📌 Today’s Highlights

Today we cover 47 IR announcements. Notable among them: リケンテクノス (4220), 東急建設 (1720), クラスターT (4240). Use the table of contents below to navigate to each company.

- 4220|リケンテクノス

- 1720|東急建設

- 4240|クラスターT

- 8219|青山商

- 3798|ULSグループ

- 8887|シーラHD

- 6294|オカダアイヨン

- 1332|ニッスイ

- 5966|京都機械工具

- 3066|JBイレブン

- 3708|特種東海

- 5852|アーレスティ

- 6262|PEGASUS

- 2340|極楽湯HD

- 3673|ブロドリーフ

- 3753|フライト

- 3918|PCIHD

- 421A|G-ムービン

- 4237|フジプレアム

- 4882|G-ペルセウス

- 6050|Eガーディアン

- 7111|INEST

- 7409|G-AeroEdge

- 7481|尾家産

- 8725|MS&AD

- 2292|S FOODS

- 9564|FCE

- 2937|G-サンクゼール

- 4720|城南進研

- 5247|G-BTM

- 6576|P-揚工舎

- 6616|トレックスセミ

- 6743|大同信号

- 8616|東海東京

- 8766|東京海上

- 5891|魁力屋

- 4755|楽天グループ

- 8411|みずほ

- 8630|SOMPOHD

- 369A|G-エータイ

- 3768|リスクモンスター

- 5994|ファインシンター

- 6343|フリージアマク

- 1443|技研ホールディングス

- 8897|ミラースHD

- 2673|夢みつけ隊

- 8771|Eギャランティ

4220|リケンテクノス

1610.0

▼ -1.83%

📎 Source:リケンテクノス Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- RIKEN TECHNOS’ consolidated results for the fiscal year ended March 2026 showed net sales of ¥131,377 million (up 2.5% year-on-year), operating profit of ¥11,408 million (up 8.8% year-on-year), ordinary profit of ¥11,786 million (up 11.3% year-on-year), and net profit attributable to owners of parent of ¥7,569 million (up 2.7% year-on-year).

- Net sales and all profit stages reached record highs for the fifth consecutive fiscal year.

- Segment-wise sales were: Transportation ¥42.8 billion (32.6% of total), Electronics ¥36.4 billion (27.8%), Daily Life & Healthcare ¥25.6 billion (19.6%), and Building & Construction ¥26.3 billion (20.0%).

- Geographically, sales were: Japan ¥65.1 billion (49.6%), Asia ¥44.9 billion (34.2%), and North America ¥20.9 billion (15.9%), with overseas sales accounting for 50.4%.

- The consolidated earnings forecast for the fiscal year ending March 2027 is net sales of ¥142,000 million (up 8.1% year-on-year), operating profit of ¥12,000 million (up 5.2% year-on-year), ordinary profit of ¥12,000 million (up 1.8% year-on-year), and net profit attributable to owners of parent of ¥6,800 million (down 10.2% year-on-year). The projected decrease in net profit reflects the impact of the gain on sale of investment securities (¥782 million) recorded in FY2026.

🤖 AI Perspective

RIKEN TECHNOS has demonstrated consistent growth, achieving record-high sales and profits for the fifth consecutive year in FY2026. The strong performance across segments like Transportation and Electronics, coupled with over 50% overseas sales, suggests a robust global presence. While operating profit is forecast to grow in FY2027, the anticipated decline in net profit due to the absence of investment securities sale gains from the previous year is a point investors may want to monitor.

1720|東急建設

1185.0

▼ -3.58%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tokyu Construction announced consolidated net sales of 341.1 billion JPY (up 16.4% year-on-year) for the fiscal year ended March 2026, marking a new record high.

- Consolidated operating profit reached 16.3 billion JPY (up 84.5% year-on-year), and net profit attributable to parent company shareholders was 13.3 billion JPY (up 101.9% year-on-year).

- Individual order backlog was 408.9 billion JPY (up 7.3% year-on-year), also a new record high for the second consecutive year.

- Koji Hisada, currently Corporate Officer and General Manager of Operations, is slated to assume the position of Representative Director, President and Executive Officer, subject to approval at the Ordinary General Meeting of Shareholders scheduled for late June 2026.

- The company plans to transition to a company with an audit and supervisory committee, pending shareholder approval, to enhance board independence and oversight functions.

🤖 AI Perspective

Tokyu Construction’s FY2026/3 financial results demonstrate significant growth in both net sales and operating profit, achieving a record-high revenue, which may suggest the effectiveness of its ongoing management reforms. The planned appointment of a new President and the transition to a company with an audit and supervisory committee could indicate a proactive stance towards strengthening corporate governance and operational efficiency. The company’s focus on profitability in order intake appears to be a key driver for these positive results amid a robust domestic construction market.

4240|クラスターT

317.0

▼ -3.35%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Cluster T (Securities Code: 4240) released materials on May 20, 2026, detailing its financial results briefing for the fiscal year ended March 2026 (35th term) and its earnings forecast for the fiscal year ending March 2027 (36th term).

- The company’s primary business activities include the development and manufacturing of resin composite materials, functional resin molded products, mold production, and the assembly of devices including molded products.

- The business is largely divided into “Nano/Micro-Technology Related Business” and “Macro-Technology Related Business,” which respectively handle functional precision molded products, pulse injectors, and resin molded insulators.

- Historically, the company transitioned to the Growth Market following the reorganization of the Tokyo Stock Exchange in 2022 and subsequently changed its listing market segment to the Standard Market of the Tokyo Stock Exchange in 2026.

- In the imaging equipment industry, while total digital camera shipments declined from 35,395 thousand units in 2015 to 7,721 thousand units in 2023, mirrorless cameras have continued to grow and are projected to account for approximately 67% of total digital camera shipments by 2025.

🤖 AI Perspective

Cluster T’s announcement provides clarity on its past performance, future outlook, and business structure, which may be crucial for investors to understand the company’s current status and growth strategies. The company’s response to changing market environments and its transition in listing market segments could indicate a dynamic management strategy. The upcoming earnings forecast and progress of its medium-term management plan are worth monitoring for assessing the company’s growth potential.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

8219|青山商

714.0

▼ -0.28%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Aoyama Trading Co., Ltd. reported consolidated results for the fiscal year ended March 2026, with net sales of ¥189.0 billion, gross profit of ¥98.1 billion, operating profit of ¥10.5 billion, ordinary profit of ¥10.9 billion, and net profit of ¥6.9 billion.

- Compared to the previous fiscal year, net sales decreased by ¥6.7 billion (▲3.4%), operating profit by ¥1.9 billion (▲15.2%), and net profit by ¥2.4 billion (▲25.8%).

- By segment, the Business Wear segment recorded net sales of ¥124.2 billion (down ¥8.8 billion year-on-year) and operating profit of ¥5.1 billion (down ¥3.1 billion year-on-year), showing decreases in both revenue and profit.

- Conversely, the Card segment, Comprehensive Repair Service segment, and Franchisee segment all reported year-on-year increases in both net sales and operating profit.

- The consolidated earnings forecast for the fiscal year ending March 2027 projects net sales of ¥194.7 billion (up 3.0% year-on-year), operating profit of ¥11.7 billion (up 10.5% year-on-year), and net profit of ¥7.6 billion (up 9.9% year-on-year).

🤖 AI Perspective

Aoyama Trading’s FY2026 results indicate that while the group as a whole made progress in improving gross profit margins and controlling selling, general, and administrative expenses, the struggles within the core Business Wear segment significantly impacted consolidated performance. However, several diversified group businesses, including the Card, Comprehensive Repair Service, and Franchisee segments, demonstrated robust growth, suggesting a successful diversification of its business portfolio. Achieving the projected sales and profit increases for the upcoming fiscal year will likely depend on the recovery of the Business Wear segment and continued strong contributions from these growing group businesses.

3798|ULSグループ

494.0

▼ -3.33%

📎 Source:ULSグループ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- ULS Group’s consolidated net sales for the fiscal year ended March 2026 reached ¥16.6 billion, representing a 25.7% increase year-on-year and marking a record high for the ninth consecutive year.

- Consolidated ordinary profit was ¥3.063 billion, a 16.1% increase year-on-year, setting a new record for the 14th consecutive year.

- Net profit attributable to owners of the parent company amounted to ¥2.027 billion, an increase of 23.9% year-on-year.

- For the fiscal year ending March 2027, the company forecasts consolidated net sales of ¥20.2 billion (a 21.7% increase YoY) and ordinary profit of ¥3.7 billion (a 20.8% increase YoY).

- The planned dividend per share for FY2027 is ¥8.20, with a guideline for the consolidated dividend payout ratio set between 20% and 30%.

🤖 AI Perspective

ULS Group’s financial results for FY2026 demonstrate consistent growth, with both net sales and ordinary profit achieving record highs for multiple consecutive years. The company’s continued investment in human capital, evident in the net increase in consultants, and strategic initiatives such as the adoption of “Devin” for AI-driven development, appear to be key drivers. As the company projects further revenue and profit growth for FY2027, the impact of these growth investments and the expansion of high-value-added services on future performance may be worth monitoring.

8887|シーラHD

353.0

▼ -1.94%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SHEILA Holdings Co., Ltd. has revised its consolidated financial forecast for the full year ending May 2026.

- Net sales are revised upwards from ¥34,500 million to ¥39,000 million (+13.0%), operating profit from ¥2,413 million to ¥3,050 million (+26.4%), and ordinary profit from ¥1,350 million to ¥2,000 million (+48.1%).

- Profit attributable to owners of parent remains unchanged at ¥6,513 million, consistent with the previous forecast.

- The revision is attributed to the steady progress in sales of new condominiums and the unscheduled sale of multiple properties, leading to higher-than-expected sales and profits.

- The year-end dividend forecast has been increased by ¥1.00 from the previously announced ¥6.00 (¥5.00 ordinary, ¥1.00 commemorative) to ¥7.00 (¥6.00 ordinary, ¥1.00 commemorative). The total annual dividend will be ¥13.00.

🤖 AI Perspective

SHEILA HD’s revised earnings forecast is notable for the significant upward adjustments in net sales, operating profit, and ordinary profit. This suggests strong operational execution, driven by on-plan sales of new condominiums and additional unexpected property sales. While profit attributable to owners of parent remains unchanged due to special losses from the liquidation of consolidated subsidiaries and asset impairments, this is identified as a one-time factor. The increased year-end dividend, following the upward revision of the earnings forecast, could be viewed positively by investors as an indication of the company’s commitment to shareholder returns.

6294|オカダアイヨン

1960.0

▼ -1.85%

📎 Source:オカダアイヨン Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Okada Aiyon Corporation announced its consolidated financial results for the fiscal year ended March 2026, with net sales reaching ¥26,991 million, a 1.5% increase year-on-year.

- Operating income for the period was ¥2,261 million (down 0.8% year-on-year), while ordinary income increased by 4.7% to ¥2,343 million and net profit by 1.1% to ¥1,491 million.

- Concurrently, the company unveiled its new mid-term management plan, “Onyx,” covering the fiscal years 2026 to 2028.

- For the fiscal year ending March 2027, the company forecasts consolidated net sales of ¥28,500 million (up 5.6%), operating income of ¥2,500 million (up 10.6%), and net profit of ¥1,700 million (up 14.0%).

- Overseas segment sales reached ¥6,326 million (up 5.8% year-on-year), with notable growth in the European region (+11.9%) and Asian region (+40.3%).

🤖 AI Perspective

The FY2026/3 results indicate Okada Aiyon’s ability to maintain stable profitability with increased top-line and bottom-line figures, despite a slight decline in operating income. This decline was primarily attributed to rental equipment write-downs and increased costs due to tariffs in overseas markets, which were partially offset by improved profitability from domestic pricing adjustments. The newly introduced “Onyx” mid-term management plan and the ambitious FY227/3 guidance could signal the company’s confidence in its future growth trajectory and strategic initiatives.

1332|ニッスイ

1326.0

▼ -2.64%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nissui Corporation announced on May 20, 2026, a correction to its “Consolidated Financial Results for the Fiscal Year Ending March 31, 2026 (Japanese GAAP) (Consolidated)” which was originally published on May 14, 2026.

- The reason for the correction was the discovery of errors in the description after the initial release.

- In the “Summary Information” section, specifically under “Significant changes in the scope of consolidation during the fiscal year,” the number of “newly” consolidated subsidiaries was corrected from “2 companies” to “1 company.” The name “CULTIVOS YADRAN S.A.” was removed.

- On page 16 of the attached materials, within “Notes to Consolidated Financial Statements (Business Combinations, etc.),” the description regarding specified subsidiaries under “Business combinations by acquisition of shares” was corrected from “PY社 and its subsidiary CULTIVOS YADRAN S.A. are classified as specified subsidiaries of our company” to “PY社 is classified as a specified subsidiary of our company.”

🤖 AI Perspective

This correction primarily concerns the precise number of consolidated subsidiaries and the designation of a specified subsidiary, rather than a significant alteration of the reported financial figures themselves. For investors, the accurate disclosure of information regarding the scope of consolidation and business combinations provides a clearer understanding of the company’s structure. While such corrections are sometimes necessary, the circumstances that led to the initial inaccuracy may be worth monitoring as they relate to the company’s internal disclosure processes.

5966|京都機械工具

2451.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kyoto Tool Co., Ltd. has entered into merger agreements with its wholly-owned subsidiaries, Hokuriku KTC Co., Ltd. and HI-TOOL Co., Ltd.

- The merger will be an absorption-type merger, with Kyoto Tool as the surviving company and Hokuriku KTC and HI-TOOL as the absorbed companies.

- The Board of Directors resolved and signed the merger agreements on May 20, 2026.

- The shareholder meeting resolution is scheduled for June 26, 2026, and the effective date of the merger is planned for October 1, 2026.

- As this is a merger with wholly-owned subsidiaries, the impact on Kyoto Tool’s consolidated business performance is stated to be minor.

🤖 AI Perspective

This announcement confirms the formalization of the merger agreements, following previous disclosures regarding the absorption merger of wholly-owned subsidiaries. Mergers involving wholly-owned subsidiaries often aim to streamline group operations and enhance overall business efficiency. The statement that the impact on consolidated performance will be minor suggests that this integration is likely an internal restructuring within the existing business framework.

3066|JBイレブン

—

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- JB Eleven announced an absorption-type merger between its wholly-owned subsidiaries, 55style Co., Ltd. and JB Symphony Co., Ltd.

- 55style will be the surviving company, and JB Symphony will be the absorbed company in this merger.

- The purpose of the merger is to integrate overlapping operational foundations and management know-how in the food and beverage and franchise-related businesses of both companies, aiming to improve organizational efficiency and strengthen profitability.

- The effective date of the merger is scheduled for July 1, 2026.

- Following the merger, there will be a change in the representative director positions at 55style, with Ryuichiro Sawa becoming Representative Director and Chairman, and Kyo Niimi becoming Representative Director and President.

- JB Eleven states that the impact of this merger on its consolidated financial performance is minor, as it is between wholly-owned subsidiaries.

🤖 AI Perspective

JB Eleven’s announced merger between its wholly-owned subsidiaries appears to be a strategic move aimed at optimizing internal operations and bolstering profitability within its F&B and franchise segments. This restructuring could lead to enhanced operational efficiency by consolidating redundant functions and streamlining management. While the immediate impact on consolidated earnings is stated as minor, the long-term potential for improved group synergy and resource allocation may be worth monitoring.

3708|特種東海

1649.0

▼ -0.72%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 2026, Tokushu Tokai reported consolidated net sales of ¥95,413 million (+0.6% YoY), operating profit of ¥4,296 million (+9.4% YoY), ordinary profit of ¥5,728 million (-8.0% YoY), and net profit of ¥4,368 million (+21.1% YoY).

- Net sales, operating profit, ordinary profit, and net profit for FY2026/3 all fell short of initial forecasts, with achievement rates of 96.4%, 85.9%, 81.8%, and 89.1% respectively.

- The annual dividend per share for FY2026/3 was ¥53.67 (post-stock split adjustment), with the year-end dividend increased from the initial forecast of ¥20 to ¥32. ROE improved from 4.6% to 5.4%.

- For the fiscal year ending March 2027, consolidated performance forecasts include net sales of ¥100,000 million (+4.8% YoY), operating profit of ¥3,200 million (-25.5% YoY), ordinary profit of ¥5,800 million (+1.2% YoY), and net profit of ¥4,600 million (+5.3% YoY).

- The forecasted annual dividend per share for FY2027/3 is ¥94.00, with total dividends projected at ¥3,285 million (an increase of ¥1,406 million YoY). The consolidated dividend payout ratio is expected to increase from 42.9% to 71.4%.

🤖 AI Perspective

Tokushu Tokai achieved revenue and profit growth in FY2026/3, driven by price revisions in the lifestyle products business and contributions from the environmental-related business, yet it missed initial forecasts due to factors such as adjustments in special functional papers. For FY2027/3, while record-high net sales are projected, the expected decline in operating profit due to one-off factors, such as expenses related to equipment renewal in the special materials business and upfront investments in the resource recycling business, is worth monitoring. The significant increase in dividend forecasts, following a change in dividend policy, may suggest a proactive stance towards shareholder returns.

5852|アーレスティ

760.0

▼ -11.73%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Ahresty Corporation announced its consolidated financial results for the fiscal year ended March 31, 2026.

- Consolidated net sales for FY2026/3 amounted to ¥167,092 million, representing a 2.6% increase year-on-year.

- Operating income for the period was ¥3,739 million, a 10.9% increase compared to the previous fiscal year.

- Ordinary income decreased by 5.9% to ¥2,865 million.

- Net income attributable to owners of the parent turned profitable at ¥3,580 million, compared to a loss of ¥2,892 million in the previous fiscal year.

- For FY2027/3, the company forecasts consolidated net sales of ¥161,600 million (3.3% decrease), operating income of ¥1,400 million (62.6% decrease), ordinary income of ¥800 million (72.1% decrease), and net income attributable to owners of the parent of ¥500 million (86.0% decrease).

- The year-end dividend for FY2026/3 was ¥26, bringing the annual dividend to ¥42. The forecast for the next fiscal year’s annual dividend is ¥34.

🤖 AI Perspective

The increase in net sales and operating income, along with the return to profitability for net income attributable to owners of the parent in FY2026/3, could suggest an improvement in the company’s operational performance. However, the projected decrease in sales and profits across all major metrics for FY2027/3 indicates a cautious outlook for the upcoming fiscal year. While the dividend increased from the previous period, the forecast for a lower dividend in the next fiscal year may be worth monitoring for investors.

6262|PEGASUS

687.0

▼ -5.11%

📎 Source:PEGASUS Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- PEGASUS announced its consolidated financial results for the 80th fiscal year ended March 2026.

- For the fiscal year ended March 2026, consolidated net sales were ¥21,657 million (down 1.7% year-on-year), operating income was ¥946 million (down 39.8% year-on-year), and profit attributable to owners of parent was ¥323 million (down 66.5% year-on-year).

- Segment sales were ¥13,830 million for the Apparel Machinery business (down 0.2% year-on-year) and ¥7,827 million for the Automotive business (down 4.4% year-on-year).

- In the Apparel Machinery business, demand for industrial sewing machines remained firm in Latin America, but caution regarding capital investment continued in Bangladesh and India.

- The Automotive business experienced a decline in sales due to pricing pressure in China and uncertainty surrounding the overall Chinese automotive industry.

- For the fiscal year ending March 2027, the company forecasts consolidated net sales of ¥22,180 million (up 2.4% year-on-year), operating income of ¥840 million (down 11.3% year-on-year), and profit attributable to owners of parent of ¥250 million (down 22.7% year-on-year).

🤖 AI Perspective

The fiscal year ended March 2026 saw a decline in key profit metrics. This was primarily attributed to reduced sales in the Automotive business, coupled with increased cost of sales due to pricing pressure in China and higher selling, general and administrative expenses from personnel reinforcement within the same segment. While the FY2027 forecast anticipates increased sales, it projects a continued decline in operating income and subsequent profit figures, suggesting that market fluctuations in each business segment could remain a key factor for investors to monitor.

2340|極楽湯HD

478.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Gokurakuyu Holdings (2340) announced consolidated financial results for the fiscal year ended March 31, 2026, with net sales of ¥16,246 million (up 7.1% year-on-year), operating profit of ¥1,236 million (up 8.5%), ordinary profit of ¥1,326 million (up 3.6%), and profit attributable to owners of parent of ¥928 million (up 20.7%).

- The net profit for the period marked a new record high since its listing, surpassing the previous year’s highest profit.

- A year-end dividend of ¥6.00 per share was declared, totaling ¥190 million. No dividend was paid in the fiscal year ended March 31, 2025.

- The dividend for the fiscal year ended March 31, 2026, includes capital surplus as a source of funds.

- The consolidated earnings forecast for the fiscal year ending March 31, 2027, has not been provided due to many uncertain factors influencing performance at this time.

3673|ブロドリーフ

1020.0

▲ +1.09%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Broadleaf Co., Ltd. announced a revision to its dividend forecast (increase) for the fiscal year ending December 2026 on May 20, 2026.

- The previous forecast (announced on February 12, 2026) was an annual dividend of ¥15.00 per share.

- The revised forecast (converted to pre-stock split basis) includes a Q2-end dividend of ¥7.50 per share and a year-end dividend of ¥4.00 per share (¥8.00 on a pre-stock split basis) after the stock split.

- When the revised year-end dividend forecast is converted to a pre-stock split basis, it becomes ¥15.50 per share, an effective increase of ¥0.50 compared to the previous forecast of ¥15.00.

- The reasons for the revision include the implementation of a 1-for-2 stock split and solid progress against the earnings forecast.

🤖 AI Perspective

This dividend forecast revision appears to be an adjustment accompanying a stock split and may indicate a reinforced commitment to shareholder returns driven by strong business performance. The effective dividend increase could be viewed as a positive signal regarding the company’s approach to shareholder value. This revision is worth monitoring for insights into the company’s future dividend policy.

3753|フライト

167.0

▲ +3.73%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Flight Solutions Inc. announced its financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- For FY2026/3, net sales were ¥2,927 million (down 4.4% year-on-year), operating loss was ¥276 million (vs. ¥298 million operating loss in the prior year), ordinary loss was ¥297 million, and net loss was ¥252 million.

- By segment, SI Solution revenue was ¥932 million (down 19.7% YoY), Payment Solution revenue was ¥1,915 million (up 7.6% YoY), and EC Solution revenue was ¥79 million (down 34.7% YoY).

- As of the end of FY2026/3, total assets were ¥1,740 million, net assets were ¥672 million, and the equity ratio was 38.6%.

- For FY2027/3 (April 1, 2026 – March 31, 2027), the company forecasts net sales of ¥5,030 million (up 71.8% YoY), operating profit of ¥380 million, ordinary profit of ¥370 million, and net profit of ¥240 million.

🤖 AI Perspective

While Flight Solutions reported a decrease in revenue and a loss for FY2026/3, the extent of the loss narrowed compared to the previous period. Notably, the Payment Solution business achieved revenue growth, positioning it as a key area for future development. The company anticipates a significant increase in revenue and a return to profitability for FY2027/3, suggesting that the execution of new projects and adaptation to market conditions will be worth monitoring.

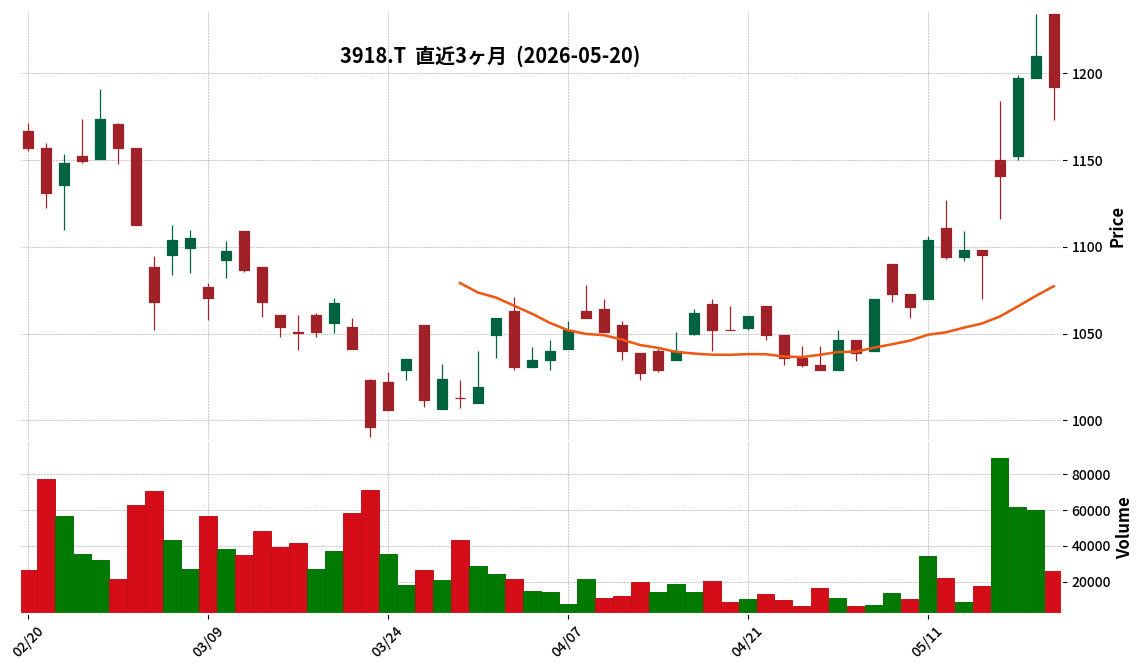

3918|PCIHD

1192.0

▼ -1.49%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- PCI Holdings (PCIHD) announced its board of directors resolved on a basic policy to transition from a pure holding company to an operating holding company by absorbing its wholly-owned subsidiary, PCI Solutions, Inc. (PSOL).

- The merger will be an absorption-type merger with PCIHD as the surviving company and PSOL as the absorbed company. It qualifies as a “simplified merger” for PCIHD and a “short-form merger” for PSOL under the Companies Act, thus shareholder approval is not required for either company.

- The planned board resolution date for merger agreement approval and contract signing is June 30, 2026, with the effective date (merger date) scheduled for October 1, 2026.

- Since this is a merger with a wholly-owned subsidiary, no shares or other monetary consideration will be allotted, and the impact on PCIHD’s consolidated performance is stated to be minor.

- PCIHD also plans to change its trade name and business description, and there is a scheduled change in Representative Director from Kensaku Morishita to Atsushi Watanabe.

🤖 AI Perspective

This announcement suggests PCIHD’s strategic intent to clarify its identity as an “IT engineering firm” and streamline its governance structure, aiming for faster decision-making and maximized management efficiency. The “deepening” of its management strategy appears to involve accelerating human capital investment and strengthening its development system to gain competitive advantage. Simplifying the business structure could potentially lead to a more accurate market valuation for the company.

421A|G-ムービン

2338.0

▼ -8.96%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Movin Strategic Career Co., Ltd. held its Q1 FY2026 (January 1, 2026 – March 31, 2026) earnings briefing on May 18, 2026.

- Q1 revenue reached ¥1.34 billion, marking a 54.8% increase year-over-year, and operating profit grew by 47.4% year-over-year to ¥0.66 billion.

- Q1 revenue surpassed the initial plan of ¥1.1 billion, achieving the ¥1.3 billion target originally set for Q3.

- The average placement fee exceeded ¥4 million, and the number of placements increased by approximately 1.5 times year-over-year.

- Productivity per career advisor improved by 14.4% compared to the full year of FY2025.

- The full-year FY2026 performance forecast was revised upwards, with revenue increased from ¥5.0 billion to ¥5.8 billion and operating profit from ¥2.29 billion to ¥2.66 billion.

🤖 AI Perspective

The company’s Q1 results show significant growth in both revenue and operating profit, exceeding both prior year figures and internal plans. This performance is attributed to the accelerating demand for AI consulting, which appears to be driving higher average placement fees and an increased number of placements. The upward revision of the full-year forecast, while described as conservative and primarily reflecting Q1 results and confirmed Q2 progress, suggests a strong start to the fiscal year that warrants monitoring.

4237|フジプレアム

344.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Fujipream Corporation announced the financial results for the fiscal year ended March 2026 of its non-listed parent company, Follow Wind Co., Ltd.

- As of March 31, 2026, Follow Wind Co., Ltd.’s balance sheet showed total assets of ¥4,935,941 thousand, total liabilities of ¥4,232,885 thousand, and total net assets of ¥703,056 thousand.

- For the period from April 1, 2025, to March 31, 2026, the income statement reported net sales of ¥162,315 thousand, operating income of ¥20,261 thousand, ordinary income of ¥150,698 thousand, and net income of ¥131,384 thousand.

- The major shareholders of Follow Wind Co., Ltd. are Mr. Michinaga Matsumoto (50.00%), Ms. Keiko Namura (20.00%), Ms. Noriko Matsumoto (20.00%), and Ms. Haruyo Matsumoto (10.00%), holding a total of 200 shares.

🤖 AI Perspective

The disclosure of financial results by a non-listed parent company like Follow Wind provides important insight into the broader financial health and capital structure of the group, which includes the listed subsidiary Fujipream. The parent company’s net assets and net income figures could indicate the stability and strategic backdrop of the group’s operations. Investors monitoring the governance and management structure of Fujipream may also find the parent company’s shareholder composition and executive details noteworthy.

4882|G-ペルセウス

170.0

▼ -2.86%

📎 Source:G-ペルセウス Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Perseus disclosed the summary of the Q&A session from its earnings call for analysts and institutional investors held on May 18, 2026.

- Out-licensing activities for PPMX-T003 are ongoing, with plans to expand adaptation beyond polycythemia vera to other diseases.

- For PPMX-T002, out-licensing activities are focused on potential partners strengthening their development in radiopharmaceuticals.

- PPMX-T004, a next pipeline candidate, is scheduled for antibody MCB and engineering batch manufacturing between January 2027 and March 2028, with Phase 1 to commence after the completion of GLP toxicity studies.

- In response to the revised listing maintenance criteria for the TSE Growth Market, the company is considering various perspectives but has no decided matters to announce at this time.

🤖 AI Perspective

The Q&A session from G-Perseus’s earnings call shed light on the progress and future strategies for its key development pipelines. The company addressed the prolonged out-licensing activities for PPMX-T003 and PPMX-T002, citing competitive landscapes, development phases, and supply instability of actinium-225 as contributing factors. These responses suggest that the company is actively working to overcome these challenges. Additionally, the disclosure of the development schedule for the next pipeline candidate PPMX-T004 and the company’s approach to the TSE Growth Market listing maintenance criteria may be of interest to investors monitoring the firm’s strategic direction.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

6050|Eガーディアン

1664.0

▼ -2.06%

📎 Source:Eガーディアン Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- E-Guardian reported for the second quarter of the fiscal year ending September 2026 (October 1, 2025 – March 31, 2026), net sales of 5,464 million yen (down 6.9% year-on-year), operating profit of 567 million yen (down 39.0% year-on-year), and net income attributable to owners of parent of 373 million yen (down 38.5% year-on-year), indicating a decrease in both revenue and profit.

- The full-year forecast (net sales of 12,009 million yen, operating profit of 1,604 million yen, ordinary profit of 1,629 million yen, and net income attributable to owners of parent of 1,033 million yen) remains unchanged. The dividend forecast also remains at 38 yen.

- The decrease in revenue for the first half was primarily due to reduced sales from existing major clients in monitoring services and the conclusion of a large project in game support. The decrease in profit was attributed to the decline in net sales, investment in AI strategy, sales, and marketing personnel, and a one-time expense of 4 million yen for office reorganization.

- For the second half of the fiscal year, the company anticipates an accumulation of large project orders, improved profitability of service centers, and enhanced profit margins through AI implementation.

- Office reorganization, including the absorption of E-Guardian Tohoku’s centers into E-Guardian, is expected to result in an annual fixed cost reduction of 60 million yen.

🤖 AI Perspective

While the first half saw a decrease in revenue and profit, the company’s decision to maintain its full-year forecast suggests an expectation of profit margin improvement through AI implementation and the accumulation of large orders in the second half. The shift from a labor-intensive model to a high-value-added “AI-BPO” business model could significantly impact future revenue structures, making the progress of this strategy worth monitoring. Additionally, fixed cost reductions from office reorganization are anticipated to contribute to profit improvement.

7111|INEST

427.0

▼ -3.39%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- INEST has published its supplemental earnings material for the full fiscal year ended March 2026.

- For the fiscal year ended March 2026, consolidated results exceeded revised forecasts across all metrics: revenue was ¥18,185 million (107% achievement), operating profit was ¥255 million (102% achievement), and net income attributable to owners of parent was ¥180 million (401% achievement).

- Key factors contributing to the achievement of the full-year operating profit target included an upside in sales volume and customer unit price in Q4, optimization of management resources, and strong sales of proprietary services.

- The key KPI of stock profit (cumulative period) reached ¥1.37 billion, achieving 105% of the full-year plan of ¥1.30 billion (118% year-on-year).

- In terms of consolidated cash flow, cash flow from operating activities temporarily decreased, while cash flow from investing activities increased due to the sale of subsidiary shares.

🤖 AI Perspective

INEST’s full-year results for March 2026 demonstrate strong performance, significantly surpassing revised forecasts, with the high achievement rate of net income attributable to owners of parent being particularly noteworthy. This outcome appears to be driven by strategic reallocation of management resources and robust sales of proprietary services in the fourth quarter. The successful achievement of stock profit targets suggests a strengthening of the company’s revenue base and may indicate enhanced stability and future growth potential, which investors could find positive.

7409|G-AeroEdge

3745.0

▼ -5.19%

📎 Source:G-AeroEdge Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-AeroEdge announced its decision on May 20, 2026, to acquire all shares of Ono Plant Co., Ltd., making it a wholly-owned subsidiary.

- The acquisition involves 59,000 shares, resulting in a 100% voting rights ownership post-transaction.

- The total acquisition cost is approximately 1,035 million yen, comprising 980 million yen for common shares and an estimated 55 million yen for advisory fees.

- The share transfer is scheduled to be executed on June 4, 2026.

- Ono Plant Co., Ltd. specializes in machining aircraft structural parts and reported sales of 1,038,487 thousand yen, operating profit of 81,189 thousand yen, and net profit of 89,967 thousand yen for the fiscal year ended March 2025.

- Ono Plant Co., Ltd. will be consolidated into G-AeroEdge’s financial statements from the fourth quarter of the fiscal year ending June 2026.

🤖 AI Perspective

G-AeroEdge’s acquisition of Ono Plant Co., Ltd. appears to be a strategic move to broaden its business scope beyond aircraft engine components to include aircraft structural parts and potentially the defense sector. The combined entity’s ability to leverage Ono Plant’s client base with major domestic heavy industry manufacturers and G-AeroEdge’s global network could create significant synergies. Investors may want to monitor how this expansion will impact the company’s consolidated performance in the upcoming fiscal periods.

7481|尾家産

2400.0

▼ -0.33%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Oie Sangyo Co., Ltd. resolved to pay a dividend from surplus (dividend increase) at its Board of Directors meeting held on May 20, 2026.

- The year-end dividend per share for the fiscal year ended March 31, 2026, will be ¥55.00 (ordinary dividend of ¥55).

- This brings the total annual dividend for the fiscal year ended March 2026 to ¥102.00 (ordinary dividend of ¥102), including the interim dividend of ¥47.00.

- The previous fiscal year’s (March 2025) annual dividend was a total of ¥102.00 (ordinary dividend of ¥90 and special dividend of ¥12).

- The total dividend amount is ¥456 million, funded by retained earnings, with an effective date of June 5, 2026.

🤖 AI Perspective

Oie Sangyo’s declared dividend maintains the same total annual payout as the previous year, which included a special dividend, but achieves this solely through ordinary dividends this period. This could be interpreted as the company aiming for more stable and sustainable shareholder returns without reliance on special dividends. Investors may want to monitor the company’s commitment to its stated goal of achieving a consolidated dividend payout ratio of 30% or more.

8725|MS&AD

4399.0

▼ -2.31%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 31, 2026, consolidated ordinary revenues reached ¥7,653,030 million, a 14.9% increase year-on-year.

- Net profit attributable to owners of parent was ¥787,339 million, marking a 13.8% increase compared to the previous fiscal year.

- Earnings per share (EPS) for FY2026 stood at ¥528.87, up from ¥445.52 in FY2025.

- The annual dividend per share for FY2026 was ¥160.00, an increase from ¥145.00 in FY2025, with an expected ¥170.00 for FY2027.

- Total assets amounted to ¥28,640,815 million and net assets to ¥4,825,140 million as of March 31, 2026.

🤖 AI Perspective

MS&AD’s FY2026 consolidated financial results demonstrate robust performance, with double-digit growth in key revenue and profit metrics. The increase in the annual dividend and the forecast for a further raise in FY2027 may signal a strong commitment to shareholder returns. Investors might monitor the impact of the announced restructuring of domestic non-life insurance operations and the enhancement of overseas business management structures on future performance.

2292|S FOODS

2825.0

▼ -0.11%

📎 Source:S FOODS Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- S FOODS Co., Ltd. announced corrections to its “FY2026 February Financial Results (Consolidated) [Japanese GAAP]” originally disclosed on April 14, 2026.

- The reason for the corrections was the discovery of aggregation errors in the summary information, overview of financial position, overview of cash flows, consolidated statements of comprehensive income, consolidated statements of cash flows, and segment information, found during a post-submission review.

- Specific changes in the consolidated cash flow situation for FY2026 February include operating cash flow revised from “8,750 million yen” to “8,832 million yen” and investing cash flow from “△8,137 million yen” to “△8,218 million yen.”

- In the overview of the financial position, the increase in merchandise and products under current assets was corrected from “796 million yen” to “818 million yen,” and the increase in deferred income taxes payable under liabilities was corrected from “2,926 million yen” to “2,966 million yen.”

- Cash flow-related indicators for FY2026 February were also adjusted: the cash flow to interest-bearing debt ratio changed from “654.9” to “648.9,” and the interest coverage ratio from “14.1” to “14.3.”

9564|FCE

459.0

▼ -4.38%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- FCE reported net sales of ¥3,434 million (up 14.0% year-on-year) and ordinary profit of ¥763 million (up 14.5% year-on-year) for the second quarter of the fiscal year ending September 2026.

- Quarterly sales for the SaaS-based DX promotion business reached ¥1,042 million, an increase of 25.4% compared to the previous year’s corresponding period.

- Monthly Recurring Revenue (MRR) for the SaaS-based business stood at ¥396 million, marking a 23.8% increase year-on-year.

- The number of companies adopting “Robo-pat AI” reached 2,055 as of March 31, 2026, with the churn rate maintained at a low 1% range.

- The company is advancing its AI-related businesses, including preparations and commencement of “AI Risk Management Training” and “AI Organizational Utilization Training & Consulting” services.

🤖 AI Perspective

FCE’s second-quarter results for FY2026 indicate a continued upward trend in revenue and profit, primarily driven by its SaaS-based DX promotion business. The consistent growth in “Robo-pat AI” adoption and a low churn rate suggest a robust and stable operational foundation. Furthermore, the strategic integration of AI technology into new training and consulting services may position the company for diversified revenue streams in the evolving market landscape.

2937|G-サンクゼール

1660.0

▼ -0.60%

📎 Source:G-サンクゼール Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Couscous Co., Ltd. announced on May 20, 2026, a change to its shareholder benefit program.

- The company cited improved shareholder convenience and satisfaction, along with deeper brand understanding, as reasons for the change.

- The revised benefits will consist of service vouchers usable at the company’s stores or online shop, varying by the number of shares held.

- Previously, benefits included a “product gift set and service voucher,” but will now be “service vouchers only.”

- The new benefit amounts are 2,500 yen for 100-299 shares, 8,000 yen for 300-499 shares, and 14,000 yen for 500 or more shares.

- This change will be implemented starting with the shareholder benefits for shareholders listed in the share register as of March 31, 2027.

- There are no changes to the eligibility criteria, which require owning 100 or more shares on the record date of March 31 and continuous ownership with the same shareholder number since September 30 of the previous year.

4720|城南進研

230.0

▼ -9.09%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Johnan Shingaku Research Institute announced its consolidated financial results for the fiscal year ended March 2026. Net sales were ¥5,621 million (down 0.1% from the previous year).

- Operating income was ¥77 million (compared to an operating loss of ¥230 million in the previous year), and ordinary income was ¥80 million (compared to an ordinary loss of ¥228 million in the previous year), marking a return to profitability.

- Net income attributable to owners of the parent company was ¥4 million due to factors including impairment losses (compared to a net loss of ¥420 million attributable to owners of the parent company in the previous year).

- As of the end of March 2026, basic earnings per share were ¥0.61, and the equity ratio was 27.2%.

- The year-end dividend for the fiscal year ended March 2026 was ¥7.00 per share, with total annual dividends amounting to ¥56 million.

- For the fiscal year ending March 2027, the company forecasts consolidated net sales of ¥5,731 million (up 2.0% year-on-year), operating income of ¥142 million (up 83.7%), ordinary income of ¥133 million (up 64.6%), net income attributable to owners of the parent company of ¥84 million, and basic earnings per share of ¥10.57.

🤖 AI Perspective

The fiscal year March 2026 results show a notable return to profitability for operating and ordinary income, despite a nearly flat sales revenue. This turnaround from a significant loss in the previous year suggests an improvement in the company’s operational efficiency. The positive forecast for sales and profit in FY March 2027 could indicate management’s confidence in sustained recovery and growth in the upcoming period.

5247|G-BTM

650.0

▼ -0.61%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Operating profit for the fiscal year ended March 2026 reached ¥108 million, exceeding the initial plan of ¥103 million.

- Net sales increased by 18.3% year-on-year, marking a new record high, and the gross profit margin improved to 15.4%, surpassing the initial forecast.

- Synergies with Quest System Design (QSD), which joined the group via M&A, are progressing smoothly, with joint proposals already securing new orders.

- The increase in key KPI “account numbers” has expanded the Serviceable Addressable Market (SAM) to ¥5.3 trillion.

- The FY2027 March performance forecast does not include any additional sales or profits from future M&A, and is calculated based solely on organic growth.

- The newly launched SaaS AI agent ‘Tracis’ has demonstrated effectiveness in significantly shortening system failure identification times and is being promoted via a freemium model.

🤖 AI Perspective

G-BTM’s FY2026 March results suggest that the focus on improving profitability, in addition to sales growth, contributed to the upward revision of operating profit. The generation of synergies through M&A and the deployment of the SaaS AI agent ‘Tracis’ could be key growth drivers going forward. Furthermore, the fact that the FY2027 March performance forecast is calculated based solely on organic growth may indicate potential for further upside from future M&A activities.

6576|P-揚工舎

—

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- P-Yoko Kosha’s consolidated financial results for the fiscal year ended March 2026 show net sales of ¥3,638 million, an increase of 17.9% from the previous fiscal year.

- Operating profit was ¥42 million (down 65.9%), ordinary profit was ¥74 million (down 46.8%), and profit attributable to owners of parent was ¥44 million (down 46.5%).

- On July 1, 2025, the company acquired Club Tourism Life Care Services Co., Ltd. (later renamed Yoko Associates Co., Ltd.) as a wholly-owned subsidiary, commencing operations of 8 day-service facilities.

- The company implemented a flat salary increase for all permanent employees and incurred intermediary fees related to the M&A.

- The consolidated earnings forecast for the fiscal year ending March 2027 projects net sales of ¥3,904 million (up 7.3%), operating profit of ¥122 million (up 189.0%), and profit attributable to owners of parent of ¥68 million (up 52.6%).

🤖 AI Perspective

P-Yoko Kosha’s FY2026/3 results indicate significant revenue growth, potentially driven by strategic M&A activities, while profitability declined due to increased personnel costs and acquisition-related expenses. The substantial projected profit recovery for FY2027/3 suggests that management anticipates improved operational efficiencies and synergies from the newly acquired businesses. Investors may want to monitor how these factors contribute to the company’s future financial performance.

6616|トレックスセミ

2446.0

▼ -1.41%

📎 Source:トレックスセミ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- TOREX SEMICONDUCTOR reported consolidated financial results for the fiscal year ended March 2026, with net sales of ¥25,073 million (up 4.7% year-on-year), operating profit of ¥1,085 million (compared to a loss of ¥632 million in the previous year), ordinary profit of ¥1,268 million (compared to a loss of ¥820 million in the previous year), and net profit attributable to owners of parent of ¥1,159 million (compared to a loss of ¥2,358 million in the previous year).

- Both Torex standalone and PeniTech reported sales recovery across all regions, leading to increased revenue and profit.

- Against the initial forecasts, net sales were as expected, but profits were revised upwards on May 11, 2026, due to factors including foreign exchange effects.

- The overseas sales ratio was 68.2% (down 1.2 percentage points year-on-year), and the average exchange rate was ¥150.9 per US dollar.

- By application for Torex standalone, sales for medical equipment increased by 57.7%, industrial equipment by 8.7%, and wearable devices by 7.0%, while automotive equipment sales decreased by 2.5%.

🤖 AI Perspective

TOREX SEMICONDUCTOR’s FY2026/3 full-year results show a significant turnaround from a loss to increased revenue and profit, driven by sales recovery across all regions. The substantial increase in sales for medical equipment within the Torex standalone segment may suggest expanding demand in specific market niches, which could be a critical factor in future business strategies. Furthermore, the upward revision of profit forecasts, attributed to favorable foreign exchange effects, could indicate an improvement in the company’s financial health.

6743|大同信号

765.0

▼ -5.09%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Daido Signal announced consolidated results for the fiscal year ended March 2026, with net sales of ¥25,695 million, a 17.3% increase from the previous year.

- Operating profit reached ¥2,187 million (up 89.8% year-on-year), and ordinary profit was ¥2,347 million (up 86.0% year-on-year).

- Net profit attributable to owners of parent was ¥1,791 million (up 16.1% year-on-year), with earnings per share of ¥112.98.

- A year-end dividend of ¥35.00 per share (total annual dividend of ¥35.00) was declared.

- For the fiscal year ending March 2027, the company forecasts consolidated net sales of ¥25,700 million (up 0.0% year-on-year), operating profit of ¥1,800 million (down 17.7% year-on-year), and net profit attributable to owners of parent of ¥1,900 million (up 6.1% year-on-year).

🤖 AI Perspective

Daido Signal’s FY2026 results show significant growth across revenue and profit metrics, with operating profit nearly doubling from the previous year. The substantial increase in the annual dividend from ¥15.00 to ¥35.00 per share suggests a stronger commitment to shareholder returns. However, the FY2027 forecast projects flat sales and a decrease in operating profit, which might indicate anticipated cost fluctuations or strategic investments.

8616|東海東京

693.0

▼ -0.86%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tokai Tokyo Financial Holdings, Inc. announced corrections to a portion of its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 [Japanese GAAP]” initially released on April 30, 2026.

- The reason for the correction was an error in the calculation of the defined benefit obligation for employees’ defined benefit corporate pensions for the fiscal year ended March 31, 2026.

- The corrections impact the consolidated balance sheet, specifically the accounts for “Net defined benefit asset,” “Deferred tax liabilities,” and “Accumulated actuarial adjustment for retirement benefits.”

- Consequently, total assets on the consolidated balance sheet were revised from JPY 1,525,011 million to JPY 1,526,284 million, and net assets from JPY 208,657 million to JPY 209,529 million.

- There is no impact on the presentation accounts in the consolidated statement of income.

🤖 AI Perspective

This correction stems from a specific calculation error and does not affect the consolidated statement of income, suggesting a limited direct impact on the company’s fundamental profitability assessment. Investors may find it worthwhile to monitor how these balance sheet adjustments could affect the company’s financial health and capital structure in the long term.

8766|東京海上

7817.0

▼ -1.66%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tokio Marine Holdings reported consolidated ordinary revenue of ¥8,872.2 billion for the fiscal year ended March 31, 2026, an increase of 5.1% year-on-year.

- Consolidated ordinary profit was ¥1,348.6 billion, a decrease of 7.6% from the previous fiscal year, and net profit attributable to owners of the parent was ¥980.4 billion, down 7.1%.

- The annual dividend per share for FY2026/3 was increased to ¥218, up from ¥172 in the prior fiscal year.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net profit attributable to owners of the parent of ¥830.0 billion, prepared under International Financial Reporting Standards (IFRS).

- Consolidated total assets at the end of the fiscal year stood at ¥31,961.9 billion, an increase of ¥724.5 billion from the previous year-end, while net assets increased by ¥354.0 billion to ¥5,457.5 billion.

🤖 AI Perspective

The revenue increase coupled with a decrease in ordinary profit and net profit for FY2026/3 is a key point for investors to observe. The announced increase in the annual dividend payment may suggest a continued commitment to shareholder returns. The adoption of IFRS for the FY2027/3 outlook could indicate a shift towards greater international comparability in financial reporting.

5891|魁力屋

1505.0

▲ +13.33%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kairikiya Co., Ltd. announced additional information on May 20, 2026, regarding the expansion of eligible stores for its shareholder benefit program.

- This announcement serves as supplementary information to the “Change (Expansion) of Shareholder Benefit Program” announced on the preceding day, May 19.

- The shareholder benefit vouchers, previously valid at “Ramen Kairikiya,” will now also be accepted at “Mita Seimenjo.”

- “Mita Seimenjo” is operated by MP Kitchen Holdings Co., Ltd., which became a group company this year.

- The purpose of this expansion is to allow shareholders to become more familiar with the company group’s various establishments.

🤖 AI Perspective

This expansion of eligible stores for the shareholder benefit program, now including “Mita Seimenjo” in addition to “Ramen Kairikiya,” could enhance the convenience and appeal of the program for shareholders. By offering a broader range of options for utilizing the vouchers, it may encourage greater engagement from shareholders and potentially contribute to increased brand awareness across the entire group. This move can be seen as an effort to maximize the value proposition of the shareholder benefits.

4755|楽天グループ

784.0

▼ -1.48%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Rakuten Group and Rakuten Bank have signed a definitive agreement for the reorganization of their FinTech businesses.

- Rakuten Bank will make Rakuten Card Co., Ltd. and Rakuten Securities Holdings, Inc. its subsidiaries through a share delivery process.

- This share delivery is subject to approval at Rakuten Bank’s ordinary general meeting of shareholders scheduled for June 24, 2026.

- Rakuten Bank plans to submit proposals to its shareholders’ meeting for amendments to its articles of incorporation, including changes to the total number of authorized shares and the establishment of provisions for Class A preferred shares, conditional on the effectiveness of the share delivery.

- Rakuten Insurance Holdings Co., Ltd. and Rakuten Wallet, Inc. are excluded from this reorganization, with Rakuten Group planning to retain 100% ownership of their shares.

- Rakuten Payment, Inc. and Rakuten Edy, Inc. are expected to transfer all shares held by Rakuten Card to Rakuten Group prior to the effective date of the share delivery.

🤖 AI Perspective

This reorganization appears to consolidate key FinTech businesses under Rakuten Bank, aiming to strengthen inter-business collaboration and optimize funding flexibility and costs. The move may suggest an effort to enhance responsiveness to diversifying customer needs, scale business operations, and stabilize revenue streams amidst an intensifying competitive landscape. Investors will likely be monitoring the implications of this restructuring on Rakuten Group’s overall “Rakuten Ecosystem” and the future trajectory of its FinTech strategy.

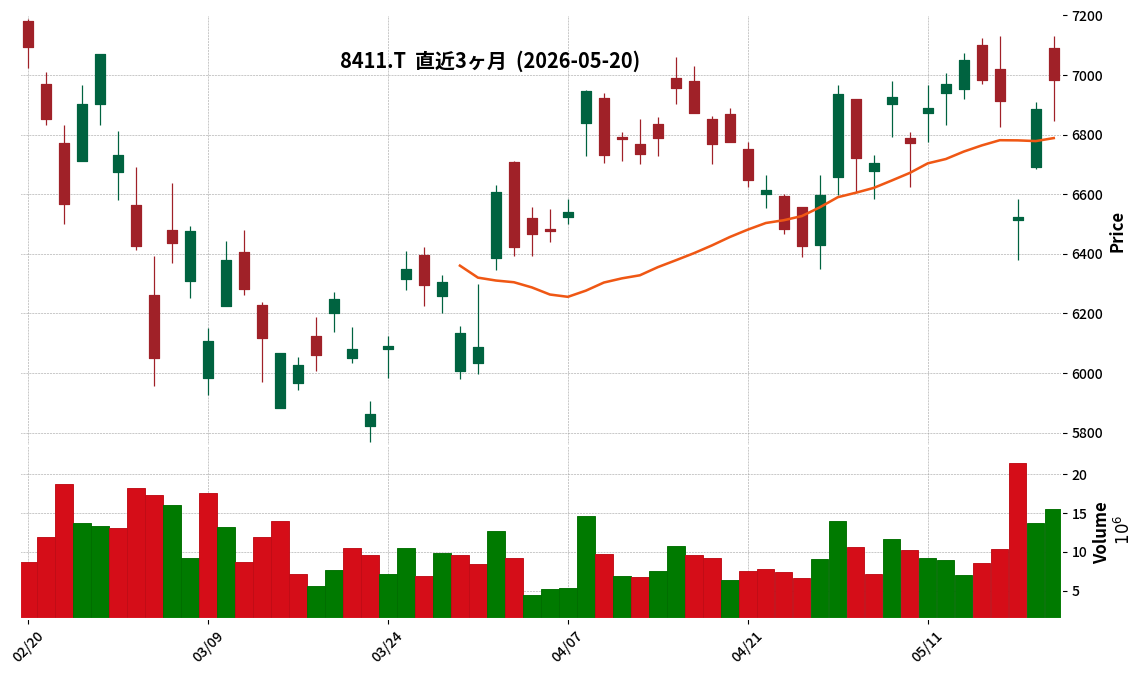

8411|みずほ

6982.0

▲ +1.39%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Mizuho Bank and Rakuten Bank formally signed a strategic capital and business alliance agreement on May 20, 2026.

- The objective of this alliance is to establish a new credit creation model by combining a mega-bank and a digital bank.

- Specific business alliance initiatives include: stable acquisition of Mizuho Bank-originated claims by Rakuten Bank, collaboration on payment and working capital needs for small corporations and sole proprietors, operational efficiency collaborations (e.g., housing loan business), and cooperation on emergency cash withdrawal services for Rakuten Bank during crises.

- As part of the capital alliance and a stock delivery that will make Rakuten Card and Rakuten Securities HD subsidiaries of Rakuten Bank, Rakuten Bank is scheduled to deliver 23,559,673 shares of its Class A preferred stock to Mizuho Bank.

- These Class A preferred shares are expected to be converted into common stock on the effective date of the stock delivery.

🤖 AI Perspective

This alliance aims to enhance the effective utilization of domestic funds and promote credit creation by combining Mizuho Bank’s robust corporate client base with Rakuten Bank’s individual deposit base. Amid the reorganization of Rakuten Group’s fintech businesses, Mizuho Bank’s expected position as a major shareholder in Rakuten Bank could significantly strengthen their collaboration. This strategic move may lead to the development of innovative financial services leveraging each bank’s core strengths.

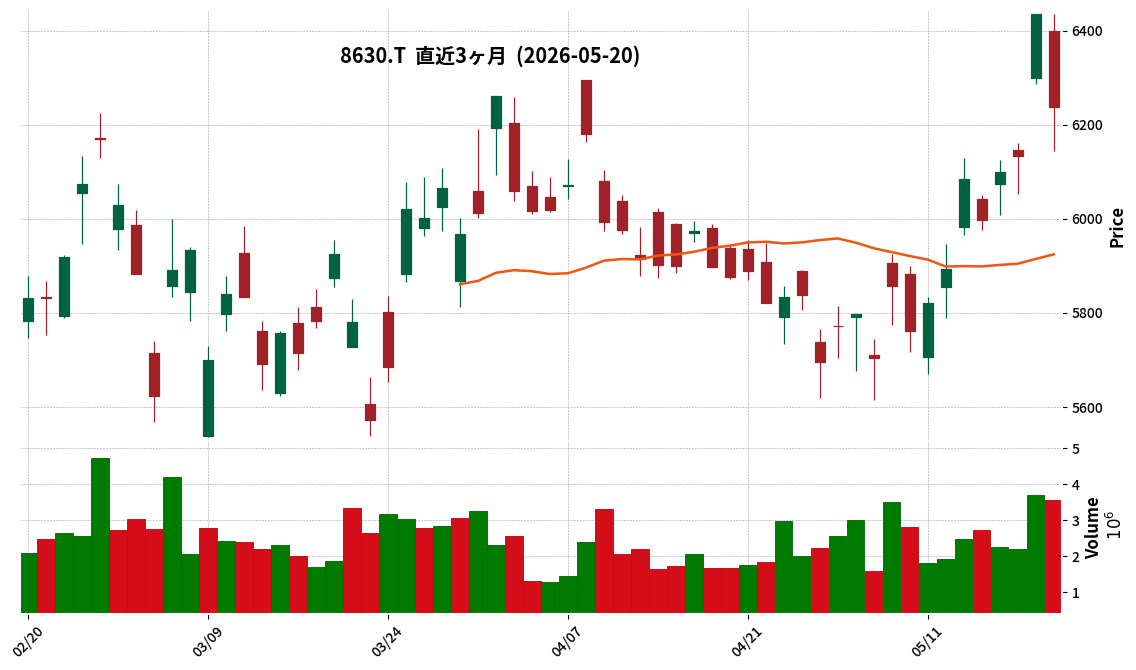

8630|SOMPOHD

6238.0

▼ -3.06%

📎 Source:SOMPOHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SOMPO Holdings, Inc. announced its consolidated financial results for the fiscal year ended March 31, 2026.

- Profit attributable to owners of parent increased by 163.3% from the previous fiscal year, reaching ¥640,086 million.

- Insurance revenue was ¥5,372,921 million, a 6.1% increase year-on-year, and profit before tax was ¥843,226 million, a 155.3% increase year-on-year.

- The annual dividend for the fiscal year ended March 31, 2026, was increased to ¥150 per share from ¥132 in the prior year.

- For the fiscal year ending March 31, 2027, the company forecasts profit attributable to owners of parent to be ¥490,000 million, a 23.4% decrease from the current fiscal year.

- Aspen Insurance Holdings Limited was newly included in the scope of consolidation during the period.

369A|G-エータイ

2150.0

▼ -4.83%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- ATIE Co., Ltd. resolved to introduce a shareholder benefit program at its Board of Directors meeting held on May 20, 2026.

- Eligibility for the program starts from August 31, 2026, targeting shareholders recorded or listed on the shareholder register who hold 200 or more shares annually thereafter.

- The shareholder benefit will be points for the “ATIE Premium Shareholder Club,” ranging from 3,000 to 15,000 points based on the number of shares held.

- Points are scheduled to be granted in early October each year and can be carried over a maximum of once, provided the shareholder is continuously listed for two consecutive times or more and maintains 200 or more shares by the end of August of the following year.

- The stated purposes of this introduction are to return profits to shareholders, enhance stock liquidity, strengthen dialogue with shareholders, and promote DX in shareholder management.

🤖 AI Perspective

The introduction of this shareholder benefit program by ATIE Co., Ltd. may suggest an effort to enhance shareholder returns and broaden its investor base. The utilization of a shareholder database through the “ATIE Premium Shareholder Club” and the planned timely distribution of IR information could potentially lead to improved engagement with shareholders. Furthermore, the option to convert points to “WILLsCoin,” which can be combined with points from other Premium Shareholder Club companies, might offer increased flexibility and appeal to shareholders.

3768|リスクモンスター

564.0

▼ -0.53%

📎 Source:リスクモンスター Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Consolidated net sales for the fiscal year ended March 2026 reached ¥3,824 million, an increase of 2.6% year-on-year.

- Operating profit for the same period was ¥360 million, marking a 36.4% increase compared to the previous fiscal year.

- Net profit attributable to owners of parent turned positive at ¥223 million, up from a loss of ¥49 million in the prior year.

- EBITDA was ¥1,119 million (up 6.7% YoY) with an EBITDA margin of 29.3% (up 1.2pt YoY).

- Total SaaS ARR stood at ¥2,331 million (up 3.2% YoY), composed of Credit Management Service, Business Portal Service, and Education-related Service segments.

🤖 AI Perspective

The FY2026 financial results indicate a positive trend with significant improvements in key financial metrics, notably a substantial increase in operating profit and a return to net profit. The steady growth in SaaS ARR suggests that Riskmonster’s business model is building a sustainable revenue base. Investors may find it worthwhile to monitor how the company’s mid-term management plan, focusing on “embedding into business infrastructure” and “expanding cross-selling,” progresses to drive future growth.

5994|ファインシンター

1065.0

▲ +5.65%

📎 Source:ファインシンター Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Fine Sinter held an online briefing for analysts and institutional investors on May 21, 2026, regarding its FY2026/3 financial results and new Mid-Term Management Plan.

- For the fiscal year ended March 2026, consolidated net sales were ¥46,206 million (up 8.2% year-on-year), operating profit was ¥1,195 million (up 75.0% year-on-year), and ordinary profit was ¥754 million (up 59.6% year-on-year). Net income for the period was -¥2,414 million.

- For the fiscal year ending March 2027, the company forecasts consolidated net sales of ¥44,500 million (down 3.7% year-on-year), operating profit of ¥1,200 million (up 0.4% year-on-year), ordinary profit of ¥800 million (up 6.1% year-on-year), and net income of ¥500 million.

- Key topics for FY2026/3 included the commencement of operations at the second facility of Thai Fine Sinter (from November 2024), the acquisition of 100% ownership of Precision Sintered Parts (Wuxi) Co., Ltd., and the establishment of an IR & Capital Strategy Office.

- Key initiatives for FY2027/3 include “Corporate Culture Reform,” “Safety,” and “Quality.”

6343|フリージアマク

150.0

▼ -6.83%

📎 Source:フリージアマク Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Freesia Macross Co., Ltd. announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- Consolidated net sales were ¥6,873 million (down 1.4% year-on-year), and operating income was ¥1,284 million (down 4.7% year-on-year).

- Consolidated ordinary income increased by 12.2% to ¥2,226 million, and net profit attributable to owners of the parent surged by 90.1% to ¥1,723 million.

- Basic earnings per share stood at ¥38.30, an increase from ¥20.15 in the prior year.

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥6,900 million (up 0.4% year-on-year), operating income of ¥1,200 million (down 6.6%), ordinary income of ¥1,800 million (down 19.2%), and net profit attributable to owners of the parent of ¥1,600 million (down 7.2%).

- The year-end dividend for both FY2026 and FY2027 (forecast) is planned at ¥0.60 per share.

🤖 AI Perspective

Freesia Macross’s FY2026 results show a significant increase in ordinary profit and net profit attributable to owners of the parent, despite a slight decline in net sales and operating income compared to the previous year. This improvement in profitability could be attributed to factors such as an increase in comprehensive income and higher investment securities and related company stocks, which contributed to the growth in net assets. Investors may want to monitor the company’s forecast for the next fiscal year, which anticipates a modest increase in sales but a decrease in profits.

1443|技研ホールディングス

265.0

▼ -6.03%

📎 Source:技研ホールディングス Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Giken Holdings announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- Consolidated net sales amounted to ¥4,675 million, representing a 4.7% decrease compared to the previous fiscal year.

- Consolidated operating profit increased by 12.5% to ¥701 million, ordinary profit rose by 15.9% to ¥892 million, and profit attributable to owners of parent increased by 24.7% to ¥613 million.

- Earnings per share (EPS) for the period were ¥37.79 (compared to ¥30.30 in the prior year), and the equity ratio improved to 70.7% (from 67.5%).

- For the fiscal year ending March 31, 2027, the company forecasts consolidated net sales of ¥4,900 million (up 4.8% year-on-year), operating profit of ¥750 million (up 6.9%), and profit attributable to owners of parent of ¥640 million (up 4.3%).

🤖 AI Perspective

Despite a decrease in net sales, the company achieved double-digit profit growth across operating, ordinary, and net profit metrics, which may suggest an improvement in profitability. The substantial increase in profit attributable to owners of parent could be a point of interest for shareholders, particularly regarding potential implications for shareholder returns. The positive outlook for the upcoming fiscal year, with forecasts for both increased sales and profits, indicates continued growth expectations for the company.

8897|ミラースHD

413.0

▼ -4.18%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- MIRARTH HD’s consolidated results for the fiscal year ended March 2026 showed record-highs in revenue at JPY 214,369 million (+9.1% YoY), operating profit at JPY 17,649 million (+22.9% YoY), and ordinary profit at JPY 14,182 million (+14.1% YoY).

- Net profit attributable to parent company shareholders decreased by 42.0% YoY to JPY 4,758 million, primarily due to impairment losses related to the “Nobeoka Biomass Power Plant” and other facilities, stemming from structural reforms in the energy business.

- The real estate segment reported significant growth and high profitability, with the new detached house sales business achieving a 26.8% increase in revenue and a 47.3% increase in gross profit YoY. The renewal resale business’s gross profit exceeded its plan by 70.4%.

- The energy business underwent a portfolio review, separating the Cambodian cashew business into a next-generation business. The company will strictly manage ROIC and focus investments on high-growth areas like grid-scale batteries.

- MIRARTH HD updated its shareholder return policy, introducing DOE (Dividend on Equity ratio) in addition to the traditional 35-40% payout ratio, with the higher of the two determining the dividend amount. A share buyback, the first in approximately 10 years, was also approved.

🤖 AI Perspective

MIRARTH HD’s record-breaking revenue and operating profits were largely driven by its robust real estate segment, while the significant decline in net profit appears to be a direct consequence of impairment losses incurred during the restructuring of its energy business. The strategic focus on the new detached housing and renewal resale businesses within real estate, coupled with strict ROIC management in the energy sector, may suggest a deliberate shift towards more profitable and sustainable growth areas. The introduction of DOE alongside a share buyback could indicate an enhanced commitment to shareholder returns and capital efficiency, which investors might monitor closely.

2673|夢みつけ隊

116.0

▲ +8.41%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Yumemitsuketai announced its consolidated financial results for the fiscal year ended March 31, 2025 (April 1, 2024 – March 31, 2025).

- Consolidated net sales reached ¥349 million, representing a 39.3% increase compared to the previous consolidated fiscal year.

- Consolidated operating profit turned positive at ¥29 million, a significant improvement from an operating loss of ¥13 million in the prior fiscal year.

- Consolidated ordinary profit was ¥156 million (+70.5% YoY), and profit attributable to owners of parent was ¥154 million (+71.2% YoY).

- The real estate business segment reported sales of ¥159 million (+341.0% YoY) and segment profit of ¥64 million (+226.7% YoY), showing increases in both revenue and profit.

- The consolidated earnings forecast for the fiscal year ending March 31, 2026, is undecided due to ongoing business reorganization considerations, making reasonable calculation difficult at this time.

🤖 AI Perspective

Yumemitsuketai’s strong performance in the fiscal year ended March 2025, with significant increases across key profitability metrics and a return to operating profit, appears to be largely driven by its real estate business. This turnaround could indicate progress in their focus on strengthening the financial structure. However, the undecided earnings forecast for the next fiscal year, citing business reorganization, suggests that investors may want to monitor the company’s strategic developments and future operational plans closely.

8771|Eギャランティ

1756.0

▼ -2.23%

📎 Source:Eギャランティ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- eGuarantee achieved its full-year performance for the fiscal year ended March 2026 as per initial forecasts.

- The company reported its 19th consecutive year of exceeding its recurring profit target and its 24th consecutive year of increased revenue and recurring profit since listing.

- The dividend policy was revised to target a dividend payout ratio of 100%.

- The company plans to accelerate business expansion, including into lending and other adjacent fields beyond accounts receivable guarantees, leveraging its unique big data (guarantee balance of ¥2.6 trillion, guarantee liabilities exceeding ¥900 billion, and transaction data for over 580,000 companies).

- Regarding its medium-term management plan, the company acknowledged an approximately 1.5-year delay in performance targets due to initial implementation setbacks, but stated that qualitative initiatives are progressing.

🤖 AI Perspective

eGuarantee’s consistent track record of revenue and profit growth, coupled with its long-term achievement of recurring profit targets, may suggest a fundamentally sound business model. The announcement of a 100% dividend payout ratio could be seen as a strong commitment to shareholder returns and an emphasis on capital efficiency, which may appeal to investors. However, the acknowledged delay in the medium-term management plan’s performance targets indicates that the company’s future progress should be carefully monitored.

💡 Start investing with IR insights

※ 本ページには広告が含まれます(PR)

Disclaimer: This article is for informational purposes only and does not constitute investment advice. All investment decisions are at your own risk.

コメント