📌 Today’s Highlights

Today we cover 37 IR announcements. Notable among them: G-犬猫生活 (556A), G-FLN (9241), iFSP500ダブル (2237). Use the table of contents below to navigate to each company.

- 556A|G-犬猫生活

- 3070|G-ジェリービーンズ

- 3461|パルマ

- 9241|G-FLN

- 6186|一蔵

- 2237|iFSP500ダブル

- 8244|近鉄百貨店

- 324A|G-ブッキングR

- 5204|石塚硝

- 7380|十六FG

- 6858|小野測器

- 4249|森六

- 1980|ダイダン

- 3766|システムズD

- 8399|琉球銀

- 3672|オルトプラス

- 4307|NRI

- 485A|G-パワーエックス

- 4880|セルソース

- 6923|スタンレー電

- 7309|シマノ

- 7751|キヤノン

- 9340|アソインター

- 9795|ステップ

- 4442|G-バルテスHD

- 1939|四電工

- 1945|東京エネシス

- 2053|中部飼料

- 3739|コムシード

- 4923|COTA

- 6592|マブチモーター

- 9326|G-関通HD

- 8700|丸八証券

- 6332|月島HD

- 3465|ケイアイスター不動産

- 7371|G-Zenken

- 9369|キユソ流通

556A|G-犬猫生活

—

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Inuneko Seikatsu Inc. listed on the Tokyo Stock Exchange Growth Market (code: 556A) on April 23, 2026.

- For the fiscal year ending April 2026, the company forecasts non-consolidated net sales of ¥4,449 million (up 53.3% year-on-year), operating profit of ¥606 million (up 557.1% year-on-year), and net profit of ¥473 million (up 127.9% year-on-year).

- Non-consolidated results for the third quarter of FY2026 were net sales of ¥3,331 million, operating profit of ¥412 million, and net profit for the quarter of ¥340 million.

- The company’s business activities include “Life Sales,” primarily D2C sales of original pet food, and “Life Services,” such as the operation of animal hospitals and grooming salons.

- In May 2025, the company newly commenced the operation of an animal hospital through an M&A.

🤖 AI Perspective

The significant projected growth in net sales and profits, particularly the over five-fold increase in operating profit for the fiscal year ending April 2026, presented alongside its listing, may draw investor attention to the company’s immediate outlook. This growth forecast appears to be underpinned by an expansion strategy, including aggressive marketing for its core D2C pet food business and the recent M&A of an animal hospital, suggesting diversification within the pet care sector. The D2C subscription model, coupled with increasing demand for high-value premium pet food, could position the company for sustained revenue stability and growth, which may be a key point for evaluation.

3070|G-ジェリービーンズ

110.0

▼ -4.35%

📎 Source:G-ジェリービーンズ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- JB Sustainable Inc., a subsidiary of G-Jellybeans Group (TSE Growth: 3070), entered into a business alliance agreement with Palma Co., Ltd. (TSE Standard: 3461) on April 23, 2026, for the installation and operation of grid-scale storage batteries.

- The alliance aims to integrate JB Sustainable’s expertise in installing and operating grid-scale storage batteries with Palma’s nationwide network of self-storage (container-type trunk rooms).

- Palma’s self-storage facilities are considered suitable for battery installation sites due to their locations near power demand areas, existing foundations and spaces for containers, and high infrastructure compatibility for power connection.

- G-Jellybeans expects this alliance to provide benefits such as rapid securing of potential installation sites, efficient infrastructure expansion on a lease basis without land purchase, and effective operation by utilizing highly compatible facilities.

- The impact of this business on the company’s performance for the fiscal year ending January 2027 is currently under review, and any timely disclosure requirements will be met promptly.

🤖 AI Perspective

This business alliance strategically addresses the need for grid-scale storage batteries to stabilize renewable energy supply by utilizing Palma’s extensive nationwide network. It may allow G-Jellybeans to accelerate its battery business expansion while aligning with broader decarbonization goals. Investors might consider monitoring the future progress of this initiative and its specific financial contributions as they become available.

3461|パルマ

564.0

▲ +0.71%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Palma Co., Ltd. announced on April 23, 2026, its decision to enter into a business alliance agreement with JB Sustainable Co., Ltd. for the installation and operation of grid-scale storage batteries.

- This alliance aims to explore utilizing a portion of Palma’s nationwide network of self-storage facilities as installation sites for grid-scale storage batteries, leveraging JB Sustainable’s expertise in battery installation and operation.

- Three deployment models for battery installation sites have been formulated: deployment at Palma’s owned/operated facilities, proposals for introduction to facilities owned by Palma’s customers, and sublease deployment utilizing facilities leased from third parties.

- JB Sustainable Co., Ltd., a subsidiary of Jelly Beans Group Co., Ltd. (Securities Code: 3070), was established on June 12, 2025, and engages in environmental solutions, energy business, and construction/logistics-related businesses.

- Palma anticipates a minor impact on its financial performance from this business alliance in the current fiscal year, while expecting it to contribute to enhancing corporate value in the mid to long term.

🤖 AI Perspective

- This alliance may suggest Palma’s potential to diversify its existing nationwide real estate network into new applications within renewable energy infrastructure.

- The initiative to convert unused spaces within self-storage facilities into energy supply hubs could be seen as a strategy for maximizing asset utilization and generating new revenue streams.

- The partnership with newly established JB Sustainable might indicate an intent to quickly enter the electricity supply-demand adjustment market.

9241|G-FLN

1362.0

▲ +1.11%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-FLN reported consolidated net sales of ¥875 million and operating income of ¥15 million for the second quarter cumulative period of the fiscal year ending August 2026.

- Monthly Recurring Revenue (MRR) sales increased by 6.3% year-on-year to ¥256 million, with the number of paid users for “Mypre-kun” exceeding 2,000 stores.

- The Furusato Nozei (hometown tax) business saw a 6.5% year-on-year decrease in sales, yet achieved a 7.4% year-on-year increase in segment profit, attributed to changes in the points system in September 2026 and contract revisions.

- The Relationship Population Creation business demonstrated significant growth, with sales increasing by 685% year-on-year, driven by initiatives such as the “Machi Spacha Project” in Kawaguchi City and the expansion of Nativ.media to private regional trading companies.

- By segment, the Local Information Distribution Business recorded a 15.4% year-on-year increase in cumulative sales, while the Public Solutions Business saw a 3.3% year-on-year decrease in cumulative sales.

🤖 AI Perspective

G-FLN’s Q2 FY2026 cumulative results indicate a steady growth trajectory for its MRR business and a rapid expansion of its emerging Relationship Population Creation business. While the Furusato Nozei segment experienced a sales decline due to system changes, its ability to maintain profit suggests effective cost management and operational efficiency. These trends may suggest the company’s strategic emphasis on growth areas within its business portfolio and a commitment to improving profitability.

6186|一蔵

380.0

▲ +1.60%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Ichikura Co., Ltd. announced on April 23, 2026, a correction to a portion of its “Notice of Partial Expansion of Shareholder Benefit Program,” which was originally published on April 22, 2026.

- The reason stated for the correction was an error in the description of the aforementioned notice.

- The correction specifically pertains to the available options under “2. Details of Shareholder Benefit Program Change.”

- Previously, the program offered six options (① to ⑥); the corrected version now includes a seventh option, “⑦ Photo Plan (Studio Merlin exclusive) 3,000 yen discount,” making a total of seven options (① to ⑦).

- There are no changes to the other existing benefit categories related to the Japanese traditional clothing business, wedding business, or the list of affiliated restaurants.

🤖 AI Perspective

This IR correction addresses an error in the previously announced details of the shareholder benefit program expansion. Consequently, a new option has been added to the shareholder benefits, effectively expanding the range of choices for shareholders. The inclusion of a photo plan may suggest an effort to enhance benefits that align with the company’s existing wedding and Japanese traditional clothing businesses, potentially offering increased value to shareholders.

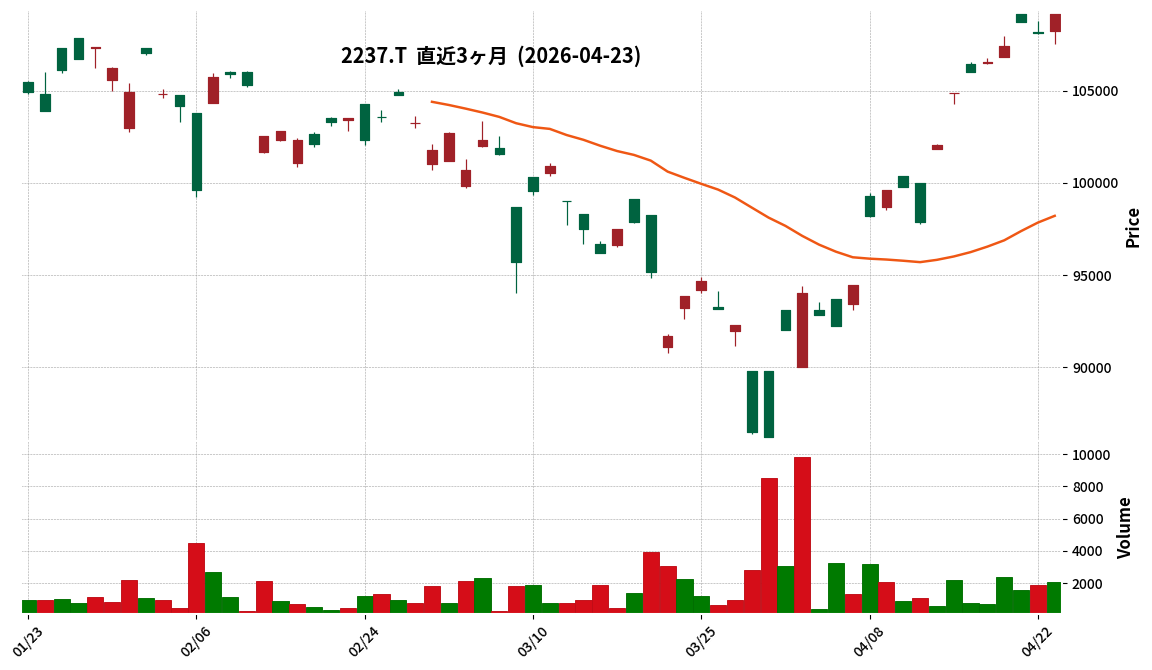

2237|iFSP500ダブル

108250.0

▲ +0.05%

📎 Source:iFSP500ダブル Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- iFreeETF S&P500 Leverage (Code: 2237) announced its financial results for the March 2026 term (September 11, 2025 – March 10, 2026) on April 23, 2026.

- Total net assets at the end of the current period reached ¥1,771 million, an increase from ¥1,719 million at the end of the previous period (September 2025 term).

- The Net Asset Value (NAV) per unit was ¥100,439.8, an increase from ¥96,727.6 at the end of the previous period.

- The distribution per unit for the current period was ¥195 (per trading unit).

- The composition ratio of major investment assets was 43.8% (¥776 million), while cash, deposits, and other assets (net of liabilities) accounted for 56.2% (¥995 million).

- During the current period, the number of units set was 13 thousand units, and the number of units exchanged was also 13 thousand units, with outstanding units remaining at 17 thousand at the end of the current period.

🤖 AI Perspective

The increase in net assets and NAV per unit for iFreeETF S&P500 Leverage during the March 2026 term suggests an improvement in the fund’s asset value. Changes in the composition ratio between major investment assets and cash/deposits could indicate shifts in the fund’s operational strategy, but the decrease in per-unit distribution compared to the prior period may be a factor for investors to observe.

8244|近鉄百貨店

1628.0

▼ -0.37%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kintetsu Department Store has published its Financial Results Briefing for the fiscal year ending February 2026.

- The company is listed on the Tokyo Stock Exchange.

🤖 AI Perspective

The provided IR text does not contain specific figures or business details from the financial results. Investors may look for further details to be disclosed in future IR announcements, making continued monitoring potentially relevant.

324A|G-ブッキングR

1028.0

▲ +0.29%

📎 Source:G-ブッキングR Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Booking R Co., Ltd. announced a revision and enhancement of its shareholder benefit program.

- This announcement was made by the company, which is listed on the Tokyo Stock Exchange.

🤖 AI Perspective

The announced enhancement to the shareholder benefit program may be viewed as an indication of the company’s commitment to strengthening shareholder returns. This could potentially contribute to increasing the company’s long-term attractiveness for investors and securing stable shareholders.

5204|石塚硝

3255.0

▼ -3.98%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Ishizuka Glass Co., Ltd. announced its consolidated financial results for the fiscal year ended March 2026 (from March 21, 2025, to March 20, 2026).

- Consolidated net sales reached ¥59,510 million (up 6.3% year-on-year), operating profit was ¥4,160 million (up 8.1% year-on-year), and ordinary profit was ¥3,882 million (up 4.5% year-on-year).

- Net profit attributable to owners of parent decreased by 15.2% year-on-year, totaling ¥2,618 million.

- The annual dividend for the fiscal year ended March 2026 was raised to ¥70.00 per share from ¥65.00 in the previous period. The forecast for the fiscal year ending March 2027 indicates an annual dividend of ¥72.00 per share.

- For the fiscal year ending March 2027, the company forecasts consolidated net sales of ¥62,000 million (up 4.2% year-on-year), but anticipates a decrease in profits: operating profit of ¥3,500 million (down 15.9% year-on-year), ordinary profit of ¥3,200 million (down 17.6% year-on-year), and net profit attributable to owners of parent of ¥2,150 million (down 17.9% year-on-year).

🤖 AI Perspective

For the fiscal year ended March 2026, the company achieved increased revenue and operating profit due to contributions from a new plant in the plastic container business, cost reduction measures, and sales price revisions. However, the decrease in net profit attributable to owners of parent may be attributed to increased tax expenses. The forecast for the fiscal year ending March 2027 projects higher sales but lower profits, which could indicate challenges in maintaining profitability amidst a changing business environment. The company’s intention to increase dividends for two consecutive periods suggests a continued focus on shareholder returns.

7380|十六FG

1986.0

▲ +1.38%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Juroku FG announced on May 10, 2024, a revision to its year-end dividend forecast for the fiscal year ended March 2024.

- The company revised its year-end dividend per share from 37.50 yen to 40.00 yen, an increase of 2.50 yen.

- Consequently, the total annual dividend for the fiscal year ended March 2024 will be 77.50 yen per share, combining the interim dividend of 37.50 yen and the revised year-end dividend.

- The record date for the dividend is March 31, 2024, with the effective date (scheduled payment commencement date) planned for June 27, 2024.

🤖 AI Perspective

- This announcement reflects Juroku FG’s commitment to shareholder returns, which is a key management priority.

- The upward revision of the year-end dividend, based on the company’s performance outlook, could be seen as an indication of confidence in its financial health and earnings stability.

- For investors, a dividend increase typically serves as a positive signal regarding the company’s current stability and potential for future growth.

6858|小野測器

923.0

▲ +3.94%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of the fiscal year ending December 2026 (January 1 to March 31, 2026), consolidated results showed net sales of JPY 4,448 million (up 19.4% year-on-year), operating profit of JPY 423 million (up 28.0%), ordinary profit of JPY 416 million (up 27.2%), and profit attributable to owners of parent of JPY 267 million (up 13.1%).

- Orders received during the quarter amounted to JPY 3,893 million (up 12.5% year-on-year), and the order backlog reached JPY 8,494 million (up 25.7% year-on-year).

- By segment, “Custom Test Systems & Services” contributed significantly with net sales of JPY 3,186 million (up 20.7% year-on-year) and segment profit of JPY 413 million (up 28.9% year-on-year).

- The full-year consolidated earnings forecast for the fiscal year ending December 2026 and the annual dividend forecast (JPY 30.00) remain unchanged from the previously announced figures.

- As of the end of the period, consolidated total assets were JPY 22,487 million, net assets JPY 16,770 million, and the equity ratio was 73.1%.

🤖 AI Perspective

The significant double-digit growth across sales and profit metrics in the first quarter indicates a strong start to the fiscal year for Ono Sokki. The increase in orders received and order backlog may suggest a continued robust business environment for the company. The decision to maintain the full-year earnings forecast could imply that the current performance is aligned with internal projections or that the company is adopting a prudent stance on its future outlook.

4249|森六

2299.0

▼ -0.95%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Moriroku Co., Ltd. (Code: 4249) announced on April 23, 2026, an upward revision to its consolidated earnings forecast for the full fiscal year ending March 31, 2026 (April 1, 2025 – March 31, 2026).

- The company revised its full-year net sales forecast from JPY 131,200 million to JPY 133,800 million, representing a 2.0% increase.

- Operating profit is projected to increase by 31.4% from JPY 3,500 million to JPY 4,600 million, and ordinary profit by 39.3% from JPY 2,800 million to JPY 3,900 million.

- Profit attributable to owners of parent is revised up by 28.9% from JPY 1,800 million to JPY 2,320 million, with earnings per share (EPS) rising from JPY 125.73 to JPY 161.91.

- Key reasons for the revision include a weaker yen than anticipated, better-than-expected recovery production in North America due to semiconductor supply improvement, smaller-than-expected production cuts in Asia, improved model mix in Japan, and fixed cost reductions in North America.

🤖 AI Perspective

This earnings forecast revision shows a significant upward adjustment, particularly with operating and ordinary profits increasing by over 30%, indicating a notable improvement in profitability. This enhancement appears to be driven by a combination of factors such as the depreciation of the yen, production recovery in North America, operational improvements in Japan, and fixed cost reductions. These multifaceted factors may suggest a strengthening financial performance that could be worth monitoring for investors.

1980|ダイダン

2691.0

▲ +0.45%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Daidan Co., Ltd. has revised its consolidated financial forecast for the fiscal year ending March 2026. While net sales were revised down by ¥5,000 million to ¥255,000 million, operating profit was revised up by ¥2,000 million to ¥34,000 million, and profit attributable to owners of parent was revised up by ¥2,900 million to ¥26,000 million.

- The upward revision in consolidated operating profit is attributed to further profit improvements in construction projects.

- Consolidated ordinary profit and profit attributable to owners of parent were further boosted by foreign exchange gains, gains on sale of investment securities from the disposal of strategic shareholdings, and tax credits from the wage increase promotion tax system, in addition to the higher operating profit.

- The forecast for consolidated orders received for the fiscal year ending March 2026 was revised upwards by ¥30,000 million to ¥350,000 million, from the previous forecast of ¥320,000 million, reflecting strong domestic order trends.

- The year-end dividend forecast for the fiscal year ending March 2026 was raised by ¥9 from the previous forecast of ¥45 per share to ¥54 per share (¥162 per share on a pre-stock split basis). This results in an annual dividend (pre-stock split basis) of ¥244 per share, up from ¥217.

🤖 AI Perspective

- Despite a slight downward revision in net sales, the significant upward revision in profits and the increased dividend are notable, driven by improved project profitability and other financial factors.

- The strong trend in orders received may suggest positive implications for future performance.

- The dividend increase, in line with the company’s policy of “a dividend payout ratio of 40% or more and a minimum dividend on equity (DOE) of 4.8%,” could be viewed as a commitment to shareholder returns.

3766|システムズD

1192.0

▼ -0.25%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Systems D announced on April 23, 2026, a revision (increase) to its year-end dividend forecast for the fiscal year ending March 2026.

- The year-end dividend forecast has been increased from the previously announced ¥50.00 per share to ¥55.00 per share in this revision.

- Consequently, the total annual dividend has also been revised from the previously expected ¥50.00 per share to ¥55.00 per share.

- The reason for the revision is to further enhance shareholder returns by clarifying a “progressive dividend policy” (not reducing dividends, but increasing or maintaining them) and setting a DOE (Dividend on Equity) target of 3.5% or more for the March 2026 fiscal year.

- This represents an increase of ¥5 per share in ordinary dividend (a ¥10 increase compared to the previous fiscal year), reflecting a policy aimed at achieving management conscious of capital cost and further enhancing shareholder returns.

🤖 AI Perspective

- The company’s clarification of a progressive dividend policy and the establishment of a specific DOE target may signal a strong commitment to shareholder returns.

- This approach could raise investor expectations for stable and continuously expanding dividends in the future.

- The emphasis on management conscious of capital cost might indicate the company’s intent to enhance corporate value through improved capital efficiency.

8399|琉球銀

2327.0

▼ -1.57%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- The Bank of the Ryukyus, Ltd. announced on April 23, 2026, that its Board of Directors resolved to revise the earnings forecast and year-end dividend forecast for the fiscal year ending March 2026.

- The consolidated earnings forecast for the full fiscal year ending March 2026 was revised upward, with ordinary income increasing from JPY 11,500 million to JPY 12,883 million (a 12.0% increase), and profit attributable to owners of parent increasing from JPY 8,000 million to JPY 8,960 million (a 12.0% increase).

- The reason for the earnings forecast revision is primarily attributed to an increase in interest and dividends from securities, along with a decrease in expenses and credit-related costs at the bank on a non-consolidated basis.

- The year-end dividend forecast for the fiscal year ending March 2026 was revised upward from JPY 27.00 per share to JPY 61.00 per share (an increase of JPY 34.00). Consequently, the annual dividend forecast will be JPY 88.00 per share, up from JPY 54.00.

- The dividend revision is based on a comprehensive consideration of performance, the financial environment, and the perspective of enhancing future shareholder value.

🤖 AI Perspective

Ryukyu Bank has announced an upward revision of its consolidated and non-consolidated earnings forecasts for the fiscal year ending March 2026, alongside an increased year-end dividend forecast. The upward revision in earnings, largely driven by higher interest and dividends from securities and lower expenses, could suggest a robust operational performance. This development also highlights a significant enhancement in shareholder returns through an increased annual dividend payout.

3672|オルトプラス

38.0

▼ -2.56%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- AltPlus Co., Ltd. announced a partial change to the payment schedule and share acquisition plan for the third-party allotment under its capital and business alliance with Okazaki Holdings Co., Ltd.

- Initially, AltPlus planned to acquire 1,600 common shares of Okazaki Holdings in April 2026 (scheduled), but this acquisition will now be split into two tranches.

- Specifically, 800 common shares will be acquired as the First Third-Party Allotment on April 27, 2026 (scheduled), and another 800 common shares will be acquired as the Second Third-Party Allotment in August 2026 (scheduled).

- The reason for the change is that the fund procurement from the exercise of the 11th series of share options by EVO FUND, initially projected at 640,000 thousand yen, only reached 432,610 thousand yen as of April 17, 2026, which is approximately half of the original target.

- Okazaki Holdings is expected to become an equity-method affiliate of AltPlus upon the share transfer and the subscription of the First Third-Party Allotment.

- The total acquisition cost of Okazaki Holdings shares, amounting to 887,000 thousand yen (840,000 thousand yen for common shares and 47,000 thousand yen for advisory fees, etc.), and the total number of shares held after acquisition, 2,000 shares (voting rights ratio of 43.48%), remain unchanged.

🤖 AI Perspective

This announcement indicates an adjustment in AltPlus’s planned investment in Okazaki Holdings, with the schedule being modified in response to the status of its funding. The company’s ability to secure the full amount of anticipated funds from its initial source appears to be a key factor in this phased approach to the investment. The timing of Okazaki Holdings becoming an equity-method affiliate is also aligned with the revised payment schedule.

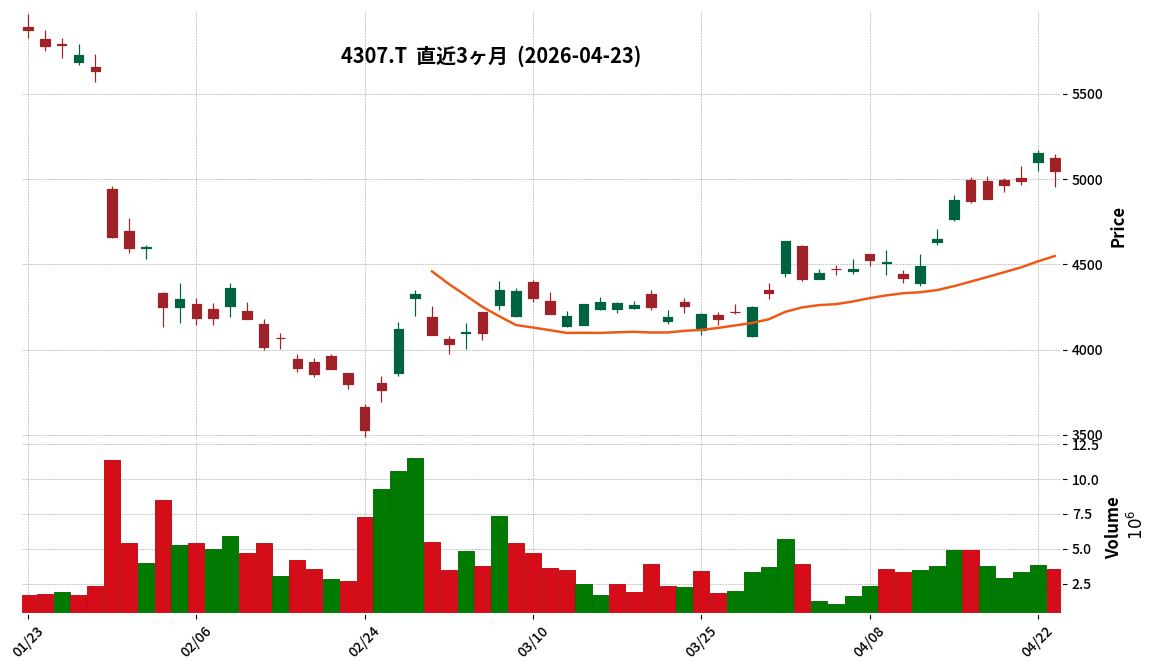

4307|NRI

5045.0

▼ -2.13%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- NRI has revised its consolidated earnings forecast for the fiscal year ending March 2026. Operating profit is now projected at ¥58.0 billion, down from the previous forecast of ¥150.0 billion, and profit attributable to owners of the parent is revised to ¥15.0 billion from ¥104.0 billion.

- The primary reason for the consolidated earnings forecast revision is the expected recording of goodwill and other impairment losses totaling ¥96.9 billion. This includes ¥76.9 billion for NRI Australia Limited and ¥19.9 billion for Core BTS, Inc. in North America.

- The impairment for NRI Australia Limited is attributed to a decrease in orders for consulting and managed services, while for Core BTS, Inc., it is due to deterioration in its cloud consulting business.

- In its individual financial statements, NRI expects to record an impairment loss of ¥48.8 billion on shares of its Australian subsidiary, NRI Australia Holdings Pty Ltd, as an extraordinary loss, as the fair value of the shares was deemed to have significantly declined.

- This impairment loss on shares of associates recorded in the individual financial statements will be eliminated in the consolidated financial statements and therefore has no impact on consolidated results.

🤖 AI Perspective

The significant downward revision of the consolidated earnings forecast primarily stems from substantial impairment losses at overseas subsidiaries, which is expected to have a considerable impact on consolidated profits. This situation may suggest challenges in global business operations or a reassessment of strategies in international markets. While the impairment loss on equity of associates in the individual financial statements does not affect consolidated results, it indicates a substantial decline in the value of a specific overseas subsidiary, which could warrant further monitoring of its operational performance.

485A|G-パワーエックス

7090.0

▼ -7.56%

📎 Source:G-パワーエックス Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- PowerX Co., Ltd. announced a stock split and a partial amendment to its Articles of Incorporation, resolved at its Board of Directors meeting on April 23, 2026.

- The company will conduct a 1-for-3 stock split for its common shares, with May 31, 2026, as the record date and June 1, 2026, as the effective date.

- As a result of the split, the total number of issued shares (based on shares outstanding as of March 31, 2026) will increase from 38,050,750 shares to 114,152,250 shares.

- There will be no change to the stated capital in conjunction with this stock split.

- The Articles of Incorporation will be partially amended, effective June 1, 2026, to increase the authorized share capital from 128,000,000 shares to 384,000,000 shares.

- The exercise prices of outstanding stock acquisition rights will also be adjusted, effective June 1, 2026, in accordance with the stock split ratio.

🤖 AI Perspective

This stock split aims to lower the per-share investment amount, potentially making PowerX stock more accessible to a wider range of investors. Such a move typically enhances stock liquidity and could broaden the company’s investor base. The amendment to the Articles of Incorporation regarding authorized shares is a standard procedural adjustment reflecting the split.

4880|セルソース

366.0

▼ -3.68%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- CellSource Inc. resolved to conduct an absorption-type merger of its wholly-owned subsidiary, Hybrid Medical Inc., and executed a merger agreement at its Board of Directors meeting held on April 23, 2026.

- CellSource Inc. will be the surviving company in this absorption-type merger, and Hybrid Medical Inc. will be dissolved. The effective date of the merger is scheduled for July 1, 2026.

- This merger qualifies as a simplified merger for CellSource Inc. under Article 796, Paragraph 2 of the Companies Act, and a short-form merger for Hybrid Medical Inc. under Article 784, Paragraph 1 of the Companies Act, meaning no general shareholders’ meetings will be held by either company for the approval of the merger agreement.

- The purpose of the merger is to optimize the allocation of management resources across the group, accelerate decision-making, improve operational efficiency, and strengthen the governance structure.

- As this is a merger with a wholly-owned subsidiary, there will be no issuance of new shares, increase in capital, or delivery of money or other assets, and the impact on CellSource Inc.’s financial performance for the October 2026 fiscal year is stated to be minor.

🤖 AI Perspective

This merger suggests CellSource is aiming to streamline its group structure and optimize resource allocation by integrating its subsidiary, which specializes in medical institution operation support. The consolidation of Hybrid Medical’s expertise with CellSource’s management resources could lead to enhanced operational efficiency and a stronger governance framework across the group. This move may indicate a strategic intent to centralize business strategies and facilitate more agile decision-making within the organization.

6923|スタンレー電

3003.0

▼ -1.41%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Stanley Electric Co., Ltd. announced on April 23, 2026, the completion of its acquisition of all shares in Iwasaki Electric Co., Ltd., making it a consolidated subsidiary.

- This completion follows previous disclosures on January 29, 2026, and March 31, 2026, regarding the acquisition.

- Iwasaki Electric Co., Ltd. is engaged in the development, manufacturing, and sales of various light sources, lighting fixtures, optical/environmental equipment (UV, IR, electron beams), and related solutions.

- Following the acquisition, Stanley Electric Co., Ltd. holds 100% of Iwasaki Electric Co., Ltd.’s shares as the major shareholder.

- Stanley Electric states that the impact of this acquisition on its consolidated financial results is currently under review, and any disclosable matters will be promptly announced.

🤖 AI Perspective

The completion of this acquisition could be viewed as a strategic step for Stanley Electric to expand its business portfolio and potentially create technological synergies. Iwasaki Electric’s expertise in light sources and optical/environmental equipment might complement Stanley Electric’s existing operations, and the integration’s impact on their combined market position will be worth monitoring. The specific effects on consolidated earnings are still being assessed, and further disclosures will be anticipated.

7309|シマノ

15975.0

▼ -5.22%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the first quarter of fiscal year 2026, Shimano reported consolidated net sales of ¥117,644 million, a 3.6% increase year-on-year, and net profit attributable to owners of parent of ¥12,814 million, a 30.9% increase year-on-year.

- However, operating profit decreased by 35.6% to ¥10,400 million, and ordinary profit decreased by 3.4% to ¥14,885 million.

- In the Bicycle Components segment, net sales were ¥87,361 million (down 0.7% YoY) and operating profit was ¥7,792 million (down 46.3% YoY).

- The Fishing Tackle segment recorded net sales of ¥30,175 million (up 18.5% YoY) and operating profit of ¥2,596 million (up 58.6% YoY).

- Shimano revised its full-year consolidated ordinary profit forecast for fiscal year 2026 upward from ¥49,000 million to ¥53,300 million, and net profit attributable to owners of parent from ¥34,000 million to ¥42,000 million.

🤖 AI Perspective

Shimano’s Q1 FY2026 results show a mixed performance with increased net sales and net profit, but a decline in operating and ordinary profits. This divergence may suggest shifts in operational efficiency or non-operating factors influencing overall profitability. The upward revision of the full-year ordinary and net profit forecasts could indicate management’s confidence in improved future earnings, while the performance of the Bicycle Components segment, particularly its declining operating profit, remains a key area for investors to monitor.

7751|キヤノン

4369.0

▼ -1.84%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Canon Inc. announced its consolidated financial results (U.S. GAAP) for the first quarter of fiscal year 2026 (January 1, 2026 to March 31, 2026) on April 23, 2026.

- Consolidated net sales for the quarter were ¥1,093,653 million, representing a 3.3% increase compared to the same period of the previous year.

- Consolidated operating profit amounted to ¥71,370 million, a decrease of 26.1% year-on-year.

- Net profit attributable to Canon Inc. shareholders for the quarter was ¥48,303 million, a 33.1% decrease from the prior year’s first quarter.

- The consolidated full-year forecast for fiscal year 2026 remains unchanged: net sales of ¥4,765,000 million (up 3.0% year-on-year), operating profit of ¥456,000 million (up 0.1% year-on-year), and net profit attributable to Canon Inc. shareholders of ¥333,000 million (up 0.3% year-on-year). This full-year forecast involved a revision from the most recently disclosed forecast.

🤖 AI Perspective

While Canon achieved a modest increase in net sales for the first quarter, the significant year-over-year decline in both operating and net profit warrants attention. This divergence between revenue growth and profit contraction could suggest pressures on profit margins from various factors, such as increased operational costs or shifts in the business environment. Given that the full-year earnings forecast remains unchanged, investors may wish to monitor how the company plans to align its subsequent quarters with these maintained profit targets.

9340|アソインター

681.0

▲ +0.59%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Aso International Co., Ltd. resolved on April 23, 2026, to form a capital and business alliance with Preteeth AI, Inc. d/b/a/Dentscape (based in California, USA) and to make an investment via a SAFE (Simple Agreement for Future Equity) contract.

- Dentscape, established on April 26, 2021, specializes in developing and providing AI dental solutions, particularly strong in enhancing digital workflows for prosthetic and aesthetic dentistry using AI.

- Through this alliance, Aso International plans to introduce Dentscape’s cloud-based AI dental prosthetics CAD service to the Japanese market, entering a new service domain.

- The investment in Dentscape amounts to $200,000 (approximately JPY 32 million) under a SAFE agreement, with the contract scheduled for May 15, 2026.

- This transaction is stated to have no impact on the company’s performance for the fiscal year ending June 2026.

🤖 AI Perspective

This alliance suggests Aso International’s move to embrace AI-driven dental CAD services in the Japanese market, potentially accelerating digital transformation in the dental industry. The initiative could address challenges such as the severe shortage of dental technicians by leveraging AI for operational efficiency and improved precision. The SAFE investment in a startup may also indicate a strategic intent to strengthen future collaborations.

9795|ステップ

2391.0

▼ -0.13%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Step Co., Ltd. announced its H1 FY2026 (interim) financial results, reporting net sales of ¥8,356 million (up 2.4% YoY), operating income of ¥2,380 million (up 1.2% YoY), ordinary income of ¥2,426 million (up 1.2% YoY), and interim net income of ¥1,697 million (up 2.7% YoY), indicating both increased revenue and profit.

- The forecast for the full-year dividend for FY2026 remains unchanged, with an interim dividend of ¥44 and a year-end dividend of ¥44, totaling ¥88 per share.

- The full-year performance forecast for FY2026 is maintained at net sales of ¥16,494 million (up 4.1% YoY) and net income of ¥2,754 million (up 2.4% YoY).

- In entrance exam results, the company achieved the No. 1 position in terms of successful applicants among all jukus for all eight “Gakuryoku Kojo Shingaku Jutenko” (academic improvement and university preparatory high schools) in Kanagawa Prefecture, and recorded a record-high number of successful applicants for Keio Gijuku High School and Tokyo Gakugei University Attached High School.

- The number of students in the after-school care division reached a record high of 661 as of March 31, 2026. The company opened the High School Exam Step Kawasaki School in March 2026 and plans to open the High School Exam Step Tomioka School in July 2026.

🤖 AI Perspective

The interim results show growth in both revenue and profit, primarily driven by strong entrance exam performance, which may suggest the company’s educational brand strength and instructional effectiveness are contributing to business expansion. The expansion of the after-school care division and new school openings could indicate a strategy for further strengthening future revenue streams. Additionally, the high equity ratio highlights the company’s robust financial health, a factor investors often monitor.

4442|G-バルテスHD

423.0

▼ -1.86%

📎 Source:G-バルテスHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-VALTES HD announced a group reorganization, effective July 1, 2026.

- The reorganization involves an absorption merger with Synfo Co., Ltd. as the surviving company and Mint Co., Ltd. as the dissolved company.

- Synfo Co., Ltd. will also succeed the entrusted development business, SES business, and software testing business from R.S.R. Co., Ltd. through an absorption-type company split.

- Synfo Co., Ltd. will change its trade name to “VALTES Solutions & AI Co., Ltd.”, and will also undergo a change in representative director and a relocation of its head office.

- The company stated that the impact of this reorganization on its consolidated performance is minor, as it is conducted between wholly-owned subsidiaries.

🤖 AI Perspective

This reorganization is stated to be aimed at strengthening group-wide operations, enhancing operational efficiency, increasing competitiveness, and improving corporate value, in line with the mid-term management plan formulated in June 2025. The consolidation of entrusted development businesses under “VALTES Solutions & AI Co., Ltd.” and the inclusion of “AI” in the new name may suggest a strategic focus on future technological trends. This move could be seen as an effort to clarify roles among consolidated subsidiaries and strengthen inter-company collaboration.

1939|四電工

1911.0

▲ +0.37%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Yondenko Co., Inc. announced on April 23, 2026, an upward revision to its consolidated and non-consolidated earnings forecasts for the fiscal year ending March 2026.

- For consolidated results, net income attributable to owners of parent is now projected to increase by 25.0% from the previous forecast, moving from ¥6,000 million to ¥7,500 million. Operating profit was revised up by 10.0% from ¥8,000 million to ¥8,800 million, and ordinary profit by 9.4% from ¥8,500 million to ¥9,300 million.

- The primary reasons for the earnings revision include an improved gross profit margin resulting from the acquisition of additional construction projects, and the recording of extraordinary gains from securities sales.

- The year-end dividend forecast for the fiscal year ending March 2026 has been revised upward from ¥72.00 per share to ¥77.00 per share.

- This dividend revision was made in accordance with the company’s “initiatives aimed at improving capital profitability,” which was announced in August 2023, and reflects the upward revision of the current year’s earnings forecast.

🤖 AI Perspective

- The upward revision of earnings suggests that the company’s net income was significantly boosted by a combination of factors, including improvements in its core business profitability and the recognition of extraordinary gains from securities sales.

- The increased year-end dividend could be interpreted as a reflection of the company’s commitment to enhancing capital profitability and its stance on returning profits to shareholders amid strong performance.

- The continued revision (increase) in dividend payments, even after the stock split implemented on October 1, 2024, may indicate a strong long-term shareholder return policy, which could be a point of interest for investors.

1945|東京エネシス

1740.0

▲ +1.05%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tokyo Enesys Co., Ltd. revised its consolidated and non-consolidated earnings forecasts for the full fiscal year ending March 2026 (April 1, 2025 – March 31, 2026) on April 23, 2026.

- For the consolidated earnings forecast, net sales were revised from ¥82.0 billion to ¥83.0 billion (an increase of 1.2%), operating profit from ¥3.9 billion to ¥4.7 billion (up 20.5%), ordinary profit from ¥4.1 billion to ¥5.5 billion (up 34.1%), and profit attributable to owners of parent from ¥3.4 billion to ¥4.3 billion (up 26.5%).

- Key reasons for the revisions include improved profit margins due to focused order-taking activities on profitability and enhanced productivity, as well as the recording of derivative valuation gains from foreign exchange fluctuations in non-operating income and extraordinary gains from the sale of policy-held shares.

- The company also revised its annual dividend forecast for the fiscal year ending March 2026, increasing the year-end dividend by ¥6.00 from the previous forecast of ¥29.00 to ¥35.00 per share, resulting in a total annual dividend of ¥63.00.

- This dividend revision is based on the company’s shareholder return policy and reflects the updated earnings forecast.

🤖 AI Perspective

The upward revision of the earnings forecast shows a significant improvement in profit figures relative to the modest increase in net sales, which may suggest a focus on enhancing profitability. The company’s emphasis on improved profit margins through strategic order-taking and enhanced productivity could indicate a sustainable improvement in operational efficiency. Furthermore, the increased dividend forecast may reflect management’s confidence in future earnings and a commitment to shareholder returns.

2053|中部飼料

1674.0

▲ +0.06%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Chubu Shiryo announced a revision to its consolidated earnings forecast for the fiscal year ending March 2026, with net sales revised downward but all profit figures (operating profit, ordinary profit, net profit attributable to owners of parent, and EPS) revised upward.

- Net profit attributable to owners of parent is now projected to increase by 34.1% from the previous forecast of JPY 4,100 million to JPY 5,500 million.

- The company explained that while net sales decreased by JPY 1,000 million due to lower-than-expected average selling prices despite increased sales volumes, the upward revision in profit was primarily driven by an unexpected improvement in the raw material position for livestock feed in the fourth quarter of the feed business, along with lower-than-anticipated increases in variable costs such as electricity and fuel.

- The annual dividend forecast for the fiscal year ending March 2026 has been revised from JPY 60 to JPY 65 per share, with the year-end dividend increased from JPY 30 to JPY 35 per share.

- This dividend revision reflects the updated earnings forecast and aims for a Dividend on Equity (DOE) of approximately 2.7%, with the goal to achieve DOE of 3% or more by the final year of the “Medium-Term Management Plan 2024” in March 2027.

🤖 AI Perspective

The significant upward revision in profit forecasts despite a slight decline in net sales may suggest an improvement in the company’s underlying profitability structure. The reported factors, such as improved raw material positioning and controlled variable costs in the feed business, could be key drivers for future earnings performance and efficiency. The increased dividend, alongside the revised earnings, indicates a commitment to shareholder returns and aligns with the company’s stated DOE targets in its medium-term plan.

3739|コムシード

—

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Comseed Co., Ltd. announced on April 23, 2026, the financial results for the fiscal year ended December 2025 of its parent company, Cykan Holdings Co., Ltd.

- As of March 31, 2026, Cykan Holdings Co., Ltd. holds 50.78% of the voting rights of Comseed, making it a direct parent company.

- Cykan Holdings reported a net profit of 6,403 million KRW for the fiscal year ended December 2025, a turnaround from a net loss of 3,348 million KRW in the previous fiscal year (ended December 2024).

- As of December 31, 2025, total equity reached 1,189 million KRW, resolving the negative equity of △3,205 million KRW recorded at the end of the previous fiscal year.

- Non-operating income significantly increased to 9,684 million KRW in the current fiscal year from 846 million KRW in the previous fiscal year.

🤖 AI Perspective

The improvement in the parent company’s financial health may contribute to the stabilization of Comseed’s management foundation. The resolution of negative equity and the substantial swing to net profit could indicate significant operational changes or one-time gains within Cykan Holdings. Investors may find this announcement relevant for understanding the broader financial context surrounding Comseed.

4923|COTA

1120.0

▼ -0.97%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- COTA Co., Ltd. announced on April 23, 2026, that the disclosure of its financial results for the fiscal year ending March 2026 is expected to exceed 50 days from the fiscal year-end.

- The original scheduled disclosure date was May 8, 2026.

- The reason for the delay is a system disruption caused by a cyberattack that occurred on March 27, 2026.

- This cyberattack has delayed the finalization of financial figures and the auditing process by the independent auditor.

- COTA stated that the new disclosure date will be announced promptly once it is determined.

🤖 AI Perspective

The delay in financial disclosure due to a cyberattack highlights the potential operational risks companies face from external threats. Investors may closely monitor the company’s progress in system recovery and the eventual financial disclosure to assess the full impact on business operations and financial performance. This situation could draw attention to the company’s IT infrastructure and cybersecurity measures, making the announcement of a new disclosure date a key point for stakeholders.

6592|マブチモーター

1600.5

▲ +0.00%

📎 Source:マブチモーター Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Mabuchi Motor Co., Ltd. announced on April 23, 2026, its board resolution to acquire all shares of food machinery manufacturer Masudac Co., Ltd., making it a wholly-owned subsidiary.

- Mabuchi Motor will acquire 2,601,996 common shares of Masudac from BCM-V Investment Limited Partnership for JPY 15.5 billion, with the estimated total acquisition cost, including advisory fees, being JPY 15.632 billion.

- Masudac Co., Ltd., established in March 1957, operates in the development, manufacturing, sales, and maintenance of food machinery, as well as food research, manufacturing, and sales.

- Upon completion, Mabuchi Motor is expected to hold 100% of Masudac’s voting rights, with the share transfer execution scheduled for mid-June 2026.

- This acquisition aligns with Mabuchi Motor’s “Management Plan 2030” and its business concept “e-MOTO,” aiming to expand its business in the “Machinery” domain, one of its three M areas (Machinery, Mobility, Medical).

🤖 AI Perspective

This acquisition appears to be a concrete step in Mabuchi Motor’s “e-MOTO” strategy, signaling a shift from its specialized small DC motor business to offer diverse “motion” solutions. Entering the food machinery sector could potentially leverage Mabuchi’s global presence and production technology to enhance Masudac’s international expansion and create synergies through the integration of both companies’ engineering capabilities. The impact on the current consolidated fiscal year’s financial results is currently under review, making future disclosures noteworthy for investors.

9326|G-関通HD

429.0

▼ -0.46%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-KANTSU Holdings Co., Ltd. announced on April 23, 2026, a correction to a part of its “FY2026 February Earnings Presentation Material.”

- The reason for the correction is that an error was found in the content of the material, which was originally disclosed on April 10, 2026.

- The correction pertains to the “Year-on-year Ordinary Profit” figure displayed on Slide 2 of the earnings presentation.

- Specifically, the erroneous figure of “+193 million yen” for “Year-on-year Ordinary Profit” has been corrected to the accurate figure of “+377 million yen.”

🤖 AI Perspective

This correction involves a significant revision to the year-on-year ordinary profit figure, which is a key indicator of the company’s profitability. Given the substantial change from the initially disclosed information, investors may need to carefully re-evaluate the company’s performance and financial position based on this updated information.

8700|丸八証券

1751.0

▼ -0.68%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Maruhachi Securities announced its preliminary financial results for the fiscal year ended March 2026 (April 1, 2025 – March 31, 2026) on April 23, 2026.

- Operating revenue increased by 16.0% year-on-year to JPY 3,576 million, primarily driven by higher stock brokerage commissions and investment trust fees.

- Selling, general and administrative expenses amounted to JPY 2,820 million, a 7.0% increase from the prior year.

- Operating profit reached JPY 739 million (up 67.5% year-on-year), and ordinary profit stood at JPY 1,006 million (up 68.0% year-on-year).

- Net profit for the period significantly increased by 74.4% year-on-year to JPY 684 million.

- Non-operating income included JPY 267 million from gains on the sale of investment securities and dividends received.

- The official financial results are scheduled to be released on April 30, 2026.

🤖 AI Perspective

These preliminary results suggest Maruhachi Securities achieved substantial year-on-year growth across key revenue and profit metrics for the fiscal year ended March 2026, with operating revenue seeing double-digit growth. The significant surge in net profit, exceeding 70%, appears to be supported not only by growth in core business activities like brokerage and investment trust fees but also by contributions from non-operating income, such as gains on investment securities and dividends received. These factors may draw investor attention ahead of the official full financial announcement.

6332|月島HD

2943.0

▲ +0.82%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Tsukishima Holdings Co. announced on April 23, 2026, revisions to its consolidated earnings forecast and year-end dividend forecast for the fiscal year ending March 2026.

- For the fiscal year ending March 2026, the consolidated earnings forecast for net sales was revised from ¥144,000 million to ¥149,000 million, and net income attributable to owners of parent from ¥15,000 million to ¥16,900 million. These represent changes of 3.5% and 12.7% respectively.

- With these revisions, net sales, operating income, ordinary income, and net income attributable to owners of parent are expected to reach record highs.

- Key reasons for the earnings forecast revision include increased revenue and profit due to progress on numerous existing orders, coupled with an increase in extraordinary gains from the sale of strategic shareholdings.

- The year-end dividend forecast for the fiscal year ending March 2026 was revised upward by ¥3 per share, from the previously announced ¥40.00 to ¥43.00, resulting in an expected annual dividend of ¥85.00 per share. This revision is based on the company’s profit distribution policy, which targets a Dividend on Equity (DOE) of 3.5% as a lower limit and a total return ratio of 50% or more.

🤖 AI Perspective

The upward revision of the earnings forecast indicates an expected overall improvement in key profitability metrics, with the notable increase in net income attributable to owners of parent. The expectation of achieving record-high profits across several key indicators could be viewed as a positive signal by investors. Furthermore, the dividend increase aligning with the company’s stated shareholder return targets may suggest a consistent commitment to shareholder value.

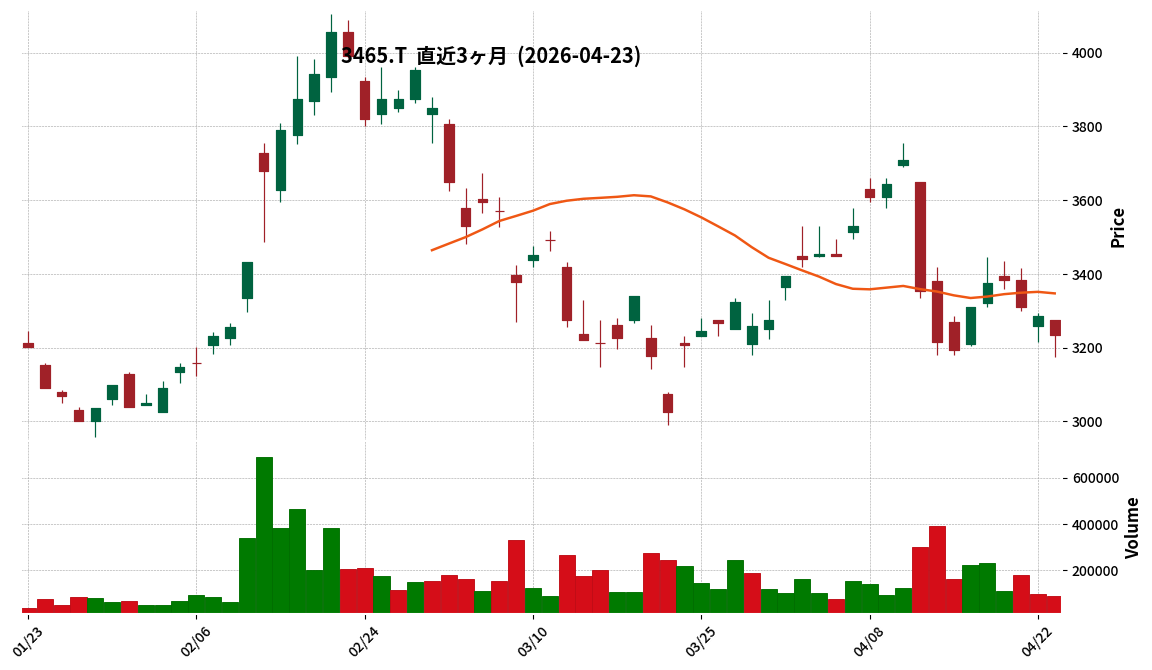

3465|ケイアイスター不動産

3235.0

▼ -1.52%

📎 Source:ケイアイスター不動産 Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- KAI STAR REAL ESTATE announced on April 23, 2026, a revision to its dividend forecast for the fiscal year ending March 2026.

- The full-year dividend forecast has been revised upwards from JPY 230.00 per share in the previous forecast to JPY 235.00 per share in the revised forecast.

- The year-end dividend forecast has been increased by JPY 5.00 per share, from JPY 130.00 to JPY 135.00.

- The company stated that the revision was based on its commitment to shareholder returns and a comprehensive consideration of robust trends in housing demand and supply.

- The revised year-end dividend per share is based on the number of shares prior to the 2-for-1 stock split that became effective on April 1, 2026.

🤖 AI Perspective

This dividend increase may suggest the company’s confidence in its current business environment and its ongoing commitment to shareholder returns. The stated reason, citing robust housing demand and supply, could be a key factor for investors monitoring the company’s future performance. A consistent and stable dividend payout strategy is generally viewed positively by investors.

7371|G-Zenken

686.0

▲ +0.29%

📎 Source:G-Zenken Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Zenkken resolved to conclude a business alliance agreement with The Kagoshima Bank, Ltd. following a Board of Directors meeting on April 23, 2026.

- The alliance aims for business development and regional economic revitalization through collaboration in service provision and sales activities.

- Under the agreement, Kagoshima Bank will introduce client companies with foreign human resources needs to G-Zenkken, which will then provide recruitment support for overseas engineers, introduce specified skilled workers for nursing care, and offer Japanese language education programs.

- The agreement conclusion date and planned business commencement date are both April 27, 2026.

- G-Zenkken anticipates that this alliance will contribute to its consolidated business performance and corporate value improvement in the medium to long term, though the impact on its consolidated results for the fiscal year ending June 2026 is currently under evaluation.

🤖 AI Perspective

This business alliance could leverage G-Zenkken’s expertise in overseas human resource introduction and support with Kagoshima Bank’s strong regional client base to address labor shortages in regional companies. It may also signify a strategic move by G-Zenkken to accelerate the growth of its overseas human resources segment, a key challenge outlined in its ‘Road to 250’ mid-term management plan, through collaboration with regional financial institutions. Investors may monitor future disclosures regarding the alliance’s financial impact, which is currently under review.

9369|キユソ流通

2721.0

▼ -4.09%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Q-Soh Logistics Co., Ltd. has decided to acquire shares and subscribe to a third-party allotment of Coldrush Logistics Private Limited, an India-based cold chain logistics company, making it a subsidiary.

- The acquisition price for Coldrush Logistics Private Limited shares is JPY 2,750 million, resulting in a voting rights ownership ratio of 51.6%.

- This acquisition is part of the company’s overseas expansion strategy under its 8th Medium-Term Management Plan (November 2025 – November 2028), which focuses on “Expanding and Further Developing New Areas.”

- The scheduled share transfer execution date is August 10, 2026.

- The company states that the impact of this acquisition on its consolidated results for the November 2026 fiscal year will be minor.

🤖 AI Perspective

- This move can be seen as a strategic expansion into India’s rapidly growing cold chain logistics market, driven by its large population and significant economic growth.

- The integration of Q-Soh Logistics’ temperature control technology with Coldrush’s existing network is intended to accelerate the provision of high-quality cold chain services, aligning with the company’s mid-term plan to strengthen its overseas business foundation.

- The plan to maintain Coldrush’s strong existing operations while establishing a governance structure suggests a balanced approach to post-acquisition integration.

💡 Start investing with IR insights

※ 本ページには広告が含まれます(PR)

Disclaimer: This article is for informational purposes only and does not constitute investment advice. All investment decisions are at your own risk.

コメント