📌 Today’s Highlights

Today we cover 50 IR announcements. Notable among them: C&R社 (4763), G-プログリット (9560), GX超長期米国債H (179A). Use the table of contents below to navigate to each company.

- 4763|C&R社

- 9560|G-プログリット

- 179A|GX超長期米国債H

- 6255|G-NPC

- 3048|ビックカメラ

- 428A|サイプレスHD

- 9835|ジュンテンド

- 8127|ヤマトインター

- 8260|井筒屋

- 9313|丸八倉

- 9974|ベルク

- 6432|竹内製作所

- 1447|G-SAAFHD

- 2747|北雄ラッキー

- 3201|ニッケ

- 4673|川崎地質

- 7611|ハイデ日高

- 7811|中本パックス

- 137A|G-Cocolive

- 1419|タマホーム

- 2157|コシダカHD

- 2164|地域新聞社

- 2735|ワッツ

- 2742|ハローズ

- 2791|大黒天

- 2999|ホームポジション

- 3063|G-jGroup

- 3192|白鳩

- 3280|エストラスト

- 3501|SUMINOE

- 3546|アレンザHD

- 3560|ほぼ日

- 3612|ワールド

- 3815|G-メディア

- 4076|G-シイエヌエス

- 4187|大有機化

- 4361|川口化

- 4370|G-モビルス

- 4430|東海ソフト

- 4443|Sansan

- 460A|G-BRANU

- 4992|北興化

- 5271|トーヨーアサノ

- 6093|エスクローAJ

- 6136|OSG

- 6289|技研製作所

- 7373|G-アイドマHD

- 2769|ヴィレッジV

- 7427|エコーTD

- 3046|JINSHD

4763|C&R社

1426.0

▼ -3.12%

📄 Announcement Facts

- C&R Inc. has announced the release of its financial results briefing material for the fiscal year ending February 2026.

- The IR information provided does not include specific details or content from this briefing material.

- Consequently, it is not possible to report on specific facts such as financial performance figures, future outlook, or business strategies presented in the material.

🤖 AI Perspective

Based on the limited information provided, an analysis of C&R Inc.’s specific financial performance or strategic direction for the fiscal year ending February 2026 cannot be made. Investors would typically need to review the comprehensive details within the official briefing material to assess the company’s current status and future prospects.

9560|G-プログリット

828.0

▲ +1.60%

📄 Announcement Facts

- PROGRIT Inc., in its Q&A regarding the 2Q FY2026 financial results, stated that it is considering business expansion into “human resource development” beyond English for business professionals and “education for younger generations” including students and children, with M&A opportunities under consideration.

- The number of consultants at the end of the third quarter is projected to be within the 161-170 range, which is the full-year forecast premise, and the company expects to achieve the initially projected number by the end of the current fiscal year.

- Contract liabilities exceeded JPY 1 billion for the first time, primarily due to concentrated marketing investments in January, the peak demand period for English learning, which resulted in more new contract acquisitions than anticipated. The new Meguro school opening did not directly impact this increase.

- The company cited three reasons for expanding its corporate services: “contribution to mission fulfillment,” “higher profit margins,” and “business stability and continuity,” with a long-term goal of achieving a 50:50 sales ratio between corporate and individual services.

- PROGRIT plans to continue operating Study Hacker Inc. as separate brands without service integration. The acquisition of approximately 100 trainers from Study Hacker has significantly reduced the risk of securing talent crucial for sales growth.

🤖 AI Perspective

The Q&A summary suggests that PROGRIT is actively pursuing new growth avenues beyond its established individual English coaching business. The strategic focus on human resource development and youth education, including potential M&A, alongside strengthening corporate services, may indicate a long-term aim for revenue diversification and enhanced stability. Furthermore, the increase in contract liabilities could be interpreted as a positive sign of robust recent customer acquisition.

179A|GX超長期米国債H

257.8

▼ -0.19%

📄 Announcement Facts

- Net assets for the 2026 February term (August 25, 2025, to February 24, 2026) increased to JPY 20,839 million, up from JPY 20,667 million at the end of the August 2025 term.

- The 100-unit Net Asset Value (NAV) at the end of the current period was JPY 26,548, rising from JPY 26,095 at the end of the August 2025 term.

- Operating income for the current term reached JPY 794 million (with net income for the period being the same amount), marking a return to profitability from an operating loss in the previous term. Gains on securities trading contributed JPY 2,163 million.

- The distribution per 100 units for the 2026 February term was JPY 270.

- The capital deficit at the end of the current period was JPY △2,710 million, a reduction from JPY △3,092 million at the end of the previous term.

🤖 AI Perspective

The latest financial results indicate an improvement in the fund’s asset value, marked by an increase in net assets and a rise in the 100-unit NAV. The significant shift from an operating loss to an operating income of approximately JPY 794 million suggests enhanced operational performance. While gains on securities trading were a major contributor to this turnaround, it is also notable that foreign exchange losses widened. The reduction in the capital deficit may suggest a positive trend towards the fund’s financial health.

6255|G-NPC

780.0

▼ -0.64%

📄 Announcement Facts

- For the second quarter of the fiscal year ending August 2026, G-NPC reported consolidated net sales of ¥1,124 million (down 64.0% year-on-year) and an operating profit of ¥6 million (down 99.1% year-on-year), turning profitable from an initial forecast of a ¥189 million loss. Net loss attributable to owners of the parent was ¥49 million, a reduction from the initial forecast loss of ¥252 million.

- Net sales of ¥1,124 million exceeded the initial forecast of ¥907 million by 23.9%. Operating profit, ordinary profit, and profit before income taxes all turned profitable from initial forecasts of losses. This was attributed to increased volume in equipment relocation work for First Solar, strong component sales, and cost reductions in relevant projects.

- Total order intake at the end of Q2 FY2026 stood at ¥3,574 million (up 237.5% year-on-year), with order backlog reaching ¥9,173 million (up 52.5% year-on-year). Orders include equipment relocation and modification projects for First Solar, perovskite development equipment, and solar panel recycling equipment.

- On the consolidated balance sheet, work-in-progress increased from ¥1,044 million at the end of August 2025 to ¥3,180 million at the end of February 2026, in preparation for large domestic projects scheduled for sales recognition in Q4.

- The company executed a share buyback totaling approximately ¥500 million, equivalent to about 3.2% of its outstanding shares.

🤖 AI Perspective

The Q2 results show net sales surpassing initial forecasts and a shift to operating profitability, which may suggest an improvement in core business performance. The significant increase in order intake and backlog, coupled with a rise in work-in-progress, could indicate robust demand and potential for strong revenue recognition in the latter half of the fiscal year, particularly in Q4. This trend could be worth monitoring for insights into future earnings potential.

3048|ビックカメラ

1755.5

▼ -3.86%

📄 Announcement Facts

- Bic Camera Co., Ltd. announced that its consolidated financial results for the second quarter of the fiscal year ending August 2026 (interim period) significantly exceeded the forecasts released on October 10, 2025. Sales reached 508,429 million yen (+2.2% vs. forecast), operating profit 18,727 million yen (+29.7% vs. forecast), ordinary profit 19,421 million yen (+30.3% vs. forecast), and profit attributable to owners of parent 11,098 million yen (+15.5% vs. forecast).

- Key factors contributing to the upward revision include strong sales of personal computers and cameras, robust performance by the consolidated subsidiary L-Net Co., Ltd., and overall efforts to control selling, general, and administrative (SG&A) expenses.

- The full-year consolidated financial forecasts for the fiscal year ending August 2026 have also been revised upwards: sales from 1,013,000 million yen to 1,022,000 million yen, operating profit from 30,500 million yen to 34,400 million yen, ordinary profit from 31,500 million yen to 35,700 million yen, and profit attributable to owners of parent from 17,500 million yen to 18,400 million yen.

- The interim dividend for the fiscal year ending August 2026, with a record date of February 28, 2026, was decided at 20.00 yen per share, consistent with the most recent dividend forecast.

- The year-end dividend forecast has been revised upwards by 2 yen to 23.00 yen per share from the previous 21.00 yen per share, resulting in a revised annual dividend forecast of 43.00 yen per share (previously 41.00 yen per share).

🤖 AI Perspective

Bic Camera’s Q2 FY2026 results significantly exceeded expectations in both sales and profits, indicating strong operational performance during the interim period. This positive performance has led to an upward revision of the full-year earnings forecast and an increase in the annual dividend, which may be viewed favorably by investors. The improvement in profitability, driven by both increased sales and effective cost control, could suggest a positive trend in the company’s financial health.

428A|サイプレスHD

880.0

▼ -0.68%

📄 Announcement Facts

- Cypress HD (428A) reported consolidated results for the second quarter of the fiscal year ending August 2026, with revenue reaching JPY 6.105 billion, a 14.6% increase from the prior corresponding period.

- Net profit attributable to owners of the parent grew by 16.5% to JPY 205 million, while operating profit increased by 12.6% to JPY 369 million.

- During the period, existing store sales rose by 2.9% year-on-year, and with the opening of 7 new stores, total store sales increased by 14.6% year-on-year.

- As of February 29, 2026, the company operated 128 stores, with the plan for new store openings in the current fiscal year increasing from an initial 10 to 16.

- The full-year consolidated forecast remains unchanged, projecting revenue of JPY 12.300 billion (up 9.0% year-on-year), net profit attributable to owners of the parent of JPY 520 million (up 19.1% year-on-year), and a year-end dividend forecast of JPY 10.00 per share.

🤖 AI Perspective

The reported interim results indicate strong top-line and bottom-line growth, primarily driven by robust existing store sales and strategic new store openings. Despite facing inflationary pressures and rising personnel costs, the company managed to meet its initial profit targets for the first half, which may suggest effective cost management and pricing strategies. The reiteration of the full-year forecast could be seen as the company maintaining confidence in its ongoing business plans.

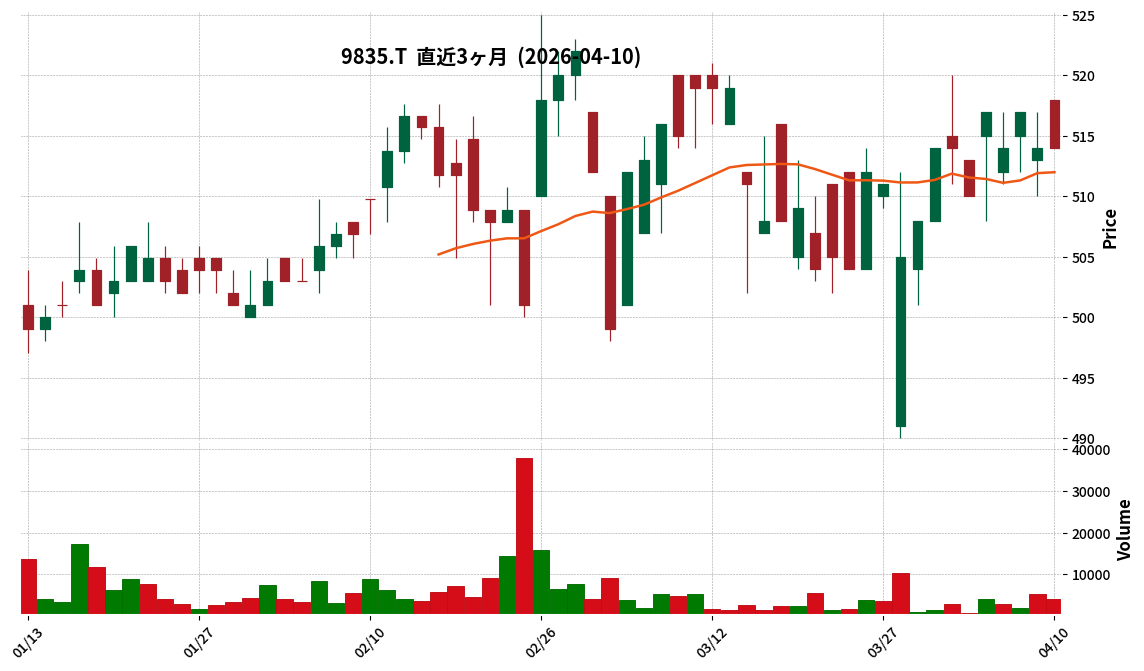

9835|ジュンテンド

514.0

▲ +0.00%

📄 Announcement Facts

- For the fiscal year ended February 2026, operating revenue was 43.04 billion yen (down 3.0% YoY), operating profit was 238 million yen (down 49.6% YoY), and ordinary profit was 208 million yen (down 54.4% YoY).

- The company reported a net loss of 361 million yen (compared to a net profit of 152 million yen in the previous year), primarily due to the recognition of impairment losses on store-related fixed assets and loss on disposal of fixed assets as extraordinary losses.

- In terms of financial position, total assets increased to 41.321 billion yen, but net assets decreased to 12.59 billion yen, resulting in a capital adequacy ratio of 30.5% (down 2.8 percentage points YoY).

- The annual dividend for the fiscal year ended February 2026 was 10.00 yen per share (final dividend 10.00 yen), with a total dividend amount of 81 million yen.

- For the fiscal year ending February 2027, the company forecasts operating revenue of 44.0 billion yen (up 2.2% YoY), operating profit of 420 million yen (up 76.4% YoY), ordinary profit of 300 million yen (up 43.8% YoY), and a net profit of 150 million yen.

🤖 AI Perspective

- The net loss reported for FY2026/2 appears to be driven by declining operating revenue, coupled with increased personnel and depreciation expenses, and significant extraordinary losses.

- The company noted that heightened consumer spending restraint, particularly in the latter half of the fiscal year, impacted sales, and the reduction in store count is a notable operational adjustment.

- Looking ahead, the forecast for FY2027/2 projects a return to net profitability, making it worthwhile to monitor the effectiveness of planned revenue improvement measures and the broader economic environment.

8127|ヤマトインター

608.0

▲ +1.33%

📄 Announcement Facts

- Yamato International reported consolidated results for the second quarter of fiscal year 2026, with net sales of ¥10,481 million (down 0.6% year-on-year), an operating loss of ¥48 million (compared to an operating profit of ¥38 million in the prior year period), and ordinary profit of ¥32 million (down 68.1% year-on-year).

- Net profit attributable to owners of parent increased by 3.8% year-on-year to ¥77 million. Diluted earnings per share for the interim period stood at ¥3.81.

- Regarding the financial position, total assets were ¥25,606 million, net assets were ¥17,923 million, and the equity ratio was 70.0%.

- The projected annual dividend for the fiscal year ending August 2026 remains unchanged from the most recently announced forecast, with an interim dividend of ¥6.00 and a year-end dividend of ¥8.00, totaling ¥14.00.

- The full-year consolidated earnings forecast for the fiscal year ending August 2026 projects net sales of ¥20,500 million (up 5.4% year-on-year) and net profit attributable to owners of parent of ¥200 million (up 39.7% year-on-year), with no revisions to the latest announced forecast.

🤖 AI Perspective

The interim results show a slight decrease in net sales and a shift to operating loss, yet an increase in net profit attributable to owners of parent, which may suggest the impact of non-operating factors on the bottom line. The unchanged full-year consolidated earnings and annual dividend forecasts could indicate that the company anticipates a recovery in the second half of the fiscal year. Furthermore, with an equity ratio of 70.0% and increased liquid assets, the company appears to maintain a strong and stable financial position.

8260|井筒屋

468.0

▲ +0.21%

📄 Announcement Facts

- For the consolidated fiscal year ended February 28, 2026, Izutsuya reported net sales of ¥21,283 million (down 3.9% year-on-year), operating profit of ¥615 million (down 40.9%), ordinary profit of ¥472 million (down 36.2%), and profit attributable to owners of parent of ¥491 million (down 50.8%).

- Diluted earnings per share for the period was ¥44.02.

- The annual dividend for the fiscal year ended February 28, 2026, was ¥6.00 per share.

- For the fiscal year ending February 28, 2027, the consolidated earnings forecast projects net sales of ¥21,000 million (down 1.3% year-on-year), operating profit of ¥800 million (up 30.0%), ordinary profit of ¥500 million (up 5.7%), and profit attributable to owners of parent of ¥500 million (up 1.7%).

- The forecast for the annual dividend for the fiscal year ending February 28, 2027, is ¥7.00 per share.

🤖 AI Perspective

While the fiscal year 2026 saw a decline in both revenue and profits, the consolidated earnings forecast for fiscal year 2027 indicates an expected increase in operating profit, ordinary profit, and profit attributable to owners of parent, despite a slight decrease in net sales. The anticipated increase in the annual dividend for the next fiscal year could also be a point of interest for investors. Additionally, the disclosed reference sales figure for the department store business, when adjusted for agency transactions, may offer further insight into the scale of operations.

9313|丸八倉

1077.0

▲ +2.38%

📄 Announcement Facts

- Maruhatsu Soko Co., Ltd. announced its consolidated financial results for the first quarter of the fiscal year ending November 2026 (December 1, 2025, to February 28, 2026).

- Net sales reached ¥1,248 million (+3.1% year-on-year), operating income ¥147 million (+2.2%), and ordinary income ¥153 million (+1.0%). Net income attributable to owners of the parent company was ¥101 million (-0.4%).

- By segment, the Logistics business reported net sales of ¥1,074 million (up ¥10 million) and segment income of ¥159 million (down ¥23 million). The Real Estate business achieved net sales of ¥174 million (up ¥26 million) and segment income of ¥86 million (up ¥16 million).

- As of the end of the first consolidated quarter (February 28, 2026), total assets stood at ¥21,030 million, net assets at ¥13,175 million, and the equity ratio was 62.5%.

- There are no revisions to the full-year consolidated performance forecast for the fiscal year ending November 2026 or the annual dividend forecast of ¥26.00 per share from the latest publicly announced figures.

9974|ベルク

7650.0

▼ -0.91%

📄 Announcement Facts

- Belc Co., Ltd. reported consolidated results for the fiscal year ended February 2026, with operating revenue of JPY 423,432 million (up 9.2% year-on-year), operating profit of JPY 17,900 million (up 5.2% year-on-year), ordinary profit of JPY 18,168 million (up 4.5% year-on-year), and net profit attributable to owners of parent of JPY 12,681 million (up 2.4% year-on-year).

- The annual dividend for the fiscal year ended February 2026 was announced as JPY 124.00 per share, an increase of JPY 4 from the previous fiscal year.

- For the fiscal year ending February 2027, the company forecasts consolidated operating revenue of JPY 434,500 million to JPY 454,600 million (up 2.6% to 7.4% year-on-year) and operating profit of JPY 18,000 million to JPY 19,800 million (up 0.6% to 10.6% year-on-year).

- During the consolidated fiscal year, Belc opened 7 new stores and renovated 6 existing stores, bringing the total number of stores to 151 as of the end of February 2026.

- The number of treasury shares increased from 21,875 at the end of February 2025 to 36,904 at the end of February 2026.

🤖 AI Perspective

The strong performance in the fiscal year ended February 2026, marked by increased revenue and profit, may suggest the positive impact of new store openings and existing store renovations. The continued increase in annual dividends could be interpreted as a commitment to shareholder returns. While the fiscal year 2027 forecast projects further revenue and profit growth, the lower end of the net profit attributable to owners of parent range indicates a potential slight decrease, suggesting that market conditions will be worth monitoring.

6432|竹内製作所

6600.0

▲ +1.38%

📄 Announcement Facts

- Takeuchi Mfg. Co., Ltd. reported consolidated financial results for the fiscal year ended February 2026, with net sales of ¥225,284 million (up 5.7% year-on-year), operating profit of ¥37,687 million (up 1.5%), ordinary profit of ¥39,187 million (up 10.1%), and profit attributable to owners of parent of ¥28,270 million (up 8.3%).

- The annual dividend for the fiscal year ended February 2026 was set at ¥210.00 per share (compared to ¥200.00 in the previous fiscal year).

- The consolidated earnings forecast for the fiscal year ending February 2027 projects net sales of ¥244,000 million (up 8.3% year-on-year), operating profit of ¥37,300 million (down 1.0%), ordinary profit of ¥36,500 million (down 6.9%), and profit attributable to owners of parent of ¥25,900 million (down 8.4%).

- Starting from the fiscal year ending February 2027, the company will shift to an annual two-dividend policy, comprising an interim dividend of ¥110.00 and a year-end dividend of ¥110.00, with an estimated total annual dividend of ¥220.00, to enhance shareholder returns.

- Unit sales during the consolidated accounting period exceeded the previous consolidated fiscal year, driven by strong sales in North America, Europe, and Asia-Oceania. Specifically, crawler loaders in North America, excavators in Europe, and a new distributor in Australia contributed to the increase in sales volume in Asia-Oceania.

🤖 AI Perspective

Takeuchi Mfg. achieved revenue and profit growth in FY2026, which appears to be supported by robust sales performance across key regions. The FY2027 earnings forecast, however, indicates a projected decline in profits despite continued revenue growth, potentially suggesting factors like increased operational costs or strategic investments. The announced increase in annual dividend and the introduction of an interim dividend could be seen as a positive step towards enhancing shareholder returns.

1447|G-SAAFHD

321.0

▼ -7.23%

📄 Announcement Facts

- G-SAAF Holdings Co., Ltd. resolved to revise its dividend forecast per share for the fiscal year ending March 31, 2026, with the record date of March 31, 2026, at a Board of Directors meeting held on April 10, 2026.

- The revision is attributed to the upward revision of the full-year performance forecast announced on February 13, 2026, indicating that net sales, operating profit, ordinary profit, and profit attributable to owners of parent are all expected to exceed the initial forecasts.

- Specifically, operating profit is projected to reach a record high for the company.

- The year-end dividend forecast for the fiscal year ending March 31, 2026, has been revised from “‐” in the previous announcement to JPY 4.50 per share (JPY 2.00 ordinary dividend, JPY 2.50 special dividend) in the revised forecast.

- The previous fiscal year’s (March 2025) year-end dividend was JPY 0.00.

🤖 AI Perspective

This dividend forecast revision appears to be a direct reflection of the company’s previously announced upward revision of its full-year performance forecast, particularly the expectation of a record-high operating profit. The decision to implement both an ordinary and a special dividend may indicate the company’s commitment to shareholder returns, aligning with its robust financial performance and marking the achievement of its highest profit since establishment. Investors may consider this an indicator of a strengthened management foundation and consistent shareholder return policy.

2747|北雄ラッキー

3070.0

▲ +0.00%

📄 Announcement Facts

- Hokuyu Lucky announced its non-consolidated financial results for the fiscal year ended February 2026 (March 1, 2025 to February 28, 2026). Net sales were ¥37,199 million (up 0.8% year-on-year), operating profit was ¥229 million (down 5.6%), and ordinary profit was ¥222 million (up 8.4%).

- Net profit for the period was ¥108 million (down 23.9% year-on-year), influenced by the recording of extraordinary losses, including an impairment loss of ¥45 million and a loss on disposal of fixed assets of ¥7 million.

- In terms of financial position, total assets at the end of the period were ¥17,385 million (down ¥790 million from the previous fiscal year-end), while net assets increased by ¥200 million to ¥5,916 million, improving the equity ratio to 34.0% (from 31.4% previously).

- Cash flows showed a significant increase in cash flow from operating activities to ¥1,439 million (from ¥231 million in the prior period), while cash flow from investing activities resulted in an outflow of ¥775 million.

- For the fiscal year ending February 2027, the company forecasts full-year net sales of ¥37,600 million (up 1.1% year-on-year), operating profit of ¥360 million (up 56.8%), ordinary profit of ¥320 million (up 43.9%), and net profit of ¥190 million (up 75.4%). The annual dividend per share is projected to remain at ¥50.00.

🤖 AI Perspective

For the fiscal year ended February 2026, Hokuyu Lucky experienced a slight increase in net sales but a decline in operating profit, with extraordinary losses further impacting net profit. However, it is noteworthy that the company improved its equity ratio and significantly increased operating cash flow. The substantial profit recovery projected for the fiscal year ending February 2027 suggests that ongoing initiatives such as cost reduction, operational efficiency improvements, and strengthened supply systems are expected to contribute significantly to profitability.

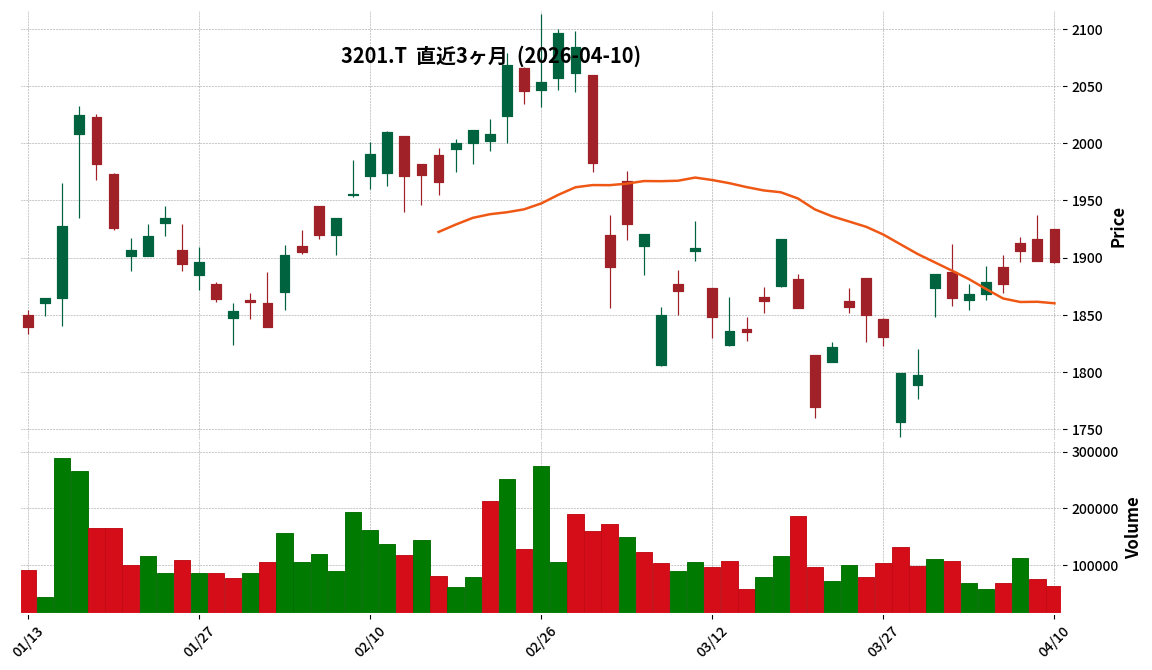

3201|ニッケ

1896.0

▼ -0.05%

📄 Announcement Facts

- For the first quarter of the fiscal year ending November 2026, Nikke reported consolidated net sales of ¥28,790 million (up 0.5% year-on-year), operating profit of ¥2,268 million (up 3.0%), ordinary profit of ¥2,620 million (up 6.8%), and net profit attributable to owners of parent of ¥2,116 million (up 28.6%).

- Diluted earnings per share for the quarter stood at ¥31.59.

- Two new companies, KAKOTECHNOS CO., LTD. and SUNTEC CO., LTD., were added to the scope of consolidation. KAKOTECHNOS contributed to the consolidated results in the Industrial Materials business.

- The Human & Future Development business recorded an operating profit of ¥1,856 million (up 17.3% year-on-year), driven by strong performance in the real estate leasing business.

- The consolidated full-year earnings forecast for the fiscal year ending November 2026 and the annual dividend forecast of ¥50.00 remained unchanged from the most recently announced figures.

🤖 AI Perspective

Nikke’s Q1 FY2026 results show a significant increase in net profit attributable to owners of parent, despite a modest rise in net sales. This notable profit growth appears to be primarily driven by the contribution of newly consolidated subsidiary KAKOTECHNOS and strong earnings from the real estate leasing business within the Human & Future Development segment. The unchanged full-year earnings and annual dividend forecasts suggest that the company is progressing in line with its initial plans.

4673|川崎地質

5580.0

▲ +2.20%

📄 Announcement Facts

- Kawasaki Geological Engineering Co., Ltd. announced on April 10, 2026, that its Board of Directors resolved to revise the dividend forecast for the fiscal year ending November 2026.

- The revised year-end dividend per share for the fiscal year ending November 2026 is JPY 95, an increase of JPY 40 from the previous forecast of JPY 55 (announced on January 14, 2026).

- Consequently, the total annual dividend per share for the fiscal year ending November 2026 is now projected to be JPY 120.00 (JPY 25 for Q2-end and JPY 95 for year-end), up from the previous forecast of JPY 80.00.

- The revision is attributed to a comprehensive consideration of the full-year performance outlook for the current fiscal year, following a previous revision of the earnings forecast disclosed on March 24, 2026.

- The actual total annual dividend for the previous fiscal year (ended November 2025) was JPY 145.00 per share.

🤖 AI Perspective

- A company revising its dividend forecast upwards, particularly following an earnings forecast revision, may suggest management’s confidence in its current fiscal year performance.

- This action could also underscore the company’s commitment to shareholder returns as a key management issue, potentially viewed as a positive indicator by investors.

- However, the revised annual dividend of JPY 120 is lower than the previous fiscal year’s actual dividend of JPY 145, a point that might warrant comprehensive consideration for investors.

7611|ハイデ日高

2958.0

▼ -1.73%

📄 Announcement Facts

- Hiday Hidaka Co., Ltd. announced its financial results for the fiscal year ended February 2026, reporting Net Sales of JPY 62,252 million (up 11.9% year-on-year), Operating Profit of JPY 6,584 million (up 19.4% year-on-year), Ordinary Profit of JPY 6,587 million (up 16.5% year-on-year), and Net Profit of JPY 4,731 million (up 15.6% year-on-year).

- The annual dividend for the fiscal year ended February 2026 was JPY 52 per share (JPY 23 interim, JPY 29 year-end), an increase from JPY 44 in the previous fiscal year.

- During the fiscal year, 21 new stores were opened and 4 stores were closed, resulting in 472 directly managed stores as of the end of February 2026. The company expanded its presence in the North Kanto area (Ibaraki, Tochigi, and Gunma prefectures) with a total of 8 new stores.

- For the fiscal year ending February 2027, the company forecasts Net Sales of JPY 67,000 million (up 7.6% year-on-year), Operating Profit of JPY 6,800 million (up 3.3% year-on-year), and Ordinary Profit of JPY 6,800 million (up 3.2% year-on-year). However, Net Profit is projected to be JPY 4,500 million (down 4.9% year-on-year).

- Cash and cash equivalents at the end of the period amounted to JPY 11,242 million, a decrease of JPY 2,235 million from the end of the previous fiscal year.

🤖 AI Perspective

The robust growth across all profit categories for FY2026 suggests that the company’s aggressive store expansion strategy has positively impacted its performance. However, the forecast for a decrease in net profit for FY2027, despite projected revenue and operating profit growth, may indicate increased costs associated with new store openings, renovations, or changes in accounting estimates, as mentioned in the report regarding impairment of fixed assets and depreciation methods. Investors may want to monitor the balance between growth investments and profitability in the upcoming fiscal year.

7811|中本パックス

1784.0

▼ -0.39%

📄 Announcement Facts

- Nakamoto Packs Co., Ltd. announced its consolidated financial results for the fiscal year ended February 2026, reporting net sales of 49,635 million yen (up 1.0% year-on-year), operating profit of 2,961 million yen (up 3.1%), ordinary profit of 3,054 million yen (up 5.0%), and profit attributable to owners of parent of 2,175 million yen (up 8.2%).

- The annual dividend for the fiscal year ended February 2026 totaled 71.00 yen per share, comprising an interim dividend of 34.00 yen and a year-end dividend of 37.00 yen, an increase from 66.00 yen in the previous fiscal year. The consolidated dividend payout ratio was 29.0%.

- Regarding the consolidated financial position, total assets stood at 40,523 million yen, and net assets were 22,093 million yen, with the equity ratio improving to 51.9% from 48.3% in the previous fiscal year.

- For the fiscal year ending February 2027, the company forecasts consolidated net sales of 52,000 million yen (up 4.8% year-on-year), operating profit of 3,265 million yen (up 10.3%), ordinary profit of 3,450 million yen (up 12.9%), and profit attributable to owners of parent of 2,183 million yen (up 0.3%).

- The forecasted annual dividend for the fiscal year ending February 2027 is 74.00 yen per share, consisting of an interim dividend of 37.00 yen and a year-end dividend of 37.00 yen. The consolidated dividend payout ratio is expected to be 30.0%.

🤖 AI Perspective

Nakamoto Packs achieved increased revenue and profits across all stages for the fiscal year ended February 2026, marking a second consecutive year of increased annual dividends. The company’s forecast for the fiscal year ending February 2027 also indicates continued growth in revenue and profits, alongside a planned further increase in annual dividends. These aspects may suggest a stable growth trajectory and a commitment to shareholder returns. The improvement in the equity ratio could indicate a strengthening of the company’s financial foundation.

137A|G-Cocolive

730.0

▲ +1.39%

📄 Announcement Facts

- For the third quarter cumulative period of the fiscal year ending May 2026 (June 1, 2025, to February 28, 2026), net sales reached ¥1,077 million, marking a 12.9% increase year-on-year.

- During the same period, operating profit was ¥166 million (a 20.1% decrease year-on-year), ordinary profit was ¥169 million (a 19.0% decrease year-on-year), and quarterly net profit was ¥115 million (a 20.2% decrease year-on-year).

- As of the end of the third quarter of the current fiscal year, total assets stood at ¥1,167 million, net assets at ¥1,039 million, and the equity ratio was 88.3%.

- The company has been promoting added value enhancement and new customer acquisition routes for “KASIKA,” a marketing automation tool specialized for the real estate industry.

- The full-year earnings forecast and annual dividend forecast (¥0.00 at term-end, ¥0.00 total) for the fiscal year ending May 2026 remain unchanged from the most recently announced figures.

🤖 AI Perspective

While the solid growth in net sales indicates business expansion, the simultaneous decline in profits may suggest that investments and increased costs associated with the growth strategy have had an impact. The high equity ratio is a point that could be seen as demonstrating the company’s stable financial foundation. The future impact of “KASIKA”‘s functional enhancements and market development on potential future profit improvements will be worth monitoring.

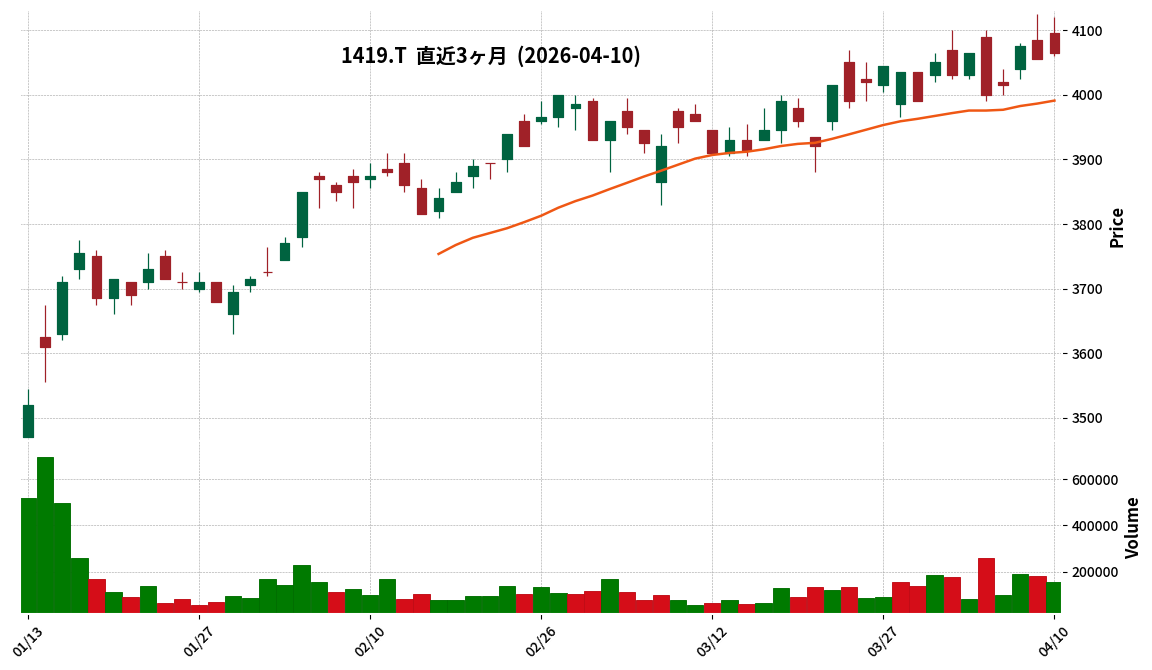

1419|タマホーム

4065.0

▲ +0.25%

📄 Announcement Facts

- For the third quarter ended February 28, 2026, Tamahome reported cumulative consolidated net sales of ¥120,824 million (down 2.5% year-on-year). The company recorded an operating loss of ¥3,375 million, an ordinary loss of ¥3,379 million, and a net loss attributable to owners of parent of ¥2,668 million, all representing a narrower deficit compared to the prior year.

- By business segment, the Housing segment reported net sales of ¥81,454 million (down 6.4% year-on-year) and an operating loss of ¥6,114 million. The Real Estate segment recorded net sales of ¥34,698 million (up 7.6% year-on-year) and an operating profit of ¥1,916 million (up 63.4% year-on-year).

- The forecast for the annual dividend for the fiscal year ending May 2026 has been revised to ¥125.00 per share.

- The full-year consolidated earnings forecast for the fiscal year ending May 2026 remains unchanged from the most recently announced forecast, projecting net sales of ¥209,000 million (up 4.1% year-on-year), operating profit of ¥4,700 million (up 14.3%), ordinary profit of ¥4,300 million (up 13.5%), and net profit attributable to owners of parent of ¥1,350 million (down 8.7%).

- The consolidated equity ratio as of the end of the third quarter of the fiscal year ending May 2026 was 26.5% (compared to 37.1% at the end of May 2025).

🤖 AI Perspective

While the company continued to report a consolidated loss, the narrowing of the deficit across operating, ordinary, and net loss metrics compared to the previous year is a key point. The Real Estate segment demonstrated notable growth in both sales and operating profit, which may indicate a difference in profitability contributions across segments. With the full-year earnings forecast remaining unchanged, the final results for the fiscal year will be worth monitoring.

2157|コシダカHD

1104.0

▲ +0.36%

📄 Announcement Facts

- For the second quarter of the fiscal year ending August 2026 (September 1, 2025, to February 28, 2026), consolidated net sales reached ¥38.932 billion (up 14.5% year-on-year), and net profit attributable to owners of parent was ¥3.884 billion (up 21.7% year-on-year).

- Operating profit was ¥5.004 billion (down 2.1% year-on-year), and ordinary profit was ¥5.224 billion (down 1.4% year-on-year).

- In the Karaoke segment, 20 new domestic stores were opened, and 70 karaoke stores were added through an absorption-type split from a consolidated subsidiary (currently K.K. Standard), resulting in 787 domestic stores, an increase of 84 from the end of the previous fiscal year. Overseas stores increased by 4 to 29.

- The company recorded an extraordinary gain from the sale of “Atsugi Vista Hotel” in the Real Estate Management segment. In the Other segment, two hot spring facilities were closed, marking the termination of the hot spring business.

- The company announced a revision to its consolidated full-year earnings forecast for the fiscal year ending August 2026 from the previously announced figures. The interim dividend forecast is ¥13.00 per share.

🤖 AI Perspective

KOSHIDAKA HOLDINGS’ Q2 FY2026 results reveal a significant increase in net sales alongside a decline in operating and ordinary profits, while net profit attributable to owners of parent saw a substantial rise, notably due to extraordinary gains. This could indicate that while the aggressive expansion of the karaoke business, including new store openings and M&A, has driven revenue growth, increased expenses from new investments and existing store operations have impacted core profitability. The revision to the full-year earnings forecast suggests a recalibration of management’s expectations for future performance, reflecting these operational dynamics and strategic adjustments, such as the divestiture of the hot spring business.

2164|地域新聞社

312.0

▼ -4.88%

📄 Announcement Facts

- Chiiki Newspaper Co., Ltd. (2164) reported net sales of JPY 1,635 million for the second quarter of the fiscal year ending August 2026, marking a 7.2% increase compared to the previous year.

- However, operating income decreased by 80.6% to JPY 2 million, while ordinary income was a loss of JPY △3 million, and net loss attributable to owners of parent was JPY △67 million, resulting in a loss per share of JPY △8.97.

- The company announced on December 15, 2025, the patenting and global expansion (PCT application) of its “Intervention Effect Maximization Technology using Generative AI-powered Psychological Digital Twins.”

- On February 6, 2026, an executive officer appointment was announced, signaling the company’s progress in establishing a system for the full-scale launch of career support businesses, including a “scholarship repayment support type” recruitment service.

- For the full fiscal year ending August 2026, the company has set a management target (not an earnings forecast) of JPY 3,500 million in net sales, an 11.0% increase year-on-year.

🤖 AI Perspective

While sales have grown, the decline into operational losses could suggest the impact of upfront investments made in alignment with the “Strategic Plan” growth strategy. The concrete steps, such as securing a patent for generative AI technology and preparing for new career support ventures, may indicate a potential shift in the company’s future business model. The stated need for funding to support these growth investments is a point worth monitoring for investors.

2735|ワッツ

623.0

▼ -0.48%

📄 Announcement Facts

- Watts Co., Ltd. announced its consolidated financial results for the second quarter (interim period) of the fiscal year ending August 2026.

- For the interim period, consolidated net sales were JPY 31,275 million (up 2.7% year-on-year), operating profit was JPY 857 million (up 4.6%), and ordinary profit was JPY 895 million (up 3.4%).

- Net income attributable to owners of parent decreased to JPY 495 million (down 7.7% year-on-year).

- The domestic 100-yen shop business achieved a 102.1% year-on-year increase in existing store sales, enhancing its product lineup with higher-priced items, lifestyle brand “Tokino:ne,” original cosmetics “fasmy,” and other specialized products.

- In the overseas business, the company shifted its strategy to scale down directly managed stores and focus on expanding wholesale operations, currently supplying products to over 30 countries.

- The consolidated earnings forecast and annual dividend forecast (year-end dividend of JPY 12.50, total JPY 20.00) for the fiscal year ending August 2026 remain unchanged from the most recently published figures.

🤖 AI Perspective

While achieving increased sales and profits, the decline in net income attributable to owners of parent may suggest an impact from increased selling, general and administrative expenses, such as store renovation costs and promotional activities for brand awareness. The robust performance in existing store sales for the domestic 100-yen shop business could indicate the effectiveness of product mix improvements, as well as enhanced convenience and labor savings from the introduction of self-checkout systems. The strategic pivot in the overseas business might be a response to evolving market conditions, aiming to explore more efficient revenue models.

2742|ハローズ

4395.0

▼ -1.68%

📄 Announcement Facts

- Harows announced a decision to increase its dividend distribution from surplus.

- This decision is based on the company’s policy of positioning stable returns to shareholders as a key management priority.

- The information was disclosed to the market by Harows, a company listed on the Tokyo Stock Exchange, in accordance with its disclosure obligations.

🤖 AI Perspective

An announcement of a dividend increase may suggest the company’s confidence in its financial health and positive outlook for future performance. Strengthening shareholder returns could lead to a positive evaluation from investors with a long-term perspective.

2791|大黒天

4965.0

▼ -0.50%

📄 Announcement Facts

- Daikokuten reported consolidated net sales of 236,206 million yen for the nine months ended February 28, 2026 (Q3 FY2026), marking a 9.8% increase year-on-year.

- For the same period, operating profit decreased by 41.2% to 4,261 million yen, ordinary profit fell by 42.0% to 4,369 million yen, and net profit attributable to owners of parent declined by 43.6% to 2,700 million yen.

- As of the end of Q3 FY2026, total assets stood at 129,430 million yen, net assets at 60,347 million yen, and the equity ratio was 46.5%.

- The full-year consolidated earnings forecast for FY2026 remains unchanged, projecting net sales of 319,900 million yen (up 9.2% year-on-year), operating profit of 6,700 million yen (down 31.7%), ordinary profit of 6,900 million yen (down 31.6%), and net profit attributable to owners of parent of 4,400 million yen (down 35.1%).

- During the nine-month period, the company opened 18 new stores, with 6 of them adopting the 100% Center-Supplied Store (SFO) format.

🤖 AI Perspective

- While sales increased, the substantial decline in profits suggests an impact from rising logistics costs, personnel expenses, and increased construction costs and selling, general and administrative expenses associated with new store openings.

- The unchanged full-year earnings forecast could indicate that the company has already factored in these cost increases and anticipates a recovery or stabilization for the remainder of the fiscal year.

- The strategy of new store expansion, particularly with the SFO store format aimed at cost reduction, may be a key area for investors to monitor regarding future profitability.

2999|ホームポジション

500.0

▼ -0.20%

📄 Announcement Facts

- For the second quarter of fiscal year 2026 (interim period), Home Position reported net sales of ¥9,051 million, representing a 25.9% increase year-over-year.

- Operating income for the same period was ¥478 million (up 128.8% YoY), ordinary income was ¥369 million (up 288.3% YoY), and interim net income was ¥264 million (compared to ¥15 million profit in the prior year’s interim period).

- As of the end of the interim period, total assets stood at ¥15,467 million, net assets at ¥5,951 million, and the equity ratio was 38.5%.

- The full-year fiscal 2026 earnings forecast and dividend forecast (¥10.00 per share annually) remain unchanged from the previously announced figures.

- The company stated that sales volume exceeded the prior year’s period due to efforts in strengthening land procurement, streamlining sales activities, and improving construction management systems.

🤖 AI Perspective

- The interim results demonstrate significant year-over-year growth in both net sales and all profit metrics, which may suggest effective operational improvements and strong market response.

- However, the decision to keep the full-year earnings forecast unchanged could indicate the company’s cautious outlook on future market conditions or business developments.

- The slight decrease in the equity ratio and an increase in liabilities appear to be primarily driven by an increase in real estate for sale in progress and related short-term and long-term borrowings.

3063|G-jGroup

813.0

▼ -0.49%

📄 Announcement Facts

- For the fiscal year ended February 28, 2026, consolidated net sales increased by 21.4% to JPY 13,045 million, operating income rose by 11.5% to JPY 420 million, and ordinary income increased by 0.3% to JPY 353 million.

- Net profit attributable to owners of parent decreased by 31.9% to JPY 312 million.

- The consolidated earnings forecast for the fiscal year ending February 28, 2027, projects net sales of JPY 13,300 million (up 1.9% year-on-year), operating income of JPY 450 million (up 7.0%), ordinary income of JPY 370 million (up 4.7%), and net profit attributable to owners of parent of JPY 320 million (up 2.5%).

- During the fiscal year, Mountain Coffee Co., Ltd. was made a consolidated subsidiary, adding 5 directly managed stores and 4 FC stores.

- The real estate business reported sales of JPY 1,586 million (up 225.1% year-on-year) and operating income of JPY 678 million (up 526.5%), driven by the sale of two real estate properties.

🤖 AI Perspective

While net sales and operating income increased, the decline in net profit attributable to owners of parent for the current period may suggest a rebalancing after specific factors, such as real estate sales gains, impacted the previous period. The growth in the dining business, supported by existing store renovations and new subsidiary integration, along with significant contributions from the real estate segment, appear to have been key drivers for the overall revenue increase. The company’s forecast for continued sales and profit growth in the next fiscal year indicates ongoing efforts in business succession and revenue improvement, which will be worth monitoring.

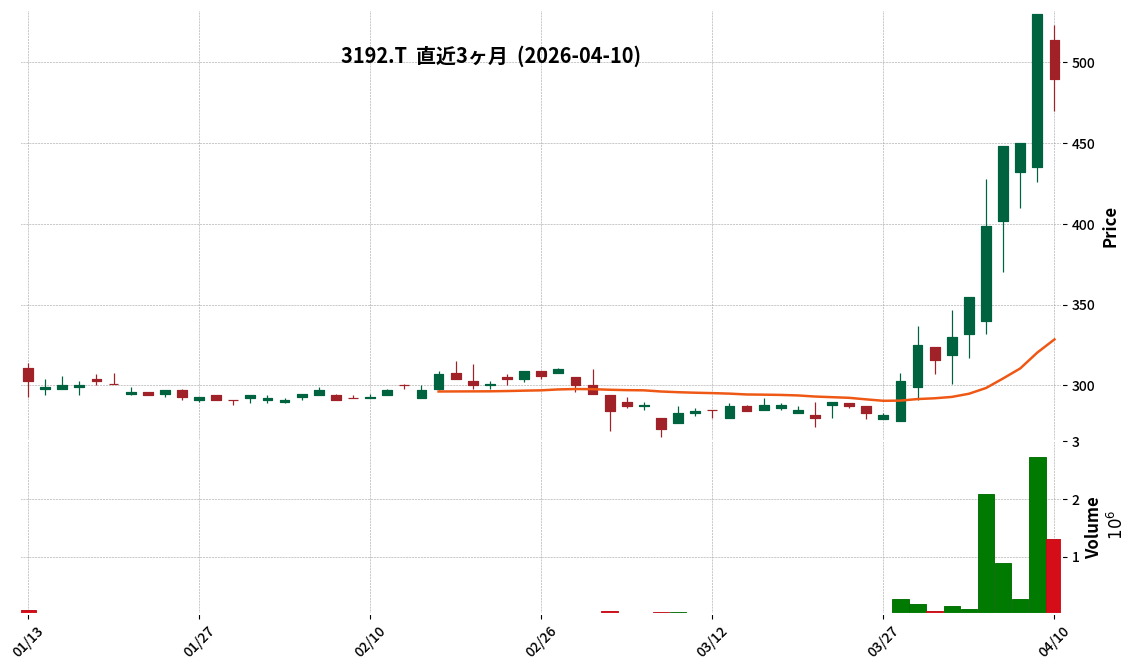

3192|白鳩

490.0

▼ -7.55%

📄 Announcement Facts

- Shirohato Co., Ltd. has announced its financial results for the first quarter of the fiscal year ending November 2026 (December 1, 2025, to February 28, 2026).

- For the quarter, net sales amounted to ¥1,743 million. The company reported an operating loss of ¥22 million, an ordinary loss of ¥28 million, and a net loss of ¥29 million.

- Diluted earnings per share for the quarter stood at △¥4.39.

- As of the end of the quarter, total assets were ¥5,209 million, net assets were ¥2,491 million, and the equity ratio was 47.8%.

- The full-year earnings forecast for FY2026 (net sales ¥6,750 million, operating profit ¥50 million, ordinary profit ¥20 million, and net profit ¥14 million) remains unchanged from the most recently announced figures.

- Due to a change in the fiscal year-end, year-on-year percentage changes for the first quarter are not provided as the comparison periods differ.

🤖 AI Perspective

- Shirohato’s Q1 FY2026 results show net sales of ¥1,743 million, but the company recorded losses at the operating, ordinary, and net income levels.

- As direct year-on-year comparisons are not available due to the fiscal year-end change, investors may focus on the absolute sales and loss figures in relation to the unchanged full-year earnings forecast to assess progress.

- In terms of financial position, total assets and liabilities decreased while the equity ratio improved, which could indicate shifts in the company’s balance sheet structure.

3280|エストラスト

1085.0

▼ -4.32%

📄 Announcement Facts

- Estrust Co., Ltd. reported consolidated results for the fiscal year ended February 2026, achieving net sales of ¥22,313 million (up 16.1% year-on-year), operating income of ¥2,095 million (up 4.8%), ordinary income of ¥1,962 million (up 1.6%), and profit attributable to owners of parent of ¥1,420 million (up 6.0%).

- The annual dividend for the fiscal year ended February 2026 was set at ¥16.00 per share for the fiscal year-end, totaling ¥30.00 per share (up ¥4.00 from the previous fiscal year) including the interim dividend.

- For the fiscal year ending February 2027, the company forecasts consolidated net sales of ¥21,000 million (down 5.9% year-on-year), operating income of ¥1,600 million (down 23.6%), ordinary income of ¥1,400 million (down 28.7%), and profit attributable to owners of parent of ¥1,000 million (down 29.6%).

- The consolidated financial position at the end of February 2026 showed a capital adequacy ratio of 28.7%, an improvement from 21.7% at the end of the previous fiscal year.

- In the real estate development business, 404 condominium units and 68 detached houses were delivered, leading to an increase in net sales (up 9.0% year-on-year) due to the progress in passing on rising construction costs.

🤖 AI Perspective

Estrust’s financial results for the fiscal year ended February 2026 showed an increase in revenue and profits, which appears to be attributed to the progress in passing on price increases in its real estate development business and an increase in managed properties. The increase in the annual dividend also suggests a commitment to shareholder returns. However, the forecast for the fiscal year ending February 2027 anticipates a decline in both revenue and profits, with the company noting that performance can be significantly affected by property handover timings, which warrants monitoring. Furthermore, the improvement in the capital adequacy ratio indicates an enhanced financial stability.

3501|SUMINOE

1342.0

▼ -4.42%

📄 Announcement Facts

- SUMINOE announced its financial results for the third quarter of the fiscal year ending May 2026 (June 1, 2025, to February 28, 2026).

- Net sales increased by 3.1% year-on-year to ¥79,091 million, but operating profit decreased by 11.8% to ¥1,315 million.

- Ordinary profit significantly increased by 48.4% year-on-year to ¥1,623 million, mainly due to a swing from foreign exchange loss to gain.

- Net income attributable to owners of parent resulted in a loss of ¥30 million (compared to a profit of ¥85 million in the prior year period), partly due to the absence of gains on sales of investment securities recorded in the previous year’s extraordinary income and increased income taxes.

- Revisions to the full-year consolidated earnings forecast and annual dividend forecast have been announced, with details to be referenced in the separate disclosure titled “Announcement Regarding Revision of Consolidated Earnings Forecast and Dividend Forecast for the Fiscal Year Ending May 2026.”

- By segment, the Interior Business segment’s profit significantly increased by 143.3% year-on-year to ¥658 million.

🤖 AI Perspective

While consolidated net sales grew, factors such as reduced production efficiency due to changes in automotive manufacturers’ production plans appear to have impacted operating profit. Conversely, a favorable shift in foreign exchange to gains substantially improved ordinary profit; however, the absence of prior year’s extraordinary income and increased taxes contributed to the net loss attributable to owners of parent. The revision of the full-year earnings and dividend forecasts suggests that these factors may continue to influence future business strategies, which is worth monitoring.

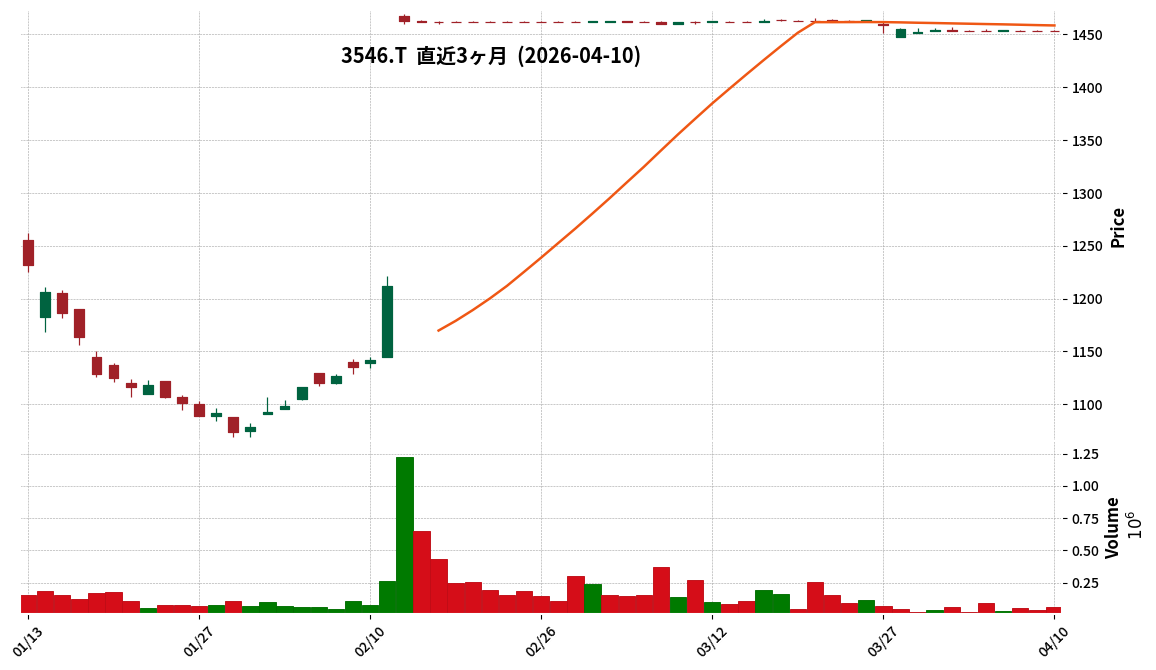

3546|アレンザHD

1453.0

▲ +0.00%

📄 Announcement Facts

- Alleanza Holdings Co., Ltd. released its supplemental financial results for the fiscal year ended February 2026 on April 10, 2026.

- For the full fiscal year 2026, consolidated net sales were ¥150,601 million, representing a 1.8% decrease compared to the previous fiscal year.

- Consolidated operating profit amounted to ¥4,098 million, an increase of 16.8% year-on-year, while net profit attributable to parent company shareholders was ¥2,544 million, up 21.8% from the prior year.

- The gross profit margin improved by 1.9 percentage points to 36.2% for the period.

- Due to the public tender offer by Kohnan Shoji Co., Ltd., the year-end dividend for FY2026/2 will not be paid, and the consolidated earnings forecast for FY2027/2 has not been provided, as the company’s shares are expected to be delisted.

🤖 AI Perspective

The FY2026/2 results show a noteworthy trend where operating and net profits increased despite a decline in net sales, suggesting an improvement in profitability, particularly driven by a higher gross profit margin. While the car accessories segment experienced a significant profit increase, the pet and other segments saw a decrease in profits. Given the ongoing tender offer by Kohnan Shoji and the anticipated delisting of Alleanza Holdings’ shares, investors may be closely monitoring the developments related to the acquisition and its future implications for the company’s business strategy and structure.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

3560|ほぼ日

3570.0

▼ -2.19%

📄 Announcement Facts

- Hobonichi Co., Ltd. announced its non-consolidated financial results for the second quarter of the fiscal year ending August 2026 (interim period: September 1, 2025, to February 28, 2026).

- For the interim period, net sales reached JPY 7,065 million (up 23.0% year-on-year), operating profit was JPY 1,733 million (up 69.6%), ordinary profit was JPY 1,748 million (up 65.2%), and interim net profit was JPY 1,210 million (up 65.4%).

- Sales of the flagship product, “Hobonichi Techo,” significantly grew both domestically and internationally, with domestic sales at JPY 2,271 million (up 24.2% YoY) and overseas sales at JPY 3,273 million (up 38.4% YoY). Total domestic and overseas sales amounted to JPY 5,544 million (up 32.2% YoY), with the ratio of overseas sales increasing to 59.0%.

- The 2026 edition of “Hobonichi Techo” surpassed 1 million units in sales, exceeding the record set by the 2025 edition. The “Hobonichi Techo App” service was also launched on October 15, 2025.

- The full-year forecast for FY2026 remains unchanged from the most recently announced figures: net sales of JPY 9,500 million, operating profit of JPY 680 million, ordinary profit of JPY 680 million, net profit of JPY 480 million, and basic earnings per share of JPY 206.79.

🤖 AI Perspective

The significant increase in profits for Hobonichi appears to be driven by robust domestic and international sales of its core product, “Hobonichi Techo,” alongside an improvement in cost of sales ratios. The rising proportion of overseas sales may suggest successful global market penetration and brand expansion. However, the full-year forecast remains conservative relative to the strong interim performance, which might lead investors to monitor the company’s outlook for the second half and future market conditions closely.

3612|ワールド

1614.0

▼ -0.68%

📄 Announcement Facts

- World Co., Ltd. announced on April 10, 2026, a partial correction to its “Consolidated Financial Results for the Fiscal Year Ended February 2026 (IFRS)” which was disclosed on April 3, 2026.

- The reason for the correction was an input error during data updates in the preparation process of the disclosure material, along with insufficient prior verification.

- The correction pertains to the “Summary Information 2. Dividend Status” for the fiscal year ended February 2026.

- Specifically, the total amount of dividends for the fiscal year ended February 2026 was revised from ¥3,746 million (before correction) to ¥3,855 million (after correction).

- The consolidated payout ratio was changed from 30.9% to 31.8%, and the payout ratio attributable to owners of the parent was revised from 4.3% to 4.4%. The total annual dividend of ¥109.00 per share remains unchanged.

🤖 AI Perspective

This correction involves key financial indicators such as total dividends and the payout ratio, which are closely watched by investors. Such revisions to reported figures can impact investor confidence in the accuracy of corporate disclosures, suggesting that strengthened information management systems might be a point of focus. Investors may use these revised figures to re-evaluate the company’s financial health and dividend policy.

3815|G-メディア

453.0

▼ -0.44%

📄 Announcement Facts

- For the second quarter of the fiscal year ending August 2026, consolidated net sales were ¥828 million, representing a 13.5% decrease compared to the same period in the prior fiscal year.

- The net loss attributable to owners of the parent for the interim period expanded to ¥268 million, compared to a loss of ¥69 million in the corresponding period of the previous fiscal year.

- The Fortune-telling Business segment reported sales of ¥769 million (down 14.6% year-on-year) and an operating profit of ¥118 million (down 39.2% year-on-year).

- The Data & Technology Business segment recorded sales of ¥53 million (up 12.0% year-on-year), while its operating loss expanded to ¥115 million from a loss of ¥31 million in the previous interim period.

- The full-year consolidated earnings forecast for the fiscal year ending August 2026 remains unchanged, projecting net sales of ¥2,163 million and a net loss attributable to owners of the parent of ¥302 million.

🤖 AI Perspective

The decline in sales and operating profit from the core Fortune-telling Business appears to have significantly impacted the overall financial results for this interim period. Conversely, the Data & Technology Business demonstrated revenue growth, with some services achieving profitability, potentially indicating a strategic focus on emerging growth areas. However, the company’s expanded net loss could be attributed to increased upfront investments for business reinforcement, as well as one-time expenses such as office relocation costs and the introduction of interim shareholder benefits.

4076|G-シイエヌエス

1769.0

▲ +2.79%

📄 Announcement Facts

- G-CNS announced an upward revision to its consolidated full-year earnings forecast for the fiscal year ending May 2026.

- The revised consolidated earnings forecast includes an operating profit of ¥710 million (up 7.9% from the previous forecast), ordinary profit of ¥734 million (up 8.7%), and profit attributable to owners of parent of ¥532 million (up 10.1%). Net sales remain unchanged at ¥8,253 million.

- The reasons for the earnings forecast revision are cited as improved profitability due to an increase in high-margin projects, particularly in the technology solutions business, and some selling, general, and administrative expenses not reaching planned levels.

- The company also revised its year-end dividend forecast for the fiscal year ending May 2026, increasing it by ¥5 from the previously announced ¥50.00 per share to ¥55.00 per share.

- This dividend revision is based on the company’s progressive dividend policy, which targets a payout ratio of 30% or more, and reflects the current business performance.

🤖 AI Perspective

- The upward revision of the earnings forecast, despite stable net sales, may suggest an enhancement in operational efficiency or a successful shift towards higher-margin projects within the company’s business segments.

- The increase in the dividend forecast aligns with the company’s progressive dividend policy, indicating a commitment to returning profits to shareholders in response to stronger financial performance.

- These announcements could be viewed by investors as positive signals regarding the company’s profitability trends and its approach to shareholder value.

4187|大有機化

3960.0

▲ +3.66%

📄 Announcement Facts

- Osaka Organic Chemical Industry Co., Ltd. announced its consolidated financial results for the first quarter of fiscal year 2026 (December 1, 2025 to February 28, 2026).

- Consolidated performance showed net sales of ¥9,072 million (up 6.5% year-on-year), operating profit of ¥1,832 million (up 34.2% year-on-year), ordinary profit of ¥1,904 million (up 28.6% year-on-year), and net profit attributable to owners of parent of ¥1,285 million (up 24.2% year-on-year).

- By segment, the Electronic Materials business recorded net sales of ¥4,552 million (up 22.2% year-on-year) and segment profit of ¥983 million (up 85.6% year-on-year), driven by a significant increase in sales of cutting-edge EUV resist materials.

- Consolidated financial position indicated total assets of ¥65,452 million, net assets of ¥52,916 million, and a capital adequacy ratio of 79.4%.

- The consolidated earnings forecast for the fiscal year ending November 2026 and the annual dividend forecast of ¥80.00 remain unchanged from previously announced figures.

- Visnex Chemicals Corporation was newly included in the scope of consolidation during this quarter. The company also plans new capital investment for advanced semiconductor materials at its Sakata Plant, with completion scheduled for 2028.

🤖 AI Perspective

The first quarter results indicate robust growth across key profitability metrics, primarily driven by strong performance in the Electronic Materials segment. The reported significant increase in sales of cutting-edge EUV resist materials suggests a positive response to demand in the advanced semiconductor market. The unchanged full-year earnings and dividend forecasts may imply that the company considers its current performance to be in line with its internal plans, while the planned capital investment at the Sakata Plant could signal a long-term strategy to bolster future production capacity and market presence.

4361|川口化

1521.0

▲ +0.33%

📄 Announcement Facts

- Kawaguchi Chemical Industry Co., Ltd. announced its consolidated financial results for the first quarter of the fiscal year ending November 2026 (December 1, 2025, to February 28, 2026) on April 10, 2026.

- Consolidated sales revenue for the quarter was JPY 1,935 million (down 2.7% year-on-year). Operating profit reached JPY 95 million (up 16.0%), ordinary profit JPY 87 million (up 14.5%), and net profit attributable to owners of parent JPY 67 million (up 19.0%).

- By segment, the Chemical Industrial Products business reported sales of JPY 1,926 million (down 2.8%) and segment profit of JPY 87 million (up 17.6%). The resin chemicals division specifically saw sales increase by 19.0% to JPY 235 million.

- The company revised its full-year consolidated earnings forecast for the fiscal year ending November 2026, stating that it is difficult to provide numerical figures at this point due to many uncertain factors affecting performance. The forecast will be disclosed when it becomes reasonably predictable.

- The annual dividend forecast for FY2026 remains unchanged from the most recently announced forecast, with an annual total of JPY 60.00 (year-end JPY 60.00).

🤖 AI Perspective

While sales decreased in the first quarter, the company managed to secure profit growth across operating, ordinary, and net profit levels, with the strong performance of the resin chemicals division likely contributing to this. However, the decision to withhold a numerical full-year earnings forecast due to uncertain factors could indicate a cautious outlook on future business conditions and may be a point of interest for investors. The market will likely be observing for updates on the full-year forecast and further business developments.

4370|G-モビルス

338.0

▼ -3.98%

📄 Announcement Facts

- For the second quarter of the fiscal year ending August 2026, Mobilus Co., Ltd. reported consolidated net sales of JPY 1,008 million.

- The company recorded an operating loss of JPY 73 million, an ordinary loss of JPY 83 million, and a net loss attributable to owners of the parent of JPY 37 million for the interim period.

- SaaS service revenue increased by 16.4% year-over-year to JPY 756,355 thousand, and Professional Service revenue increased by 24.8% year-over-year to JPY 251,918 thousand.

- As of February 29, 2026, the number of SaaS product contracts stood at 318, with an average contract value of JPY 311 thousand.

- The full-year consolidated earnings forecast for the fiscal year ending August 2026 remains unchanged, projecting net sales of JPY 2,298 million, an operating loss of JPY 110 million, an ordinary loss of JPY 120 million, and a net loss attributable to owners of the parent of JPY 45 million.

🤖 AI Perspective

While the consolidated results show a loss, the double-digit growth in both SaaS and Professional Services, which are the company’s core businesses, could be a key point for investors. The increase in average contract value, despite a slight rise in contract numbers, may suggest strengthened revenue generation from existing clients or the acquisition of larger new projects. With the full-year forecast maintained, the progress of profitability improvements in the latter half of the fiscal year will be worth monitoring.

4430|東海ソフト

1824.0

▼ -0.38%

📄 Announcement Facts

- Consolidated net sales for the third quarter cumulative period amounted to JPY 9,203 million, marking a 20.3% increase year-on-year.

- Operating profit was JPY 1,137 million (+18.3% YoY), ordinary profit JPY 1,164 million (+21.7% YoY), and net profit attributable to owners of parent JPY 713 million (+12.6% YoY).

- Earnings per share for the quarter were JPY 148.93.

- The equity ratio stood at 62.0% as of the end of the third quarter of FY2026.

- The full-year consolidated earnings forecast and dividend forecast have been revised, with the annual dividend projection increasing from JPY 55.00 in the previous fiscal year to JPY 60.00.

🤖 AI Perspective

The significant growth in sales and profits during this cumulative period appears to be supported by the company’s strategic initiatives, such as focusing on SDV and electrification in the embedded systems business, enhancing DX support solutions in manufacturing/distribution/business systems, and promoting digitalization in the financial/public sector. The upward revision of the full-year earnings and dividend forecasts could suggest management’s confidence in sustained performance, while the strong equity ratio may indicate a robust financial position.

4443|Sansan

1239.0

▼ -2.82%

📄 Announcement Facts

- For the nine months ended February 29, 2026 (Q3 FY2026), Sansan reported revenue of 39,265 million JPY (up 26.1% year-on-year) and adjusted operating profit of 6,087 million JPY (up 131.1% year-on-year).

- Annual Recurring Revenue (ARR) reached 48,013 million JPY, marking a 21.8% increase compared to the previous year.

- Revenue from the accounting AX service “Bill One” grew by 40.7% year-on-year to 9,876 million JPY, with its Monthly Recurring Revenue (MRR) net increase expanding for the fourth consecutive quarter.

- The full-year FY2026 earnings forecast has been revised upwards, projecting revenue growth of 24.0% to 25.0% year-on-year and adjusted operating profit growth of 126.0% to 143.0% year-on-year.

- For the medium-term financial plan, the adjusted operating profit margin for the full-year FY2027 is now targeted at 20% to 23%.

🤖 AI Perspective

Sansan’s strong third-quarter results, marked by significant growth in both revenue and adjusted operating profit, suggest effective business execution, particularly within the Bill One segment. The upward revision of the full-year earnings forecast and the ambitious adjusted operating profit margin target for FY2027 may indicate management’s confidence in sustained growth and improving profitability. Investors might consider these developments as indicators of the company’s potential to continue its expansion in the SaaS market.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

460A|G-BRANU

710.0

▼ -1.66%

📄 Announcement Facts

- BRANU Corporation (Code: 460A) disclosed its responses to questions from investors on April 10, 2026, following the announcement of its Q1 FY2026 financial results (released on March 17, 2026).

- Regarding Q1 performance, although inbound marketing investment expanded, a significant number of cases failed credit screening, preventing sales recognition. As a recovery plan, the company implemented changes to its negotiation flow to strengthen credit information pre-screening and refined SNS advertising, aiming for profit growth from Q2 onwards.

- The “Work Style Reform (2024 problem)” in the construction industry delayed new sales negotiations in Q1. However, BRANU believes demand for “CAREECON Plus” is rising, positioning the current period as the prime expansion phase for sales channels.

- The company’s revenue model consists of an initial “Media Package” (flow revenue: 2.2 million yen) and the mandatory “CAREECON Plus” mini plan (stock revenue: 12,000 yen/month), with upselling to higher-tier plans. This dual flow and stock revenue model emphasizes Customer Lifetime Value (LTV).

- BRANU announced its focus on three key areas for stock price measures: “execution for sustainable growth,” “consideration of shareholder returns,” and “fundamental improvement of IR (Investor Relations) system.” Additionally, the company analyzed that the impact of rising material and labor costs due to macroeconomic conditions on small and medium-sized construction companies is “gradual” and “posterior,” anticipating annual churn rates for the mini plan around 0.25% and Standard plan around 2.5% for the current fiscal year.

🤖 AI Perspective

- The company’s proactive disclosure of specific recovery plans for the challenges faced in Q1, particularly regarding inbound marketing effectiveness, may suggest a focused approach to improving future profitability.

- BRANU’s view of the “2024 problem” in the construction industry as an opportunity, leading to increased demand for its core services, could indicate a resilient business model in a changing market.

- The commitment to considering shareholder returns and enhancing IR communication might be seen as an effort to build investor confidence and reflect the company’s value more accurately.

4992|北興化

1812.0

▲ +0.95%

📄 Announcement Facts

- Hokko Chemical Industry Co., Ltd. announced its consolidated financial results for the first quarter of the fiscal year ending November 2026 (December 1, 2025, to February 28, 2026) on April 10, 2026.

- Consolidated net sales increased by 5.8% year-on-year to ¥16,243 million. Operating profit rose by 20.5% to ¥2,286 million, ordinary profit by 19.6% to ¥2,436 million, and net income attributable to parent company shareholders by 22.6% to ¥1,734 million.

- By segment, the Agrochemicals business reported net sales of ¥12,359 million (+11.3% YoY) and operating profit of ¥1,669 million (+57.5% YoY), driven by robust domestic sales of rice paddy and horticultural agrochemicals and increased overseas sales, particularly to India and Brazil.

- The Fine Chemicals business saw net sales decrease by 9.9% year-on-year to ¥3,402 million, with operating profit declining by 26.3% to ¥601 million. This was influenced by demand fluctuations and delayed timing in the pharmaceuticals and agrochemicals fields, as well as inventory adjustments in the electronic materials field.

- The consolidated earnings forecast for the full fiscal year ending November 2026 remains unchanged from the forecast announced on January 13, 2026.

🤖 AI Perspective

Hokko Chemical Industry’s strong first-quarter results for FY2026 appear to be largely driven by the robust performance of its Agrochemicals business. Conversely, the Fine Chemicals business experienced a decline in both revenue and profit, which may indicate specific market challenges or demand shifts in certain areas. Given that the full-year forecast remains unchanged, investors might be monitoring the performance of each segment in the upcoming quarters to assess the overall trajectory towards the annual targets.

5271|トーヨーアサノ

2370.0

▲ +1.28%

📄 Announcement Facts

- Toyo Asano Co., Ltd. reported consolidated results for the fiscal year ended February 2026, with net sales of ¥11,690 million (down 18.8% year-on-year), operating profit of ¥102 million (down 83.1% year-on-year), and ordinary profit of ¥28 million (down 95.2% year-on-year).

- The company recorded a net loss attributable to owners of parent of ¥221 million for FY2026/2, a significant change from the ¥363 million net profit in the previous year.

- The annual dividend per share for FY2026/2 was maintained at ¥85.00 (interim ¥40.00, year-end ¥45.00), consistent with the prior year. The company also plans to pay an annual dividend of ¥85.00 for FY2027/2 (forecast).

- For the consolidated earnings forecast for FY2027/2 (full year), Toyo Asano anticipates net sales of ¥13,500 million (up 15.5% year-on-year), operating profit of ¥550 million (up 436.7% year-on-year), and a return to net profit of ¥280 million attributable to owners of parent.

- The core foundation business experienced a decline in sales to ¥11,492 million (down 19.1% year-on-year) and operating profit to ¥632 million (down 43.1% year-on-year), attributed to sluggish demand in key markets and delays in construction project commencements.

🤖 AI Perspective

- The sharp decline in performance for FY2026/2 appears to be a result of reduced sales in its core business due to weakened demand and construction delays, compounded by increased fixed cost burdens from lower operating rates, leading to a net loss.

- However, the company’s FY2027/2 earnings forecast projects a substantial recovery in sales and profits, with an anticipated return to profitability, which may suggest expectations of improved market conditions or the effectiveness of ongoing strategic reforms.

- Despite reporting a net loss in the current fiscal year, the decision to maintain the annual dividend at the same level for both the current and the upcoming fiscal year could indicate a continued commitment to shareholder returns.

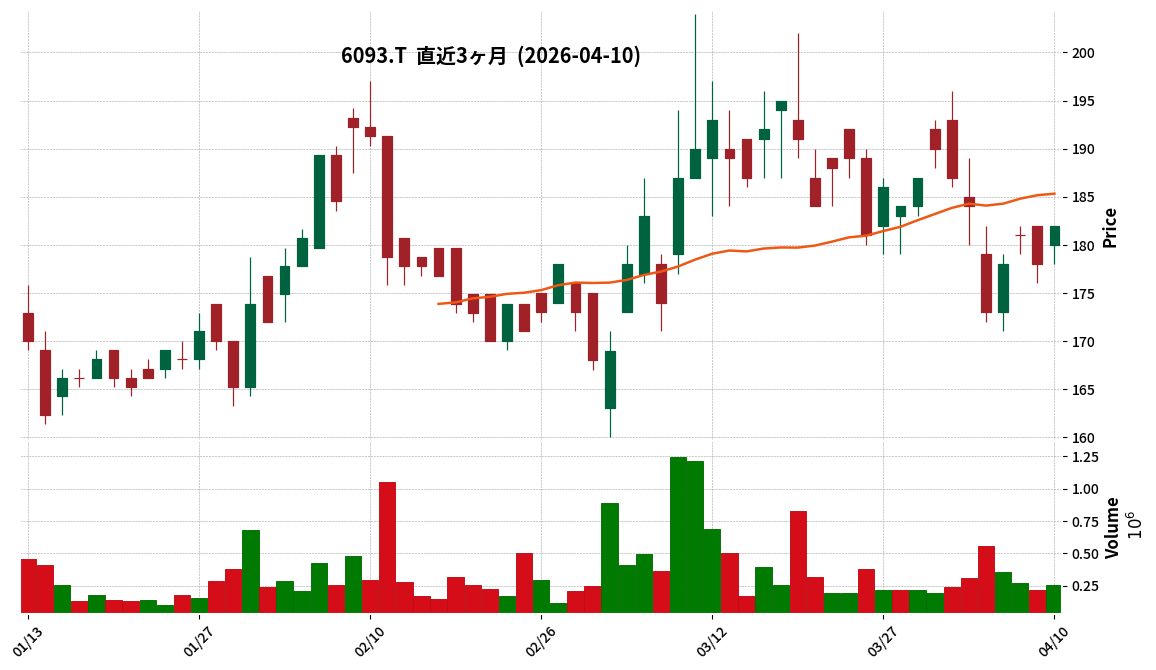

6093|エスクローAJ

182.0

▲ +2.25%

📄 Announcement Facts

- Escrow AJ’s full-year performance for the fiscal year ended February 2026 fell below plans due to a 100 million yen provision for doubtful accounts in the Financial Solutions business and delays in contract/settlement timings for real estate auctions, primarily large-scale properties. Net sales were △6.6% below forecast, and operating profit was △32.3% below forecast.

- Among the factors for missing targets, the 100 million yen provision for doubtful accounts is recognized as a one-time factor, and the delay in real estate auctions is a timing shift, not a loss of projects, with recovery anticipated from the fiscal year ending February 2027 onwards.

- For the fiscal year ending February 2027, the company forecasts net sales of 6,211 million yen (+22.3% year-on-year) and operating profit of 624 million yen. This is based on the recovery and new accumulation of real estate auction projects, continued high growth in the Construction Solutions business, and the elimination of the aforementioned profit-reducing factors.

- As part of shareholder returns, the company plans to initiate an interim dividend from the fiscal year ending February 2027, with 3 yen per share for interim and 3 yen for year-end, totaling 6 yen annually.

- The Professional Solutions business is projected to see a decrease in revenue and profit in FY2027/2 due to a reactionary decline from one-time sales of information processing equipment (which saw a significant increase in FY2026/2) not recurring in FY2027/2, and ongoing upfront investments in service development like “AI Mitsuro-kun for Inheritance.” The company aims for recovery and expansion in FY2028/2.

🤖 AI Perspective

The financial results for the fiscal year ended February 2026 highlight a shortfall primarily attributed to temporary factors, while the company expresses strong confidence in business recovery and growth for the fiscal year ending February 2027. The resolution of delayed real estate auction projects, the absence of the loan loss provision, and the robust performance of the Construction Solutions business may serve as key drivers for future profit improvement. Furthermore, the company’s stated policies for enhancing external environment resilience and pursuing M&A and alliances under its Mid-Term Management Plan could be significant points for monitoring its future business expansion.

6136|OSG

2750.0

▲ +2.80%

📄 Announcement Facts

- OSG’s consolidated net sales for the first quarter of fiscal year 2026 (December 1, 2025, to February 28, 2026) reached ¥42,627 million, an increase of 12.8% compared to the prior year period.

- Net profit attributable to owners of parent surged by 93.2% year-on-year to ¥5,040 million.

- Operating profit rose by 57.9% to ¥6,134 million, and ordinary profit increased by 61.1% to ¥6,694 million.

- The equity ratio stood at 68.8% at the end of the first quarter, showing an improvement from 67.5% at the end of the previous fiscal year.

- The consolidated earnings forecast for the full fiscal year 2026 (for the second quarter cumulative and full year) remains unchanged from the figures announced on January 8, 2026.

🤖 AI Perspective

The reported results indicate a strong start to the fiscal year for OSG, with significant growth in net sales and all profit metrics, particularly the net profit attributable to owners of parent. The increased overseas sales ratio of 70.8% and reported sales growth in European, African, Asian, and American segments may suggest diversified growth drivers for the company. The improvement in the equity ratio could be seen as a positive indicator for financial stability, while the unchanged full-year forecast implies that management views current performance as aligned with their initial expectations.

6289|技研製作所

1996.0

▲ +1.27%