📌 Today’s Highlights

Today we cover 47 IR announcements. Notable among them: IMV (7760), オーウエル (7670), A&Aマテリアル (5391). Use the table of contents below to navigate to each company.

- 7760|IMV

- 7670|オーウエル

- 5391|A&Aマテリアル

- 3663|セルシス

- 2730|エディオン

- 9831|ヤマダHD

- 5902|ホッカンHD

- 6292|カワタ

- 7279|ハイレックス

- 9244|G-デジタリフト

- 490A|P-センス・トラスト

- 1914|日基礎

- 7265|エイケン工業

- 9478|SE H&I

- 3854|アイル

- 2353|日駐

- 2413|エムスリー

- 3193|エターナルホスピG

- 3662|エイチームHD

- 3915|テラスカイ

- 4056|G-ニューラル

- 4263|G-サスメド

- 436A|G-サイバーSOL

- 4502|武田薬

- 6040|G-日本スキー

- 6045|G-レントラックス

- 6046|リンクバル

- 7039|G-ブリッジグループ

- 7694|G-いつも

- 8253|クレセゾン

- 8439|東京センチュリー

- 9505|北陸電力

- 9678|カナモト

- 6999|KOA

- 3733|ソフトウェアS

- 2160|G-GNI

- 4436|G-ミンカブ

- 4493|G-サイバーセキュリ

- 6562|G-ジーニー

- 8917|ファースト住建

- 9366|サンリツ

- 6574|G-コンヴァノ

- 7078|G-INC HD

- 9686|東洋テック

- 6777|santecHD

- 7984|コクヨ

- 2894|石井食

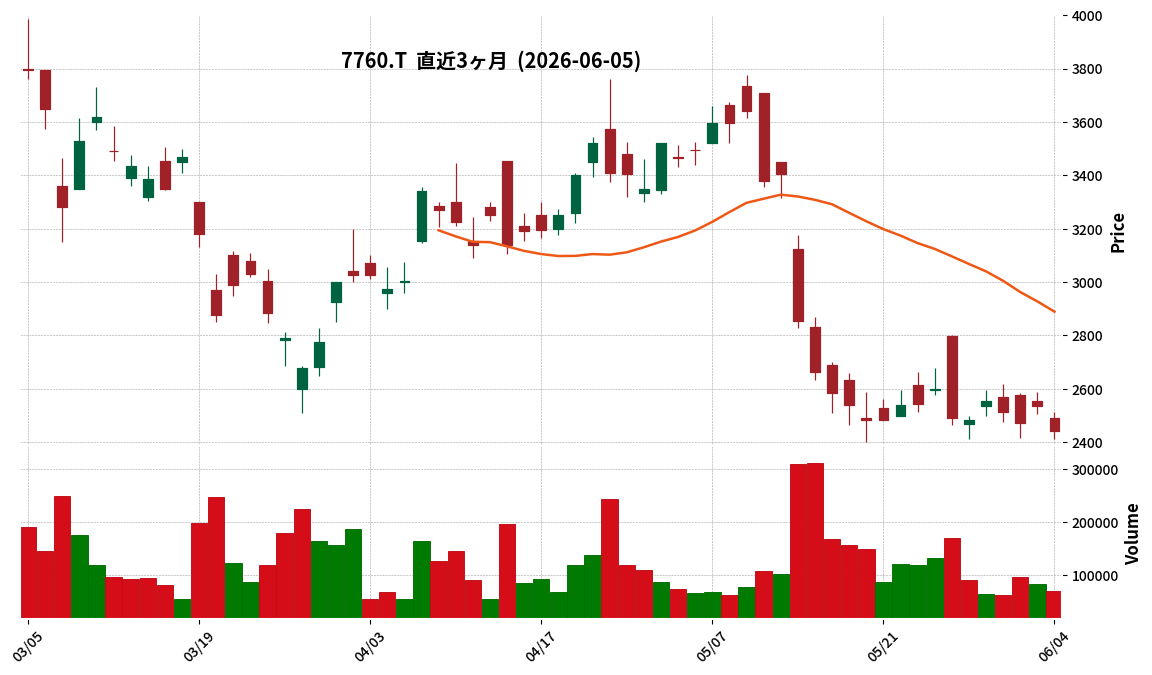

7760|IMV

2444.0

▼ -3.55%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- IMV reported for the first half of fiscal year 2026 (ending September), net sales of ¥11,511 million (+20.8% YoY), operating profit of ¥1,873 million (+26.6% YoY), ordinary profit of ¥2,088 million (+33.2% YoY), and net profit attributable to owners of parent of ¥1,462 million (+22.4% YoY).

- This marks the fourth consecutive period of increased revenue and profit for the cumulative second quarter.

- By segment, DSS (Vibration Simulation System) net sales reached ¥8,727 million (+24.6% YoY) and TSS (Test & Solution Service) net sales were ¥2,200 million (+17.9% YoY). MES (Measuring System) net sales were ¥582 million (△11.1% YoY).

- A new service hub was established in Orange County, California, in March 2026.

- Sales to the aerospace and defense industries showed growth, with expanding transactions not only in Japan but also with major companies in Europe and the U.S.

🤖 AI Perspective

IMV’s strong performance in H1 FY2026, with significant growth in both revenue and profit across all stages, is notable, primarily driven by the robust DSS and TSS segments. Achieving four consecutive periods of revenue and profit growth may suggest the company’s stable business foundation and growth potential. The establishment of a new service hub on the U.S. West Coast and increasing sales in the aerospace and defense industries could indicate future global expansion and potential shifts in revenue structure, making them worth monitoring for investors.

7670|オーウエル

1005.0

▼ -0.10%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the consolidated fiscal year ended March 2026, O-WELL reported net sales of JPY 68.268 billion, a 1.7% decrease year-on-year.

- Operating profit was JPY 1.261 billion (up 1.8%), ordinary profit was JPY 1.680 billion (up 5.5%), and profit attributable to owners of parent was JPY 1.798 billion (up 1.0%). All profit figures exceeded both the previous year’s results and initial forecasts.

- By segment, the Electronics-Related Business recorded sales of JPY 20.407 billion (down 0.2%) and achieved an increase in segment profit to JPY 761 million (up 32.7%).

- The Coating-Related Business saw sales of JPY 47.861 billion (down 2.3%) and segment profit of JPY 2.253 billion (down 9.2%).

- The equity ratio improved from 46.6% at the end of the previous fiscal year to 52.5%.

🤖 AI Perspective

O-WELL’s fiscal year 2026 results show resilience with profit growth despite a slight dip in net sales. The robust performance of the Electronics-Related Business appears to have been a key driver of overall profitability. The improved equity ratio suggests a strengthening of the company’s financial position, which could be a positive indicator for future stability.

5391|A&Aマテリアル

1429.0

▲ +1.13%

📎 Source:A&Aマテリアル Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- A&A Material reported consolidated financial results for the fiscal year ended March 2026, with net sales of ¥45,700 million (up 5.2% year-on-year), operating income of ¥1,674 million (down 12.6% year-on-year), and net income of ¥1,701 million.

- For the fiscal year ending March 2027, the company forecasts net sales of ¥52,600 million (up 15.1% year-on-year), operating income of ¥2,100 million (up 25.4% year-on-year), and net income of ¥1,200 million.

- A capital policy was announced to achieve a PBR of 1x. This includes the acquisition of 2,150 thousand treasury shares, the cancellation of 850 thousand treasury shares, and a third-party allotment through the issuance of 1,300 thousand stock acquisition rights.

- In FY2026/3, the Building Materials business saw sales increase to ¥23,067 million (up 23.4% year-on-year) but segment profit decreased to ¥2,253 million (down 8.0%). The Industrial Products business recorded sales of ¥22,575 million (down 8.5% year-on-year) and segment profit of ¥1,323 million (down 6.4% year-on-year).

- Research and development expenses for FY2025 amounted to ¥522 million, and capital expenditures were ¥1,874 million.

🤖 AI Perspective

While net sales increased for the fiscal year ended March 2026, operating income declined, yet the company projects a recovery with increased revenue and profit for the next fiscal year. The announced capital policy, including treasury share transactions to achieve a PBR of 1x, addresses the Tokyo Stock Exchange’s request and may signal a strong commitment to enhancing corporate value. The funds raised through stock acquisition rights are expected to be allocated to future growth investments, making future business developments worth monitoring.

3663|セルシス

1642.0

▲ +2.11%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Celsys Co., Ltd. announced a revision to its per-share dividend forecast following a board meeting held on June 5, 2026.

- The interim dividend forecast for the fiscal year ending December 2026 has been revised upwards from ¥18 to ¥20 per share.

- Consequently, the full-year dividend forecast for the fiscal year ending December 2026 has been revised from ¥38 to ¥40 per share.

- The revision is attributed to record-high net sales and operating income in Q1 FY2026, marking a year-on-year increase, and strong current business progress as detailed in the “May 2026 Monthly Business Progress Report.”

- The previous fiscal year’s (December 2025) interim dividend of ¥22 included a ¥10 commemorative dividend for the Tokyo Stock Exchange Prime Market transition.

🤖 AI Perspective

This dividend revision, driven by robust Q1 performance and favorable business progress, may signal Celsys’s commitment to shareholder returns. When excluding the previous year’s commemorative dividend, this revision could be viewed as a substantive increase in ordinary dividends. Investors might also monitor the company’s stated intent to “flexibly implement additional shareholder return measures for the current fiscal year.”

2730|エディオン

2585.0

▼ -3.07%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Yamada Holdings Co., Ltd. and Edion Corporation signed a basic agreement on June 5, 2026, for a management integration through a holding company structure.

- The integration will primarily involve a joint share transfer to establish a holding company, making both companies wholly owned subsidiaries.

- If the share transfer is completed, the combined net sales of both companies for the fiscal year ended March 2026 would be approximately 2.5 trillion yen (Yamada Holdings: ¥1,691.8 billion, Edion: ¥793.746 billion).

- The share transfer is expected to take effect, and the holding company is scheduled to be listed on October 1, 2027, with an application for a new listing (technical listing) on the Tokyo Stock Exchange Prime Market.

- Stated objectives for the integration include pursuing scale merits, expanding business domains centered on “lifestyle,” strengthening national distribution networks, and optimizing the supply chain.

🤖 AI Perspective

This management integration appears to be a strategic move to address intense competition and market shifts within Japan’s domestic consumer electronics retail industry. The creation of a retail entity with approximately ¥2.5 trillion in sales could represent a significant step in industry restructuring, with anticipated synergy effects from joint procurement and mutual utilization of customer bases. The focus on expanding “lifestyle”-centric business areas and strengthening the renovation business may suggest both companies’ intent to establish revenue streams beyond traditional appliance sales.

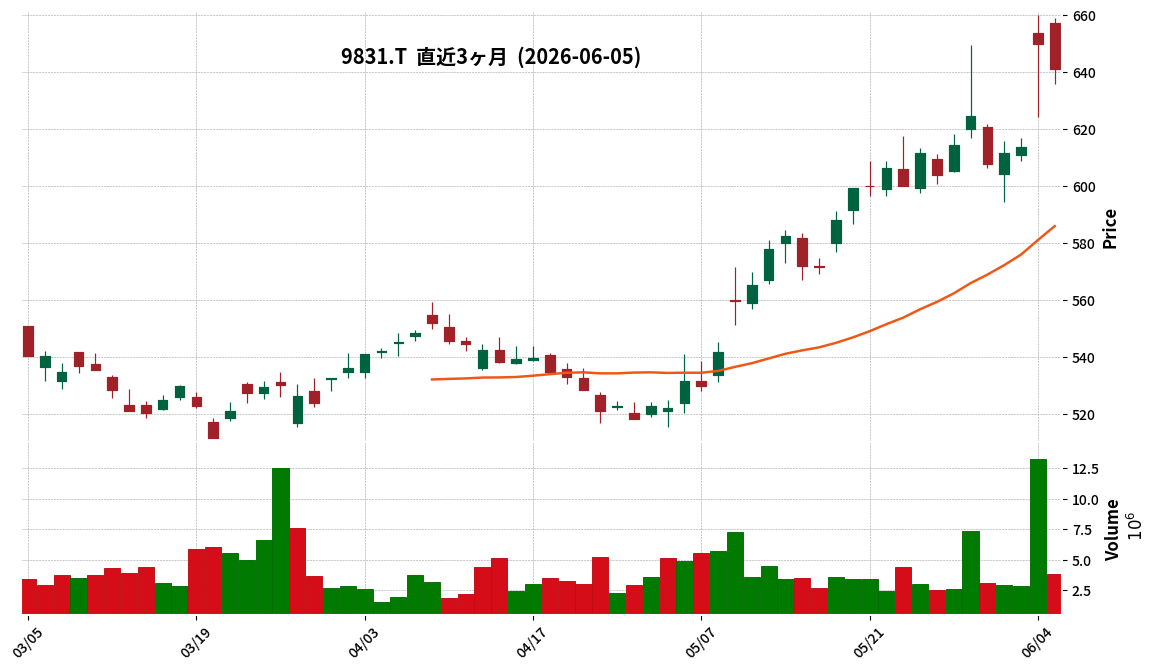

9831|ヤマダHD

641.0

▼ -1.38%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Yamada Holdings Co., Ltd. and Edion Corporation signed a basic agreement today (June 5, 2026) for a management integration under a holding company structure.

- The integration will primarily involve establishing a new holding company through a joint share transfer, making both companies wholly-owned subsidiaries of the new entity.

- The new holding company plans to apply for a new listing (technical listing) on the Tokyo Stock Exchange Prime Market. Both Yamada Holdings and Edion are expected to be delisted.

- The effective date for the management integration and the listing of the holding company’s shares is scheduled for October 1, 2027.

- If realized, the combined sales of both companies (Yamada HD ¥1,691.8 billion, Edion ¥793.7 billion for FY2026/3) would create a retail entity with a scale of approximately ¥2.5 trillion.

🤖 AI Perspective

This basic agreement between two major Japanese home electronics retailers marks a significant step in industry consolidation. The creation of a retail entity with approximately ¥2.5 trillion in sales could lead to substantial scale merits in procurement and opportunities for new business development leveraging their combined customer bases. Investors will likely be monitoring the progress of detailed discussions towards the final integration agreement.

5902|ホッカンHD

2281.0

▲ +1.97%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 2026, consolidated net sales were ¥90.5 billion (down 2.0% year-on-year), and operating profit was ¥3.7 billion (down 16.5% year-on-year).

- Net profit attributable to owners of parent was ¥3.2 billion (up 0.5% year-on-year).

- By segment, the container business reported sales of ¥31.7 billion (up 1.2% year-on-year) and operating profit of ¥1.6 billion (up 53.7% year-on-year). The filling business reported sales of ¥39.7 billion (up 0.9% year-on-year) and operating profit of ¥3.8 billion (up 8.3% year-on-year).

- The overseas business reported sales of ¥15.3 billion (down 14.5% year-on-year) and operating profit of ¥0 billion (down 98.0% year-on-year). This was impacted by reduced orders due to the slowdown in the Indonesian economy.

- Key initiatives under the medium-term management plan “VENTURE-5” included the expansion of a preform production line at Hokkai Can Co., Ltd. (operations started January 2026) and the introduction of cup molding and printing equipment at Hokkan Delta Pack Industri (operations started February 2026).

🤖 AI Perspective

Hokkan Holdings’ FY2026/3 results show a contrast between declining consolidated sales and operating profit and growth in its domestic container and filling segments. The significant decline in overseas business performance, primarily due to the Indonesian economic slowdown, appears to be the main factor pulling down overall results. This highlights the substantial impact of economic conditions in Indonesia on the company’s international operations, suggesting that future developments in its overseas business strategy will be a key area for investors to monitor.

6292|カワタ

811.0

▲ +0.12%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kawata Co., Ltd. has released its consolidated financial results presentation for the fiscal year ended March 2026.

- Net sales for FY2026/3 were ¥19,367 million, exceeding the revised plan (¥19,200 million) by 0.9% and the initial plan (¥18,600 million) by 4.1%. This represents a 6.7% decrease compared to the previous fiscal year.

- Operating profit was ¥447 million, falling 17.0% below the revised plan (¥540 million) but exceeding the initial plan (¥420 million) by 6.7%. This is a 54.5% decrease year-on-year.

- Net profit for the period was ¥36 million, a significant decrease of 38.4% compared to the revised plan (¥60 million) and 80.5% compared to the initial plan (¥190 million). This marks a 93.6% decrease from the previous fiscal year.

- Key factors contributing to the substantial decline in net profit include the recognition of ¥151 million in structural reform costs at a Chinese subsidiary as extraordinary losses, and an increase in corporate taxes due to differences in intra-group profit and loss composition.

- By segment, the East Asia segment posted a substantial operating loss due to the slowdown in the Chinese economy, while the Japan segment, despite reduced sales, drove overall group profit through cost reduction efforts.

- Ordinary profit was ¥572 million, down 4.5% from the revised plan, benefiting from foreign exchange gains of ¥85 million due to the weakening yen (the plan had projected a foreign exchange loss of ¥31 million).

🤖 AI Perspective

Kawata’s FY2026/3 results show that while net sales surpassed the revised plan, net profit experienced a significant decline. The structural reform costs incurred by its Chinese subsidiary appear to have substantially impacted the final profit. Conversely, foreign exchange gains contributed to ordinary profit, highlighting the significant influence of currency fluctuations on performance. The future trajectory of the Chinese market and the effectiveness of the structural reforms will likely be crucial elements for the company’s business recovery.

7279|ハイレックス

2364.0

▲ +0.60%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hi-Lex Corporation announced its consolidated financial results for the second quarter (interim) of the fiscal year ending October 2026.

- For the interim period, net sales were ¥209,107 million (up 37.3% year-on-year), and operating income was ¥2,226 million (down 5.0% year-on-year).

- Net income attributable to owners of parent reached ¥34,857 million (compared to ¥1,779 million in the prior interim period). This was primarily due to the recognition of a gain on negative goodwill of ¥28,305 million and a gain on sales of investment securities of ¥8,315 million as extraordinary income.

- Interim net income per share for the second quarter of FY2026 was ¥942.98.

- From the current fiscal period, Hi-Lex ACT Co., Ltd. and its ten subsidiaries have been included in the scope of consolidation, which impacted net sales by approximately ¥52.2 billion and operating income by approximately ¥0.8 billion.

- The full-year consolidated performance forecast for FY2026 remains unchanged, projecting net sales of ¥401,000 million (up 31.9% year-on-year), operating income of ¥5,400 million (up 59.2% year-on-year), and net income attributable to owners of parent of ¥36,850 million (up 337.7% year-on-year).

🤖 AI Perspective

Hi-Lex’s Q2 FY2026 results show a significant increase in net sales but a decrease in operating income. However, the substantial rise in net income attributable to owners of parent was driven by extraordinary gains from negative goodwill and the sale of investment securities. This suggests that the company’s M&A strategy and asset management had a notable positive impact on its bottom line during this period.

9244|G-デジタリフト

1050.0

▲ +0.00%

📎 Source:G-デジタリフト Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Digitalift published a Q&A summary regarding its Q2 FY2026 financial results on June 5, 2026.

- Sales progress for Q2 FY2026 was 40% of the full-year forecast, on par with the previous year, and is stated to be in line with internal plans. The annual budget is weighted towards the second half, particularly Q4.

- Operating profit significantly increased from ¥4 million in the same period last year to approximately ¥120 million. This was attributed to a substantial increase in gross profit for Digitalift Co., Ltd. and its subsidiaries, as well as an improvement in group-wide profitability resulting from a strategic review of the business portfolio towards higher-profit areas.

- The company stated its intention to continue the shareholder benefit program in the future.

- Regarding the integrated BI tool “LIFT Engine,” the company explained that it aims to optimize operational costs through significant reduction of man-hours, establish a highly reproducible operational structure, and improve profitability and proposal sophistication through AI-driven process improvements.

🤖 AI Perspective

The company’s explanation that its Q2 sales progress is in line with the previous year’s and that the sales budget is concentrated in the second half, especially Q4, suggests that the future performance trajectory will be an important point to monitor. The significant increase in operating profit indicates that the strategic shift towards a higher-profit business portfolio has been effective, potentially highlighting the validity of their management strategy. The introduction of the integrated BI tool “LIFT Engine” could contribute to future operational efficiency and enhanced value proposition, making it worthwhile to continuously gather information on how its impact on performance materializes.

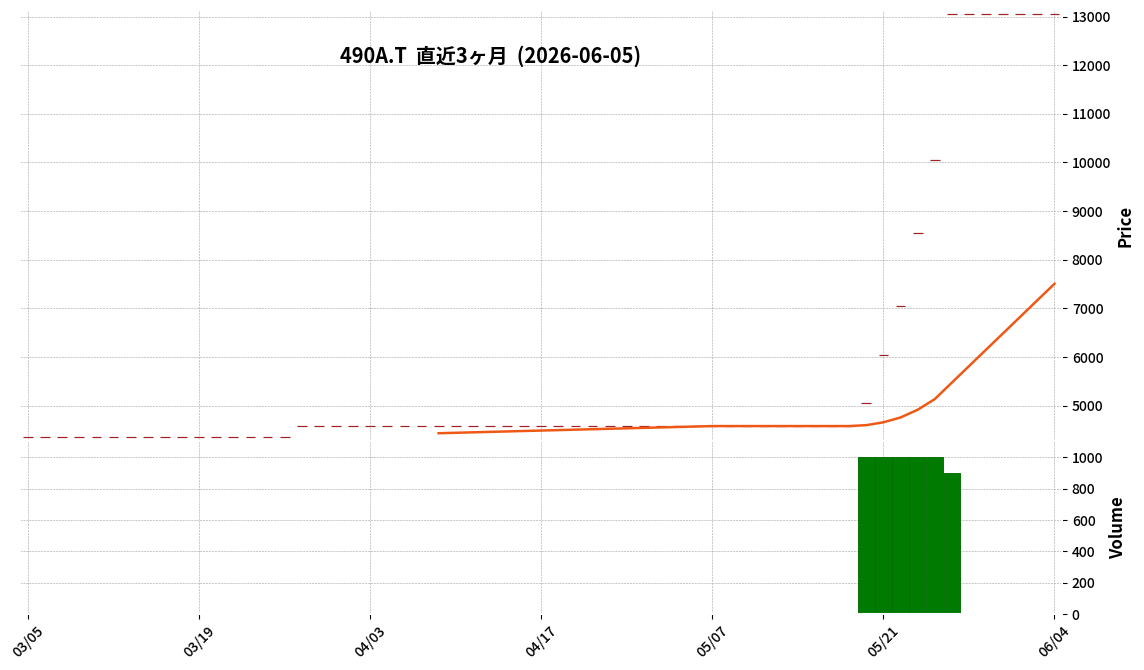

490A|P-センス・トラスト

13050.0

▲ +0.00%

📎 Source:P-センス・トラスト Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- On June 5, 2026, P-Sense-Trust announced a re-amendment to its non-consolidated financial results for the fiscal year ended March 2026.

- The reason for the amendment was the discovery of errors in the financial statements and main notes included in the earnings report published on May 15, 2026.

- Revisions were made to the “Liabilities section” of the balance sheet.

- For the current fiscal year (March 31, 2026), “Long-term borrowings due within one year” changed from 2,379,562 thousand yen (pre-amendment) to 5,893,266 thousand yen (post-amendment).

- Consequently, “Total current liabilities” for the current fiscal year changed from 17,577,863 thousand yen (pre-amendment) to 21,091,567 thousand yen, and “Long-term borrowings” changed from 8,182,072 thousand yen (pre-amendment) to 4,668,368 thousand yen.

- The “Total liabilities” and “Total liabilities and net assets” amounts remained unchanged after the amendment.

🤖 AI Perspective

This re-amendment introduces significant changes to the breakdown of liabilities on the balance sheet, particularly the reclassification of long-term debt to current liabilities, which could impact liquidity ratios. Ensuring the accuracy of financial information is crucial for investors, and this amendment will likely prompt a re-evaluation of the company’s financial position.

1914|日基礎

678.0

▲ +3.51%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nihon Kiso Gijutsu Co., Ltd. announced a correction to a portion of its consolidated financial results for the fiscal year ending March 2026.

- The correction pertains to the content of the “FY2026 March Earnings Report [Japanese GAAP] (Consolidated)” initially disclosed on May 14, 2026.

- The reason for the correction is stated as the discovery of errors in part of the disclosed content after the initial publication.

- The correction specifically impacts the information regarding sales to major customers.

- Sales to Bechtel Energy, Inc. were revised from the original 3,710,420 thousand yen.

- The corrected sales figure for Bechtel Energy, Inc. is 4,183,022 thousand yen.

- The related segment remains “Construction Works.”

🤖 AI Perspective

This correction indicates an upward revision of approximately 470 million yen in sales attributed to a key customer, Bechtel Energy, Inc. For investors, this ensures that the reported financial figures in the earnings report are accurate and updated. Such revisions are typically made to uphold the integrity and reliability of a company’s financial disclosures.

7265|エイケン工業

3715.0

▼ -3.13%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Eiken Kogyo announced its non-consolidated financial results for the second quarter of the fiscal year ending October 2026 (interim period: November 1, 2025 – April 30, 2026).

- Net sales amounted to ¥3,889 million, representing a 4.4% decrease compared to the same period of the previous year.

- Operating profit was ¥102 million, a 58.9% decrease year-on-year.

- Ordinary profit stood at ¥115 million, down 57.7% from the prior interim period.

- Net income for the interim period was ¥97 million, a 50.6% decrease year-on-year.

- Earnings per share for the interim period were ¥94.83.

- The full-year forecast for the fiscal year ending October 2026 remains unchanged: net sales of ¥8,351 million (up 3.1% YoY), operating profit of ¥408 million (down 0.7% YoY), ordinary profit of ¥431 million (down 4.7% YoY), and net income of ¥301 million (down 7.7% YoY).

- The interim dividend forecast is ¥0.00, and the year-end dividend forecast is ¥110.00, for a total annual dividend forecast of ¥110.00, with no revision from the latest forecast.

🤖 AI Perspective

Eiken Kogyo’s Q2 FY2026 results showed declines across net sales and all profit metrics compared to the prior interim period. The significant reduction in operating and ordinary profits, exceeding 50%, may draw investor attention. While the full-year forecast remains unchanged, the gap between the interim results and the annual forecast could be a point of focus moving forward.

9478|SE H&I

510.0

▼ -2.11%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SE H&I reported consolidated results for the fiscal year ended March 2026 with net sales of 7,026 million yen (down 3.0% YoY), operating income of 955 million yen (up 16.8% YoY), and net income attributable to owners of parent of 633 million yen (up 19.2% YoY).

- By segment, the investment management business achieved significant increases in both revenue and profit, with sales of 629 million yen (up 170.7% YoY) and segment profit of 522 million yen (up 107.9% YoY).

- The software and network business turned profitable, reporting 45 million yen in segment profit for sales of 787 million yen (up 3.3% YoY), compared to a loss of 10 million yen in the previous period.

- The publishing business saw decreased revenue and profit, the corporate service business experienced revenue decline and reduced segment profit, and the education and human resources business maintained flat revenue but decreased profit.

- For the full consolidated fiscal year ending March 2027, the company forecasts net sales of 6,500 million yen (down 7.5% YoY), operating income of 850 million yen (down 11.0% YoY), and net income attributable to owners of parent of 500 million yen (down 21.1% YoY).

🤖 AI Perspective

SE H&I’s consolidated results for FY2026/3 indicate that while overall group revenue declined, strong performance in the investment management segment and the return to profitability of the software and network business contributed to the increase in profit. The significant boost in the investment management segment’s performance appears to be driven by gains from the sale of some held shares, considering market conditions. However, the struggles in the publishing and corporate service segments, along with the forecast for declining revenue and profit in FY2027/3, suggest that ongoing business restructuring and its progress will be key areas for investors to monitor.

3854|アイル

2509.0

▲ +1.37%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Aile Inc. announced its consolidated financial results for the third quarter of the fiscal year ending July 2026 (August 1, 2025, to April 30, 2026).

- Net sales reached JPY 15.543 billion, marking a 10.2% increase compared to the same period of the previous fiscal year.

- Operating profit was JPY 4.240 billion, an increase of 22.4% year-on-year.

- Ordinary profit stood at JPY 4.268 billion, up 24.7% from the prior year’s period.

- Net income attributable to parent shareholders increased by 24.4% year-on-year to JPY 2.931 billion.

- Diluted earnings per share for the quarter were JPY 117.22.

- The full-year consolidated earnings forecast remains unchanged: net sales of JPY 20.700 billion (up 7.3% YoY), operating profit of JPY 5.500 billion (up 14.1% YoY), ordinary profit of JPY 5.540 billion (up 16.2% YoY), net income attributable to parent shareholders of JPY 4.050 billion (up 16.1% YoY), and basic earnings per share of JPY 161.95.

🤖 AI Perspective

Aile’s Q3 FY2026 results indicate a robust performance, with double-digit growth across sales and all profit metrics compared to the previous year. The improvement in operating profit margin suggests enhanced operational efficiency, which could be a positive sign for investors. With the full-year earnings forecast remaining unchanged, market participants may continue to monitor the company’s performance towards its annual targets.

2353|日駐

241.0

▲ +2.99%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nippon Parking Development Co., Ltd. (Code 2353) announced its consolidated financial results for the third quarter of the fiscal year ending July 2026 (August 1, 2025 – April 30, 2026).

- During the cumulative third quarter, net sales reached ¥31.107 billion (up 9.4% year-on-year), operating profit was ¥7.016 billion (up 5.6%), ordinary profit was ¥7.178 billion (up 8.4%), and net profit attributable to owners of parent was ¥4.208 billion (up 11.6%).

- The company achieved record-high figures for net sales and all profit stages.

- The parking business saw a net increase of 118 new properties (up from 76 in the prior year period), achieving record-high sales and operating profit in both domestic and overseas operations.

- The ski resort business recorded a record-high 543 thousand inbound visitors (up 23.3% year-on-year), also achieving record-high sales.

- The theme park business experienced an increase in amusement park visitors, and the villa/accommodation business expanded with the acquisition of all shares in Izu Kanko Kaihatsu Co., Ltd., leading to record-high sales and operating profit.

- The full-year consolidated earnings forecast remains unchanged, with projected net sales of ¥40.8 billion (up 10.8% year-on-year) and net profit attributable to owners of parent of ¥5.7 billion (up 18.8%).

🤖 AI Perspective

NPD’s Q3 FY2026 results indicate strong performance across its core businesses, including parking, ski resorts, and theme parks, with record-high sales and profits. The company’s strategic focus on acquiring new parking properties, leveraging strong inbound demand in ski resorts, and expanding its theme park and accommodation offerings appears to have driven this growth. With the full-year forecast maintained, investors may monitor the performance in the final quarter to assess the company’s trajectory.

2413|エムスリー

1590.0

▲ +2.91%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- M3, Inc. announced its board of directors’ decision on June 5, 2026, to acquire all outstanding shares of Wiseman Co., Ltd., making it a consolidated subsidiary.

- Wiseman, established in 1983, specializes in one-stop software development, sales, and support for the medical, nursing care, and welfare sectors.

- Wiseman’s net sales for the past three fiscal years (ending June 2023 to June 2025) ranged from 11,354 million yen to 12,377 million yen, with operating losses and net losses reported in the fiscal years ending June 2024 and June 2025.

- The acquisition price was not disclosed, but it was determined based on an valuation report from KPMG FAS, an independent third-party appraisal firm, to ensure fairness.

- The scheduled execution date for the share transfer is July 1, 2026.

🤖 AI Perspective

M3’s acquisition of Wiseman suggests a strategic move to leverage Wiseman’s established customer base and expertise in the nursing care and welfare domains, combining it with M3’s technology to accelerate DX in nursing care and enhance medical-nursing collaboration. Given Wiseman’s reported losses in the past two fiscal years, investors may monitor M3’s future business restructuring and specific initiatives aimed at improving profitability.

3193|エターナルホスピG

2724.0

▲ +1.60%

📎 Source:エターナルホスピG Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the nine months ended April 30, 2026 (Q3 FY2026), consolidated net sales reached ¥38,318,717 thousand, representing a 13.3% increase year-over-year.

- Operating profit for the same period was ¥2,367,053 thousand, marking a 16.9% increase compared to the previous year.

- Ordinary profit grew by 20.5% to ¥2,394,975 thousand, and net profit attributable to parent company shareholders increased by 37.2% to ¥1,532,564 thousand.

- Domestic “Torikizoku” existing directly-managed stores saw a 4.9% increase in customer count, a 4.0% increase in average spending per customer, and a 9.1% increase in sales year-over-year for the cumulative third quarter.

- Eternal Hospitality Japan Co., Ltd. was newly included in the scope of consolidation during this cumulative quarter.

🤖 AI Perspective

Eternal Hospitality Group’s Q3 results demonstrate robust growth across key financial metrics, with double-digit increases in revenue and all profit categories. The strong performance of domestic “Torikizoku” existing stores, driven by both customer traffic and average spending, appears to be a significant factor. Additionally, the acceleration of overseas expansion and the inclusion of a new subsidiary in the consolidated scope could indicate the company’s strategic focus on broadening its operational base.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

3662|エイチームHD

925.0

▲ +0.00%

📎 Source:エイチームHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Ateam Holdings announced its consolidated financial results for the third quarter of the fiscal year ending July 2026 (August 1, 2025, to April 30, 2026).

- Net sales reached ¥17,242 million, marking a 4.0% decrease compared to the same period of the previous year.

- Net profit attributable to owners of parent was ¥343 million, a decrease of 66.1% year-on-year.

- Adjusted EBITDA stood at ¥778 million, down 44.9% from the prior year’s third quarter.

- The decline in performance was attributed to decreased revenue from some existing media in the Digital Marketing business and an overall decrease in game application revenue within the Entertainment business.

- The consolidated full-year forecast for July 2026 remains unchanged, projecting net sales of ¥24,500 million and net profit attributable to owners of parent of ¥600 million.

🤖 AI Perspective

Ateam HD’s Q3 results show a year-on-year decline across key financial metrics, with both net sales and profits decreasing. This performance is primarily attributed to a reduction in revenue from existing operations within both the Digital Marketing and Entertainment segments. The reported increase in common expenses, partly due to a rise in the number of shareholders eligible for shareholder benefits, also impacted the adjusted EBITDA. Investors may want to monitor the company’s strategies to revitalize existing businesses and manage its cost structure in the coming quarters.

3915|テラスカイ

3375.0

▼ -3.16%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Terrasky Co., Ltd. entered into a capital and business alliance agreement with Bridge International Group Co., Ltd. on June 5, 2026.

- Terrasky will acquire 113,100 shares of Bridge International Group’s treasury stock through a third-party allotment for JPY 182,317,200.

- This acquisition will result in Terrasky holding a 3% voting rights stake in Bridge International Group (based on total voting rights as of December 31, 2025).

- The business alliance includes four key initiatives: co-development and provision of “Sales Engagement BPaaS,” establishment of an AI co-creation sales process, process integration support through Revenue Operations (RevOps), and pursuit of a performance-based business model.

- The execution date for the share subscription is scheduled for June 22, 2026.

🤖 AI Perspective

This capital and business alliance appears to aim at accelerating sales support DX by integrating Terrasky’s Salesforce and AI technologies with Bridge International Group’s inside sales outsourcing expertise. The joint development of “Sales Engagement BPaaS,” AI utilization, and the pursuit of performance-based business models could potentially enhance revenue for client companies through synergistic effects between the two firms. This strategic move may indicate a focus on addressing the growing demand for efficient and data-driven sales operations.

4056|G-ニューラル

232.0

▲ +4.50%

📎 Source:G-ニューラル Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Neural Group Co., Ltd. announced a partial correction to its “Q1 FY22026 (9th Fiscal Period) Earnings Presentation Materials” on June 5, 2026.

- The reason for the correction is that, subsequent to the presentation’s release on May 13, 2026, the refinement of ongoing business plans for companies that joined the group during the current fiscal year led to discrepancies between the quarterly performance forecasts and the information stated in the original presentation.

- The specifics of the correction are detailed in a separate attachment, primarily concerning page 5, “2026 Performance Outlook (Consolidated performance including Neural Marketing, Pomato Pro, Cactus, and Mahou).”

- The corrected PDF version of the materials has already been updated and is available on the company’s IR website.

🤖 AI Perspective

This correction suggests that revisions to the business plans of newly consolidated group companies have led to adjustments in the company’s performance outlook. For investors, this highlights the importance of not only monitoring existing operations but also understanding the impact of newly acquired subsidiaries on overall financial performance. The changes in the quarterly performance trajectory could influence future business strategies and profitability, making detailed disclosures a key area of focus.

4263|G-サスメド

638.0

▲ +3.91%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Susmed Co., Ltd. announced on June 5, 2026, the achievement of a development milestone under its sales alliance agreement with Shionogi Pharmaceutical Co., Ltd. for the insomnia treatment app “Susmed Insomnia Disorder App Medcle.”

- This milestone was triggered by the app’s successful inclusion in health insurance coverage at or above a certain point threshold, as stipulated in the agreement.

- The exact amount of the milestone payment and the timing of its revenue recognition are currently under discussion with Shionogi Pharmaceutical and will be disclosed promptly once finalized.

- Sales of the “Susmed Insomnia Disorder App Medcle” commenced on June 1, 2026.

- The original sales alliance agreement with Shionogi Pharmaceutical for an insomnia treatment app was executed on December 27, 2021.

🤖 AI Perspective

The achievement of this milestone signals a significant step forward in the commercialization of Susmed’s insomnia treatment app, “Medcle.” The fact that the milestone was tied to obtaining health insurance coverage at a specific point threshold may suggest the product’s value proposition is being recognized within the healthcare system. Investors may find it worthwhile to monitor the upcoming announcement regarding the milestone payment amount and its impact on Susmed’s revenue recognition.

436A|G-サイバーSOL

1084.0

▲ +3.24%

📎 Source:G-サイバーSOL Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Cyber SOL announced its non-consolidated financial results for the fiscal year ended April 2026 (May 1, 2025 to April 30, 2026), having transitioned to a non-consolidated basis in the fiscal year ended April 2025 due to a partial transfer of shares in Internet Secure Services Corporation.

- For the fiscal year ended April 2026, revenue was ¥3,525 million (up 12.8% year-on-year), operating profit was ¥1,500 million (up 21.7% year-on-year), profit before tax was ¥1,498 million (up 23.1% year-on-year), and profit for the period was ¥1,083 million (up 20.0% year-on-year).

- Basic earnings per share for the period stood at ¥70.32.

- The annual dividend for the fiscal year ended April 2026 was announced as ¥16.00 for the year-end dividend, totaling ¥32.00 (total dividends of ¥505 million).

- For the fiscal year ending April 2027, the company forecasts revenue of ¥4,000 million (up 13.5% year-on-year), operating profit of ¥1,800 million (up 20.0% year-on-year), and profit for the period of ¥1,200 million (up 10.8% year-on-year).

🤖 AI Perspective

G-Cyber SOL’s fiscal year 2026 results show double-digit growth across revenue and profit categories, which may suggest a strong operational performance. The substantial increase in the dividend payment, coupled with a forecast for continued revenue and profit growth in the next fiscal year, could indicate confidence in the company’s business trajectory and a commitment to shareholder returns. The shift to non-consolidated reporting and the classification of Internet Secure Services as a discontinued operation are important considerations when evaluating the year-on-year comparisons.

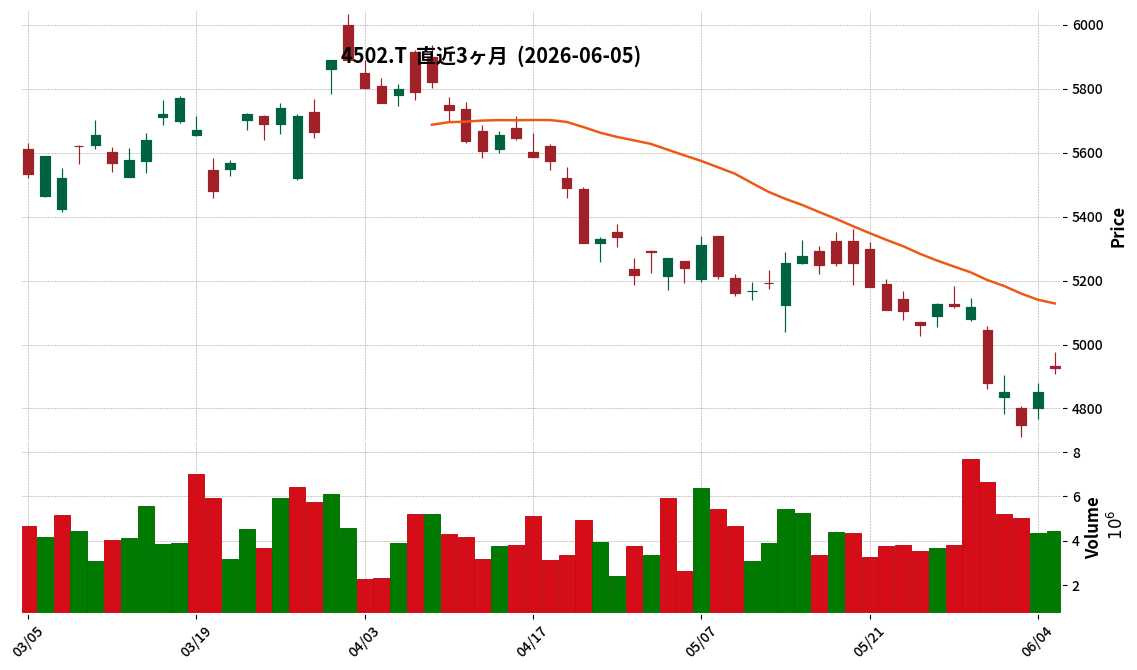

4502|武田薬

4926.0

▲ +1.57%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Takeda Pharmaceutical Co. announced amendments to its full-year financial results for the fiscal year ended March 2026, originally published on May 13, 2026, to reflect the impact of a subsequent event.

- The subsequent event is related to a jury verdict received on May 18, 2026 (U.S. Eastern Time) in the U.S. District Court for the District of Massachusetts concerning the AMITIZA® (lubiprostone) antitrust litigation.

- An additional litigation provision of JPY 402.5 billion was recognized in the consolidated financial statements for FY2025 (fiscal year ended March 2026), along with a related tax benefit of JPY 58.4 billion.

- This amendment does not impact the company’s Core results for FY2025, the year-end dividend for FY2025 (JPY 100 per share), the FY2026 (fiscal year ending March 2027) full-year forecast, management guidance, or the FY2026 annual dividend forecast (JPY 204 per share).

- Takeda plans to file post-verdict motions and an appeal, and intends to seek a stay of execution of the judgment pending appeal.

🤖 AI Perspective

Takeda has reported a significant litigation provision in its FY2026/3 financial results due to the AMITIZA® antitrust lawsuit verdict. While this is a substantial charge, the announcement specifies that Core results, future forecasts, and dividend plans remain unchanged, which may offer some reassurance to investors. The company’s intent to appeal and seek a stay of execution suggests the financial impact is not yet final, making the ongoing legal process a key area for investors to monitor.

6040|G-日本スキー

465.0

▲ +0.87%

📎 Source:G-日本スキー Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Nippon Ski announced its consolidated financial results for the third quarter of the fiscal year ending July 2026 (August 1, 2025, to April 30, 2026).

- Net sales reached ¥9,977 million, marking an 8.9% increase compared to the same period of the previous year.

- Operating profit decreased by 4.5% year-on-year to ¥2,719 million, and ordinary profit decreased by 3.7% to ¥2,735 million.

- Net income attributable to owners of parent increased by 16.6% year-on-year to ¥2,228 million.

- The increase in net income attributable to owners of parent was primarily due to the recording of extraordinary gains from the completed sale of land at Iwatake Resort base.

- Basic earnings per share for the quarter were ¥48.45.

- The full-year consolidated forecast projects net sales of ¥11,480 million (up 9.7% YoY), operating profit of ¥2,300 million (up 2.4% YoY), ordinary profit of ¥2,260 million (up 0.6% YoY), and net income attributable to owners of parent of ¥2,470 million (up 55.7% YoY).

- The full-year forecast for net income attributable to owners of parent is expected to exceed ordinary profit due to the recognition of extraordinary gains from the land sale at Iwatake Resort.

- The dividend forecast for the fiscal year ending July 2026 is ¥1.50 at year-end, totaling ¥3.50 annually.

🤖 AI Perspective

The reported results show an increase in net sales but a decrease in operating and ordinary profits, while net income attributable to owners of parent significantly rose due to an extraordinary gain from a land sale. This suggests a mixed performance where core business profitability might be distinct from the overall net income. Investors may want to analyze the impact of this one-time gain on the company’s financial health and future earnings sustainability. The full-year forecast, which incorporates this gain, indicates strong growth in net income attributable to owners of parent, making it important to monitor how the company’s operational performance evolves going forward.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

6045|G-レントラックス

1391.0

▲ +0.36%

📎 Source:G-レントラックス Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Rentracks disclosed the financial results of its unlisted parent company, Team Kaneko Co., Ltd., for the fiscal year ended March 2026.

- As of March 31, 2026, Team Kaneko Co., Ltd. reported total assets of ¥1,773,440 thousand and net assets of ¥1,712,937 thousand.

- For the period from April 1, 2025, to March 31, 2026, the company recorded no sales revenue and an operating loss of ¥2,407 thousand.

- Non-operating income totaled ¥144,430 thousand, including ¥137,213 thousand in dividends received, resulting in a net income of ¥140,990 thousand for the period.

- The parent company’s voting rights are 100% held by Mr. Eiji Kaneko, who is also the sole major shareholder (3,900,100 shares, 100.00% of outstanding shares).

🤖 AI Perspective

The disclosure of an unlisted parent company’s financial results provides investors with additional insight into the broader group’s financial health and stability. Team Kaneko Co., Ltd.’s net income was primarily driven by non-operating income, particularly dividends received, which suggests a focus on investment activities rather than core business operations for the parent entity. Understanding the financial standing of the parent company could be relevant for evaluating potential impacts on the consolidated operations of G-Rentracks.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

6046|リンクバル

114.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Linkbal Inc. released its Q&A session regarding the second quarter financial results for the fiscal year ending September 2026 on June 5, 2026.

- The company is considering expanding aquarium-themed events and planning new large-scale events as part of its growth strategy.

- Its AI engine is built on millions of “Linkbal IDs” with accumulated big data, aiming to enhance the quality of matching.

- The AI solution business is expanding revenue opportunities through external offerings such as AI consulting and contract development.

- The company’s performance exhibits a seasonality with stronger sales in the second half of the fiscal year.

🤖 AI Perspective

The Q&A document from Linkbal indicates that the expansion of the matching event business and the growth of the AI solution business are central to its future strategy. The utilization of the AI engine appears to offer potential not only for enhancing existing services but also for generating new revenue streams through external provision. Given the seasonal nature of the company’s performance, with stronger results in the second half, the impact of future large-scale events on earnings will be a noteworthy point for investors to monitor.

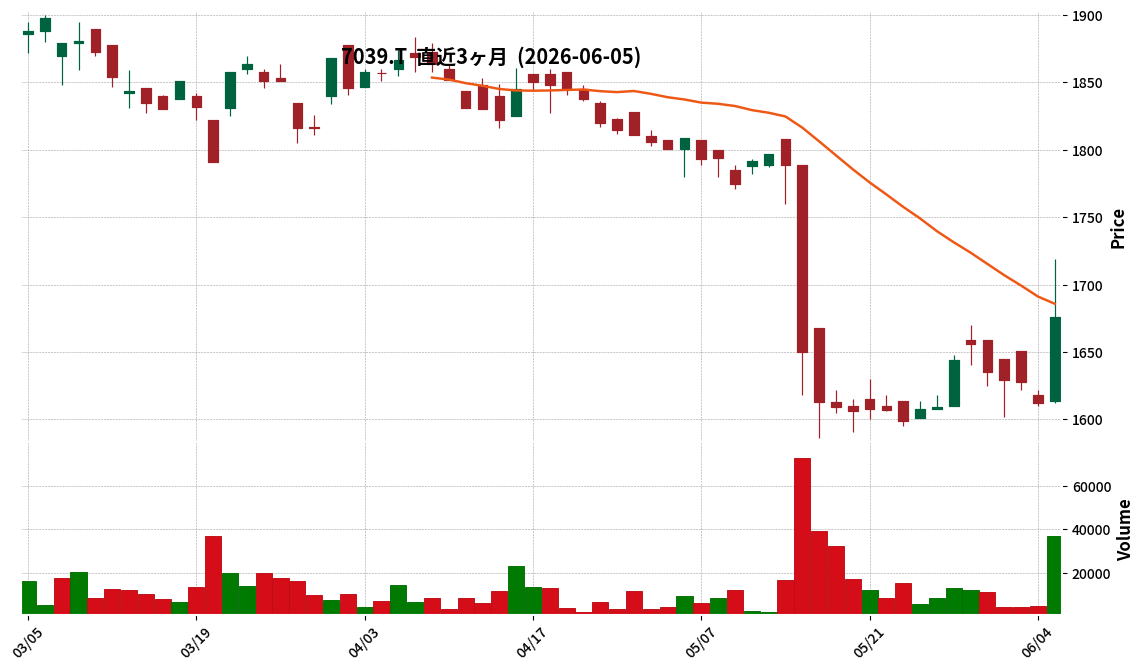

7039|G-ブリッジグループ

1676.0

▲ +3.97%

📎 Source:G-ブリッジグループ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Bridge Group resolved at its Board of Directors meeting on June 5, 2026, to enter into a capital and business alliance agreement with Terrasky Corporation.

- The alliance aims for joint development and provision of “Sales Engagement BPaaS,” establishment of AI co-creation sales processes, integrated process support through Revenue Operations (RevOps), and pursuit of performance-linked business models.

- As part of the capital alliance, G-Bridge Group will dispose of 113,100 treasury shares to Terrasky through a third-party allotment.

- The payment per share is JPY 1,612, totaling JPY 182,317,200 (approx. JPY 182 million).

- Terrasky’s voting rights ratio in G-Bridge Group is expected to be 3.16% after this disposal of treasury shares. The raised funds will be allocated to long-term working capital and growth strategy investments.

🤖 AI Perspective

This capital and business alliance appears to aim at creating new sales support services by combining G-Bridge Group’s inside sales expertise with Terrasky’s sales tech and AI capabilities. The pursuit of a performance-linked business model, in particular, suggests potential shifts in future revenue structures. The third-party allotment of treasury shares could be interpreted as a strategic move prioritizing the strengthening of the relationship with Terrasky, rather than solely focusing on fundraising.

7694|G-いつも

429.0

▼ -4.88%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- The full-year performance forecast for the fiscal year ending March 2027 does not include any sales or profits from new brand projects that are not yet confirmed.

- The ¥15.4 billion plan for the Collaborative Brand Partner business in FY2027/3 is based on natural growth of existing brands and sales from multiple brands newly contracted in the previous period and fully operational in the current period.

- The company reorganized several subsidiaries, including BAAAN, starting from the previous fiscal year.

- Drastic structural reforms in key subsidiaries (especially Beelun) resulted in an annual SG&A reduction of tens of millions of yen as of the start of FY2027/3.

- In FY2026/3, the company achieved a 31% increase in gross profit while reducing the total number of employees across the group by approximately 11%.

- The company will sequentially begin implementing its proprietary “AI Agent” for major marketplaces (Amazon, Rakuten, TikTok, etc.) from FY2027/3.

- Inventory in the Collaborative Brand Partner business is managed under a low-risk, high-turnover system by carefully selecting highly recognized major and famous brands and utilizing iDM and AI-driven demand forecasting.

🤖 AI Perspective

This IR disclosure from G-itsumo primarily addresses investor questions, providing specific information on future business strategies and financial health. The emphasis on a conservative FY2027/3 performance forecast excluding unconfirmed projects, cost reductions through subsidiary reforms, and productivity enhancements via AI implementation suggests the company’s clear focus on improving profitability and efficiency. The simultaneous achievement of reduced employee count and increased gross profit could indicate progress in its transition towards becoming a technology-driven enterprise.

8253|クレセゾン

4140.0

▲ +2.35%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Credit Saison Co., Ltd. announced a correction to a portion of its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 [IFRS] (Consolidated)” originally disclosed on May 15, 2026.

- The reason for the correction was an error identified in the aggregation of assets and liabilities held for sale in connection with a company split of a subsidiary.

- The correction revised the consolidated operating results for FY2026/3, with pre-tax profit adjusted from ¥91,190 million to ¥89,980 million (period-on-period change from △1.7% to △3.0%).

- Profit attributable to owners of the parent was revised from ¥62,751 million to ¥61,728 million (period-on-period change from △5.5% to △7.0%).

- In the consolidated financial position, total assets were adjusted from ¥4,953,204 million to ¥4,952,181 million, and equity attributable to owners of the parent from ¥761,657 million to ¥760,634 million.

- Regarding consolidated cash flows, cash flows from operating activities were revised from △¥137,657 million to △¥135,671 million, and cash flows from investing activities from △¥25,970 million to △¥26,925 million.

🤖 AI Perspective

This correction by Credit Saison is attributed to an accounting error related to a subsidiary’s company split, specifically an aggregation mistake concerning assets and liabilities held for sale. While pre-tax profit and profit attributable to owners of the parent have been revised downwards, the absence of changes to net revenue and operating profit suggests that the impact on core profitability may be limited. However, with revisions also affecting the balance sheet and cash flow statement, investors monitoring financial health and liquidity metrics may find these adjusted figures noteworthy.

8439|東京センチュリー

2393.5

▲ +1.61%

📎 Source:東京センチュリー Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tokyo Century Corporation announced a partial correction to its “FY2026/3 IR Materials” originally published on May 19, 2026.

- The correction applies only to the IR materials and does not impact previously announced financial statements or earnings reports.

- The reason for the correction was the discovery of an error in a portion of the disclosed content.

- Of the “return of tax expenses from aircraft business (JPY 10.8 billion)” previously stated as a factor for increased net income in FY2025, JPY 8.3 billion was reclassified to “profit accumulation from each business segment.”

- Consequently, net income excluding one-off factors (core profitability) increased by JPY 8.3 billion.

- Corresponding adjustments have also been made to the profit plan for FY2026, including factors affecting increases and decreases.

- The corrections are located on pages 4, 6, 7, 9, 10, and 23 of the IR materials.

🤖 AI Perspective

This correction to the IR materials impacts the composition of profits for both the FY2205 results and the FY2026 profit plan. The reclassification, specifically the JPY 8.3 billion increase in “net income excluding one-off factors (core profitability),” may be noteworthy for assessing the company’s underlying earning power. Investors may wish to review the revised IR materials to understand the implications of these changes on future performance outlooks and business portfolio evaluations.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

9505|北陸電力

820.6

▲ +2.61%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hokuriku Electric Power Co. announced an amendment to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 (Japanese GAAP),” originally disclosed on April 28, 2026.

- The reason for the amendment was the discovery of errors in the stated wholesale electricity sales volume.

- The wholesale electricity sales volume for the consolidated accounting period was corrected from 8,364 million kWh to 8,381 million kWh.

- Consequently, the total electricity sales volume for the period was revised from 33,140 million kWh (3.8% increase year-on-year) to 33,157 million kWh (3.9% increase year-on-year).

- The full-year forecast for total electricity sales volume (forecast) for the fiscal year ending March 2026 was also amended from “approximately 94% of previous fiscal year” to “approximately 93% of previous fiscal year.”

🤖 AI Perspective

This amendment primarily concerns a correction in electricity sales volumes, specifically stemming from an error in wholesale sales figures. While the historical and projected sales volumes have been revised, other key assumptions for the outlook, such as exchange rates and CIF prices for crude oil, coal, and LNG, remain unchanged. Investors may want to assess the materiality of these numerical corrections on the company’s overall operational performance and future guidance.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

9678|カナモト

5140.0

▲ +1.18%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- KANAMOTO announced on June 5, 2026, a resolution by its Board of Directors to issue an interim dividend based on the record date of April 30, 2026.

- The interim dividend per share has been increased by ¥5 from the previous forecast (announced December 5, 2025) of ¥50.00 to ¥55.00.

- The total dividend amount is ¥1,888 million, with an effective date of July 2, 2026.

- The year-end dividend forecast for the October 2026 fiscal year has also been revised, increasing by ¥5 from the previous forecast of ¥50.00 to ¥55.00 per share.

- The full-year dividend forecast is now ¥110.00 per share, an increase of ¥10 from the previous forecast of ¥100.00.

🤖 AI Perspective

This dividend increase is attributed to the upward revision of the consolidated earnings forecast for the second quarter (interim period) of the October 2026 fiscal year, reflecting the company’s commitment to shareholder returns. The company’s stated goal of progressive dividends suggests a strategy to provide stable returns while adding further distributions based on performance.

6999|KOA

2866.0

▲ +1.16%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- KOA Corporation announced corrections to its “FY2026 March Earnings Report (Consolidated) [Japanese GAAP],” “FY2026 March Supplemental Materials,” and “FY2026 March Earnings Presentation Materials” on June 5, 2026, which were originally disclosed on April 24 and April 27, 2026.

- The reason for the corrections was the discovery of errors in parts of the consolidated cash flow statement, capital expenditures, and depreciation expenses.

- For FY2026 March, the corrected consolidated cash flow shows operating activities cash flow revised from ¥8,849 million to ¥9,069 million, and investing activities cash flow revised from △¥6,841 million to △¥7,061 million.

- The cash and cash equivalents at the end of the period remain unchanged at ¥27,410 million after the correction.

- Capital expenditures for FY2025 were revised from ¥5.9 billion to ¥6.0 billion, and depreciation expenses from ¥7.0 billion to ¥7.1 billion.

🤖 AI Perspective

These corrections primarily involve numerical adjustments within the consolidated cash flow statement and related financial documents, specifically impacting operating and investing cash flows. The unchanged year-end cash and cash equivalents suggest that the overall liquidity position of the company is not significantly altered. Investors may want to consider the implications of these revisions on the company’s operational transparency and the accuracy of future financial disclosures.

3733|ソフトウェアS

11560.0

▲ +4.71%

📎 Source:ソフトウェアS Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Software Service Co., Ltd. announced its consolidated financial results for the second quarter (interim period) of the fiscal year ending October 2026.

- During this interim period, net sales reached ¥24,334 million, marking a 20.8% increase compared to the previous interim period.

- Operating profit was ¥4,180 million (down 2.2% year-on-year), ordinary profit was ¥4,223 million (down 1.6% year-on-year), and net income attributable to owners of parent was ¥2,752 million (down 7.7% year-on-year).

- Total assets stood at ¥50,715 million, net assets at ¥40,396 million, and the equity ratio was 79.7%.

- The full-year dividend forecast for the fiscal year ending October 2026 remains unchanged at ¥170.00 per share.

- The consolidated full-year earnings forecast for FY2026 also remains unrevised, projecting net sales of ¥44,338 million (up 4.8% year-on-year), operating profit of ¥8,795 million (up 4.8% year-on-year), ordinary profit of ¥8,875 million (up 4.8% year-on-year), and net income attributable to owners of parent of ¥5,982 million (down 2.1% year-on-year).

- A special loss of ¥240 million was recorded in the interim period due to demolition costs associated with the rebuilding of the company dormitory in Osaka.

🤖 AI Perspective

Software Service’s interim results show a solid increase in net sales, but profitability declined due to rising procurement costs, a higher proportion of hardware sales, and the recording of a special loss. The unchanged full-year earnings forecast suggests the company anticipates profit recovery in the second half. The ongoing push for medical DX and related market conditions could influence future performance.

2160|G-GNI

2833.0

▲ +5.55%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- GNI Group resolved on June 5, 2026, to acquire all shares of Ayumi Pharmaceutical Holdings Co., Ltd. (Ayumi Pharma HD), making it a wholly-owned subsidiary.

- A third-party allotment of new shares will be issued to Ayumi Pharma HD’s shareholders: BCP Asia AYM Holding (Cayman) L.P., Toho Holdings Co., Ltd., and Hisamitsu Pharmaceutical Co., Inc.

- Ayumi Pharma HD possesses a strong product portfolio including the antipyretic analgesic “Calonal” and other products in the orthopedic and rheumatism fields, reporting consolidated net revenue of JPY 38,543 million and operating profit of JPY 6,206 million for the fiscal year ended March 2026.

- Following the acquisition, Ayumi Pharmaceutical Co., Ltd., a wholly-owned subsidiary of Ayumi Pharma HD, will become a sub-subsidiary of GNI Group.

- GNI Group’s objective for this acquisition is to secure Ayumi Pharma HD’s commercial platform in the Japanese market, aiming for revenue diversification and stabilization.

🤖 AI Perspective

This announcement suggests GNI Group’s strategic move to establish a robust revenue base in Japan by integrating Ayumi Pharmaceutical Holdings, a company with a strong domestic sales network. This acquisition could potentially serve as a gateway for GNI to introduce its global pipeline into the Japanese market. Investors may focus on the potential for synergy creation and the evolution of the business portfolio. The third-party share issuance is also an important element of the funding plan for this acquisition.

4436|G-ミンカブ

455.0

▲ +3.17%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Minkabu The Infonoid Co., Ltd. announced on June 5, 2026, a partial correction to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 [Japanese GAAP]”.

- The reason for the correction is that an error was discovered in a part of the Consolidated Statement of Comprehensive Income after the submission of the financial results announced on May 15, 2026.

- The corrections are located in the “Summary Information (1) Consolidated Operating Results” and on page 9 of the accompanying materials under “3. Consolidated Financial Statements and Primary Notes (2) Consolidated Statements of Income and Comprehensive Income”.

- Corrected numerical data (XBRL data) will also be submitted.

🤖 AI Perspective

This correction indicates a revision to some of the previously disclosed figures in the consolidated financial results. Investors may want to carefully review which specific items in the Consolidated Statement of Comprehensive Income are affected and how these changes might impact the interpretation of past financial performance. Such corrections, while not uncommon, can influence investor confidence in financial reporting accuracy, making it prudent to understand the detailed implications of these revisions.

4493|G-サイバーセキュリ

1771.0

▲ +1.14%

📎 Source:G-サイバーセキュリ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Cybersecurity Cloud Inc. announced on June 5, 2026, a correction to a portion of its “Q1 FY2026 Financial Results Presentation” initially released on May 15, 2026.

- The reason for the correction was stated as the need to amend certain descriptive content.

- The correction pertains to the “ARR Trend” section on page 6 of the original document.

- The “2026 Q1 CloudFastener Year-on-Year growth” was revised from +11.6% to +120.6%.

- The “2026 Q1 webtru Year-on-Year growth” was revised from +5.2% to +25.1%.

🤖 AI Perspective

The announced corrections significantly revise the year-on-year growth rates for key services, CloudFastener and webtru ARR (Annual Recurring Revenue), potentially altering the perceived business performance. The substantial upward adjustment, particularly CloudFastener’s growth rate increasing more than tenfold, could be a focal point for investors. It suggests a more robust performance in these segments than initially reported, which may influence market perception of the company’s operational strength.

6562|G-ジーニー

959.0

▲ +7.27%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Genie announced on June 5, 2026, that its Board of Directors resolved to enter into an investment agreement with dip Corporation and to dispose of treasury shares through a third-party allocation to dip.

- The third-party allocation involves the disposition of 902,820 shares of common stock to dip (5.00% of outstanding common shares), resulting in dip’s voting rights ratio in G-Genie becoming 6.78%.

- Based on dip’s recommendation, Shingo Fujiwara has been nominated as a new director candidate, with the proposal to be submitted at the 16th Ordinary General Meeting of Shareholders scheduled for June 30, 2026.

- A change in the controlling shareholder (other than the parent company) is anticipated as a result of this treasury share disposition.

- The disposition price per share is 972 yen, generating total proceeds of 877,541,040 yen (net estimated proceeds of 874,091,040 yen). These funds are earmarked for joint development costs utilizing next-generation AI and promoting business collaboration.

🤖 AI Perspective

This capital and business alliance appears to aim for enhanced corporate value and business expansion for both G-Genie and dip by deepening their collaboration in marketing DX support products and HR/DX services. The nomination of a director from dip and agreements on share transfer restrictions could indicate an intention to build a strong, long-term cooperative relationship and strengthen governance. The allocation of funds towards joint development using next-generation AI suggests a strategic investment for future growth.

8917|ファースト住建

1033.0

▲ +1.97%

📎 Source:ファースト住建 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- First Juken Co., Ltd. announced its consolidated financial results for the second quarter of the fiscal year ending October 2026.

- Net sales for the period were ¥18,706 million, representing a 12.3% decrease compared to the same period last year.

- Operating profit increased by 13.8% year-over-year to ¥1,294 million, and ordinary profit rose by 13.9% to ¥1,224 million.

- Net profit attributable to owners of parent was ¥723 million, an increase of 13.0% from the prior year’s interim period.

- Basic earnings per share for the interim period stood at ¥52.03.

- The full-year consolidated earnings forecast remains unchanged: net sales of ¥43,400 million (up 1.2% year-on-year), operating profit of ¥2,650 million (up 6.4%), ordinary profit of ¥2,500 million (up 6.3%), and net profit attributable to owners of parent of ¥1,500 million (up 4.5%).

🤖 AI Perspective

Despite a decline in net sales, the company achieved double-digit increases in operating profit, ordinary profit, and net profit for the interim period, which may suggest an improvement in profit margins. The enhanced profitability, particularly in the detached housing segment despite fewer sales units, could indicate the effectiveness of strategic land procurement and thorough cost management. Investors might monitor how these profitability improvements contribute to achieving the full-year forecast.

9366|サンリツ

960.0

▼ -0.21%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sanritsu announced its financial results for the fiscal year ended March 2026, reporting net sales of ¥20,532 million (up ¥410 million year-over-year) and operating profit of ¥1,035 million (up ¥1 million year-over-year).

- Recurring profit reached ¥987 million (up ¥185 million year-over-year), and net profit was ¥687 million (up ¥219 million year-over-year).

- The increase in net sales was due to strong performance in the handling of machine tools and power conversion devices in Japan, while operating profit remained largely flat due to sluggish machine tool handling at its U.S. subsidiary.

- The new mid-term management plan for FY2027/3 to FY2029/3 sets consolidated management targets for FY2029/3 as net sales of ¥23,500 million, operating profit of ¥1,600 million, and an operating profit margin of 6.8%.

- In the previous mid-term management plan (FY2024/3 to FY2026/3), while net sales were not achieved, the operating profit margin of 5.0% met its target.

🤖 AI Perspective

Sanritsu’s FY2026/3 results show a flat operating profit despite increased sales, which may suggest a balancing act between strong domestic performance and softer international demand. The significant rise in recurring and net profits could indicate effective cost control or reduced non-operating expenses, a factor worth monitoring for investors assessing the company’s financial health. The ambitious targets set in the new mid-term plan provide a clear outlook on the company’s growth strategy and could be a positive signal for future valuation.

6574|G-コンヴァノ

89.0

▲ +1.14%

📎 Source:G-コンヴァノ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Convano Inc. announced a further partial amendment to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 [IFRS]” on June 5, 2026, following a previous amendment disclosed on May 29, 2026.

- The primary reasons for this amendment include additional revisions to the classification of revenue, cost of sales, and selling, general and administrative expenses in the consolidated statement of profit or loss, as well as revisions to the amounts of certain current asset and current liability accounts in the consolidated statement of financial position, identified during the preparation and audit process of the Annual Securities Report.

- After the amendment, consolidated revenue is reported as 15,517 million yen (previously 15,500 million yen), and net profit for the period is △1,061 million yen (previously △951 million yen).

- In the consolidated statement of financial position, total assets have been revised to 18,896 million yen (previously 18,943 million yen), and total equity to 10,891 million yen (previously 11,001 million yen).

- An omission in the recognition of treasury shares held by a consolidated subsidiary, based on IAS 32, was discovered, leading to a revision of the number of treasury shares at the end of the period from 520,100 shares to 10,520,100 shares.

🤖 AI Perspective

Multiple amendments to financial statements can be a significant event for investors, as it may raise questions about the reliability of the company’s financial reporting. The changes in key financial figures such as revenue, profit, and total assets, along with the discovery of an unrecorded treasury share issue, could draw investor attention to the accuracy of future disclosures. The company has stated these are additional corrections resulting from ongoing discussions with auditors and further review, indicating efforts towards transparency.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

7078|G-INC HD

362.0

▲ +0.56%

📎 Source:G-INC HD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-INC HD announced on June 5, 2026, a partial correction to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 (Japanese GAAP),” originally disclosed on May 14, 2026.

- The reason for the correction was identified accounting errors during the audit process, specifically concerning sales, cost of sales, selling, general and administrative expenses, assets, and liabilities, including tax effect accounting and reclassification of accounts.

- As a result of the correction, consolidated net sales for FY2026/3 decreased by 9 million yen from the pre-correction figure of 4,569 million yen to 4,560 million yen (△0.2%).

- Consolidated gross profit decreased by 22 million yen from 1,722 million yen to 1,699 million yen (△1.4%), and consolidated operating loss increased by 3 million yen from △414 million yen to △417 million yen.

- Net loss attributable to owners of parent decreased by 1 million yen from △173 million yen to △174 million yen.

🤖 AI Perspective

This correction, prompted by multiple accounting errors identified during the audit, impacts several key consolidated financial metrics. The downward revisions to sales and various profit figures may raise concerns among investors regarding the reliability of disclosed information and the company’s internal control systems. It is worth monitoring how these corrected figures might influence future business operations and financial health.

9686|東洋テック

1689.0

▲ +1.99%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- TOYO-TEC announced on June 5, 2026, a correction to a portion of its “Notice Regarding Distribution of Financial Results Briefing Video for the Fiscal Year Ended March 2026.”

- The reason for the correction is the discovery of numerical errors in the financial results briefing video, which was disclosed on May 25, 2026, after its distribution.

- The corrected section is on page 11, titled “(Reference) Transition of Management Indicators,” within the financial results briefing materials.

- Concurrently with the correction, the URL for the financial results briefing video has been changed to https://youtu.be/gsQDc_RJEg.

- The comparison between the corrected and uncorrected financial results briefing materials shows revisions to key financial figures (net sales, operating income, ordinary income, net income attributable to owners of parent, earnings per share), as well as segment-specific net sales, segment income, performance of individual consolidated subsidiaries and the parent company, consolidated statements of income, operating expenses and cost of sales, and non-operating income/expenses and extraordinary gains/losses.

🤖 AI Perspective

This correction addresses numerical inaccuracies in the financial results briefing video, demonstrating the company’s commitment to ensuring disclosure accuracy. Investors should note that the primary focus of this correction is on the numerical data within “Transition of Management Indicators” on page 11, along with the updated video URL. It is advisable for investors to review the latest materials and video to confirm the updated content.

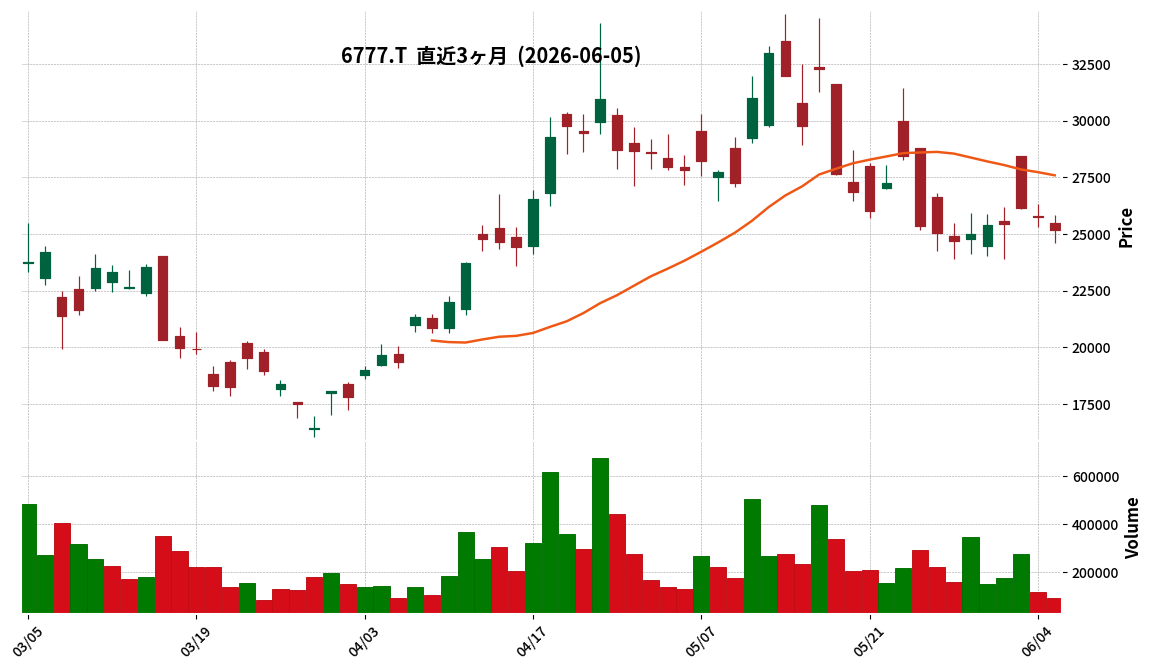

6777|santecHD

25170.0

▼ -2.18%

📎 Source:santecHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Santec HD reported consolidated results for the fiscal year ended March 2026, with net sales of ¥31.507 billion (up 31.1% year-on-year), operating profit of ¥10.325 billion (up 39.0% year-on-year), ordinary profit of ¥10.958 billion (up 38.9% year-on-year), and net profit attributable to owners of the parent of ¥7.667 billion (up 51.3% year-on-year).

- The Optical Components segment achieved sales of ¥6.356 billion (up 41.2% year-on-year) and operating profit of ¥1.754 billion (up 76.4% year-on-year), driven by strong sales of optical monitors for optical transceivers in North America.

- The Optical Measurement Equipment segment reported sales of ¥22.368 billion (up 24.6% year-on-year) and operating profit of ¥8.254 billion (up 31.4% year-on-year), with a significant increase in optical fiber cable inspection equipment in North America.

- Total current assets on the balance sheet increased by ¥7.673 billion year-on-year to ¥27.941 billion, primarily due to increases in cash and deposits, trade receivables, and raw materials. Net assets increased by ¥6.407 billion year-on-year to ¥27.835 billion.

- Operating cash flow amounted to ¥14.860 billion.

🤖 AI Perspective

Santec HD’s robust performance in FY2026, with double-digit growth across all key financial metrics, suggests a strong market demand for its optical components and measurement equipment, possibly driven by expanding investments in data centers and generative AI. The significant growth in net profit indicates effective leverage of increased sales. The strong contributions from specific products in North America across both segments highlight the company’s regional and product-specific strengths.

7984|コクヨ

800.3

▲ +1.54%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- KOKUYO announced changes to its shareholder benefits program, effective for shareholders recorded in the shareholder registry as of December 31, 2026.

- A new category for “500 shares to less than 2,000 shares” has been established, offering ¥4,000 worth of company group products or a donation to social contribution activities, conditional on continuous ownership for at least six months.

- Shareholder benefits will now include limited edition shareholder-exclusive goods, which will be provided regardless of the number of shares held.

- A new benefit provides priority invitation to shareholder events, with increased chances of winning based on the period of continuous ownership and the number of shares held (3x for 500+ shares held for 6+ months; 5x for 2,000+ shares held for 3+ years).