📌 Today’s Highlights

Today we cover 91 IR announcements. Notable among them: スカパーJSAT (9412), インフロニアHD (5076), MARUWA (5344). Use the table of contents below to navigate to each company.

- 9412|スカパーJSAT

- 5076|インフロニアHD

- 5344|MARUWA

- 178A|GX革新優良企業

- 3190|ホットマン

- 1897|金下建設

- 3563|F&LC

- 8282|ケーズHD

- 2371|カカクコム

- 4528|小野薬

- 5015|BPカストロール

- 6758|ソニーグループ

- 8173|Joshin

- 2193|COOKPAD

- 4792|山田コンサル

- 5941|中西製作所

- 3663|セルシス

- 3766|システムズD

- 4025|多木化学

- 5729|日精鉱

- 6023|ダイハツインフィ

- 7013|IHI

- 8084|RYODEN

- 9362|兵機海運

- 9432|NTT

- 9902|日伝

- 4556|カイノス

- 5464|モリ工業

- 5830|いよぎんHD

- 6085|G-アーキテクツSJ

- 2883|大冷

- 3839|ODK

- 3946|トーモク

- 4417|G-グローバルセキュ

- 5411|JFE

- 6326|クボタ

- 6340|渋谷工

- 7989|立川ブライ

- 8020|兼松

- 8367|南都銀

- 7203|トヨタ自

- 6062|チャームケア

- 9359|伊勢湾海

- 1899|福田組

- 2461|ファンコミ

- 5186|ニッタ

- 5380|新東

- 6470|大豊工業

- 7791|ドリームベッド

- 7963|興研

- 8864|空港施設

- 9532|大瓦斯

- 6929|日セラミック

- 6327|北川精機

- 1382|ホーブ

- 151A|G-ダイブ

- 2693|YKT

- 2790|ナフコ

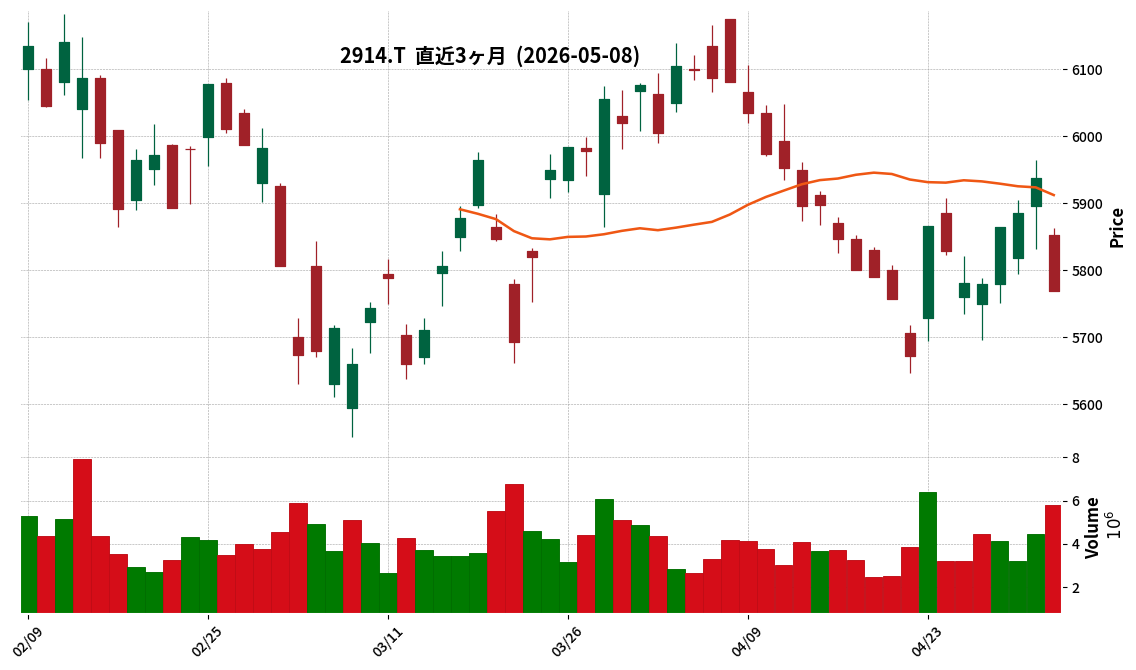

- 2914|JT

- 3238|セントラル総

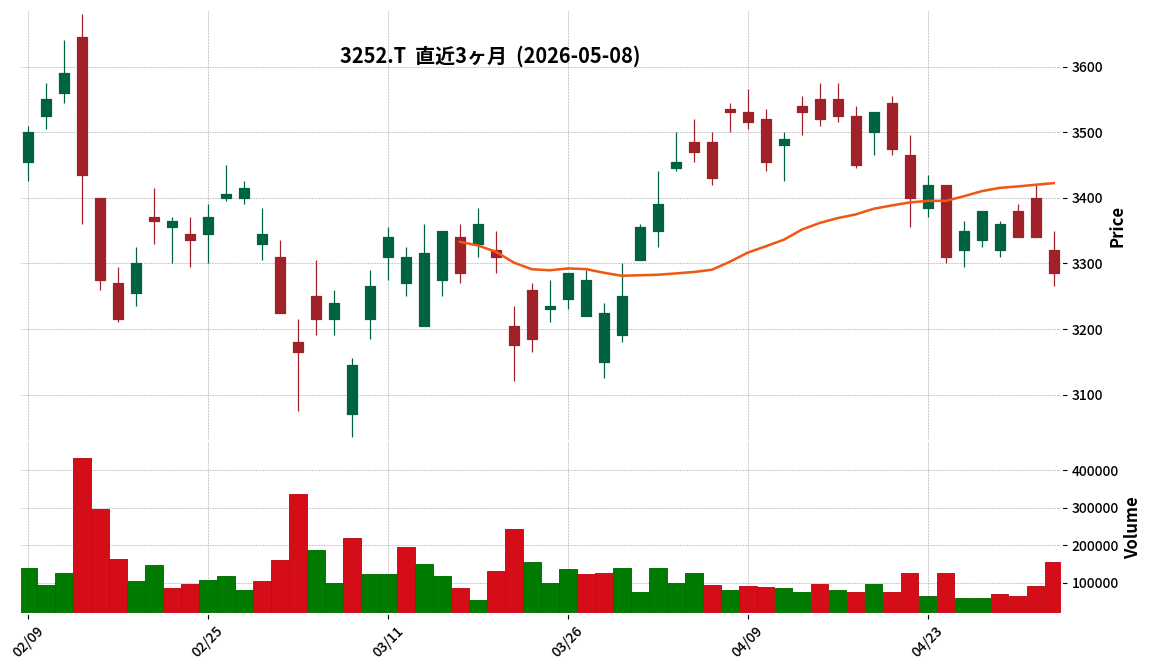

- 3252|地主

- 3286|トラストHD

- 3302|帝繊維

- 3712|情報企画

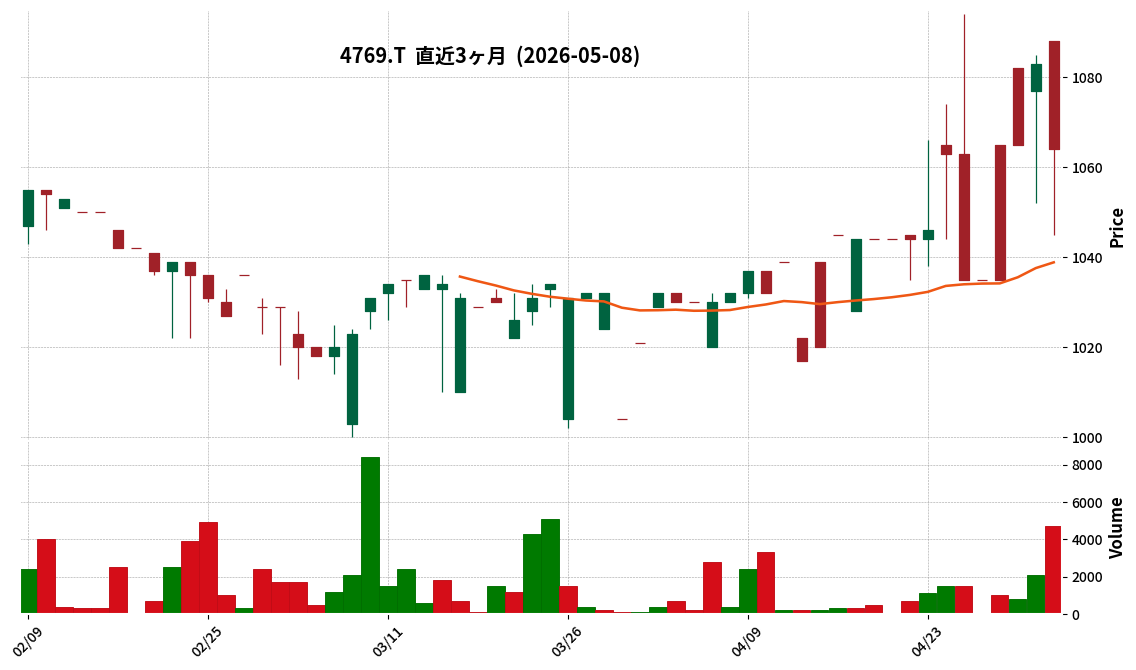

- 4769|IC

- 7875|竹田iP

- 9753|IXナレッジ

- 303A|G-visumo

- 4563|G-アンジェス

- 4958|長谷川香

- 7224|新明和工

- 8113|ユニチャーム

- 8996|ハウスフリーダム

- 9339|コーチ・エィ

- 9376|ユーラシア

- 9413|テレ東HD

- 9421|エヌジェイHD

- 3823|WHY HOW DO

- 7273|イクヨ

- 7578|ニチリョク

- 8798|アドバンスクリエイト

- 4970|東洋合成

- 7980|重松製作

- 9444|トーシンHD

- 4335|IPSHD

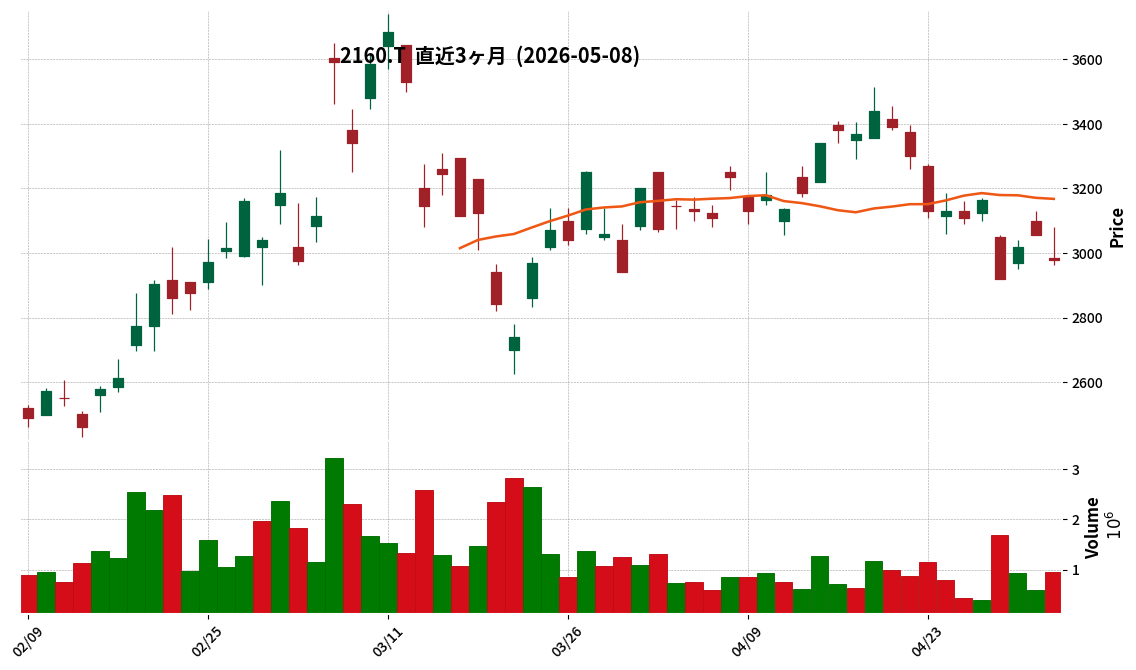

- 2160|G-GNI

- 6877|OBARA-G

- 9973|KOZOHD

- 3083|スターシーズ

- 8158|ソーダニッカ

- 2678|アスクル

9412|スカパーJSAT

3485.0

▼ -0.85%

📎 Source:スカパーJSAT Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- On May 8, 2026, SKY Perfect JSAT Corporation announced a correction to a part of its “SKY Perfect JSAT Group FY2026 Full-Year Financial Results Briefing Material.”

- The correction pertains to the FY2026 figures for “Security Sector Revenue Targets” on page 21 of the briefing material, which was originally disclosed on April 28, 2026.

- The revenue target for the Space Intelligence business was revised from the incorrect figure of ¥9.6 billion to the corrected figure of ¥11.3 billion.

- Concurrently, the revenue target for the Communication-related business was revised from the incorrect figure of ¥10.1 billion to the corrected figure of ¥8.4 billion.

- There are no corrections to the previously announced financial results (Kessan Tanshin).

🤖 AI Perspective

This correction specifically addresses figures within the earnings presentation material, with no impact on the previously disclosed official financial results. The revision of revenue targets within the security sector, showing an upward adjustment for the Space Intelligence business and a downward adjustment for the Communication-related business, may suggest a refined focus or evolving growth expectations within this segment. Investors might consider these updated figures when assessing the company’s strategic emphasis and future revenue drivers in the security domain.

5076|インフロニアHD

2155.5

▲ +0.00%

📎 Source:インフロニアHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- INFRONEER Holdings has revised its consolidated earnings forecast for the fiscal year ending March 31, 2026. Net profit attributable to owners of the parent company is now projected at ¥76.5 billion, a 27.5% increase from the previous forecast of ¥60.0 billion.

- Operating profit (事業利益) is expected to rise by 8.8% to ¥84.1 billion from ¥77.3 billion, and profit before income taxes by 15.6% to ¥107.2 billion from ¥92.7 billion.

- Revenue, however, was slightly revised down by 0.4% from ¥1,130.0 billion to ¥1,125.0 billion.

- The revisions are attributed to factors such as the successful acquisition of design changes in the building and civil engineering businesses for operating profit, and the recognition of valuation gains on financial assets for profit before income taxes and net profit.

- The company decided to increase the year-end dividend for common stock to ¥90.00 per share, with a record date of March 31, 2026. This results in an annual dividend of ¥120.00 per share (interim ¥30.00, year-end ¥90.00), up from the previous forecast of ¥62.00.

🤖 AI Perspective

- The significant upward revision in net profit, despite a slight decrease in revenue, may suggest an improvement in the company’s profitability or cost management effectiveness.

- The substantial increase in the annual common stock dividend, aligned with the mid-term management plan’s policy of a dividend payout ratio of 40% or more and a minimum dividend of ¥60, indicates a strong commitment to shareholder returns.

- As valuation gains on financial assets contributed to the increase in profit, investors may want to monitor the sustainability of core business earnings going forward.

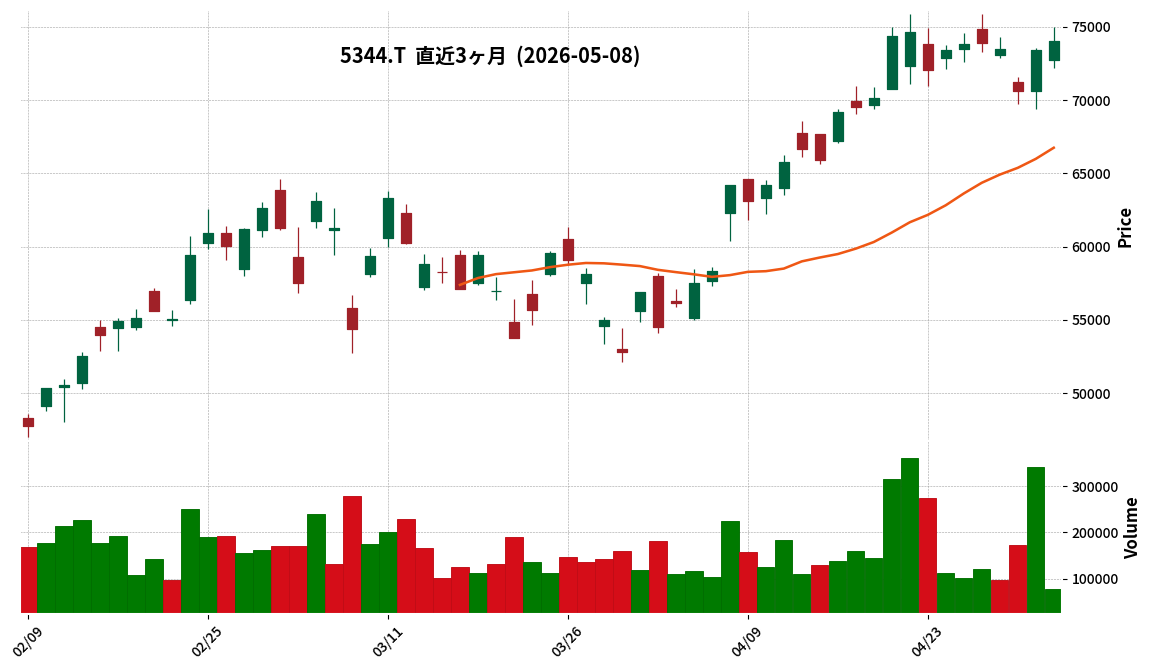

5344|MARUWA

74010.0

▲ +0.83%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- **FY2026 Consolidated Financial Results:**

- Net sales reached ¥74,476 million, a 3.7% increase year-on-year.

- Operating profit decreased by 7.2% to ¥24,976 million, ordinary profit decreased by 2.6% to ¥26,321 million, and profit attributable to owners of parent decreased by 5.6% to ¥18,163 million.

- The operating profit margin on net sales was 33.5%, and the ROE was 13.2%.

- **Segment Performance:**

- The Ceramic Parts Business reported net sales of ¥63,797 million (up 2.1% YoY) and segment profit of ¥24,573 million (down 9.3% YoY). This segment experienced weakness in the automotive market and delays in some semiconductor-related areas, but next-generation high-speed communication remained strong, with mass production of next-generation models starting in the fourth quarter.

- The Lighting Equipment Business reported net sales of ¥10,679 million (up 14.1% YoY) and segment profit of ¥2,141 million (up 49.0% YoY), driven by increased LED demand and high value-added lighting.

- **Financial Position and Cash Flow:**

- Total assets at the end of the period were ¥162,691 million (up ¥20,405 million from previous year-end), and net assets were ¥147,262 million (up ¥19,408 million from previous year-end). The equity ratio was 90.5%.

- Cash flow from operating activities was ¥16,933 million, while cash flow from investing activities was △¥21,757 million.

- **Dividend Information:**

- The annual dividend per share for FY2026 increased by ¥8 from the previous year, totaling ¥102.00.

- **FY2027 Consolidated Financial Forecast:**

- The company forecasts net sales of ¥84,100 million (up 12.9% YoY) and operating profit of ¥29,700 million (up 18.9% YoY).

- An annual dividend of ¥110.00 per share (up ¥8 YoY) is projected.

- **Key Highlights:**

- The fourth quarter achieved record-high sales and profits, driven by the launch of next-generation high-speed communication related models. Delays in general-purpose memory recovery and initial yield rate issues for some new products are reportedly on track for resolution.

🤖 AI Perspective

MARUWA’s FY2026 results indicated revenue growth but a decline in profits, which appears to be influenced by a softening in the automotive market and some delays in the semiconductor sector. However, strong performance in next-generation high-speed communication, especially a record-breaking fourth quarter, could suggest a significant growth driver for the company. The positive FY2027 outlook, including projected increases in both sales and operating profit, along with planned dividend hikes, may reflect management’s confidence in continued expansion, potentially led by high-speed communication technologies. The consistently high equity ratio of 90.5% also highlights the company’s robust financial stability, which is worth monitoring.

178A|GX革新優良企業

1613.0

▼ -0.25%

📎 Source:GX革新優良企業 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Global X Innovative Bluechip ETF (Code: 178A) announced its financial results for the period from September 25, 2025, to March 24, 2026 (FY2026/3).

- Total net assets at the end of the period stood at JPY 4,477 million, a decrease from the previous period’s end (JPY 4,613 million).

- The Net Asset Value (NAV) per 100 units increased to JPY 144,448, up from JPY 139,789 at the end of the previous period.

- No distribution was declared for the current period (JPY 0 per 100 units), compared to JPY 300 in the prior period.

- Net income for the period was JPY 172 million, representing a significant decrease from the JPY 1,113 million reported in the previous period.

- In the statement of income, foreign exchange gains exceeded JPY 346 million, while losses from securities trading and derivative transactions exceeded JPY 132 million and JPY 41 million, respectively.

🤖 AI Perspective

The operational results indicate that while the NAV per 100 units increased, total net assets and outstanding units decreased, suggesting that redemptions outpaced subscriptions during the period. Despite no distribution, the fund secured net income, primarily due to significant foreign exchange gains which offset losses from securities trading and derivative transactions. This highlights the substantial impact of currency fluctuations on the fund’s performance, given its reference index is yen-denominated.

3190|ホットマン

573.0

▲ +0.70%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hotman Co., Ltd. (3190) resolved to increase its surplus dividend at the Board of Directors meeting held on May 8, 2026.

- The dividend per share for the record date of March 31, 2026, has been set at 11 yen.

- This represents an upward revision of 1 yen from the most recent dividend forecast of 10 yen per share, which was announced on May 9, 2025.

- The actual dividend for the previous fiscal year (FY2025/3) was 10 yen per share.

- The total dividend amount is 77 million yen, with an effective date of June 5, 2026.

🤖 AI Perspective

[COMMENTARY]

This dividend increase by Hotman may suggest the company’s confidence in its operational performance for the fiscal year ending March 2026 and its future business prospects. The decision aligns with its stated basic policy of providing stable and continuous dividends while securing necessary internal reserves for future growth and strengthening its management foundation. Investors may observe that the company maintains its policy of a single year-end dividend payout.

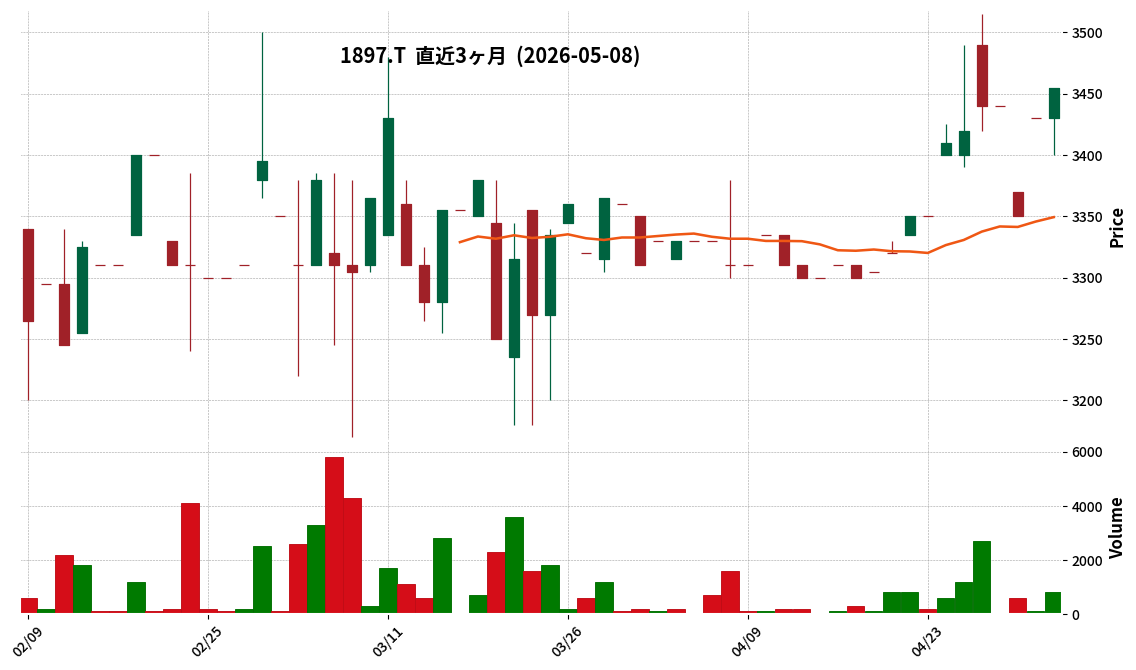

1897|金下建設

3455.0

▲ +0.73%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kaneshita Construction Co., Ltd. announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026 – March 31, 2026) on May 8, 2026.

- Consolidated net sales increased by 17.4% year-on-year to JPY 2,699 million. Operating profit rose by 1.1% to JPY 184 million, ordinary profit by 8.4% to JPY 202 million, and net profit attributable to owners of parent increased by 3.6% to JPY 121 million.

- By segment, the Construction Business recorded net sales of JPY 2,581 million (up 16.7%) and orders received of JPY 2,007 million (up 4.4%). The Manufacturing and Sales Business, etc., reported net sales of JPY 203 million (up 14.6%) and segment profit of JPY 26 million (up 684.5%).

- As of the end of the first quarter, consolidated total assets stood at JPY 24,458 million, net assets at JPY 20,300 million, and the equity ratio was 81.4%.

- The consolidated full-year earnings forecast for the fiscal year ending December 2026, as well as the dividend forecast (year-end JPY 50.00, total annual JPY 50.00), remain unchanged from the latest publicly announced figures.

🤖 AI Perspective

- The first quarter of the fiscal year ending December 2026 saw Kaneshita Construction achieve increased revenue and profits, driven by higher sales in both the Construction Business and the Manufacturing and Sales Business segments.

- Despite the positive start to the year with growth in sales and various profit metrics amidst a challenging business environment, the company has maintained its full-year consolidated earnings forecast, which may suggest a cautious outlook on future business developments or potential cost fluctuations.

- The equity ratio of 81.4% indicates continued strong financial health, reinforcing the company’s stable financial position.

3563|F&LC

10435.0

▲ +8.90%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- FOOD & LIFE COMPANIES (F&LC) announced its consolidated financial results for the second quarter of the fiscal year ending September 2026 on May 8, 2026, covering the period from October 1, 2025, to March 31, 2026.

- For the interim period, consolidated revenue reached 254,182 million yen (up 24.7% year-on-year), operating profit was 28,080 million yen (up 43.7% year-on-year), and net profit attributable to owners of the parent was 17,788 million yen (up 49.9% year-on-year).

- The company revised its full-year consolidated earnings forecast for the fiscal year ending September 2026, projecting revenue of 505,000 million yen (up 17.6% year-on-year), operating profit of 48,500 million yen (up 34.4% year-on-year), and net profit attributable to owners of the parent of 30,000 million yen (up 30.8% year-on-year).

- F&LC announced a stock split at a ratio of two shares for every one common share, effective July 1, 2026.

- In conjunction with the stock split, the forecast for the year-end dividend per share for the fiscal year ending September 2026 was revised to 20.00 yen (40 yen before considering the stock split).

🤖 AI Perspective

- The significant increase in revenue and profits for the interim period appears to be driven by robust performance in both its domestic and overseas Sushiro businesses, along with proactive strategic initiatives.

- The upward revision of the full-year earnings and dividend forecasts may suggest a positive outlook on the sustained growth of existing operations.

- The announced stock split could aim to lower the per-unit investment amount, potentially making the shares more accessible to a broader range of investors.

8282|ケーズHD

1751.5

▼ -0.26%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- K’s Holdings announced on May 8, 2026, the progress update and partial revision (upward revision) of its “Mid-Term Management Plan 2027” as of the end of the second year.

- The company has revised upward its management targets for net sales and operating profit for the final fiscal year of the plan, March 2027, based on recent business performance.

- The revised targets for the fiscal year ending March 2027 are ¥785 billion for net sales and ¥30.5 billion for operating profit.

- Regarding the shareholder return policy, the minimum annual dividend per share during the Mid-Term Management Plan period has been revised from ¥46 to ¥48.

- For the fiscal year ended March 2026, K’s Holdings achieved consolidated net sales of ¥759.7 billion and operating profit of ¥26.8 billion.

🤖 AI Perspective

This upward revision may suggest the company’s strategic initiatives for efficiency and robust demand for home appliances are progressing well. The increase in both sales and operating profit targets, along with the higher dividend floor, could indicate K’s Holdings’ commitment to enhancing shareholder returns. These adjustments align with the company’s stated focus on management conscious of capital costs and stock prices, which investors may find noteworthy.

2371|カカクコム

2853.5

▲ +5.37%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kakaku.com, Inc. (Code: 2371) announced its consolidated financial results for the fiscal year ended March 31, 2026, on May 8, 2026.

- For the fiscal year 2026/3, revenue reached JPY 94,127 million, marking a 20.0% increase from the previous year. This growth was primarily driven by the robust performance of the Tabelog, Incubation, and Kyujin Box businesses.

- Operating profit for the same period was JPY 27,243 million, a decrease of 7.0% year-on-year. This decline is attributed to increased growth investments, particularly in the Kyujin Box business, which led to higher expenses.

- Profit attributable to owners of the parent decreased by 6.1% to JPY 18,803 million, with basic earnings per share at JPY 95.05.

- The annual dividend for FY2026/3 was JPY 50.00. For FY2027/3, the company projects consolidated revenue of JPY 114,500 million (up 21.6% YoY) and operating profit of JPY 30,800 million (up 13.1% YoY).

🤖 AI Perspective

The significant increase in revenue suggests strong underlying business growth, while the decline in operating profit appears to be a result of strategic investments aimed at future expansion. The company’s forecast for renewed revenue and profit growth in the upcoming fiscal year could indicate confidence in these investments yielding returns. Investors may focus on the execution of these growth strategies and the realization of their benefits.

4528|小野薬

2284.5

▼ -3.22%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Ono Pharmaceutical Co., Ltd. announced its consolidated financial results (IFRS) for the fiscal year ended March 31, 2026.

- Consolidated revenue for FY2026/3 was ¥515,785 million, an increase of 5.9% from the previous fiscal year.

- Profit attributable to owners of the parent for FY2026/3 was ¥69,767 million, up 39.4% year-on-year.

- Core consolidated operating profit reached ¥137,135 million, representing a 21.7% increase compared to the prior year.

- While domestic product sales decreased by 3.5% to ¥281,400 million, overseas product sales surged by 56.5% to ¥61,200 million, and royalties and other income rose by 10.9% to ¥173,200 million.

- The consolidated earnings forecast for FY2027/3 projects revenue of ¥455,000 million (a decrease of 11.8% year-on-year) and profit attributable to owners of the parent of ¥71,000 million (an increase of 1.8% year-on-year).

🤖 AI Perspective

For FY2026/3, increased overseas product sales and royalty income appear to have offset a decline in domestic product sales, contributing to overall revenue and profit growth. The full-year contribution from Deciphera Pharmaceuticals products and higher royalty income from Bristol-Myers Squibb are noteworthy factors. The guidance for FY2027/3, forecasting a decrease in revenue but a slight increase in profit, might indicate a shift in the business portfolio or ongoing efforts in cost optimization and efficiency improvements.

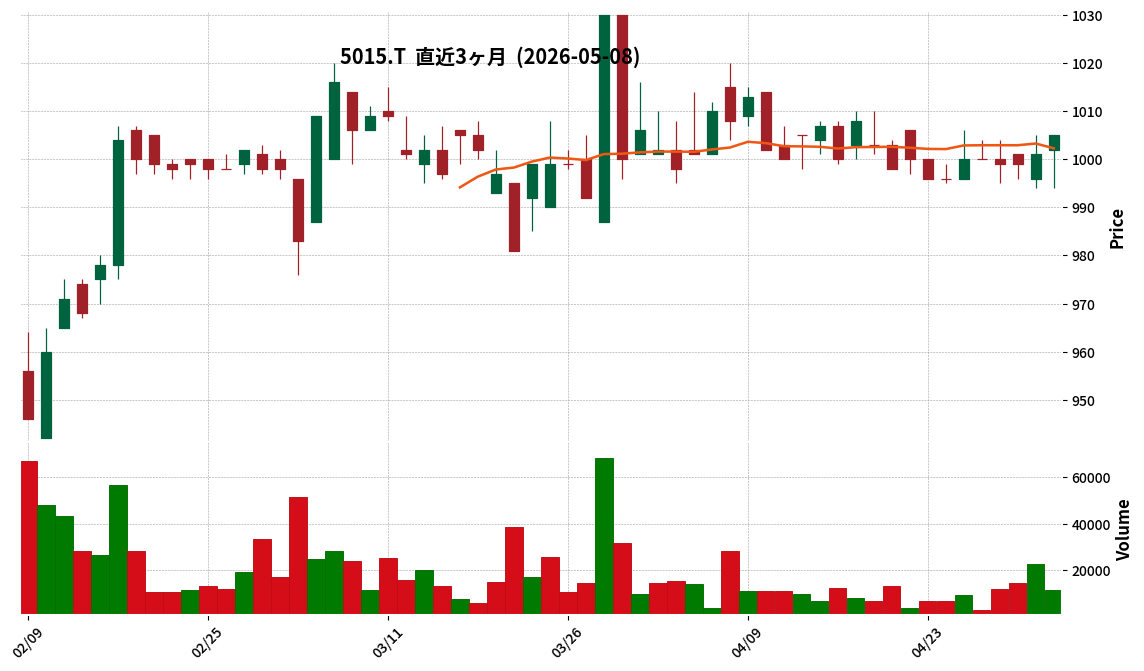

5015|BPカストロール

1005.0

▲ +0.40%

📎 Source:BPカストロール Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of fiscal year 2026 (January 1 to March 31, 2026), Net Sales amounted to ¥3,393 million, representing a 2.4% increase compared to the same period of the previous year.

- During the same quarter, Operating Profit was ¥464 million (+255.1% year-on-year), Ordinary Profit was ¥481 million (+189.8% year-on-year), and Quarterly Net Profit reached ¥325 million (+330.2% year-on-year), indicating significant profit growth across all categories.

- As of March 31, 2026, Total Assets stood at ¥12,858 million, Net Assets at ¥9,802 million, and the Equity Ratio was 76.2%.

- The full-year FY2026 earnings forecast and the annual dividend forecast of ¥50.00 per share remain unchanged from the most recent public announcement.

- Regarding the planned transfer of the Castrol business from the bp group to Stonepeak, announced on December 26, 2025, the company stated that any significant new developments will be promptly disclosed.

6758|ソニーグループ

3080.0

▼ -1.60%

📎 Source:ソニーグループ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, Sony Group’s continuing operations reported sales of JPY 12,479.62 billion (a 3.7% increase year-on-year) and operating income of JPY 1,447.51 billion (a 13.4% increase).

- Net income attributable to Sony Corporation’s stockholders from continuing operations decreased by 3.4% year-on-year to JPY 1,030.89 billion.

- The partial spin-off of Sony Financial Group Inc. was executed on October 1, 2025, leading to the reclassification of the financial business as discontinued operations. This resulted in a loss of JPY 1,377.80 billion from discontinued operations.

- For the fiscal year ending March 31, 2027, the consolidated forecast for continuing operations projects sales of JPY 12,300 billion (a 1.4% decrease), operating income of JPY 1,600 billion (a 10.5% increase), and net income attributable to Sony Corporation’s stockholders of JPY 1,160 billion (a 12.5% increase).

- The annual dividend for FY2026/3 was JPY 25.00 per share (JPY 12.50 year-end), with a forecast of JPY 35.00 per share (JPY 17.50 year-end) for FY2027/3.

🤖 AI Perspective

Sony Group’s FY2026/3 results indicate solid growth in sales and operating income for its continuing operations, despite the reported net income decrease reflecting the accounting treatment from the financial business spin-off. The forecast for FY2027/3 projects an increase in operating and net income, suggesting an expected rebound in core profitability. The planned increase in the annual dividend for the upcoming fiscal year may also be of interest to investors as an indicator of future shareholder returns.

8173|Joshin

2919.0

▼ -2.70%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Joshin Co., Ltd. reported consolidated results for the fiscal year ended March 31, 2026, with net sales of 436,650 million yen (up 8.3% year-on-year), operating profit of 5,422 million yen (up 47.0%), and ordinary profit of 5,113 million yen (up 46.5%). Net profit attributable to owners of parent was 3,280 million yen (down 3.7% year-on-year).

- As of March 31, 2026, the consolidated financial position showed total assets of 228,813 million yen, net assets of 105,364 million yen, and an equity ratio of 46.0%.

- The annual dividend for FY2026 was 100.00 yen per share (including a year-end dividend of 50.00 yen), consistent with the previous fiscal year.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of 438,000 million yen (up 0.3% year-on-year), operating profit of 6,000 million yen (up 10.7%), ordinary profit of 5,500 million yen (up 7.6%), and net profit attributable to owners of parent of 3,500 million yen (up 6.7%).

- The projected annual dividend for FY2027 is 100.00 yen per share (including a year-end dividend of 50.00 yen).

🤖 AI Perspective

The substantial increases in operating and ordinary profits for FY2026, alongside an 8.3% rise in net sales, may suggest improved operational performance during the period. While net profit attributable to owners of parent experienced a slight decline, the company’s forecast for FY2027 projects a recovery with expected growth in both revenue and profit, notably with over 10% growth anticipated in operating profit. This outlook could indicate the company’s confidence in its future business strategies and potential for continued improvement.

2193|COOKPAD

138.0

▼ -0.72%

📎 Source:COOKPAD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of the fiscal year ending December 2026 (January 1 to March 31, 2026), consolidated revenue decreased by 7.7% year-over-year to JPY 1,267 million.

- Operating income shifted from a profit of JPY 89 million in the prior year to a loss of JPY 137 million, primarily due to a one-time expense of JPY 182 million related to personnel restructuring at overseas locations.

- Quarterly profit attributable to owners of the parent turned from a profit of JPY 111 million in the prior year to a loss of JPY 417 million, influenced by fair value adjustments of marketable securities recorded as financial expenses due to market fluctuations, mainly in the U.S.

- As of March 31, 2026, consolidated total assets amounted to JPY 13,499 million (a decrease of JPY 603 million from the end of the previous fiscal year), and total equity was JPY 12,262 million (a decrease of JPY 635 million). The decline in equity was mainly attributed to the acquisition of treasury shares and the recording of quarterly losses attributable to owners of the parent.

- The consolidated earnings forecast for the fiscal year ending December 2026 is not disclosed, as it is deemed difficult to reasonably calculate due to the flexible nature of investment timing and scale based on changes in the business environment.

🤖 AI Perspective

The decline in revenue and the shift to an operating loss may suggest challenges stemming from a reduction in premium service subscribers, compounded by significant one-off costs for overseas personnel restructuring. Furthermore, financial expenses from fair value adjustments of marketable securities indicate external market factors also contributed to the quarter’s performance. With no full-year earnings forecast provided, the company’s future investment strategies and operational efficiency initiatives could be worth monitoring.

4792|山田コンサル

1689.0

▲ +3.18%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Yamada Consulting Group Co., Ltd. reported consolidated net sales of JPY 26,711 million for the fiscal year ended March 2026, a 17.3% increase year-on-year.

- Operating profit was JPY 3,740 million (down 9.4% year-on-year), and ordinary profit was JPY 3,712 million (down 9.4% year-on-year). Net profit attributable to owners of parent increased by 0.4% to JPY 2,895 million.

- The annual dividend for FY2026/3 was JPY 77 (interim JPY 38, year-end JPY 39), maintained from the previous fiscal year. The forecast for FY22027/3 annual dividend is also JPY 77.

- For FY2027/3, the company forecasts consolidated net sales of JPY 26,900 million (up 0.7% year-on-year), operating profit of JPY 4,500 million (up 20.2% year-on-year), and net profit attributable to owners of parent of JPY 2,900 million (up 0.1% year-on-year).

- During the consolidated fiscal year, the scope of consolidation significantly changed with the addition of two new companies: Manas Corporate Partners Co., Ltd. and Daikoku Building Co., Ltd.

🤖 AI Perspective

The FY2026/3 consolidated results show a notable increase in net sales but a decrease in operating and ordinary profits, while net profit attributable to owners of parent saw a slight increase. This divergence in profit metrics may warrant further examination by investors to understand the underlying factors. For FY2027/3, the company projects a modest increase in net sales but a significant recovery in operating and ordinary profits, which could suggest an anticipated improvement in profitability.

5941|中西製作所

2578.0

▲ +2.14%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nakanishi Co., Ltd. reported record-high net sales of ¥41,008 million for the fiscal year ended March 31, 2026, marking a 2.7% increase year-on-year.

- Operating profit grew by 15.9% to ¥3,049 million, ordinary profit by 13.6% to ¥3,169 million, and net profit increased by 22.3% to ¥2,210 million.

- The annual dividend per share for FY2026/3 was raised to ¥110.00, up from ¥87.00 in the previous fiscal year.

- For FY2027/3, the company forecasts net sales of ¥41,200 million (+0.5% YoY), but anticipates a decrease in profits with operating profit at ¥2,400 million (-21.3% YoY) and net profit at ¥2,000 million (-9.5% YoY).

- As of March 31, 2026, total assets stood at ¥33,899 million, and net assets were ¥22,475 million, with an equity ratio of 66.3%.

🤖 AI Perspective

The robust performance in FY2026/3, marked by record sales and significant profit growth, along with an increased dividend, suggests a period of strong operational execution. However, the projected decline in profits for FY2027/3 indicates potential headwinds or strategic adjustments that could impact the upcoming fiscal year. The high equity ratio may suggest a stable financial foundation, providing resilience against future market fluctuations.

3663|セルシス

1585.0

▲ +9.69%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- CELSYS, Inc. announced its unaudited financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026 – March 31, 2026).

- During this quarter, net sales reached JPY 2,803 million (up 16.7% year-on-year), operating income JPY 1,211 million (up 59.6% year-on-year), ordinary income JPY 1,213 million (up 61.7% year-on-year), and quarterly net income JPY 813 million (up 18.9% year-on-year), achieving record highs for key revenue indicators.

- “CLIP STUDIO PAINT,” the core product, reached 63.17 million cumulative units shipped by March 2026 and 64.30 million by April 2026. Its subscription ARR (Annual Recurring Revenue) hit JPY 5.8 billion by March 2026 (up 25.9% year-on-year), a new record.

- The company forecasts an annual dividend of JPY 38 for the fiscal year ending December 2026, consisting of an interim dividend of JPY 18 and a year-end dividend of JPY 20, which represents a JPY 2 increase from the previous year.

- CELSYS executed a cancellation of 1.5 million shares of treasury stock on March 16, 2026.

🤖 AI Perspective

CELSYS’s first-quarter results show significant increases in both sales and profit, with key revenue indicators reaching new record highs, which may suggest robust business momentum. The continued growth of “CLIP STUDIO PAINT” and the expansion of its subscription revenue appear to be driving this performance. Additionally, the treasury stock cancellation and increased dividend forecast could indicate a focus on enhancing capital efficiency and shareholder returns.

3766|システムズD

1300.0

▲ +4.17%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Systems Design Co., Ltd. (Code: 3766) has announced its consolidated financial results for the fiscal year ended March 31, 2026.

- For FY2026, consolidated net sales were ¥9,993 million (up 4.0% year-on-year), operating profit was ¥595 million (up 31.1%), ordinary profit was ¥604 million (up 26.6%), and profit attributable to owners of parent was ¥393 million (up 32.1%).

- Basic earnings per share for FY2026 were ¥115.00.

- The year-end dividend for FY2026 was set at ¥55.00, resulting in an annual dividend of ¥55.00 (compared to ¥45.00 for the previous year).

- For FY2027, the company forecasts consolidated net sales of ¥10,418 million (up 4.2% year-on-year), operating profit of ¥631 million (up 5.9%), profit attributable to owners of parent of ¥415 million (up 5.7%), and an annual dividend of ¥60.00.

🤖 AI Perspective

The substantial increase in operating profit, outpacing sales growth, and the significant rise in cash flow from operating activities, may suggest improvements in the company’s operational efficiency and profitability. The forward-looking guidance for continued revenue and profit growth, coupled with an increased dividend projection, could indicate management’s positive outlook on future performance and commitment to shareholder returns.

4025|多木化学

5000.0

▲ +8.58%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Takii Chemical announced its consolidated results for the first quarter of fiscal year 2026. Net sales were ¥10,776 million (up 9.2% year-on-year), operating profit was ¥946 million (up 37.1% YoY), ordinary profit was ¥983 million (up 27.4% YoY), and net profit attributable to owners of parent was ¥695 million (up 25.0% YoY).

- Revenue and profit growth were achieved across the Agri, Chemicals, Construction Materials, and Transportation segments. Notably, the Chemicals segment saw a 12.6% increase in net sales and a 51.5% rise in operating profit compared to the prior year.

- As of March 31, 2026, total assets amounted to ¥68,412 million, net assets were ¥45,386 million, and the equity ratio stood at 65.7%.

- The consolidated earnings forecast for the full fiscal year 2026 and the annual dividend forecast (¥80.00 per share for year-end) remain unchanged from the announcement made on February 9, 2026.

🤖 AI Perspective

The significant increases in sales and all profit categories during the first quarter, driven by efforts to improve the profitability of existing businesses, may suggest a strong start to the fiscal year. As the full-year earnings forecast remains unchanged, the impact of future business environment changes and the progress of various initiatives on performance will likely continue to be monitored. The high equity ratio could indicate a stable financial foundation for the company.

5729|日精鉱

2209.0

▲ +0.32%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nippon Seiko K.K. disclosed on May 8, 2026, the financial results for the fiscal year ended January 2026 of Kawashima Co., Ltd., an unlisted “other related company.” Kawashima’s primary business is non-ferrous metal wholesaling, and Nippon Seiko holds a 26.52% voting rights stake (including 16.58% indirect ownership) as of March 31, 2026.

- For the fiscal year ended January 31, 2026 (from February 1, 2025, to January 31, 2026), Kawashima Co., Ltd. reported net sales of ¥21,209 million, operating income of ¥751 million, and net income of ¥439 million in its statement of income.

- As of January 31, 2026, Kawashima’s balance sheet showed total assets of ¥18,598 million, total liabilities of ¥12,012 million, and total net assets of ¥6,586 million.

- The Nippon Seiko Group engages in raw material procurement transactions with Kawashima Co., Ltd.

🤖 AI Perspective

The disclosure of financial information for an unlisted related company is intended to enhance transparency regarding related party transactions and to allow investors to understand the indirect impact on Nippon Seiko’s management. As Kawashima Co., Ltd. is a raw material supplier for the Nippon Seiko Group, its financial performance and business results could be a key factor in analyzing Nippon Seiko’s operational activities. It may also be worth monitoring how Kawashima’s performance as a non-ferrous metal wholesaler correlates with international market trends.

6023|ダイハツインフィ

3300.0

▲ +8.55%

📎 Source:ダイハツインフィ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Daihatsu Infi Earth Corporation announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- For the period, consolidated net sales were ¥88,066 million, representing a 0.8% decrease from the previous fiscal year, and operating profit was ¥7,621 million, a 0.2% decrease.

- In contrast, ordinary profit increased by 4.7% to ¥7,959 million, and profit attributable to owners of parent increased by 3.6% to ¥5,920 million.

- The annual dividend for the fiscal year ended March 31, 2026, was set at ¥69.00 per share, an increase from ¥62.00 in the prior fiscal year.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥104,000 million (up 18.1%), operating profit of ¥8,000 million (up 5.0%), ordinary profit of ¥8,000 million (up 0.5%), and profit attributable to owners of parent of ¥5,700 million (down 3.7%).

🤖 AI Perspective

Daihatsu Infi’s FY2026/3 results show a slight decline in net sales and operating profit, yet a rise in ordinary and net profits. This mixed performance may suggest that while average selling prices were affected by a shift towards smaller engines, internal cost control or other operational efficiencies could have supported profitability. Looking ahead to FY2027/3, the company projects increased sales and operating profit, but a decrease in net profit, indicating that navigating market dynamics will be a key area for observation.

7013|IHI

3283.0

▲ +7.82%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026 (FY2026), IHI reported consolidated revenue of JPY 1,643,402 million, an increase of 1.0% year-on-year.

- Profit attributable to owners of parent for FY2026 stood at JPY 160,992 million, marking a significant increase of 42.8% compared to the previous fiscal year.

- Basic earnings per share for FY2026 was JPY 151.88 (after stock split adjustment).

- IHI projects consolidated revenue for FY2027 (ending March 31, 2027) to be JPY 1,830,000 million (an 11.4% increase year-on-year), and operating profit to be JPY 240,000 million (a 45.0% increase year-on-year).

- The annual dividend per share for FY2026 was JPY 80.00 (JPY 10.00 year-end, JPY 70.00 interim, adjusted for stock split), with a forecast of JPY 23.00 for FY2027.

🤖 AI Perspective

The substantial increase in profit attributable to owners of parent for FY2026, alongside a moderate revenue growth, may indicate improved operational efficiency and profitability. The robust projections for FY2027, particularly the 45.0% increase in operating profit, could suggest management’s confidence in the company’s strategic initiatives and future earnings potential. These results and forecasts might be viewed by investors as a positive sign regarding IHI’s trajectory.

8084|RYODEN

3685.0

▲ +1.66%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- RYODEN Corporation announced on May 8, 2026, a revision to its dividend forecast for the fiscal year ending March 2026.

- The annual dividend per share has been revised to JPY 138, up from the previously projected JPY 136 (announced on May 9, 2025).

- The year-end dividend has been revised from JPY 68 to JPY 70 (the second quarter-end dividend remains unchanged at JPY 68).

- The revision is attributed to the company’s commitment to enhancing shareholder returns, based on its dividend policy revised on May 9, 2025.

- This dividend policy sets a lower limit of either a consolidated total return ratio of 50% or a consolidated Dividend on Equity (DOE) of 3.5%.

- Separately, an announcement regarding a change in dividend policy (introduction of progressive dividends) to be applied from the fiscal year ending March 2027 has also been made today.

🤖 AI Perspective

This revised dividend forecast represents a tangible increase under the company’s updated shareholder return policy, which was initially changed on May 9, 2025, suggesting a commitment to strengthening medium-to-long-term shareholder returns. The company’s stance on stable shareholder returns, independent of short-term performance, with a floor of a consolidated total return ratio of 50% or a consolidated DOE of 3.5%, has been reaffirmed. Investors may also observe how this aligns with the separately announced progressive dividend policy set to begin from the fiscal year ending March 2027.

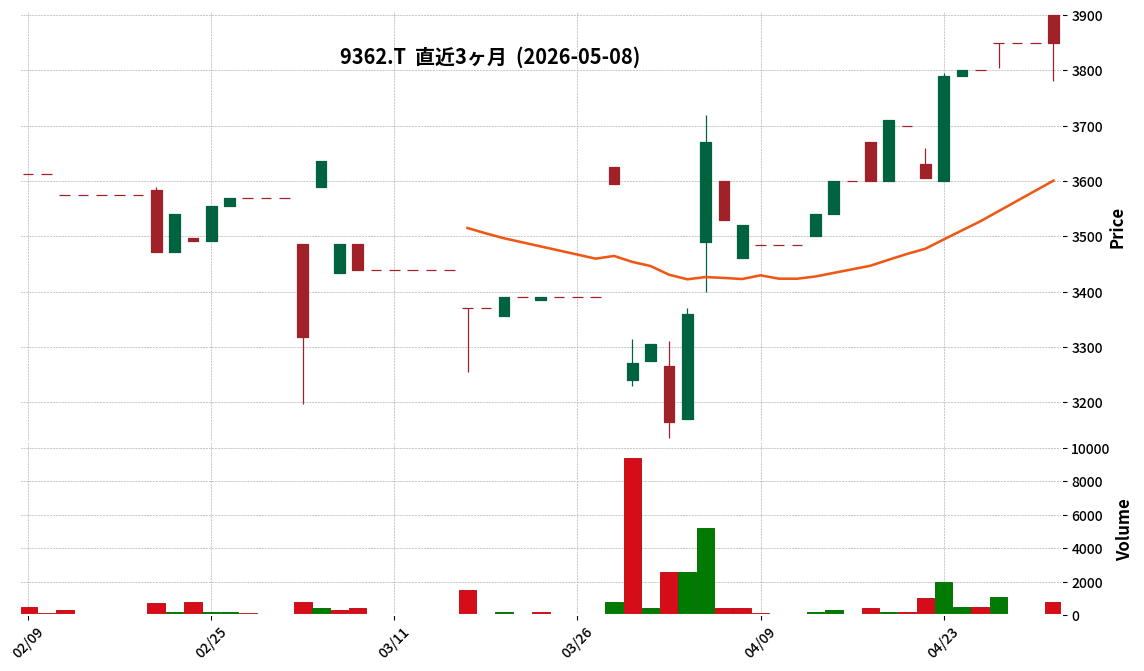

9362|兵機海運

3850.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hyoki Kaiun reported consolidated results for the fiscal year ended March 31, 2026, with net sales of ¥13,389 million, operating profit of ¥436 million, ordinary profit of ¥499 million, and net profit of ¥397 million, representing a decrease in both revenue and profit compared to the previous fiscal year.

- Compared to the full-year forecast announced on October 30, 2025, operating profit achieved 106.5%, ordinary profit 106.3%, and net profit 110.3%, exceeding the revised plan.

- By segment, port transportation sales increased to ¥4,085 million (+109.9% year-on-year) and warehousing sales to ¥1,704 million (+102.4% year-on-year), while domestic and international shipping segments experienced revenue declines.

- The self-capital ratio at the end of March 2026 increased to 43.3% from 38.7% in the previous fiscal year, a rise of 4.6 percentage points.

- For the fiscal year ending March 31, 2027, the company forecasts net sales of ¥14,500 million, operating profit of ¥510 million, ordinary profit of ¥540 million, and net profit of ¥400 million.

🤖 AI Perspective

While Hyoki Kaiun reported a decrease in revenue and profit for FY2026 due to challenges in the shipping business, the results surpassed revised forecasts, driven by growth in port transportation and warehousing. The improvement in the self-capital ratio to 43.3% may suggest a strengthening of the company’s financial position. The projected increase in revenue and profit for FY2027, under the mid-term management plan, could indicate an anticipated recovery and potential benefits from strategic initiatives.

9432|NTT

150.6

▼ -0.13%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- NTT announced its consolidated financial results for fiscal year 2025 (April 1, 2025, to March 31, 2026), with operating revenue reaching ¥14,409.1 billion, a 5.1% increase year-on-year.

- Profit attributable to owners of the parent company amounted to ¥1,037.0 billion, representing a 3.7% increase from the previous fiscal year.

- The annual dividend for FY2025 was set at ¥5.30 per share (interim ¥2.65, year-end ¥2.65), an increase from the prior fiscal year.

- For FY2026, NTT forecasts consolidated operating revenue of ¥15,060.0 billion, projecting a 4.5% increase year-on-year.

- Conversely, profit attributable to owners for FY2026 is projected to decrease by 5.5% to ¥980.0 billion.

🤖 AI Perspective

NTT’s FY2025 results show solid growth in revenue and profit, accompanied by an increased annual dividend, which may be viewed positively by investors. However, the FY2026 forecast indicates a projected decrease in profit attributable to owners despite continued revenue growth. This divergence could suggest a focus on strategic investments or potential cost increases, which market participants may monitor for underlying causes and future implications.

9902|日伝

2486.0

▲ +2.26%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the consolidated fiscal year ended March 31, 2026, Nichiden reported net sales of JPY 141,033 million, a 4.6% increase compared to the previous fiscal year.

- Operating profit for the period decreased by 3.0% to JPY 6,622 million, while ordinary profit rose by 3.7% to JPY 7,465 million, and net profit attributable to owners of parent increased by 4.5% to JPY 5,114 million.

- The annual dividend for the fiscal year ended March 31, 2026, was announced as JPY 70.00 per share (JPY 35.00 interim, JPY 35.00 year-end).

- The consolidated earnings forecast for the fiscal year ending March 31, 2027, projects net sales of JPY 150,000 million (up 6.4% year-on-year), operating profit of JPY 7,300 million (up 10.2%), and net profit attributable to owners of parent of JPY 5,500 million (up 7.5%).

- The forecasted annual dividend for the fiscal year ending March 31, 2027, is JPY 100.00 per share (JPY 50.00 interim, JPY 50.00 year-end).

🤖 AI Perspective

While Nichiden achieved increased sales, ordinary profit, and net profit for FY2026, the decline in operating profit may prompt further examination of profit margin dynamics. The company’s forecast for FY2027 indicates anticipated growth across sales, all profit categories, and an increase in the annual dividend, suggesting a positive outlook for the upcoming fiscal year.

4556|カイノス

2273.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kainos Co., Ltd. reported net sales of ¥5,479 million for the fiscal year ended March 31, 2026 (non-consolidated), marking a 3.3% increase compared to the previous year.

- Operating profit for the period was ¥747 million (down 9.2% year-on-year), ordinary profit was ¥788 million (down 4.8% year-on-year), and net profit was ¥449 million (down 29.9% year-on-year). The decline in net profit was attributed to the recording of tender offer related expenses.

- The annual dividend for the fiscal year ended March 31, 2026, was ¥0. For reference, the annual dividend for the prior fiscal year (ended March 31, 2025) was ¥35.00 per share (¥32.00 ordinary dividend, ¥3.00 commemorative dividend for the 50th anniversary).

- No earnings forecast or dividend forecast has been provided for the fiscal year ending March 31, 2027. This is due to the planned delisting of the company’s shares following a tender offer by Flowers Co., Ltd., as announced in a press release dated February 6, 2026.

- Cash and cash equivalents at the end of the period totaled ¥3.40 billion, an increase of ¥344 million from the end of the previous fiscal year.

🤖 AI Perspective

Kainos’s fiscal year 2026 results show a unique situation with increased revenue but decreased profits, particularly net profit, which was impacted by expenses related to the tender offer. The absence of an earnings or dividend forecast for the upcoming fiscal year, attributed to the planned delisting, indicates a significant transition for the company’s corporate structure and future trajectory. Investors may find it important to consider the implications of this upcoming change in ownership and listing status.

5464|モリ工業

928.0

▼ -1.90%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- MORY Industries reported consolidated results for the fiscal year ended March 2026, with net sales of ¥43,288 million (down 6.2% YoY), operating profit of ¥4,378 million (down 18.9% YoY), ordinary profit of ¥4,879 million (down 14.7% YoY), and net income attributable to owners of parent of ¥3,358 million (down 18.6% YoY).

- Diluted earnings per share for FY2026 March was ¥88.37, and net assets per share were ¥1,540.24.

- The annual dividend for FY2026 March was ¥36.00 (total dividends ¥1,374 million), with a consolidated dividend payout ratio of 40.7%.

- For the fiscal year ending March 2027, the company forecasts consolidated net sales of ¥44,300 million (up 2.3% YoY), operating profit of ¥4,100 million (down 6.4% YoY), ordinary profit of ¥4,600 million (down 5.7% YoY), and net income attributable to owners of parent of ¥3,200 million (down 4.7% YoY).

- The forecast for the annual dividend for FY2027 March is ¥34.00.

- The company implemented a five-for-one stock split of common shares on April 1, 2025; per-share information for the previous fiscal year is calculated assuming this stock split had occurred at the beginning of that period.

🤖 AI Perspective

While MORY Industries concluded FY2026 March with decreased revenue and profit, the FY2027 March consolidated forecast projects an increase in net sales but a decrease in profits. Although the annual dividend is expected to slightly decrease from the previous year’s actual to the current year’s forecast, the company maintains a high equity ratio of 80.5%, which could be a point of stability. The evolution of earnings and dividend policy may be key areas for investors to monitor.

5830|いよぎんHD

2994.5

▼ -4.02%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- **FY2026 Results**: Consolidated ordinary revenue reached ¥266,118 million (up 14.8% YoY), ordinary profit ¥99,206 million (up 32.2% YoY), and net profit attributable to parent company shareholders ¥74,253 million (up 39.3% YoY).

- **Dividends**: The annual dividend for FY2026 has been set at ¥60.00 per share (interim ¥30.00, year-end ¥30.00).

- **FY2027 Forecast**: Consolidated ordinary revenue is projected to be ¥270,000 million (full-year forecast, up 1.5% YoY), ordinary profit ¥111,000 million (up 11.9% YoY), and net profit attributable to parent company shareholders ¥77,000 million (up 3.7% YoY).

- **FY2027 Dividend Forecast**: The company plans an annual dividend of ¥80.00 per share (interim ¥40.00, year-end ¥40.00), representing a ¥20.00 increase per share compared to the previous fiscal year.

- **Financial Position**: As of the end of March 2026, total assets were ¥9,539,812 million, net assets were ¥877,882 million, and the capital adequacy ratio stood at 9.2%.

🤖 AI Perspective

Iyogin HD’s strong performance in FY2026 appears to be driven by increased funding income from rising domestic interest rates and growth in loan balances, alongside gains from securities sales. The reported net profit also benefited from a ¥6.0 billion special gain from a settlement regarding a “system upgrade plan change.” The projected increase in earnings and dividends for FY2027 could signal the company’s commitment to its shareholder return policy outlined in its mid-term management plan.

6085|G-アーキテクツSJ

570.0

▼ -7.32%

📎 Source:G-アーキテクツSJ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Architects Studio Japan Co., Ltd. announced on May 8, 2026, corrections to its “Consolidated Financial Results for the Fiscal Year Ended February 2026 (Japanese GAAP),” originally published on April 17, 2026.

- The primary reason for the corrections was the omission of an increase in treasury stock and a decrease in net assets resulting from odd-lot share purchases during the fiscal year.

- The corrected number of treasury shares at the end of February 2026 increased by 21 shares, from 11,925 shares to 11,946 shares.

- In the consolidated balance sheet, total liabilities at the end of the current consolidated fiscal year increased by 12 thousand yen, from 634,564 thousand yen to 634,576 thousand yen, and total net assets decreased by 13 thousand yen, from △223,168 thousand yen to △223,181 thousand yen.

- In the consolidated cash flow statement, cash flows from operating activities were revised from △656,177 thousand yen to △656,165 thousand yen (a 12 thousand yen change), and cash flows from financing activities were revised from 109,763 thousand yen to 109,751 thousand yen (a 12 thousand yen change).

🤖 AI Perspective

These corrections stem from an oversight in accounting for treasury stock, with the magnitude of the numerical adjustments being relatively minor—21 shares and approximately 12 to 13 thousand yen—suggesting a limited overall impact on the company’s financial statements. While the company notes that the corrections affect multiple sections, the small individual variances indicate that the fundamental integrity of the financial results remains intact. Investors may view this as a routine measure to maintain disclosure accuracy, highlighting the importance of precise information for informed decision-making.

2883|大冷

1975.0

▼ -0.25%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- DAIREI Co., Ltd. announced its non-consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025, to March 31, 2026). Net sales were ¥25,053 million (down 2.6% year-on-year), operating profit was ¥660 million (down 21.5% year-on-year), and ordinary profit was ¥693 million (down 17.9% year-on-year). Net profit for the period was ¥482 million, a swing to profit from a net loss of ¥574 million in the previous fiscal year.

- Regarding the financial position, total assets as of March 31, 2026, were ¥11,313 million, and net assets were ¥8,823 million. The equity ratio improved to 78.0%, an increase of 1.6 percentage points compared to the previous fiscal year.

- Cash flows for the fiscal year showed ¥309 million in cash inflow from operating activities, ¥31 million in cash outflow from investing activities, and ¥468 million in cash outflow from financing activities. Cash and cash equivalents at the end of the period stood at ¥3,577 million.

- The annual dividend for the fiscal year ended March 31, 2026, was ¥60.00 per share (including a year-end dividend of ¥60.00), with total dividends paid amounting to ¥354 million.

- For the fiscal year ending March 31, 2027 (April 1, 2026, to March 31, 2027), the company forecasts net sales of ¥25,200 million (up 0.6% year-on-year), operating profit of ¥780 million (up 18.1% year-on-year), ordinary profit of ¥780 million (up 12.5% year-on-year), and net profit of ¥525 million (up 8.8% year-on-year). The forecasted annual dividend is ¥60.00 per share.

🤖 AI Perspective

For the fiscal year ended March 31, 2026, Dairei reported a decline in revenue and operating/ordinary profit, but notably achieved a net profit of ¥482 million, swinging from a loss in the prior year. This decline in sales and profits may be attributed to a decrease in gross profit margin, driven by increased discounts to cater to consumer demand for lower prices amid rising raw material and energy costs in the domestic food industry. The company’s forecast for the fiscal year ending March 31, 2027, projects an increase in both revenue and profit, suggesting an expectation for improved market conditions or the effectiveness of ongoing business strategies.

3839|ODK

620.0

▼ -0.64%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- ODK’s consolidated financial results for the fiscal year ended March 2026 show net sales of JPY 6,657 million, a 2.9% increase year-on-year, marking a record high for the second consecutive term.

- Ordinary profit increased by 14.3% year-on-year to JPY 659 million.

- Net profit attributable to owners of the parent decreased by 47.0% year-on-year to JPY 139 million.

- The Education business recorded JPY 4,138 million (+5.9% YoY) and the Securities/Hofuri business recorded JPY 1,277 million (+9.7% YoY), showing growth in key segments.

- Intangible assets decreased by JPY 595 million from the previous fiscal year-end to JPY 869 million, primarily due to impairment losses on goodwill from subsidiary shares.

🤖 AI Perspective

The fiscal year 2026/3 results indicate strong performance in sales and ordinary profit, primarily driven by growth in the Education and Securities/Hofuri segments. However, the decline in net profit appears to be influenced by special losses taken from a conservative perspective and impairment of goodwill. Investors may find it worthwhile to monitor the company’s efforts in managing subsidiary performance and the contribution of new business initiatives in future reports.

3946|トーモク

3515.0

▼ -3.30%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 2026, Tomoku reported consolidated net sales of ¥224,090 million (up 2.0% year-on-year), operating profit of ¥11,378 million (up 21.6%), ordinary profit of ¥11,445 million (up 21.7%), and net income attributable to owners of parent of ¥7,361 million (up 13.1%).

- The annual dividend per share for FY2026 was ¥130, an increase of ¥30 from ¥100 in the previous fiscal year.

- For the fiscal year ending March 2027, the company forecasts consolidated net sales of ¥220,500 million (down 1.6% year-on-year), operating profit of ¥12,700 million (up 11.6%), ordinary profit of ¥11,900 million (up 4.0%), and net income attributable to owners of parent of ¥8,100 million (up 10.0%).

- The projected annual dividend per share for FY2027 is ¥170, representing an increase of ¥40 from the previous fiscal year’s actual dividend.

- During the fiscal year, Niei Shikoh Co., Ltd. and Enshu Shikoh Co., Ltd. were newly included in the scope of consolidation, while Sweden House Reform Co., Ltd. was excluded.

🤖 AI Perspective

The consolidated results for FY2026, showing double-digit profit growth despite a modest increase in net sales, may suggest an improvement in profitability. The consistent increase in the annual dividend, both for the past fiscal year and projected for the next, indicates a potentially proactive stance on shareholder returns. While the FY2027 forecast anticipates a decrease in net sales, the projected profit growth could imply ongoing efforts in business restructuring and cost efficiency.

4417|G-グローバルセキュ

2889.0

▲ +4.00%

📎 Source:G-グローバルセキュ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Global Security Experts Inc. (GSX) announced on May 8, 2026, a business alliance with CoWorker Co., Ltd. concerning AI and cybersecurity.

- The alliance aims to accelerate GSX’s stated ‘Growth Strategy in the Age of AI’ and achieve further growth for the group in the AI era.

- CoWorker Co., Ltd. specializes in IT consulting and service development focused on AI and security, offering system development, IT consulting/AI development consulting, and cybersecurity services.

- GSX’s ‘Growth Strategy in the Age of AI’ defines three evolutions: “Leaner Existing Businesses” (efficiency/price competitiveness via AI), “Acquisition of New Value in Cybersecurity” (new AI-driven services), and “New Market Development” (AI market implementation with security expertise).

- The impact of this alliance on GSX’s financial performance for the fiscal year ending March 2027 is currently under review.

🤖 AI Perspective

This business alliance appears to be a strategic move for Global Security Experts to accelerate and solidify its ‘Growth Strategy in the Age of AI,’ indicating a clear focus on integrating AI into its core cybersecurity offerings. The partnership with CoWorker, a specialist in AI and security, could significantly enhance GSX’s capabilities in developing new services and expanding into AI-driven markets. Investors may find it worthwhile to monitor the specifics of future service rollouts and the eventual financial impact, which GSX has stated is currently under review.

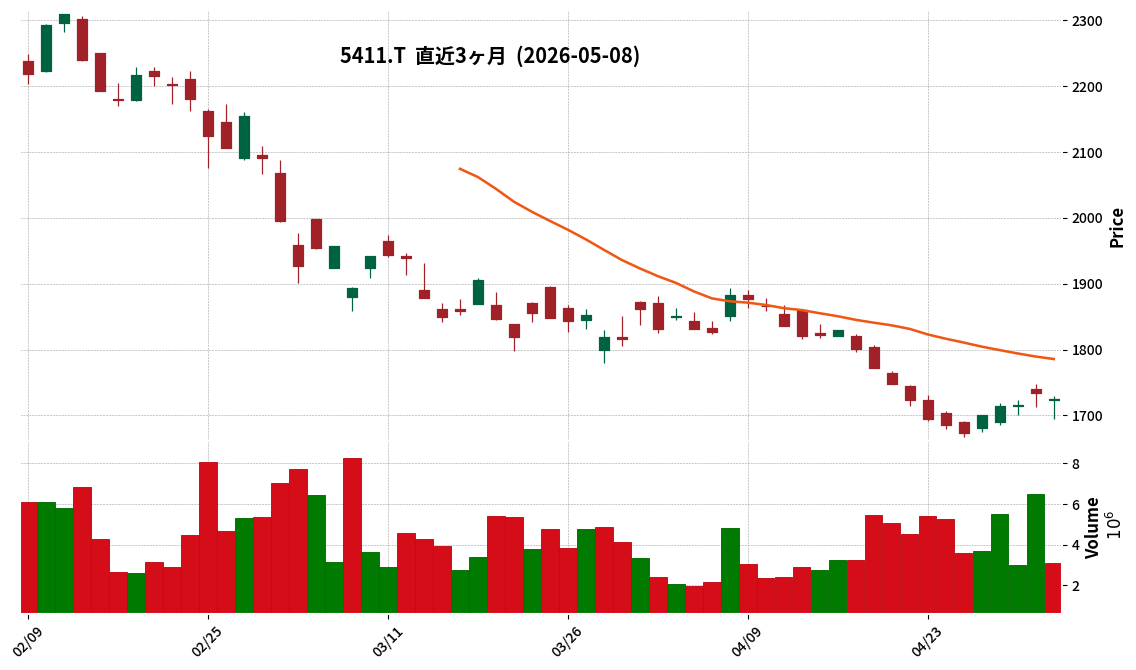

5411|JFE

1725.5

▼ -0.52%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- JFE Holdings announced its consolidated financial results for the fiscal year ended March 31, 2026.

- The business environment for the steel segment was recognized as challenging due to the slump in electric furnace steel product markets, sluggish demand for domestic construction and industrial machinery, and an adjusting overseas steel market, despite robust demand from the automotive sector.

- The company noted persistent high resource and electricity prices, leading to increased production costs from rising energy prices. Conversely, the yen’s depreciation contributed to improved export profitability but also resulted in higher imported raw material costs.

- The engineering segment and the trading house segment performed robustly.

- The year-end dividend forecast for the fiscal year ended March 31, 2026, has been declared as “undecided.”

🤖 AI Perspective

JFE Holdings’ qualitative assessment for the fiscal year ended March 31, 2026, highlights the challenging business environment for its core steel segment, potentially indicating ongoing pressures on the company’s profitability. The robust performance of the engineering and trading house segments, however, may suggest the benefits of diversified business operations in mitigating some of these challenges. Investors might focus on how the company plans to navigate persistent high resource costs and foreign exchange fluctuations in the upcoming periods.

6326|クボタ

2695.5

▼ -0.17%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kubota Corporation announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026 – March 31, 2026).

- For Q1 FY2026, consolidated net sales reached ¥810,012 million, marking a 13.7% increase year-on-year, while operating profit rose 59.1% to ¥98,042 million.

- Profit attributable to owners of the parent was ¥73,285 million (up 77.2% year-on-year), and basic earnings per share were ¥64.45.

- By segment, the Machinery segment reported sales of ¥700,800 million (up 14.9% year-on-year) and segment profit of ¥79,700 million (up 45.0% year-on-year). The Water & Environment segment recorded sales of ¥105,200 million (up 6.5% year-on-year) and segment profit of ¥14,300 million (up 6.9% year-on-year).

- The consolidated full-year earnings forecast for fiscal year 2026 and the annual dividend forecast of ¥52.00 remain unchanged from the most recently published figures.

🤖 AI Perspective

Kubota’s Q1 FY2026 results show a significant year-on-year increase in net sales and various profit metrics, suggesting a strong start to the fiscal year. The Machinery segment appears to be a key driver of this growth, with improved foreign exchange rates, increased sales volume, and price revisions contributing to profitability. While the full-year outlook remains unchanged, the strong Q1 performance may indicate positive momentum worth monitoring.

6340|渋谷工

3590.0

▼ -1.24%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

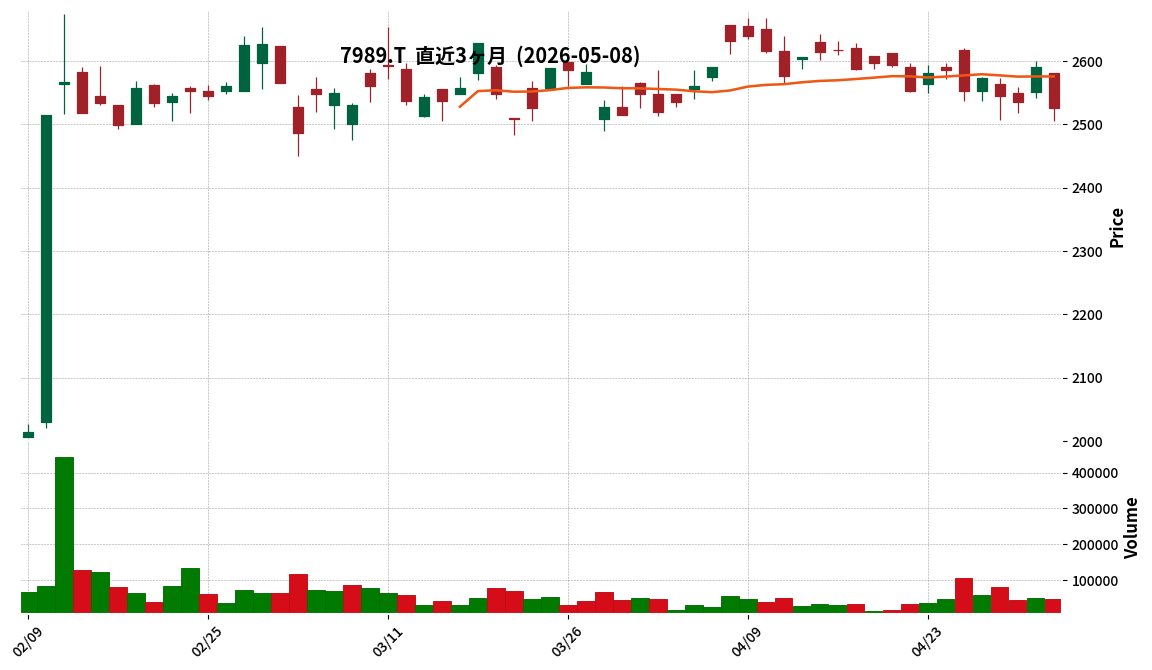

7989|立川ブライ

2525.0

▼ -2.51%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tachikawa Blind Industry Co., Ltd. announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1 to March 31, 2026).

- For the quarter, consolidated net sales were ¥11,353 million, an 8.0% increase year-on-year. Operating profit rose by 17.3% to ¥1,566 million, ordinary profit increased by 18.5% to ¥1,604 million, and profit attributable to owners of parent grew by 0.1% to ¥1,064 million.

- By segment, the Parking System Related Business recorded significant growth, with sales of ¥1,101 million (up 82.7% year-on-year) and operating profit of ¥209 million (up 105.6% year-on-year). The Reducer Related Business also showed substantial increases, with sales of ¥838 million (up 19.5% year-on-year) and operating profit of ¥51 million (up 742.5% year-on-year).

- In terms of consolidated financial position, total assets stood at ¥67,171 million and net assets at ¥56,682 million, resulting in an equity ratio of 84.4%, an increase of 1.2 percentage points from the end of the previous fiscal year.

- The consolidated full-year earnings forecast for December 2026 and the annual dividend forecast of ¥120.00 remain unchanged from the most recently announced figures.

🤖 AI Perspective

Tachikawa Blind Industry’s first-quarter results for the fiscal year ending December 2026 indicate a strong start, with increases in net sales, operating profit, and ordinary profit. The Parking System Related Business and Reducer Related Business appear to be key drivers of this performance, demonstrating significant growth in both sales and operating profit. Furthermore, the high equity ratio suggests the company maintains a stable financial foundation.

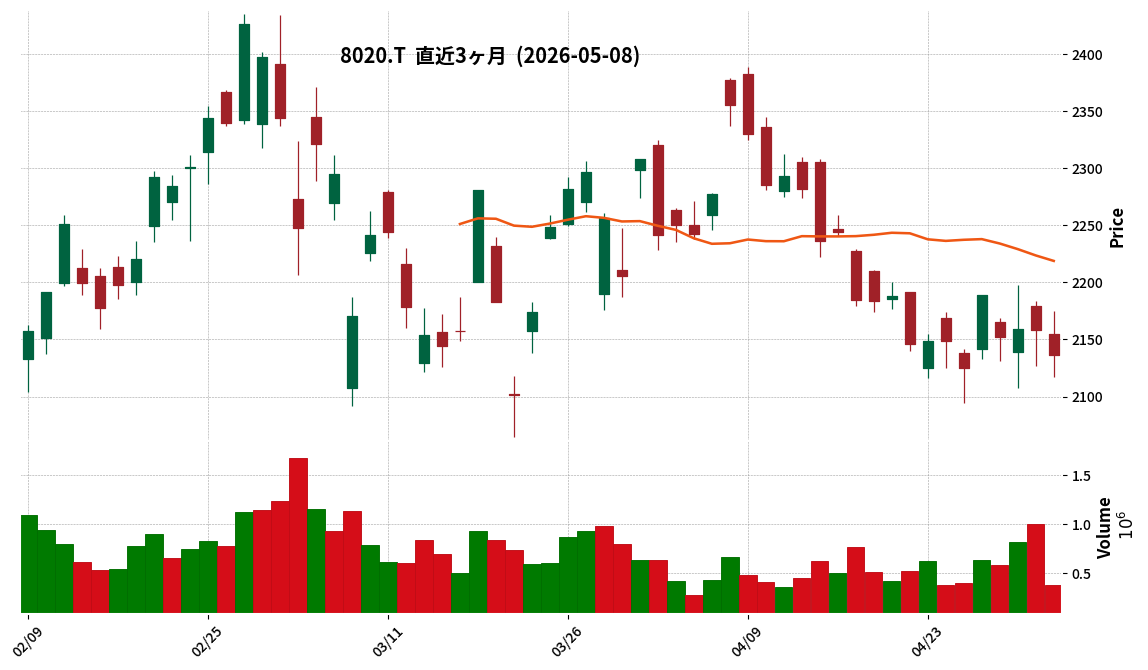

8020|兼松

2136.0

▼ -1.04%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kanematsu Corporation resolved to revise its year-end dividend forecast for the fiscal year ending March 2026 at a Board of Directors meeting held on May 8, 2026.

- The revised year-end dividend forecast for the fiscal year ending March 2026 is ¥34.25 per share (post-stock split), an increase of ¥3 from the previous forecast.

- Consequently, the total annual dividend per share for the fiscal year ending March 2026 is expected to be ¥63.00 (post-stock split), or ¥126.00 (pre-stock split).

- The revision is attributed to the company’s performance for the fiscal year ending March 2026 exceeding its initial outlook.

- The company conducted a 2-for-1 stock split of its common shares effective January 1, 2026.

🤖 AI Perspective

Kanematsu’s revision to its year-end dividend forecast likely reflects a strong commitment to shareholder returns and robust business performance. This move appears consistent with the progressive dividend policy and the 30-35% dividend payout ratio target outlined in its medium-term management plan. The clarification of post-stock split dividend amounts may offer investors valuable insight for their future investment decisions.

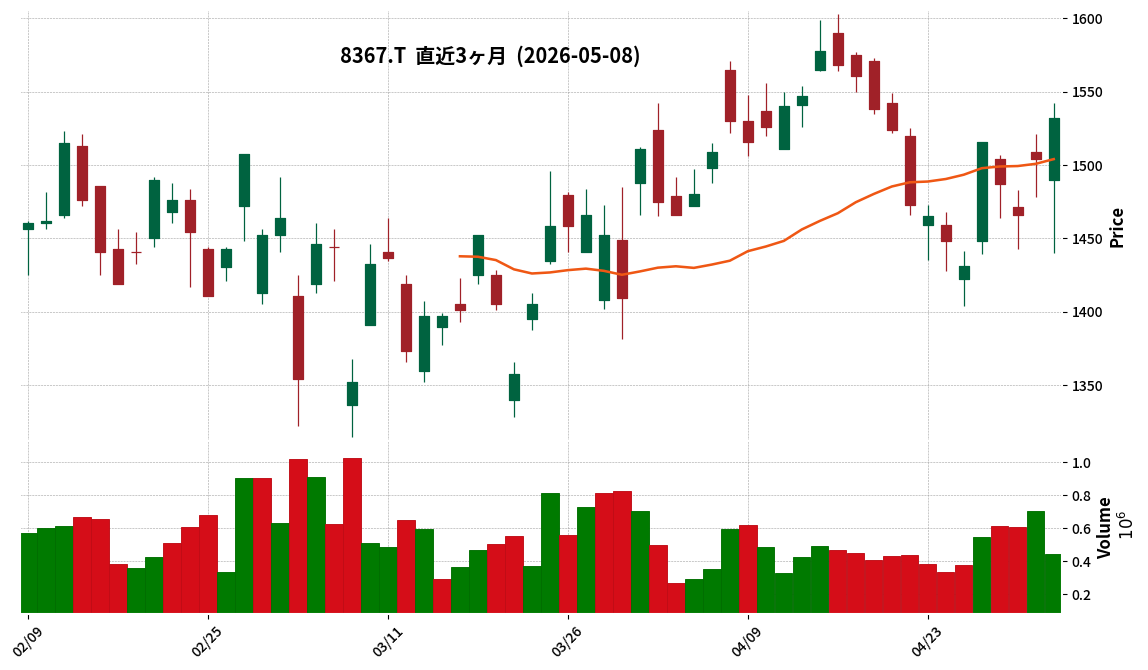

8367|南都銀

1532.0

▲ +1.86%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nanto Bank Co., Ltd. announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 to March 31, 2026).

- Consolidated ordinary revenues for FY2026/3 increased by 12.2% to JPY 115,665 million, ordinary profit rose by 26.1% to JPY 24,820 million, and profit attributable to owners of parent grew by 26.2% to JPY 17,062 million.

- The annual dividend for FY2026/3 was declared at JPY 215.00 per share, an increase of JPY 45.00 from the previous fiscal year.

- For the fiscal year ending March 31, 2027 (FY2027/3), Nanto Bank forecasts consolidated ordinary profit to be JPY 32,500 million (a 30.9% increase year-on-year) and profit attributable to owners of parent to be JPY 22,000 million (a 28.9% increase year-on-year).

- The company implemented a 5-for-1 stock split effective April 1, 2026.

🤖 AI Perspective

Nanto Bank’s FY2026/3 results show significant growth across key revenue and profit metrics, coupled with an increased dividend. The positive outlook for FY2027/3, projecting continued profit growth, may suggest a strong business trajectory. The recently implemented stock split could be viewed as a strategy to reduce the per-share investment amount, potentially aiming to enhance stock liquidity and broaden investor accessibility.

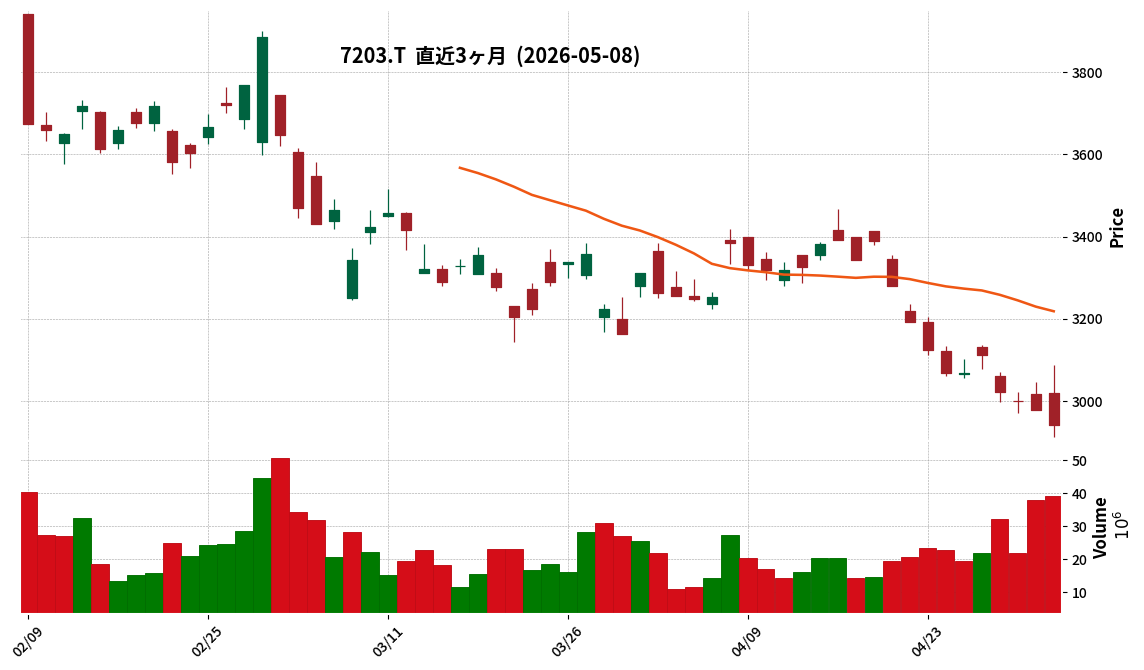

7203|トヨタ自

2942.0

▼ -1.21%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, Toyota Motor Corporation reported consolidated operating revenue of JPY 50,684,952 million, a 5.5% increase year-on-year.

- Consolidated operating profit for FY2026/3 decreased by 21.5% to JPY 3,766,216 million, and profit attributable to owners of the parent decreased by 19.2% to JPY 3,848,098 million.

- The full-year dividend for FY2026/3 was JPY 95.00 per share, an increase of JPY 5.00 from the prior fiscal year.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated operating revenue of JPY 51,000,000 million (up 0.6% year-on-year), operating profit of JPY 3,000,000 million (down 20.3%), and profit attributable to owners of the parent of JPY 3,000,000 million (down 22.0%).

- A full-year dividend of JPY 100.00 per share is forecasted for FY2027/3.

- U.S. tariff policies had a JPY 1,380 billion negative impact on operating profit for FY2026/3.

🤖 AI Perspective

While operating revenue showed growth, the notable declines in operating profit and profit attributable to owners of the parent for FY2026/3 may suggest a challenging profitability environment. Despite the projected profit contraction for FY2027/3, the company’s decision to increase the full-year dividend for FY2026/3 and forecast a further increase for FY2027/3 could indicate a consistent commitment to shareholder returns. The significant JPY 1,380 billion impact from U.S. tariff policies highlights the influence of external factors on the company’s financial performance.

6062|チャームケア

1313.0

▲ +1.47%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the nine months ended March 31, 2026 (FY2026 Q3 cumulative period), Charm Care reported consolidated net sales of ¥33,893 million (up 11.8% year-on-year), operating profit of ¥3,603 million (up 43.9%), and net income attributable to owners of the parent of ¥2,560 million (up 39.0%).

- Diluted earnings per share for the period were ¥78.37.

- The full-year consolidated earnings forecast for FY2026 remains unchanged from the most recently announced projections, with net sales of ¥48,585 million, operating profit of ¥4,460 million, and net income attributable to owners of the parent of ¥3,090 million.

- The annual dividend forecast for FY2026 totals ¥37.00 per share, comprising an interim dividend of ¥20.00 (including a ¥3 special commemorative dividend) and a projected year-end dividend of ¥17.00, with no revisions from the latest forecast.

- The company’s performance overview states that robust performance in the nursing care business and improved productivity were key drivers for the expanded revenue and profit.

🤖 AI Perspective

Charm Care achieved significant revenue and profit increases during the third quarter cumulative period, primarily driven by the solid performance of its nursing care business and enhanced productivity. The company has implemented human resource strategies, including improving employee compensation, expanding work-style options, and shifting to an OJT-focused training system, which appear to be contributing to its business growth. The unchanged full-year earnings and annual dividend forecasts suggest that current business strategies are progressing as planned.

9359|伊勢湾海

—

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Isewan Terminal Service Co. resolved a dividend of surplus (special dividend) for the fiscal year ended March 31, 2026, at its Board of Directors meeting on May 8, 2026.

- The year-end dividend for the fiscal year ending March 31, 2026, will be JPY 24.00 per share, consisting of an ordinary dividend of JPY 13.00 and a special dividend of JPY 11.00.

- This decision results in an annual dividend of JPY 37.00 per share for the fiscal year ending March 31, 2026, including the interim dividend of JPY 13.00.

- The total dividend amount is JPY 612 million, with an effective date of June 29, 2026.

- This matter is scheduled to be proposed at the 103rd Ordinary General Meeting of Shareholders on June 26, 2026.

🤖 AI Perspective

- The implementation of a special dividend may suggest the company’s commitment to shareholder returns.

- This decision results in an increased annual dividend for the fiscal year ending March 31, 2026, compared to the previous fiscal year (JPY 29.00), which could be a point of interest for investors.

- The company’s statement of considering “current consolidated business performance” for the special dividend might indicate strong recent financial results.

1899|福田組

8390.0

▼ -2.33%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Fukuda Corp. announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (January 1, 2026 – March 31, 2026).

- For the cumulative first quarter, net sales reached ¥41.864 billion, an increase of 4.0% year-on-year. Operating profit rose by 26.4% to ¥2.873 billion, ordinary profit increased by 26.6% to ¥3.001 billion, and profit attributable to owners of parent grew by 30.6% to ¥2.008 billion.

- Basic earnings per share for the quarter stood at ¥242.55.

- The company plans a 2-for-1 stock split of its common shares, effective July 1, 2026. Consequently, the annual dividend forecast for the fiscal year ending December 2026 has been revised to ¥130.00 per share (post-split).

- The full-year consolidated earnings forecast for the fiscal year ending December 2026 remains unchanged, projecting net sales of ¥175.600 billion (up 4.5% year-on-year), operating profit of ¥7.600 billion (down 2.2%), and profit attributable to owners of parent of ¥5.000 billion (down 9.9%).

🤖 AI Perspective

- Fukuda Corp. achieved strong first-quarter results for FY2026, with significant year-on-year increases in sales and all profit categories, suggesting a robust start to the fiscal year.

- The concurrent announcement of a stock split, effective July 1, 2026, may aim to lower the price per investment unit, potentially broadening the company’s investor base.

- Despite the strong Q1 performance, the full-year consolidated earnings forecast remains unchanged, which anticipates a decline in operating and net profits compared to the previous fiscal year, a point that investors might monitor as the year progresses.

2461|ファンコミ

455.0

▲ +0.89%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- FUNCOM Corporation announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 on May 8, 2026, covering the period from January 1 to March 31, 2026.

- Consolidated performance showed net sales of ¥1,733 million (down 6.6% year-on-year), operating profit of ¥273 million (down 53.9% year-on-year), ordinary profit of ¥225 million (down 60.1% year-on-year), and quarterly net profit attributable to parent company shareholders of ¥108 million (down 72.3% year-on-year).

- In the CPA Solutions segment, net sales decreased by 16.8% year-on-year to ¥1,280 million, with segment profit down 18.9% year-on-year to ¥847 million. This was attributed to a decrease in active advertisers and lower commission rates for “A8.net.”

- The Strategic Business segment recorded a 42.8% year-on-year increase in net sales to ¥452 million, but the segment loss expanded to ¥253 million (compared to a loss of ¥154 million in the prior year’s first quarter) due to upfront investments, such as advertising expenses, outpacing sales growth.

- The consolidated full-year earnings forecast for the fiscal year ending December 2026 and the annual dividend forecast of ¥21.00 per share remain unchanged from the previously announced figures.

🤖 AI Perspective

- The first quarter results indicate a year-on-year decline across key consolidated financial metrics, including sales and various profit indicators.

- While the core CPA Solutions business experienced a revenue decline affecting overall profits, the company continues its upfront investments in the Strategic Business segment, which saw increased sales but expanded losses.

- Structural changes in the digital marketing market, such as shifts in user search behavior due to the proliferation of generative AI, are noted, suggesting that the company’s response to these environmental changes and the progress of its strategic business monetization will be worth monitoring.

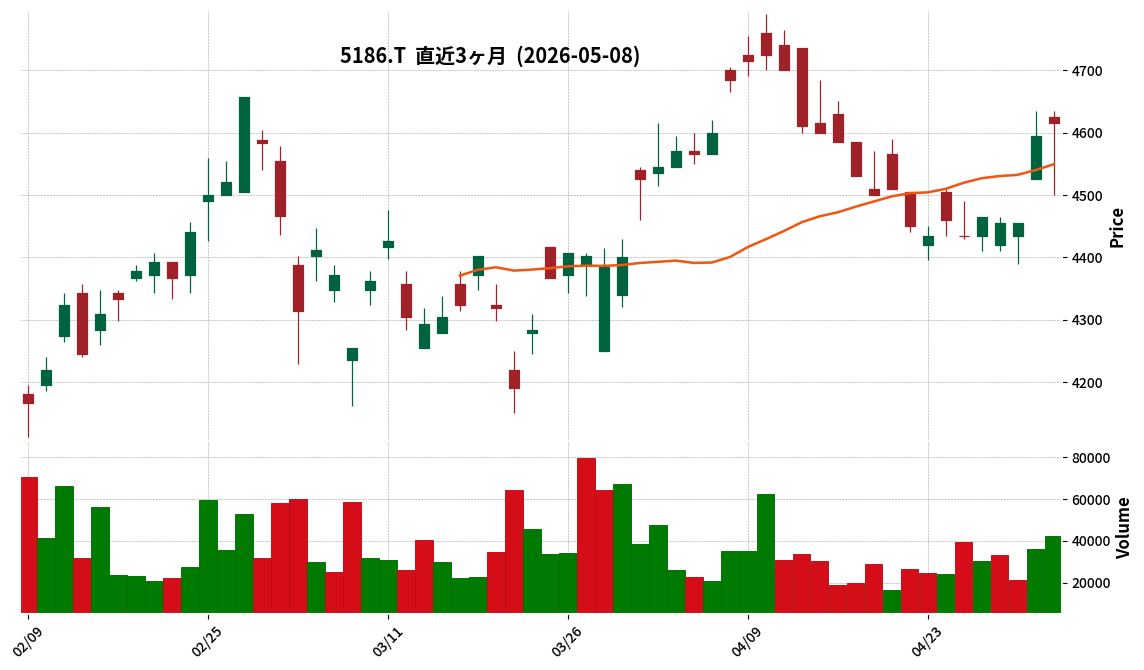

5186|ニッタ

4615.0

▲ +0.44%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nitta has decided on a year-end dividend of JPY 88.00 per share for the surplus dividend with a record date of March 31, 2026.

- This represents an increase of JPY 15 from the most recent dividend forecast of JPY 73.00, which was announced on May 9, 2025.

- Consequently, the annual dividend per share for the fiscal year ending March 2026 is projected to be JPY 160, including an interim dividend of JPY 72.

- This annual dividend of JPY 160 constitutes an increase of JPY 25 compared to the ordinary dividend of JPY 135 for the previous fiscal year (excluding the JPY 5 commemorative dividend for the company’s 140th anniversary).

- The dividend increase is based on the company’s policy to steadily increase dividends (by at least JPY 10 per share annually) during the mid-to-long-term management plan ‘SHIFT2030’ Phase 2 period (FY2024-FY2028), aiming for a consolidated payout ratio of 30% or more and a DOE (Dividend on Equity) of 2.5% or more.

🤖 AI Perspective