminary estimates show operating profit increasing by 4 million yen (from 31 million yen to 35 million yen) and net assets decreasing by 8 million yen (from 2,537 million yen to 2,528 million yen).

- All disclosed impact figures are on a consolidated basis, are provisional estimates not yet reviewed by the accounting auditor, and do not account for tax expenses.

🤖 AI Perspective

G-BlueMeme’s disclosure of preliminary impacts from past accounting errors provides investors with crucial information to reassess the financial position of various fiscal years. The ongoing external investigation, initiated by the accounting auditor’s input, along with the explicit statement that preliminary figures are subject to change, suggests that continuous monitoring of future developments will be necessary. As the company is also considering the necessity of amending past statutory disclosure documents, investors may want to await the final impact figures and the announcement of corrective measures.

8143|ラピーヌ

180.0

▲ +0.56%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Lapine Co., Ltd. announced a partial correction to its Consolidated Financial Results for the Fiscal Year Ended February 2026 on May 28, 2026.

- The correction addresses certain items that required revision in the individual financial results, as initially disclosed on April 20, 2026.

- Specifically, the individual financial statements were revised to account for “provision for loss on related company business” under fixed liabilities and “reversal of allowance for doubtful accounts for related companies” as extraordinary income.

- There are no revisions to the consolidated financial results as a result of this correction.

- The corrected full financial summary is attached, with underlines indicating the revised sections in the summary of individual financial results.

🤖 AI Perspective

This correction primarily impacts the classification of specific accounts within the individual financial statements and the recognition of an extraordinary income item. The fact that consolidated results remain unchanged suggests that the overall financial position and performance, from a group perspective, are not altered. Investors may view this as an effort by the company to ensure the accuracy and proper presentation of its financial reporting for individual operations.

3905|G-データセクション

5140.0

▲ +15.90%

📎 Source:G-データセクション Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Datasection announced corrections to a portion of its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 [Japanese GAAP]” originally disclosed on May 15, 2026.

- The “Net assets per share” for the consolidated fiscal year ended March 2026 were corrected from 624.42 yen to 625.40 yen, and for the non-consolidated figures from 577.96 yen to 578.87 yen.

- The forecast range for “Earnings per share” for the consolidated fiscal year ending March 2027 was revised from 179.14 yen – 231.16 yen to 179.31 yen – 231.45 yen.

- In the notes on “Number of shares outstanding,” the number of treasury shares at the end of March 2026 was corrected from 90,952 shares to 137,615 shares.

- The “Net income attributable to non-controlling interests” in the consolidated statement of income for the fiscal year ended March 2026 was adjusted from 5,379 thousand yen to 5,397 thousand yen.

🤖 AI Perspective

These corrections primarily impact key financial metrics such as net assets per share for FY2026 and the projected earnings per share range for FY2027. Investors typically use these figures as fundamental inputs for valuation and decision-making, and the specific impact may vary depending on individual investment strategies. The company attributed the corrections to “errors found in part of the stated content,” suggesting the importance of reviewing the revised disclosure for accurate assessment.

4060|G-rakumo

1045.0

▼ -0.29%

📎 Source:G-rakumo Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-rakumo announced a partial correction to its “FY2026 Q1 Financial Results Briefing Material” originally published on May 14, 2026.

- The reason for the correction was an error in the display units for “Adjusted EPS” on page 23 and “Paid License Count Trend” on page 27.

- The corrected sections are marked with red frames within the updated document.

- The revised document has been attached to the announcement.

🤖 AI Perspective

This correction addresses errors in presentation units within the previously released financial briefing material, rather than changes to the underlying financial figures themselves. Investors may view this as a measure to ensure the accuracy of disclosed information. It is important for stakeholders to refer to the corrected document when analyzing or comparing G-rakumo’s first-quarter performance with previous periods.

9348|G-ispace

699.0

▲ +16.50%

📎 Source:G-ispace Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-ispace announced corrections to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026” and “Presentation Materials for the Fiscal Year Ended March 31, 2026,” originally disclosed on May 15, 2026.

- The reason for the corrections is stated as errors in the consolidated earnings forecast for the fiscal year ending March 2027, individual financial results for the fiscal year ended March 2026, the consolidated cash flow statement, and impairment losses on fixed assets.

- For the fiscal year ended March 2026, consolidated cash flows from operating activities were revised from “△13,190 million yen” to “△13,568 million yen,” and cash flows from investing activities from “△2,203 million yen” to “△1,825 million yen.” This reclassification involved moving cash flows related to forward exchange contracts from operating to investing activities.

- The consolidated ordinary profit forecast for the fiscal year ending March 2027 was corrected from “△11,700 million yen” to “△17,700 million yen.” Project revenue, net sales, operating profit, net profit attributable to owners of parent, and basic earnings per share remained unchanged.

- For the individual financial results for the fiscal year ended March 2026, ordinary profit was revised from “△4,572 million yen” to “△12,867 million yen,” and net profit from “△4,582 million yen” to “△12,878 million yen.” Consequently, basic earnings per share also changed from “△37.08 yen” to “△104.20 yen.” Individual balance sheet items including total assets, net assets, equity ratio, and net assets per share were also corrected.

🤖 AI Perspective

These corrections encompass multiple financial figures impacting both past performance and future outlook. The substantial revision to the consolidated ordinary profit forecast for FY2027 and the increased loss figures in the FY2026 individual results are noteworthy points for investors evaluating the company’s future business plans and financial health. The reclassification of cash flows could also influence how the company’s funding dynamics are perceived.

5821|平河ヒューテ

3640.0

▲ +6.74%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hirakawa Hewtech announced on May 28, 2026, a partial correction to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 (Japanese GAAP).”

- The reason for the correction was the discovery of an error in the previously disclosed financial results released on May 11, 2026.

- The correction pertains to the “Total Equity (Reference)” item within the “Summary Information (Reference) Overview of Non-consolidated Operating Results (2) Non-consolidated Financial Position.”

- The “Total Equity (Reference)” for the fiscal year ended March 2026 was corrected from “46,456 million yen” to “16,456 million yen.”

- The “Total Equity (Reference)” for the fiscal year ended March 2025 remains unchanged at “16,380 million yen.”

🤖 AI Perspective

This correction addresses a reporting error in the self-capital section of the non-consolidated financial statements, rather than a fundamental change in the company’s financial position itself. Prompt disclosure of such numerical corrections is generally viewed positively, as it ensures investors have accurate information for their analysis. Given that the correction is limited to a specific item, its direct impact on the company’s overall earnings outlook or business strategy is likely to be minimal.

6574|G-コンヴァノ

101.0

▲ +2.02%

📎 Source:G-コンヴァノ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Convanon Co., Ltd. announced a partial correction on May 28, 2026, to its “Notice of Change of Fiscal Year (End of Business Year) and Partial Amendment to Articles of Incorporation” originally published on May 25, 2026.

- The reason for the correction was an omission in the supplementary provisions of the proposed Articles of Incorporation regarding the transitional measures for the interim dividend record date for the transitional fiscal year (14th fiscal year).

- The correction involves adding a new “Article 2 (Record Date for Interim Dividends in the Transitional Fiscal Year)” to the supplementary provisions. This article specifies September 30, 2026, as the record date for interim dividends during the transitional fiscal year (14th fiscal year), spanning from April 1, 2026, to December 31, 2026.

- The company states that this correction aims to clarify the transitional provisions of the Articles of Incorporation amendment and does not significantly impact the proposals or other key matters to be submitted to the 13th Ordinary General Meeting of Shareholders.

🤖 AI Perspective

This correction appears to be a technical adjustment to previously announced amendments to the Articles of Incorporation, clarifying the transitional measures for the interim dividend record date. For investors, this may indicate the company’s commitment to accuracy in its public disclosures. While not directly impacting major business plans or financial performance, it reflects attention to detail in corporate governance.

💡 Start investing with IR insights

※ 本ページには広告が含まれます(PR)

Disclaimer: This article is for informational purposes only and does not constitute investment advice. All investment decisions are at your own risk.

コメント