📌 Today’s Highlights

Today we cover 57 IR announcements. Notable among them: セキュアヴェイル (3042), 日本酸素HD (4091), ホクト (1379). Use the table of contents below to navigate to each company.

- 3042|セキュアヴェイル

- 4091|日本酸素HD

- 1379|ホクト

- 2623|iSユロIG社債ヘジ

- 488A|iS円高フォーカス

- 5579|GSI

- 1595|NZAM Jリート

- 3675|クロスマーケティング

- 8104|クワザワHD

- 2502|アサヒ

- 8958|R-グロバル

- 7878|光・彩

- 7794|G-イーディーピー

- 2117|ウェルネオシュガー

- 9823|マミーマートHD

- 2676|高千穂交

- 5269|日コンクリ

- 5832|ちゅうぎんFG

- 7476|アズワン

- 1720|東急建設

- 3431|宮地エンジ

- 7291|日本プラスト

- 7908|KIMOTO

- 1429|日本アクア

- 143A|G-イシン

- 2469|ヒビノ

- 2668|タビオ

- 3224|G-Gオイスター

- 377A|エージェントIGHD

- 3927|フーバーブレイン

- 3976|G-シャノン

- 4017|G-クリーマ

- 4449|ギフティ

- 4809|パラカ

- 4887|サワイグループHD

- 6050|Eガーディアン

- 6250|やまびこ

- 6267|ゼネパッカー

- 9220|エフビー介護サービス

- 7709|クボテック

- 9878|セキド

- 2338|クオンタムS

- 3571|ソトー

- 6240|ヤマシンフィルタ

- 6800|ヨコオ

- 7460|ヤギ

- 9692|シーイーシー

- 2183|リニカル

- 3320|クロスプラス

- 4635|東インキ

- 9799|旭情報

- 4078|堺化学

- 7172|JIA

- 7990|グローブライド

- 9790|福井コンピ

- 1301|極洋

- 7578|ニチリョク

3042|セキュアヴェイル

297.0

▲ +0.68%

📎 Source:セキュアヴェイル Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SecureVail Co., Ltd. announced its consolidated financial results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026).

- For FY2026, consolidated net sales were ¥1,279 million (up 11.4% year-on-year), gross profit was ¥580 million (up 28.8%), operating income was ¥112 million (up 220.9%), ordinary income was ¥115 million (up 208.2%), and profit attributable to owners of parent was ¥105 million (up 146.9%).

- Net sales, operating income, and ordinary income reached record highs, marking five consecutive years of revenue growth.

- Sales of the amortized software product “LogStare,” which had development expenses fully amortized, contributed to the company’s profitability.

- For FY2027, the company forecasts consolidated net sales of ¥1,438 million (up 12.4% year-on-year), operating income of ¥138 million (up 22.4%), ordinary income of ¥138 million (up 19.9%), and profit attributable to owners of parent of ¥95 million (down 9.5%).

🤖 AI Perspective

The FY2026 results highlight significant revenue and profit growth, with net sales, operating income, and ordinary income reaching record highs. The contribution of sales from the fully amortized “LogStare” software product appears to have played a key role in the improved profitability. Investors may note the FY2027 forecast, which anticipates continued revenue and operating income growth but a decrease in net profit, attributed to an expected increase in corporate income tax due to the elimination of a subsidiary’s accumulated deficit and higher advertising expenses.

4091|日本酸素HD

6270.0

▲ +7.14%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nippon Sanso Holdings released its full-year earnings presentation for the fiscal year ending March 2026 on May 22, 2026.

- All financial KPIs of the previous mid-term management plan, “NS Vision 2026” (Net Sales, Core Operating Income, Adjusted Net D/E Ratio, ROCE after Tax, EBITDA Margin), were achieved.

- Some non-financial KPIs under “NS Vision 2026” were achieved ahead of schedule in the fiscal year ending March 2025.

- The outline of the new mid-term management plan, “Next Innovation 2030”, was presented, indicating a succession and reorganization of the five key strategies.

- During the previous mid-term plan period, the company faced demand fluctuations due to COVID-19, supply chain disruptions, and rising costs from global inflation, with overall product shipment volumes generally remaining sluggish.

1379|ホクト

1884.0

▼ -0.37%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- HOKTO reported consolidated results for the fiscal year ended March 2026, achieving net sales of ¥85.9 billion (up 3.4% year-on-year), operating profit of ¥7.0 billion (up 6.1%), ordinary profit of ¥8.1 billion (up 17.7%), and net profit of ¥7.0 billion (up 57.8%).

- The domestic mushroom business contributed to increased sales and profits due to successful marketing strategies, maintaining stable mushroom prices.

- The chemical products business saw sales increase by ¥1,463 million (12.1%) and operating profit increase by ¥132 million (39.2%), driven by securing large-scale projects.

- The company increased its annual dividend to ¥55 (up ¥5 year-on-year) and enhanced shareholder benefits.

- HOKTO aims for net sales of ¥100 billion, operating profit of ¥10 billion, and an operating profit margin of 10% by the final year of its medium-term management plan, March 2029.

🤖 AI Perspective

The FY2026/3 results indicate that HOKTO achieved increased sales and profits, primarily driven by the successful push for higher unit prices in its domestic mushroom business and large-scale projects in the chemical products segment, despite an unstable cost environment. The announcement of enhanced shareholder returns, alongside progress towards its medium-term management plan, suggests a focus on sustained value creation. The effectiveness of domestic marketing strategies in improving profit margins could be a key factor to monitor.

2623|iSユロIG社債ヘジ

1937.0

▲ +0.31%

📎 Source:iSユロIG社債ヘジ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- iShares Euro IG Corporate Bond ETF (Hedged) (Code: 2623) released its Q4 FY2026 financial results (October 12, 2025 – April 11, 2026) on May 22, 2026.

- As of the end of the current period (April 11, 2026), net assets totaled ¥4,773 million, a decrease of ¥3,140 million compared to the previous period-end.

- The number of outstanding units at the end of the current period was 2,460 thousand units, a decrease of 1,295 thousand units from the previous period-end.

- The net asset value per unit was ¥1,940.28 (a decrease of ¥60.75 from the previous period-end), and the distribution per unit was ¥45 (a decrease of ¥7 from the previous period).

- Total operating revenue was recorded at △¥52,284,618, resulting in an operating loss of △¥60,481,684.

🤖 AI Perspective

These results indicate a decrease in net assets and outstanding units, suggesting that negative trading gains/losses on investment trust beneficiary certificates and negative foreign exchange differences may have impacted operating revenue. Changes in net assets and NAV per unit could be key points of interest for investors monitoring the fund’s size and performance.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

488A|iS円高フォーカス

774.2

▲ +0.03%

📎 Source:iS円高フォーカス Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- iShares Yen Focus ETF (Nickname: Yen Hunter, Ticker: 488A) announced its financial results for the Q4 FY2026 period (December 15, 2025 to April 11, 2026).

- As of the end of the period (April 11, 2026), net assets totaled JPY 1,088 million, with the net asset value per unit at JPY 775.034.

- During the period, new subscriptions amounted to 5,005 thousand units and redemptions were 3,600 thousand units, resulting in 1,405 thousand units outstanding at the end of the period.

- The asset breakdown shows that the primary investment asset (government bonds) accounted for JPY 1,072 million, representing 98.5% of the total.

- The statement of income reported total operating revenue of △JPY 93,852,240 and operating loss of △JPY 95,759,140. This included an exchange loss on foreign currency transactions of △JPY 97,111,027.

- The distribution per 10 units was JPY 0.

🤖 AI Perspective

The iShares Yen Focus ETF aims to generate returns in a strengthening yen environment, making its operational performance a key focus for investors. The current financial results indicate that government bonds constitute the majority of the fund’s assets, while exchange rate fluctuations significantly impacted operating revenue. The absence of a distribution suggests that the fund’s strategy or prevailing market conditions may have led to this outcome.

5579|GSI

—

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- GSI Co., Ltd. announced its consolidated financial results for the fiscal year ended March 2026, reporting sales of ¥4,629 million (+9.1% YoY), operating profit of ¥493 million (+21.8% YoY), and net profit attributable to parent company shareholders of ¥376 million (+43.2% YoY).

- The system development business achieved sales of ¥4,546 million (+8.5% YoY) and operating profit of ¥474 million (+7.8% YoY), driven by securing existing and new projects, an increase in operational personnel, and a rise in the average unit price for engineers.

- The employment support business saw robust user numbers at its key locations, resulting in sales of ¥82 million (+65.7% YoY) and achieving an operating profit of ¥19 million for the full year, moving from a prior year loss.

- Operating profit analysis indicated that increased gross profit, stemming from higher average engineer unit prices and increased personnel, more than offset increased costs from human capital investment and license fees for enhanced package sales.

- The company maintained a strong financial foundation with an equity ratio of 67.6% and generated ¥462 million in cash flow from operating activities.

🤖 AI Perspective

GSI’s FY2026 results suggest that strategic personnel allocation and rising unit prices in the system development business, combined with the employment support business turning profitable, were key drivers of overall performance. Exceeding initial plans for sales, operating profit, and net profit could indicate effective business operations and successful growth strategies. The ability to achieve revenue growth that surpasses ongoing human capital investments might be a factor worth monitoring for future corporate value enhancement.

1595|NZAM Jリート

1839.0

▼ -0.65%

📎 Source:NZAM Jリート Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- NZAM J-REIT (Code: 1595) announced its financial results for the April 2026 fiscal period (October 16, 2025 – April 15, 2026).

- Net assets for the April 2026 period were ¥169,896 million, a decrease from ¥198,486 million in the October 2025 period.

- Total outstanding units at the end of the current period were 86,469 thousand units, down from 101,253 thousand units at the end of the previous period.

- Distribution per unit for the April 2026 period was ¥25.7, an increase from ¥24.8 in the October 2025 period.

- The 100-unit NAV for the current period was ¥196,483, showing an increase compared to ¥196,030 in the October 2025 period.

🤖 AI Perspective

The latest results show a decrease in net assets and outstanding units, while distribution per unit and 100-unit NAV have increased. The rise in distribution per unit could be viewed favorably by investors. Additionally, the trading unit was changed from 10 units to 1 unit on January 31, 2026, which may influence market liquidity moving forward and is a factor worth monitoring.

3675|クロスマーケティング

594.0

▲ +2.77%

📎 Source:クロスマーケティング Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the nine months ended March 31, 2026, cumulative sales totaled ¥23.6 billion (up 5.9% year-on-year), and operating profit was ¥2.12 billion (down 10.6% year-on-year).

- Sales for the third quarter (January-March) alone reached a record ¥8.49 billion.

- The Digital Marketing segment recorded cumulative sales of ¥10.78 billion (up 14.3% year-on-year) and segment profit of ¥0.86 billion (up 19% year-on-year) for the nine-month period.

- The Research & Insight segment’s cumulative sales were ¥12.81 billion (down 0.2% year-on-year), with domestic sales increasing but international sales declining. However, the segment’s sales turned to growth in the third quarter (January-March).

- In April 2026, Cross Marketing Group made DIGITALIO, Research Panel, and Startling Co., Ltd. consolidated subsidiaries.

- The full-year forecast for the fiscal year ending June 2026 remains unchanged, with projected sales of ¥32.0 billion and operating profit of ¥2.8 billion.

🤖 AI Perspective

Cross Marketing Group’s Q3 results highlight record cumulative sales, primarily driven by strong performance in its Digital Marketing segment. The three M&A transactions completed in the third quarter could significantly impact future business growth strategies, potentially enhancing both digital marketing and research capabilities. Investors may wish to monitor the performance of the international segment and the progress toward achieving the full-year forecast, which typically has a stronger second half.

8104|クワザワHD

608.0

▲ +0.16%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- KUWAZAWA HD reported consolidated revenue of ¥64.802 billion for the fiscal year ended March 2026, a 0.9% decrease year-over-year, and operating profit of ¥1.378 billion, a 5.8% decrease year-over-year.

- Net profit attributable to owners of the parent increased by 44.2% year-over-year to ¥1.078 billion.

- By segment, Construction Materials revenue was ¥34.926 billion (up 1.9% YoY) with segment profit of ¥673 million (down 4.4% YoY), while Construction Works revenue was ¥25.725 billion (down 4.7% YoY) with segment profit of ¥453 million (down 1.0% YoY).

- For the fiscal year ending March 2027, the consolidated forecast projects revenue of ¥68.000 billion (up 4.9% YoY), operating profit of ¥1.650 billion (up 19.7% YoY), and net profit attributable to owners of the parent of ¥1.150 billion (up 6.7% YoY), with operating, ordinary, and net profits expected to reach record-high levels.

- The company announced a dividend of ¥26 per share for FY2026/3, an ¥8 increase from the previous year, and stated that for FY2027/3 and beyond, it aims for continuous dividend payments with a consolidated payout ratio target of 40%.

🤖 AI Perspective

The significant increase in net profit attributable to owners of the parent for FY2026/3, despite a slight decline in revenue, suggests improved profitability at the bottom line, potentially driven by factors such as an increase in equity method investment income and a reduction in one-time expenses. The record-high performance projected for FY2027/3, particularly the substantial increase in operating profit, could indicate the positive impact of reduced one-time costs from the previous period and ongoing improvements in business segment profitability. The commitment to a 40% consolidated dividend payout ratio for future periods may be viewed favorably by investors seeking stable shareholder returns.

2502|アサヒ

1563.0

▼ -1.14%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Asahi Group Holdings has postponed the announcement of its Q1 FY2026 financial results, with no new date set yet.

- The postponement is a direct consequence of system disruptions caused by a cyberattack that occurred on September 29, 2025.

- In constant currency terms, Europe’s Q1 revenue decreased by 2.4% year-on-year, and operating profit declined by an early double-digit percentage. Operating profit, however, progressed in line with annual plans due to cost efficiencies.

- Asia-Pacific’s Q1 revenue increased by 1.5% year-on-year, and operating profit grew by a mid-single-digit percentage. Both revenue and operating profit were slightly below annual plans.

- For Japan and East Asia, Q1 revenue and operating profit are not yet finalized due to the system disruption. However, sales trends for major Japanese businesses for January-March 2026 were provided (Asahi Breweries: 84% of prior year, Asahi Soft Drinks: 88%, Asahi Group Foods: 98%).

- The full-year FY2026 financial forecast is scheduled to be released during the FY2025 full-year earnings announcement, which is planned for July 8.

🤖 AI Perspective

The delay in earnings announcement due to a cyberattack highlights potential challenges in timely financial reporting, which could be a point of focus for investors regarding corporate governance and risk management. While overseas business segments show mixed results, the undefined financial impact on the Japan and East Asia segments remains a key area of uncertainty for the overall group performance. Investors may closely monitor the company’s progress in restoring full system functionality and its ability to achieve full-year targets given the ongoing disruptions.

8958|R-グロバル

114700.0

▼ -1.12%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Global One Real Estate Investment Corporation (Code: 8958) announced a partial correction to its “45th Fiscal Period (March 2026) Financial Results Presentation Material” on May 22, 2026.

- The correction pertains to the document originally released on May 21, 2026.

- The reason for the correction was an error found in Note 3 under “2. Progress of Medium-Term Growth Strategy (April 2025 – March 2028)”.

- The specific correction is located on page 7 of the material, within Note 3 of “2. Progress of Medium-Term Growth Strategy (April 2025 – March 2028)”.

- The correction alters the description of rent holidays: the original stated “rent holidays of 1 month in odd fiscal periods and 3 months in even fiscal periods until December 2028,” which has been corrected to “rent holidays of 1 month in even fiscal periods and 3 months in odd fiscal periods until December 2028.”

🤖 AI Perspective

This correction addresses a specific detail regarding rent holidays within the medium-term growth strategy. For investors, information on rent holidays can be relevant for understanding the timing of revenue recognition and cash flow. Therefore, this adjustment may warrant attention when assessing the investment corporation’s financial projections. Continued monitoring of the investment corporation’s disclosures would be prudent to understand any broader implications of this correction.

7878|光・彩

865.0

▲ +0.70%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hikari & Sai Inc. announced on May 22, 2026, that its parent company, ESTIO Co., Ltd., has finalized its financial results for the fiscal year ended February 2026.

- As of February 28, 2026, ESTIO’s total assets amounted to ¥469,712 thousand, total liabilities were ¥232,971 thousand, and total net assets were ¥236,740 thousand.

- ESTIO’s income statement for the period from March 1, 2025, to February 28, 2026, reported net sales of ¥794 thousand, an operating loss of ¥10,915 thousand, ordinary income of ¥8,279 thousand, and net income of ¥8,208 thousand.

- ESTIO holds ¥463,966 thousand in subsidiary shares under “Investments and other assets.”

- The major shareholders are Eiji Fukasawa, holding 19,210 shares (96.05%), and Akihiko Fukasawa, holding 790 shares (3.95%), totaling 100.00% of the outstanding shares.

🤖 AI Perspective

The disclosed financial results for parent company ESTIO show a net income of ¥8,208 thousand for the period, which appears to be primarily driven by dividend income of ¥20,370 thousand, contributing to ordinary income despite an operating loss. The substantial holding of ¥463,966 thousand in subsidiary shares as a significant portion of fixed assets on ESTIO’s balance sheet indicates a notable aspect of its asset structure. This information regarding the parent company may offer indirect insights into the operational context of its listed subsidiary, Hikari & Sai.

7794|G-イーディーピー

1131.0

▲ +4.14%

📎 Source:G-イーディーピー Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 2026, consolidated sales were 516 million JPY, marking a 42.8% decrease compared to the previous fiscal year.

- Operating loss was 1,360 million JPY, ordinary loss was 1,341 million JPY, and net loss attributable to parent company shareholders was 2,415 million JPY.

- The decline in sales was primarily due to the underperformance of seed crystal sales at SFD India, although sales of substrates and wafers increased due to orders from domestic automotive companies, diamond device ventures, and universities.

- In April 2025, the company launched 1-inch wafers and began development of 2-inch mosaic wafers.

- The production and sale of blue and pink colored diamond gemstones commenced, with the company exhibiting at the Tokyo International Jewellery Exhibition.

- A total of 707 million JPY was raised through the exercise of stock acquisition rights during the fiscal year ended March 2026.

🤖 AI Perspective

G-EDP’s financial results for FY2026/3 indicate a challenging period primarily due to sluggish seed crystal sales, yet a notable increase in substrate and wafer sales suggests a potential shift in business focus. The initiation of large wafer development and colored diamond gemstone sales could represent strategic moves to diversify future revenue streams. Investors may find it worthwhile to monitor how these new business segments contribute to the company’s performance going forward.

2117|ウェルネオシュガー

2617.0

▲ +0.27%

📎 Source:ウェルネオシュガー Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Welneo Sugar announced its organizational structure and executive appointments effective October 1, 2026, following the absorption merger with its consolidated subsidiary, Toyo Seito Co., Ltd.

- A new “Functional Materials Division” will be established, integrating Welneo Sugar’s Neo Functional Materials Department and Toyo Seito’s functional materials business-related departments, comprising four departments and one office.

- Hiroki Anzai will assume the role of Executive Officer, Head of the Functional Materials Division, effective October 1, 2026 (currently Executive Officer, in charge of Neo Functional Materials Department).

- Three new Directors will be appointed: Takashi Matsuzawa as Director, Strategy and Planning Manager of the Functional Materials Division; Kazuaki Takayanagi as Director, Deputy Head of the Production Division; and Kyoji Tsunashima as Director, Research and Development Manager of the Functional Materials Division.

- Takashi Matsuzawa is scheduled to be appointed Representative Director and President Executive Officer of Toyo Seito Co., Ltd. effective June 18, 2026.

🤖 AI Perspective

This announcement suggests a clear strategic focus on strengthening the “functional materials” domain within the post-merger structure. The establishment of a new division dedicated to functional materials and the pre-emptive appointment of its key personnel prior to the merger’s effective date could indicate a proactive approach to integration and future growth. Investors may interpret these changes as an effort to maximize synergies and drive innovation in specialized material segments.

9823|マミーマートHD

1042.0

▲ +1.26%

📎 Source:マミーマートHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Mammy Mart Holdings Co., Ltd. announced its interim financial results presentation materials for the fiscal year ending September 2026 (October 1, 2025 – March 31, 2026).

- For the first half, operating revenue reached ¥112,902 million (up 20.9% year-on-year), operating profit was ¥4,356 million (up 0.8%), ordinary profit ¥4,761 million (up 4.9%), and net profit attributable to parent company shareholders ¥3,223 million (up 4.9%).

- The company opened 6 new stores and renovated 2 existing stores, totaling 8 projects, indicating that the expansion phase is progressing as planned.

- Full-year forecasts for FY2026 remain unchanged: operating revenue ¥235,000 million, operating profit ¥7,000 million, ordinary profit ¥7,600 million, and net profit ¥5,300 million.

- The group’s first fresh fish processing center commenced operations in April 2026, aiming to improve store operational efficiency, expand product assortment, and enhance freshness.

🤖 AI Perspective

Mammy Mart HD’s first-half results show significant revenue and profit growth, primarily driven by new store openings and renovations. The company’s strategic investments in new facilities like the fresh fish processing center and MD support systems could bolster long-term competitiveness. However, the softening growth rate of existing stores and a declining trend in ordinary profit margin are points investors may wish to monitor in the coming quarters.

2676|高千穂交

1991.0

▲ +0.40%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Takachiho Koheki Co., Ltd. announced its full-year results for the fiscal year ended March 2026, reporting net sales of ¥29,510 million (+5.0% year-on-year), operating profit of ¥2,098 million (+0.9% year-on-year), and ordinary profit of ¥2,408 million (+20.1% year-on-year).

- Operating profit and ordinary profit reached record highs since listing.

- By segment, the Business Security division achieved increased revenue and profit with net sales of ¥15,152 million (+10.5% year-on-year) and operating profit of ¥1,402 million (+21.6% year-on-year). The Electromechanical division saw a decrease in both revenue and profit, with net sales of ¥14,358 million (-0.2% year-on-year) and operating profit of ¥695 million (-24.9% year-on-year).

- For the fiscal year ending March 2027, the company forecasts net sales of ¥32,000 million, operating profit of ¥2,350 million, ordinary profit of ¥2,300 million, and net profit of ¥1,650 million.

- The company plans to adopt a progressive dividend policy starting from the fiscal year ending March 2027, with an annual dividend of ¥76 per share, maintaining the same amount as the previous year.

🤖 AI Perspective

The FY2026/3 financial results highlight the strong performance of the Business Security segment, which propelled overall operating and ordinary profits to record highs. Conversely, the decline in the Electromechanical segment’s profitability could be a point of continued monitoring. The announced progressive dividend policy for FY2027/3 onwards may suggest a commitment to shareholder returns, potentially fostering expectations for sustained enhancement of shareholder value.

5269|日コンクリ

326.0

▲ +0.31%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- NICCON Corporation resolved to merge its wholly-owned subsidiary, NC Management Service Co., Ltd., via absorption, at a Board of Directors meeting on May 22, 2026, and signed the merger agreement on the same day.

- The effective date of the merger is scheduled for October 1, 2026.

- The purpose of this merger is to centralize operations and enhance group management efficiency.

- The merger format is an absorption-type merger, with NICCON Corporation as the surviving company and NC Management Service Co., Ltd. as the absorbed company.

- A special loss (difference from extinguished intercompany shares) is expected to be recorded in NICCON Corporation’s non-consolidated financial statements due to the merger, but this difference will be eliminated in the consolidated financial statements, resulting in no impact on consolidated earnings.

🤖 AI Perspective

NICCON’s absorption-type merger of its wholly-owned subsidiary suggests a strategic move to optimize internal resources and improve operational efficiency across the group. While a special loss is anticipated in non-consolidated accounts, the explicit statement of no impact on consolidated earnings may be a key point for investors. As a merger with a wholly-owned subsidiary, the absence of new share issuance or cash consideration is also noteworthy.

5832|ちゅうぎんFG

3134.0

▼ -0.82%

📎 Source:ちゅうぎんFG Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Chugin Financial Group, Inc. announced on May 22, 2026, the addition of supplementary materials to its “Consolidated Financial Results for the Fiscal Year Ending March 31, 2026 (Japanese GAAP).”

- The added materials include “FY2025 Financial Highlights (Additional)” and “FY2026/3 Financial Results Presentation Materials (Additional).”

- The “FY2025 Financial Highlights (Additional)” reported total capital of 640.6 billion yen (an increase of 75.7 billion yen from FY2025/3) and Common Equity Tier 1 (CET1) of 583.9 billion yen (an increase of 64.0 billion yen) as of the end of March 2026. The consolidated leverage ratio was 5.57% (regulatory minimum 3.15%), and the Liquidity Coverage Ratio (LCR) was 145.8% (regulatory minimum 100%).

- The “FY2026/3 Financial Results Presentation Materials (Additional)” provided detailed net interest margins for The Chugoku Bank (standalone, covering all branches, domestic, and international operations), as well as capital ratios (under international uniform standards) for both Chugin Financial Group (consolidated) and The Chugoku Bank (standalone).

- As of the end of March 2026, the consolidated total capital ratio for Chugin Financial Group was 13.35%, and the standalone total capital ratio for The Chugoku Bank was 14.23%.

🤖 AI Perspective

The addition of these supplementary materials could provide investors with a more comprehensive view into Chugin Financial Group’s financial health and profitability. Key metrics like capital ratios, leverage ratios, and the Liquidity Coverage Ratio, which are crucial for assessing a financial institution’s stability under Basel regulations, have been further elaborated, enhancing transparency. Additionally, the detailed breakdown of net interest margins for The Chugoku Bank on a standalone basis may assist in understanding the revenue structure across different business segments.

7476|アズワン

2083.0

▼ -0.10%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- AS ONE Corporation announced record-high consolidated net sales of ¥110.6 billion (+6.7% YoY) and operating profit of ¥12.8 billion (+10.7% YoY) for the fiscal year ended March 2026.

- The company achieved its 16th consecutive year of revenue growth, with operating profit increasing by double digits due to effective cost control.

- By segment, the Lab & Industry division showed strong growth of 8.3% driven by a 12.8% increase in e-commerce sales, while the Medical division saw a 1.0% decrease.

- The annual dividend per share was ¥65.0 (+¥3.0 YoY), marking the 15th consecutive year of dividend increases, with a payout ratio of 50.6%.

- The company conducted a share buyback of approximately ¥1 billion through market purchases, resulting in a total shareholder return ratio of 61.5% and a record-high ROE of 13.3%.

🤖 AI Perspective

AS ONE’s FY2026/3 results highlight strong financial performance, with both sales and operating profit reaching record highs and marking 16 consecutive years of revenue growth. The robust growth in the Lab & Industry segment, coupled with double-digit operating profit expansion driven by efficient cost management, suggests the company’s business strategies are proving effective. Furthermore, the 15th consecutive dividend increase and the share buyback program indicate a strong commitment to shareholder returns and capital efficiency, which could be viewed positively by investors.

1720|東急建設

1165.0

▼ -1.19%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tokyu Construction announced a partial correction to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 (Japanese GAAP).”

- The reason for the correction was an error found in the aggregation of certain transactions within the reportable segment information (real estate business, etc.).

- The corrections are located in the “Segment Information, etc.” section under “Notes to Consolidated Financial Statements,” specifically in “3. Information on Sales, Profit or Loss, and Breakdown of Revenue by Reportable Segment.”

- Specifically, “Revenue from contracts with customers” for the real estate business, etc., was corrected from 6,046 million yen to 6,001 million yen (a difference of 45 million yen).

- Similarly, “Other revenue” for the real estate business, etc., was corrected from 1,547 million yen to 1,592 million yen (a difference of 45 million yen).

- Post-correction, there are no changes to “Net sales to external customers” or “Segment profit” for the real estate business, etc.

🤖 AI Perspective

This correction stems from an internal aggregation error within the real estate business segment, and it is notable that there is no change to the total net sales to external customers or segment profit. The adjustment appears to be a reclassification between different revenue items, which might suggest a limited impact on the overall financial position. However, from an internal control perspective, the circumstances leading to such aggregation errors could be an area worth monitoring.

3431|宮地エンジ

1504.0

▲ +2.24%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Miyaji Engineering announced its FY2026/3 financial results presentation material on May 22, 2026.

- For the fiscal year ended March 2026, order intake was ¥50.57 billion, marking a 29.2% decrease year-on-year.

- Net sales for the same period amounted to ¥56.65 billion, a 24.2% decrease compared to the previous fiscal year.

- Operating profit decreased by 50.6% to ¥4.52 billion, ordinary profit by 49.1% to ¥4.83 billion, and profit attributable to owners of parent by 32.7% to ¥3.26 billion.

- Key factors contributing to the decrease in revenue and profit include the absence of intensive large-scale renewal and maintenance projects, alongside a challenging business environment.

- In the core bridge business, new construction orders decreased to ¥199.0 billion (vs. ¥252.5 billion prior year) in monetary value and 96 thousand tons (vs. over 100 thousand tons prior year) in steel weight.

🤖 AI Perspective

Miyaji Engineering’s FY2026/3 results indicate a broad-based decline across order intake, sales, and all profit metrics compared to the previous year. The absence of large-scale, intensive renewal and maintenance projects appears to be a significant factor impacting overall performance. Investors may also consider the broader macroeconomic challenges, such as a downtrend in public investment and rising construction costs, which could continue to influence the company’s operational landscape.

7291|日本プラスト

462.0

▼ -0.43%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nihon Plast Co., Ltd. reported consolidated results for the fiscal year ended March 31, 2026, with net sales of ¥114,861 million (down 4.8% year-on-year), operating profit of ¥2,647 million (down 4.5% year-on-year), ordinary profit of ¥2,499 million (up 24.5% year-on-year), and net profit attributable to owners of parent of ¥2,012 million.

- By segment, sales decreased in Japan (△6.0%), China (△20.8%), and Asia (△16.2%), while North America saw an increase (+1.1%).

- By product, airbag sales decreased by 12.1% year-on-year, but steering wheel and resin component sales remained at a similar level to the previous year.

- For the fiscal year ending March 31, 2027, the company forecasts net sales of ¥118,000 million (up 2.7% year-on-year), operating profit of ¥2,400 million (down 9.4% year-on-year), ordinary profit of ¥2,000 million (down 20.0% year-on-year), and net profit attributable to owners of parent of ¥1,600 million.

- The dividend per share for FY2026/3 was ¥30.00, and the forecast for FY2027/3 is ¥25.00.

🤖 AI Perspective

Despite a decrease in net sales, Nihon Plast achieved a significant increase in ordinary profit for FY2026/3, which may suggest that rationalization efforts and fixed cost reductions partially offset the impact of reduced revenue and increased variable costs. However, the FY2027/3 outlook projects increased revenue but decreased profit, indicating that the forecasted exchange rates and increased capital expenditures could impact profitability and warrant close monitoring by investors.

7908|KIMOTO

224.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- KIMOTO announced its consolidated financial results for the fiscal year ended March 2026.

- Consolidated net sales were ¥10,546 million (98.6% of budget ¥10,700 million), and operating profit was ¥1,064 million (96.7% of budget ¥1,100 million).

- Consolidated net profit for the period was ¥565 million, a decrease of ¥647 million from the previous year’s ¥1,212 million. Key factors contributing to the decline in net profit included a decrease in ordinary profit, the occurrence of extraordinary losses, and adjustments to income taxes.

- The full-year earnings forecast for the fiscal year ending March 2027 is undetermined, citing “high uncertainty in the business environment, such as the impact on crude oil and naphtha procurement due to tensions in the Middle East, making it difficult to calculate a reasonable earnings forecast at this time.”

- By segment, sales for the High-Performance Materials business were ¥9,590 million (down 5.0% year-on-year), and for the Digital Twin business were ¥358 million (down 8.8% year-on-year). Sales for “Industrial Equipment” within the High-Performance Materials business increased by 22.5% year-on-year.

🤖 AI Perspective

KIMOTO’s FY2026/3 results show net sales and operating profit near budgeted levels, but a significant decline in net profit is a key point. The decision to keep the FY227/3 forecast undetermined highlights the high level of current business environment uncertainty. While growth in the “Industrial Equipment” segment within High-Performance Materials indicates strength in specific areas, revenue decreases in other segments and overseas operations appear to have impacted overall performance.

1429|日本アクア

708.0

▲ +1.43%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Nihon Aqua Co., Ltd. announced on May 22, 2026, a “Correction Regarding a Part of Market Environment Information in the Q1 FY2026 Financial Results Briefing Material.”

- The correction pertains to the “Q1 FY2026 Financial Results Briefing Material” originally published on May 8, 2026.

- The reason for the correction was an error in the description of supply from building material manufacturers within the “Market Environment: Continued Price Hikes for All Building Materials, Supply Constraint Risks Also Materializing” section (page 6) of the briefing material, which differed from the intent of each company’s publicly disclosed information.

- The specific parts corrected relate to the descriptions concerning Achilles Corporation and Asahi Kasei Construction Materials Corporation.

- The affected document has already been replaced on Nihon Aqua’s official website.

🤖 AI Perspective

- This correction highlights Nihon Aqua’s commitment to ensuring the accuracy of information provided, especially concerning market conditions and supply constraints from building material manufacturers.

- Financial briefing materials are a critical resource for investors, and such corrections may indicate a focus on transparent information disclosure by the company.

- With the updated material already available, investors can access the latest and accurate information to evaluate the company’s situation, which could be beneficial for informed decision-making.

143A|G-イシン

698.0

▼ -0.43%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-ISIN’s Board of Directors resolved on May 22, 2026, to conduct an absorption-type merger (simplified merger) with its wholly-owned subsidiary, OK Junction Co., Ltd.

- The effective date of the merger is scheduled for October 1, 2026.

- G-ISIN will be the surviving company, and OK Junction Co., Ltd. will be the absorbed company.

- No new shares will be issued, and no cash or other assets will be allotted in connection with this merger.

- A loss on cancellation of treasury stock is expected to be recorded as an extraordinary loss in G-ISIN’s non-consolidated financial statements due to the merger, but there will be no impact on consolidated net income.

🤖 AI Perspective

This merger aims to further accelerate group growth by enhancing synergies with OK Junction, which has already been integrated into the group through M&A. As a merger with a wholly-owned subsidiary, it is conditioned upon approval of the merger agreement at G-ISIN’s ordinary general meeting of shareholders scheduled for June 26, 2026. While an extraordinary loss is anticipated in the non-consolidated financial statements, the absence of an impact on consolidated earnings suggests a limited effect on the overall group’s financial health.

2469|ヒビノ

2825.0

▲ +0.82%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Hibino Corporation resolved to execute an absorption-type merger where Hibino Space Tech Co., Ltd. will be the surviving company and Hibino Imaginia Ring Co., Ltd. will be the dissolving company.

- The effective date of the merger is scheduled for October 1, 2026.

- The purpose of this merger is to consolidate management resources, strengthen sales capabilities, and streamline business operations to achieve further growth.

- Hibino Space Tech Co., Ltd. (surviving company) engages in the sale, system design, construction, and maintenance of professional audio and video equipment, while Hibino Imaginia Ring Co., Ltd. (dissolving company) focuses on the sale, system design, construction, and maintenance of professional audio and video equipment for cinemas and halls.

- As this is a merger between consolidated subsidiaries of Hibino Corporation, there will be no allocation of shares or other property, and the impact on Hibino’s consolidated financial performance is stated to be minor.

🤖 AI Perspective

This merger between consolidated subsidiaries aims to enhance sales and streamline business operations by consolidating management resources. Integrating subsidiaries with similar business scopes could potentially lead to reduced redundancies and an expanded customer base. Since the impact on Hibino’s consolidated performance is stated as minor, this move may be viewed as part of a broader organizational restructuring effort to improve overall group efficiency.

2668|タビオ

1277.0

▲ +1.67%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tabio Corporation announced the financial results for the fiscal year ended February 2026 (March 1, 2025, to February 28, 2026) of its non-listed parent company, Ochi Sangyo Co., Ltd.

- Ochi Sangyo Co., Ltd. does not engage in business activities. Its voting rights ownership in Tabio Corporation was 27.33% as of February 28, 2026.

- As of February 28, 2026, Ochi Sangyo’s balance sheet showed total assets of ¥1,533,474 thousand and total net assets of ¥1,353,151 thousand. “Shares of affiliated companies” accounted for ¥1,327,876 thousand.

- For the fiscal year ended February 2026, Ochi Sangyo reported an operating loss of ¥1,607 thousand, but non-operating income, including dividends received of ¥55,560 thousand, resulted in a net income of ¥52,055 thousand.

- The major shareholders of Ochi Sangyo Co., Ltd. are Ms. Keiko Ochi and Mr. Yasuhiko Ochi, each holding 49.18% of the shares, and they also serve as directors.

🤖 AI Perspective

Given that the parent company, Ochi Sangyo Co., Ltd., does not conduct business activities and largely depends on dividend income for its revenue, the dividend policies of affiliated companies, including Tabio, likely significantly impact its financial performance. The fact that a substantial portion of Ochi Sangyo’s assets consists of shares in affiliated companies like Tabio could indicate a direct link between Tabio’s corporate value and its parent company’s asset value. This disclosure of the non-listed parent company’s information is considered a critical factor for investors to understand the controlling shareholder structure of the listed company, Tabio.

3224|G-Gオイスター

755.0

▲ +1.07%

📎 Source:G-Gオイスター Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-G Oyster Co., Ltd. announced a merger between its wholly-owned subsidiaries, Marine Deep Seawater Oyster Center Co., Ltd. and Japan Oyster Center Co., Ltd., resolved at a Board of Directors meeting on May 22, 2026.

- The effective date of the merger is scheduled for July 1, 2026.

- The merger will be an absorption-type merger, with Marine Deep Seawater Oyster Center Co., Ltd. as the surviving company and Japan Oyster Center Co., Ltd. as the absorbed company.

- The purpose of this merger is to integrate the oyster purification business and oyster wholesale business, thereby unifying the group’s oyster business supply chain.

- Expected outcomes include strengthening quality control, improving logistics and inventory management efficiency, optimizing management resources, and enhancing the revenue structure.

🤖 AI Perspective

This merger appears to be a strategic move by G-G Oyster to streamline its core oyster business operations by integrating the purification and wholesale segments. By consolidating these functions, the company aims to enhance overall operational efficiency and strengthen quality control across the supply chain, from procurement to sales. While the company stated that the impact on its consolidated financial performance is expected to be minor due to the merger being between wholly-owned subsidiaries, the long-term benefits of improved food safety and potential profitability through synergistic operations could be worth monitoring.

377A|エージェントIGHD

—

▲ +0.00%

📎 Source:エージェントIGHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- The company experienced a strong start in Q1 FY2026, but the full-year performance forecast remains unchanged.

- The decision to maintain the full-year forecast is attributed to planned strategic upfront investments aimed at strengthening “governance infrastructure,” “next-generation human resources infrastructure,” and “productivity/DX infrastructure” for a transition to a “high-profit, high-leverage structure” from 2027 onwards.

- M&A targets are being expanded beyond conventional exclusive agencies to include “large exclusive agencies,” “in-house agencies,” and “related businesses in other industries.”

- A new shareholder benefit program has been introduced with the goal of enhancing investment appeal and encouraging long-term support from investors.

- The acquisition of shares in Fujikoshi Sogo Hoken Jimusho Co., Ltd. is part of a business succession strategy aimed at strengthening the customer base in the Fukuoka area.

- The company acknowledges the U.S. market as the world’s largest insurance market, believing its cultivated business succession know-how and “insurance agency support platform” model can be effectively utilized there, and is steadily preparing its local structure.

- The mutual customer referral program with Matsui Securities is not currently factored into the earnings forecast and is considered an additional upside contributor.

🤖 AI Perspective

The decision to maintain the full-year forecast despite a strong Q1 performance suggests a focus on strategic long-term investments for future growth, rather than short-term adjustments. The expansion of M&A targets to include larger and in-house agencies indicates a proactive approach to industry restructuring driven by regulatory changes, aiming for sustained customer base expansion. Furthermore, the introduction of a shareholder benefit program and the strategic move into the U.S. market could signal efforts to enhance investor engagement and pursue new growth opportunities.

3927|フーバーブレイン

940.0

▲ +2.29%

📎 Source:フーバーブレイン Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Fuva Brain Co., Ltd. released the video and materials for its Q3 FY2026 earnings presentation (for institutional investors and analysts) on May 22, 2026.

- For the fiscal year ended March 2026, adjusted sales reached ¥6,057 million (up 38.5% from the previous period), and adjusted operating profit was ¥734 million (up 152.7% from the previous period).

- Net profit attributable to owners of the parent company was ¥308 million (up 181.9% from the previous period).

- The IT Tools segment recorded sales of ¥3,219 million and a profit of ¥300 million (profit margin of 9.3%).

- The IT Services segment reported sales of ¥2,421 million and a profit of ¥335 million (profit margin of 13.9%).

🤖 AI Perspective

Fuva Brain’s Q3 FY2026 earnings presentation materials indicate significant revenue and profit growth, driven by expansion in its core IT Tools and IT Services businesses, alongside capital gains from investment activities. The adjusted sales and operating profit figures may suggest robust underlying business performance. While net profit also showed substantial growth, the company noted an impact from M&A-related taxation, which could be a factor for investors to monitor in future M&A strategies.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

3976|G-シャノン

468.0

▼ -0.64%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Shannon reported for Q1 FY2026 sales of ¥744 million, gross profit of ¥528 million (gross profit margin 71.0%), operating profit of ¥174 million, ordinary profit of ¥174 million, and net income attributable to owners of parent of ¥159 million.

- The operating profit of ¥174 million marks a new quarterly record high for the company.

- Profitability improvements were attributed to the contribution from Innovation X Solutions (IX) acquired at the end of the previous fiscal year, restructuring of unprofitable businesses, control of selling, general and administrative expenses, and productivity enhancements.

- Operating profit turned positive for the first time in four periods, following operating losses since FY2022, under a profit-oriented management policy.

- By segment, subscription revenue in the Marketing Cloud business performed strongly at ¥515 million, aided by IX, with the recurring revenue ratio increasing to 69.3%.

4017|G-クリーマ

216.0

▼ -0.92%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Creema Inc. announced on May 22, 2026, a partial correction to its “Consolidated Financial Results for the Fiscal Year Ending February 2026.”

- The corrections cover “Summary Information,” “1. Consolidated Results for the Fiscal Year Ended February 2026 (1) Consolidated Operating Results,” “(Reference) Summary of Non-consolidated Results (1) Non-consolidated Operating Results,” “Appendix Page 11: 3. Consolidated Financial Statements and Principal Notes (4) Consolidated Statements of Cash Flows,” and “Appendix Page 15: 3. Consolidated Financial Statements and Principal Notes (5) Notes to Consolidated Financial Statements (Per Share Information).”

- In the “Consolidated Operating Results,” the “Diluted earnings per share” for the fiscal year ended February 2026 was corrected from “4.08 yen” to “— (hyphen).”

- In the “Non-consolidated Operating Results,” the “Diluted earnings per share” for the fiscal year ended February 2026 was corrected from “5.52 yen” to “— (hyphen).”

- In the “Consolidated Statements of Cash Flows,” the order of “Proceeds from issuance of shares” and “Proceeds from issuance of shares by exercise of share options” within “Cash flows from financing activities” was swapped. The respective amounts (554 thousand yen and 1,876 thousand yen) remain unchanged.

- The PDF document on the company’s IR website has already been updated to reflect these corrections.

🤖 AI Perspective

These corrections primarily involve the presentation of “Diluted earnings per share” and a reordering of certain items within the cash flow statement, without altering key profit and loss figures such as consolidated and non-consolidated net sales, operating income, ordinary income, or net income attributable to owners of the parent. Therefore, the impact on overall business performance is likely to be limited. Investors may wish to review the updated financial statements for precise information.

4449|ギフティ

1123.0

▼ -0.80%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Giftify resolved a capital and business alliance with Kyash Inc. at a board meeting held on May 22, 2026.

- The alliance will enable Giftify to provide functionalities to its corporate and local government clients, utilizing Kyash’s wallet application and remittance solutions.

- Giftify plans to acquire a total of 68,128 shares of Kyash, representing a 19.07% stake, for a total of 1.6 billion yen.

- The execution date for the share acquisition and the commencement date for the capital and business alliance are both scheduled for June 10, 2026.

- Giftify anticipates the impact of this alliance on its consolidated financial results for the full fiscal year ending December 2026 to be minor.

🤖 AI Perspective

This alliance aligns with Giftify’s growth strategy of expanding its e-gift platform. The integration of Kyash’s financial licenses and operational infrastructure could enhance Giftify’s capabilities in addressing diverse needs within the corporate and local government benefits sector. This move may suggest an increased focus on solutions that involve immediate cash-equivalent value transfers, which could be worth monitoring for future service developments.

4809|パラカ

1934.0

▼ -1.23%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Paraca Inc. achieved revenue growth in the second quarter of the fiscal year ending September 2026, primarily due to aggressive new facility openings.

- The company reported a decrease in profit for the quarter, attributed to upfront costs for new parking facilities and the impact of heavy snowfall.

- New parking facilities are expected to contribute to profits from the second half of the fiscal year, with Paraca aiming for a fourth consecutive year of record profits through continued aggressive expansion of both leased and owned parking lots.

- As of March 31, 2026, the total number of managed parking spaces reached 51,000, setting a new record. The company operates in 45 prefectures across Japan (excluding Fukui and Tottori).

- The presentation also included updates on the partnership with Itochu Group and the development of parking facilities attached to other establishments.

🤖 AI Perspective

Paraca’s IR presentation suggests a company actively pursuing long-term growth strategies despite short-term profit setbacks. The expectation of new parking facilities contributing to profits in the latter half of the fiscal year, coupled with record-high operational scale, could indicate potential for future earnings recovery and growth. Given the expanding domestic parking industry market, Paraca’s distinctive strategy centered on owned parking lots may be a key factor in establishing a competitive advantage.

4887|サワイグループHD

1768.0

▲ +0.60%

📎 Source:サワイグループHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sawai Group Holdings Co., Ltd. has resolved to merge its wholly-owned subsidiaries, Sawai Pharmaceutical Co., Ltd. (surviving company) and Trust Pharmatech Co., Ltd. (dissolving company), through an absorption-type merger.

- The effective date of the merger is scheduled for April 1, 2027.

- The purpose of the merger is to strengthen the Group’s management base through effective utilization and efficiency improvement of management resources.

- No new shares will be issued, and no monetary or other allocations will be made in connection with this merger.

- Sawai Pharmaceutical Co., Ltd. is engaged in manufacturing and sales of ethical pharmaceuticals, primarily generic drugs, while Trust Pharmatech Co., Ltd. is engaged in manufacturing ethical pharmaceuticals.

🤖 AI Perspective

This merger appears to be a strategic move to optimize the group’s internal production and sales structure, aiming for greater efficiency. Consolidating a manufacturing-focused subsidiary into the parent pharmaceutical company could streamline supply chains and potentially reduce operational costs. This integration may contribute to strengthening the overall competitiveness of the Sawai Group.

6050|Eガーディアン

1663.0

▼ -0.18%

📎 Source:Eガーディアン Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- E-Guardian Inc. has entered into a stock transfer agreement to acquire all shares of Outsourcing Communications Co., Ltd. (OSCOM), making it a wholly-owned subsidiary.

- This acquisition specifically targets OSCOM’s contact center business; other operations were transferred within the BREXA Group prior to this transaction.

- The scheduled acquisition date is June 1, 2026, with an acquisition cost of 290 million yen, totaling an estimated 294.5 million yen including related expenses.

- OSCOM’s revenue for the past three fiscal years (December 2023 to December 2025) ranged from 1,670,826 thousand yen to 1,821,937 thousand yen.

- This acquisition is positioned as a strategic step in E-Guardian’s development of its next-generation “AI-BPO” model.

🤖 AI Perspective

This acquisition appears to be a key move by E-Guardian to bolster its contact center operations and establish a hybrid outbound platform integrating AI with human interaction. The synergy between OSCOM’s high-quality communication skills and E-Guardian’s AI technology may suggest a strategic aim to create new value in the domestic contact center market. Investors might monitor the potential for short-term cross-selling and profit margin improvements through resource sharing, alongside the long-term shift towards a high-profitability model driven by data accumulation.

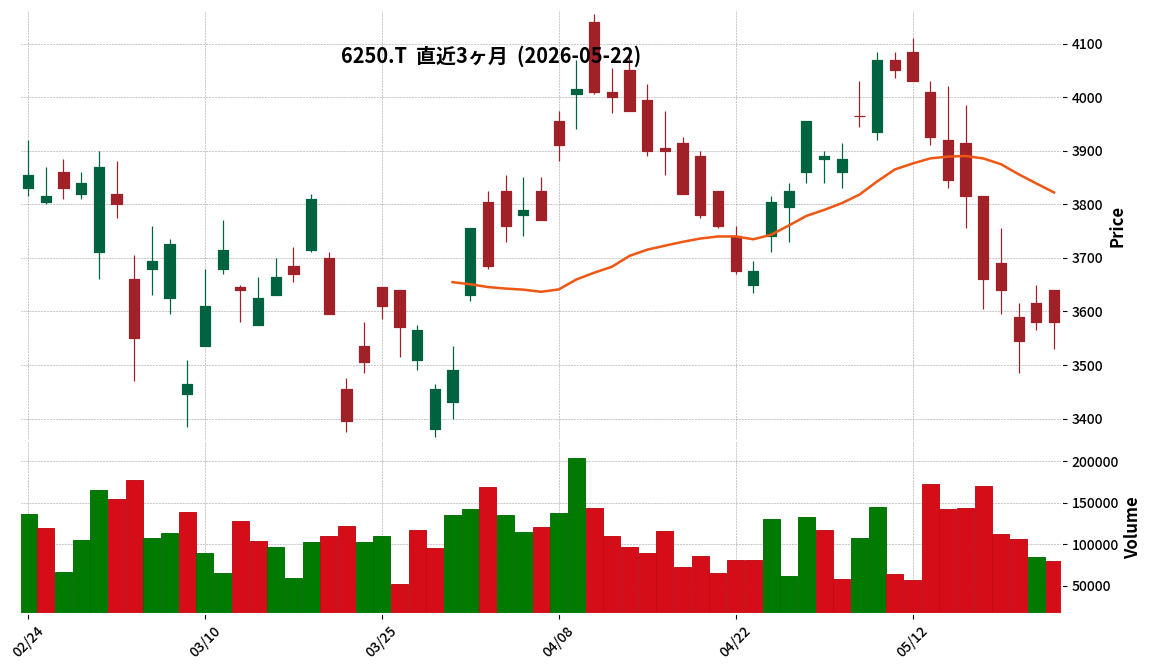

6250|やまびこ

3580.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- YAMABIKO Corporation announced its financial results for the first quarter of the fiscal year ending December 2026.

- Consolidated net sales amounted to ¥49.351 billion, representing a 12.7% increase compared to the same period of the previous year.

- Consolidated operating income was ¥6.500 billion, a 16.6% increase year-on-year.

- Net income attributable to owners of parent reached ¥4.495 billion, up 46.8% from the prior year’s first quarter.

- By segment, Outdoor Power Equipment (OPE) sales were ¥39.100 billion, a 15.3% increase year-on-year, with operating income of ¥8.857 billion, up 9.9%.

- The full-year forecast for FY2026 remains unchanged, projecting net sales of ¥185.0 billion (+6.3% YoY) and operating income of ¥20.0 billion (+2.4% YoY).

🤖 AI Perspective

The announced results highlight the strong performance of the core OPE business, which significantly contributed to the overall increase in sales and profit. This growth was driven by robust sales of riding lawn mowers and chainsaws in the North American market, particularly to home centers, as well as the positive contribution of robotic lawn mowers in the European market. The shift from foreign exchange loss to gain also appears to have boosted ordinary and net profit. The unchanged full-year forecast suggests that management anticipates continued favorable business conditions for the remainder of the fiscal year.

6267|ゼネパッカー

3720.0

▲ +1.36%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Zenepecker Corporation announced the finalization of the financial results for its non-listed parent company, FAMS Co., Ltd., for the fiscal year ended February 2026.

- FAMS Co., Ltd. is described as a company located in Mitsuke City, Niigata Prefecture, engaged in the manufacturing and sales of electrical machinery, equipment, and systems, with a capital of 100 million yen.

- As of February 28, 2026, Yaskawa Electric Corporation holds 100.00% (1,000 shares) of FAMS Co., Ltd.’s shares.

- FAMS Co., Ltd.’s consolidated balance sheet for the fiscal year ended February 2026 showed total assets of 1,357,264 thousand yen and total liabilities and net assets also of 1,357,264 thousand yen.

- FAMS Co., Ltd.’s consolidated statement of income for the fiscal year ended February 2026 reported net sales of 852,845 thousand yen, an operating loss of △90,194 thousand yen, an ordinary loss of △60,219 thousand yen, and a net loss of △45,688 thousand yen.

🤖 AI Perspective

The financial results of a non-listed parent company can offer insights into the business environment and future strategies of its listed subsidiary. Given that FAMS Co., Ltd. is wholly owned by Yaskawa Electric Corporation, understanding its position within the Yaskawa Electric Group and its business collaboration with Zenepecker could be a factor for investors to consider. The financial health and operating performance of the parent company may indirectly influence Zenepecker, making continuous monitoring of related information worthwhile.

9220|エフビー介護サービス

1251.0

▼ -0.16%

📎 Source:エフビー介護サービス Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- FB Care Service achieved record high sales and ordinary profit in the fiscal year ended March 2026. The company stated that operating profit effectively reached its highest level.

- In FY2026/3, the company expanded its business by acquiring two welfare equipment sales offices through M&A (business transfer) and establishing one care service facility (group home) in the care business.

- The severe home care business, which the company entered in April 2025, was withdrawn during the fiscal year ended March 2026.

- An impairment loss was recorded in the care business, as announced on May 15, 2026, regarding “Recording of Extraordinary Losses (Impairment Losses).”

- For the fiscal year ending March 2027, the company plans to convert one existing care facility (residential fee-based nursing home) in Ueda City, Nagano Prefecture, into a group home, and projects a dividend increase of 5 yen per share (interim dividend).

🤖 AI Perspective

The FY2026/3 results, achieving record sales and ordinary profit despite a challenging operational environment of labor shortages and rising costs, are notable. Conversely, the withdrawal from the severe home care business and the recording of impairment losses may suggest a strategic review of the business portfolio and a focus on asset efficiency. The planned second consecutive year of dividend increases could indicate a commitment to shareholder returns.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

7709|クボテック

73.0

▼ -1.35%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kubotech Co., Ltd. announced on May 22, 2026, a correction to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 [Japanese GAAP]” which was originally published on May 15, 2026.

- The primary corrections are in “Summary Information Page 1 (3) Consolidated Cash Flow Statement,” “Attachment Page 3 (3) Overview of Current Period Cash Flows,” and “Attachment Page 10 (4) Consolidated Cash Flow Statement.”

- The Investing Activities Cash Flow for the fiscal year ended March 2026 was revised from “△247 million yen” to “△303 million yen.”

- Consequently, Cash and Cash Equivalents at the end of the period for March 2026 were revised from “169 million yen” to “113 million yen.”

- The correction includes the addition of “expenditure from time deposits of 56 million yen” under investing activities.

🤖 AI Perspective

This correction impacts Kubotech’s cash flow statement for the fiscal year ended March 2026, specifically increasing the outflow from investing activities and reducing the period-end cash and cash equivalents. The revised figures indicate a larger utilization of funds for investments and a lower cash balance compared to the initial disclosure. Investors may wish to monitor how these changes might influence the company’s future liquidity and operational strategies.

9878|セキド

458.0

▲ +1.10%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Sekido Co., Ltd. announced on May 22, 2026, a correction to its “Financial Results for the Fiscal Year Ended March 2026 (Non-consolidated)” initially released on May 7, 2026.

- The reasons for the correction include the additional recognition of impairment losses for some stores based on a more conservative estimation, and errors in some figures presented in the financial statements.

- The revised net loss for the fiscal year ended March 2026 increased from the previously reported ¥1,097 million to ¥1,141 million.

- The equity ratio at the end of March 2026 was revised from the initial 1.9% to 0.9%.

- The reported impairment loss increased from the previous ¥263 million to ¥312 million.

🤖 AI Perspective

This correction indicates that additional impairment losses on certain stores have impacted the company’s net income and financial position. The revision of the equity ratio, a key indicator of financial health, may be a point of interest for investors. The inclusion of errors in the financial statement figures could suggest a need for enhanced internal review processes.

2338|クオンタムS

106.0

▲ +4.95%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Quantum Solutions Co., Ltd. resolved to acquire all shares of its equity-method affiliate, Compass Cloud AI Japan Inc., making it a wholly-owned subsidiary as of May 22, 2026.

- The company acquired 500 shares, increasing its total ownership to 1,000 shares, representing a 100% voting rights stake.

- The acquisition price for the 500 shares was 100 yen in total, determined by considering the subsidiary’s lack of sales revenue since establishment and its impaired net assets.

- Compass Cloud AI Japan Inc., established in July 2023, had not generated any sales revenue and reported net assets of △3,836 thousand yen as of February 2025.

- The full acquisition aims to centralize management of AI infrastructure-related businesses (AIDC business), including GPU facilities, data center contracts, and financing, within the Quantum Solutions Group.

- The company stated that the impact of this transaction on its consolidated performance for the fiscal year ending February 2027 will be minor.

3571|ソトー

698.0

▲ +0.29%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- SOTOH Co., Ltd. announced a partial correction to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 (Japanese GAAP),” originally disclosed on May 12, 2026.

- The reason for the correction was an error in the elimination of intercompany transactions in the consolidated statement of income.

- The corrected consolidated net sales for the fiscal year ended March 31, 2026, are JPY 10,715 million, revised from the previous JPY 10,699 million (a 6.7% increase year-on-year).

- No changes were made to operating loss, ordinary loss, profit attributable to owners of parent, or comprehensive income figures.

- Sales for the “Product Sales Business” segment were also corrected from JPY 4,518 million to JPY 4,534 million (a 22.2% increase year-on-year).

🤖 AI Perspective

This correction stems from an accounting error related to the elimination of intercompany transactions, impacting consolidated sales and segment sales. Given that operating profit and subsequent profit figures remain unchanged, it may suggest that the revisions are primarily technical adjustments within accounting processes. Investors might consider assessing whether this correction has a limited impact on the company’s fundamental profitability or overall business performance.

6240|ヤマシンフィルタ

611.0

▲ +2.17%

📎 Source:ヤマシンフィルタ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- YAMASHIN-FILTER achieved record-high consolidated net sales of JPY 20.941 billion (+4.2% YoY) and net income for the fiscal year ended March 2026.

- Consolidated operating income for the same period was JPY 2.592 billion (-1.4% YoY).

- For the fiscal year ending March 2027, the company projects new record highs across all key metrics: consolidated net sales of JPY 22.560 billion (+7.7% YoY) and consolidated operating income of JPY 2.825 billion (+9.0% YoY), as well as record ordinary income and net income.

- Sales for the construction machinery filters business reached JPY 18.654 billion (+6.7% YoY) in FY2026, while air filters business sales were JPY 2.286 billion (-12.5% YoY).

- The equity ratio was 81.3% for FY2026, with a projected 74.7% for the beginning of FY2027.

🤖 AI Perspective

YAMASHIN-FILTER’s FY2026 results show record sales and net income, despite a slight decrease in operating income. This could indicate robust performance in its core construction machinery filter business, partially offset by underperformance in the air filter segment and upfront investments in new ventures. The company’s FY2027 projections for all-time high figures suggest confidence in continued growth, potentially driven by stable demand for both line and aftermarket construction machinery filters.

6800|ヨコオ

5080.0

▲ +4.10%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Yokowo Co., Ltd. announced a correction to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 (Japanese GAAP)” which was originally released on May 13, 2026.

- The reason for the correction was an error in aggregating the number of treasury shares to be deducted when calculating the total dividend amount.

- The specific correction is in the “Summary Information, 2. Dividends” section, for the “Total Dividends” amount for the fiscal year ended March 31, 2026.

- The previously stated “Total Dividends” for FY2026/3 was JPY 1,305 million, which has been corrected to JPY 1,313 million.

- There is no change to the per-share dividend amount, which remains JPY 56.00 for FY2026/3.

🤖 AI Perspective

This correction primarily concerns an aggregation error in treasury shares affecting the total dividend amount, but with no change to the per-share dividend, it suggests no direct impact on the dividends received by shareholders. However, the accuracy of disclosed information is crucial for corporate credibility, so investors might monitor the circumstances leading to the correction and the company’s future information management. As these figures form the basis for financial metrics like the dividend payout ratio and dividend on equity ratio, accurate information is considered important for investors.

7460|ヤギ

4500.0

▼ -1.21%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- YAGI Co., Ltd. announced on May 22, 2026, a correction to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 [Japanese GAAP]” and “Supplementary Explanatory Materials for the Fiscal Year Ended March 31, 2026.”

- The reason for the correction is that errors were found in a part of the consolidated cash flow statement during the preparation process of the consolidated financial statements, after the initial release of the financial results on May 11, 2026.

- The corrections pertain to the consolidated cash flow statement, and numerical data has also been revised.

- To provide full disclosure, the company has attached the complete corrected version of the “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 [Japanese GAAP].”

- This correction relates to the consolidated performance for the fiscal year ended March 31, 2026 (April 1, 2025, to March 31, 2026).

🤖 AI Perspective

Corrections to consolidated cash flow statements are significant as they impact key information regarding a company’s financial liquidity. Investors may wish to review the revised figures carefully to understand any potential implications for the company’s financial health or future cash flow projections. The company’s prompt release of the full corrected document suggests a commitment to transparency, which could be viewed positively by the market.

9692|シーイーシー

1947.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- CEC Co., Ltd. has revised its consolidated earnings forecast upward for the second quarter (interim period) of the fiscal year ending January 2027.

- The revised consolidated earnings forecast includes net sales of ¥35.0 billion (6.5% increase from previous forecast), operating profit of ¥4.1 billion (7.9% increase), ordinary profit of ¥4.13 billion (8.1% increase), and interim net profit attributable to parent company shareholders of ¥2.8 billion (7.7% increase).

- Interim earnings per share are projected to be ¥89.71 (an increase of ¥6.40 from the previous forecast).

- The interim dividend forecast has also been revised upward from ¥35 to ¥40 per share, making the total annual dividend ¥85 per share (including ¥40 for interim).

- The upward revision is attributed to strong ICT investment demand driven by corporate DX promotion and AI utilization, as well as robust performance across all segments, including large projects secured in the previous fiscal year.

- The full-year consolidated earnings forecast for the fiscal year ending January 2027 is currently under review and is scheduled to be announced at the time of the Q2 financial results release.

🤖 AI Perspective

CEC’s upward revision of its earnings forecast and increased interim dividend suggest a strong performance driven by robust demand for digital transformation (DX) and AI-related investments. The across-the-board improvement in key financial metrics may indicate the company is effectively capitalizing on current market trends. The increased dividend payout could also be interpreted as a sign of management’s confidence in future performance and commitment to shareholder returns.

2183|リニカル

225.0

▼ -0.88%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Runicol Co., Ltd. released supplementary explanatory materials for its FY2026/3 financial results, updating its order backlog information.

- As of May 22, 2026, the order backlog reached JPY 13.0 billion.

- This represents a 10.9% increase compared to the end of March 2025.

- The updated figure incorporates the completion of two contracts that were previously described as being in the process of signing in the financial results announcement on May 15, 2026.

- Regionally, the order backlog for the US and Europe increased compared to the end of March 2025, while Japan saw a decrease and Asia an increase.

🤖 AI Perspective