📌 Today’s Highlights

Today we cover 21 IR announcements. Notable among them: イオンファン (4343), 芝浦機械 (6104), 兼松 (8020). Use the table of contents below to navigate to each company.

7733|オリンパス

1806.5

▲ +1.18%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Olympus Corporation announced the completion of its acquisition of all outstanding shares of BioProtect Ltd., making it a wholly-owned subsidiary, on June 1, 2026.

- BioProtect Ltd. is an Israeli medical device manufacturer specializing in the research, development, and manufacturing of biodegradable balloon rectal spacers for prostate cancer.

- Olympus acquired 16,925,621 shares, resulting in a 100% ownership stake post-acquisition.

- The acquisition price was $270 million (approximately JPY 43.3 billion, converted at an exchange rate of JPY 160.39 per USD as of April 2026).

- BioProtect Ltd. was established on September 22, 2004, and had a capital of JPY 11,451 million as of December 31, 2025.

🤖 AI Perspective

Olympus’s complete acquisition of BioProtect Ltd. appears to be a strategic move to strengthen its medical device business in the specific area of prostate cancer treatment. This acquisition of an Israel-based technology company could expand Olympus’s global product portfolio. The impact of this acquisition on Olympus’s financial performance is currently under review, and further disclosures are anticipated.

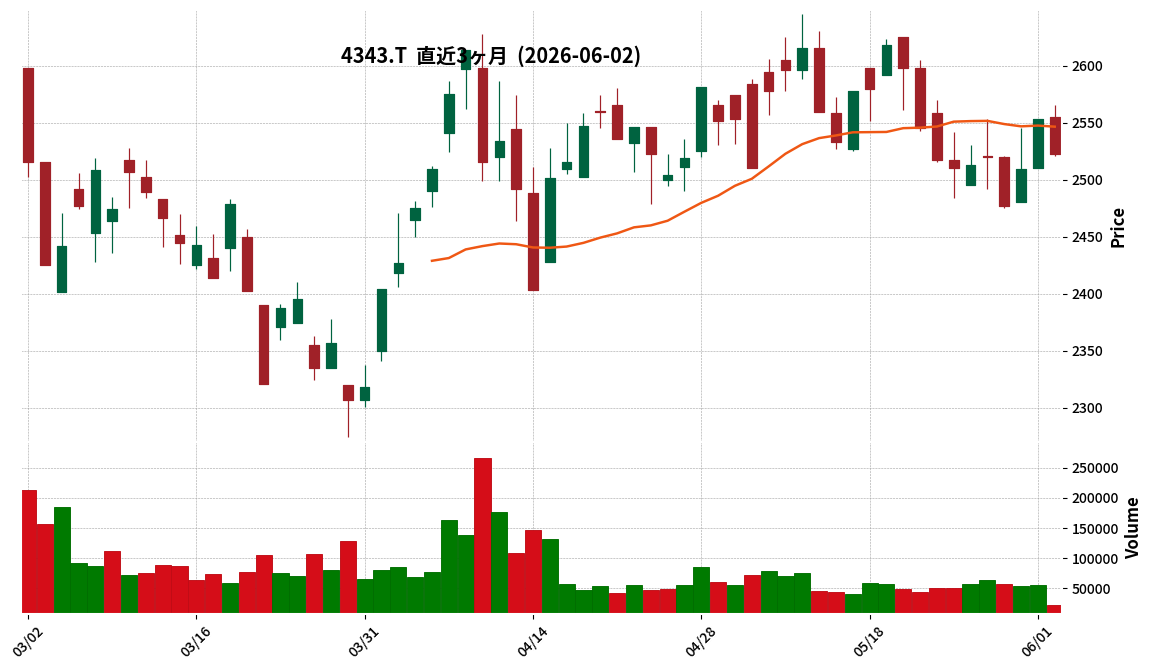

4343|イオンファン

2522.0

▼ -1.21%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- AEON FANTASY Co., Ltd. announced on June 2, 2026, a “Correction to a part of the ‘Q2 FY2026 Financial Results Supplementary Material'”.

- The correction pertains to the “Q2 FY2026 Financial Results Supplementary Material” disclosed on October 14, 2025.

- The specific corrections are on page 33, under “[New Stores Amusement for the Current Period]”, regarding the unit for the “Interim Sales Trend Table for Capsule Toy Specialty Stores” and the “Interim Sales Trend Table for Prize Specialty Stores”.

- The incorrect unit displayed was “(Incorrect) (Unit: JPY billion / store)”.

- The correct unit has been revised to “(Correct) (Unit: JPY million / store)”.

🤖 AI Perspective

This correction addresses a unit discrepancy in the supplementary financial materials, which may provide a more accurate understanding of the sales scale for capsule toy and prize specialty stores. For investors, this clarification ensures that previously disclosed data can be interpreted with the correct magnitude. It is generally advisable for stakeholders to note such corrections for precise financial analysis.

6104|芝浦機械

3990.0

▼ -0.87%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Shibaura Machine published its earnings presentation for the fiscal year ending March 2026 on June 2, 2026.

- For FY2025, actual net sales were ¥132.8 billion, a shortfall of ¥7.2 billion compared to the forecast of ¥140.0 billion. Operating profit was ¥4.3 billion, ¥0.7 billion below the forecast of ¥5.0 billion.

- Ordinary profit met the forecast at ¥5.0 billion, but net profit attributable to owners of parent was ¥1.0 billion, a shortfall of ¥2.3 billion against the forecast of ¥3.3 billion.

- The miss in net profit was primarily due to special losses, including impairment loss on goodwill of SHIBAURA MACHINE LWB GmbH and special retirement benefits.

- Total orders received were ¥119.1 billion, ¥18.9 billion below the forecast of ¥138.0 billion. However, orders for large machine tools and ultra-precision machine tools increased. Orders for the “BSF” (separator film manufacturing equipment for lithium-ion batteries) for extrusion molding machines included a full line for the first time in approximately two years, though this segment did not meet its initial plan.

8020|兼松

2013.0

▼ -1.40%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kanematsu Co. released the summary of the Q&A from its FY2026/3 full-year earnings briefing on June 2, 2026, which was held on May 18, 2026.

- The net profit for FY2026/3 landed at 32.5 billion yen (estimated underlying profit of approximately 33.0 billion yen), exceeding expectations, with all segments performing well towards the fiscal year-end.

- Of the 60.0 billion yen growth investment planned under the Mid-Term Management Plan (MTP), the actual execution for ICT-related investments is currently 2.0 billion yen against a target of 40.0 billion yen.

- The delay in large-scale ICT-related investments is attributed to factors such as target company valuations not aligning with Kanematsu’s expectations or target companies declining offers.

- Kanematsu plans to continue considering large-scale ICT investments, stating a willingness to exceed the initial 40.0 billion yen framework if suitable, high-quality projects emerge.

- No additional shareholder returns are planned for the current MTP period; however, they may be considered in the next MTP, balancing growth investment execution.

🤖 AI Perspective

The Q&A summary highlights Kanematsu’s stronger-than-expected underlying profit, driven by robust performance across all segments. Investors may note the significant gap between planned and executed ICT-related growth investments, yet management’s flexible approach to exceeding the initial investment framework for opportune deals could signal future growth potential. The decision to prioritize growth investments over additional shareholder returns during the current MTP period suggests a focus on long-term expansion.

2818|ピエトロ

1721.0

▼ -0.06%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Pietro Co., Ltd. announced a partial correction to its “Financial Results for the Fiscal Year Ending March 31, 2026 (Consolidated, Japanese GAAP),” originally published on May 15, 2026.

- The reason for the correction is that certain matters requiring amendment in the descriptions were identified after the submission.

- The correction applies to “4. Non-consolidated Financial Statements and Principal Notes (1) Balance Sheet” on page 20 of the attached document.

- It is explicitly stated that this correction has no impact on the company’s business performance.

- Numerical data (XBRL) was also corrected, and the revised XBRL data will be transmitted.

🤖 AI Perspective

Corrections to financial statements by listed companies are critical for investors to ensure information accuracy. This correction from Pietro is specified as a revision to descriptive content with no impact on business performance, which may suggest that it does not indicate a fundamental change in financial position or operational outlook. The accompanying XBRL data correction means data users should ensure they are referencing the updated version.

4750|ダイサン

569.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Daisan Co., Ltd. announced its consolidated financial results for the fiscal year ended April 2026 (April 21, 2025, to April 20, 2026).

- Consolidated results show net sales of ¥11,139 million (up 2.8% year-on-year), operating profit of ¥268 million (down 27.5% year-on-year), ordinary profit of ¥290 million (down 15.9% year-on-year), and profit attributable to owners of parent of ¥262 million (down 21.8% year-on-year).

- By segment, the construction services business reported sales of ¥7,669 million (up 6.0% year-on-year), and the manufactured goods sales business reported sales of ¥1,009 million (down 14.5% year-on-year).

- The annual dividend for the fiscal year ended April 2026 was ¥22.00 per share (¥11.00 for year-end), a decrease from ¥24.00 in the previous fiscal year.

- For the full fiscal year ending April 2027, the company forecasts consolidated net sales of ¥12,000 million (up 7.7% year-on-year), ordinary profit of ¥220 million (down 24.4% year-on-year), and profit attributable to owners of parent of ¥130 million (down 50.4% year-on-year).

🤖 AI Perspective

Daisan’s FY2026 results show a divergence between revenue growth and declining profits across key metrics. This appears to be influenced by increased personnel costs in the construction services business, anticipating future order expansion, and reduced demand in the manufactured goods sales business due to market cautiousness and a reactionary decline following regulatory changes. The forecast for FY2027 indicates continued sales growth but further anticipated profit declines, which may prompt investors to closely monitor the company’s business structure and cost management strategies.

5076|インフロニアHD

2415.0

▼ -0.25%

📎 Source:インフロニアHD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Infroneer Holdings’ subsidiary, Sumitomo Mitsui Construction Co., Ltd., completed the full acquisition of Mitsui Sumitomo Kensetsu Road Co., Ltd. on June 2, 2026.

- Sumitomo Mitsui Construction had acquired 8,848,998 shares of Mitsui Sumitomo Kensetsu Road (representing 95.38% of voting rights) as of April 28, 2026, through a tender offer initiated on March 10, 2026.

- Following the tender offer, Sumitomo Mitsui Construction decided on May 8, 2026, to request the sale of all shares from minority shareholders of Mitsui Sumitomo Kensetsu Road under Article 179, Paragraph 1 of the Companies Act, acquiring all such shares on the acquisition date.

- Consequently, Mitsui Sumitomo Kensetsu Road has become a wholly-owned subsidiary of Sumitomo Mitsui Construction.

🤖 AI Perspective

This announcement confirms the scheduled completion of a full subsidiary acquisition within the Infroneer Holdings Group, representing a step in internal business restructuring. The full integration of Sumitomo Mitsui Construction and Mitsui Sumitomo Kensetsu Road could facilitate optimized resource allocation and investment across the group, potentially enhancing corporate value. The realization of synergies within the group’s future strategies will be worth monitoring.

6050|Eガーディアン

1622.0

▼ -0.12%

📎 Source:Eガーディアン Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- E-Guardian published a Q&A on June 2, 2026, regarding its Q2 FY2026 financial results and the complete acquisition of Outsourcing Communications Co., Ltd.

- The Q&A addresses expectations for large projects in the second half of the fiscal year, including additional orders from existing clients and new client acquisitions in monitoring and screening operations.

- The improvement in gross profit margin is attributed to the full-scale implementation of AI, establishing an “AI-human collaboration model (AI-BPO)” that structurally elevates profitability.

- The closure of the Tachikawa and Koriyama centers is viewed as a positive outcome of AI strategy-driven efficiency, transitioning to a new structure where personnel and facility growth are not necessarily proportional to revenue growth.

- The full acquisition of Outsourcing Communications is positioned as the first step into new BPO domains, aiming to apply the “AI-BPO” model to the acquired company for a high-profit business model.

- E-Guardian plans to pursue multiple M&A deals during the current and next fiscal year, with investment sizes ranging from several hundred million to several billion yen, depending on the nature of the deals.

🤖 AI Perspective

The released Q&A suggests that E-Guardian’s AI strategy is yielding tangible results, such as improved profit margins and operational efficiency. The establishment of the “AI-BPO” model, potentially leading to a shift away from labor-intensive business, could be a critical factor for understanding future business structure changes. Furthermore, the company’s clear strategy to integrate M&A with its AI initiatives to expand into new BPO areas and enhance profitability is worth monitoring.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

6562|G-ジーニー

969.0

▼ -5.28%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Geniee Co., Ltd. resolved at its Board of Directors meeting on June 2, 2026, to absorb and merge its consolidated subsidiary, CATS Inc.

- The merger will be conducted as an absorption-type merger with G-Geniee as the surviving company, and CATS Inc. will be dissolved.

- The effective date of the merger is scheduled for October 1, 2026, subject to approval at G-Geniee’s shareholder meetings. CATS Inc. will not hold a general meeting of shareholders as it qualifies as a short-form merger.

- No shares or other monetary consideration will be allotted in connection with this merger.

- As this merger involves a 100% owned consolidated subsidiary, there will be no impact on consolidated business performance, according to the announcement.

🤖 AI Perspective

This absorption merger is stated to consolidate management resources, streamline operations, and accelerate decision-making. It suggests an aim to further strengthen existing business synergies, such as product collaboration and customer base utilization, through organizational integration. While the direct impact on consolidated performance is expected to be limited due to CATS being a 100% subsidiary, this move could be seen as part of a broader management strategy to enhance corporate value.

6678|テクノメディカ

2004.0

▲ +1.57%

📎 Source:テクノメディカ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Techno Medica Corporation resolved to abolish its shareholder special benefit program at a Board of Directors meeting held on June 2, 2026.

- Reasons cited for the abolition include rising costs of the benefit item (rice), unstable procurement environment for packaging materials, and increased delivery expenses.

- The company stated its intention to consolidate shareholder returns to stable and equitable dividends, discontinuing the special benefit program.

- The abolition will take effect from the shareholder benefit program based on the record date of September 30, 2026.

- Techno Medica previously resolved, as announced on May 11, 2026, to aim for a payout ratio of 80% or more during the 26th Mid-Term Business Plan period and to increase the dividend per share from the initially planned ¥68 to ¥129.

6810|マクセル

1995.0

▲ +1.27%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Maxell announced a re-correction to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 [Japanese GAAP]” on June 2, 2026, following an initial release on April 27, 2026, and a partial correction on May 22, 2026.

- The reason for the correction is stated as errors found in the number of treasury shares at the end of the period, the average number of shares during the period, and depreciation expenses.

- The “number of treasury shares at the end of the period” for FY2026 March was corrected from “10,094,968 shares” to “10,094,913 shares.”

- The “average number of shares during the period” for FY2026 March was corrected from “40,884,720 shares” to “40,884,754 shares.”

- “Depreciation expenses” for FY2026 March were corrected from “5,293 million yen” to “5,299 million yen.”

- Consequently, the description of “cash flows from operating activities” was corrected from “8,925 million yen income” to “8,372 million yen income.”

- In the consolidated cash flow statement, the “cash flows from operating activities” figure of “8,372 million yen” remained unchanged from the previous correction, but specific components such as “depreciation expenses” and “other” were revised (Depreciation expenses: 5,293 million yen -> 5,299 million yen; Other: △2,075 million yen -> △2,081 million yen).

🤖 AI Perspective

This re-correction indicates multiple adjustments to key numerical data in the financial results. Errors in fundamental accounting items like treasury shares, average shares, and depreciation expenses could be a point of focus for investors evaluating the company’s financial reporting accuracy. The adjustment to operating cash flow may also impact the perception of the company’s cash-generating capabilities.

7031|G-インバウンド

628.0

▼ -1.72%

📎 Source:G-インバウンド Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Inbound has issued a re-correction to a portion of its disclosure regarding “Notice on Making FW Co., Ltd. a Subsidiary Through a Simplified Share Exchange and Change in Subsidiaries,” originally published on May 13, 2026.

- The corrections are located in the “Summary of the Share Exchange” under “Method of the Share Exchange, etc.” within “I. Making FW a Subsidiary through Share Exchange (Simplified Share Exchange),” specifically in the note for “① Shareholder Structure Before the Share Exchange.”

- The revised content adds a statement that “Prior to the effective date of this share exchange, the exercise of stock acquisition rights by Hikari Tsushin for 1,800 common shares of FW is planned, which will result in FW’s total outstanding shares becoming 12,000 shares.”

- Furthermore, a detail was added stating, “Subsequently, Hikari Tsushin’s 1,626 common shares of FW and Mr. Fujishima’s 100 common shares of FW are planned to be converted into 1,626 Class B preferred shares and 100 Class B preferred shares, respectively.”

- Additionally, the note for Class B preferred shares under “② Shareholder Structure After the Share Exchange” was extended to include: “As for the terms of Class B preferred shares, Hikari Tsushin and Mr. Fujishima, after June 9, 2026, and three years and six months have passed, and even if Hikari Tsushin or Mr. Fujishima exercised their right to request acquisition in exchange for cash, the Class B preferred shares to be exchanged for cash…”

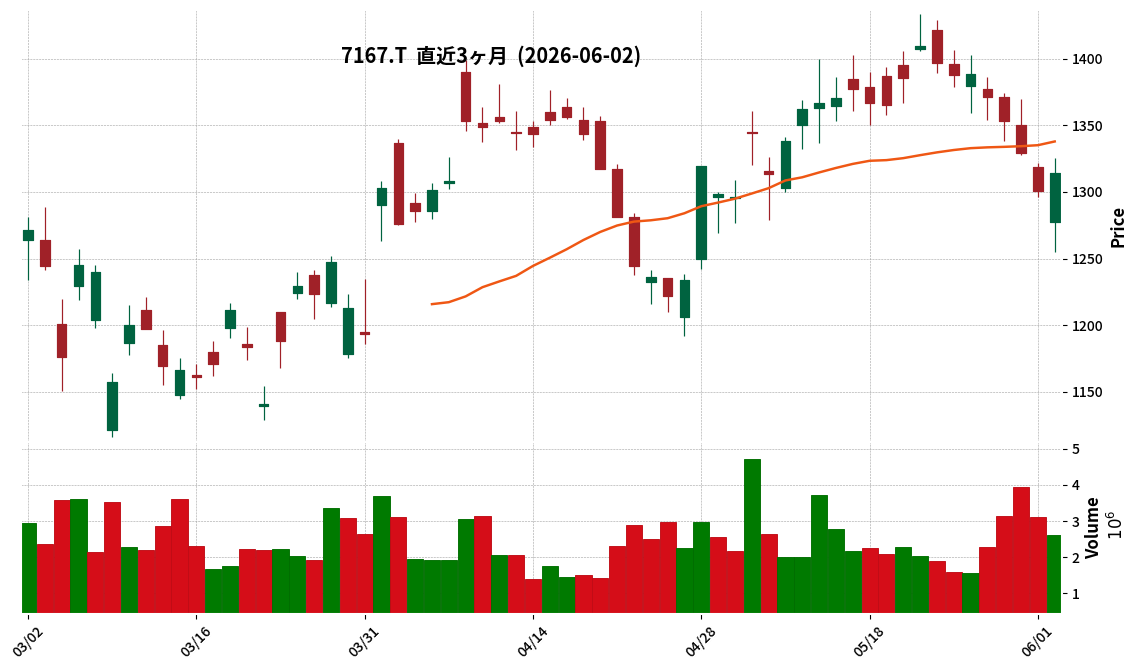

7167|めぶきFG

1314.5

▲ +1.08%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Mebuki Financial Group announced a correction to a part of its “FY2025 Financial Results Overview” on June 2, 2026.

- The correction pertains to the “FY2025 Financial Results Overview” originally announced on May 13, 2026.

- The specific item corrected is the year-on-year change in the “FY2026 Ordinary Profit Forecast” on page 3 of the document.

- The original figure for the year-on-year change was “+22.3 billion yen.”

- The revised figure for the year-on-year change is “+23.3 billion yen.”

- The corrected “FY2025 Financial Results Overview” is available on the company’s website.

🤖 AI Perspective

This correction notice highlights a revision in a specific financial forecast, specifically the year-on-year change in ordinary profit for FY2026. Investors may find it important to note the updated figure, as it slightly modifies previously released information. Such corrections, even for minor numerical adjustments, underscore the company’s commitment to maintaining accuracy and transparency in its financial disclosures.

7318|G-セレンディップ

2470.0

▲ +8.57%

📎 Source:G-セレンディップ Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- G-Serendipity Holdings Co., Ltd. announced corrections to parts of its “FY2026 March Earnings Supplementary Materials” and “FY2026 March Full-Year Earnings Explanatory Materials” previously released on May 14 and May 29, 2026.

- The reason for the correction is to adjust the actual figures for the fiscal year ended March 2026 to ensure comparability with the forecasted segment-specific revenue and profit for FY2027 March, following the transfer of the consulting business on April 1, 2026.

- The corrections are located on page 16 of the “FY2026 March Earnings Supplementary Materials” and page 26 of the “FY2026 March Full-Year Earnings Explanatory Materials,” highlighted in red frames in the attached appendix.

- The correction announcement date is June 2, 2026.

🤖 AI Perspective

This correction primarily concerns the reclassification of past performance data due to a business transfer, aiming to enhance comparability with future segment-specific earnings forecasts. For investors, this adjustment may provide a clearer picture for evaluating the company’s performance against its new business structure.

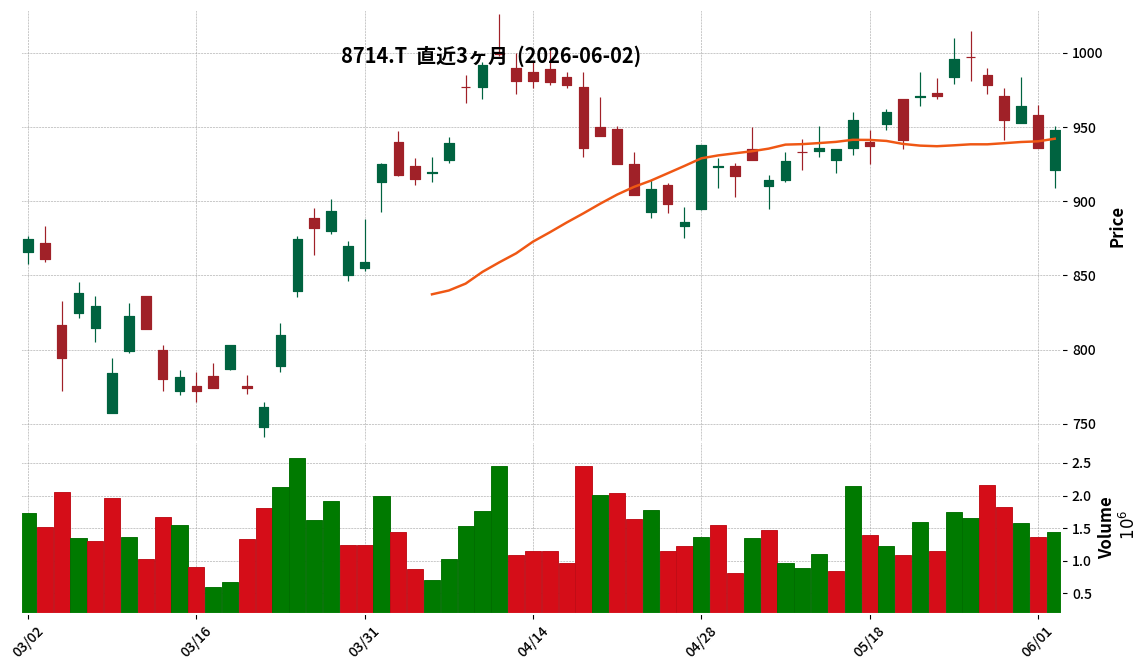

8714|池田泉州

948.0

▲ +1.28%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Ikeda Senshu Holdings reported consolidated net profit of ¥17.3 billion and ROE of 7.1% for FY2025, achieving the targets for the final year of the 5th Medium-Term Management Plan Plus.

- The dividend per share for FY2025 was raised to ¥25.0 (from an initial plan of ¥21.0), and the FY2026 dividend is projected to be ¥27.5, with a target payout ratio of 40%.

- The long-term management strategy, the “6th Medium-Term Management Plan” (FY2026-FY2028), sets targets of ¥30 billion in consolidated net profit and an ROE of 10% or more by FY2028.

- The company announced the formulation of its purpose and long-term management strategy (vision for 10 years ahead) in March 2026.

- Strategic investments totaling approximately ¥12.0 billion over three years are allocated to human capital investment and systems/DX, aiming for a core OHR of 55% or less for Ikeda Senshu Bank (non-consolidated) by FY2028.

🤖 AI Perspective

The FY2025 results indicate that key KPIs and management targets were met or exceeded, signaling a strong close to the previous medium-term plan. The newly announced 6th Medium-Term Management Plan outlines a strategy focused on aggressive growth investments, diversification of revenue streams, and deepening community-based solution sales to achieve an ROE of over 10%, which may be a key point for investors to monitor.

136A|P-三興商事

4330.0

▲ +0.00%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- P-SANKO SHOJI (Code: 136A) decided on June 2, 2026, to apply for delisting of its shares from TOKYO PRO Market.

- Concurrently, the Board of Directors resolved to transfer all shares to a special purpose company established by SADOSHIMA Corporation for capital tie-up, making P-SANKO SHOJI a wholly-owned subsidiary of SADOSHIMA Corporation.

- The application date for delisting and the share transfer agreement date are June 2, 2026, with the scheduled delisting and share transfer date set for June 30, 2026.

- The company obtained written consent from shareholders holding more than two-thirds of the voting rights in advance, thereby omitting the special resolution of the shareholders’ meeting for the delisting application.

- SADOSHIMA Corporation is a specialized trading company for steel and non-ferrous metals with a 150-year history, also engaged in the manufacturing and sales of metal products for construction.

🤖 AI Perspective

This announcement indicates P-SANKO SHOJI’s strategic move to delist from TOKYO PRO Market and become a wholly-owned subsidiary of SADOSHIMA Corporation. This decision appears aimed at strengthening its management foundation and business structure, expanding product offerings, and enlarging its sales regions. For existing shareholders, the transfer of shares will lead to the company’s privatization, which is a key point of interest.

1871|ピーエス

2085.0

▼ -0.33%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- For the fiscal year ended March 2026, consolidated orders received totaled ¥148.711 billion (up 4.6% year-on-year), and consolidated net sales reached ¥149.370 billion (up 10.1% year-on-year).

- Net profit attributable to owners of parent was ¥9.328 billion (up 13.5% year-on-year), with gross profit and all subsequent profit metrics achieving new record highs for two consecutive periods.

- By segment, Civil Engineering reported orders received of ¥85.948 billion (up 22.9% year-on-year) and net sales of ¥75.814 billion (up 10.5% year-on-year), driven by an increase in new bridge constructions and progress in existing projects.

- The Building Construction segment recorded orders received of ¥53.011 billion (down 10.1% year-on-year) and net sales of ¥62.905 billion (up 19.0% year-on-year).

- The annual dividend per share for FY2026 was increased from the initial forecast of ¥80 to ¥120.

🤖 AI Perspective

PS Co., Ltd.’s FY2026 results demonstrate significant growth in both revenue and profit, primarily driven by the Civil Engineering segment. The achievement of record-high profits for two consecutive periods in key metrics suggests an ongoing improvement in the company’s profitability. Furthermore, the substantial increase in the annual dividend per share may be viewed by investors as a positive sign regarding shareholder returns.

3521|テルマー湯HD

149.0

▲ +0.00%

📎 Source:テルマー湯HD Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Thermae-Yu Holdings Co., Ltd. announced a partial correction to its “Consolidated Financial Results for the Fiscal Year Ended March 2026 (Japanese Standards),” originally disclosed on May 13, 2026.

- The reason for the correction is stated as errors in the amounts of “advance payments” and “net sales” for some subsidiaries.

- The revised consolidated operating results for the fiscal year ended March 31, 2026 (April 1, 2025 – March 31, 2026) are as follows: Net sales of 2,694 million yen (up 36.0% year-on-year), Operating profit of 306 million yen (down 10.2%), Ordinary profit of 307 million yen (down 9.6%), and Net profit attributable to owners of parent of 160 million yen (down 16.3%).

- The revised basic earnings per share is 6.06 yen, and diluted earnings per share is 5.94 yen.

- For the consolidated financial position, total assets for March 2026 are 6,000 million yen, net assets are 4,967 million yen, and the equity ratio is 82.5%.

🤖 AI Perspective

This correction, attributed to errors in specific accounts of a subsidiary, ensures the accuracy of the disclosed numerical data. For investors, it is important to analyze the company’s financial situation based on these revised figures, as they are now considered more accurate. The fact that key performance indicators such as net sales and profits have been corrected could potentially influence future company valuations.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

5998|アドバネクス

3100.0

▲ +6.57%

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Advanex Co., Ltd. announced a partial correction to its “Consolidated Financial Results for the Fiscal Year Ended March 2026 (Japanese GAAP) (Consolidated)” which was originally released on May 15, 2026.

- For the fiscal year ended March 2026, consolidated cash flow from operating activities was corrected from ¥2,280 million to ¥2,202 million, cash flow from investing activities from △¥3,221 million to △¥2,866 million, and cash flow from financing activities from ¥1,561 million to ¥1,285 million. The year-end cash and cash equivalents balance of ¥5,158 million remains unchanged.

- In the non-consolidated performance, the non-consolidated net income for the fiscal year ended March 2026 was corrected from ¥196 million to ¥81 million. Consequently, basic earnings per share were revised from ¥47.81 to ¥19.96.

- For the non-consolidated financial position for the fiscal year ended March 2026, total assets were corrected from ¥20,323 million to ¥20,208 million, net assets from ¥1,629 million to ¥1,514 million, equity ratio from 8.0% to 7.5%, and net assets per share from ¥394.81 to ¥366.96.

- The descriptions in “Overview of Business Performance” regarding cash flow and the figures in the “Consolidated Statements of Cash Flows” were also revised due to these corrections.

🤖 AI Perspective

This correction modifies previously announced figures for the fiscal year ended March 2026, impacting various aspects of consolidated cash flow and non-consolidated net income and financial position. The significant downward revision of non-consolidated net income could affect key indicators such as earnings per share and the equity ratio. Investors may find it beneficial to carefully examine how these adjustments impact the company’s financial health and cash flow dynamics when comparing with prior disclosures.

Disclaimer: This article is for informational purposes only and does not constitute investment advice.

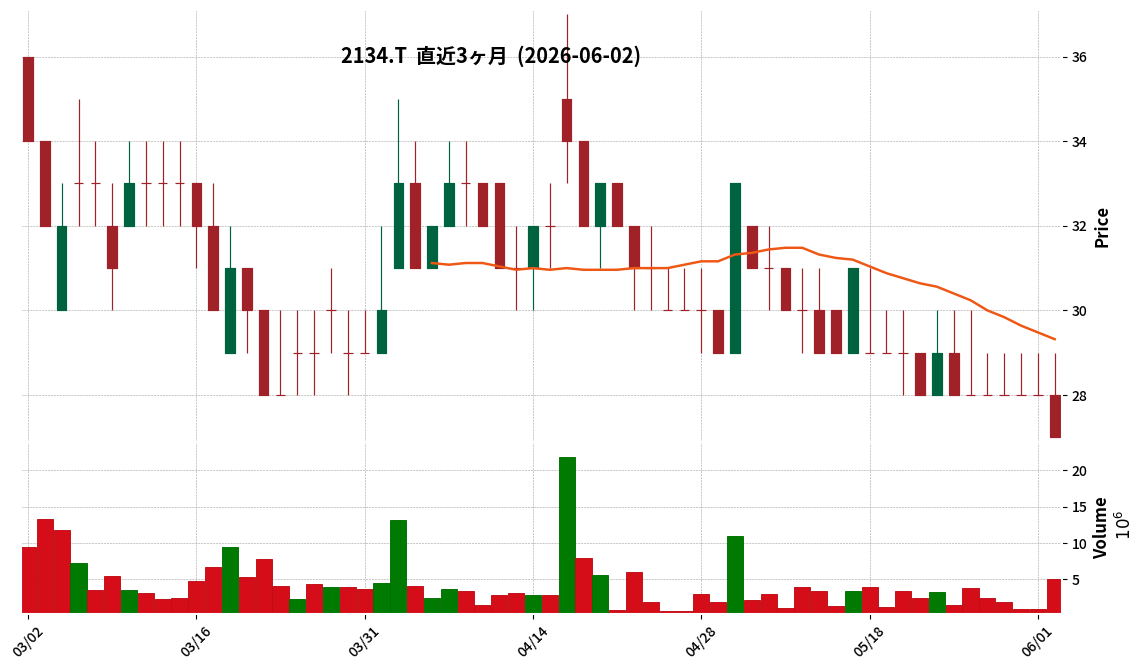

2134|キタハマキャピタル

27.0

▼ -3.57%

📎 Source:キタハマキャピタル Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- Kitahama Capital Partners announced a partial revision to its “Consolidated Financial Results for the Fiscal Year Ended March 31, 2026 (Japanese GAAP),” originally disclosed on May 15, 2026.

- The reason for the revision was an auditor’s指摘 during the year-end audit process, specifically regarding the overstatement of deferred tax assets and the non-recognition of impairment losses on investment securities held by a subsidiary.

- As a result, an adjustment of ¥31,908 thousand for deferred tax assets and an impairment loss of ¥8,804 thousand on investment securities were recognized.

- In addition to these material corrections, other minor numerical changes confirmed during the year-end audit were also incorporated into the revised document.

- Due to the numerous correction points, the full revised text has been provided, with all amended sections underlined.

🤖 AI Perspective

This revision addresses accounting adjustments identified during the audit process, which is a standard procedure to ensure financial reporting accuracy. The adjustments related to deferred tax assets and impairment losses directly impact the company’s net income, making it important for investors to review the revised financial statements for an accurate understanding of the company’s financial position.

2335|キューブシステム

1001.0

▼ -0.99%

📎 Source:キューブシステム Official IR →

This article is an AI-generated summary and analysis of official IR disclosures.

📄 Announcement (AI-Reviewed)

- CUBE SYSTEM Co., Ltd. resolved on June 2, 2026, to form a capital and business alliance with System Create Co., Ltd.

- The alliance involves CUBE SYSTEM acquiring an additional 44 shares of common stock through a third-party allocation of System Create’s treasury shares.

- The payment due date for the shares is June 30, 2026, after which CUBE SYSTEM’s voting rights in System Create will be 21.1%.

- The business alliance includes joint promotion of system development and operation projects in the Tokyo and Kyushu areas, deeper collaboration in human resource securing, sharing of quality and development standards, joint R&D, business development, and human resource development and exchange.

- CUBE SYSTEM states that the impact of this alliance on its consolidated performance is expected to be minor.

🤖 AI Perspective

This alliance can be seen as CUBE SYSTEM strengthening its long-standing collaborative relationship with System Create both operationally and financially. The move suggests an aim to enhance corporate value over the medium to long term through deepened collaboration in system development and SES domains, as well as mutual complementary efforts between their respective operational bases. A 21.1% voting rights stake may indicate a more strategic partnership in the future.

💡 Start investing with IR insights

※ 本ページには広告が含まれます(PR)

Disclaimer: This article is for informational purposes only and does not constitute investment advice. All investment decisions are at your own risk.

コメント