📌 Today’s Highlights

Today we cover 50 IR announcements. Notable among them: TSI HD (3608), G-インタファクトリ (4057), ヴィッツ (4440). Use the table of contents below to navigate to each company.

- 4565|ネクセラファーマ

- 3608|TSI HD

- 4057|G-インタファクトリ

- 4440|ヴィッツ

- 7434|オータケ

- 9835|ジュンテンド

- 1419|タマホーム

- 7937|ツツミ

- 9982|タキヒヨー

- 139A|P-東日本地所

- 152A|P-オプティ

- 284A|P-フクヤ建設

- 3143|オーウイル

- 6217|津田駒工

- 8095|アステナHD

- 8167|リテールパートナーズ

- 3065|ライフフーズ

- 6159|ミクロン精密

- 9235|G-売れるネットG

- 5250|GMOプライム

- 1434|JESCO HD

- 198A|G-ポストプライム

- 2186|ソーバル

- 276A|G-ククレブ

- 3030|ハブ

- 3075|銚子丸

- 3111|オーミケンシ

- 3168|MERF

- 3236|プロパスト

- 3281|R-GLP

- 3349|コスモス薬品

- 340A|G-ジグザグ

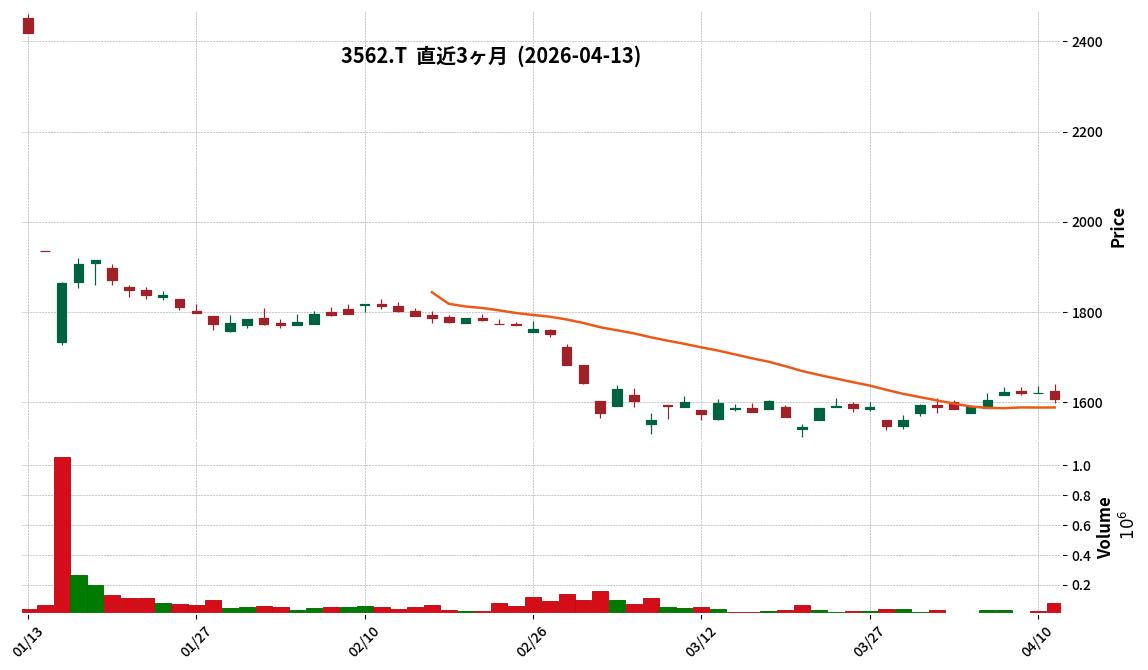

- 3562|No.1

- 3612|ワールド

- 3678|メディアドゥ

- 3760|ケイブ

- 3996|サインポスト

- 4167|G-ココペリ

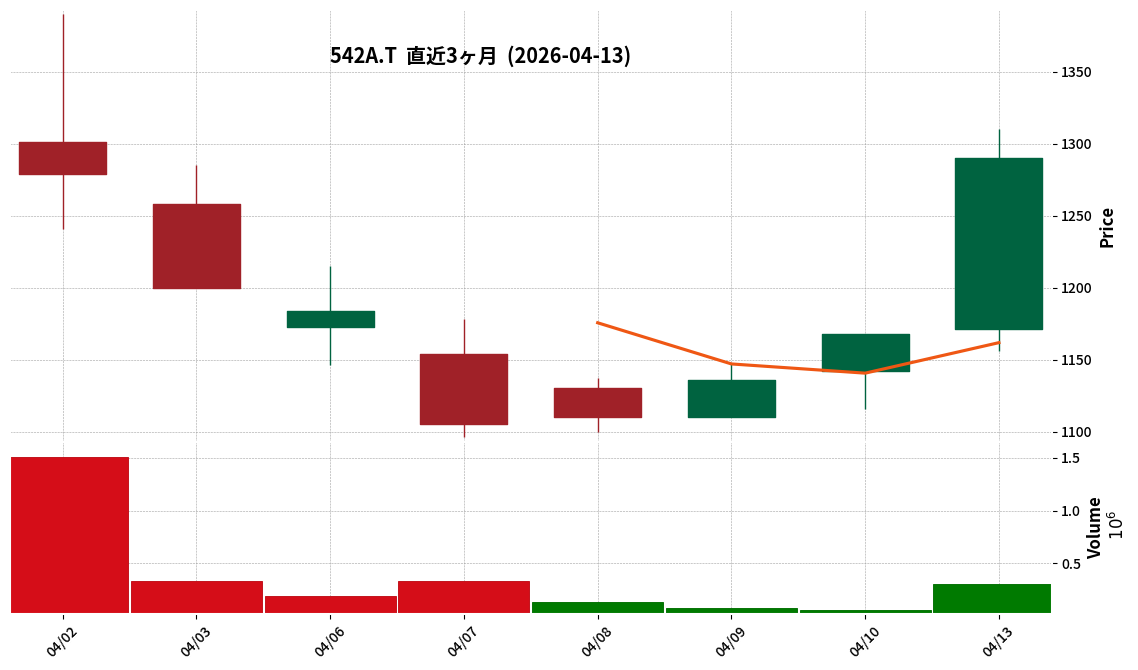

- 542A|G-ビタブリッドJ

- 6505|東洋電

- 6634|JNグループ

- 5578|G-ARアドバンスト

- 1401|G-エムビーエス

- 2736|フェスタリアHD

- 3063|G-jGroup

- 3679|じげん

- 373A|G-リップス

- 3907|シリコンスタジオ

- 4199|G-ワンプラ

- 4829|日本エンタープライズ

4565|ネクセラファーマ

1021.0

▼ -0.29%

📄 Announcement (AI-Reviewed)

- Nxera Pharma announced that its partner, Neurocrine Biosciences Inc., has initiated a Phase 2 study for NBI-1117570 in adults with schizophrenia and has dosed the first patient.

- This initiation of the Phase 2 study triggers a milestone payment of $22.5 million (approximately JPY 3,574 million) from Neurocrine Biosciences to Nxera Pharma, based on their agreement.

- The milestone payment is expected to be recorded entirely as revenue in the first quarter of the fiscal year ending December 2026.

- NBI-1117570 is an oral, selective muscarinic M1/M4 receptor agonist created using Nxera Pharma’s proprietary drug discovery platform, NxWave™.

- The Phase 2 study is a double-blind, placebo-controlled trial targeting approximately 120 adult patients with schizophrenia requiring inpatient care, with the primary endpoint being the change from baseline in the Positive and Negative Syndrome Scale (PANSS) total score at Day 35.

🤖 AI Perspective

The advancement of NBI-1117570 into Phase 2 represents a significant development for Nxera Pharma’s pipeline, potentially indicating progress in its strategic partnership and drug development capabilities. The associated milestone payment is anticipated to positively impact the company’s Q1 2026 financial results, which may draw investor attention to future pipeline milestones. Given the substantial unmet medical need in schizophrenia, the continued development of novel treatment options like NBI-1117570 could be a noteworthy factor for market observers.

3608|TSI HD

1329.0

▲ +18.03%

📄 Announcement (AI-Reviewed)

- TSI Holdings reported consolidated net sales of JPY 167.0 billion (up 6.7% year-on-year) and operating profit of JPY 4.3 billion (up 164.4% year-on-year) for the full fiscal year ended February 2026.

- The increase in net sales was primarily due to the consolidation of Daytona International Co., Ltd. and Waterfront Co., Ltd.

- The significant rise in operating profit was driven by structural reform initiatives, which contributed approximately JPY 5.2 billion in profit improvement. However, both net sales and operating profit fell short of the revised plan due to the weaker performance of core existing brands, difficulties in new customer acquisition, and a decline of approximately JPY 3.5 billion in existing business sales.

- Net profit attributable to owners of the parent decreased to JPY 3.7 billion year-on-year, primarily influenced by the reversal of real estate sale gains from the prior period and an impairment loss of JPY 1.8 billion related to goodwill in the U.S. business recorded in the current period.

- A share repurchase of JPY 12.0 billion, executed in July 2025, was fully cancelled by the end of January 2026.

🤖 AI Perspective

The reported increase in sales driven by M&A and substantial operating profit growth from structural reforms suggest a focus on expanding the business and improving profitability. However, the underperformance of existing businesses against revised plans and the decline in net profit due to one-off factors like impairment losses and the absence of prior year’s gains could indicate underlying challenges. Investors may continue to monitor the company’s efforts to revitalize existing operations and further enhance inventory management alongside its inorganic growth initiatives.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

4057|G-インタファクトリ

400.0

▲ +2.56%

📄 Announcement (AI-Reviewed)

- For the third quarter cumulative period of the fiscal year ending May 2026 (June 1, 2025 to February 28, 2026), G-INTERFACTORY reported net sales of ¥2,112 million (up 2.8% year-on-year), operating profit of ¥74 million (down 51.9%), ordinary profit of ¥70 million (down 53.4%), and quarterly net profit of ¥44 million (down 60.8%).

- The full-year earnings forecast for FY2026 (June 1, 2025 to May 31, 2026) remains unchanged from the most recently published forecast, with projected net sales of ¥3,223 million (up 12.5% year-on-year) and net profit of ¥53 million (down 61.0%).

- The “Cloud Commerce Platform Business” recorded net sales of ¥2,032,651 thousand (up 8.5%) and segment profit of ¥640,902 thousand (up 0.4%). The “EC Business Growth Support Business” posted net sales of ¥79,382 thousand (down 55.9%) but achieved a segment profit of ¥414 thousand (compared to a loss in the prior year). The newly launched “Data Utilization Platform Business” generated no sales and incurred a segment loss of ¥42,938 thousand.

- Total assets stood at ¥1,996 million, net assets at ¥1,222 million, and the equity ratio improved to 61.2% from 55.9% at the end of the previous fiscal year.

- Supplementary financial materials have been prepared, and an earnings briefing is scheduled to be held.

🤖 AI Perspective

While net sales showed an increase year-on-year, operating, ordinary, and quarterly net profits all experienced significant declines. This trend may suggest the impact of aggressive investments in new business areas such as the “EC Business Growth Support Business” and “Data Utilization Platform Business,” alongside increased company-wide expenses due to enhanced marketing activities. Conversely, the improvement in the equity ratio could indicate a strengthened financial foundation for the company.

4440|ヴィッツ

1554.0

▼ -0.38%

📄 Announcement (AI-Reviewed)

- Witz Co., Ltd. reported consolidated results for the second quarter of the fiscal year ending August 2026, with net sales of ¥2,618 million (up 12.0% year-on-year), operating profit of ¥340 million (up 11.1% year-on-year), ordinary profit of ¥357 million (up 10.3% year-on-year), and net profit attributable to owners of the parent of ¥249 million (up 10.9% year-on-year).

- Diluted earnings per share for the interim period were ¥62.63.

- By segment, the Software business achieved net sales of ¥2,347 million (up 20.8% year-on-year) and segment profit of ¥344 million (up 24.9% year-on-year). In contrast, the Sensing business reported net sales of ¥244 million (down 38.0% year-on-year) and a segment loss of ¥23 million.

- The consolidated full-year earnings forecast for the fiscal year ending August 2026 remains unchanged, projecting net sales of ¥5,600 million (up 15.3% year-on-year), operating profit of ¥580 million (up 2.4% year-on-year), ordinary profit of ¥596 million (up 1.3% year-on-year), and net profit attributable to owners of the parent of ¥435 million (up 2.5% year-on-year).

- The year-end dividend forecast is ¥18.00 per share (total annual dividend of ¥18.00), with no revisions from the most recently announced dividend forecast.

🤖 AI Perspective

Witz’s strong performance in the second quarter of fiscal year 2026 appears to be primarily driven by the robust growth in its Software business segment. The steady sales in embedded software for automobiles, simulator/virtual space technology, and security/safety fields are considered key contributors to the overall revenue and profit increase. Conversely, the Sensing business experienced a decline in sales and a loss, reportedly due to a portion of large projects being rescheduled for delivery in the third quarter or later, indicating varied performance across segments during this period. The company’s full-year earnings and dividend forecasts remain unchanged, suggesting management’s view on the overall outlook.

7434|オータケ

1923.0

▲ +1.64%

📄 Announcement (AI-Reviewed)

- For the nine months ended February 28, 2026 (Q3 FY2026), Otake Co., Ltd. reported consolidated net sales of JPY 26,361 million (up 8.0% year-on-year), operating profit of JPY 812 million (up 13.0%), ordinary profit of JPY 967 million (up 11.2%), and profit attributable to owners of parent of JPY 654 million (up 10.7%).

- As of February 28, 2026, the consolidated financial position showed total assets of JPY 30,268 million, net assets of JPY 17,067 million, and an equity ratio of 56.4%.

- The annual dividend forecast for the fiscal year ending May 2026 has been revised to JPY 40.00.

- The full-year consolidated earnings forecast for the fiscal year ending May 2026 remains unchanged from the previous announcement, projecting net sales of JPY 34,000 million, operating profit of JPY 1,000 million, ordinary profit of JPY 1,220 million, and profit attributable to owners of parent of JPY 860 million.

🤖 AI Perspective

The consolidated operating results show an increase in net sales and all profit metrics compared to the prior year, indicating a stable performance trend. While the full-year earnings forecast was maintained, the revision to the annual dividend forecast may suggest an updated stance on shareholder returns, which could be a point of interest for investors. In terms of financial position, total assets increased, but the equity ratio slightly decreased from the previous fiscal year-end, hinting at changes in asset composition.

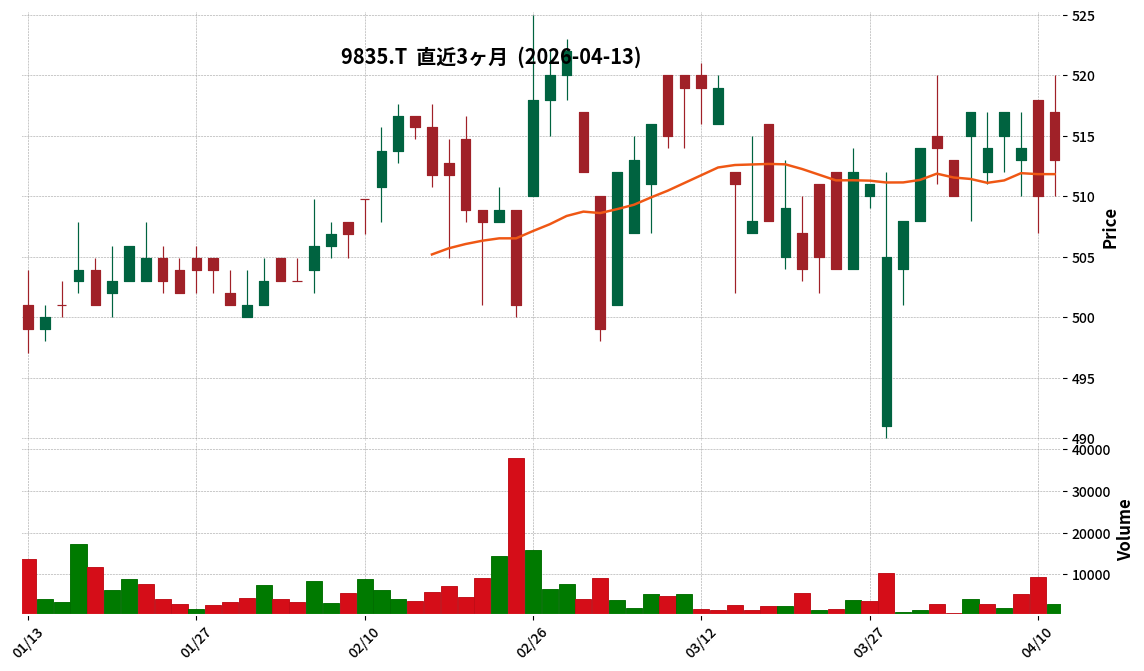

9835|ジュンテンド

513.0

▲ +0.59%

📄 Announcement (AI-Reviewed)

- JUNTENDO Co., Ltd. announced a partial correction to its “Supplemental Explanation Material for the Fiscal Year Ended February 29, 2026,” originally published on April 10, 2026.

- The correction involves minor adjustments to the year-on-year change rates for the full-year forecasts for the fiscal year ending February 2027: operating profit was revised from 76.5% to 76.4%, and ordinary profit from 44.2% to 43.8%.

- For the fiscal year ended February 2026, the company reported operating revenue of 43,040 million yen, operating profit of 238 million yen, and ordinary profit of 208 million yen.

- Net profit for the period was a loss of 361 million yen, primarily due to extraordinary losses including impairment losses of 507 million yen and retirement of fixed assets of 63 million yen.

- While the gross profit margin for the home center (HC) business improved from 29.7% to 30.1%, full-year sales decreased year-on-year due to factors such as reduced customer traffic and rising prices.

🤖 AI Perspective

- This correction primarily concerns minor adjustments to the percentage change rates of future performance forecasts, suggesting that the direct impact on the overall financial results may be limited.

- However, the reported fiscal year results indicate an improvement in gross profit margin alongside a decline in sales due to decreased customer traffic and a net loss from impairment charges, highlighting the need to monitor the company’s response to changing business conditions moving forward.

1419|タマホーム

3665.0

▼ -9.73%

📄 Announcement (AI-Reviewed)

- Tama Home Co., Ltd. disclosed the summary of Q&A from its Q3 FY2026 earnings conference call held on April 13, 2026.

- Strong order performance in March was primarily attributed to an increase in closing rates due to securing and training personnel, as well as a rise in proactive purchase considerations amidst an upward trend in interest rates.

- Improvements in the operating profit margin within the real estate segment were due to the selective acquisition of prime land (especially for subdivisions with 10 lots or fewer) for the detached housing business, and the acquisition of quality properties for the office condominium sales business.

- Regarding building material price increases, the company is responding with appropriate adjustments, and is working with manufacturers to secure materials despite changes in the supply chain influenced by the Middle East situation.

- The decision to reduce the dividend was made considering the current business environment and balancing future investments, from a capital allocation perspective. The ¥125 per share dividend was set to ensure the successful execution of initiatives for strengthening sales operations and improving profitability.

🤖 AI Perspective

The Q&A summary from Tama Home’s IR provides key insights into the company’s current business status and future strategy. The robust order performance appears to stem from a combination of internal operational enhancements and evolving market conditions, while profit margin improvements in the real estate segment may reflect successful land acquisition strategies. The dividend reduction, on the other hand, suggests a strategic focus on future investments and business foundation rebuilding aimed at long-term performance recovery, which investors may find worth monitoring.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

7937|ツツミ

3085.0

▲ +0.49%

📄 Announcement (AI-Reviewed)

- Tutumi Co., Ltd. resolved to revise its year-end dividend forecast for the fiscal year ending March 31, 2026, at a Board of Directors meeting held on April 13, 2026.

- The revised year-end dividend per share is ¥70.00 (previously ¥45.00).

- Consequently, the total annual dividend forecast for the current fiscal year has been revised to ¥115.00 (previously ¥90.00).

- The revised annual dividend forecast of ¥115.00 represents an increase of ¥35.00 per share compared to the actual result of ¥80.00 for the previous fiscal year.

- This revision is scheduled to be proposed at the 53rd Annual General Meeting of Shareholders, planned for June 25, 2026.

🤖 AI Perspective

This dividend forecast revision suggests Tutumi’s commitment to shareholder returns as a key management priority. The increase in the dividend, resulting from a comprehensive consideration of recent business performance, financial condition, and capital efficiency, may be viewed positively by investors. The upward revision of the annual dividend compared to the previous year’s actual performance could indicate a stable financial outlook and dedication to enhancing shareholder value.

9982|タキヒヨー

2673.0

▲ +4.13%

📄 Announcement (AI-Reviewed)

- Takihyo Co., Ltd. announced its consolidated financial results for the fiscal year ended February 2026, reporting net sales of ¥63,970 million (+5.5% year-on-year), operating profit of ¥1,942 million (+48.0% year-on-year), ordinary profit of ¥1,947 million (+43.3% year-on-year), and profit attributable to owners of parent of ¥1,615 million (+45.9% year-on-year).

- Sales increased across all business segments, with the Material Business specifically growing by 7.4% year-on-year to ¥5,269 million.

- The annual dividend for the fiscal year ended February 2026 was set at ¥45.00 (interim dividend ¥20.00, year-end dividend ¥25.00), an increase from ¥35.00 in the previous fiscal year.

- For the fiscal year ending February 2027, the company forecasts consolidated net sales of ¥64,800 million (+1.3% year-on-year), operating profit of ¥1,950 million (+0.4% year-on-year), ordinary profit of ¥1,950 million (+0.1% year-on-year), and profit attributable to owners of parent of ¥1,620 million (+0.3% year-on-year).

- The consolidated equity ratio at the end of February 2026 was 63.8%.

🤖 AI Perspective

Takihyo’s FY2026/2 results show significant profit growth outpacing revenue, which may suggest improved operational efficiency or favorable market conditions during the period. The increase in the annual dividend and the forecast for continued revenue and profit growth in FY2027/2 could indicate management’s confidence in future performance. Furthermore, sales growth across all segments might point to a robust and diversified business foundation.

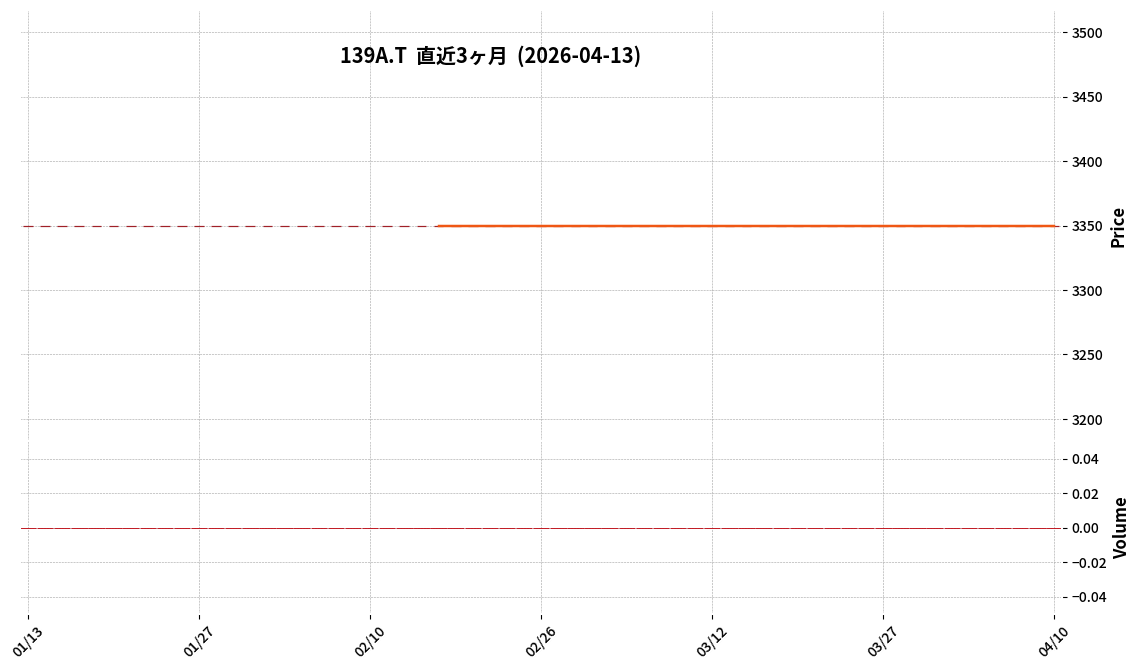

139A|P-東日本地所

3350.0

▲ +0.00%

📄 Announcement (AI-Reviewed)

- P-Higashi-Nihon Jisho announced its interim financial results for the fiscal year ending August 2026 (September 1, 2025, to February 28, 2026).

- Consolidated operating results show net sales of ¥2,627 million (up 3.1% year-on-year), operating profit of ¥193 million (down 13.7%), ordinary profit of ¥194 million (down 10.1%), and net income attributable to owners of the parent of ¥134 million (down 8.5%).

- The consolidated financial position at the end of the interim period includes total assets of ¥3,824 million, net assets of ¥1,213 million, and an equity ratio of 31.7%.

- The full-year consolidated performance forecast for the fiscal year ending August 2026 remains unchanged from the most recently announced forecast, with net sales projected at ¥6,500 million (up 17.1% year-on-year), operating profit at ¥400 million (up 10.8%), and net income attributable to owners of the parent at ¥250 million (up 0.3%).

- During this interim period, the number of housing starts under construction contracts was 111 buildings/132 units (up 36.1% year-on-year), completions were 68 buildings/84 units (up 21.7%), and new construction contracts signed were 118 buildings/131 units (up 13.9%). Additionally, a model house was opened in Saitama City, Saitama Prefecture in February 2026.

🤖 AI Perspective

While net sales increased, the decline in operating profit and other profit metrics year-on-year is a key point, which may suggest impacts from rising construction material and labor costs. Conversely, the steady increase in housing starts and new construction contracts could indicate a positive outlook for future revenue growth. The unchanged full-year forecast might suggest the company anticipates profit improvement in the latter half of the fiscal year.

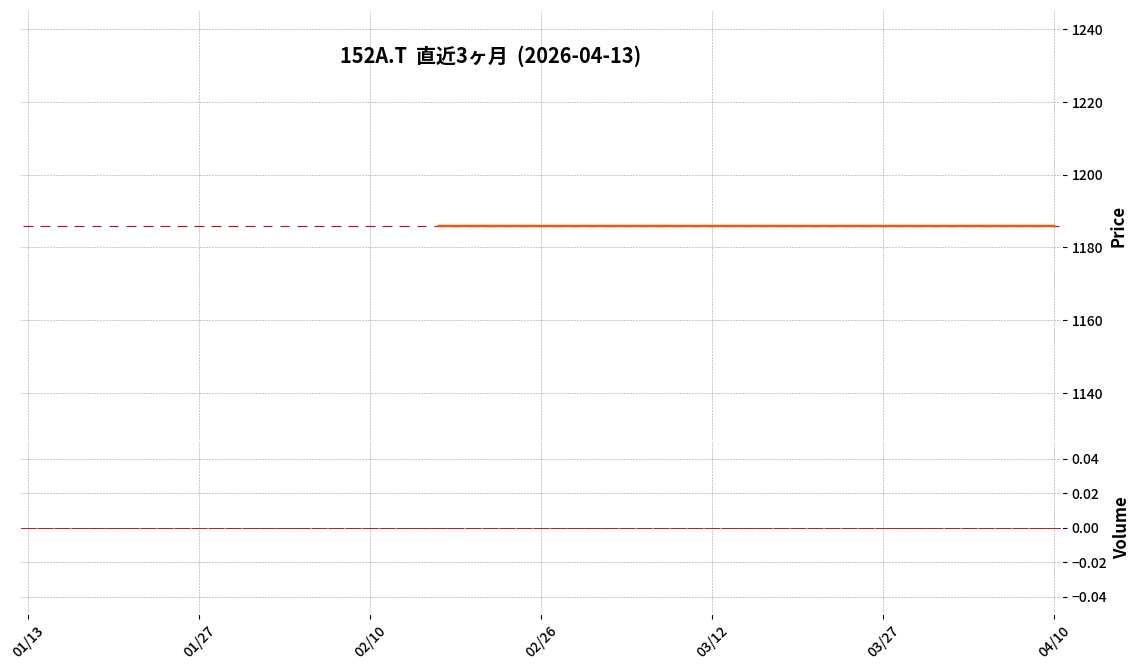

152A|P-オプティ

1186.0

▲ +0.00%

📄 Announcement (AI-Reviewed)

- P-OPTY Co., Ltd. has announced its non-consolidated financial results for the fiscal year ended February 2026 (March 1, 2025 to February 28, 2026).

- For the current fiscal year, net sales were ¥2,001 million (up 5.7% year-on-year), operating profit was ¥101 million (up 146.4%), ordinary profit was ¥101 million (up 274.9%), and net profit was ¥67 million (up 236.2%).

- The equity ratio improved to 70.8% (67.0% at the end of the previous fiscal year), and cash and cash equivalents at the end of the period stood at ¥261 million (¥169 million at the end of the previous fiscal year).

- The annual dividend per share for FY2026 and the forecast for FY2027 (both interim and year-end) is ¥0.00.

- For the fiscal year ending February 2027 (March 1, 2026 to February 28, 2027), the company forecasts net sales of ¥2,191 million (up 9.5% year-on-year), operating profit of ¥99 million (down 1.9%), ordinary profit of ¥97 million (down 3.4%), and net profit of ¥64 million (down 4.2%).

🤖 AI Perspective

The significant increase in operating, ordinary, and net profits, alongside a rise in sales for the current period, may suggest improved operational efficiency. However, the forecast for the upcoming fiscal year indicates a decline in various profits despite projected revenue growth, which could potentially be influenced by factors such as cost fluctuations or strategic investments. The consistent ¥0.00 dividend payout may reflect a focus on retaining earnings for future growth.

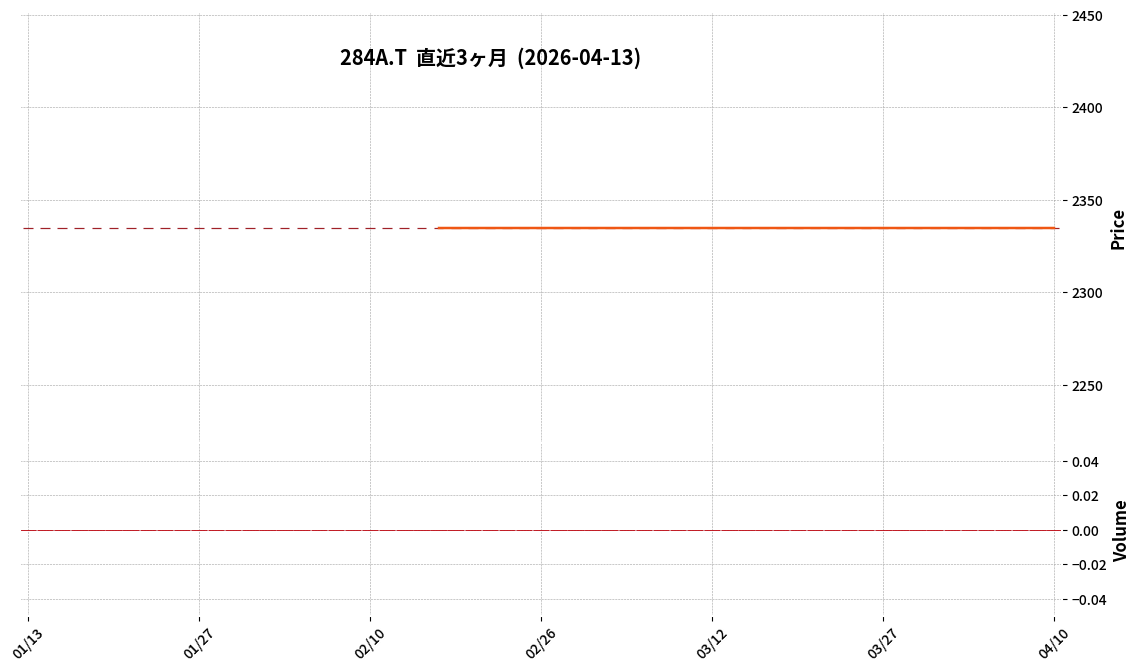

284A|P-フクヤ建設

2335.0

▲ +0.00%

📄 Announcement (AI-Reviewed)

- P-Fukuya Kensetsu announced its consolidated financial results for the first half of the fiscal year ending August 2026 (September 1, 2025 to February 28, 2026).

- Consolidated net sales reached JPY 1,988 million, representing a 71.3% increase compared to the same period last year.

- The company reported an operating profit of JPY 74 million, ordinary profit of JPY 100 million, and net profit attributable to parent company shareholders of JPY 66 million, marking a return to profitability from losses in the prior year.

- The Construction Business segment recorded sales of JPY 1,667 million (up 88.7% YoY) and segment profit of JPY 185 million (up 81.7% YoY), driven by strong order intake, including the consolidation of Fukuya Architectural Design Office Co., Ltd.

- The full-year consolidated performance forecast for FY2026 remains unchanged, projecting net sales of JPY 3,750 million (up 30.6% YoY) and net profit attributable to parent company shareholders of JPY 179 million (up 140.1% YoY).

- The annual dividend forecast is JPY 185.00 per share, with no revision.

🤖 AI Perspective

The significant increase in net sales and the return to profitability across key earnings metrics in the first half may suggest a positive operational turnaround. Strong performance in the construction business, bolstered by a new consolidated subsidiary, appears to be a primary driver of these results. The reaffirmation of the full-year outlook indicates management’s expectation for continued solid performance throughout the fiscal year.

3143|オーウイル

711.0

▲ +0.42%

📄 Announcement (AI-Reviewed)

- Owille resolved at its Board of Directors meeting on April 13, 2026, to acquire additional shares of its consolidated subsidiary, NIITAKAYA U.S.A. INC., making it a wholly-owned subsidiary.

- This acquisition will increase Owille’s voting rights ratio in NIITAKAYA U.S.A. INC. from 95.0% to 100.0%.

- NIITAKAYA U.S.A. INC. is engaged in the manufacturing and sales of pickled ginger (Gari Shoga) and tenant sales in the U.S., having previously become Owille’s consolidated subsidiary on April 16, 2025.

- The share transfer execution date is scheduled for April 16, 2026.

- The acquisition price is not disclosed due to a confidentiality agreement but was determined based on a stock price evaluation by external experts and deemed fair and appropriate by Owille’s board.

🤖 AI Perspective

Owille’s decision to make NIITAKAYA U.S.A. INC. a wholly-owned subsidiary can be interpreted as a move to accelerate its overseas expansion, a key growth strategy, and deepen group management within the U.S. market. By fully integrating NIITAKAYA, which holds a significant share in the U.S. pickled food market, Owille appears to aim for enhanced group synergies and a strengthened revenue base, ultimately seeking to improve long-term corporate value.

6217|津田駒工

471.0

▲ +5.84%

📄 Announcement (AI-Reviewed)

- For the first quarter of the fiscal year ending November 2026 (December 1, 2024 to February 28, 2025), consolidated net sales increased by 15.2% year-on-year to ¥6,939 million.

- The operating loss for the period narrowed to ¥134 million (compared to an operating loss of ¥276 million in the prior year’s first quarter), and the ordinary loss narrowed to ¥119 million (compared to an ordinary loss of ¥389 million).

- Total order intake increased by 31.6% year-on-year to ¥11,421 million, with the Machine Tool Related Business recording a significant 47.2% increase to ¥1,740 million in orders.

- The company noted the existence of events or conditions that raise significant doubt about its ability to continue as a going concern, primarily due to sustained operating and ordinary losses for five consecutive fiscal years since November 2019, including the previous fiscal year and the current first quarter.

- The consolidated full-year forecast for FY2026 remains unchanged, projecting net sales of ¥36,000 million, operating profit of ¥700 million, ordinary profit of ¥500 million, and net profit attributable to parent company shareholders of ¥250 million.

🤖 AI Perspective

- The reported increase in sales and order intake, coupled with a narrowing of operating and ordinary losses, may suggest an improving operational environment and the potential early effects of ongoing business reforms.

- The significant increase in operating profit within the Machine Tool Related Business segment could indicate a strengthening performance in that specific area.

- However, the continued disclosure of significant doubt about the going concern highlights the importance for investors to closely monitor the company’s strategic initiatives aimed at achieving sustainable profitability and strengthening its financial position.

8095|アステナHD

476.0

▼ -0.83%

📄 Announcement (AI-Reviewed)

- Astena Holdings Co., Ltd. announced its consolidated financial results for the first quarter of the fiscal year ending November 2026 (December 1, 2025, to February 28, 2026) on April 13, 2026.

- Consolidated net sales were JPY 16,557 million (up 15.5% year-on-year), operating income was JPY 1,152 million (up 11.7%), ordinary income was JPY 1,079 million (up 3.6%), and net income attributable to owners of parent was JPY 586 million (up 16.0%).

- The HBC and Food Business segment recorded net sales of JPY 5,504 million (up 49.8% year-on-year) and operating income of JPY 265 million (up 27.5%), driven by strong sales of imported cosmetics such as “Torriden”.

- The Chemicals Business segment achieved net sales of JPY 2,928 million (up 32.6% year-on-year) and operating income of JPY 376 million (up 177.3%), with both the surface treatment chemicals and equipment divisions performing well.

- The Fine Chemicals Business segment reported a decrease in sales to JPY 5,125 million (down 8.7% year-on-year) and operating income to JPY 214 million (down 41.3%). The Medical Business also experienced a decline in operating income to JPY 260 million (down 26.7%).

- The company stated that there are no revisions to its consolidated full-year performance forecast for the fiscal year ending November 2026 from the latest publicly announced figures.

8167|リテールパートナーズ

1340.0

▲ +4.85%

📄 Announcement (AI-Reviewed)

- Retail Partners Co., Ltd. announced its consolidated financial results for the fiscal year ended February 2026.

- Operating revenue increased by 4.3% year-on-year to ¥278,197 million.

- Conversely, operating profit decreased by 5.2% to ¥6,468 million, ordinary profit decreased by 5.5% to ¥7,557 million, and profit attributable to owners of parent decreased by 1.7% to ¥5,138 million.

- The annual dividend per share for FY2026/2 was ¥40 (interim dividend ¥20, year-end dividend ¥20), an increase of ¥2 from ¥38 in the previous fiscal year.

- The consolidated business forecast for FY2027/2 projects operating revenue of ¥288,500 million (up 3.7% year-on-year), operating profit of ¥6,800 million (up 5.1%), ordinary profit of ¥7,700 million (up 1.9%), and profit attributable to owners of parent of ¥5,350 million (up 4.1%), indicating expected growth in both revenue and profit.

- During the consolidated fiscal year, Nagano Co., Ltd. was newly included in the scope of consolidation, and accounting policies were changed due to revisions of accounting standards.

🤖 AI Perspective

- The FY2026/2 results show an increase in operating revenue, while profits across all stages declined, which may warrant attention. This trend could indicate challenges in maintaining profitability despite revenue growth, potentially influenced by the addition of a new consolidated company and changes in accounting policies.

- The increase in the annual dividend by ¥2 and the forecast for revenue and profit growth in FY2027/2 might be viewed as a positive signal regarding the company’s future outlook and management’s confidence.

- The slight improvement in the equity ratio to 67.3% from the previous period could be considered an indicator of the company’s stable financial position.

3065|ライフフーズ

1615.0

▼ -0.06%

📄 Announcement (AI-Reviewed)

- For the fiscal year ended February 2026, Life Foods reported net sales of JPY 9,614 million (down 1.7% year-on-year), operating income of JPY 87 million (down 74.8%), ordinary income of JPY 128 million (down 69.0%), and net income of JPY 35 million (down 91.1%), marking a decrease in both revenue and profit.

- As of February 29, 2026, total assets were JPY 3,923 million and net assets were JPY 1,710 million, with the equity ratio improving from 41.3% at the end of the previous fiscal year to 43.6%.

- Cash flow from operating activities increased to a net inflow of JPY 505 million, compared to a net inflow of JPY 314 million in the prior fiscal year.

- The annual dividend per share for the fiscal year ended February 2026 was JPY 5.00, with the same dividend of JPY 5.00 per share projected for the fiscal year ending February 2027.

- The full-year forecast for the fiscal year ending February 2027 includes net sales of JPY 9,619 million (up 0.0% year-on-year), operating income of JPY 118 million (up 35.7%), ordinary income of JPY 157 million (up 22.4%), and net income of JPY 73 million (up 104.0%).

🤖 AI Perspective

- The significant decline in net income for FY2026 reflects challenging operational conditions such as rising raw material costs and labor expenses, as detailed in the report.

- However, the improvement in the equity ratio and the increased operating cash flow may suggest a strengthening of the company’s financial structure.

- The substantial projected recovery in net income for FY2027 indicates an expectation for positive outcomes from ongoing business initiatives, which investors may find worth monitoring.

6159|ミクロン精密

2231.0

▼ -0.84%

📄 Announcement (AI-Reviewed)

- Micron Seimitsu Co., Ltd. announced its Consolidated Financial Results for the Second Quarter of the Fiscal Year Ending August 31, 2026 (Japanese GAAP) on April 13, 2026.

- For the cumulative second quarter, net sales totaled JPY 1,851 million, representing a 34.4% decrease compared to the same period in the previous year.

- The company reported an operating loss of JPY 3 million, a significant shift from an operating profit of JPY 374 million in the prior year’s interim period.

- Ordinary profit amounted to JPY 616 million (down 21.7% year-on-year), and net income attributable to owners of parent was JPY 408 million (down 23.3% year-on-year).

- The full-year consolidated earnings forecast for the fiscal year ending August 31, 2026, remains unchanged from the forecast announced on October 10, 2025, projecting net sales of JPY 5,467 million, operating profit of JPY 381 million, ordinary profit of JPY 668 million, and net income attributable to owners of parent of JPY 452 million.

- The year-end dividend forecast for FY2026 is maintained at JPY 12.00 per share.

🤖 AI Perspective

The shift to an operating loss, despite maintaining positive ordinary and net profits, may suggest challenges in core business profitability, potentially offset by non-operating income. The company’s high equity ratio of 85.3% indicates a strong financial foundation, which could provide resilience amidst fluctuating earnings. The reaffirmation of the full-year forecast suggests that management either anticipates a recovery in the latter half of the fiscal year or that current results align with prior expectations, making future performance worth monitoring.

9235|G-売れるネットG

561.0

▼ -1.92%

📄 Announcement (AI-Reviewed)

- G-Ureru Net G (Ureru Net Advertising Group Co.,Ltd.) has entered into a basic agreement to acquire 100% of the shares of Step y’s Inc., a company specializing in call center and BPO services.

- Step y’s Inc. reported revenue of JPY 300 million and is projected to have a post-acquisition real earning power of JPY 90 million. Post-acquisition real earning power is defined as the earning power after excluding fixed cost reductions achieved through leveraging existing resources of the Group.

- This acquisition marks the third M&A transaction for the current fiscal year, increasing the total revenue contribution from M&A activities for the period to approximately JPY 950 million.

- Through this M&A, the company aims to internalize the entire process from customer acquisition to order fulfillment, customer support, and continuous use, thereby evolving into an “LTV management model.”

- Step y’s Inc. operates on a recurring revenue model based on long-term continuous contracts, characterized by its stable cash flow generation.

🤖 AI Perspective

This M&A appears to be a strategic move by G-Ureru Net G to solidify its “LTV management model” by integrating customer support functions. The acquisition of a call center and BPO company could enhance the company’s ability to provide end-to-end services across the entire customer lifecycle, potentially securing stable recurring revenue streams. Furthermore, the stated synergies, including accelerated new customer acquisition, expansion into cross-border e-commerce, and AI integration, may indicate the company’s intention to tap into new growth avenues.

5250|GMOプライム

1139.0

▲ +3.55%

📄 Announcement (AI-Reviewed)

- GMO Prime Strategy announced its consolidated financial results for the first quarter of the fiscal year ending December 2026 (period: December 1, 2025, to February 28, 2026).

- For the quarter, revenue reached ¥232 million (up 4.1% year-on-year), while operating profit was ¥36 million (down 9.9% year-on-year), ordinary profit was ¥37 million (down 7.6% year-on-year), and profit attributable to owners of parent was ¥27 million (down 3.4% year-on-year).

- The full-year consolidated earnings forecast for the fiscal year ending December 2026 was revised to ¥1,124 million for revenue, ¥70 million for operating profit, ¥72 million for ordinary profit, and ¥51 million for profit attributable to owners of parent.

- The company confirmed its group-join with GMO Internet Group, Inc. on December 26, 2025, and announced plans to release “MAGATAMA Stack” in June 2026 to further strengthen its AI business.

🤖 AI Perspective

While revenue increased, the decline in profits appears to be influenced by increased expenses for medium-to-long term growth and outsourcing costs, as explained by the company. The revision of the full-year earnings forecast, the company’s integration into the GMO Internet Group, and the planned release of the new “MAGATAMA Stack” in June 2026 could be key points for investors to monitor regarding future business development. A high equity ratio of 88.7% may also suggest a stable financial foundation.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

1434|JESCO HD

1875.0

▲ +0.86%

📄 Announcement (AI-Reviewed)

- For the second quarter of the fiscal year ending August 2026 (September 1, 2025 – February 28, 2026), JESCO HD reported consolidated net sales of JPY 10,934 million, an increase of 25.9% compared to the previous interim period.

- Operating profit rose by 119.8% to JPY 1,315 million, ordinary profit increased by 117.9% to JPY 1,340 million, and net profit attributable to owners of parent surged by 118.0% to JPY 831 million.

- Order intake for the interim period reached JPY 13,689 million, representing an 81.5% increase year-on-year, with the domestic EPC business alone seeing an 89.6% increase to JPY 9,219 million.

- The consolidated full-year forecast for FY2026 remains unchanged, projecting net sales of JPY 20,000 million, operating profit of JPY 1,800 million, ordinary profit of JPY 1,750 million, and net profit attributable to owners of parent of JPY 1,100 million.

- The year-end dividend forecast is JPY 48.00 per share (total annual dividend JPY 48.00), with no revisions to the latest publicly announced dividend forecast.

🤖 AI Perspective

JESCO HD’s strong performance in the second quarter, marked by significant increases across key profitability metrics, suggests a robust operational period. The substantial growth in order intake, particularly within the domestic EPC business, could indicate positive momentum for future revenue generation. Investors may want to monitor how the company’s unchanged full-year forecasts align with this strong interim performance in the coming quarters.

198A|G-ポストプライム

214.0

▲ +7.00%

📄 Announcement (AI-Reviewed)

- For the third quarter of the fiscal year ending May 2026 (cumulative), G-PostPrime reported consolidated net sales of 452 million yen, an operating loss of 188 million yen, and a net loss attributable to parent company shareholders of 205 million yen.

- Compared to the prior year’s same period (Q3 FY2025), net sales decreased from 684 million yen to 452 million yen, and the company shifted from an operating profit of 198 million yen to an operating loss of 188 million yen.

- The decline in net sales is attributed to a decrease in new paid subscriptions and a lower retention rate for its SNS platform “PostPrime,” along with limited revenue contribution from its CFD trading platform “TakaTrade.”

- Future growth strategies include expanding creators and community, diversifying revenue streams through M&A, and initiating the application process for a Type I Financial Instruments Business registration, with a target acquisition in FY2026 to enter stock index, FX, and options markets.

- Management changes include the appointment of Satoru Matsushima as Representative Director and President, and Tsubasa Mizoguchi as Chairman of the Board, reflecting a shift to a business company-led management structure through a capital and business alliance with Cybridge LLC.

🤖 AI Perspective

The financial results indicate a decrease in revenue and an expanded net loss, which may suggest ongoing challenges in user acquisition and revenue generation within its core businesses. In response, the company has outlined a refreshed management structure and comprehensive growth strategies, including M&A and expansion into new financial product areas, which could be critical for its future trajectory. The pursuit of a Type I Financial Instruments Business license is a notable development, potentially enabling the company to broaden its product offerings and diversify its revenue base.

2186|ソーバル

907.0

▲ +0.44%

📄 Announcement (AI-Reviewed)

- Sobal Corporation announced its consolidated financial results for the fiscal year ended February 2026, reporting net sales of JPY 8,976 million (up 3.4% year-on-year), operating profit of JPY 662 million (up 8.1%), ordinary profit of JPY 680 million (up 5.5%), and net income attributable to owners of parent of JPY 460 million (up 6.5%).

- The annual dividend for the fiscal year ended February 2026 was set at JPY 33.00 per share (JPY 16.50 interim, JPY 16.50 year-end), consistent with the previous fiscal year.

- For the fiscal year ending February 2027, the consolidated earnings forecast projects net sales of JPY 10,000 million (up 11.4% year-on-year), while operating profit is expected to be JPY 650 million (down 1.8%), ordinary profit JPY 670 million (down 1.6%), and net income attributable to owners of parent JPY 420 million (down 8.7%).

- During the consolidated fiscal year, Riso Co., Ltd. was newly included in the scope of consolidation.

- An impairment loss on investment securities of JPY 23 million was recorded as an extraordinary loss in the consolidated fiscal year.

🤖 AI Perspective

While Sobal Corporation achieved increased revenue and profit in its consolidated results for FY2026/2, the forecast for FY2027/2 indicates a projected increase in sales but a decrease in profit, which may draw investor attention. The inclusion of a new subsidiary in the scope of consolidation suggests efforts to expand the business foundation. However, factors such as plan changes and unprofitable projects in some core businesses, alongside the recording of an extraordinary loss, are noted as having influenced performance. The strong performance in the embedded systems sector versus challenges in other areas could be a key focus for investors monitoring the company’s future earnings structure.

276A|G-ククレブ

3490.0

▼ -1.55%

📄 Announcement (AI-Reviewed)

- G-Creb Advisors, Inc. (Code: 276A) announced on April 13, 2026, an upward revision to its consolidated financial forecast for the fiscal year ending August 2026.

- The consolidated net sales forecast has been revised from the previous JPY 4,700 million to JPY 7,000 million, representing a 48.9% increase.

- The forecasts for consolidated operating profit, ordinary profit, profit attributable to owners of parent, and basic earnings per share remain unchanged.

- The revision is attributed to the acceleration of the capital recycling strategy for properties held for sale, in response to global uncertainties and financial market conditions, which clarified the outlook for B/S utilization projects’ exit strategies.

- The dividend forecast remains unchanged at this time, but the company states it will consider flexible adjustments, including an increase, based on progress in the second half and its shareholder return policy.

🤖 AI Perspective

The significant upward revision in revenue while profit figures remain unchanged may be a key point for investors to consider. This could suggest that the accelerated capital recycling strategy for properties resulted in earlier revenue recognition without a proportional increase in profitability, possibly due to the nature of the deals or associated costs. Investors may look to future quarterly reports for detailed breakdowns of profit contributions and the ongoing impact of this strategy.

3030|ハブ

959.0

▼ -1.03%

📄 Announcement (AI-Reviewed)

- HUB Co., Ltd. announced a discrepancy between its full-year earnings forecast and actual results for the fiscal year ended February 2026 (March 1, 2025 – February 28, 2026).

- Actual full-year results were Net Sales of ¥11,335 million (up 0.3% from forecast), Operating Profit of ¥534 million (up 13.7%), and Ordinary Profit of ¥528 million (up 17.4%).

- Net Profit for the period reached ¥609 million against a forecast of ¥420 million, exceeding the forecast by ¥189 million (+45.2%). This increase was primarily due to the recognition of deferred tax assets totaling ¥157 million.

- The annual dividend forecast for the fiscal year ended February 2026 has been revised upwards from the previously announced ¥10 per share to ¥11 per share, which includes a ¥1 special dividend in addition to the ¥10 ordinary dividend.

- This dividend revision aims to enhance shareholder returns following the increase in net profit and is subject to approval at the 28th Annual General Meeting of Shareholders scheduled for May 2026.

🤖 AI Perspective

- HUB’s full-year performance for the fiscal year ending February 2026 highlights a significant upward revision in net profit, mainly driven by the recognition of deferred tax assets, while sales through ordinary profit generally tracked within expectations.

- The company’s decision to implement a special dividend, reflecting the boosted net profit, may suggest a strong commitment to shareholder returns in line with its profit distribution policy.

- However, it is worth noting that this profit increase resulted from an accounting adjustment rather than a direct increase in cash and equivalents, which could be a factor for investors to consider when assessing the sustainability of future dividends and the company’s financial health.

3075|銚子丸

1610.0

▲ +0.31%

📄 Announcement (AI-Reviewed)

- Choushimaru Co., Ltd. announced its financial results for the fiscal year ended February 2026 (March 1, 2025, to February 28, 2026).

- The company reported net sales of ¥23,667 million, operating profit of ¥1,575 million, ordinary profit of ¥1,596 million, and net profit of ¥1,006 million for the period.

- Earnings per share (EPS) for the fiscal year were ¥80.57.

- The annual dividend per share was ¥14.00 for the fiscal year ended February 2026, an increase from ¥12.00 in the previous fiscal year ended February 2025.

- The total number of stores reached 93 at the end of the fiscal year, with new openings including the Futamatagawa store in Kanagawa Prefecture and Shinjuku Subnade store (a new urban format) in Tokyo.

- On November 1, 2025, Choushimaru achieved a Guinness World Records™ title for “Most simultaneous tuna cutting shows (multiple venues)” across 71 stores.

- Due to a change in the fiscal year end from the previous period, a year-over-year percentage change is not provided as the comparison periods differ.

🤖 AI Perspective

Choushimaru’s fiscal year ended February 2026 results show an increase in net sales and all profit figures compared to the previous fiscal year ended February 2025. While a direct year-over-year comparison is not provided due to the change in fiscal year period, the reported figures suggest robust business activity. Strategic initiatives such as achieving a Guinness World Records™ title, new store openings, and DX promotion may have contributed to customer engagement and strengthening the business foundation in a competitive market.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

3111|オーミケンシ

226.0

▼ -1.74%

📄 Announcement (AI-Reviewed)

- Omi Kenshi announced on April 13, 2026, the postponement of its financial results announcement for the fiscal year ending March 2026, which was originally scheduled for May 13, 2026 (Wednesday).

- The reason for the delay is a system disruption caused by unauthorized access (cyberattack) that occurred on March 16, 2026, leading to a halt in core systems and delays in financial settlement procedures.

- The company will promptly announce the new date for the financial results presentation once it is determined, based on the progress of the overall system recovery efforts.

- The impact of this incident on the company group’s financial performance for the fiscal year ending March 2026 and subsequent periods is currently under investigation, with information to be disclosed promptly if required.

🤖 AI Perspective

The postponement of the financial results due to a cyberattack highlights the critical importance of IT security in corporate operations. Investors will likely focus on the new announcement date and any disclosed impacts on performance for the fiscal year ending March 2026 and beyond. The progress of system recovery and its potential implications for business operations are aspects worth monitoring.

3168|MERF

1561.0

▲ +5.97%

📄 Announcement (AI-Reviewed)

- For the second quarter of the fiscal year ending August 2026 (interim period), consolidated net sales increased by 5.9% year-over-year to ¥45,592 million.

- Operating income turned profitable to ¥2,515 million (from a loss of ¥164 million in the prior interim period), ordinary income to ¥2,582 million (from a loss of ¥227 million), and net income attributable to owners of parent to ¥1,682 million (from a loss of ¥177 million).

- Ordinary income marked a record high for an interim consolidated accounting period in 15 terms.

- An interim dividend of ¥20.00 per share (¥10.00 ordinary, ¥10.00 commemorative) is planned for the second quarter of FY2026. The full-year dividend forecast remains unchanged at ¥30.00 per share (interim ¥20.00, year-end ¥10.00).

- The full-year consolidated earnings forecast for FY2026, announced on February 13, 2026, remains unchanged, projecting net sales of ¥89,234 million (up 8.2% year-over-year) and net income attributable to owners of parent of ¥1,853 million.

🤖 AI Perspective

The significant turnaround to profitability and the record high ordinary income for this interim period may suggest the effectiveness of MERF’s strategies, including rising sales prices in the non-ferrous metals business, a review of less profitable transactions, and the expansion into the North American market through its overseas subsidiaries. The steady demand in the fine arts and crafts business could also have contributed to the overall performance. With the full-year earnings forecast remaining unchanged, it appears the company anticipates these positive factors to continue into the second half of the fiscal year, making future developments worth monitoring.

3236|プロパスト

367.0

▲ +1.10%

📄 Announcement (AI-Reviewed)

- Properst Co., Ltd. announced its consolidated financial results for the third quarter of the fiscal year ending May 2026 (June 1, 2025 – February 28, 2026) on April 13, 2026.

- For the cumulative period, consolidated net sales were JPY 17,612 million, operating income JPY 2,223 million, ordinary income JPY 2,204 million, and net income attributable to owners of parent JPY 1,570 million.

- By segment, the Rental Development business reported net sales of JPY 15,752 million and the Value-Up business reported JPY 1,849 million, while the Condominium Development business reported zero net sales.

- Ogawa Construction Co., Ltd. was consolidated as a subsidiary with an acquisition date of October 27, 2025; however, only its balance sheet as of December 31, 2025, was consolidated for this third quarter, and its operating results are not included.

- The consolidated full-year forecast for the fiscal year ending May 2026 is net sales of JPY 30,246 million, operating income of JPY 3,586 million, ordinary income of JPY 3,433 million, and net income attributable to owners of parent of JPY 2,138 million, representing a revision from the most recently published forecast.

🤖 AI Perspective

Properst’s Q3 FY2026 results indicate that its Rental Development and Value-Up segments are the primary drivers of consolidated sales. The absence of sales from the Condominium Development segment suggests a shift in focus or timing of projects, which may be an area for investor monitoring. Furthermore, while Ogawa Construction Co., Ltd. has been consolidated, its operational results are not yet reflected, suggesting that its full impact on consolidated performance will emerge in future periods. The revision to the full-year forecast may also warrant close attention from investors.

3281|R-GLP

133400.0

▲ +0.60%

📄 Announcement (AI-Reviewed)

- R-GLP announced that its Net DPU for the fiscal period ending February 2026 (28th period) reached ¥2,741, surpassing its initial forecast by 3.3%.

- The DPU for the same period was ¥3,399, exceeding the initial forecast by 9.6%.

- Rent increase rates on contract renewals achieved 9.0%, while CPI-linked rent adjustments recorded 8.7%.

- The REIT established a maximum ¥13 billion unitholder unit acquisition program and acquired two properties at a 10.8% discount to appraisal value, contributing ¥45/year to DPU.

- R-GLP anticipates an annual Net DPU growth of 3.8% towards the fiscal period ending February 2027, with a target of over 4% growth towards the fiscal period ending August 2028.

🤖 AI Perspective

The strong performance in the February 2026 fiscal period suggests that accelerated internal growth and efficient capital allocation may have contributed to the higher-than-expected DPU. High rent increase rates and the utilization of inflation-responsive contracts could indicate a robust revenue base. The establishment of a unit acquisition program and planned increase in excess distribution may also reflect a proactive stance towards unitholder returns.

3349|コスモス薬品

6348.0

▼ -1.12%

📄 Announcement (AI-Reviewed)

- Cosmos Pharmaceutical Co., Ltd. announced its consolidated financial results for the third quarter of the fiscal year ending May 2026 (June 1, 2025, to February 28, 2026).

- For the nine months ended February 28, 2026, net sales increased by 7.7% year-on-year to ¥810,380 million. Operating profit rose by 1.2% to ¥32,021 million, ordinary profit by 0.3% to ¥33,865 million, and profit attributable to owners of parent by 1.8% to ¥22,748 million.

- As of the end of the third consolidated accounting period, the total number of stores was 1,662, following the opening of 57 new stores and the closing of 4 stores.

- The forecast for the annual dividend for the fiscal year ending May 2026 is ¥75.00 per share (interim ¥37.50, year-end ¥37.50), with no revisions from the most recently announced dividend forecast.

- The consolidated full-year earnings forecast for the fiscal year ending May 2026 remains unchanged from the forecast announced on July 11, 2025, projecting net sales of ¥1,057,000 million, operating profit of ¥40,500 million, ordinary profit of ¥43,200 million, and profit attributable to owners of parent of ¥31,000 million.

🤖 AI Perspective

While the company achieved increased revenue and profits in the third quarter, the profit growth rate was lower than the sales growth rate. This may suggest that the company’s strategy of pursuing further low-cost operations and offering products at the lowest possible prices, amidst economic uncertainties and increased consumer frugality, along with aggressive store expansion, has influenced profitability. The unchanged full-year earnings forecast could indicate the company’s confidence in realizing the benefits of these strategies in the remaining period.

340A|G-ジグザグ

396.0

▲ +3.39%

📄 Announcement (AI-Reviewed)

- G-Zigzag announced its financial results for the third quarter ended February 28, 2026 (cumulative from June 1, 2025).

- Net sales for the period totaled JPY 1,088 million, marking a 2.2% increase compared to the same period in the previous year.

- Operating profit stood at JPY 209 million (down 21.4% year-on-year), ordinary profit at JPY 219 million (down 18.5%), and quarterly net profit at JPY 150 million (down 14.5%).

- In December 2025, the company announced the establishment of its first overseas subsidiary in Taiwan and proceeded with the introduction of JKOPAY, one of Taiwan’s largest payment methods.

- Total assets reached JPY 2,357 million, and net assets grew to JPY 1,297 million, with the equity ratio improving from 52.4% at the end of the previous fiscal year to 55.0%.

- The full-year earnings forecast for the fiscal year ending May 2026 remains unchanged from the most recently announced figures: net sales of JPY 1,639 million, operating profit of JPY 328 million, ordinary profit of JPY 328 million, and net profit of JPY 240 million.

🤖 AI Perspective

While net sales showed an increase year-on-year, all profit metrics experienced a decline. This could suggest that the company’s strategic investments, such as the establishment of an overseas subsidiary and payment system integration, may have impacted short-term profitability. The improvement in the equity ratio indicates a strengthening of the company’s financial foundation. With the full-year forecast unchanged, management likely anticipates a recovery or positive impact from ongoing initiatives in the remaining period.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

3562|No.1

1607.0

▼ -0.86%

📄 Announcement (AI-Reviewed)

- For the fiscal year ended February 2026, consolidated net sales were JPY 17,529 million (+23.4% year-on-year), operating profit was JPY 1,330 million (+28.1%), ordinary profit was JPY 1,393 million (+34.5%), and profit attributable to owners of parent was JPY 713 million (+24.3%).

- The annual consolidated dividend for FY2026/2 was JPY 78 (interim JPY 18, year-end JPY 60), marking an increase from JPY 35 in the previous fiscal year.

- For the fiscal year ending February 2027, the company forecasts consolidated net sales of JPY 21,200 million (+20.9% year-on-year), operating profit of JPY 1,650 million (+24.0%), and profit attributable to owners of parent of JPY 1,000 million (+40.1%). The estimated annual dividend is JPY 79.

- During the consolidated fiscal year, six companies, including 株式会社アイ・ステーション and 株式会社LGIC, were newly added to the scope of consolidation, while one company, 株式会社オフィスアルファ, was excluded.

- The company implemented changes in accounting policies due to revisions in accounting standards.

🤖 AI Perspective

The substantial increase in both revenue and profits for the current fiscal year, along with optimistic forecasts for the next period, may suggest a positive business momentum for No.1 Co., Ltd. The significant rise in the annual dividend for the current fiscal year and the projected further increase for the next fiscal year could indicate a commitment to shareholder returns. Changes in the scope of consolidation, with multiple new additions and one exclusion, might have contributed to the reported financial results, and are worth monitoring for their future impact.

3612|ワールド

1546.0

▼ -4.21%

📄 Announcement (AI-Reviewed)

- WORLD Co., Ltd. announced on April 13, 2026, the Q2 FY2026 interim financial results (September 1, 2025 – February 28, 2026) for its wholly-owned subsidiary, Right-on Co., Ltd., which was delisted on February 26, 2026, and fully acquired by WORLD on March 1, 2026.

- For the interim period, net sales were ¥10,388 million (down 38.6% year-on-year), with an operating loss of ¥610 million (vs. ¥244 million operating loss in the prior year interim period), an ordinary loss of ¥813 million (vs. ¥469 million ordinary loss), and a net loss of ¥846 million (vs. ¥239 million net loss).

- In terms of financial position, total net assets at the end of the interim fiscal period were negative ¥389 million, resulting in an insolvent position (compared to ¥496 million at the end of the previous fiscal year). The equity ratio was -3.5%.

- No full-year earnings forecast for FY2026 is provided due to the company’s delisting.

- At the end of the interim period, Right-on operated 206 stores, following the closure of 24 stores. While the gross profit margin improved to 52.1% (from 49.3% in the prior year) due to initiatives such as MD review, expansion of private brand ratio, and strengthened supply chain information sharing under the medium-term management plan, sales were below plan due to persistent issues with product assortment.

🤖 AI Perspective

- This disclosure represents the first financial announcement for Right-on since its full acquisition by parent company WORLD Co., Ltd. and subsequent delisting, offering insights into its operational status under the new structure.

- While revenue decline and expanded losses persist, initiatives such as MD review, private brand expansion, and cost reduction efforts under the medium-term management plan have led to an improved gross profit margin, suggesting ongoing foundational work for business reconstruction.

- The transition to a negative equity position due to the recorded net loss indicates that restoring financial health may be a key focus going forward.

3678|メディアドゥ

1581.0

▲ +0.70%

📄 Announcement (AI-Reviewed)

- For the fiscal year ended February 2026, Media Do Co., Ltd. reported consolidated net sales of ¥108,537 million (up 6.5% year-on-year), operating income of ¥2,453 million (down 0.9%), ordinary income of ¥2,548 million (up 8.0%), and net income attributable to owners of parent of ¥1,818 million (up 33.3%).

- Earnings per share for the period were ¥119.85.

- The company paid an annual dividend of ¥40.00 per share for the fiscal year ended February 2026. The forecast for the fiscal year ending February 2027 is an annual dividend of ¥40.00 per share.

- The consolidated earnings forecast for the fiscal year ending February 2027 projects net sales of ¥118,000 million (up 8.7% year-on-year), operating income of ¥2,400 million (down 2.2%), ordinary income of ¥2,050 million (down 19.6%), and net income attributable to owners of parent of ¥1,200 million (down 34.0%).

- The Electronic Book Distribution business recorded sales of ¥101,107 million (up 7.8%) and operating income of ¥4,919 million (down 1.2%). The Strategic Investment business recorded sales of ¥8,716 million (down 7.4%) and an operating loss of ¥631 million (an improvement of ¥322 million year-on-year).

🤖 AI Perspective

The consolidated results for the fiscal year ended February 2026 show an increase in net sales and net income attributable to owners of parent, while operating income experienced a slight decrease. Looking ahead, the consolidated earnings forecast for the fiscal year ending February 2027 anticipates higher net sales but projects a decline in operating income, ordinary income, and net income attributable to owners of parent, which may be a key area for investor attention.

3760|ケイブ

655.0

▼ -1.50%

📄 Announcement (AI-Reviewed)

- For the third quarter of fiscal year 2026 (June 1, 2025 – February 28, 2026), consolidated net sales were ¥8,750 million (down 13.9% year-on-year), and net loss attributable to owners of parent was ¥3,406 million (compared to a profit of ¥985 million in the prior year). Operating and ordinary income also turned into losses.

- The full-year consolidated earnings forecast was revised downwards, projecting net sales of ¥11,900 million (down 14.8% year-on-year) and a net loss attributable to owners of parent of ¥3,200 million.

- The Game Business segment recorded net sales of ¥7,957 million (down 14.2% year-on-year) and a segment loss of ¥1,037 million (compared to a segment profit of ¥825 million in the prior year).

- The service for “Meteo Arena Stars” ended in December 2025, and “OUTRANKERS” closed in February 2026, with related costs impacting financial performance in the third quarter.

- CAVE transferred all shares of its consolidated subsidiary, capable Inc., on March 31, 2026, and capable is expected to be excluded from consolidation.

🤖 AI Perspective

The key takeaways from this earnings report appear to be the decline in net sales, significant losses reported for the quarter, and a downward revision of the full-year forecast. The cessation and early withdrawal of multiple game titles, along with associated costs, may have contributed to the expanded losses. Furthermore, the transfer of shares in the video streaming-related subsidiary could suggest a restructuring of the business portfolio.

3996|サインポスト

224.0

▲ +0.45%

📄 Announcement (AI-Reviewed)

- Signpost Co., Ltd. reported a revenue of 3,138 million JPY for the fiscal year ended February 2026 (March 1, 2025 – February 28, 2026), marking a 3.8% increase year-on-year.

- However, operating profit significantly decreased by 50.8% to 98 million JPY, ordinary profit by 53.2% to 92 million JPY, and net profit by 70.4% to 76 million JPY.

- The primary factors cited for the profit decline include development costs for “Global GO! Smooth EC” and generative AI tools, increased personnel expenses related to sales and business development, and the reversal of deferred tax assets.

- For the fiscal year ending February 2027 (March 1, 2026 – February 28, 2027), the company forecasts an increase in revenue to 3,850 million JPY (22.7% increase year-on-year), but anticipates further declines in operating profit to 56 million JPY (43.1% decrease), ordinary profit to 51 million JPY (44.9% decrease), and net profit to 66 million JPY (13.4% decrease).

- The company announced the transfer of all shares in TOUCH TO GO Co., Ltd., a developer and seller of unmanned payment systems, to Secure Inc., effective April 1, 2026. The gain on sale of these shares is expected to be recorded in the financial statements for the fiscal year ending February 2027.

🤖 AI Perspective

In the fiscal year ended February 2026, Signpost maintained revenue growth, but aggressive investments in new solution development and personnel expenses appear to have impacted profitability. The fiscal year 2027 forecast also projects increased revenue alongside decreased profits, suggesting that the future returns on these upfront investments will be a key area for investors to monitor. Furthermore, the divestiture of TOUCH TO GO shares could indicate a strategic optimization of the business portfolio or a reallocation of management resources.

4167|G-ココペリ

324.0

▲ +5.88%

📄 Announcement (AI-Reviewed)

- Kokopelli, Inc. announced a business alliance agreement with CCREB Advisors Inc. on April 13, 2026, aimed at promoting regional revitalization.

- Through this alliance, G-Kokopelli’s “BM Portal,” a business matching management service for financial institutions, will be system-integrated with CCREB Advisors’ “CCREB Matching Box,” a commercial real estate matching service.

- The partnership aims to strengthen real estate matching for regional financial institutions and local companies, and to jointly develop and expand new businesses that contribute to solving challenges in regional communities.

- CCREB Advisors Inc., the partner company, specializes in Corporate Real Estate (CRE) and provides a unique real estate tech system utilizing AI.

- G-Kokopelli anticipates that the impact of this alliance on its performance for the fiscal year ending March 2027 will be minor.

🤖 AI Perspective

This business alliance is seen as an integration of G-Kokopelli’s nationwide network of regional financial institutions and CCREB Advisors’ specialized expertise in commercial real estate matching. This synergy could lead to the effective utilization of idle assets in rural areas and promote the liquidity of small to medium-sized factories and warehouses. Such developments, by enhancing the management support provided by regional financial institutions, may contribute to G-Kokopelli’s medium-to-long-term business expansion.

542A|G-ビタブリッドJ

1290.0

▲ +10.45%

📄 Announcement (AI-Reviewed)

- G-Vitabrid Japan announced its non-consolidated financial results for the fiscal year ended February 2026.

- For the period from March 1, 2025, to February 28, 2026, net sales reached ¥15,296 million, marking a 21.2% increase from the previous fiscal year.

- Operating profit was ¥1,022 million (up 45.8%), ordinary profit was ¥991 million (up 46.7%), and net profit was ¥689 million (up 50.0%).

- The flagship product “Terminalia First” continued its steady growth, while “Vitabrid Daily GABA” achieved significant sales growth. “Active Rich 5,” launched in July 2025, has also shown a favorable performance track record.

- For the fiscal year ending February 2027, the company forecasts net sales of ¥17,600 million (up 15.1%), operating profit of ¥1,100 million (up 7.6%), ordinary profit of ¥1,082 million (up 9.2%), and net profit of ¥717 million (up 4.1%).

🤖 AI Perspective

- The fiscal year 2026/2 saw profit growth outpace revenue growth, which may suggest an improvement in profitability potentially driven by a recovery in advertising efficiency following a temporary decline.

- The sustained growth of core products, coupled with the introduction of new products and an expansion of wholesale distribution, could indicate a strategic focus on diversifying the product portfolio and strengthening sales channels.

- The projected diluted EPS for FY2027/2, calculated considering public stock offerings and over-allotment shares, is a relevant detail for investors to consider in the context of future valuation.

6505|東洋電

2300.0

▼ -1.96%

📄 Announcement (AI-Reviewed)

- For the third quarter of fiscal year 2026 (cumulative), consolidated net sales totaled ¥28,961 million, a 0.2% decrease year-on-year.

- Consolidated operating profit reached ¥1,895 million (up 47.2% YoY), ordinary profit was ¥2,241 million (up 31.9% YoY), and net profit attributable to parent company shareholders was ¥1,851 million (up 46.7% YoY).

- The Transportation segment’s profit increased by 71.7% to ¥3,827 million, while the Industrial segment’s profit decreased by 23.6% to ¥770 million, and the ICT Solutions segment recorded a loss of ¥90 million.

- The consolidated full-year earnings forecast for fiscal year 2026 and the annual dividend forecast (¥75.00 at fiscal year-end) remain unchanged from the most recent public announcement.

- As of the end of the current cumulative quarter, consolidated total assets stood at ¥59,012 million, net assets at ¥31,049 million, and the equity ratio at 52.6%.

🤖 AI Perspective

Despite nearly flat net sales, the substantial increases in operating, ordinary, and net profits suggest an improvement in the company’s profitability. Segment performance indicates a divergence, with significant profit growth in the Transportation segment contrasting with decreased profits or losses in the Industrial and ICT Solutions segments, which is worth monitoring. The unchanged full-year earnings and dividend forecasts suggest that the company views the current progress as consistent with its original projections.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

6634|JNグループ

99.0

▼ -1.98%

📄 Announcement (AI-Reviewed)

- JN Group has announced its consolidated financial results for the first quarter of the fiscal year ending November 2026 (December 1, 2025 – February 28, 2026).

- Consolidated net sales for the quarter were ¥683 million (up 5.9% year-on-year), but the company recorded an operating loss of ¥347 million, an ordinary loss of ¥513 million, and a net loss attributable to owners of parent of ¥490 million.

- By segment, the “Metaverse and Digital Content Business” reported sales of ¥144 million (up 6.0% year-on-year) and an operating income of ¥11 million (compared to an operating loss of ¥12 million in the previous period).

- This segment highlighted strong e-book sales and the commission service “Skeb” surpassing 3.87 million registered users as of February 2026.

- The full-year consolidated earnings forecast for the fiscal year ending November 2026 remains unchanged, with projected net sales of ¥4,383 million, operating income of ¥103 million, and net income attributable to owners of parent of ¥111 million.

🤖 AI Perspective

While the overall consolidated results for the quarter showed an expanded loss, the sales growth and shift to operating profitability within the key “Metaverse and Digital Content Business” segment could be noteworthy. The unchanged full-year earnings forecast may suggest management anticipates an improvement in subsequent quarters. The performance of digital content businesses is likely to be a critical factor in the company’s overall consolidated results moving forward.

5578|G-ARアドバンスト

863.0

▼ -2.49%

📄 Announcement (AI-Reviewed)

- G-AR Advanced reported consolidated results for the first half of FY2026 (ended February 29, 2026) with net sales of ¥7,948 million (up 21.1% year-on-year) and ordinary profit of ¥612 million (up 125.1% year-on-year).

- The gross profit margin for the same period increased by 5.5 percentage points year-on-year to 31.2%.

- The company revised its full-year FY2026 consolidated earnings forecast upwards, with net sales adjusted from ¥16,010 million to ¥16,433 million, and ordinary profit from ¥960 million to ¥1,194 million.

- A new service, “InnovaCall,” which supports talent development through practical voice role-playing using generative AI, launched in April 2026.

- A record 55 new graduates joined the group in April 2026.

🤖 AI Perspective

The reported first half results show significant growth in both sales and profit, indicating a robust operational performance. The substantial increase in gross profit margin may suggest a successful shift towards high-value AI-related projects. The upward revision of the full-year forecast could reflect continued strong demand in the DX and AI sectors, combined with the successful integration of new talent.

1401|G-エムビーエス

1401.0

▼ -1.62%

📄 Announcement (AI-Reviewed)

- For the third quarter ended February 28, 2026 (June 1, 2025 – February 28, 2026), G-MBS reported consolidated net sales of 3,415 million JPY (up 1.3% year-on-year), operating profit of 522 million JPY (up 21.6%), ordinary profit of 552 million JPY (up 18.3%), and quarterly net profit of 379 million JPY (up 15.6%).

- Basic earnings per share for the quarter amounted to 54.17 JPY.

- As of February 28, 2026, total assets were 5,310 million JPY, net assets were 3,729 million JPY, and the equity ratio stood at 70.2%.

- The full-year earnings forecast for the fiscal year ending May 2026 remains unchanged from the most recently announced figures: net sales of 5,200 million JPY, operating profit of 700 million JPY, ordinary profit of 739 million JPY, and annual net profit of 500 million JPY.

- The annual dividend forecast for the fiscal year ending May 2026 also remains unchanged at 15.00 JPY per share.

🤖 AI Perspective

G-MBS demonstrated robust performance in its Q3 FY2026, with year-on-year increases in both revenue and various profit metrics. The notable 21.6% rise in operating profit may suggest effective cost management and improved operational efficiencies, potentially contributing to the overall positive results. With both the full-year earnings and dividend forecasts maintained, the company appears to be on track to meet its annual targets, indicating continued focus on strengthening existing businesses and enhancing profitability.

2736|フェスタリアHD

675.0

▲ +2.43%

📄 Announcement (AI-Reviewed)

- Festaria Holdings Co., Ltd. announced its consolidated financial results for the second quarter of the fiscal year ending August 2026 (interim period: September 1, 2025, to February 28, 2026).

- Consolidated net sales for the interim period amounted to ¥4,976 million, representing a 5.9% increase compared to the same period in the previous year.

- Operating profit was ¥60 million (down 56.8% year-on-year), ordinary profit was ¥61 million (down 50.0% year-on-year), and net profit attributable to owners of parent was ¥47 million (down 43.3% year-on-year).

- In the domestic business, store sales increased by 4.5% year-on-year, e-commerce sales by 29.9%, and high-net-worth business sales by 6.2%.

- The gross profit margin decreased by 1.6 percentage points, and selling, general and administrative expenses increased by 6.2% year-on-year. The full-year consolidated earnings forecast remains unchanged, projecting net sales of ¥10,100 million, operating profit of ¥330 million, and net profit attributable to owners of parent of ¥160 million.

🤖 AI Perspective

While the interim period saw an increase in sales, significant pressure on profits appears to stem from rising raw material costs and increased selling, general, and administrative expenses. The unchanged full-year earnings forecast may suggest management anticipates a recovery or improved efficiency in the latter half of the fiscal year, making the progress of profit improvement strategies a key area to monitor. Fluctuations in raw material prices and the profitability trends across various sales channels could potentially influence future performance.

3063|G-jGroup

815.0

▲ +0.25%

📄 Announcement (AI-Reviewed)

- G-jGroup Holdings, Inc. reported consolidated net sales of 13,045 million yen (up 121.4% YoY), exceeding 13 billion yen, for the fiscal year ended February 2026.

- Operating profit reached 420 million yen (up 111.5% YoY), marking the third consecutive period of revenue and profit growth since the COVID-19 pandemic, with both operating and ordinary profits achieving record highs for three consecutive periods.

- Net profit for the period decreased to 312 million yen (down 68.1% YoY), primarily due to a special gain of 322 million yen recorded in the previous fiscal year related to compensation for store closures.

- Cash and deposits significantly increased to 2,454 million yen, largely attributable to the sale of inventory assets (real estate).

- During the fiscal year ended February 2026, Mountain Coffee Co., Ltd. was integrated into the group through M&A, and M&A activities conducted in the fiscal year ended February 2025 (EOC Group and A-Round) also contributed steadily to performance.

🤖 AI Perspective

G-jGroup Holdings appears to be strengthening its revenue base through strategic initiatives such as M&A and real estate sales, in addition to recovering from the pandemic. The record-high operating profit for three consecutive periods may suggest an improvement in the profitability of its core business. The substantial increase in cash and deposits could provide a strong foundation for future business expansion, including further M&A, new store openings, and large-scale renovations.

3679|じげん

409.0

▼ -0.24%

📄 Announcement (AI-Reviewed)

- Zigexn announced the expected recording of non-operating income in its unconsolidated financial results for the first quarter of the fiscal year ending March 2027 (April 1 to June 30, 2026).

- The non-operating income will consist of dividends received, totaling 1,711 million JPY.

- These dividends are derived from the distribution of retained earnings from six consolidated subsidiaries, including ReJOB Co., Ltd. (779 million JPY), Ties Co., Ltd. (481 million JPY), and Appleworld Co., Ltd. (300 million JPY).

- The receipt date for these dividends is scheduled for around April 2026.

- The aforementioned dividends will be eliminated in the consolidated financial statements, therefore having no impact on consolidated earnings.

🤖 AI Perspective

- This announcement indicates a prospective increase in non-operating income for Zigexn’s unconsolidated financial statements.

- The receipt of dividends from consolidated subsidiaries may suggest internal capital reallocation or profit distribution within the group.