📌 Today’s Highlights

Today we cover 13 IR announcements. Notable among them: G-スタジオアタオ (3550), クラスターT (4240), 明光ネット (4668). Use the table of contents below to navigate to each company.

3550|G-スタジオアタオ

229.0

▲ +1.78%

📄 Announcement Facts

- For the fiscal year ended February 2026, G-Studioatao reported net sales of 4,126 million yen (up 11.6% year-on-year), operating profit of 239 million yen (up 31.1%), ordinary profit of 243 million yen (up 33.0%), and net profit of 151 million yen (up 121.4%).

- By sales channel, internet sales increased by 20.0% to 2,143,022 thousand yen, while store sales grew by 3.9% to 1,978,184 thousand yen.

- The launch of the new EC site “ATAOLAND+” and the opening of ATAO Rakuten and Yahoo! stores contributed significantly to the growth in internet sales.

- As of the end of FY2026/2, total assets stood at 3,182 million yen, net assets at 2,586 million yen, and the equity ratio was 81.3%.

- For the fiscal year ending February 2027, the company forecasts net sales of 4,500 million yen (up 9.1% year-on-year), operating profit of 330 million yen (up 37.9%), ordinary profit of 335 million yen (up 37.8%), and net profit of 220 million yen (up 45.2%).

🤖 AI Perspective

G-Studioatao’s FY2026/2 financial results show double-digit growth across sales and all profit metrics, with net profit experiencing a substantial increase. This may suggest that the company’s sales strategies, including the introduction of the new EC site “ATAOLAND+” and expansion of product lineups, effectively contributed to revenue growth and improved profitability. The high equity ratio of 81.3% could indicate a strong financial foundation, and combined with the forecast for continued revenue and profit growth in FY2027/2, reflects the company’s confidence in its ongoing business strategies.

4240|クラスターT

391.0

▲ +2.09%

📄 Announcement Facts

- Cluster Technology has decided to pay a dividend of JPY 6 per share for shareholders of record as of March 31, 2026.

- This dividend comprises an ordinary dividend of JPY 5 and a commemorative dividend of JPY 1 per share.

- The latest dividend forecast (announced on May 15, 2025) was JPY 4 per share, and the previous fiscal year’s actual dividend (FY ended March 2025) was also JPY 4 per share.

- The ordinary dividend was increased by JPY 1 to JPY 5 per share.

- A commemorative dividend of JPY 1 per share will be distributed to mark the company’s dual listing on the Nagoya Stock Exchange Main Market and its market segment change to the Tokyo Stock Exchange Standard Market.

- The total dividend amount is JPY 34 million, with an effective date of June 29, 2026. The source of the dividend is retained earnings.

🤖 AI Perspective

Cluster Technology’s dividend increase, including both an enhanced ordinary dividend and a commemorative dividend, may suggest the company’s commitment to shareholder returns. The distribution of a commemorative dividend, in particular, could indicate an effort to acknowledge shareholders following significant market changes. This decision, representing an increase from both the previous forecast and the prior year’s actuals, might be viewed as a reflection of management’s confidence in the company’s current and future financial performance.

4668|明光ネット

713.0

▼ -0.70%

📄 Announcement Facts

- For the second quarter (interim period) of the fiscal year ending August 2026, consolidated net sales increased by 5.5% year-on-year to JPY 12,901 million. Operating profit decreased by 0.9% to JPY 1,459 million, ordinary profit increased by 0.8% to JPY 1,552 million, and net profit attributable to owners of parent decreased by 4.3% to JPY 966 million.

- The full-year consolidated earnings forecast for the fiscal year ending August 2026 remains unchanged from the most recently announced figures, projecting net sales of JPY 25,500 million (up 2.7% year-on-year), operating profit of JPY 1,800 million (up 6.4%), ordinary profit of JPY 1,870 million (up 0.1%), and net profit attributable to owners of parent of JPY 1,010 million (down 41.5%).

- The forecast for the annual dividend for the fiscal year ending August 2026 is JPY 28 per share (JPY 14 interim, JPY 14 year-end), an increase of JPY 1 from the previous fiscal year, with no changes from the latest publicly announced dividend forecast.

- The Meiko Gijuku directly managed business reported net sales of JPY 7,683 million (up 5.8% year-on-year) and segment profit of JPY 1,331 million (up 12.5%). In contrast, the Meiko Gijuku franchise business showed net sales of JPY 2,046 million (up 0.4%), but its segment profit decreased by 17.5% to JPY 579 million.

- During the interim period, Meiko Mirai Co., Ltd. was newly included in the scope of consolidation.

🤖 AI Perspective

* Despite an increase in net sales, the decrease in both operating profit and net profit attributable to owners of parent compared to the prior year’s interim period may be a key point of interest from this earnings announcement.

* The company’s decision to maintain its full-year earnings and annual dividend forecasts could suggest management’s expectation of achieving its targets in the latter half of the fiscal year.

* The divergent profit trends between the directly managed and franchise operations within the core Meiko Gijuku business may indicate specific segmental dynamics influencing the overall consolidated performance.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

5341|ASAHI EITO

303.0

▲ +16.99%

📄 Announcement Facts

- ASAHI EITO Holdings reported consolidated net sales of ¥1,064 million for Q1 FY2026 (December 1, 2025 to February 28, 2026), marking a 0.1% decrease compared to the same period last year.

- The company recorded a consolidated operating loss of ¥51 million (compared to a loss of ¥41 million in the prior year), an ordinary loss of ¥45 million (compared to a loss of ¥26 million), and a net loss attributable to parent company shareholders of ¥53 million (compared to a loss of ¥44 million).

- By segment, the “Lifestyle Business” sales increased by 17.2% year-on-year to ¥385 million, while “Housing Business” sales decreased by 8.2% to ¥675 million.

- Rising raw material prices and the impact of the depreciating yen on cost of sales were cited as factors preventing profit recovery.

- During the cumulative first quarter, the company raised ¥141 million in funds, of which ¥30 million was allocated to acquiring crypto assets.

🤖 AI Perspective

The first quarter results indicate a widening of losses despite relatively stable net sales, primarily attributed to increased costs from rising raw material prices and yen depreciation. However, the growth in the “Lifestyle Business,” including solar battery systems, combined with strategic investments in new areas like rare gas operations and crypto assets, may suggest a diversification strategy for future revenue streams. These new business initiatives could be a point of interest for investors monitoring the company’s long-term growth prospects.

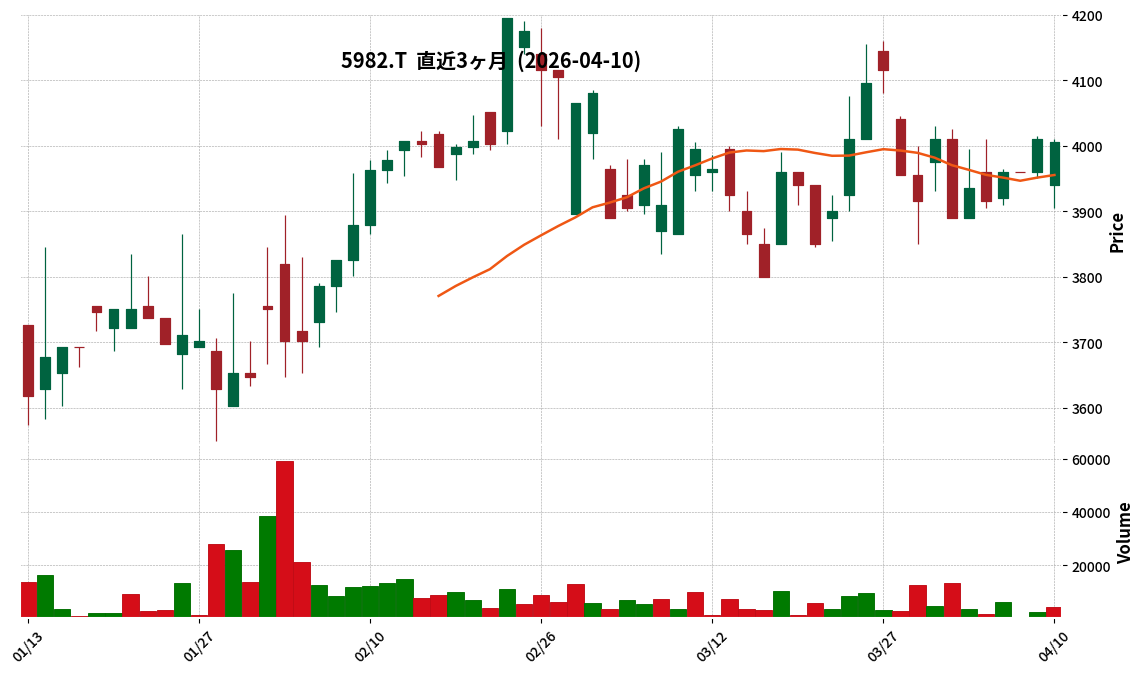

5982|マルゼン

4005.0

▼ -0.12%

📄 Announcement Facts

- Maruzen Co., Ltd. announced its consolidated financial results for the fiscal year ended February 2026 (March 1, 2025 to February 28, 2026) on April 10, 2026.

- Consolidated net sales reached ¥66,782 million (+3.9% year-on-year), operating profit ¥6,636 million (+8.9% year-on-year), ordinary profit ¥7,341 million (+10.3% year-on-year), and net profit attributable to owners of parent ¥5,216 million (+12.3% year-on-year).

- Net sales, operating profit, ordinary profit, and net profit attributable to owners of parent all achieved record highs for the period.

- The annual dividend for the fiscal year ended February 2026 was ¥125.00 per share (interim ¥55.00, year-end ¥70.00), an increase of ¥10.00 from the previous fiscal year.

- For the fiscal year ending February 2027, the company forecasts consolidated net sales of ¥67,000 million (+0.3% year-on-year), operating profit of ¥6,700 million (+1.0% year-on-year), ordinary profit of ¥7,400 million (+0.8% year-on-year), and net profit attributable to owners of parent of ¥5,300 million (+1.6% year-on-year).

🤖 AI Perspective

The fiscal year 2026/2 results indicate a period of strong performance for Maruzen, with all key financial metrics reaching new record highs. This growth was reported to be supported by robust sales in the commercial kitchen equipment division, particularly to restaurant chains and food supermarkets. The company’s positive forecast for FY2027/2, coupled with an increased annual dividend, may suggest management’s confidence in continued profitability and shareholder returns.

6506|安川電

4894.0

▲ +4.71%

📄 Announcement Facts

- For the fiscal year ended February 28, 2026 (FY2026/2), consolidated revenue reached ¥542,122 million, representing a 0.8% increase year-on-year.

- During the same period, consolidated operating profit was ¥47,307 million (down 5.7% year-on-year), and profit attributable to owners of the parent was ¥35,240 million (down 38.2% year-on-year). Basic earnings per share stood at ¥135.88.

- For the fiscal year ending February 28, 2027 (FY2027/2), the company forecasts consolidated revenue of ¥580,000 million (up 7.0% year-on-year), operating profit of ¥60,000 million (up 26.8% year-on-year), and profit attributable to owners of the parent of ¥47,000 million (up 33.4% year-on-year). Basic earnings per share are projected at ¥181.21.

- The annual dividend forecast for FY2207/2 is ¥72.00 per share (interim ¥36.00, year-end ¥36.00).

🤖 AI Perspective

While the fiscal year 2026/2 saw a decrease in profit, the consolidated earnings forecast for fiscal year 2027/2 projects substantial increases in both revenue and profit, which may indicate anticipated recovery in the business environment and the impact of strategic initiatives. Furthermore, the forecast of an increased annual dividend for fiscal year 2027/2 suggests a positive stance on shareholder returns.

6555|MSコンサル

456.0

▲ +2.01%

📄 Announcement Facts

- MS&Consulting reported consolidated revenue of JPY 2,585 million for the fiscal year ended February 2026, representing a 1.3% increase year-on-year.

- Operating profit, profit before tax, and profit attributable to owners of the parent all turned profitable, reaching JPY 252 million, JPY 251 million, and JPY 173 million respectively, from losses in the prior year. Basic earnings per share were JPY 40.21.

- The company focused on “company-wide profitability improvement,” resulting in the Mystery Shopping Research (MSR) gross profit margin improving from 43.9% in the previous period to 48.5%.

- In terms of financial position, total assets increased to JPY 3,704 million, and equity attributable to owners of the parent rose to JPY 2,956 million. Cash and cash equivalents at year-end were JPY 1,030 million.

- For the fiscal year ending February 2027, the company forecasts consolidated revenue of JPY 2,757 million (+6.7% YoY), operating profit of JPY 355 million (+40.7% YoY), and profit attributable to owners of the parent of JPY 220 million (+27.2% YoY).

🤖 AI Perspective

The company’s focus on “company-wide profitability improvement,” including enhancing MSR gross profit margins and utilizing AI for cost reduction, appears to have driven the significant return to profitability. The positive outlook for the next fiscal year, projecting further revenue and profit growth, could indicate a sustained improvement in the company’s earnings structure.

7487|小津産業

1965.0

▼ -1.26%

📄 Announcement Facts

- OZU Corporation announced its consolidated financial results for the third quarter of the fiscal year ending May 2026 (June 1, 2025, to February 28, 2026) on April 10, 2026.

- For the cumulative consolidated period, net sales were ¥8,085 million (up 3.8% year-on-year), operating profit was ¥526 million (up 15.0%), ordinary profit was ¥717 million (up 21.1%), and net profit attributable to owners of parent was ¥503 million (up 32.3%).

- In the non-woven fabric business, strong performance was observed in AI-related demand and optical-related demand within the clean sector, cosmetic products in the wellness care sector, and disinfectant wet products and eyeglass cleaners in the consumer sector.

- The full-year consolidated earnings forecast for the fiscal year ending May 2026 was revised upwards: operating profit to ¥450 million (up 9.8% from previous forecast), ordinary profit to ¥670 million (up 17.5%), and net profit attributable to owners of parent to ¥430 million (up 16.2%). The net sales forecast of ¥10,500 million remains unchanged.

- As of February 28, 2026, the equity ratio in the consolidated financial position was 73.9%.

🤖 AI Perspective

The third-quarter consolidated performance shows an increase in net sales and all profit metrics compared to the same period last year. This suggests that the strong performance across various product lines within the non-woven fabric business is a key driver of overall results. The upward revision of the full-year consolidated earnings forecast following these strong cumulative results may indicate a robust business environment compared to the company’s initial plans.

7607|進和

3150.0

▼ -0.94%

📄 Announcement Facts

- For the second quarter of the fiscal year ending August 2026 (interim period, September 1, 2025 – February 28, 2026), consolidated net sales were ¥44,771 million (up 6.1% year-on-year), operating profit was ¥2,913 million (up 27.2%), ordinary profit was ¥3,012 million (up 22.2%), and net income attributable to parent company shareholders was ¥2,053 million (up 23.8%).

- The equity ratio as of the end of the second quarter of the fiscal year ending August 2026 was 64.2%, an increase from 58.4% at the end of the previous fiscal year.

- An interim dividend of ¥62.00 per share was announced for the fiscal year ending August 2026, with the full-year dividend forecast remaining unchanged at ¥62.00 for the year-end, totaling ¥124.00.

- The full-year consolidated earnings forecast remains unrevised, projecting net sales of ¥87,000 million (up 1.0% year-on-year), operating profit of ¥4,300 million (down 5.2%), ordinary profit of ¥4,500 million (down 6.4%), and net income attributable to parent company shareholders of ¥3,100 million (down 6.4%).

- By segment, the Japan segment reported net sales of ¥37,767 million (up 5.6% year-on-year) and segment profit of ¥2,173 million (up 47.6%), driven by the steady performance of its smart factory innovation business.

🤖 AI Perspective

Shinwa’s Q2 FY2026 results show a notable increase in sales and profits compared to the previous interim period, which appears to be supported by the robust performance of the smart factory innovation business, particularly in the Japan segment. Investors may find it noteworthy that while the interim results were strong, the full-year consolidated earnings forecast remains unchanged and projects a year-on-year decline in profits. This discrepancy between the interim performance and the full-year guidance could be a point of focus for monitoring future business developments.

7610|テイツー

146.0

▼ -1.35%

📄 Announcement Facts

- Teitoo Co., Ltd. has revised its consolidated financial forecast for the fiscal year ending February 2026 (March 1, 2025 to February 28, 2026) upwards.

- The revised forecasts are: Net Sales of 42,233 million yen (up 5.6% from previous), Operating Income of 1,377 million yen (up 25.2%), Ordinary Income of 1,355 million yen (up 23.2%), and Net Income Attributable to Owners of Parent of 867 million yen (up 23.9%).

- Key reasons for the upward revision of the financial forecast include increased sales of new game-related products associated with the launch of the new “Nintendo Switch 2” console, robust sales of trading cards and used products, and improved profitability through optimized product mix and enhanced sales strategies.

- The year-end dividend forecast for the fiscal year ending February 2026 has been revised from 4.00 yen per share to 5.00 yen per share, including a special dividend of 1.00 yen. The total annual dividend will also be 5.00 yen.

- The reason for the dividend forecast revision is to enhance shareholder returns, considering the current fiscal year’s performance outlook and the expected recording of gains from the sale of the company’s treasury shares.

🤖 AI Perspective

The upward revision of performance forecasts, driven by anticipated sales expansion from the “Nintendo Switch 2” and strong performance in existing segments like trading cards and used goods, may suggest positive momentum across multiple business areas. The decision to include a special dividend, attributed to a favorable performance outlook and a gain from the sale of shares, could indicate the company’s commitment to shareholder returns.

9270|G-バリュエンスHD

2091.0

▼ -2.61%

📄 Announcement Facts

- For the second quarter (interim period) of the fiscal year ending August 2026, consolidated net sales were JPY 51,970 million, marking a 27.3% increase year-on-year.

- Operating income reached JPY 3,554 million (up 408.9% YoY), ordinary income JPY 3,454 million (up 415.8% YoY), and net income attributable to owners of parent JPY 2,252 million (up 694.2% YoY).

- The full-year consolidated earnings forecast for the fiscal year ending August 2026 was revised upwards, projecting net sales of JPY 106,000 million, operating income of JPY 5,500 million, ordinary income of JPY 5,260 million, and net income attributable to owners of parent of JPY 3,000 million.

- The annual dividend forecast was revised to JPY 45.00 per share for the fiscal year-end (revision from the most recently announced forecast).

- During the interim consolidated accounting period, total procurement amounted to JPY 40,967 million (up 29.8% YoY), and the total number of purchasing stores reached 192 (139 domestic, 53 overseas).

🤖 AI Perspective

The significant growth in net sales and profits during the interim period may suggest that the company’s structural reforms and focused investments in retail expansion and overseas procurement are yielding positive results. The steady increase in procurement volume and the launch of cross-border e-commerce could indicate a strengthening of future revenue streams. Furthermore, the upward revision of both the full-year earnings forecast and the dividend forecast might be interpreted as a sign of management’s confidence in the current business performance.

3454|ファーストブラザーズ

1227.0

▼ -0.73%

📄 Announcement Facts

- First Brothers announced its consolidated financial results for the first quarter of the fiscal year ending November 2026 (December 1, 2025, to February 28, 2026).

- Consolidated net sales reached ¥3,789 million, marking a 61.6% increase year-on-year. Operating profit was ¥506 million (+63.6% YoY), ordinary profit was ¥319 million (+272.1% YoY), and net income attributable to owners of parent was ¥491 million (+622.3% YoY).

- Diluted earnings per share for the quarter stood at ¥35.02.

- By business segment, the Investment Banking business reported net sales of ¥3,254 million (+76.5% YoY) and operating profit of ¥722 million (+25.6% YoY), contributing significantly to the overall revenue and profit growth.

- The full-year consolidated earnings forecast for FY2026 (net sales ¥17,730 million, net income attributable to owners of parent ¥2,620 million) and the year-end dividend forecast (¥37.00) remain unchanged from the previously announced figures.

🤖 AI Perspective

The strong revenue and profit growth in Q1 appears to be largely driven by proactive property sales in the Investment Banking segment from the start of the period. Given that the company’s quarterly performance can fluctuate significantly based on the timing of property sales, the full-year consolidated earnings forecast has been maintained. The notable increase in net income attributable to owners of parent for Q1, coupled with a full-year forecast anticipating a 49.7% increase, suggests that the initial quarter’s performance may provide a solid start towards annual targets.

2769|ヴィレッジV

951.0

▼ -0.11%

📄 Announcement Facts

- Village Vanguard Co., Ltd. concluded a business alliance agreement with Growth Partners Co., Ltd. on April 10, 2026.

- On the same day, the company resolved to issue the 7th series of stock acquisition rights and the 1st series of unsecured convertible bond-type stock acquisition rights through a third-party allocation to GP Listed Company Investment Limited Partnership, a fund serviced by Growth Partners.

- The issuance of the 7th series of stock acquisition rights is expected to raise a total of JPY 1,507,448,630 (JPY 7,482,430 for issuance and JPY 1,499,966,200 for exercise) on the payment date of April 30, 2026.

- The background to this business and capital alliance includes operating losses, ordinary losses, and net losses attributable to parent company recorded in the fiscal years ending May 2024 and May 2025, leading to a breach of financial covenants with financial institutions.

- Growth Partners will provide management and business support, including sales data analysis, product strategy development, partner introductions, human resource support, cost structure analysis, and operational efficiency proposals. Growth Partners will also be granted the right to appoint one director to the company’s board.

🤖 AI Perspective

This alliance appears to be a critical step for Village Vanguard to strengthen its financial foundation and advance its business restructuring, especially given its past losses and financial covenant issues. The swift capital injection from the third-party allocation and specialized management support from Growth Partners could enable accelerated profitability improvements and growth investments. Investors may monitor the tangible progress of business improvements and their impact on future performance.

💡 Start investing with IR insights

※ 本ページには広告が含まれます(PR)

Disclaimer: This article is for informational purposes only and does not constitute investment advice. All investment decisions are at your own risk.

コメント