📌 Today’s Highlights

Today we cover 29 IR announcements. Notable among them: コシダカHD (2157), SMDAM Jリート (1398), iFJリート (1488). Use the table of contents below to navigate to each company.

- 2157|コシダカHD

- 1398|SMDAM Jリート

- 1488|iFJリート

- 8624|いちよし

- 4728|トーセ

- 5078|セレコーポレーション

- 2411|ゲンダイAG

- 3462|R-NMF

- 3488|R-セントラル

- 441A|G-NE

- 523A|G-セイワHD

- 7175|今村証券

- 7271|安永

- 7366|LITALICO

- 9147|NXHD

- 9332|NISSOHD

- 2080|PBR1倍割れ解消

- 3967|G-エルテス

- 459A|野村高利回りJリート

- 6025|日本PCサービス

- 6927|ヘリオステクノH

- 8366|滋賀銀

- 8714|池田泉州

- 2930|北の達人

- 3823|WHY HOW DO

- 8233|高島屋

- 8707|岩井コスモ

- 304A|G-フォルシア

- 7050|G-フロンティアI

2157|コシダカHD

1050.0

▲ +0.67%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Koshidaka Holdings Co., Ltd. officially announced the release of additional explanatory materials for its “Q2 FY2026 Earnings Briefing” on April 17, 2026.

- The added content includes “3 EIP Final Stage – Towards FY2027/8” from page 27 onwards, supplementing the previously released “1 Q2 FY2026 Earnings Overview” and “2 FY2025/8 Business Forecast” sections.

- For the cumulative period of Q2 FY2026, consolidated results reported net sales of JPY 38,932 million (up 14.5% year-on-year), operating profit of JPY 5,004 million (down 2.1% year-on-year), and net profit attributable to owners of parent of JPY 3,884 million (up 21.7% year-on-year).

- The decrease in operating profit was primarily attributed to a decline in sales from the previous period’s large-scale collaboration projects (existing stores excluding collaborations were up 101.5% year-on-year) and increased fixed costs due to upfront investments, including the introduction of new POS systems and E-bo.

- The increase in net profit was due to the recording of a gain on the transfer of fixed assets (Atsugi Vista Hotel). The projected annual dividend is JPY 26 (JPY 13 interim, JPY 13 year-end), representing a JPY 2 increase and marking the highest amount on record, considering stock splits, for the fifth consecutive year.

🤖 AI Perspective

- The additional disclosure of earnings presentation materials, particularly the “EIP Final Stage” section, may suggest Koshidaka Holdings’ intent to provide further insights into its future business strategies to investors.

- The combination of record-high net sales, a decline in operating profit due to upfront investments, and an increase in net profit driven by asset sales highlights a mixed financial picture that could warrant closer examination of underlying business performance versus one-off gains.

- The planned fifth consecutive annual dividend increase may be viewed positively by shareholders as an indicator of the company’s commitment to shareholder returns.

1398|SMDAM Jリート

1980.5

▲ +0.43%

📎 Source:SMDAM Jリート Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SMDAM TSE REIT Index ETF (1398) announced its financial results for the 2026 March fiscal period (September 9, 2025 to March 8, 2026) on April 17, 2026.

- Total net assets for the 2026 March period amounted to JPY 148,220 million, an increase from JPY 141,203 million in the previous specific period (2025 September period).

- The NAV per 100 units for the same period was JPY 200,917, showing an increase compared to JPY 194,011 in the previous specific period.

- The distribution per 100 units was announced as JPY 4,510 (JPY 4,210 in the 2025 September period), with the distribution payment scheduled to begin on April 16, 2026.

- Total operating revenue was JPY 8,414 million and net income for the period was JPY 8,208 million, both decreasing compared to the previous specific period.

🤖 AI Perspective

The financial results for the SMDAM TSE REIT Index ETF for the 2026 March period indicate growth in total net assets, NAV per 100 units, and distribution per 100 units, which may suggest an expansion in the fund’s asset base and increased returns to beneficiaries. While total operating revenue and net income for the period decreased from the previous specific period, this could be influenced by the timing and valuation methods of securities trading gains and losses in an ETF’s income statement. The trends in net assets, NAV, and distributions are worth monitoring as key indicators of the fund’s performance.

1488|iFJリート

1993.0

▼ -0.35%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- iFreeETF Tokyo Stock Exchange REIT Index (Code: 1488) released its earnings report for the fiscal period ended March 2026 (September 5, 2025 – March 4, 2026) on April 17, 2026.

- Total net assets at the end of the period (as of March 4, 2026) amounted to JPY 274,166 million.

- The Net Asset Value per unit for the period was JPY 2,011.59, and the dividend per unit was JPY 32.

- Primary invested assets totaled JPY 268,376 million, representing a 97.9% composition ratio of the net assets.

- The number of issued units at the end of the period reached 136,293 thousand units, with 17,180 thousand units created and 15,482 thousand units exchanged during the period.

🤖 AI Perspective

The reported increase in total net assets and Net Asset Value per unit from the previous period, coupled with the dividend payment of JPY 32 per unit, may suggest stable fund performance during this period. The rise in issued units could indicate ongoing market interest and demand for the fund.

8624|いちよし

1494.0

▼ -2.73%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Ichiyoshi Securities Co., Ltd. announced preliminary consolidated financial results for the fiscal year ended March 2026 on April 17, 2026. The official announcement is scheduled for April 28, 2026.

- Consolidated operating revenue for the fiscal year ended March 2026 was ¥24,579 million, representing a 30.7% increase compared to the previous year’s ¥18,804 million.

- Consolidated operating profit for the same period reached ¥6,160 million, a substantial increase of 169.5% from ¥2,285 million in the prior fiscal year.

- Net profit attributable to owners of parent amounted to ¥4,392 million, an increase of 180.8% from ¥1,564 million in the previous fiscal year. Earnings per share were ¥137.32.

- The company cited the smooth accumulation of fund wrap and investment trust balances, indicating further progress in shifting towards a stock-type business model, and an increase in other fees received from beneficiary certificates, as key reasons for the revenue growth.

🤖 AI Perspective

The preliminary results indicate significant year-over-year growth across key profit metrics, which may be attributed to a strategic shift towards a stock-type business model. The reported increase in fund wrap and investment trust balances could suggest a strengthening of recurring revenue streams, a development that might be viewed positively by investors in the context of a market sensitive industry like securities. This shift towards stable revenue sources is a factor worth monitoring for its potential impact on long-term performance.

4728|トーセ

637.0

▲ +0.47%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the second quarter of the fiscal year ending August 2026 (interim period), TOSE reported consolidated net sales of ¥3,459 million (up 9.7% year-on-year), operating profit of ¥331 million (up 3.8% year-on-year), and net profit attributable to parent company shareholders of ¥242 million (up 156.2% year-on-year).

- The Game Business segment recorded net sales of ¥3,272 million (up 17.6% year-on-year) and segment operating profit of ¥324 million (up 22.6% year-on-year), driving the overall performance.

- Within the Game Business, console and PC-related sales increased to ¥2,710 million (up 28.7% year-on-year), while smartphone-related sales decreased to ¥559 million (down 16.8% year-on-year).

- Among key development projects projected to generate over ¥500 million in sales between FY2026 and FY2027, Project D with an overseas client has been temporarily halted with no confirmed restart date. Conversely, new Project E with a domestic existing client has been launched.

- The significant increase in net profit attributable to parent company shareholders is primarily due to the absence of special losses in the current interim period, which occurred in the prior year related to the rebuilding of Nagaokakyo TOSE Building (impairment loss on buildings and tenant relocation compensation expenses).

🤖 AI Perspective

TOSE’s interim results indicate that its game business, particularly console and PC-related projects, is a key driver of performance. While smartphone-related sales have declined, the company achieved overall revenue and profit growth. The temporary halt of one development project and the launch of a new one may suggest a dynamic shift in the company’s project portfolio.

5078|セレコーポレーション

4810.0

▲ +1.05%

📎 Source:セレコーポレーション Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- CEL Corporation released its FY2026/2 earnings presentation on April 17, 2026.

- The company has formulated “Vision 2030,” targeting a business group with ¥100 billion in sales and a 10% operating profit margin by 2030. Financial targets include a market capitalization of ¥25 billion, ROE of 9%, and PBR of 1x.

- As of February 28, 2026, the tradable share ratio was 25.65%, meeting the TSE’s listing maintenance standard of 25%, with a commitment to further improvement.

- Effective March 1, 2026, organizational restructuring was implemented, establishing a new Design Company separated from the Construction Company and integrating the Reform Company into the Property Community Company.

- Following the Ordinary General Meeting of Shareholders scheduled for May 28, 2026, the executive structure will be revised, increasing the number of outside directors from three to four and female directors to three.

🤖 AI Perspective

The company’s explicit financial targets within its long-term “Vision 2030” may suggest a strong commitment to future growth and shareholder value creation. Meeting the TSE listing maintenance criteria and the stated intention to further improve the tradable share ratio could indicate an ongoing focus on corporate governance and market confidence. The organizational restructuring and executive board changes might be viewed as strategic steps to optimize the management structure for achieving the outlined business objectives.

2411|ゲンダイAG

491.0

▲ +2.72%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the consolidated fiscal year ended March 31, 2026, net sales amounted to JPY 7,531 million, representing a 1.9% decrease year-on-year, while operating profit was JPY 674 million (up 61.2% year-on-year), ordinary profit JPY 680 million (up 63.3% year-on-year), and profit attributable to owners of parent JPY 473 million (up 32.0% year-on-year).

- The annual dividend for FY2026/3 was JPY 24.00 (compared to JPY 20.00 for the previous fiscal year), with an estimated JPY 25.00 for FY2027/3.

- The consolidated performance forecast for FY2027/3 anticipates net sales of JPY 8,000 million (up 6.2% year-on-year), operating profit of JPY 800 million (up 18.6% year-on-year), ordinary profit JPY 800 million (up 17.6% year-on-year), and profit attributable to owners of parent JPY 520 million (up 9.8% year-on-year).

- Regarding the business environment, a rapid decline in print media advertising due to a digital shift in the pachinko hall advertising market was reported. However, the company stated that the issuance of the “Advertising Guideline Third Edition” clarified the scope of possible advertising methods, mitigating risks affecting business performance.

🤖 AI Perspective

Gendai AG’s FY2026/3 results highlight a notable increase in profits despite a slight decline in revenue, which may suggest improved operational efficiency or a strategic shift towards higher-margin services. The positive forecast for FY2027/3, including projected revenue and profit growth and a further dividend increase, indicates management’s confidence in continued performance. The company’s adaptation to the digital shift in the pachinko hall advertising market and the clarification of advertising guidelines could also be a factor worth monitoring for future stability.

3462|R-NMF

165300.0

▼ -0.18%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal period ended February 2026 (September 1, 2025 to February 28, 2026), operating revenue was JPY 41,186 million, marking a 5.8% decrease compared to the previous period.

- Net income for the same period amounted to JPY 13,355 million, a 17.1% decrease from the prior period.

- The distribution per unit for February 2026, including JPY 522 in excess distributions, totaled JPY 3,634.

- The payout ratio for the February 2026 period stood at 108.2%.

- The forecast for the August 2026 period (March 1, 2026 to August 31, 2026) projects an operating revenue of JPY 43,116 million (+4.7% QoQ) and net income of JPY 15,052 million (+12.7% QoQ).

🤖 AI Perspective

Although R-NMF reported a decrease in operating revenue and net income for the February 2026 period compared to the previous period, the distribution per unit, including excess distributions, remained strong at JPY 3,634, exceeding the prior period’s JPY 3,542. The operational forecasts for the upcoming August 2026 and February 2027 periods indicate anticipated fluctuations in both operating revenue and net income, making future performance trends worth monitoring. A payout ratio exceeding 100% suggests management’s strategy to utilize excess distributions to maintain stable distribution levels for investors.

3488|R-セントラル

111900.0

▼ -0.27%

📎 Source:R-セントラル Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Operating revenue for the fiscal period ending February 2026 reached ¥2,156 million, marking a 25.8% increase compared to the previous period (August 2025).

- During the same period, operating income was ¥936 million (up 1.1% period-on-period), ordinary income was ¥809 million (up 0.4%), and net income was ¥808 million (up 0.4%).

- Distribution per unit (DPU) was ¥3,238 (excluding excess distributions), with a dividend payout ratio of 100.0%.

- Total assets at the end of the period were ¥48,956 million, net assets were ¥26,410 million, and the equity ratio was 53.9%.

- The forecast DPU for the August 2026 period is ¥3,343, and for the February 2027 period, it is ¥3,143.

🤖 AI Perspective

The substantial increase in operating revenue may suggest positive developments in portfolio management. The DPU increased period-on-period, and a 100.0% payout ratio indicates a continued commitment to returning earnings to unitholders. With DPU forecasts provided for upcoming periods, the investment corporation’s future operational performance could be worth monitoring.

441A|G-NE

628.0

▼ -0.63%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-NE Inc. resolved to conclude a “Basic Agreement for Business Alliance” with Cafe24 Corp. at its Board of Directors meeting held on April 17, 2026.

- The basic agreement is scheduled to be signed on April 20, 2026, with the comprehensive business alliance agreement slated for May 18, 2026.

- The alliance aims to strongly support cross-border e-commerce businesses for customers of both companies by combining Cafe24’s strengths in global e-commerce platforms and G-NE’s expertise in automating EC backend operations.

- Key aspects of the agreement include supporting Cafe24 customers’ entry into the Japanese market, G-NE customers’ entry into the Korean and Asian markets, efforts towards system and data integration, and joint marketing activities.

- Cafe24 Corp., based in South Korea, reported consolidated sales of 271.1 billion won and consolidated operating profit of 1.5 billion won for the fiscal year ended December 2023.

🤖 AI Perspective

- This basic agreement is viewed as a preliminary step towards establishing a framework for mutual support, enabling Japanese EC businesses to enter Korean and Asian markets, and Korean brands to enter the Japanese market.

- The integration of both companies’ platforms could potentially enhance efficiency and expand sales channels for client companies engaged in cross-border e-commerce.

- Amid intensifying competition in the global e-commerce market, alliances between companies with complementary strengths are observed as a strategic move to foster growth.

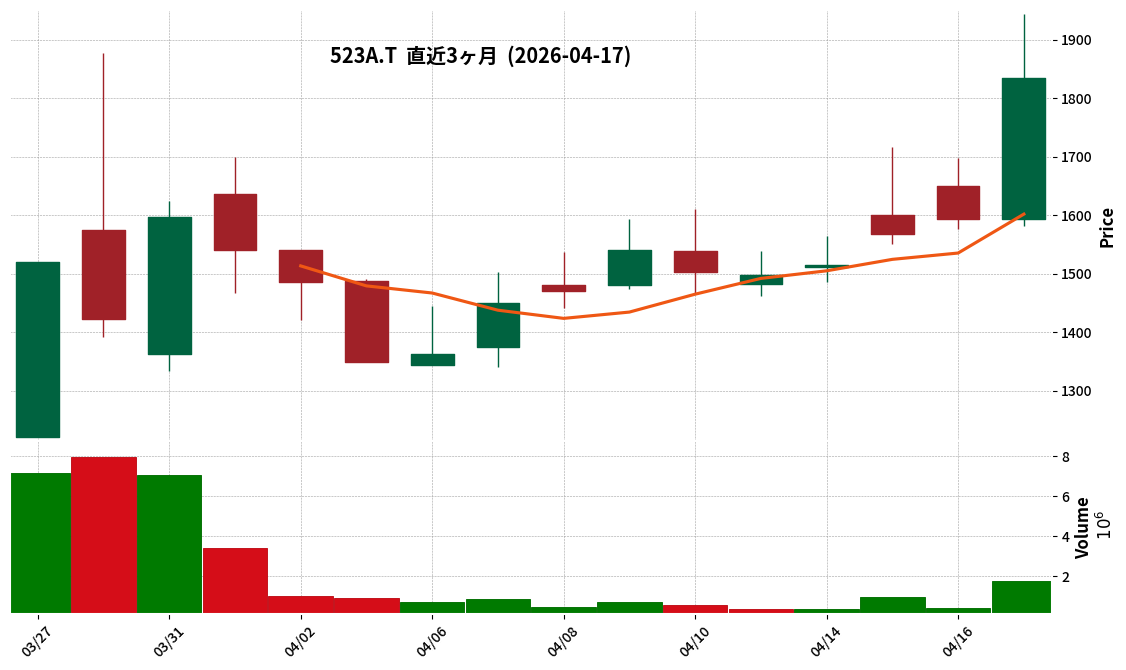

523A|G-セイワHD

1835.0

▲ +15.12%

📎 Source:G-セイワHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Seiwa Holdings Co., Ltd. released its Q3 FY2026 earnings presentation video and transcript on April 17, 2026.

- The achievement rate for net profit based on the current period budget for Q3 FY2026 reached 87.4%, exceeding the company’s plan.

- The company announced that its full-year guidance is expected to be achieved.

- The company operates a manufacturing-focused business succession platform and possesses an investment capacity of approximately JPY 5.7 billion to JPY 7.6 billion.

- Four new potential investment targets are currently under active consideration.

7175|今村証券

1349.0

▲ +1.28%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Imamura Securities announced preliminary financial results for the fiscal year ending March 31, 2026, on April 17, 2026. The official announcement is scheduled for April 24, 2026.

- According to the preliminary figures for FY2026 (April 1, 2025 – March 31, 2026), operating revenue is 4,914 million yen (up 17.4% year-on-year), operating income is 1,407 million yen (up 42.7%), ordinary income is 1,466 million yen (up 44.1%), and net income is 1,055 million yen (up 38.8%).

- The company attributes these increases in revenue and profit primarily to a rise in commission fees from stocks and beneficiary certificates, as well as the recording of a gain on sale of investment securities as an extraordinary profit.

- Conversely, trading gains from the sale of U.S. dollar-denominated corporate bonds and similar instruments decreased.

- Imamura Securities notes that due to the nature of the financial instruments business, it does not disclose earnings forecasts, and these preliminary figures are current estimates that may differ from actual results.

🤖 AI Perspective

* Investors may observe the significant year-over-year increases across key profitability metrics such as operating revenue, operating income, ordinary income, and net income reported in Imamura Securities’ preliminary FY2026 results.

* This performance could indicate positive momentum driven by increased commission fees from stocks and beneficiary certificates, alongside a strategic gain on the sale of investment securities.

* While these are preliminary figures pending the official release, such robust growth in profitability metrics may warrant monitoring by market participants.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

7271|安永

1097.0

▲ +2.43%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Yasunga Co., Ltd. (Code: 7271) announced on April 17, 2026, a revision to its year-end dividend forecast for the fiscal year ending March 31, 2026.

- The revised year-end dividend per share is 16 yen, an increase of 9 yen from the previous forecast of 7 yen (announced on November 14, 2025).

- This revision results in an expected annual dividend per share of 23 yen for the fiscal year ending March 2026, combining the interim dividend of 7 yen and the revised year-end dividend of 16 yen.

- The annual dividend forecast has been revised upward by 9 yen, from the previously announced 14 yen (7 yen interim + 7 yen year-end).

- The reason for the dividend revision is stated as a comprehensive consideration of recent business performance and the company’s basic policy of maintaining stable dividends.

🤖 AI Perspective

This dividend forecast revision suggests Yasunga’s commitment to a stable profit distribution to shareholders. The significant increase in the year-end dividend, leading to a substantial rise in the annual dividend from 13 yen in the previous period to 23 yen, could be a key point of interest for investors. This move may also indicate a positive trend in the company’s recent business performance.

7366|LITALICO

1263.0

▲ +1.04%

📎 Source:LITALICO Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- LITALICO Co., Ltd. absorbed its wholly owned subsidiary, Plus One Solutions Inc., effective November 1, 2025.

- An extraordinary loss of 140 million yen (loss on cancellation of treasury stock) will be recorded in LITALICO’s non-consolidated financial statements due to this merger.

- This extraordinary loss occurred on the effective date of the merger, November 1, 2025.

- The stated amount of the extraordinary loss is an estimate based on currently available information and may differ from the actual amount.

- This extraordinary loss will be eliminated in the consolidated financial statements, resulting in no impact on LITALICO’s consolidated performance for the fiscal year ending March 2026.

🤖 AI Perspective

This announcement highlights an extraordinary loss recorded solely in LITALICO’s non-consolidated financial statements, with no impact on its consolidated results. A loss on cancellation of treasury stock typically arises from the accounting treatment of an absorption merger of a consolidated subsidiary, representing the difference between the parent company’s book value of the subsidiary’s shares and the net assets taken over. The absence of an impact on consolidated earnings may suggest that investors primarily focused on consolidated performance would not need to factor this specific loss into their valuation.

9147|NXHD

3847.0

▼ -0.03%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nippon Express Holdings (NXHD) resolved and signed a stock transfer agreement on April 17, 2026, to acquire shares of Metro Supply Chain Group Inc. through its wholly-owned Canadian special purpose company, making it a subsidiary.

- Metro Supply Chain Group Inc. is a 3PL provider primarily based in Canada, the U.S., and the U.K., offering contract logistics services across diverse sectors including retail, consumer goods, automotive, and healthcare.

- The acquisition value is CAD 1,800 million (approximately JPY 207 billion) on an enterprise value basis, with a potential earn-out payment of up to CAD 400 million (approximately JPY 46 billion) contingent on the target company’s financial performance.

- The transaction is expected to be executed between July and December 2026, subject to the fulfillment of preconditions such as the completion of competition law procedures in various countries.

- NXHD states that this transaction aims to enhance its presence in the North American market, expand its sales logistics domain, and create synergies in the logistics business by leveraging complementary customer bases and regional strengths.

🤖 AI Perspective

This acquisition appears to be a key move in NXHD’s “NX Group Management Plan 2028” strategy to accelerate global business growth. The strengthening of its North American market presence and the integration of Metro Supply Chain Group’s diverse client base and expertise could potentially reshape NXHD’s revenue streams. Given the scale of this M&A, investors may wish to monitor the realization of post-integration synergy effects and the impact on the consolidated financial performance for the fiscal year ending December 2026, as further details are expected to be disclosed.

9332|NISSOHD

624.0

▲ +0.97%

📎 Source:NISSOHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- NISSO HOLDINGS Co., Ltd. resolved to merge its consolidated subsidiary and grandchild company at a board meeting held on April 17, 2026.

- The merger will take place between Man to Man Holdings Co., Ltd. (the dissolving company), a consolidated subsidiary of NISSO HOLDINGS, and Man to Man Co., Ltd. (the surviving company), its grandchild company.

- The effective date of this merger is scheduled for June 1, 2026.

- The stated purpose of the merger is to eliminate dual holding company functions within the group, promote management integration, restructure businesses, and improve operational efficiency to strengthen overall group profitability and growth.

- As this merger is between consolidated subsidiary and grandchild companies, its impact on NISSO HOLDINGS’ consolidated financial results is expected to be minor.

🤖 AI Perspective

This merger appears to be a move by NISSO HOLDINGS to streamline its internal organizational structure and enhance management efficiency. By dissolving the dual holding company functions, the company likely aims to strengthen its governance framework and enable operating companies to execute strategies more swiftly and flexibly. Given the minor expected impact on consolidated results, the focus seems to be on reinforcing the group’s long-term operational foundation rather than short-term financial gains.

2080|PBR1倍割れ解消

1817.0

▼ -1.20%

📎 Source:PBR1倍割れ解消 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- PBR1倍割れ解消推進ETF (Code 2080) announced its interim financial results for the fiscal year ending September 2026 (September 11, 2025 – March 10, 2026) on April 17, 2026.

- Total net assets as of the end of the interim period (March 10, 2026) amounted to ¥12,663 million, an increase from ¥8,924 million at the end of the previous fiscal period (September 10, 2025).

- The Net Asset Value per unit at the end of the interim period was ¥1,761, up from ¥1,414 at the end of the previous fiscal period.

- Operating revenue for the interim period was ¥2,231,159,121, with interim net income reported at ¥2,175,702,987.

- The number of outstanding units at the end of the interim period was 7,190 thousand units, an increase from 6,310 thousand units at the end of the previous fiscal period.

🤖 AI Perspective

The PBR1倍割れ解消推進ETF recorded increases in net assets, Net Asset Value per unit, and interim net income during the latest interim period. This suggests that the fund has generated positive returns through its investments primarily in equities. The rise in outstanding units may also indicate continued investor interest in the fund, potentially reflecting a broader market focus on companies improving their Price-to-Book Ratio.

3967|G-エルテス

589.0

▲ +0.17%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Elites Co., Ltd. released its full-year earnings presentation video and script for the fiscal year ended February 2026 on April 17, 2026.

- For the fiscal year ended February 2026, sales, EBITDA, and operating profit reached record highs, showing year-over-year growth of +22%, +51%, and +362%, respectively.

- While the operating profit margin recovered to 4.8%, a net loss of 168 million yen was recorded due to extraordinary losses totaling 274 million yen, which included approximately 200 million yen related to the JAPANDX carve-out.

- The carve-out of the DX promotion business aims for a sale during the first quarter of the current fiscal year, targeting an exclusion from consolidation as of the beginning of the period, with preparations for individual sales of the four JAPANDX Group companies underway.

- The full-year earnings forecast for the fiscal year ending February 2027, premised on the execution of the DX promotion business carve-out, projects sales of 8.5 billion yen, operating profit of 460 million yen (expected to be a new record high), and an operating profit margin of 5.4%.

🤖 AI Perspective

The record-high sales, EBITDA, and operating profit for the fiscal year ended February 2026 suggest progress in core business growth investments and company-wide cost optimization. However, the net loss driven by extraordinary items, linked to business portfolio restructuring, may be viewed as a temporary measure in the ongoing structural reform. Investors are likely to focus on the impact of the DX promotion business carve-out on next year’s forecasts and the concretization of growth strategies for continuing operations.

459A|野村高利回りJリート

10950.0

▲ +0.00%

📎 Source:野村高利回りJリート Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nomura High Yield J-REIT ETF (Code: 459A) announced its financial results for the fiscal period ending March 2026 (November 11, 2025, to March 12, 2026).

- Net assets for the period totaled JPY 342 million, with the NAV per unit reported at JPY 11,203.69.

- A distribution of JPY 120 per unit was announced, with the distribution payment scheduled to commence on April 20, 2026.

- The number of units set during the period was 30 thousand units, resulting in 30 thousand units outstanding at the end of the specified period.

- The fund recorded an operating loss and a net loss for the current period, both totaling JPY 3,452,736.

🤖 AI Perspective

- As an ETF aiming to track the Nomura High Yield J-REIT Index, primarily investing in real estate investment trust securities, net assets, NAV per unit, and distributions are key indicators of the fund’s performance.

- The reporting of an operating loss and net loss for the period, while still announcing a distribution, may be a point for investors to consider when evaluating the fund’s financials.

- This marks the first financial announcement for the ETF, which was established in November 2025, and future operational results and market conditions will likely be observed for further insights.

6025|日本PCサービス

—

▲ +0.00%

📎 Source:日本PCサービス Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the second quarter of the fiscal year ending August 2026, consolidated net sales reached ¥4,103 million, an increase of ¥869 million compared to the same period last year.

- Consolidated operating profit was ¥116 million and ordinary profit was ¥113 million, marking significant increases of ¥113 million and ¥112 million, respectively, year-on-year.

- Net profit attributable to owners of parent was ¥44 million, reversing a net loss of ¥12 million in the prior year’s corresponding period.

- The revenue growth was attributed to strong performance in corporate DX support, including kitting and proxy setup services, as well as a special demand related to Windows 11 migration.

- The number of individual fixed-rate subscription service members reached 714,063, and corporate insurance-backed maintenance service contracts increased by 21 companies from the previous fiscal year-end to 454 companies as of the end of Q2 FY2026.

🤖 AI Perspective

The significant increase in sales and profit, particularly driven by corporate DX support, suggests a strong demand for digital infrastructure support services. The turnaround from a net loss to a net profit indicates an improvement in profitability, and the sustained demand from Windows 11 migration could continue to support performance. The steady growth in both individual and corporate memberships may also contribute to strengthening a stable revenue base for the future.

6927|ヘリオステクノH

1176.0

▲ +0.00%

📎 Source:ヘリオステクノH Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Helios Techno Holdings Co., Ltd. resolved at its Board of Directors meeting held on April 17, 2026, to absorb its wholly-owned subsidiary, Helios Techno Investments Co., Ltd. (HTI).

- The effective date of the merger is scheduled for June 30, 2026.

- This will be an absorption-type merger with Helios Techno Holdings as the surviving company and HTI being dissolved. The merger will be conducted as a simplified merger for the parent company and a short-form merger for the subsidiary, thus not requiring shareholder approval.

- The stated purpose of the merger is to simplify decision-making processes, improve management efficiency, and further accelerate management judgments, including M&A, within the group.

- As HTI is a wholly-owned subsidiary, the impact of this merger on the company’s consolidated financial results for the current and subsequent periods is expected to be minor.

🤖 AI Perspective

This absorption-type merger of a wholly-owned subsidiary may suggest the company’s ongoing efforts to streamline its group management structure. Integrating M&A-related operations directly into the parent company could potentially lead to faster decision-making and more efficient resource allocation. This move might also indicate a strategic step towards enhancing the speed of future M&A strategy execution.

8366|滋賀銀

2056.0

▼ -2.37%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- The Shiga Bank, Ltd. resolved to form a capital and business alliance with Senshu Ikeda Holdings, Inc. at its Board of Directors meeting held on April 17, 2026.

- Named the “Senshu Ikeda Shiga Alliance,” this partnership involves mutual share acquisition to establish a capital relationship, with an anticipated acquisition ratio of 0.5% to 1% based on current stock prices, aiming to enhance the alliance’s effectiveness.

- The primary areas of business collaboration encompass corporate, individual, sustainability/regional support, and human resources/digital sectors.

- Shiga Bank’s main operating areas are Shiga and Kyoto Prefectures, while Senshu Ikeda Holdings primarily operates in Osaka and Hyogo Prefectures, with the alliance aiming for mutual leverage of management resources across these adjacent service areas.

- Shiga Bank has assessed the immediate impact of this alliance on its consolidated financial results as minor.

🤖 AI Perspective

Amidst an evolving landscape for regional financial institutions, this alliance between two banks with adjacent operating areas appears to be a strategic move to leverage mutual resources and strengthen long-term collaboration. The broad scope of cooperation, from corporate and individual services to digital and sustainability initiatives, could contribute to enhancing their respective regional financial capabilities. The mutual share acquisition suggests a strong commitment to solidifying this partnership.

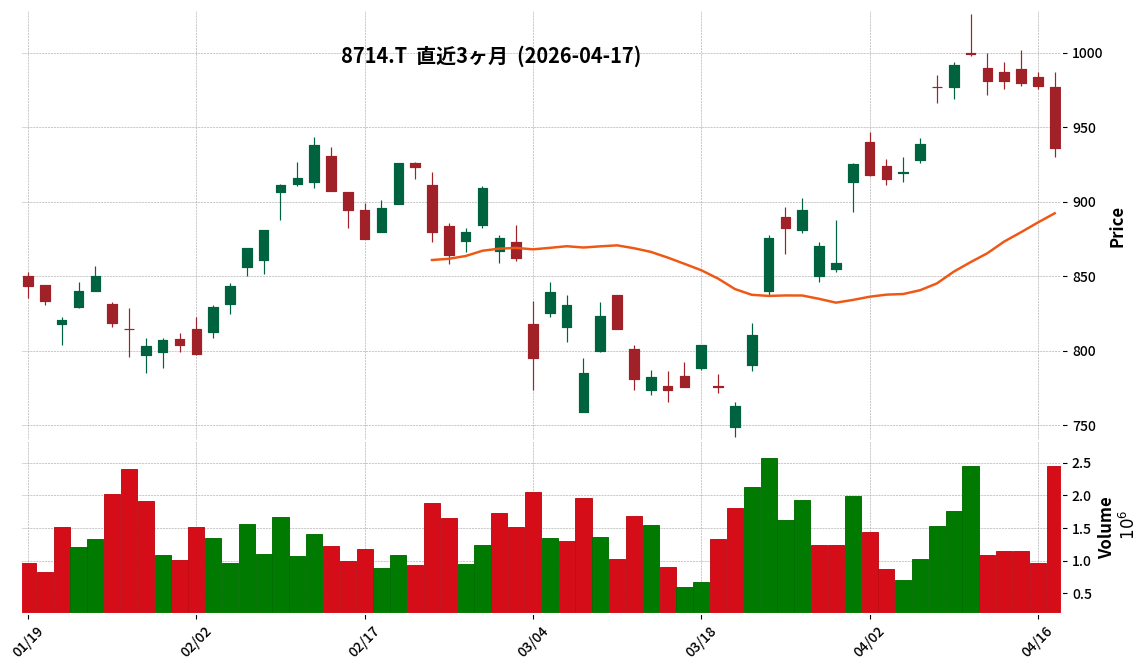

8714|池田泉州

936.0

▼ -4.29%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Ikeda Senshu Holdings Co., Ltd. resolved to enter into a capital and business alliance (named “Ikeda Senshu-Shiga Alliance”) with The Shiga Bank, Ltd. at a Board of Directors meeting held on April 17, 2026.

- Under this alliance, both companies will mutually acquire shares to establish a capital relationship, with an anticipated acquisition ratio of approximately 0.5% to 1% based on current stock prices. The specific number of shares and acquisition method will be determined jointly, considering market conditions.

- Key areas of business collaboration include the corporate sector (corporate growth support, business succession/M&A support, collaboration in growth areas), individual sector (asset formation/succession, wealth management, strengthening consulting functions), sustainability/regional support, and human resources/digital fields.

- Ikeda Senshu Holdings primarily operates in Osaka and Hyogo Prefectures, while Shiga Bank operates mainly in Shiga and Kyoto Prefectures, indicating an intention to mutually leverage their adjacent branch networks, customer bases, human resources, and brand strengths.

- The immediate impact of this alliance on consolidated financial results is considered minor, with a commitment to promptly disclose any significant impacts should they become evident.

🤖 AI Perspective

This alliance appears to be a strategic move by two regional financial institutions to bolster their “regional financial capabilities” in response to environmental shifts such as population decline, changes in industrial structure, and digital advancement. By mutually leveraging management resources in adjacent operating areas, the companies may aim to not only strengthen existing businesses but also create new value. The mutual share acquisition is expected to solidify a long-term cooperative relationship and enhance the effectiveness of the alliance.

2930|北の達人

131.0

▲ +2.34%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kitanotatsujin Corporation announced on April 17, 2026, that it held an earnings presentation for institutional investors and analysts regarding its fiscal year ended February 2026 results on April 16, 2026.

- For the fiscal year ended February 2026, consolidated net sales reached JPY 11,210 million (+9.0% vs. forecast) and operating income was JPY 1,000 million (+11.6% vs. forecast), both exceeding company projections.

- New customer acquisitions, which bottomed out in Q3 FY2025, continued to perform well in Q4 FY2026, marking five consecutive quarters of increase.

- The company forecasts a record-high consolidated net sales of JPY 15,962 million for FY2027 (+42.4% year-on-year), while anticipating only a slight increase in profits due to accelerated upfront investment.

- New products “Refist” and “Coromo” were launched in FY2026, with “Jinax” following in FY2027. The Deep Patch series achieved its sixth consecutive Guinness World Record for the world’s best-selling micro-needle skin patch.

🤖 AI Perspective

The company’s performance exceeding forecasts for FY2026 may suggest that increased advertising expenditure effectively drove new customer acquisition. While FY2027 projects substantial revenue growth, the muted profit increase indicates a strategic focus on upfront investment for business expansion. The consolidation of Karacon Direct Co., Ltd. could signal a diversification of the company’s business portfolio.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

3823|WHY HOW DO

55.0

▲ +34.15%

📎 Source:WHY HOW DO Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- WHY HOW DO announced on April 17, 2026, the determination of the stock exchange ratio for the simplified stock exchange to make Iiyama Doken Co., Ltd. a wholly-owned subsidiary (change in specified subsidiary).

- In this stock exchange, WHY HOW DO will serve as the wholly owning parent company, and Iiyama Doken as the wholly owned subsidiary.

- For each common share of Iiyama Doken, 2,060.338 common shares of WHY HOW DO will be allotted, with no allocation for Iiyama Doken common shares already held by WHY HOW DO.

- The total number of common shares to be delivered by WHY HOW DO in this stock exchange is 1,555,500 shares.

- The stock exchange ratio was calculated by dividing Iiyama Doken’s valuation of JPY 92,715.232 by the average closing price of WHY HOW DO’s common shares over the most recent three weeks (JPY 45) at the reference time (April 17, 2026, 3:30 PM).

🤖 AI Perspective

- This announcement signifies the finalization of specific terms for WHY HOW DO’s complete acquisition of Iiyama Doken, marking a key step in the corporate reorganization process.

- The determined stock exchange ratio is a critical component for investors to understand the valuation and structure of the transaction.

- Given the change in the status of a specified subsidiary, this information could impact WHY HOW DO’s consolidated financial position and business strategy, making it a relevant point for investor monitoring.

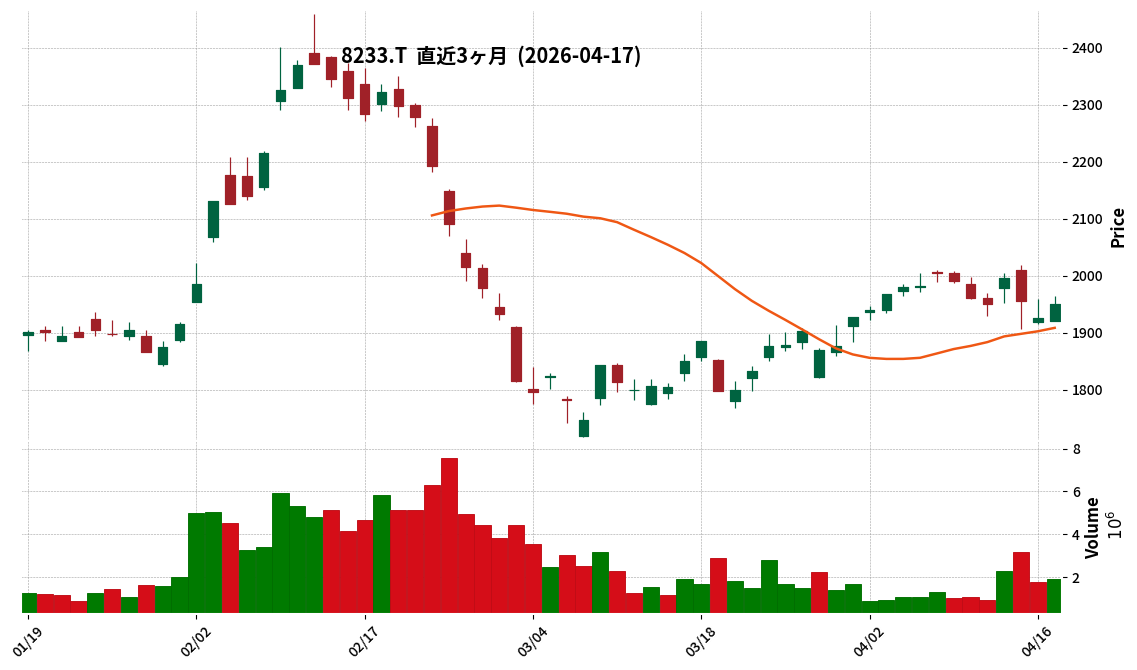

8233|高島屋

1950.5

▲ +1.25%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Takashimaya plans a +6% year-on-year growth for domestic customer sales in FY2026, encompassing both outside sales and general sales.

- Inbound sales for FY2026 are projected at JPY 84.5 billion, a △11% decrease year-on-year, factoring in risks such as exchange rate fluctuations and increased fuel surcharges impacting customer numbers and average spend.

- The company aims to improve its store product profit margin by 0.25 percentage points from the previous year in FY2026, primarily through increasing sales in fashion categories such as women’s clothing and accessories.

- The share repurchase policy for FY2026, previously announced in the FY2025 interim settlement, has been temporarily withdrawn following the repurchase and cancellation of convertible bonds (CB).

- Takashimaya announced its transition to a company with an Audit and Supervisory Committee, aiming to enhance management transparency and objectivity, secure more time for growth strategy discussions, and clearly separate supervision from execution.

🤖 AI Perspective

Takashimaya’s Q&A summary highlights a robust growth plan for domestic customer sales within its department store segment, contrasting with a more conservative inbound sales forecast that accounts for external risks, suggesting a balanced approach to its business portfolio. The temporary withdrawal of the share repurchase policy following the convertible bond repurchase indicates a flexible capital allocation strategy; future distribution of profits among multiple stakeholders when exceeding free cash flow targets may be a point of interest for investors. Furthermore, the shift to an an Audit and Supervisory Committee structure could be viewed as a commitment to enhancing corporate governance and management transparency.

8707|岩井コスモ

3810.0

▲ +0.40%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Iwai Cosmo Holdings announced preliminary consolidated financial results for the fiscal year ended March 31, 2026, on April 17, 2026.

- For FY2026 (April 1, 2025 – March 31, 2026), operating revenue was ¥32,260 million (up 25.3% year-on-year), operating profit was ¥13,007 million (up 50.4% year-on-year), and ordinary profit was ¥13,550 million (up 48.1% year-on-year).

- Net profit attributable to parent company shareholders reached ¥10,443 million (up 55.3% year-on-year), with earnings per share at ¥444.61 (up 55.3% year-on-year).

- The announced operating revenue, operating profit, ordinary profit, and net profit attributable to parent company shareholders all reached record highs.

- The company achieved its 54th consecutive quarter of ordinary profit, with the increase in operating revenue primarily attributed to higher revenue from U.S. equities.

🤖 AI Perspective

The preliminary consolidated results indicate significant year-on-year increases across key revenue metrics, with operating revenue, operating profit, ordinary profit, and net profit attributable to parent company shareholders all reaching record highs. The growth appears to be primarily driven by increased revenue from U.S. equities, suggesting a positive alignment with market trends. The achievement of 54 consecutive quarters of ordinary profit could reflect the company’s consistent operational stability in varying market conditions.

304A|G-フォルシア

2049.0

▲ +3.48%

📎 Source:G-フォルシア Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- FORCIA, Inc. announced its full-year financial results for the fiscal year ending February 2026.

- For the fiscal year 2026/2, revenue was JPY 2,197 million (down 4.9% year-on-year), and operating profit was JPY 71 million (down 66.8% year-on-year).

- The primary reasons for the decrease in revenue and profit were a review of revenue recognition timing for a large project, shifting revenue recognition to the next fiscal year upon customer acceptance, and upfront investments made for development system expansion and product enhancement recognized in the current period.

- Monthly revenue from SaaS-type services increased by 27.0% year-on-year, and the ratio of monthly revenue to total revenue grew to approximately 56%.

- A new large project, expected to be secured in Q3, was successfully awarded and contracted in Q4, with the project progressing as planned.

🤖 AI Perspective

While the reported decline in revenue and profit was attributed to a change in revenue recognition timing for a large project and upfront investments, the company stated that there was no change in the underlying business progress. The robust growth in SaaS monthly revenue and the increasing proportion of recurring revenue may suggest a steady transition towards a stock-based revenue model. Furthermore, the successful completion of new large project contracts and their on-schedule progression could indicate potential future revenue contributions.

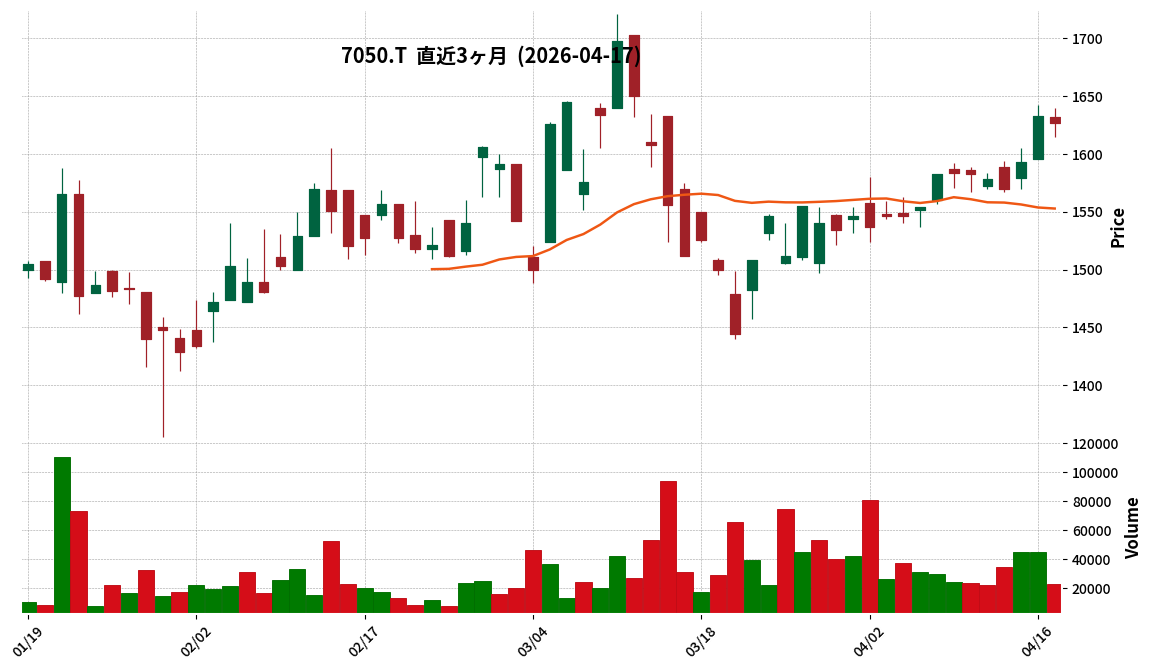

7050|G-フロンティアI

1627.0

▼ -0.37%

📎 Source:G-フロンティアI Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Frontier I Co., Ltd. announced a further upward revision to its consolidated earnings forecast for the fiscal year ending April 2026.

- The revised forecast for the fiscal year ending April 2026 includes net sales of ¥30,175 million (up 5.9% from previous forecast), operating profit of ¥2,097 million (up 16.5%), ordinary profit of ¥2,106 million (up 15.7%), and profit attributable to owners of parent of ¥1,140 million (up 2.7%).

- The reasons for the earnings forecast revision are cited as favorable business progress and the completion of adjustments for Purchase Price Allocation (PPA) and its amortization for NPU Co., Ltd., which became a consolidated subsidiary in the second quarter.

- The company revised its year-end dividend forecast for the fiscal year ending April 2026 from ¥63.00 per share to ¥65.00 per share (an increase).

- This dividend revision is based on the updated consolidated earnings forecast and the company’s dividend policy which targets a payout ratio of approximately 50%.

🤖 AI Perspective

This announcement, being a “further upward revision” to the full-year earnings forecast, may suggest continued strong business performance. The integration of NPU Co., Ltd.’s Purchase Price Allocation (PPA) into the forecast could indicate increased clarity in future financial outlooks by resolving some uncertainties. Furthermore, the dividend increase, guided by a payout ratio target of 50%, can be seen as reflecting the company’s proactive stance towards shareholder returns.

💡 Start investing with IR insights

※ 本ページには広告が含まれます(PR)

Disclaimer: This article is for informational purposes only and does not constitute investment advice. All investment decisions are at your own risk.

コメント